Effect of Stakeholders-Oriented Behavior on the Performance of Sustainable Business

Abstract

:1. Introduction

2. Literature Review

2.1. Stakeholder-Oriented Organizational Behavior

2.1.1. Organizational Culture

2.1.2. Organizational Behavior

2.2. Impacts of Stakeholder-Oriented Behavior on Organizational Performance

2.2.1. Market and Financial Performance

2.2.2. Organizational Reputation

2.2.3. Organizational Commitment

3. Methodology

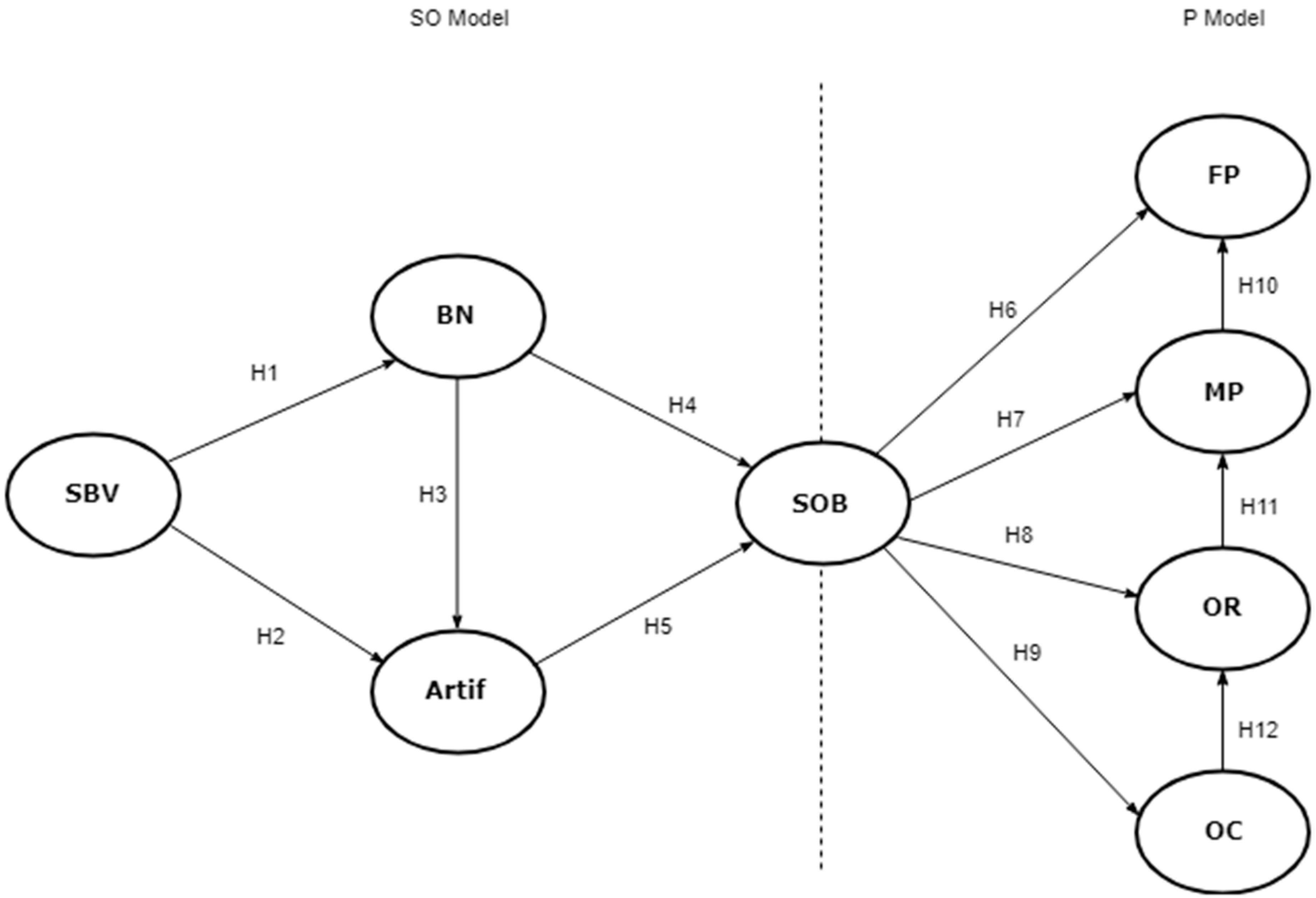

3.1. Proposed Model

3.2. Participants and Procedure

3.3. Instruments

3.4. Common Method Bias

4. Results

4.1. Measurement Model Analysis

4.2. Structural Model Analysis

5. Discussion

5.1. Research Implications

5.2. Managerial Implications

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Skouloudis, A.; Avlonitis, G.J.; Malesios, C.; Evangelinos, K. Priorities and perceptions of corporate social responsibility: Insights from the perspective of Greek business professionals. Manag. Decis. 2015, 53, 375–401. [Google Scholar] [CrossRef]

- Baden, D.; Harwood, I.A. Terminology matters: A critical exploration of corporate social responsibility terms. J. Bus. Ethics 2013, 116, 615–627. [Google Scholar] [CrossRef]

- Skouloudis, A.; Evangelinos, K. Exogenously driven CSR: Insights from the consultants’ perspective. Bus. Ethics Eur. Rev. 2014, 23, 258–270. [Google Scholar] [CrossRef]

- Khalid, R.U.; Seuring, S.; Beske, P.; Land, A.; Yawar, S.A.; Wagner, R. Putting sustainable supply chain management into base of the pyramid research. Supply Chain Manag. 2015, 20, 681–696. [Google Scholar] [CrossRef]

- Bulgacov, S.; Ometto, M.P.; May, M.R. Differences in sustainability practices and stakeholder involvement. Soc. Responsib. J. 2015, 11, 149–160. [Google Scholar] [CrossRef]

- Samant, S.M.; Sangle, S. A selected literature review on the changing role of stakeholders as value creators. J. Sci. Technol. Sustain. Dev. 2016, 13, 100–119. [Google Scholar] [CrossRef]

- Ferrell, O.C.; Gonzalez-Padron, T.L.; Hult, G.T.M.; Maignan, I. From market orientation to stakeholder orientation. J. Public Policy Mark. 2010, 29, 93–96. [Google Scholar] [CrossRef]

- Maignan, I.; Gonzalez-Padron, T.L.; Hult, G.T.M.; Ferrell, O.C. Stakeholder orientation: Development and testing of a framework for socially responsible marketing. J. Strateg. Mark. 2011, 19, 313–338. [Google Scholar] [CrossRef]

- Patel, V.K. Extended Stakeholder Orientation: Influence on Innovation Orientation and Firm Performance. Dissertations, Theses and Capstone Projects. Doctor of Business Administration (DBA); Kennesaw State University: Kennesaw, GA, USA, 2012; Available online: https://digitalcommons.kennesaw.edu/etd/501 (accessed on 17 November 2017).

- Gibson, K. The moral basis of stakeholder theory. J. Bus. Ethics 2000, 26, 245–257. [Google Scholar] [CrossRef]

- Littau, P.; Jujagiri, N.J.; Adlbrecht, G. 25 Years of stakeholders’ theory in project management literature (1984–2009). Proj. Manag. J. 2010, 41, 17–29. [Google Scholar] [CrossRef]

- Garvare, R.; Johansson, P. Management for sustainability—A stakeholder theory. Total Qual. Manag. 2010, 21, 737–744. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Pitman: Boston, MA, USA, 1984; ISBN 10 0273019139. [Google Scholar]

- Freeman, R.E.; Harrison, J.; Wicks, A.; Parmar, B.; de Colle, S. Stakeholder Theory: The State of the Art; Cambridge University Press: Cambridge, UK, 2010; ISBN -13 978-0-521-19081-7. [Google Scholar]

- Donaldson, T.; Preston, L.E. The stakeholder theory of the corporation: Concepts, evidence and implications. Acad. Manag. Rev. 1995, 20, 65–91. [Google Scholar] [CrossRef]

- Kochan, T.A.; Rubinstein, S.A. Toward a stakeholder theory of the firm: The Saturn partnership. Organ. Sci. 2000, 11, 367–386. [Google Scholar] [CrossRef]

- Sachs, S.; Ruhli, E. Changing managers’ values towards a broader stakeholder orientation. Corp. Gov. Int. J. Bus. Soc. 2005, 5, 89–98. [Google Scholar] [CrossRef]

- Clarkson, M.E. A stakeholder framework for analyzing and evaluating corporate social performance. Acad. Manag. Rev. 1995, 20, 92–117. [Google Scholar] [CrossRef]

- Freeman, R.; Wicks, A.C.; Parmar, B. Stakeholder theory and the corporate objective revisited. Organ. Sci. 2004, 15, 364–369. [Google Scholar] [CrossRef]

- Harrison, J.; Bosse, D.; Phillips, R. Managing for stakeholders, stakeholder utility functions, and competitive advantage. Strateg. Manag. J. 2010, 31, 58–74. [Google Scholar] [CrossRef]

- Post, J.; Preston, L.; Sachs, S. Managing the extended enterprise: The new stakeholder view. Calif. Manag. Rev. 2002, 45, 6–28. [Google Scholar] [CrossRef]

- Aguilera, R.V.; Rupp, D.E.; Williams, C.A.; Ganapathi, J. Putting the S back in corporate social responsibility: A multilevel theory of social change in organizations. Acad. Manag. Rev. 2007, 32, 836–863. [Google Scholar] [CrossRef] [Green Version]

- Barrena-Martinez, J.; López-Fernández, M.; Romero-Fernandez, P.M. Drivers and Barriers in Socially Responsible Human Resource Management. Sustainability 2018, 10, 1532. [Google Scholar] [CrossRef]

- Barrena-Martínez, J.; López-Fernández, M.; Romero-Fernández, P.M. Corporate social responsibility: Evolution through institutional and stakeholder perspectives. Eur. J. Manag. Bus. Econ. 2016, 25, 8–14. [Google Scholar] [CrossRef]

- Maignan, I.; Ferrell, O.C. Corporate social responsibility and marketing: An integrative framework. J. Acad. Mark. Sci. 2004, 32, 3–19. [Google Scholar] [CrossRef]

- Narver, J.C.; Slater, S.F. The effect of a market orientation on business profitability. J. Mark. 1990, 54, 20–35. [Google Scholar] [CrossRef]

- Calantone, R.J.; Cavusgil, S.T.; Zhao, Y. Learning orientation, firm innovation capability, and firm performance. Ind. Mark. Manag. 2002, 31, 515–524. [Google Scholar] [CrossRef]

- Sinkula, J.M.; Baker, W.E.; Noordewier, T. A framework for market-based organizational learning: Linking values, knowledge, and behaviour. J. Acad. Mark. Sci. 1997, 25, 305–318. [Google Scholar] [CrossRef]

- Slater, S.F.; Narver, J.C. Market orientation and the learning organization. J. Mark. 1995, 59, 63–74. [Google Scholar] [CrossRef]

- Barney, J. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Gill, S.J. Developing a Learning Culture in Nonprofit Organizations; Sage: Thousand Oaks, CA, USA, 2009; ISBN 1412967678. [Google Scholar]

- Han, X.; Hansen, E.; Panwar, R.; Hamner, R.; Orozco, N. Connecting market orientation, learning orientation and corporate social responsibility implementation: Is innovativeness a mediator? Scand. J. For. Res. 2013, 28, 784–796. [Google Scholar] [CrossRef]

- Wagner, B.; Svensson, G. A framework to navigate sustainability in business networks: The transformative business sustainability (TBS) model. Eur. Bus. Rev. 2014, 26, 340–367. [Google Scholar] [CrossRef]

- Basu, K.; Palazzo, G. Corporate social responsibility: A process model of sensemaking. Acad. Manag. Rev. 2008, 33, 122–136. [Google Scholar] [CrossRef]

- Bower, J.L.; Paine, L.S. The error at the heart of corporate leadership. Harv. Bus. Rev. 2017, 95, 50–60. Available online: https://hbr.org/2017/05/managing-for-the-long-term (accessed on 20 February 2018).

- Campbell, J.L. Why would corporations behave in socially responsible ways? An institutional theory of corporate social responsibility. Acad. Manag. Rev. 2007, 32, 946–967. [Google Scholar] [CrossRef]

- Jaworski, B.J.; Kohli, A.K. Market orientation: Review, refinement, and roadmap. J. Mark. Focus. Manag. 1996, 1, 119–135. [Google Scholar] [CrossRef]

- Kohli, A.K.; Jaworski, B.J. Market orientation: The construct, research propositions, and managerial implications. J. Mark. 1990, 54, 1–18. [Google Scholar] [CrossRef]

- Ruekert, R.W. Developing a market orientation: An organizational strategy perspective. Int. J. Res. Mark. 1992, 9, 225–245. [Google Scholar] [CrossRef]

- Slater, S.F.; Narver, J.C. Does competitive environment moderate the market orientation-performance relationship? J. Mark. 1994, 58, 46–55. [Google Scholar] [CrossRef]

- Svensson, G.; Høgevold, N.; Padin, C.; Ferro, C.; Sosa Varela, J.C.; Wagner, B. Framing stakeholder considerations and business sustainability efforts: A construct, its dimensions and items. J. Bus. Ind. Mark. 2016, 31, 287–300. [Google Scholar] [CrossRef]

- Van Marrewijk, M. Concepts and definitions of CSR and corporate sustainability: Between agency and communion. J. Bus. Ethics 2003, 44, 95–105. [Google Scholar] [CrossRef]

- Freeman, R.E. The politics of stakeholder theory: Some future directions. Bus. Ethics Q. 1994, 4, 409–421. [Google Scholar] [CrossRef]

- Harrison, J.S.; Wicks, A.C. Stakeholder theory, value, and firm performance. Bus. Ethics Q. 2013, 23, 97–124. [Google Scholar] [CrossRef]

- Jones, T.M. Instrumental stakeholder theory: A synthesis of ethics and economics. Acad. Manag. Rev. 1995, 20, 404–437. [Google Scholar] [CrossRef]

- Jones, T.M.; Wicks, A.C. Convergent stakeholder theory. Acad. Manag. Rev. 1999, 24, 206–221. [Google Scholar] [CrossRef]

- Burke, L.; Logsdon, J.M. How corporate social responsibility pays off. Long Range Plan. 1996, 29, 495–502. [Google Scholar] [CrossRef]

- Homburg, C.; Pflesser, C. A multiple-layer model of market-oriented organizational culture: Measurement issues and performance outcomes. J. Mark. Res. 2000, 37, 449–462. [Google Scholar] [CrossRef]

- Grinstein, A. The effect of market orientation and its components on innovation consequences: A meta-analysis. J. Acad. Mark. Sci. 2008, 36, 166–173. [Google Scholar] [CrossRef]

- Laplume, A.; Sonpar, K.; Litz, R. Stakeholder theory: Reviewing a theory that moves us. J. Manag. 2008, 34, 1152–1189. [Google Scholar] [CrossRef]

- Ostergaard, C.; Schindele, I.; Vale, B. Social Capital and the Viability of Stakeholder-Oriented Firms: Evidence from Savings Banks. Rev. Financ. 2016, 20, 1673–1718. [Google Scholar] [CrossRef]

- Jensen, M.C. Value maximization, stakeholder theory, and the corporate objective function. J. Appl. Corp. Financ. 2001, 14, 8–21. [Google Scholar] [CrossRef]

- Greenley, G.; Graham, J.; John, M. Market orientation in a multiple stakeholder orientation context: Implications for marketing capabilities and assets. J. Bus. Res. 2005, 58, 1483–1494. [Google Scholar] [CrossRef]

- Ruf, B.M.; Muralidhar, K.; Brown, R.M.; Janney, J.J.; Paul, K. An empirical investigation of the relationship between change in corporate social performance and financial performance: A stakeholder theory perspective. J. Bus. Ethics 2001, 32, 143–156. [Google Scholar] [CrossRef]

- Matsuno, K.; Mentzer, J.T.; Rentz, J.O. A conceptual and empirical comparison of three market orientation scales. J. Bus. Res. 2005, 58, 1–8. [Google Scholar] [CrossRef]

- Fombrun, C.; Van Riel, C. The reputational landscape. Corp. Reput. Rev. 1997, 1, 1–13. [Google Scholar] [CrossRef]

- Gray, B.J.; Hooley, G.J. Guest editorial: Market orientation and service firm performance-a research agenda. Eur. J. Mark. 2002, 36, 980–989. [Google Scholar] [CrossRef]

- Kohli, A.K.; Jaworski, B.J.; Kumar, A. MARKOR: A measure of market orientation. J. Mark. Res. 1993, 30, 467–477. [Google Scholar] [CrossRef]

- Yau, O.H.; Chow, R.P.; Sin, L.Y.; Tse, A.C.; Luk, C.L.; Lee, J.S. Developing a scale for stakeholder orientation. Eur. J. Mark. 2007, 41, 1306–1327. [Google Scholar] [CrossRef]

- Fombrun, C.J.; Gardberg, N.A.; Sever, J.M. The Reputation QuotientSM: A multi-stakeholder measure of corporate reputation. J. Brand Manag. 2000, 7, 241–255. [Google Scholar] [CrossRef]

- Jaworski, B.J.; Kohli, A.K. Market orientation: Antecedents and consequences. J. Mark. 1993, 57, 53–70. [Google Scholar] [CrossRef]

- Arditi, D.; Nayak, S.; Damci, A. Effect of organizational culture on delay in construction. Int. J. Proj. Manag. 2017, 35, 136–147. [Google Scholar] [CrossRef]

- Cameron, K.S.; Quinn, R.E. Diagnosing and Changing Organizational Culture: Based on the Competing Values Framework; John Wiley and Sons: San Francisco, CA, USA, 2011; ISBN -10 0-7879-8283-0. [Google Scholar]

- Schein, E.H. Organizational Culture and Leadership, 3rd ed.; Jossey-Bass: San Francisco, CA, USA, 2006; ISBN 978-0-787-98505-9. [Google Scholar]

- Deshpandé, R.; Webster, F.E., Jr. Organizational culture and marketing: Defining the research agenda. J. Mark. 1989, 53, 3–15. [Google Scholar] [CrossRef]

- George, J.M.; Jones, G. Understanding and Managing Organizational Behavior, 6th ed.; Prentice Hall: Upper Saddle River, NJ, USA, 2010; ISBN 978-0-13-612443-6. [Google Scholar]

- Schein, E.H. Coming to a new awareness of organizational culture. Sloan Manag. Rev. 1984, 25, 3–16. Available online: http://www.sietmanagement.fr/wp-content/uploads/2016/04/culture_schein.pdf (accessed on 14 March 2017).

- Napitupulu, I.H. Organizational Culture in Management Accounting Information System: Survey on State-owned Enterprises (SOEs) Indonesia. Glob. Bus. Rev. 2018, 19, 556–571. [Google Scholar] [CrossRef]

- Carroll, A.B. Corporate social responsibility. The centerpiece of competing and complementary frameworks. Organ. Dyn. 2015, 44, 87–96. [Google Scholar] [CrossRef]

- Ford, R.C.; Richardson, W.D. Ethical decision making: A review of the empirical literature. J. Bus. Ethics 1994, 13, 205–221. [Google Scholar] [CrossRef]

- Bovée, C.; Thill, J. Business Communication Today, 13th ed.; Pearson: Harlow, UK, 2016; ISBN 9780133851915. [Google Scholar]

- Tourish, D.; Hargie, O. Key Issues in Organizational Communication; Routledge: London, UK, 2004; ISBN 0415260949. [Google Scholar]

- Kalla, H.K. Integrated internal communications: A multidisciplinary perspective. Corp. Commun. Int. J. 2005, 10, 302–314. [Google Scholar] [CrossRef]

- Argenti, P.A.; Forman, J. The Power of Corporate Communication: Crafting the Voice and Image of your Business; McGraw Hill: New York, NY, USA, 2002; ISBN 0071379495. [Google Scholar]

- O’Reilly, C. Corporations, culture, and commitment: Motivation and social control in organizations. Calif. Manag. Rev. 1989, 31, 9–25. [Google Scholar] [CrossRef]

- Luthans, F. Organizational Behavior: An Evidence-Based Approach, 12th ed.; McGraw-Hill Irwin: New York, NY, USA, 2011; ISBN 0071289399. [Google Scholar]

- Trice, H.M.; Beyer, J.M. The Cultures of Work Organizations; Prentice-Hall, Inc.: Englewood Cliffs, NJ, USA, 1993; ISBN 0131914383. [Google Scholar]

- Smircich, L. Concepts of culture and organizational analysis. Adm. Sci. Q. 1983, 28, 339–358. [Google Scholar] [CrossRef]

- Dandridge, T.C.; Mitroff, I.; Joyce, W.F. Organizational symbolism: A topic to expand organizational analysis. Acad. Manag. Rev. 1980, 5, 77–82. [Google Scholar] [CrossRef]

- Hatch, M.J. The dynamics of organizational culture. Acad. Manag. Rev. 1993, 18, 657–693. [Google Scholar] [CrossRef]

- Alles, M. Comportamiento Organizacional: Cómo Lograr un Cambio Cultural a Través de Gestión por Competencias; Ediciones Granica: Buenos Aires, Argentina, 2013; ISBN 9506417121. [Google Scholar]

- Cole, G. Organisational Behaviour: Theory and Practice; Thomson Learning: London, UK, 1995; ISBN 0826453872. [Google Scholar]

- Heide, J.B.; John, G. Do norms matter in marketing relationships? J. Mark. 1992, 56, 32–44. [Google Scholar] [CrossRef]

- Treviño, L.K.; Butterfield, K.D.; McCabe, D.L. The ethical context in organizations: Influences on employee attitudes and behaviors. Bus. Ethics Q. 1998, 8, 447–476. [Google Scholar] [CrossRef]

- Rego, A.; Leal, S.; Cunha, M.P.; Faria, J.; Pinho, C. How the perceptions of five dimensions of corporate citizenship and their inter-inconsistencies predict affective commitment? J. Bus. Ethics 2010, 94, 107–127. [Google Scholar] [CrossRef]

- Siguaw, J.A.; Brown, G.; Widing, R.E. The influence of the market orientation of the firm on sales force behavior and attitudes. J. Mark. Res. 1994, 31, 106–116. [Google Scholar] [CrossRef]

- Ogbonna, E.; Lloyd, C.H. Managing organizational culture: Insights from the hospitality industry. Hum. Resour. Manag. J. 2002, 12, 33–53. [Google Scholar] [CrossRef]

- Ogbonna, E.; Wilkinson, B. Corporate strategy and corporate culture: The view from the checkout. Person Rev. 1990, 19, 9–15. [Google Scholar] [CrossRef]

- Raju, P.S.; Lonial, S.C.; Gupta, Y.P.; Ziegler, C. The relationship between market orientation and performance in the hospital industry: A structural equations modeling approach. Health Care Manag. Sci. 2000, 3, 237–247. [Google Scholar] [CrossRef] [PubMed]

- Narver, J.C.; Slater, S.F. Product-market strategy and performance: An analysis of the Miles and Snow strategy types. Eur. J. Mark. 1993, 27, 33–51. [Google Scholar] [CrossRef]

- Ngai, J.; Ellis, P. Market orientation and business performance: Some evidence from Hong Kong. Int. Mark. Rev. 1998, 15, 119–139. [Google Scholar] [CrossRef]

- Duesing, R.J. Stakeholder Orientation and its Impact on Performance in Small Businesses. Ph.D. Thesis, Degree of Doctor of Philosophy, Oklahoma State University, Stillwater, OK, USA, 2009. [Google Scholar]

- Berman, S.L.; Wicks, A.C.; Kotha, S.; Jones, T.M. Does stakeholder orientation matter? The relationship between stakeholder management models and firm financial performance. Acad. Manag. J. 1999, 42, 488–506. [Google Scholar] [CrossRef]

- Choi, J.; Wang, H. Stakeholder relations and the persistence of corporate financial performance. Strateg. Manag. J. 2009, 30, 895–907. [Google Scholar] [CrossRef]

- Hillman, A.J.; Keim, G.D. Shareholder value, stakeholder management, and social issues: What’s the bottom line? Strateg. Manag. J. 2001, 22, 125–139. [Google Scholar] [CrossRef]

- Panwar, R.; Nybakk, E.; Hansen, E.; Pinkse, J. Does the business case matter? The effect of a perceived business case on small firms’ social engagement. J. Bus. Ethics 2017, 144, 597–608. [Google Scholar] [CrossRef]

- Grewal, R.; Tansuhaj, P. Building organizational capabilities for managing economic crisis: The role of market orientation and strategic flexibility. J. Mark. 2001, 65, 67–80. [Google Scholar] [CrossRef]

- Fombrun, C. Reputation: Realizing Value from the Corporate Image; Harvard Business School Press: Boston, MA, USA, 1996; ISBN 0875846335. [Google Scholar]

- Gotsi, M.; Wilson, A.M. Corporate reputation: Seeking a definition. Corp. Commun. Int. J. 2001, 6, 24–30. [Google Scholar] [CrossRef]

- Hall, R. A framework linking intangible resources and capabilities to sustainable competitive advantage. Strateg. Manag. J. 1993, 14, 607–618. [Google Scholar] [CrossRef]

- Fombrun, C.J.; Ponzi, L.J.; Newburry, W. Stakeholder tracking and analysis: The RepTrak® system for measuring corporate reputation. Corp. Reput. Rev. 2015, 18, 3–24. [Google Scholar] [CrossRef]

- Helm, S. Employees’ awareness of their impact on corporate reputation. J. Bus. Res. 2011, 64, 657–663. [Google Scholar] [CrossRef]

- Fombrun, C.; Shanley, M. What’s in a name? Reputation building and corporate strategy. Acad. Manag. J. 1990, 33, 233–258. [Google Scholar] [CrossRef]

- Flanagan, D.J.; O’shaughnessy, K.C.; Palmer, T.B. Re-assessing the relationship between the fortune reputation data and financial performance: Overwhelming influence or just a part of the puzzle? Corp. Reput. Rev. 2011, 14, 3–14. [Google Scholar] [CrossRef]

- Schwaiger, M. Components and parameters of corporate reputation—An empirical study. Schmalenbach Bus. Rev. 2004, 56, 46–71. [Google Scholar] [CrossRef]

- Schwaiger, M.; Raithel, S.; Schloderer, M. Recognition or rejection—How a company’s reputation influences stakeholder behaviour. In Reputation Capital; Klewes, J., Wreschniok, R., Eds.; Springer: Berlin/Heidelberg, Germany, 2009; pp. 39–55. ISBN 978-3-642-01629-5. [Google Scholar]

- Helm, S. One reputation or many? Comparing stakeholders’ perceptions of corporate reputation. Corp. Commun. Int. J. 2007, 12, 238–254. [Google Scholar] [CrossRef]

- Mowday, R.; Porter, L.; Steers, R. Employee-Organization Linkages: The Psychology of Commitment, Absenteeism, and Turnover, 1st ed.; Academic Press: New York, NY, USA, 1982; ISBN 9781483267395. [Google Scholar]

- Meyer, J.P.; Allen, N.J. A three-component conceptualization of organizational commitment. Hum. Resour. Manag. Rev. 1991, 1, 61–89. [Google Scholar] [CrossRef]

- Meyer, J.P.; Herscovitch, L. Commitment in the workplace: Toward a general model. Hum. Resour. Manag. Rev. 2001, 11, 299–326. [Google Scholar] [CrossRef]

- Van Dyne, L.; LePine, J.A. Helping and voice extra-role behaviors: Evidence of construct and predictive validity. Acad. Manag. J. 1998, 41, 108–119. [Google Scholar] [CrossRef]

- Sandra, L.R.; O’Leary-Kelly, A.M. Monkey see, monkey do: The influence of work groups on the antisocial behavior of employees. Acad. Manag. J. 1998, 41, 658–672. [Google Scholar] [CrossRef]

- Lapointe, E. Examination of the relationships between servant leadership, organizational commitment, and voice and antisocial behaviors. J. Bus. Ethics 2018, 148, 99–115. [Google Scholar] [CrossRef]

- Stanley, L.; Vandenberghe, C.; Vandenberg, R.; Bentein, K. Commitment profiles and employee turnover. J. Vocat. Behav. 2013, 82, 176–187. [Google Scholar] [CrossRef]

- Bentein, K.; Vandenberg, R.; Vandenberghe, C.; Stinglhamber, F. The role of change in the relationship between commitment and turnover: A latent growth modeling approach. J. Appl. Psychol. 2005, 90, 468–482. [Google Scholar] [CrossRef] [PubMed]

- Morrison, E.W. Employee voice behavior: Integration and directions for future research. Acad. Manag. Ann. 2011, 5, 373–412. [Google Scholar] [CrossRef]

- Lok, P.; Crawford, J. The effect of organisational culture and leadership style on job satisfaction and organisational commitment: A cross-national comparison. J. Manag. Dev. 2004, 23, 321–338. [Google Scholar] [CrossRef]

- Themba, G.; Marandu, E.E. The effects of market orientation on employees: A study of retail organizations in Botswana. Int. Bus. Res. 2013, 6, 130–136. [Google Scholar] [CrossRef]

- Powpaka, S. How market orientation affects female service employees in Thailand. J. Bus. Res. 2006, 59, 54–61. [Google Scholar] [CrossRef]

- Lau, K.C.; Lim, L. Transformational branding for B2B business: Protective packaging company. Asia Pac. J. Mark. Logist. 2018, 30, 517–530. [Google Scholar] [CrossRef]

- Walsh, G.; Mitchell, V.W.; Jackson, P.R.; Beatty, S.E. Examining the antecedents and consequences of corporate reputation: A customer perspective. Br. J. Manag. 2009, 20, 187–203. [Google Scholar] [CrossRef]

- Satorra, A.; Bentler, P.M. Scaling Corrections for Chi Square Statistics in Covariance Structure Analysis. In American Statistical Associations Proceedings of the Business and Economic Sections; American Statistical Association: Alexandria, VA, USA, 1988; pp. 308–313. ISBN -10 9998335418. [Google Scholar]

- Johnson, R.E.; Rosen, C.C.; Chang, C.H. To aggregate or not to aggregate: Steps for developing and validating higher-order multidimensional constructs. J. Bus. Psychol. 2011, 26, 241–248. [Google Scholar] [CrossRef]

- Fuller, C.M.; Simmering, M.J.; Atinc, G.; Atinc, Y.; Babin, B.J. Common methods variance detection in business research. J. Bus. Res. 2016, 69, 3192–3198. [Google Scholar] [CrossRef]

- Harman, H.H. Modern Factor Analysis, 2nd ed.; University of Chicago Press: Chicago, IL, USA, 1976; ISBN -10 0226316521. [Google Scholar]

- Hair, J.F.; Anderson, R.E.; Babin, B.J.; Black, W.C. Multivariate Data Analysis, 7th ed.; Pearson: Upper Saddle River, NJ, USA, 2009; ISBN -10 0138132631. [Google Scholar]

- Steenkamp, J.-B.; van Trijp, H.C.M. The use of lisrel in validating marketing construct. Int. J. Res. Mark. 1991, 8, 283–299. [Google Scholar] [CrossRef]

- Fornell, C.; Larcker, D.F. Structural equation models with unobservable variables and measurement error: Algebra and statistics. J. Mark. Res. 1981, 18, 382–388. [Google Scholar] [CrossRef]

- Bentler, P.M. Fit indexes, Lagrange multipliers, constraint changes and incomplete data in structural models. Multivar. Behav. Res. 1990, 25, 163–172. [Google Scholar] [CrossRef]

- Bentler, P.M.; Bonett, D.G. Significance tests and goodness of fit in the analysis of covariance structures. Psychol. Bull. 1980, 88, 588–606. [Google Scholar] [CrossRef]

- Byrne, B.M. Structural Equation Modeling with Amos: Basic Concepts, Applications, and Programming, 3rd ed.; Routledge/Taylor y Francis Group: New York, NY, USA, 2016; ISBN -10 1138797022. [Google Scholar]

- Carmines, E.G.; McIver, J.P. Analyzing models with unobserved variables. In Social Measurement: Current Issues, 1st ed.; Bohrnstedt, G.W., Borgatta, E.F., Eds.; Sage Publications: Beverly Hills, CA, USA, 1981; pp. 65–115. ISBN -10 0803915969. [Google Scholar]

- Hoyle, R.H.; Panter, A.T. Writing about structural equation models. In Structural Equation Modeling: Concepts, Issues, and Applications; Hoyle, R.H., Ed.; Sage: Thousand Oaks, CA, USA, 1995; pp. 158–176. ISBN 0803953186. [Google Scholar]

- Schumacker, R.E.; Lomax, R.G. A Beginner’s Guide to Structural Equation Modeling; Lawrence Erlbaum Associates: Mahwah, NJ, USA, 2004; ISBN 10 0805840184. [Google Scholar]

- James, L.R.; Mulaik, S.A.; Brett, J.M. Causal Analysis: Assumptions, Models, and Data; Sage: Beverly Hills, CA, USA, 1982; ISBN 10 0803918682. [Google Scholar]

- Aier, S. The role of organizational culture for grounding, management, guidance and effectiveness of enterprise architecture principles. Inf. Syst. e-Bus. Manag. 2014, 12, 43–70. [Google Scholar] [CrossRef]

- Langerak, F.; den Hartigh, E. Managing increasing returns. Eur. Manag. J. 2001, 19, 370–378. [Google Scholar] [CrossRef]

- Raithel, S.; Schwaiger, M. The effects of corporate reputation perceptions of the general public on shareholder value. Strateg. Manag. J. 2015, 36, 945–956. [Google Scholar] [CrossRef]

- Walsh, G.; Beatty, S.E.; Holloway, B.B. Measuring client-based corporate reputation in B2B professional services: Scale development and validation. J. Serv. Mark. 2015, 29, 173–187. [Google Scholar] [CrossRef]

- Anderson, E.W.; Sullivan, M.W. The antecedents and consequences of customer satisfaction for firms. Mark. Sci. 1993, 12, 125–143. [Google Scholar] [CrossRef]

- Mena, J.A.; Chabowski, B.R. The role of organizational learning in stakeholder marketing. J. Acad. Mark. Sci. 2015, 43, 429–452. [Google Scholar] [CrossRef]

- Voegtlin, C.; Greenwood, M. Corporate social responsibility and human resource management: A systematic review and conceptual analysis. Hum. Resour. Manag. Rev. 2016, 26, 181–197. [Google Scholar] [CrossRef]

- Shahzad, F.; Xiu, G.Y.; Shahbaz, M. Organizational culture and innovation performance in Pakistan’s software industry. Technol. Soc. 2017, 51, 66–73. [Google Scholar] [CrossRef]

- Heikkurinen, P.; Bonnedahl, K.J. Corporate responsibility for sustainable development: A review and conceptual comparison of market- and stakeholder-oriented strategies. J. Clean. Prod. 2013, 43, 191–198. [Google Scholar] [CrossRef]

{kind=link}

| Size | % | Sector | % |

|---|---|---|---|

| Large | 104 (37.28%) | Manufacturing | 86 (30.82%) |

| Medium | 100 (35.84%) | Services | 79 (28.32%) |

| Small | 75 (26.88%) | Commerce | 76 (27.24%) |

| Farming | 19 (6.8%) | ||

| Construction | 18 (6.45%) | ||

| Miner | 1 (0.36%) | ||

| Total | 279 | Total | 279 |

| Construct | Description | Items | Scale |

|---|---|---|---|

| Stakeholder-oriented behaviors (SOB) | Three kind of stakeholder-oriented behaviors: intelligence generation (IG), intelligence dissemination (ID), and responsiveness (RE) | 12 IG—4 items ID—4 items RE—4 items | Maignan et al. [5] based on Maignan and Ferrel [51], according to Kohli and Jaworski [27] and Jaworski and Kohli [50] |

| Shared basic values (SBV) | Second-order multidimensional construct consisted of ethical values (EV), team orientation (TO), and openness of internal communications (OIC). | 11 EV—4 items TO—4 items OIC—3 items | Maignan et al. [5] |

| Behavioral norms (BN) | Related to stakeholder policies (SP) and procedures (PR) | 12 SP—6 items PR—6 items | Maignan et al. [5] |

| Artifacts (Artif) | Related to stakeholder strengthening (SS) and communication with stakeholders (SC) | 12 SS—6 items SC—6 items | Maignan et al. [5] |

| Financial performance (FP) | Financial performance evolution during last three years, in comparison with competitors | 3 | Maignan et al. [5] adapted from Homburg and Pflesser [38] |

| Market performance (MP) | Market share evolution during last three years, in comparison with competitors | 6 | Homburg and Pflesser [38] |

| Organizational reputation (OR) | Confidence in or reliability of products or services | 4 | Maignan et al. [5] scale, adapted from Homburg and Pflesser [38] |

| Organizational commitment (OC) | Sense of employee pride of belonging to a company, or making personal sacrifices in order to achieve organizational goals | 7 | Jaworski and Kohli [50] |

| Variables | Indicator | Standardized Loads | t-Value | R2 | Cronbach’s Alpha | CRI | AVE |

|---|---|---|---|---|---|---|---|

| Shared basic values (SBV) (second order) | EV | 0.833 ** | 9.348 | 0.693 | --- | 0.919 | 0.791 |

| TO | 0.938 ** | 9.938 | 0.879 | ||||

| OIC | 0.894 ** | 11.447 | 0.799 | ||||

| Ethical values (EV) | EV1 | 0.737 1 | --- | 0.543 | 0.885 | 0.890 | 0.700 |

| EV2 | 0.901 ** | 16.121 | 0.812 | ||||

| EV3 | 0.811 ** | 13.390 | 0.658 | ||||

| EV4 | 0.816 ** | 15.778 | 0.667 | ||||

| Team orientation (TO) | TO1 | 0.826 1 | --- | 0.683 | 0.879 | 0.879 | 0.710 |

| TO2 | 0.853 ** | 22.625 | 0.728 | ||||

| TO4 | 0.845 ** | 15.027 | 0.715 | ||||

| Openness of internal communications (OIC) | OIC1 | 0.853 1 | --- | 0.728 | 0.888 | 0.917 | 0.790 |

| OIC2 | 0.908 ** | 19.815 | 0.824 | ||||

| OIC3 | 0.804 ** | 13.819 | 0.646 | ||||

| Behavioral norms (BN) | BN_SP_CL | 0.828 ** | 16.378 | 0.685 | 0.932 | 0.928 | 0.590 |

| BN_PR_CL | 0.807 ** | 11.920 | 0.651 | ||||

| BN_SP_SU | 0.868 ** | 14.146 | 0.754 | ||||

| BN_SP_HR | 0.828 ** | 11.596 | 0.686 | ||||

| BN_PR_HR | 0.814 ** | 11.532 | 0.662 | ||||

| BN_SP_PA | 0.717 ** | 8.232 | 0.514 | ||||

| BN_PR_PA | 0.662 ** | 10.231 | 0.438 | ||||

| BN_PR_CO | 0.706 ** | 11.319 | 0.498 | ||||

| BN_PR_SH | 0.665 ** | 8.093 | 0.442 | ||||

| Artifacts (Artif) | Artif_CL | 0.781 ** | 15.151 | 0.610 | 0.916 | 0.923 | 0.670 |

| Artif_SU | 0.784 ** | 15.377 | 0.614 | ||||

| Artif_HR | 0.843 ** | 17.250 | 0.710 | ||||

| Artif_PA | 0.855 ** | 17.143 | 0.732 | ||||

| Artif_CO | 0.894 ** | 17.237 | 0.799 | ||||

| Artif_SH | 0.733 ** | 14.824 | 0.538 | ||||

| Stakeholder-oriented behaviors (SOB) | SOB_IG_1 | 0.935 ** | 16.354 | 0.875 | 0.989 | 0.990 | 0.890 |

| SOB_IG_2 | 0.964 ** | 18.119 | 0.929 | ||||

| SOB_IG_3 | 0.973 ** | 23.970 | 0.947 | ||||

| SOB_IG_4 | 0.949 ** | 24.088 | 0.901 | ||||

| SOB_ID_1 | 0.922 ** | 25.182 | 0.851 | ||||

| SOB_ID_2 | 0.951 ** | 27.194 | 0.904 | ||||

| SOB_ID_3 | 0.952 ** | 25.938 | 0.906 | ||||

| SOB_ID_4 | 0.947 ** | 26.710 | 0.898 | ||||

| SOB_RE_1 | 0.942 ** | 25.258 | 0.887 | ||||

| SOB_RE_2 | 0.934 ** | 24.484 | 0.873 | ||||

| SOB_RE_3 | 0.890 ** | 21.314 | 0.792 | ||||

| SOB_RE_4 | 0.955 ** | 20.000 | 0.912 |

| SBV | BN | Artif | SOB | |

|---|---|---|---|---|

| SBV | 0.889 | 0.876 * (40.777) | 0.416 * (7.597) | 0.587 * (13.455) |

| BN | (0.834; 0.918) | 0.770 | 0.397 * (7.319) | 0.599 * (14.485) |

| Artif | (0.306; 0.526) | (0.289; 0.505) | 0.817 | 0.734 * (24.159) |

| SOB | (0.499; 0.675) | (0.517; 0.681) | (0.674; 0.794) | 0.943 |

| χ2(df); p-Value | χ2/df | CFI | TLI | NFI | RMSEA | GFI | AGFI |

|---|---|---|---|---|---|---|---|

| 1392.166 (591); 0.000 | 2.356 | 0.94 | 0.932 | 0.901 | 0.070 | 0.782 | 0.74 |

| Variables | Indicator | Standardized Loads | t-Value | R2 | Cronbach’s Alpha | CRI | AVE |

|---|---|---|---|---|---|---|---|

| Financial performance (FP) | FP1 | 0.941 * | 20.860 | 0.886 | 0.958 | 0.957 | 0.880 |

| FP2 | 0.933 * | 20.690 | 0.870 | ||||

| FP3 | 0.946 * | 21.093 | 0.894 | ||||

| Market performance (MP) | MP1 | 0.954 * | 19.214 | 0.909 | 0.909 | 0.926 | 0.800 |

| MP 2 | 0.934 * | 20.872 | 0.872 | ||||

| MP 3 | 0.852 * | 18.442 | 0.726 | ||||

| MP 4 | 0.729 * | 14.580 | 0.532 | ||||

| Organizational reputation (OR) | OR1 | 0.935 * | 18.333 | 0.874 | 0.966 | 0.977 | 0.914 |

| OR 2 | 0.951 * | 14.178 | 0.904 | ||||

| OR 3 | 0.944 * | 14.200 | 0.892 | ||||

| OR4 | 0.916 * | 13.354 | 0.839 | ||||

| Organizational commitment (OC) | OC1 | 0.747 * | 15.909 | 0.558 | 0.909 | 0.904 | 0.665 |

| OC2 | 0.750 * | 13.462 | 0.563 | ||||

| OC4 | 0.915 * | 14.000 | 0.837 | ||||

| OC5 | 0.761 * | 15.302 | 0.579 | ||||

| OC7 | 0.860 * | 15.122 | 0.739 | ||||

| Stakeholder-oriented behaviors (SOB) | SOB_IG_1 | 0.898 * | 15.667 | 0.806 | 0.989 | 0.987 | 0.864 |

| SOB_IG_2 | 0.938 * | 19.500 | 0.879 | ||||

| SOB_IG_3 | 0.928 * | 20.972 | 0.862 | ||||

| SOB_IG_4 | 0.897 * | 20.342 | 0.804 | ||||

| SOB_ID_1 | 0.864 * | 19.487 | 0.746 | ||||

| SOB_ID_2 | 0.905 * | 18.250 | 0.818 | ||||

| SOB_ID_3 | 0.927 * | 20.711 | 0.859 | ||||

| SOB_ID_4 | 0.899 * | 20.179 | 0.809 | ||||

| SOB_RE_1 | 0.987 * | 21.051 | 0.975 | ||||

| SOB_RE_2 | 0.966 * | 23.114 | 0.934 | ||||

| SOB_RE_3 | 0.954 * | 20.125 | 0.911 | ||||

| SOB_RE_4 | 0.983 * | 18.860 | 0.966 |

| FP | MP | OR | OC | SOB | |

|---|---|---|---|---|---|

| FP | 0.940 | 0.592 * (14.214) | 0.361 * (6.845) | 0.382 * (7.149) | 0.270 * (4.897) |

| MP | (0.508; 0.676) | 0.872 | 0.631 * (16.335) | 0.605 * (14.295) | 0.527 * (11.692) |

| OR | (0.255; 0.467) | (0.553; 0.709) | 0.956 | 0.708 * (21.015) | 0.469 * (9.763) |

| OC | (0.276; 0.488) | (0.521; 0.689) | (0.640; 0.776) | 0.810 | 0.610 * (15.048) |

| SOB | (0.160; 0.380) | (0.437; 0.617) | (0.373; 0.565) | (0.528; 0.692) | 0.930 |

| χ2(df); p-Value | χ2/df | CFI | TLI | NFI | RMSEA | GFI | AGFI |

|---|---|---|---|---|---|---|---|

| 933.068 (317); 0.000 | 2.943 | 0.951 | 0.942 | 0.928 | 0.084 | 0.798 | 0.742 |

| Hypothesis No. | Structural Relationship | Standardized Coefficients | Robust t-Value | Conclusion | ||

|---|---|---|---|---|---|---|

| H1 | SBV-BN | 0.878 * | 10.590 | Accepted | ||

| H2 | SBV-Artif | 0.293 | 1.301 | Not Accepted | ||

| H3 | BN-Artif | 0.139 | 0.664 | Not Accepted | ||

| H4 | BN-SOB | 0.374 * | 8.745 | Accepted | ||

| H5 | Artif-SOB | 0.580 * | 11.469 | Accepted | ||

| Fit Results | ||||||

| χ2(df); p-Value | χ2/df | CFI | TLI | NFI | RMSEA | RMR |

| 1380.812 (591); 0.000 | 2.336 | 0.941 | 0.933 | 0.902 | 0.069 | 0.037 |

| Hypothesis No. | Structural Relationship | Standardized Coefficients | Robust t-Value | Conclusion | ||

|---|---|---|---|---|---|---|

| H6 | SOB-FP | −0.055 | −0.826 | Not Accepted | ||

| H7 | SOB-MP | 0.304 * | 5.424 | Accepted | ||

| H8 | SOB-OR | 0.066 | 0.949 | Not Accepted | ||

| H9 | SOB-OC | 0.610 * | 7.562 | Accepted | ||

| H10 | MP-FP | 0.648 * | 10.519 | Accepted | ||

| H11 | OR-MP | 0.489 * | 10.167 | Accepted | ||

| H12 | OC-OR | 0.673 * | 6.742 | Accepted | ||

| Fit Results | ||||||

| χ2(df); p-Value | χ2/df | CFI | TLI | NFI | RMSEA | RMR |

| 954.102 (319); 0.000 | 2.991 | 0.950 | 0.94 | 0.93 | 0.008 | 0.036 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ferro-Soto, C.; Macías-Quintana, L.A.; Vázquez-Rodríguez, P. Effect of Stakeholders-Oriented Behavior on the Performance of Sustainable Business. Sustainability 2018, 10, 4724. https://doi.org/10.3390/su10124724

Ferro-Soto C, Macías-Quintana LA, Vázquez-Rodríguez P. Effect of Stakeholders-Oriented Behavior on the Performance of Sustainable Business. Sustainability. 2018; 10(12):4724. https://doi.org/10.3390/su10124724

Chicago/Turabian StyleFerro-Soto, Carlos, Luz Amparo Macías-Quintana, and Paula Vázquez-Rodríguez. 2018. "Effect of Stakeholders-Oriented Behavior on the Performance of Sustainable Business" Sustainability 10, no. 12: 4724. https://doi.org/10.3390/su10124724

APA StyleFerro-Soto, C., Macías-Quintana, L. A., & Vázquez-Rodríguez, P. (2018). Effect of Stakeholders-Oriented Behavior on the Performance of Sustainable Business. Sustainability, 10(12), 4724. https://doi.org/10.3390/su10124724