Does a Board Chairman’s Political Connection Affect Green Investment?—From a Sustainable Perspective

,

,

Abstract

:1. Introduction

2. Literature Review

2.1. Environmental Performance

2.2. The Roles of Political Connection

3. Hypotheses Development

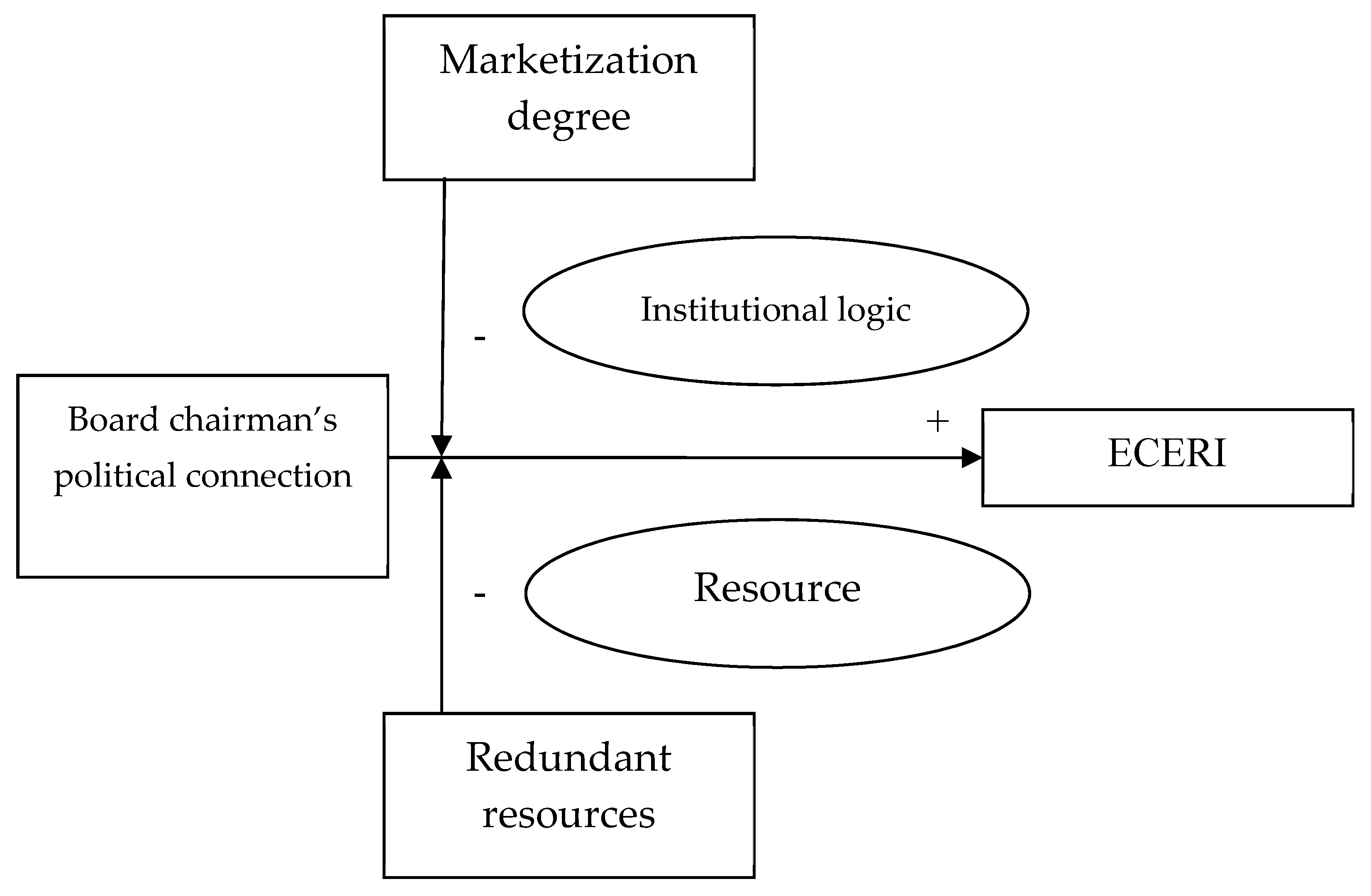

3.1. The Impact of Board Chairmen’s Political Connection on ECERI

3.2. The Moderating Effect of Marketization Degree

3.3. The Moderating Effect of Redundant Resources

4. Research Design

4.1. Sample and Data Sources

4.2. Measurements

4.3. Regression Models

5. Empirical Results

5.1. Descriptive Statistics

5.2. Correlation Analysis

5.3. Regression Analysis

5.4. Robustness Tests

6. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Walden, W.D.; Schwartz, B.N. Environmental disclosures and public policy pressure. J. Account. Public Policy 1997, 16, 125–154. [Google Scholar]

- Ahmad, Z.; Hassan, S.; Mohammad, J. Determinants of environmental reporting in Malaysia. Int. J. Bus. Stud. 2003, 11, 69–90. [Google Scholar]

- Zeng, S.X.; Xu, X.D.; Yin, H.T.; Tam, C.M. Factors that drive Chinese listed companies in voluntary disclosure of environmental information. J. Bus. Ethics 2012, 109, 309–321. [Google Scholar] [CrossRef]

- Chen, J.C.; Cho, C.H.; Patten, D.M. Initiating disclosure of environmental liability information: An empirical analysis of firm choice. J. Bus. Ethics 2014, 125, 681–692. [Google Scholar] [CrossRef]

- Jizi, M.I.; Salama, A.; Dixon, R.; Stratling, R. Corporate governance and corporate social responsibility disclosure: Evidence from the US banking sector. J. Bus. Ethics 2014, 125, 601–615. [Google Scholar] [CrossRef] [Green Version]

- Lewis, B.W.; Walls, J.L.; Dowell, G.W.S. Difference in degrees: CEO characteristics and firm environmental disclosure. Strateg. Manag. J. 2014, 35, 712–722. [Google Scholar] [CrossRef]

- Liu, X.; Zhang, C. Corporate governance, social responsibility information disclosure, and enterprise value in China. J. Clean. Prod. 2017, 142, 1075–1084. [Google Scholar] [CrossRef]

- Freedman, M.; Jaggi, B. Pollution disclosure, pollution performance and economic performance. Omega 1982, 10, 167–176. [Google Scholar] [CrossRef]

- Richardson, A.; Welker, M. Social disclosure, financial disclosure and the cost of equity capital. Account. Organ. Soc. 2001, 26, 597–616. [Google Scholar] [CrossRef]

- Cooke, P. Green governance and green clusters: Reginal & national policies for the climate change challenge of central & Eastern Europe. J. Open Innov. Technol. Mark. Complex. 2015, 1, 1. [Google Scholar]

- Cong, Y.; Freedman, M. Corporate governance and environmental performance and disclosures. Adv. Account. Incorp. Adv. Int. Account. 2011, 27, 223–232. [Google Scholar] [CrossRef]

- Kock, C.J.; Santalo, J.; Diestre, L. Corporate governance and the environment: What type of governance creates greener companies? J. Manag. Stud. 2012, 49, 492–514. [Google Scholar] [CrossRef]

- Adhikari, A.; Derashid, C.; Zhang, H. Public policy, political connections, and effective tax rates: Longitudinal evidence from Malaysia. J. Account. Public Policy 2006, 25, 574–595. [Google Scholar] [CrossRef]

- Claessens, S.; Feijen, E.; Laeven, L. Political connections and preferential access to finance: The role of campaign contributions. J. Financ. Econ. 2008, 88, 554–580. [Google Scholar] [CrossRef]

- Liu, Q.; Tang, J.; Tian, G.G. Does political capital create value in the IPO market? Evidence from China. J. Corp. Financ. 2013, 23, 395–413. [Google Scholar] [CrossRef]

- Kim, J.; Jung, S. Study on CEO characteristics for management of public art performance centers. J. Open Innov. Technol. Mark. Complex. 2015, 1, 5. [Google Scholar] [CrossRef]

- Shi, W.; Markoczy, L.; Stan, C.V. The continuing importance of political ties in China. Acad. Manag. Perspect. 2014, 28, 57–75. [Google Scholar] [CrossRef]

- Yuan, Q. Public Governance, Political Connectedness, and CEO Turnover: Evidence from Chinese State-Owned Enterprises; Working Paper; The University of Melbourne: Melbourne, Australia, 2011. [Google Scholar]

- Chan, K.S.; Dang, V.Q.T.; Yan, I.K.M. Chinese firm’s political connection, ownership and financial constraints. Econ. Lett. 2012, 115, 164–167. [Google Scholar] [CrossRef] [Green Version]

- Wang, L. Protection or expropriation: Politically connected independent directors in China. J. Bank. Financ. 2015, 55, 92–106. [Google Scholar] [CrossRef]

- Fan, J.P.H.; Wong, T.J.; Zhang, T. Politically connected CEOs, corporate governance and post-IPO performance of China’s newly partially privatized firms. J. Financ. Econ. 2007, 84, 330–357. [Google Scholar] [CrossRef]

- Al-Tuwaijri, S.A.; Christensen, T.E.; Hughes, K.E., II. The relations among environmental disclosure, environmental performance, and economics performance: A simultaneous equations approach. Account. Organ. Soc. 2004, 29, 447–471. [Google Scholar] [CrossRef]

- Hughes, S.B.; Anderson, A.; Golden, S. Corporate environmental disclosures: Are they useful in determining environmental performance? J. Account. Public Policy 2001, 20, 217–240. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Overell, M.B.; Chapple, L. Environmental reporting and its relation to corporate environmental performance. Abacus 2011, 47, 27–60. [Google Scholar] [CrossRef]

- Liu, Z.G.; Liu, T.T.; McConkey, B.G.; Li, X. Empirical analysis on environmental disclosure and environmental performance level of listed steel companies. Energy Procedia 2011, 5, 2211–2218. [Google Scholar] [CrossRef]

- Luo, L.; Tang, Q. Does voluntary carbon disclosure reflect underlying carbon performance? J. Contemp. Account. Econ. 2014, 10, 191–205. [Google Scholar] [CrossRef]

- Cho, C.H.; Patten, D.M. The role of environmental disclosures as tools of legitimacy: A research note. Account. Organ. Soc. 2007, 32, 639–647. [Google Scholar] [CrossRef]

- Jo, H.; Harjoto, M.A. The causal effect of corporate governance on corporate social responsibility. J. Bus. Ethics 2012, 106, 53–72. [Google Scholar] [CrossRef]

- Wang, Q.; Wong, T.J.; Xia, L. State ownership, the institutional environment, and auditor choice: Evidence from China. J. Account. Econ. 2008, 46, 112–134. [Google Scholar] [CrossRef]

- Chaney, P.K.; Faccio, M.; Parsley, D. The quality of accounting information in politically connected firms. J. Account. Econ. 2011, 51, 58–76. [Google Scholar] [CrossRef]

- Huang, M.; Wong, T.J.; Zhang, T. Political considerations in the decision of Chinese SOEs to list in Hong Kong. J. Account. Econ. 2012, 53, 435–449. [Google Scholar] [CrossRef]

- Li, S.; Song, X.; Wu, H. Political connection, ownership structure, and corporate philanthropy in China: A strategic-political perspective. J. Bus. Ethics 2015, 129, 399–411. [Google Scholar] [CrossRef]

- Bertrand, M.; Kramarz, F.; Schoar, A.; Thesmar, D. Politicians, Firms and the Political Business Cycle: Evidence from France; Working Paper; University of Chicago: Chicago, IL, USA, 2007. [Google Scholar]

- Kim, C.; Zhang, L. Corporate political connections and tax aggressiveness. Contemp. Account. Res. 2015, 33, 78–114. [Google Scholar] [CrossRef]

- Berkman, H.; Cole, R.A.; Fu, L.J. Political connections and minority-shareholder protection: Evidence from securities-market regulation in China. J. Financ. Qual. Anal. 2010, 45, 1391–1417. [Google Scholar] [CrossRef]

- Niessen, A.; Ruenzi, S. Political connectedness and firm performance: Evidence from Germany. Ger. Econ. Rev. 2010, 11, 441–464. [Google Scholar] [CrossRef]

- Sheng, S.; Zhou, K.Z.; Li, J.J. The effects of business and political ties on firm performance: Evidence from China. J. Mark. 2011, 75, 1–15. [Google Scholar] [CrossRef]

- Wang, H.; Qian, C. Corporate philanthropy and corporate financial performance: The roles of stakeholder response and political access. Acad. Manag. J. 2011, 54, 1159–1181. [Google Scholar] [CrossRef]

- Fan, J.P.H.; Rui, O.M.; Zhao, M. Public governance and corporate finance: Evidence from corruption cases. J. Comp. Econ. 2008, 36, 343–364. [Google Scholar] [CrossRef]

- Li, H.; Meng, L.; Wang, Q.; Zhou, L. Political connections, financing and firm performance: Evidence from Chinese private firms. J. Dev. Econ. 2008, 87, 283–299. [Google Scholar] [CrossRef]

- Houston, J.F.; Jiang, L.; Lin, C.; Ma, Y. Political connections and the cost of bank loans. J. Account. Res. 2014, 52, 193–243. [Google Scholar] [CrossRef]

- Bunkanwanicha, P.; Wiwattanakantang, Y. Big business owners in politics. Rev. Financ. Stud. 2009, 22, 2133–2168. [Google Scholar] [CrossRef]

- Johnson, S.; Mitton, T. Cronyism and capital controls: Evidence from Malaysia. J. Financ. Econ. 2003, 67, 351–382. [Google Scholar] [CrossRef]

- Tahoun, A. The role of stock ownership by US members of congress on the market for political favors. J. Financ. Econ. 2014, 111, 86–110. [Google Scholar] [CrossRef]

- Thornton, P.H.; Ocasio, W. Institutional logics and the historical contingency of power in organizations: Executive succession in the higher education publishing industry, 1958–1990. Am. J. Sociol. 1999, 105, 801–843. [Google Scholar] [CrossRef]

- Fisman, R.; Wang, Y. The mortality cost of political connections. Rev. Econ. Stud. 2015, 82, 1346–1382. [Google Scholar] [CrossRef]

- Thompson, J. Organizations in Action: Social Science Bases of Administrative Theory; McGraw-Hill Book Company: New York, NY, USA, 1967. [Google Scholar]

- Pfeffer, J.; Salancik, G. The External Control of Organizations: A Resource Dependence Perspective; Harper and Row: New York, NY, USA, 1978. [Google Scholar]

- Hillman, A.J.; Zardkoohi, A.; Bierman, L. Corporate political strategies and firm performance: Indications of firm-specific benefits from personal service in the US government. Strateg. Manag. J. 1999, 20, 67–81. [Google Scholar] [CrossRef]

- Ozer, M.; Alakent, E.; Ahsan, M. Institutional ownership and corporate political strategies: Does heterogeneity of institutional owners matter? Strateg. Manag. Rev. 2010, 4, 18–29. [Google Scholar]

- Vanacker, T.; Collewaert, V.; Zahra, S.A. Slack resources, firm performance, and the institutional context: Evidence from privately held European firms. Strateg. Manag. J. 2016, 38, 1305–1326. [Google Scholar] [CrossRef]

- Zhou, W. Political connections and entrepreneurial investment: Evidence from China’s transition economy. J. Bus. Ventur. 2013, 28, 299–315. [Google Scholar] [CrossRef]

- Fan, G.; Wang, X.; Zhu, H. NERI Index of Marketization of China’s Provinces 2011 Report; Economics Science Press: Beijing, China, 2011. [Google Scholar]

- Lin, Z.; Liu, S.; Sun, F. The impact of financing constraints and agency costs on corporate R&D investment: Evidence from China. Int. Rev. Financ. 2017, 17, 3–42. [Google Scholar]

- Fan, J.P.H.; Wong, T.J. Corporate ownership structure and the informativeness of accounting earning in East Asia. J. Account. Econ. 2002, 33, 401–425. [Google Scholar] [CrossRef]

- Inoue, C.F.K.V.; Lazzarini, S.G.; Musacchio, A. Leviathan as a minority shareholder: Firm-level implications of state equity purchases. Acad. Manag. J. 2013, 56, 1775–1801. [Google Scholar] [CrossRef]

- Liu, T.; Deng, Y.; Chan, F. Evidential supplier selection based on DEMATEL and game theory. Int. J. Fuzzy Syst. 2017, 1–13. [Google Scholar] [CrossRef]

{kind=link}

| Variable | Obs | Mean | SD | Min | Max |

|---|---|---|---|---|---|

| ECERI | 146 | 0.004 | 0.009 | 0.000 | 0.066 |

| BCPC | 146 | 0.315 | 0.466 | 0 | 1 |

| size | 146 | 23.051 | 1.339 | 20.407 | 26.166 |

| roa | 146 | 0.045 | 0.049 | −0.096 | 0.184 |

| age | 146 | 12.226 | 5.270 | 1 | 22 |

| no1share | 146 | 0.407 | 0.160 | 0.114 | 0.743 |

| pid | 146 | 0.363 | 0.051 | 0.300 | 0.571 |

| state | 146 | 0.781 | 0.415 | 0 | 1 |

| index | 146 | 9.042 | 2.120 | 0.380 | 11.800 |

| rr | 146 | 0.694 | 0.160 | 0.335 | 0.942 |

| Variable | ECERI | BCPC | Size | Roa | Age | No1share | Pid | State | Index | rr |

|---|---|---|---|---|---|---|---|---|---|---|

| ECERI | 1 | |||||||||

| BCPC | 0.109 | 1 | ||||||||

| size | 0.064 | −0.054 | 1 | |||||||

| roa | −0.112 | 0.135 | −0.013 | 1 | ||||||

| age | −0.147 * | 0.111 | 0.296 *** | −0.057 | 1 | |||||

| no1share | −0.077 | −0.152 * | 0.202 ** | −0.057 | 0.004 | 1 | ||||

| pid | 0.004 | 0.212 ** | −0.026 | 0.077 | 0.062 | 0.161 * | 1 | |||

| state | 0.115 | −0.247 *** | 0.202** | −0.305 *** | 0.209 ** | 0.219 *** | −0.142 * | 1 | ||

| index | −0.277 *** | 0.055 | −0.314 *** | 0.222 *** | −0.191** | −0.011 | −0.017 | −0.217 *** | 1 | |

| rr | −0.364 *** | −0.144 * | 0.001 | 0.293 *** | 0.013 | −0.109 | −0.158 * | −0.027 | 0.221 *** | 1 |

| Variable | Model 1 | Model 2 | Model 3 | Model 4 |

|---|---|---|---|---|

| BCPC | 0.004 ** (0.002) | 0.015 ** (0.006) | 0.017 ** (0.007) | |

| md | −0.001 (0.000) | |||

| md*BCPC | −0.001 * (0.001) | |||

| rr | −0.012 ** (0.006) | |||

| rr*BCPC | −0.021 ** (0.009) | |||

| size | 0.001 ** (0.001) | 0.001 ** (0.001) | 0.001 (0.001) | 0.001 * (0.001) |

| roa | −0.013 (0.016) | −0.016 (0.016) | −0.007 ( 0.015) | 0.003 (0.016) |

| age | −0.000 ** (0.000) | −0.000** (0.000) | −0.000 *** (0.000) | −0.000 ** (0.000) |

| no1share | −0.008 (0.005) | −0.006 (0.005) | −0.003 (0.005) | −0.007 (0.005) |

| pid | 0.015 (0.015) | 0.009 (0.015) | 0.003 (0.014) | −0.002 (0.014) |

| state | 0.003 (0.002) | 0.004 * (0.002) | 0.003 (0.002) | 0.004 ** (0.002) |

| year | Controlled | Controlled | Controlled | Controlled |

| _cons | −0.015 (0.014) | −0.015 (0.014) | 0.004 (0.015) | −0.003 (0.014) |

| Obs | 146 | 146 | 146 | 146 |

| F-value | 1.430 | 1.740 * | 2.500 *** | 3.290 *** |

| R2 | 0.114 | 0.146 | 0.224 | 0.275 |

| Variable | Model 5 | Model 6 | Model 7 | Model 8 | Model 9 |

|---|---|---|---|---|---|

| Subsample consisting of SOEs | Full sample | Heckman Stage 2 | |||

| BCPC | 0.004* (0.002) | 0.029 *** (0.009) | 0.025 *** (0.008) | 0.003 ** (0.002) | |

| md | −0.001 (0.001) | ||||

| md*BCPC | −0.003 *** (0.001) | ||||

| rr | −0.016 ** (0.007) | ||||

| rr*BCPC | −0.033 *** (0.012) | ||||

| BCPCt-1 | 0.004 ** (0.002) | ||||

| size | 0.001 * (0.000) | 0.001 (0.001) | 0.001 (0.001) | 0.001 * (0.001) | −0.002 (0.002) |

| roa | −0.024 (0.022) | −0.010 (0.021) | 0.019 (0.022) | −0.012 (0.017) | −0.036 ** (0.018) |

| age | −0.000 ** (0.000) | −0.000 ** (0.000) | −0.000 (0.000) | −0.000 ** (0.000) | −0.001 *** (0.000) |

| no1share | −0.007 (0.007) | −0.006 (0.006) | −0.006 (0.006) | −0.006 (0.005) | −0.000 (0.000) |

| pid | 0.008 (0.020) | −0.010 (0.019) | 0.004 (0.018) | 0.009 (0.016) | 0.018 (0.015) |

| state | 0.005 ** (0.002) | −0.002 (0.003) | |||

| year | Controlled | Controlled | Controlled | Controlled | Controlled |

| _cons | −0.009 (0.018) | 0.014 (0.018) | −0.001 (0.016) | −0.017 (0.015) | 0.107 * (0.061) |

| Inverse Mills ratio | −0.014 ** (0.007) | ||||

| Obs | 114 | 114 | 114 | 138 | 146 |

| F-value | 1.520 | 3.030 *** | 3.660 *** | 1.640 * | 1.950 ** |

| R2 | 0.153 | 0.300 | 0.341 | 0.146 | 0.173 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wang, K.; Zhang, H.-M.; Tsai, S.-B.; Wu, L.-D.; Xue, K.-K.; Fan, H.-J.; Zhou, J.; Chen, Q. Does a Board Chairman’s Political Connection Affect Green Investment?—From a Sustainable Perspective. Sustainability 2018, 10, 582. https://doi.org/10.3390/su10030582

Wang K, Zhang H-M, Tsai S-B, Wu L-D, Xue K-K, Fan H-J, Zhou J, Chen Q. Does a Board Chairman’s Political Connection Affect Green Investment?—From a Sustainable Perspective. Sustainability. 2018; 10(3):582. https://doi.org/10.3390/su10030582

Chicago/Turabian StyleWang, Kai, Hao-Min Zhang, Sang-Bing Tsai, Li-Dong Wu, Kun-Kun Xue, He-Jun Fan, Jie Zhou, and Quan Chen. 2018. "Does a Board Chairman’s Political Connection Affect Green Investment?—From a Sustainable Perspective" Sustainability 10, no. 3: 582. https://doi.org/10.3390/su10030582

APA StyleWang, K., Zhang, H. -M., Tsai, S. -B., Wu, L. -D., Xue, K. -K., Fan, H. -J., Zhou, J., & Chen, Q. (2018). Does a Board Chairman’s Political Connection Affect Green Investment?—From a Sustainable Perspective. Sustainability, 10(3), 582. https://doi.org/10.3390/su10030582