Cost-Sharing Contracts for Energy Saving and Emissions Reduction of a Supply Chain under the Conditions of Government Subsidies and a Carbon Tax

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

- (1)

- If the retailer cooperates with the manufacturer to save energy and reduce emissions using cost-sharing contracts, which contract should that retailer select: sharing the energy-saving R&D cost, carbon emissions reduction cost during production, or both? Which represents the optimal cost-sharing strategy?

- (2)

- How do the above three cost-sharing strategies influence the energy-saving and emissions reduction strategies of the manufacturer? In particular, how does energy-saving cost-sharing on the part of the retailer impact the carbon emissions reduction strategy of the manufacturer? Can cost-sharing for carbon emissions reduction from the retailer improve the level of energy saving among manufacturers?

- (3)

- What are the influences of government subsidies and carbon tax policies on cooperation, energy saving and emissions reduction, and the profits of node enterprises in the supply chain?

2. Literature Review

3. Model Description and Hypotheses

- (1)

- The manufacturer has a marginal production cost of and it sells products to the retailer at wholesale price . Then, the retailer sells the products to consumers at retail price p.

- (2)

- The energy-saving level of products is . The higher the energy-saving level, the lower the energy consumption of the products per unit service life. After the products are designed, all finished products have the same energy-saving level. In reference to [16], the energy-saving R&D cost of the products is , where is the energy-saving cost coefficient.

- (3)

- The manufacturer has carbon emissions during the production process, and the initial carbon-emissions level for producing per unit of product is . To reduce the tax burden or for the sake of social responsibility, the manufacturer is likely to reduce their carbon emissions. The carbon-emissions level while producing the unit product is () after emissions reduction. The emission-reduction cost is , where is the cost coefficient of carbon emissions reduction [23].

- (4)

- On the one hand, currently more than ten countries and regions have implemented a carbon labelling system. By using the system, the amount of greenhouse gas discharged during the production of goods is indicated using quantitative indices on product labels, so as to inform consumers of the carbon information of products. Therefore, as consumers’ consciousness of environmental protection gets stronger, market demand is influenced by the carbon-emissions level of enterprises [23,34]. On the other hand, many countries have implemented an energy efficiency labelling system for energy-saving products, to inform consumers of the energy consumption grade of products. Therefore, market demand is also affected by the energy-saving level of products [16,17,18]. By combining these studies, it is assumed that the market demand is jointly influenced by the retail price, carbon-emissions level, and energy-saving level of products. The demand function is:where is the potential market capacity, is the retail price of products, () is the sensitivity coefficient of consumers to the carbon-emission level of enterprises, and () is the sensitivity coefficient of consumers to the energy-saving level of products.

- (5)

- To encourage enterprises to produce more energy-saving products, the government entrusts a third party to carry out free energy-saving certification for enterprises, and then provides subsidies for the enterprises according to the certification results. Zhang et al. [19] set the government subsidy to be a fixed amount that is unrelated to product/process energy-saving levels; however, in reality, the subsidy intensity is classified according to the energy efficiency index of products. For example, the Chinese government provides subsidies of 240 to 400 yuan for each variable-frequency air conditioner, and 100 to 400 yuan for each LCD TV set [3]. Therefore, the research supposes that the government provides subsidies for manufacturers based on the energy-saving level of products. The energy-saving subsidy per unit of product is —that is, the higher the energy-saving level, the larger the subsidy, in which denotes the subsidy coefficient .

- (6)

- To protect the environment, the government levies a carbon tax on enterprises, to force them to reduce their carbon emissions. It imposes carbon tax per unit carbon emission [34].

- (7)

- Owing to the downstream retailer selling the final products to consumers, that retailer shares a common interest with the manufacturer. For this reason, the retailer has the motivation to encourage the manufacturer to save energy and reduce emissions, so as to improve market demand and profits. For example, Wal-Mart abates pollution jointly with upstream manufacturers, and also cooperates with them to improve the energy efficiency of most energy-intensive products by 25%. Suppose that the retailer provides a cost-sharing contract for the manufacturer, where and represent the shared proportion of the energy-saving and emission-reduction costs, respectively—in that case, (i) when , the retailer does not provide any contract and does not cooperate with the manufacturer, or NCS; (ii) if , then the retailer only offers an ECS contract; (iii) if , then the retailer only provides a CCS contract; (iv) when , then it represents the BCS for energy saving and emissions reduction.

- (8)

- According to the above descriptions, the profit function of the retailer is:The profit function of the manufacturer is:

- (9)

- To make our research realistic and avoid trivial results, we assume , and (see the proof of Theorem 1 for more details).

- Stage 1

- (contract incentive): the retailer decides the cost-sharing contract .

- Stage 2

- (product R&D): the manufacturer decides the energy-saving level of the products.

- Stage 3

- (product production): the manufacturer determines the carbon emissions level .

- Stage 4

- (product wholesale): the manufacturer sets the wholesale price of the products.

- Stage 5

- (product retail): the retailer determines the retail price of the products.

4. Centralised Decision-Making

5. Decentralised Decision-Making

5.1. No Cost-Sharing (NCS) Contract

5.2. Energy-Saving Cost-Sharing Contract

5.3. Carbon Emissions Reduction Cost-Sharing Contract

5.4. Bivariate Cost-Sharing Contract

6. Influence of Government Policies on Energy Saving and Emissions Reduction of the Supply Chain

7. Numerical Analysis

8. Conclusions

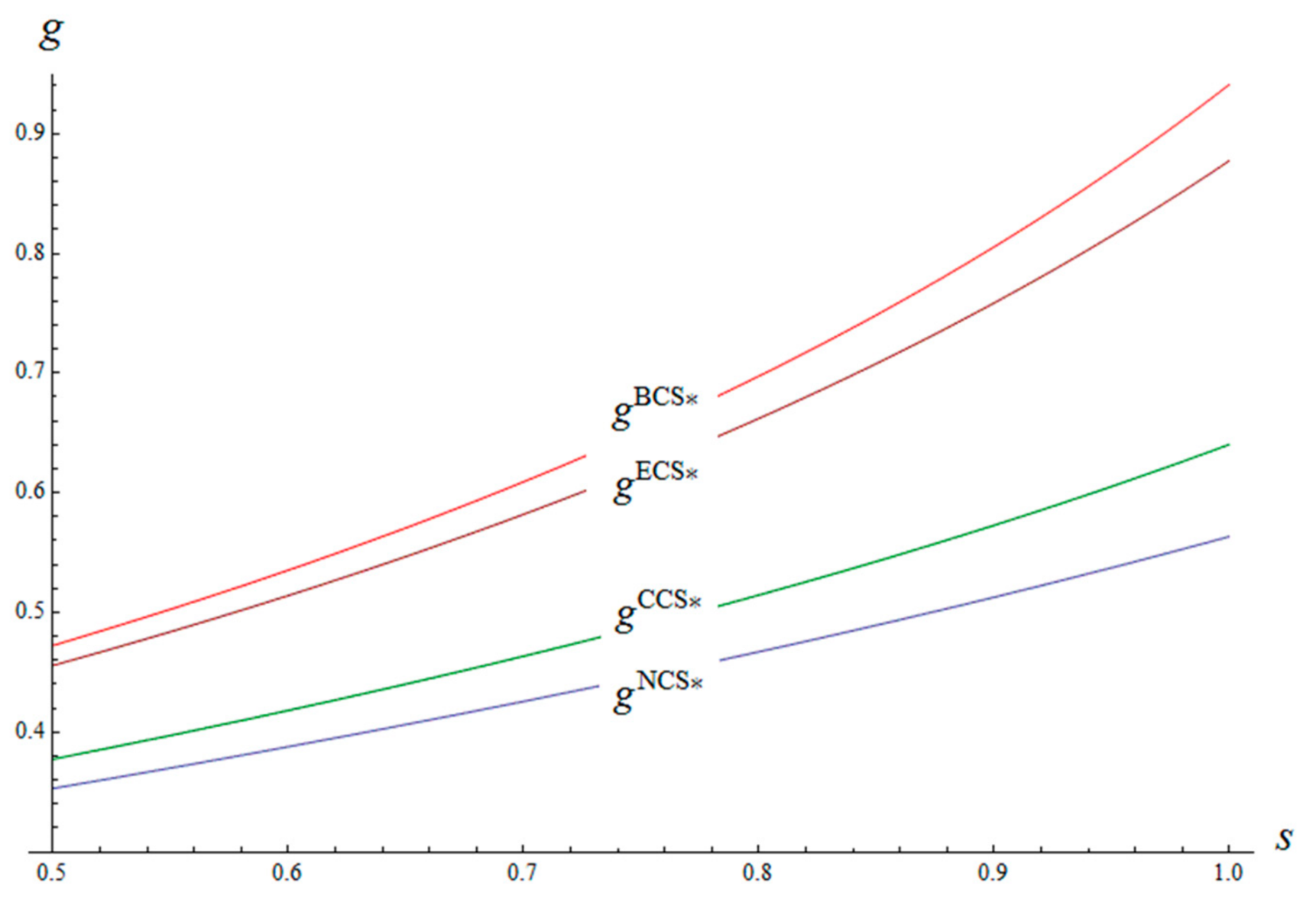

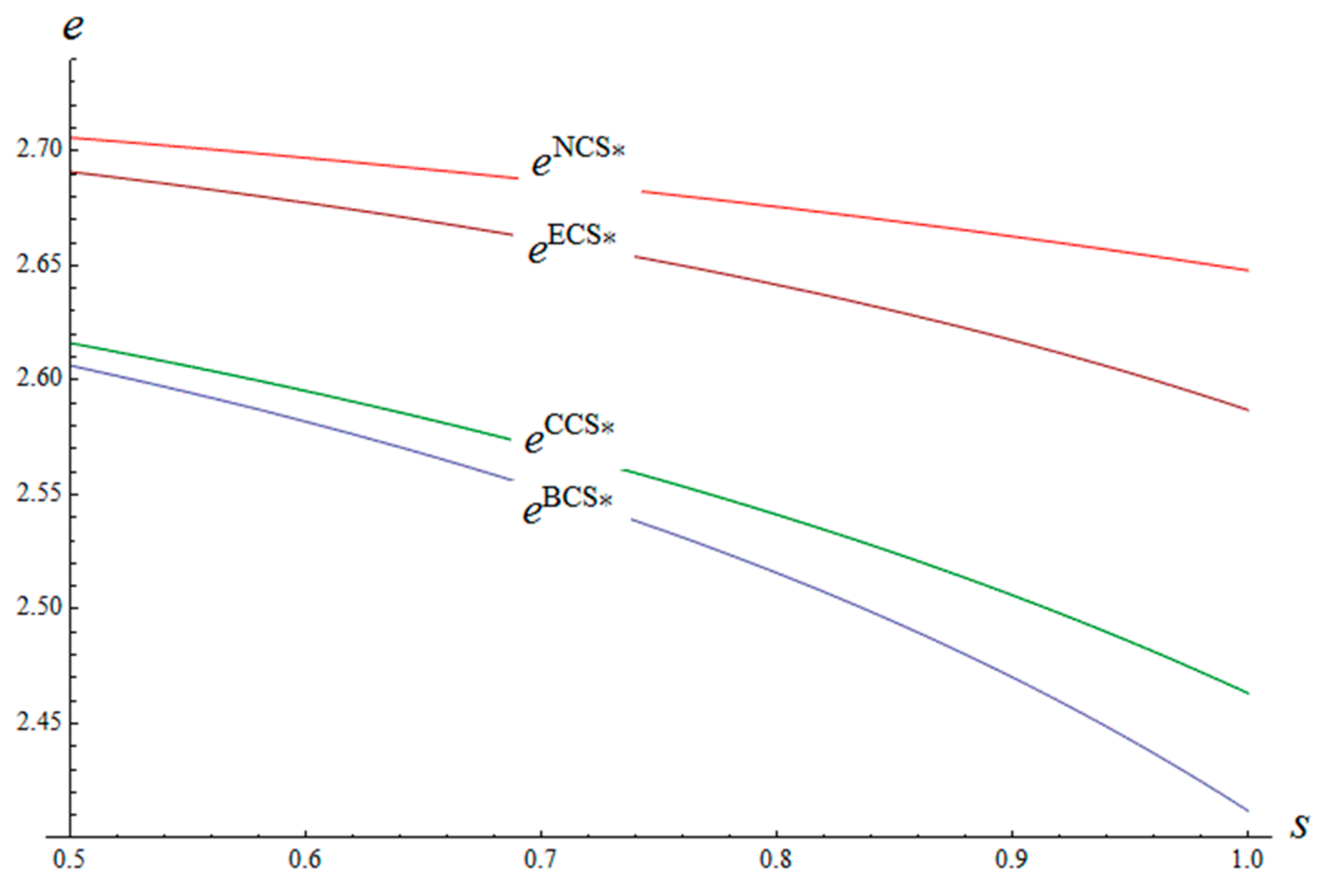

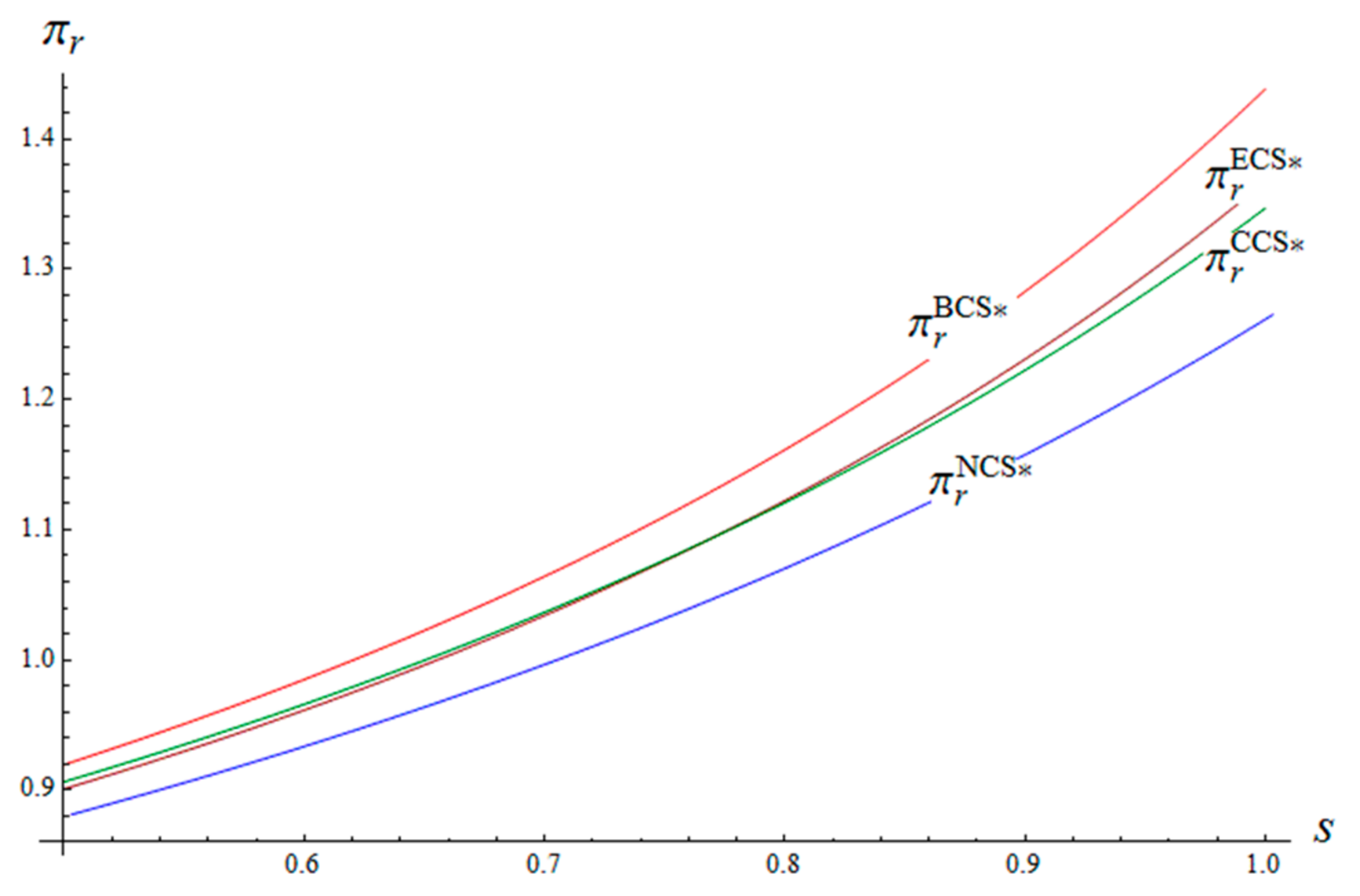

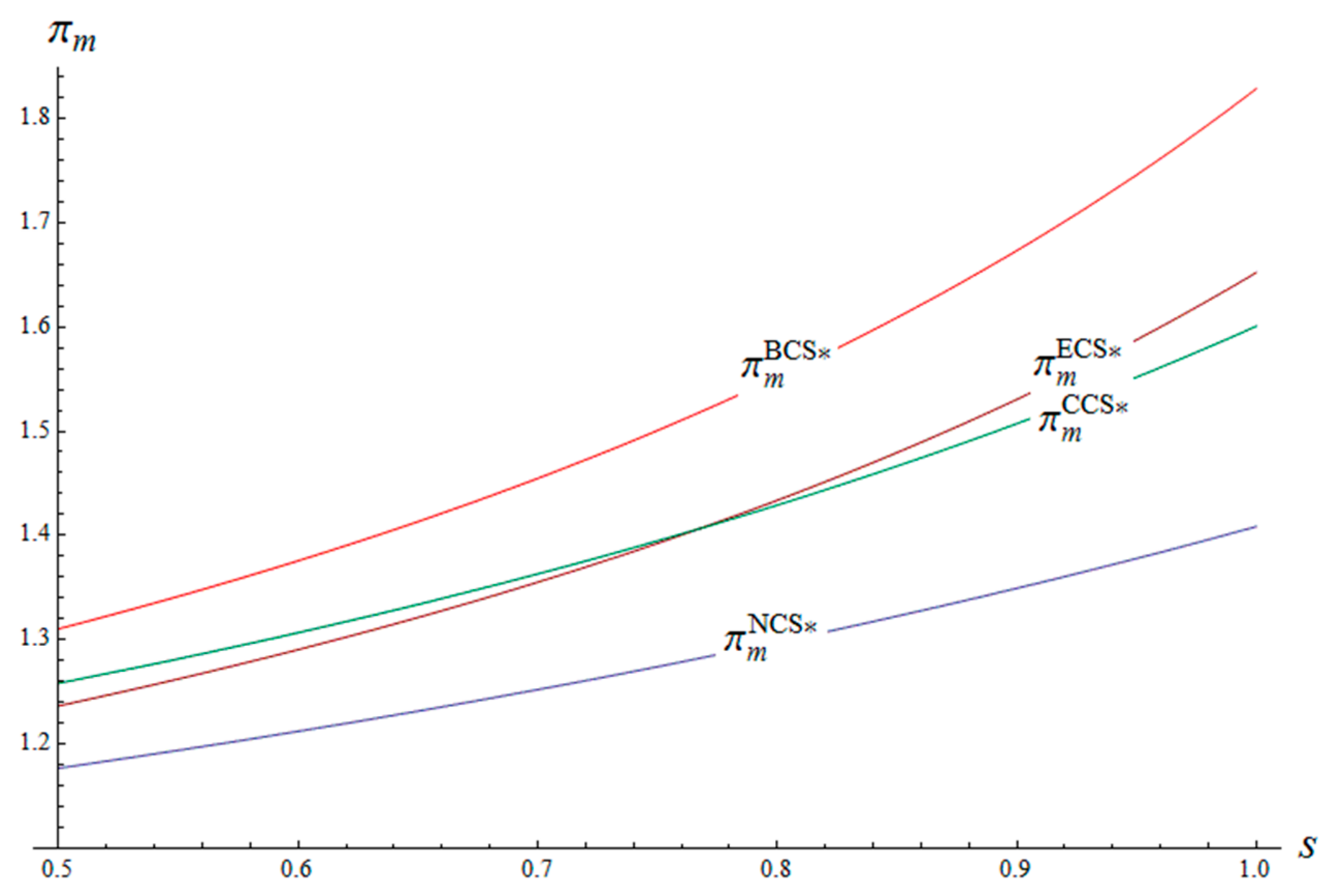

- (1)

- Compared with an NCS contract, cost-sharing contracts can better promote energy saving and emissions reduction among manufacturers, and are also beneficial to the profits of the enterprises in the supply chain.

- (2)

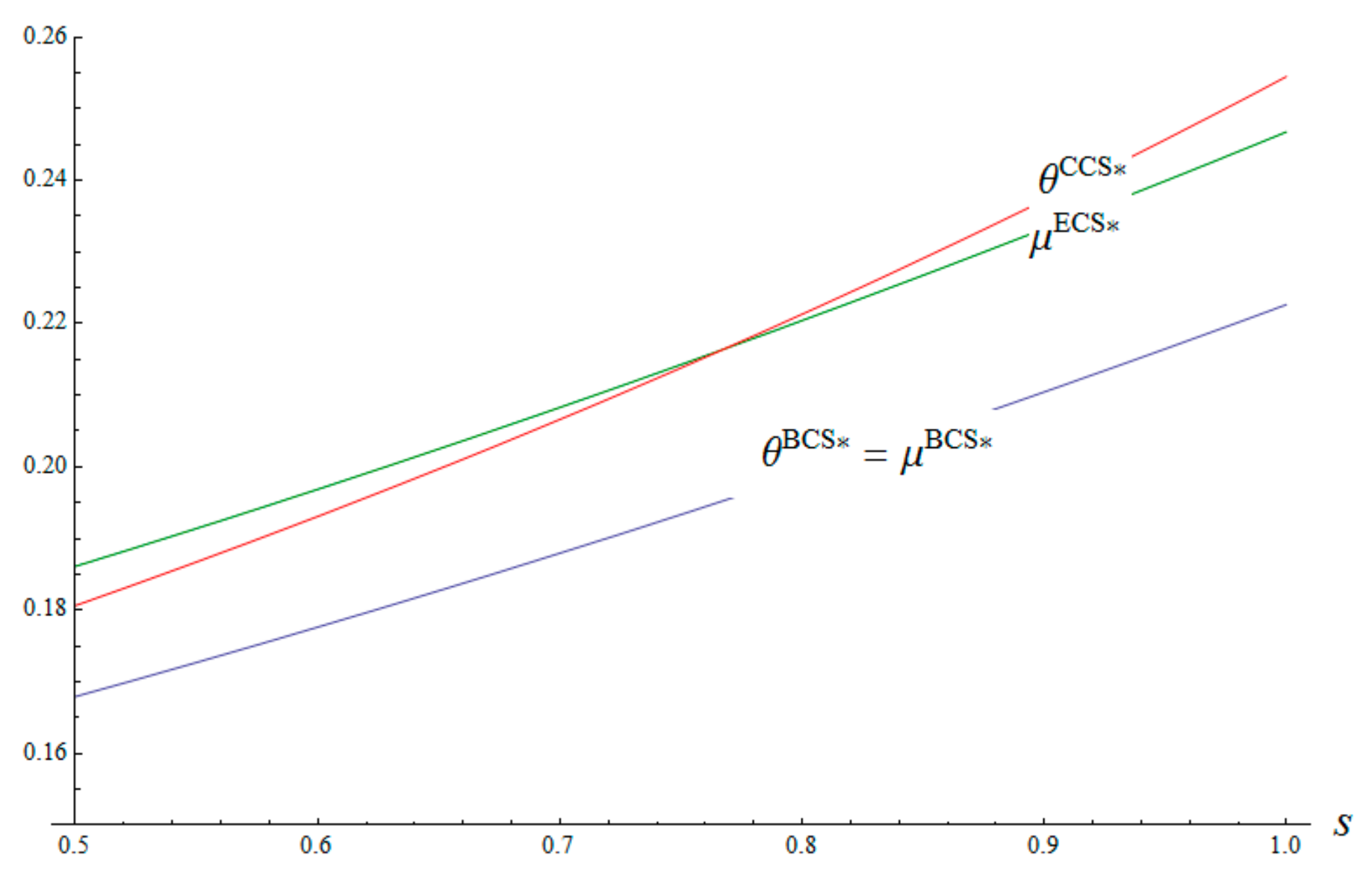

- If the retailer only offers a single cost-sharing contract, then the following conclusions apply: the manufacturer pays more attention to the input with regards to emissions reduction (the carbon-emission level thus decreases) when the retailer provides a CCS contract, while the manufacturer focuses on energy-saving R&D (energy-saving levels become higher) when the retailer offers an ECS contract. The manufacturer and the retailer pay more attention to emissions reduction when the carbon tax is imposed by the government and the carbon emissions consciousness of consumers are high enough. Under these conditions, a CCS contract is better able to improve the profits of the two parties, compared with an ECS contract. When the energy-saving subsidies from the government and consumer awareness of energy conservation are high enough, the manufacturer and retailer tend to pay closer attention to energy saving. In that context, the ECS contract earns both parties more profit than under a CCS contract.

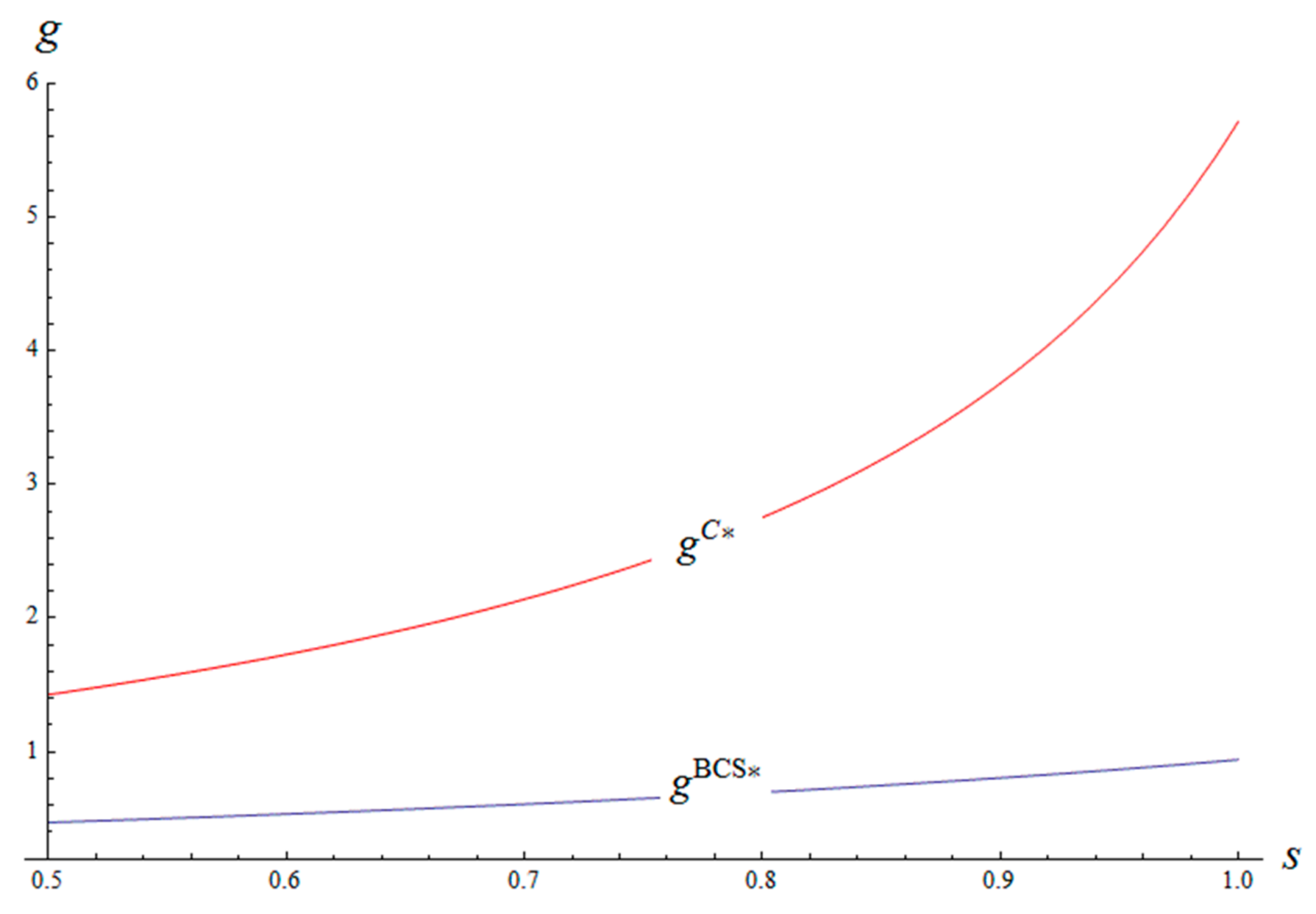

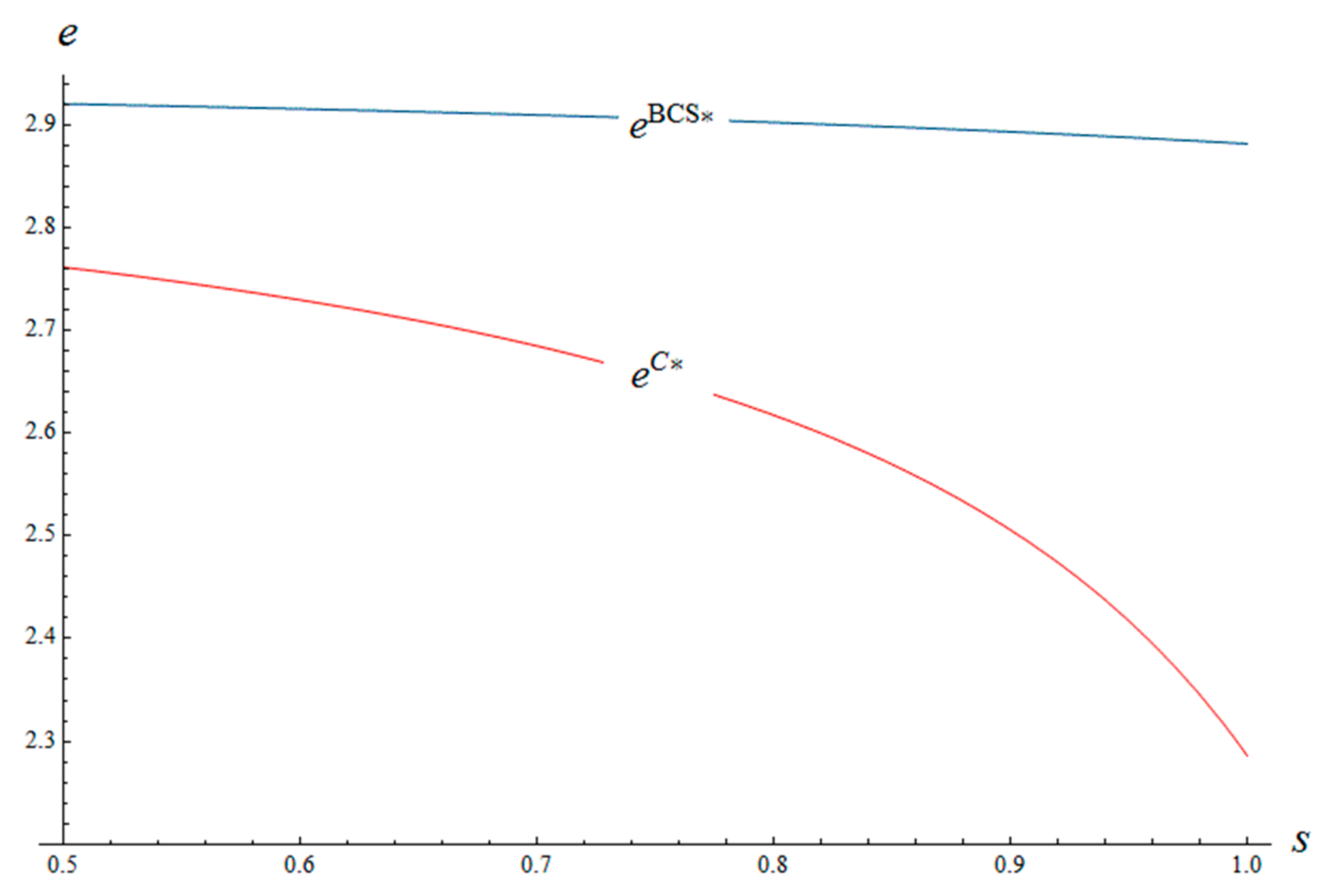

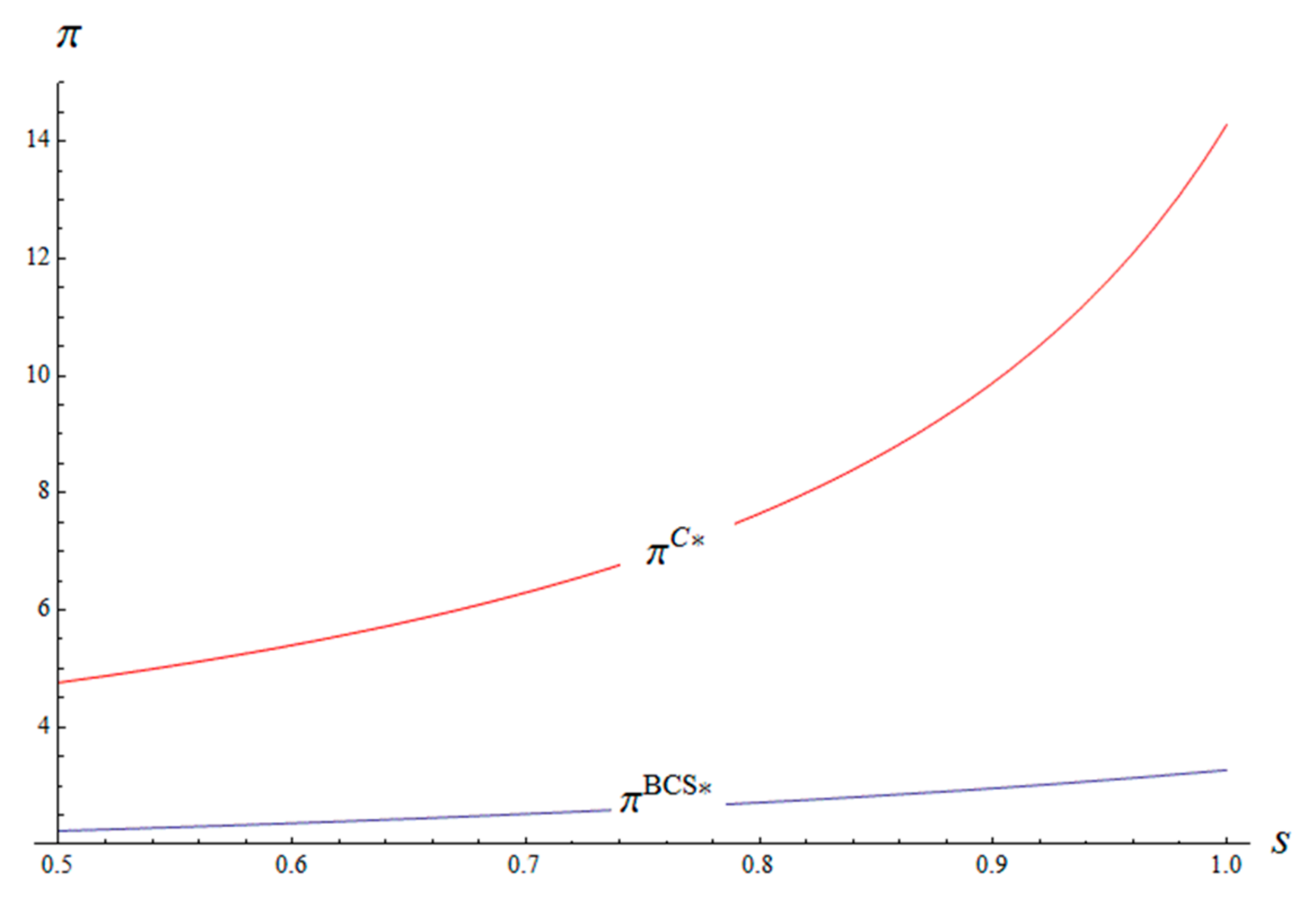

- (3)

- The BCS contract (from the retailer) is superior to single cost-sharing contracts, and brings about smaller cost-shares than those under a single cost-sharing contract. Although the BCS contract improves the supply chain, the energy-saving level and carbon-emissions level of the manufacturer, as well as the total profit of the supply chain, are lower than those under a centralised decision-making framework. In other words, the BCS contract fails to coordinate the supply chain perfectly.

- (4)

- An increase in the subsidy coefficient not only improves cost-sharing proportions, but also facilitates energy saving and emissions reduction along the supply chain. Aside from these, it also boosts the profits of the retailer and the manufacturer. Therefore, the government should actively implement a subsidy policy and enhance the intensity thereof.

- (5)

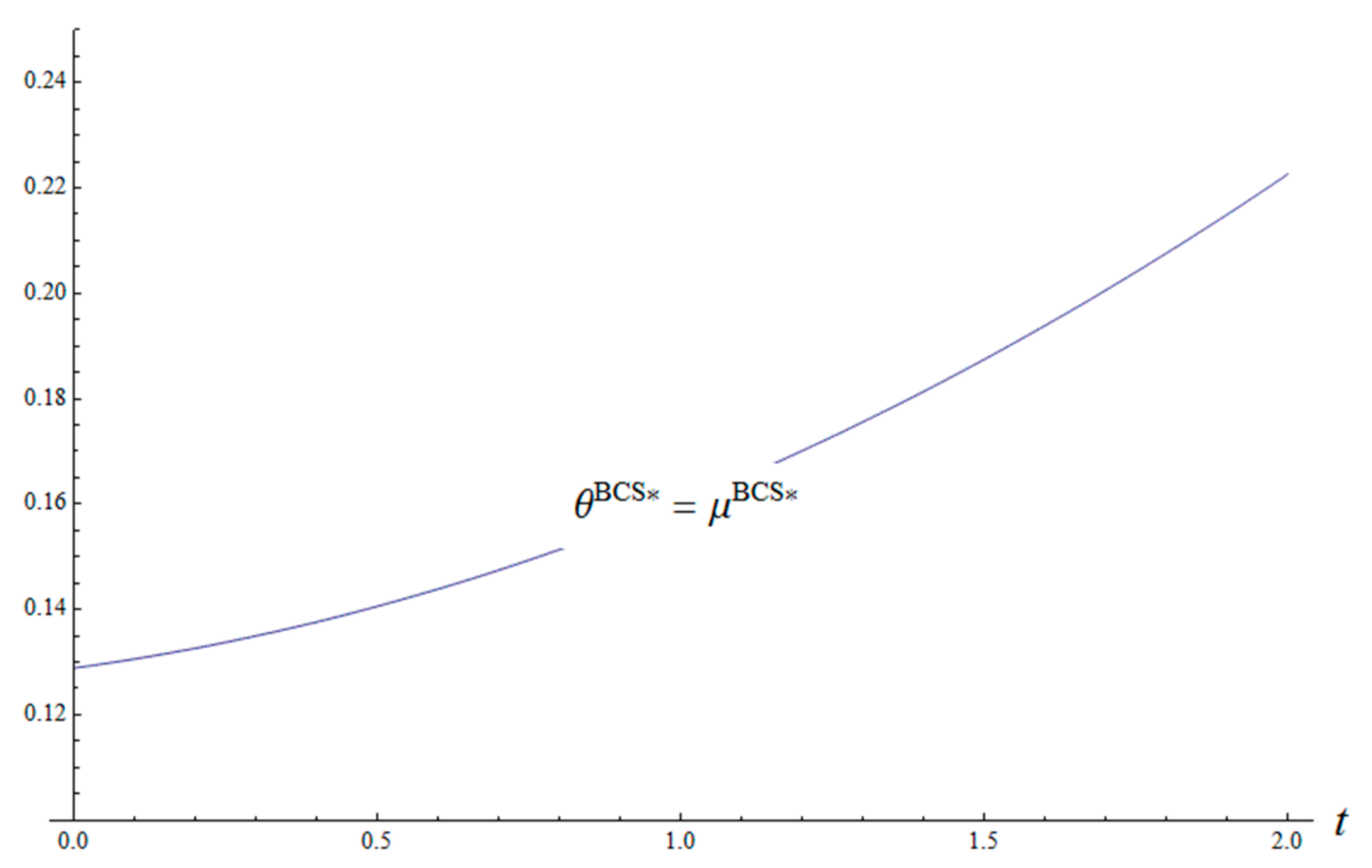

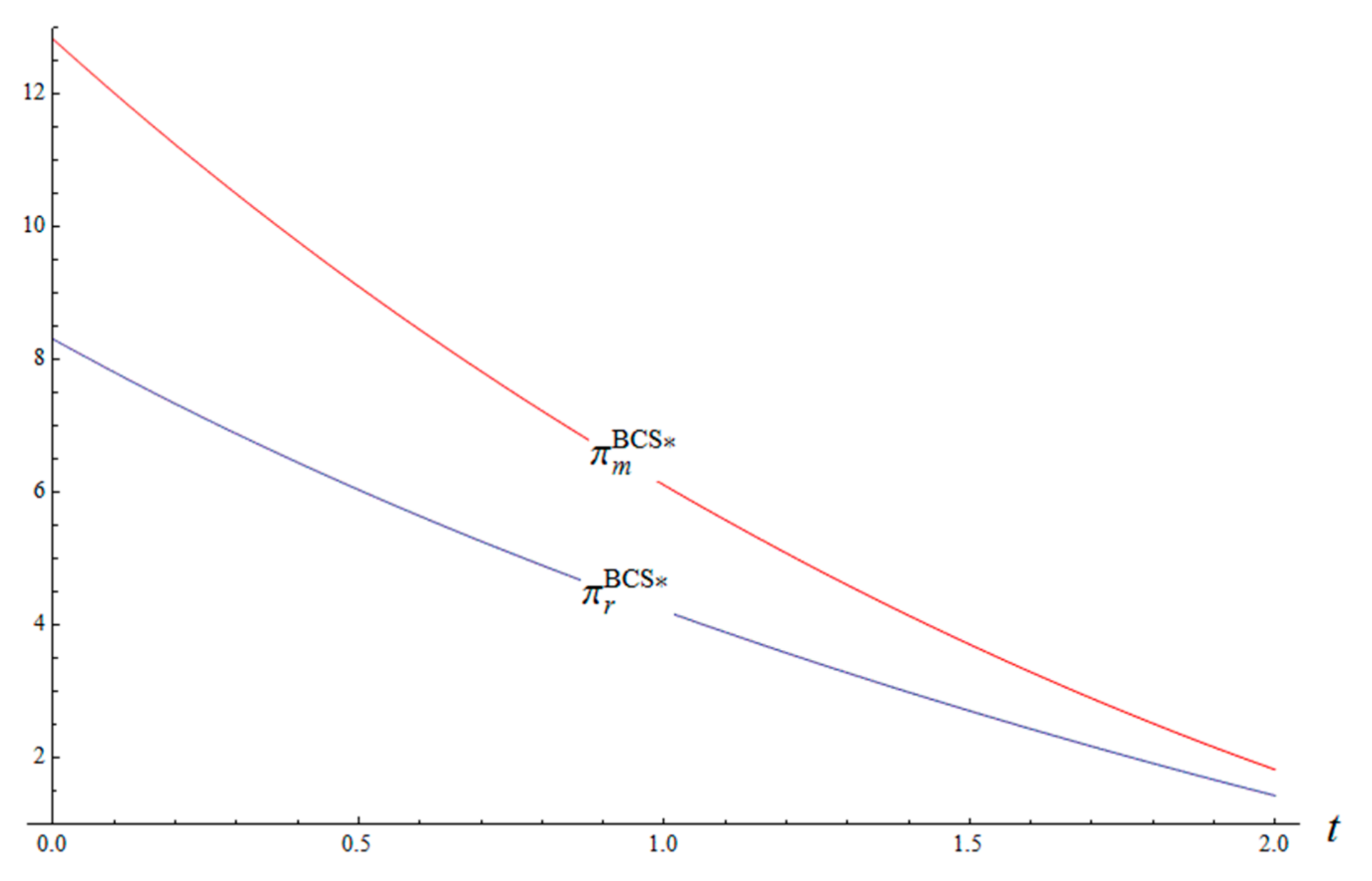

- The improvement of the carbon tax regime increases the cost-sharing proportion and reduces the profits of the retailer and the manufacturer. Under conditions in which the government levies a lower carbon tax, a carbon tax policy is able to promote energy savings and emissions reduction among enterprises with low initial pollution levels; however, for enterprises generating high initial pollution levels, such a policy curbs energy savings and emissions reductions. If the government imposes too high a carbon tax, the policy always exerts adverse effects, on any type of enterprise. Therefore, government probably cannot obtain the expected result, but instead gets just the opposite, if it blindly levies too high a carbon tax. The government should impose a carbon tax in a discriminative fashion for different types of enterprises: for enterprises with heavy initial pollution loads, the government should not enact too strict a carbon tax policy, but is advised to use a conciliatory policy and increase the energy-saving subsidy thereto. In this way, the manufacturer can have enough funds to carry out technology innovation to reduce carbon emissions and build a benign environmental corporate image. While due to the low emission reduction cost, the manufacturer with a lower initial pollution load is motivated to reduce emissions under the pressure imposed by government increases in carbon tax. Under these conditions, the government is suggested to impose a carbon tax and provide energy-saving subsidies at the same time, to more effectively guide the manufacturer to reducing carbon emissions.

- (6)

- The carbon-emissions level, energy-saving level, and total profit of the supply chain under a centralised decision-making framework have increasingly greater differences from those under a BCS contract with an increasing subsidy coefficient. A subsidy policy decreases the coordination efficiency along the supply chain; therefore, while increasing subsidies, government needs to advocate for more coordination of the supply chain, so that upstream and downstream enterprises therein can systematically carry out energy saving and emission reductions.

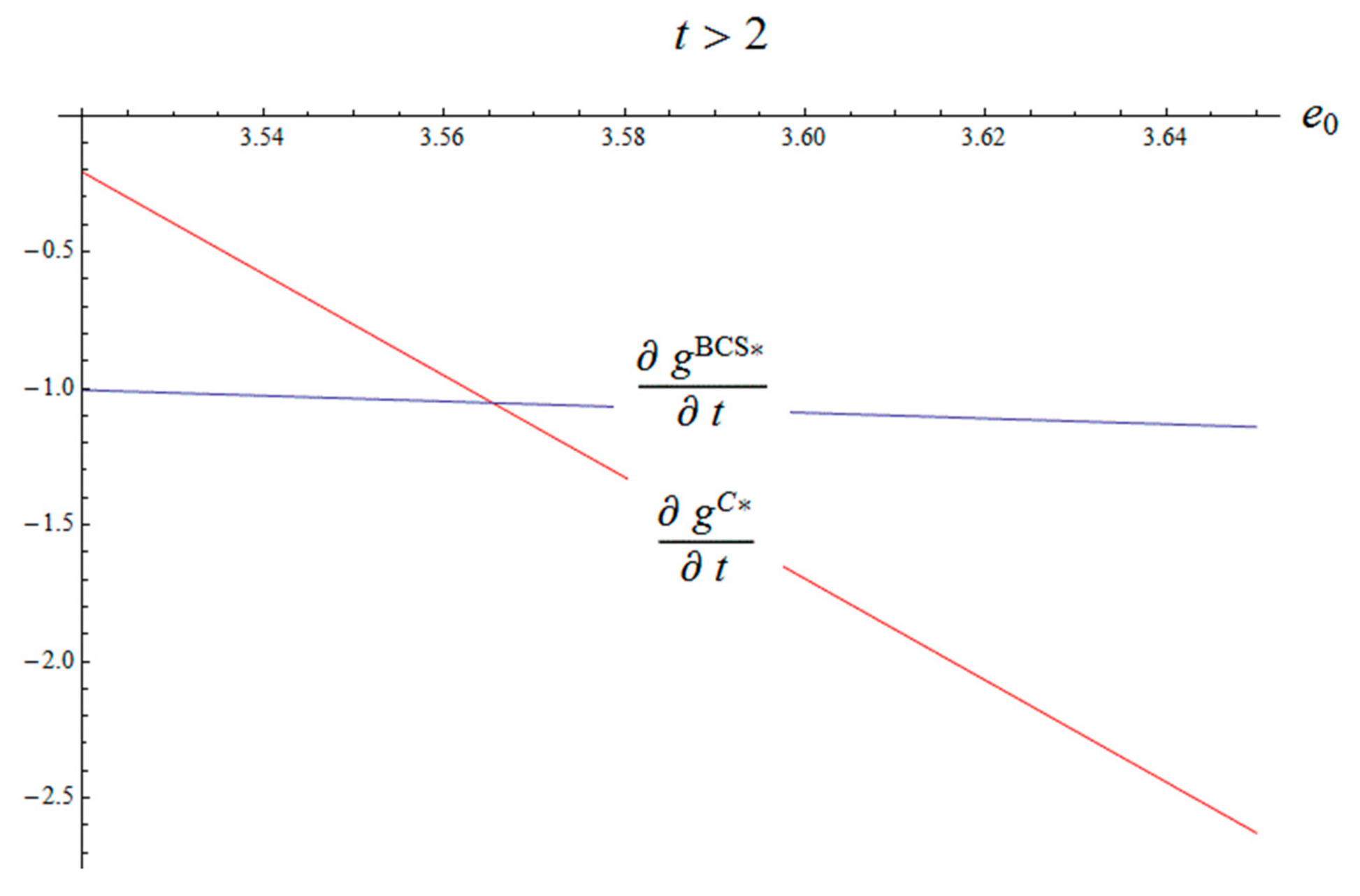

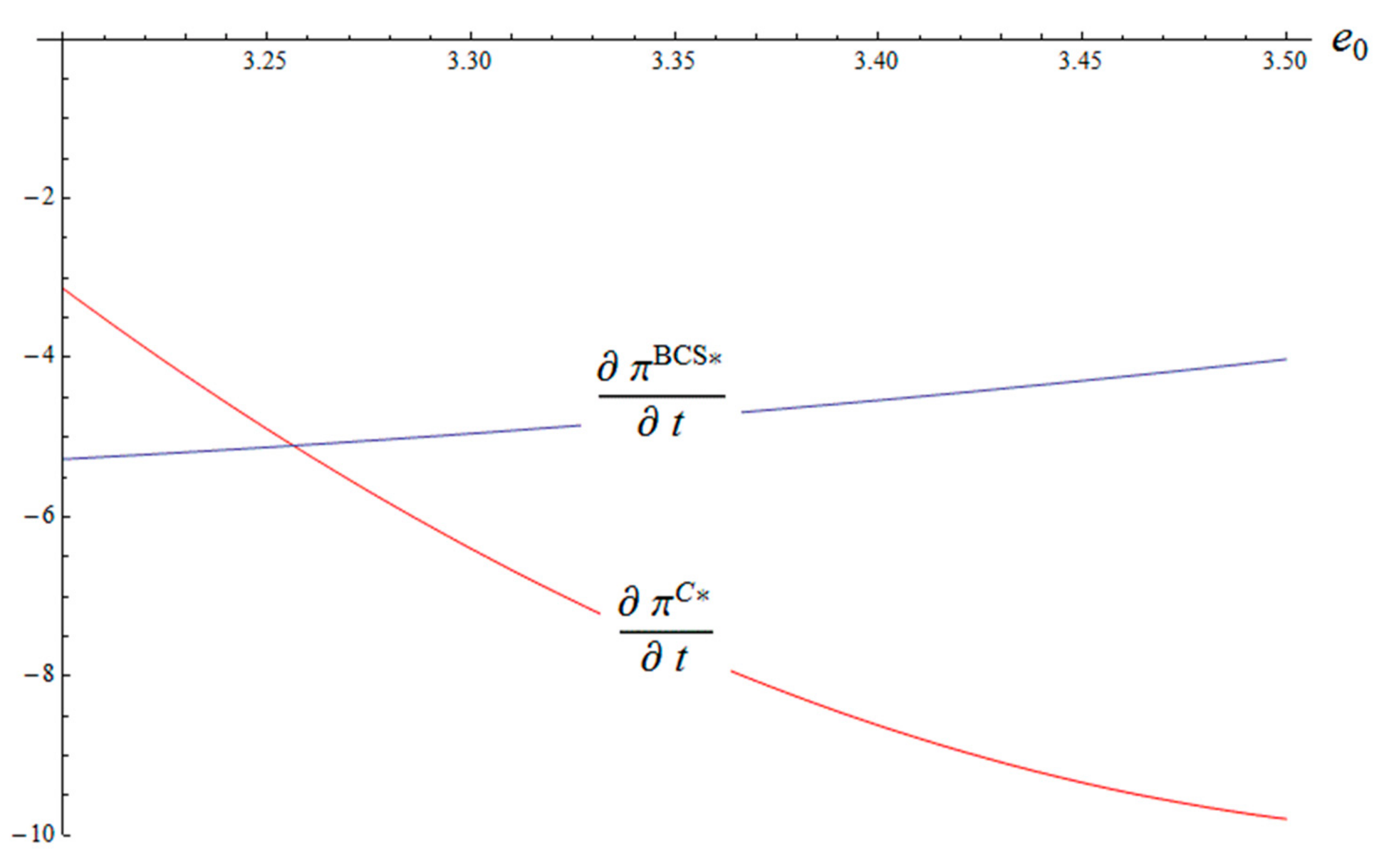

- (7)

- For enterprises with low initial pollution levels, the carbon-emissions level, energy-saving level, and total profit of the supply chain under a centralised decision-making framework show growing differences with those under the BCS contract with an increasing carbon tax. This indicates that the increasing carbon tax decreases coordination efficiency in the supply chain. However, for enterprises with a high initial pollution load, these differences, under a centralised decision-making framework and a BCS contract decrease with an increasing carbon tax. This implies that an increasing carbon tax increases the coordination efficiency of the supply chain; therefore, for those manufacturers initially generating less pollution, government needs to support close cooperation between upstream and downstream enterprises and encourage production when it increases its carbon tax. As for manufacturers generating heavy initial pollution loads, the government is advised to reduce their total carbon emissions by limiting the productivity of the supply chain, rather than encouraging joint decisions between upstream and downstream enterprises. This is because, even given cooperation between upstream and downstream enterprises in the supply chain, this fails to obtain satisfactory emissions reduction effects.

Acknowledgments

Author Contributions

Conflicts of Interest

Appendix A

Appendix A.1. Proof of Theorem 1

Appendix A.2. Proof of Theorem 2

Appendix A.3. Proof of Theorem 5

Appendix A.4. Proof of Proposition 1

Appendix A.5. Proof of Proposition 2

Appendix A.6. Proof of Proposition 3

Appendix A.7. Proof of Proposition 4

Appendix A.8. Proof of Proposition 5

Appendix A.9. Proof of Proposition 6

Appendix A.10. Proof of Proposition 7

Appendix A.11. Proof of Proposition 8

Appendix A.12. Proof of Proposition 9

Appendix A.13. Proof of Proposition 10

References

- Friedler, F. Process integration, modelling and optimisation for energy saving and pollution reduction. Appl. Therm. Eng. 2010, 30, 2270–2280. [Google Scholar] [CrossRef]

- Varbanov, P.S.; Manenti, F.; Klemeš, J.J.; Lund, H. Special section: Process integration, modelling and optimisation for energy saving and pollution reduction—PRES 2014. Energy 2015, 90, 1–4. [Google Scholar] [CrossRef]

- Zhou, W.H.; Huang, W.X. Contract designs for energy-saving product development in a monopoly. Eur. J. Oper. Res. 2016, 250, 902–913. [Google Scholar] [CrossRef]

- Shao, L.L.; Yang, J.; Zhang, M. Subsidy scheme or price discount scheme? Mass adoption of electric vehicles under different market structures. Eur. J. Oper. Res. 2017, 262, 1181–1195. [Google Scholar] [CrossRef]

- Li, X.; Li, Y.J. On green market segmentation under subsidy regulation. Supply Chain Manag. 2017, 22, 284–294. [Google Scholar] [CrossRef]

- Luo, Z.; Chen, X.; Wang, X.J. The role of co-opetition in low carbon manufacturing. Eur. J. Oper. Res. 2016, 253, 392–403. [Google Scholar] [CrossRef]

- Andersen, M.S. Europe’s experience with carbon-energy taxation. Inst. Veolia Environ. 2010, 3, 1–11. [Google Scholar]

- Houghton, J.T.; MeiraFilho, L.G.; Callender, B.A.; Harris, N.; Kattenberg, A.; Maskell, K. Climate Change 1995: The Science of Climate Change; Cambridge University Press: Cambridge, UK, 1996. [Google Scholar]

- Moon, W.; Florkowski, W.J.; Bruckner, B. Willingness to pay for environmental practices: Implications for eco-labeling. Land Econ. 2002, 78, 88–102. [Google Scholar] [CrossRef]

- Dai, J.; Cantor, D.E.; Montabon, F.L. Examining corporate environmental proactivity and operational performance: A strategy-structure-capabilities-performance perspective within a green context. Int. J. Prod. Econ. 2017, 193, 272–280. [Google Scholar] [CrossRef]

- Saberi, S.; Cruz, J.M.; Sarkis, J.; Nagurney, N. A competitive multiperiod supply chain network model with freight carriers and green technology investment option. Eur. J. Oper. Res. 2018, 266, 934–949. [Google Scholar] [CrossRef]

- Bhaskaran, S.R.; Krishnan, V. Effort, revenue, and cost sharing mechanisms for collaborative new product development. Manag. Sci. 2009, 55, 1152–1169. [Google Scholar] [CrossRef]

- Ghosh, D.; Shah, J. Supply chain analysis under green sensitive consumer demand and cost sharing contract. Int. J. Prod. Econ. 2015, 164, 319–329. [Google Scholar] [CrossRef]

- Xu, L.; Wang, C.X.; Li, H. Decision and coordination of low-carbon supply chain considering technological spillover and environmental awareness. Sci. Rep. 2017, 7, 3107. [Google Scholar] [CrossRef] [PubMed]

- Zhou, N.; Fridley, D.; Mcneil, M.; Zheng, N.N.; Letschert, V.; Ke, J. Analysis of potential energy saving and CO2 emission reduction of home appliances and commercial equipments in China. Energy Policy 2011, 39, 4541–4550. [Google Scholar] [CrossRef]

- Xie, G. Modelling decision processes of a green supply chain with regulation on energy saving level. Comput. Oper. Res. 2015, 54, 266–273. [Google Scholar] [CrossRef]

- Xie, G. Cooperative strategies for sustainability in a decentralized supply chain with competing suppliers. J. Clean. Prod. 2016, 113, 807–821. [Google Scholar] [CrossRef]

- Hafezalkotob, A. Competition, cooperation, and coopetition of green supply chains under regulations on energy saving levels. Transp. Res. Part E Logist. Transp. Rev. 2017, 97, 228–250. [Google Scholar] [CrossRef]

- Zhang, H.M.; Li, L.S.; Zhou, P.; Hou, J.M.; Qiu, Y.M. Subsidy modes, waste cooking oil and biofuel: Policy effectiveness and sustainable supply chains in China. Energy Policy 2014, 65, 270–274. [Google Scholar] [CrossRef]

- He, L.F.; Zhao, D.Z.; Xia, L.J. Game theoretic analysis of carbon emission abatement in fashion supply chains considering vertical incentives and channelstructures. Sustainability 2015, 7, 4280–4309. [Google Scholar] [CrossRef]

- Du, S.F.; Hu, L.; Wang, L. Low-carbon supply policies and supply chain performance with carbon concerned demand. Ann. Oper. Res. 2017, 255, 569–590. [Google Scholar] [CrossRef]

- Choi, T.M. Carbon footprint tax on fashion supply chain systems. Int. J. Adv. Manuf. Technol. 2013, 68, 835–847. [Google Scholar] [CrossRef]

- Liu, B.; Li, T.; Tsai, S.B. Low carbon strategy analysis of competing supply chains with different power structures. Sustainability 2017, 9, 835. [Google Scholar]

- Xiao, Y.J.; Yang, S.; Zhang, L.M.; Kuo, Y.H. Supply chain cooperation with price-sensitive demand and environmental impacts. Sustainability 2016, 8, 716. [Google Scholar] [CrossRef]

- Yang, H.X.; Luo, J.W.; Wang, H.J. The role of revenue sharing and first-mover advantage in emission abatement with carbon tax and consumer environmental awareness. Int. J. Prod. Econ. 2017, 193, 691–702. [Google Scholar] [CrossRef]

- Yenipazarli, A. Managing new and remanufactured products to mitigate environmental damage under emissions regulation. Eur. J. Oper. Res. 2016, 249, 117–130. [Google Scholar] [CrossRef]

- Du, S.F.; Zhu, J.A.; Jiao, H.F.; Ye, W.Y. Game-theoretical analysis for supply chain with consumer preference to low carbon. Int. J. Prod. Res. 2015, 53, 3753–3768. [Google Scholar] [CrossRef]

- Zhang, L.H.; Wang, J.G.; You, J.X. Consumer environmental awareness and channel coordination with two substitutable products. Eur. J. Oper. Res. 2015, 241, 63–73. [Google Scholar] [CrossRef]

- Xu, J.T.; Chen, Y.Y.; Bai, Q.G. A two-echelon sustainable supply chain coordination under cap-and-trade regulation. J. Clean. Prod. 2016, 135, 42–56. [Google Scholar] [CrossRef]

- Yang, L.; Zhang, Q.; Ji, J.N. Pricing and carbon emission reduction decisions in supply chains with vertical and horizontal cooperation. Int. J. Prod. Econ. 2017, 191, 286–297. [Google Scholar] [CrossRef]

- Wang, Q.P.; Zhao, D.Z.; He, L.F. Contracting emission reduction for supply chains considering market low-carbon preference. J. Clean. Prod. 2016, 120, 72–84. [Google Scholar] [CrossRef]

- Zhou, Y.J.; Bao, M.J.; Chen, X.H.; Xu, X.H. Co-op advertising and emission reduction cost sharing contracts and coordination in low-carbon supply chain based on fairness concerns. J. Clean. Prod. 2016, 133, 402–413. [Google Scholar] [CrossRef]

- Yu, W.; Han, R.Z. Coordinating a two-echelon supply chain under carbon tax. Sustainability 2017, 9, 2360. [Google Scholar] [CrossRef]

- Yang, H.X.; Chen, W.B. Retailer-driven carbon emission abatement with consumer environmental awareness and carbon tax: Revenue-sharing versus cost-sharing. Omega 2017. [Google Scholar] [CrossRef]

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yi, Y.; Li, J. Cost-Sharing Contracts for Energy Saving and Emissions Reduction of a Supply Chain under the Conditions of Government Subsidies and a Carbon Tax. Sustainability 2018, 10, 895. https://doi.org/10.3390/su10030895

Yi Y, Li J. Cost-Sharing Contracts for Energy Saving and Emissions Reduction of a Supply Chain under the Conditions of Government Subsidies and a Carbon Tax. Sustainability. 2018; 10(3):895. https://doi.org/10.3390/su10030895

Chicago/Turabian StyleYi, Yuyin, and Jinxi Li. 2018. "Cost-Sharing Contracts for Energy Saving and Emissions Reduction of a Supply Chain under the Conditions of Government Subsidies and a Carbon Tax" Sustainability 10, no. 3: 895. https://doi.org/10.3390/su10030895

APA StyleYi, Y., & Li, J. (2018). Cost-Sharing Contracts for Energy Saving and Emissions Reduction of a Supply Chain under the Conditions of Government Subsidies and a Carbon Tax. Sustainability, 10(3), 895. https://doi.org/10.3390/su10030895