Sustainable Venture Capital Investments: An Enabler Investigation

, , ,

, , ,

Abstract

:1. Introduction

2. Background and Enablers

2.1. Background of Sustainable Venture Capital Investments

2.2. Enablers for Sustainable Venture Capital Investments

2.2.1. Internal Enablers

- The VC firm is willing to provide necessary human resources support. The venture capital investments usually imply lengthy monitoring and support for the start-ups in the portfolio [71,72]. When the venture capital firm decides to invest in a sustainable start-up, it must be ready to provide the necessary qualified human resources and favor the environmental and social outcome as opposed to a possible higher profit from a non-sustainable investment option [73]. The size of the firm can influence the adoption of proactive environmental practices and small venture capital firms may not always be capable of providing the necessary human resources support for sustainable start-ups [74,75].

- Venture capitalists deeply understand the sustainable business models. Robust understanding of sustainable business models is crucial for investing in sustainable start-ups [76]. The business models of sustainable start-ups may require investing substantial amounts of money for more extended periods, focusing on mixed projects of information technology, energy or medicine, with a high risk of failure [75]. The better venture capitalists understand these characteristics, the more chance they have to choose a sustainable start-up with great potential [9,77,78].

- Venture capitalists are morally committed to sustainability. Venture capitalists committed to sustainability usually believe that they are accountable for the well-being of the future generations, and that sustainability is good for business [9]. They are more likely to invest in sustainable projects and support the implementation of sustainable business models [80,81,82].

- VC investments in sustainable start-ups can create new demand. Most of the start-ups are creating new products and new markets for their products [90]. Given that sustainable development and environmental protection require many innovative and unconventional solutions and cutting-edge technologies, new markets for these products and solutions are also emerging [9,89,90]. The venture capitalists that adopt the long-term strategy prefer to include in their investment portfolios sustainable start-ups [102,103].

2.2.2. External Enablers

- SMEs and venture capital firms’ credible collaborations and networking. The networks are elemental because the entrepreneurs want to communicate with other more experienced entrepreneurs, want to receive the feedback from experts, and seek the help from venture capitalists regarding the best market and investor exit strategies [9,78,91]. Many venture capitalists who are networking with sustainable entrepreneurs, decide to invest in sustainable products and services [104,105,106].

- Government policies, regulations, and programs for sustainable investments. Empirical results from the U.S. and Europe suggest that many government policies are highly regarded by the venture capitalists, especially in the renewable energy business [9,11]. Most of the venture capital firms need a mix of consistent government policies to invest in sustainable projects [79,92,93,94].

- Government use of international standards for sustainable investments. To reduce the risks of the intellectual propriety breach of the innovative sustainable start-ups, and to increase the transparency in the sustainable venture capital investing, governments ought to use international standards [38,95,96].

2.3. Gap Analysis and Research Highlights

- Identify and propose enablers for SVC investments from the scientific literature review and interviews with experienced professionals.

- Put forward a framework to analyze enablers for SVC investments in Saudi Arabia using the grey-based DEMATEL.

- Identify and explain, with the insight of four venture capital experts, the crucial enablers for SVC investments in Saudi Arabia.

- Validate these enablers for SVC investments through feedback from practitioners. Compare the acquired results to the current SVC research.

3. Methodology

3.1. Data Acquisition

3.2. Grey-Based Decision-Making Trial and Evaluation Laboratory Approach

4. Results and Discussion

4.1. Results

4.2. Discussion of Results

5. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| E1 | E2 | E3 | E4 | E5 | E6 | E7 | E8 | E9 | E10 | |

|---|---|---|---|---|---|---|---|---|---|---|

| E1 | 0 | 3 | 3 | 3 | 3 | 2 | 2 | 3 | 2 | 2 |

| E2 | 4 | 0 | 4 | 4 | 4 | 3 | 3 | 4 | 2 | 2 |

| E3 | 4 | 4 | 0 | 4 | 3 | 3 | 3 | 4 | 2 | 2 |

| E4 | 3 | 4 | 3 | 0 | 3 | 3 | 3 | 4 | 2 | 2 |

| E5 | 2 | 3 | 3 | 3 | 0 | 2 | 4 | 3 | 2 | 2 |

| E6 | 2 | 2 | 2 | 2 | 2 | 0 | 2 | 2 | 2 | 2 |

| E7 | 3 | 3 | 3 | 3 | 4 | 2 | 0 | 4 | 2 | 2 |

| E8 | 3 | 4 | 3 | 3 | 3 | 2 | 4 | 0 | 2 | 2 |

| E9 | 3 | 3 | 4 | 2 | 3 | 3 | 4 | 4 | 0 | 3 |

| E10 | 3 | 3 | 4 | 2 | 3 | 3 | 4 | 3 | 4 | 0 |

| E1 | E2 | E3 | E4 | E5 | E6 | E7 | E8 | E9 | E10 | |

|---|---|---|---|---|---|---|---|---|---|---|

| E1 | 0 | 3 | 3 | 3 | 3 | 2 | 3 | 3 | 2 | 2 |

| E2 | 4 | 0 | 4 | 4 | 4 | 2 | 3 | 4 | 2 | 2 |

| E3 | 4 | 4 | 0 | 4 | 4 | 3 | 4 | 4 | 2 | 2 |

| E4 | 3 | 3 | 3 | 0 | 4 | 2 | 3 | 4 | 2 | 2 |

| E5 | 3 | 3 | 3 | 3 | 0 | 2 | 3 | 3 | 2 | 2 |

| E6 | 2 | 3 | 2 | 2 | 2 | 0 | 2 | 2 | 2 | 2 |

| E7 | 3 | 3 | 3 | 3 | 3 | 2 | 0 | 4 | 2 | 2 |

| E8 | 3 | 3 | 3 | 3 | 3 | 2 | 3 | 0 | 3 | 3 |

| E9 | 3 | 3 | 4 | 2 | 4 | 4 | 3 | 3 | 0 | 2 |

| E10 | 2 | 3 | 4 | 2 | 4 | 3 | 3 | 3 | 3 | 0 |

| E1 | E2 | E3 | E4 | E5 | E6 | E7 | E8 | E9 | E10 | |

|---|---|---|---|---|---|---|---|---|---|---|

| E1 | 0 | 3 | 3 | 2 | 3 | 2 | 3 | 4 | 2 | 1 |

| E2 | 3 | 0 | 3 | 4 | 4 | 2 | 4 | 4 | 2 | 1 |

| E3 | 4 | 3 | 0 | 3 | 4 | 1 | 4 | 4 | 2 | 1 |

| E4 | 2 | 4 | 4 | 0 | 4 | 2 | 4 | 4 | 2 | 1 |

| E5 | 3 | 3 | 2 | 2 | 0 | 2 | 4 | 3 | 2 | 1 |

| E6 | 1 | 1 | 2 | 1 | 1 | 0 | 1 | 1 | 2 | 1 |

| E7 | 3 | 3 | 3 | 2 | 2 | 2 | 0 | 3 | 2 | 1 |

| E8 | 3 | 3 | 3 | 3 | 4 | 2 | 3 | 0 | 2 | 1 |

| E9 | 4 | 3 | 4 | 2 | 4 | 4 | 4 | 4 | 0 | 3 |

| E10 | 3 | 3 | 3 | 2 | 3 | 3 | 3 | 4 | 3 | 0 |

| E1 | E2 | E3 | E4 | E5 | E6 | E7 | E8 | E9 | E10 | |

|---|---|---|---|---|---|---|---|---|---|---|

| E1 | 0 | 3 | 3 | 3 | 3 | 2 | 3 | 3 | 2 | 2 |

| E2 | 4 | 0 | 3 | 4 | 3 | 2 | 3 | 4 | 2 | 2 |

| E3 | 3 | 3 | 0 | 3 | 3 | 2 | 3 | 3 | 2 | 2 |

| E4 | 3 | 3 | 2 | 0 | 4 | 1 | 3 | 4 | 2 | 2 |

| E5 | 3 | 2 | 3 | 2 | 0 | 2 | 3 | 3 | 2 | 2 |

| E6 | 2 | 3 | 2 | 2 | 2 | 0 | 2 | 2 | 1 | 1 |

| E7 | 3 | 3 | 3 | 1 | 3 | 2 | 0 | 4 | 2 | 2 |

| E8 | 3 | 4 | 3 | 3 | 4 | 2 | 3 | 0 | 3 | 3 |

| E9 | 2 | 3 | 4 | 2 | 3 | 3 | 4 | 3 | 0 | 2 |

| E10 | 2 | 3 | 4 | 2 | 3 | 3 | 4 | 3 | 3 | 0 |

| E1 | E2 | E3 | E4 | E5 | E6 | E7 | E8 | E9 | E10 | |

|---|---|---|---|---|---|---|---|---|---|---|

| E1 | 0.0000 | 3.0000 | 3.0000 | 2.7500 | 3.0000 | 2.0000 | 2.7500 | 3.2500 | 2.0000 | 1.7500 |

| E2 | 3.7500 | 0.0000 | 3.5000 | 4.0000 | 3.7500 | 2.2500 | 3.2500 | 4.0000 | 2.0000 | 1.7500 |

| E3 | 3.7500 | 3.5000 | 0.0000 | 3.5000 | 3.5000 | 2.2500 | 3.5000 | 3.7500 | 2.0000 | 1.7500 |

| E4 | 2.7500 | 3.5000 | 3.0000 | 0.0000 | 3.7500 | 2.0000 | 3.2500 | 4.0000 | 2.0000 | 1.7500 |

| E5 | 2.7500 | 2.7500 | 2.7500 | 2.5000 | 0.0000 | 2.0000 | 3.5000 | 3.0000 | 2.0000 | 1.7500 |

| E6 | 1.7500 | 2.2500 | 2.0000 | 1.7500 | 1.7500 | 0.0000 | 1.7500 | 1.7500 | 1.7500 | 1.5000 |

| E7 | 3.0000 | 3.0000 | 3.0000 | 2.2500 | 3.0000 | 2.0000 | 0.0000 | 3.7500 | 2.0000 | 1.7500 |

| E8 | 3.0000 | 3.5000 | 3.0000 | 3.0000 | 3.5000 | 2.0000 | 3.2500 | 0.0000 | 2.5000 | 2.2500 |

| E9 | 3.0000 | 3.0000 | 4.0000 | 2.0000 | 3.5000 | 3.5000 | 3.7500 | 3.5000 | 0.0000 | 2.5000 |

| E10 | 2.5000 | 3.0000 | 3.7500 | 2.0000 | 3.2500 | 3.0000 | 3.5000 | 3.2500 | 3.2500 | 0.0000 |

| E1 | E2 | E3 | E4 | E5 | E6 | E7 | E8 | E9 | E10 | |

|---|---|---|---|---|---|---|---|---|---|---|

| E1 | 0.0000 | 0.1043 | 0.1043 | 0.0957 | 0.1043 | 0.0696 | 0.0957 | 0.1130 | 0.0696 | 0.0609 |

| E2 | 0.1304 | 0.0000 | 0.1217 | 0.1391 | 0.1304 | 0.0783 | 0.1130 | 0.1391 | 0.0696 | 0.0609 |

| E3 | 0.1304 | 0.1217 | 0.0000 | 0.1217 | 0.1217 | 0.0783 | 0.1217 | 0.1304 | 0.0696 | 0.0609 |

| E4 | 0.0957 | 0.1217 | 0.1043 | 0.0000 | 0.1304 | 0.0696 | 0.1130 | 0.1391 | 0.0696 | 0.0609 |

| E5 | 0.0957 | 0.0957 | 0.0957 | 0.0870 | 0.0000 | 0.0696 | 0.1217 | 0.1043 | 0.0696 | 0.0609 |

| E6 | 0.0609 | 0.0783 | 0.0696 | 0.0609 | 0.0609 | 0.0000 | 0.0609 | 0.0609 | 0.0609 | 0.0522 |

| E7 | 0.1043 | 0.1043 | 0.1043 | 0.0783 | 0.1043 | 0.0696 | 0.0000 | 0.1304 | 0.0696 | 0.0609 |

| E8 | 0.1043 | 0.1217 | 0.1043 | 0.1043 | 0.1217 | 0.0696 | 0.1130 | 0.0000 | 0.0870 | 0.0783 |

| E9 | 0.1043 | 0.1043 | 0.1391 | 0.0696 | 0.1217 | 0.1217 | 0.1304 | 0.1217 | 0.0000 | 0.0870 |

| E10 | 0.0870 | 0.1043 | 0.1304 | 0.0696 | 0.1130 | 0.1043 | 0.1217 | 0.1130 | 0.1130 | 0.0000 |

References

- Dergiades, T.; Kaufmann, R.K.; Panagiotidis, T. Long-run changes in radiative forcing and surface temperature: The effect of human activity over the last five centuries. J. Environ. Econ. Manag. 2016, 76, 67–85. [Google Scholar] [CrossRef]

- Gordon, K.; Pohl, J. Environmental concerns in international investment agreements: A survey. SSRN 2011. [Google Scholar] [CrossRef]

- Beyer, A.; Cohen, D.A.; Lys, T.Z.; Walther, B.R. The financial reporting environment: Review of the recent literature. J. Account. Econ. 2010, 50, 296–343. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate social and financial performance: A meta-analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Griffin, J.J.; Mahon, J.F. The corporate social performance and corporate financial performance debate: Twenty-five years of incomparable research. Bus. Soc. 1997, 36, 5–31. [Google Scholar] [CrossRef]

- Singer, P.L.; Bonvillian, W.B. “Innovation Orchards”: Helping Tech Start-Ups Scale; Information Technology & Innovation Foundation: Washington, DC, USA, 2017. [Google Scholar]

- United Nations Development Programme. Impact Investment. Available online: http://www.undp.org/content/sdfinance/en/home/solutions/impact-investment.html (accessed on 25 January 2018).

- Bürer, M.J.; Wüstenhagen, R. Cleantech venture investors and energy policy risk: An exploratory analysis of regulatory risk management strategies. Sustain. Innov. Entrep. 2008, 290–309. [Google Scholar] [CrossRef]

- Bocken, N.M.P. Sustainable venture capital—Catalyst for sustainable start-up success? J. Clean. Prod. 2015, 108, 647–658. [Google Scholar] [CrossRef]

- Stack, J.B.J.; Epstein, B.; Hanggi, T. Cleantech Venture Capital: How Public Policy Has Stimulated Private Investment; Cleantech Venture Network LLC.: Ann Arbor, MI, USA, 2007; p. E2. [Google Scholar]

- Wustenhagen, R.; Teppo, T. Do venture capitalists really invest in good industries? Risk-return perceptions and path dependence in the emerging European energy VC market. Int. J. Technol. Manag. 2006, 34, 63–87. [Google Scholar] [CrossRef]

- O’Rourke, A. The message and methods of ethical investment. J. Clean. Prod. 2003, 11, 683–693. [Google Scholar] [CrossRef]

- Berry, T.C.; Junkus, J.C. Socially responsible investing: An investor perspective. J. Bus. Ethics 2013, 112, 707–720. [Google Scholar] [CrossRef]

- Entine, J. The myth of social investing: A critique of its practice and consequences for corporate social performance research. Organ. Environ. 2003, 16, 352–368. [Google Scholar] [CrossRef]

- Nilsson, J. Investment with a conscience: Examining the impact of pro-social attitudes and perceived financial performance on socially responsible investment behavior. J. Bus. Ethics 2008, 83, 307–325. [Google Scholar] [CrossRef]

- Sparkes, R.; Cowton, C.J. The maturing of socially responsible investment: A review of the developing link with corporate social responsibility. J. Bus. Ethics 2004, 52, 45–57. [Google Scholar] [CrossRef]

- Bugg-Levine, A.; Emerson, J. Impact investing: Transforming how we make money while making a difference. Innovations 2011, 6, 9–18. [Google Scholar] [CrossRef]

- Jackson, E.T. Evaluating social impact bonds: Questions, challenges, innovations, and possibilities in measuring outcomes in impact investing. Community Dev. 2013, 44, 608–616. [Google Scholar] [CrossRef]

- Web of Science Core Collection. Sustainable Venture Capital Research by Regions/Countries; Web of Science Core Collection: London, UK, 2018. [Google Scholar]

- MENA Private Equity Association. Eleventh Private Equity and Venture Capital Annual Report 2016; MENA Private Equity Association: Dubai, United Arab Emirates, 2017; p. 70. [Google Scholar]

- CBINSIGTHS. Blooming Desert: The Top United Arab Emirates-Based VCS and Their Tech Investments. Available online: https://www.cbinsights.com/research/uae-tech-startup-venture-capital-investment/ (accessed on 12 April 2018).

- DubaiBeat. Middle East Investors Directory. Available online: https://www.dubaibeat.com/middle_east_investors_directory_details.php (accessed on 12 April 2018).

- OECD. Venture Capital Development in Mena Countries–Taking Advantage of the Current Opportunity. In Mena Investment Policy Brief; OECD: Paris, France, 2006. [Google Scholar]

- Ramady, M.A. Aramco’s new 2030 vision and mission mandate: Managing expectations. In Saudi Aramco 2030; Springer: Berlin, Germany, 2018; pp. 61–91. [Google Scholar]

- Future Investment Initiative. The Public Investment Fund. Available online: http://futureinvestmentinitiative.com/en/pif (accessed on 12 April 2018).

- Public Investment Fund. Blackstone to Launch $40 Billion Infrastructure Investment Vehicle and New Infrastructure Business. Available online: http://www.pif.gov.sa/News/News14.html (accessed on 12 April 2018).

- Public Investment Fund. Portfolio. Available online: http://pif.gov.sa/Portfolio.html (accessed on 12 April 2018).

- Thukral, I.S.; Von Ehr, J.; Walsh, S.; Groen, A.J.; Van Der Sijde, P.; Akmaliah Adham, K. Entrepreneurship, emerging technologies, emerging markets. Int. Small Bus. J. 2008, 26, 101–116. [Google Scholar] [CrossRef]

- Looney, R.E. Handbook of Emerging Economies; Routledge: Abingdon, UK, 2014. [Google Scholar]

- Tracey, P.; Phillips, N. Entrepreneurship in emerging markets. Manag. Int. Rev. 2011, 51, 23–39. [Google Scholar] [CrossRef]

- Anderson, A.; Ronteau, S. Towards an entrepreneurial theory of practice; emerging ideas for emerging economies. J. Entrep. Emerg. Econ. 2017, 9, 110–120. [Google Scholar] [CrossRef]

- London, T.; Hart, S.L. Reinventing strategies for emerging markets: Beyond the transnational model. J. Int. Bus. Stud. 2004, 35, 350–370. [Google Scholar] [CrossRef]

- Gu, W.; Qian, X.; Lu, J. Venture capital and entrepreneurship: A conceptual model and research suggestions. Int. Entrep. Manag. J. 2018, 14, 35–50. [Google Scholar] [CrossRef]

- Aptheker, H. The quakers and negro slavery. J. Negro Hist. 1940, 25, 331–362. [Google Scholar] [CrossRef]

- Wesley, J. The use of money, a sermon on luke. In Sermons on Several Occasions; Christian Classics Ethereal Library: Grand Rapids, MI, USA, 1760; pp. 127–144. [Google Scholar]

- Kornbluh, F. Black buying power: Welfare rights, consumerism, and northern protest. In Freedom North: Black Freedom Struggles outside the South, 1940–1980; Springer: Berlin, Germany, 2003; pp. 199–222. [Google Scholar]

- Mizumura-Pence, R. Confronting trauma and toxins, rejecting closure: Three recent investigations of america’s war on vietnam. Am. Stud. 2014, 53, 7–20. [Google Scholar] [CrossRef]

- Richardson, B.J. Keeping ethical investment ethical: Regulatory issues for investing for sustainability. J. Bus. Ethics 2009, 87, 555–572. [Google Scholar] [CrossRef]

- Richardson, B.J. Socially Responsible Investment Law: Regulating the Unseen Polluters; Oxford University Press: Oxford, UK, 2008. [Google Scholar]

- Winston, A. Does Wall Street Finally Care about Sustainability? Available online: https://hbr.org/2018/01/does-wall-street-finally-care-about-sustainability#comment-section (accessed on 23 February 2018).

- The Economist. Sustainable Investment Joins the Mainstream. Available online: https://www.economist.com/news/finance-and-economics/21731640-millennials-are-coming-money-and-want-invest-it-responsibly-sustainable (accessed on 23 February 2018).

- US Forum for Sustainable and Responsible Investment. Report on Us Sustainable, Responsible and Impact Investing Trends. Available online: https://www.ussif.org/trends (accessed on 23 February 2018).

- Global Sustainable Investment Alliance. Global Sustainable Investment Review 2016; Global Sustainable Investment Alliance: Brussels, Belgium, 2017. [Google Scholar]

- Lemos Stain, M. More Shareholder Proposals Spotlight Climate Change. Available online: https://blogs.wsj.com/riskandcompliance/2018/02/08/more-shareholder-proposals-spotlight-climate-change/ (accessed on 24 February 2018).

- ISS Corporate Solutions. 2017 Governance Report Walkthrough. Available online: https://www.isscorporatesolutions.com/library/2017-governance-report-walkthrough-replay/ (accessed on 24 February 2018).

- Mrkajic, B.; Murtinu, S.; Scalera, V.G. Is green the new gold? Venture capital and green entrepreneurship. Small Bus. Econ. Group 2017, 1–22. [Google Scholar] [CrossRef]

- National Venture Capital Association. NVCA 2017 Yearbook: The Go-To Resource on the Venture Ecosystem; National Venture Capital Association: Washington, DC, USA, 2017. [Google Scholar]

- Hess, J.M. Smart Green VCS You Should Know. Available online: https://ecosummit.net/articles/smart-green-vcs-you-should-know (accessed on 23 February 2018).

- Lubber, M. We Need 2018 to Be the Year of Investor Leadership on Climate. Available online: https://www.forbes.com/sites/mindylubber/2018/02/06/we-need-2018-to-be-the-year-of-investor-leadership-on-climate/4/#2791a1035f65 (accessed on 24 February 2018).

- Cuff, M. Un Hails Fresh Push to Mobilise Global Green Investment. Available online: https://www.businessgreen.com/bg/news-analysis/3025795/un-hosts-fresh-push-for-green-investment (accessed on 24 February 2018).

- Frangoul, A. World Bank Group Will Stop Financing Upstream Oil and Gas after 2019. Available online: https://www.cnbc.com/2017/12/12/world-bank-group-will-stop-financing-upstream-oil-and-gas-from-2019.html (accessed on 24 February 2018).

- Winston, A. The Big Pivot: Radically Practical Strategies for a Hotter, Scarcer, and More Open World; Harvard Business Review Press: Boston, MA, USA, 2014. [Google Scholar]

- KAUST Innovation Fund. Explore High-Potential Partnerships with High-Tech Startups. Available online: https://innovation.kaust.edu.sa/entrepreneurs/browse-startups/ (accessed on 24 February 2018).

- Dou, Y.; Zhu, Q.; Sarkis, J. Green multi-tier supply chain management: An enabler investigation. J. Purchas. Supply Manag. 2017. [Google Scholar] [CrossRef]

- Zupic, I.; Čater, T. Bibliometric methods in management and organization. Organ. Res. Methods 2015, 18, 429–472. [Google Scholar] [CrossRef]

- Fahimnia, B.; Tang, C.S.; Davarzani, H.; Sarkis, J. Quantitative models for managing supply chain risks: A review. Eur. J. Oper. Res. 2015, 247, 1–15. [Google Scholar] [CrossRef]

- Archambault, É.; Campbell, D.; Gingras, Y.; Larivière, V. Comparing bibliometric statistics obtained from the web of science and scopus. J. Am. Soc. Inf. Sci. Technol. 2009, 60, 1320–1326. [Google Scholar] [CrossRef]

- Thomson Reuters. Social Sciences Citation Index. Available online: http://thomsonreuters.com/en/products-services/scholarly-scientific-research/scholarly-search-and-discovery/social-sciences-citation-index.html (accessed on 30 June 2016).

- Lockett, A.; Moon, J.; Visser, W. Corporate social responsibility in management research: Focus, nature, salience and sources of influence. J. Manag. Stud. 2006, 43, 115–136. [Google Scholar] [CrossRef]

- OpenHeatMap. Turn Your Spreadsheet into a Map. Available online: http://www.openheatmap.com/ (accessed on 3 April 2018).

- Knutas, A.; Hajikhani, A.; Salminen, J.; Ikonen, J.; Porras, J. Cloud-Based Bibliometric Analysis Service for Systematic Mapping Studies. In Proceedings of the 16th International Conference on Computer Systems and Technologies, Dublin, Ireland, 25–26 June 2015; ACM: New York, NY, USA, 2015; pp. 184–191. [Google Scholar]

- Kolle, S.R.; Shankarappa, T.; Manjunatha Reddy, T.; Muniyappa, A. Scholarly communication in the international journal of pest management: A bibliometric analysis from 2005 to 2014. J. Agric. Food Inf. 2015, 16, 301–314. [Google Scholar] [CrossRef]

- Juho Salminen, A.K.; Hajikhani, A. Hammer—Create New Analysis Job. Available online: http://hammer.nailsproject.net/ (accessed on 17 December 2017).

- Barney, J. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Ray, G.; Barney, J.B.; Muhanna, W.A. Capabilities, business processes, and competitive advantage: Choosing the dependent variable in empirical tests of the resource-based view. Strateg. Manag. J. 2004, 25, 23–37. [Google Scholar] [CrossRef]

- Hart, S.L. A natural-resource-based view of the firm. Acad. Manag. Rev. 1995, 20, 986–1014. [Google Scholar]

- Menguc, B.; Ozanne, L.K. Challenges of the “green imperative”: A natural resource-based approach to the environmental orientation–business performance relationship. J. Bus. Res. 2005, 58, 430–438. [Google Scholar] [CrossRef]

- Jensen, M.C. Value maximization, stakeholder theory, and the corporate objective function. J. Appl. Corp. Financ. 2010, 22, 32–42. [Google Scholar] [CrossRef]

- Gabrielsson, J.; Huse, M. The venture capitalist and the board of directors in smes: Roles and processes. Ventur. Cap. Int. J. Entrep. Financ. 2002, 4, 125–146. [Google Scholar] [CrossRef]

- Darnall, N.; Henriques, I.; Sadorsky, P. Adopting proactive environmental strategy: The influence of stakeholders and firm size. J. Manag. Stud. 2010, 47, 1072–1094. [Google Scholar] [CrossRef]

- Van Osnabrugge, M. A comparison of business angel and venture capitalist investment procedures: An agency theory-based analysis. Ventur. Cap. Int. J. Entrep. Financ. 2000, 2, 91–109. [Google Scholar] [CrossRef]

- Vanacker, T.; Collewaert, V.; Paeleman, I. The relationship between slack resources and the performance of entrepreneurial firms: The role of venture capital and angel investors. J. Manag. Stud. 2013, 50, 1070–1096. [Google Scholar] [CrossRef]

- Bjornali, E.S.; Ellingsen, A. Factors affecting the development of clean-tech start-ups: A literature review. Energy Procedia 2014, 58, 43–50. [Google Scholar] [CrossRef]

- Haber, S.; Reichel, A. The cumulative nature of the entrepreneurial process: The contribution of human capital, planning and environment resources to small venture performance. J. Bus. Ventur. 2007, 22, 119–145. [Google Scholar] [CrossRef]

- Marcus, A.; Malen, J.; Ellis, S. The promise and pitfalls of venture capital as an asset class for clean energy investment: Research questions for organization and natural environment scholars. Organ. Environ. 2013, 26, 31–60. [Google Scholar] [CrossRef]

- Seelos, C.; Mair, J. Social entrepreneurship: Creating new business models to serve the poor. Bus. Horiz. 2005, 48, 241–246. [Google Scholar] [CrossRef]

- Baum, J.A.C.; Silverman, B.S. Picking winners or building them? Alliance, intellectual, and human capital as selection criteria in venture financing and performance of biotechnology startups. J. Bus. Ventur. 2004, 19, 411–436. [Google Scholar] [CrossRef]

- De Carolis, D.M.; Litzky, B.E.; Eddleston, K.A. Why networks enhance the progress of new venture creation: The influence of social capital and cognition. Entrep. Theory Pract. 2009, 33, 527–545. [Google Scholar] [CrossRef]

- Burer, M.J.; Wustenhagen, R. Which renewable energy policy is a venture capitalist’s best friend? Empirical evidence from a survey of international cleantech investors. Energy Policy 2009, 37, 4997–5006. [Google Scholar] [CrossRef]

- Juravle, C.; Lewis, A. The role of championship in the mainstreaming of sustainable investment (SI) what can we learn from SI pioneers in the United Kingdom? Organ. Environ. 2009, 22, 75–98. [Google Scholar] [CrossRef]

- Kerr, J.E. Sustainability meets profitability: The convenient truth of how the business judgment rule protects a board’s decision to engage in social entrepreneurship. Cardozo L. Rev. 2007, 29, 623. [Google Scholar] [CrossRef]

- Abbott, F.M.; Reichman, F.H. The doha round’s public health legacy: Strategies for the production and diffusion of patented medicines under the amended trips provisions. J. Int. Econ. Law 2007, 10, 921–987. [Google Scholar] [CrossRef]

- Masini, A.; Menichetti, E. Investment decisions in the renewable energy sector: An analysis of non-financial drivers. Technol. Forecast. Soc. Chang. 2013, 80, 510–524. [Google Scholar] [CrossRef]

- Teece, D.J. Explicating dynamic capabilities: The nature and microfoundations of (sustainable) enterprise performance. Strateg. Manag. J. 2007, 28, 1319–1350. [Google Scholar] [CrossRef]

- Jansson, M.; Biel, A. Motives to engage in sustainable investment: A comparison between institutional and private investors. Sustain. Dev. 2011, 19, 135–142. [Google Scholar] [CrossRef]

- Székely, F.; Knirsch, M. Responsible leadership and corporate social responsibility:: Metrics for sustainable performance. Eur. Manag. J. 2005, 23, 628–647. [Google Scholar] [CrossRef]

- Mill, G.A. The financial performance of a socially responsible investment over time and a possible link with corporate social responsibility. J. Bus. Ethics 2006, 63, 131. [Google Scholar] [CrossRef]

- Lützkendorf, T.; Lorenz, D. Sustainable property investment: Valuing sustainable buildings through property performance assessment. Build. Res. Inf. 2005, 33, 212–234. [Google Scholar] [CrossRef]

- Daub, C.-H.; Ergenzinger, R. Enabling sustainable management through a new multi-disciplinary concept of customer satisfaction. Eur. J. Mark. 2005, 39, 998–1012. [Google Scholar] [CrossRef]

- Petrick, I.J.; Echols, A.E. Technology roadmapping in review: A tool for making sustainable new product development decisions. Technol. Forecast. Soc. Chang. 2004, 71, 81–100. [Google Scholar] [CrossRef]

- Chang, S.J. Venture capital financing, strategic alliances, and the initial public offerings of internet startups. J. Bus. Ventur. 2004, 19, 721–741. [Google Scholar] [CrossRef]

- Lerner, J. The government as venture capitalist: The long-run impact of the SBIR program. J. Bus. 1999, 72, 285–318. [Google Scholar] [CrossRef]

- Lerner, J. When bureaucrats meet entrepreneurs: The design of effective ‘public venture capital’ programmes. Econ. J. 2002, 112, F73–F84. [Google Scholar] [CrossRef]

- Lee, C.; Lee, K.; Pennings, J.M. Internal capabilities, external networks, and performance: A study on technology-based ventures. Strateg. Manag. J. 2001, 22, 615–640. [Google Scholar] [CrossRef]

- Brown, H.S.; de Jong, M.; Levy, D.L. Building institutions based on information disclosure: Lessons from GRI’S sustainability reporting. J. Clean. Prod. 2009, 17, 571–580. [Google Scholar] [CrossRef]

- Waelde, T.; Kolo, A. Environmental regulation, investment protection and ‘regulatory taking’in international law. Int. Comp. Law Q. 2001, 50, 811–848. [Google Scholar] [CrossRef]

- Dushnitsky, G.; Lenox, M.J. When do incumbents learn from entrepreneurial ventures? Corporate venture capital and investing firm innovation rates. Res. Policy 2005, 34, 615–639. [Google Scholar] [CrossRef]

- Dushnitsky, G.; Lenox, M.J. When do firms undertake R&D by investing in new ventures? Strateg. Manag. J. 2005, 26, 947–965. [Google Scholar]

- Chesbrough, H.; Crowther, A.K. Beyond high tech: Early adopters of open innovation in other industries. R&D Manag. 2006, 36, 229–236. [Google Scholar]

- Chesbrough, H.; Rosenbloom, R.S. The role of the business model in capturing value from innovation: Evidence from xerox corporation’s technology spin-off companies. Ind. Corp. Chang. 2002, 11, 529–555. [Google Scholar] [CrossRef]

- Chrun, E.; Dolsak, N.; Prakash, A. Corporate environmentalism: Motivations and mechanisms. In Annual Review of Environment and Resources; Gadgil, A., Gadgil, T.P., Eds.; Annual Reviews: Palo Alto, CA, USA, 2016; Volume 41, pp. 341–362. [Google Scholar]

- Nidumolu, R.; Prahalad, C.K.; Rangaswami, M.R. Why sustainability is now the key driver of innovation. Harv. Bus. Rev. 2009, 87, 56–64. [Google Scholar]

- Hockerts, K.; Wüstenhagen, R. Greening goliaths versus emerging davids—Theorizing about the role of incumbents and new entrants in sustainable entrepreneurship. J. Bus. Ventur. 2010, 25, 481–492. [Google Scholar] [CrossRef]

- Bhatt, P.; Altinay, L. How social capital is leveraged in social innovations under resource constraints? Manag. Decis. 2013, 51, 1772–1792. [Google Scholar] [CrossRef]

- Ghosh, S.; Nanda, R. Venture capital investment in the clean energy sector. SSRN 2010. [Google Scholar] [CrossRef]

- Petkova, A.P.; Wadhwa, A.; Yao, X.; Jain, S. Reputation and decision making under ambiguity: A study of us venture capital firms’ investments in the emerging clean energy sector. Acad. Manag. J. 2014, 57, 422–448. [Google Scholar] [CrossRef]

- International Monetary Fund. Growth and Stability in the Middle East and North Africa. Available online: https://www.imf.org/external/pubs/ft/mena/04econ.htm (accessed on 15 December 2017).

- World Bank. Global Economic Prospects—Middle East and North Africa. Available online: http://pubdocs.worldbank.org/en/154781493655499238/Global-Economic-Prospects-June-2017-Middle-East-and-North-Africa-analysis.pdf (accessed on 15 December 2017).

- Kingdom of Saudi Arabia Government. Saudi Vision 2030; Kingdom of Saudi Arabia: Riyadh, Saudi Arabia, 2016.

- Kingdom of Saudi Arabia Government. National Transformation Program 2020; Kingdom of Saudi Arabia: Riyadh, Saudi Arabia, 2016.

- Public Investment Fund. Public Investment Fund to Increase Assets under Management to over $400 Billion by 2020. Available online: http://pif.gov.sa/News/News22.html (accessed on 15 December 2017).

- World Bank, Doing Business. Measuring Business Regulations. Entrepreneurship. Available online: http://www.doingbusiness.org/data/exploretopics/entrepreneurship (accessed on 15 December 2017).

- The Global Entrepreneurship and Development Institute. Global Entrepreneurship Index 2018; The Global Entrepreneurship and Development Institute: London, UK, 2017. [Google Scholar]

- NOMADD Desert Solar Solutions. The Desert Solar Challenge. Available online: http://www.nomaddesertsolar.com/the-desert-solar-challenge.html (accessed on 15 December 2017).

- CURA. CURA Story—Why CURA Is Made? Available online: http://cura.healthcare/#demoLightbox (accessed on 15 December 2017).

- WAMDA. Saudi Web Startup Focuses on Rehab for Disabled Children. Available online: https://www.wamda.com/memakersge/2015/07/saudi-web-startup-focuses-rehab-disabled-children (accessed on 15 December 2017).

- RWAQ. Free Online Arabic Courses. Available online: https://www.rwaq.org/ (accessed on 15 December 2017).

- Solvoltaics. Investors. Available online: https://solvoltaics.com/solar-nanotechnology/#investors (accessed on 15 December 2017).

- Siluria. Investors. Available online: http://siluria.com/About/Investors (accessed on 15 December 2017).

- Parsable. Investors. Available online: https://www.parsable.com/about-us (accessed on 15 December 2017).

- Xia, X.; Govindan, K.; Zhu, Q. Analyzing internal barriers for automotive parts remanufacturers in China using grey-dematel approach. J. Clean. Prod. 2015, 87, 811–825. [Google Scholar] [CrossRef]

- Zhu, Q.; Sarkis, J.; Lai, K.-H. Supply chain-based barriers for truck-engine remanufacturing in Cina. Transp. Res. Part E Logist. Transp. Rev. 2014, 68, 103–117. [Google Scholar] [CrossRef]

- Wang, W.; Tian, Y.; Zhu, Q.; Zhong, Y. Barriers for household e-waste collection in China: Perspectives from formal collecting enterprises in Liaoning province. J. Clean. Prod. 2017, 153, 299–308. [Google Scholar] [CrossRef]

- Gabus, A.; Fontela, E. World Problems, an Invitation to Further Thought within the Framework of Dematel; Battelle Geneva Research Center: Geneva, Switzerland, 1972. [Google Scholar]

- Fontela, E.; Gabus, A. The Dematel Observer, Dematel 1976 Report; Battelle Geneva Research Center: Geneva, Switzerland, 1976. [Google Scholar]

- Fu, X.; Zhu, Q.; Sarkis, J. Evaluating green supplier development programs at a telecommunications systems provider. Int. J. Prod. Econ. 2012, 140, 357–367. [Google Scholar] [CrossRef]

- Bai, C.; Sarkis, J. A grey-based dematel model for evaluating business process management critical success factors. Int. J. Prod. Econ. 2013, 146, 281–292. [Google Scholar] [CrossRef]

- Wu, W.-W.; Lee, Y.-T. Developing global managers’ competencies using the fuzzy dematel method. Expert Syst. Appl. 2007, 32, 499–507. [Google Scholar] [CrossRef]

- Zhu, Q.; Sarkis, J.; Geng, Y. Barriers to environmentally-friendly clothing production among Chinese apparel companies. Asian Bus. Manag. 2011, 10, 425–452. [Google Scholar] [CrossRef]

- Lin, R.-J. Using fuzzy Dematel to evaluate the green supply chain management practices. J. Clean. Prod. 2013, 40, 32–39. [Google Scholar] [CrossRef]

- Dou, Y.; Sarkis, J. A multiple stakeholder perspective on barriers to implementing China ROHS regulations. Resour. Conserv. Recycl. 2013, 81, 92–104. [Google Scholar] [CrossRef]

- Dou, Y.; Zhu, Q.; Sarkis, J. Integrating strategic carbon management into formal evaluation of environmental supplier development programs. Bus. Strateg. Environ. 2015, 24, 873–891. [Google Scholar] [CrossRef]

- Tsai, W.-H.; Chou, W.-C.; Hsu, W. The sustainability balanced scorecard as a framework for selecting socially responsible investment: An effective MCDM model. J. Oper. Res. Soc. 2009, 60, 1396–1410. [Google Scholar] [CrossRef]

- Bai, C.; Sarkis, J. Evaluating supplier development programs with a grey based rough set methodology. Expert Syst. Appl. 2011, 38, 13505–13517. [Google Scholar] [CrossRef]

- Bai, C.; Kusi-Sarpong, S.; Sarkis, J. An implementation path for green information technology systems in the ghanaian mining industry. J. Clean. Prod. 2017, 164, 1105–1123. [Google Scholar] [CrossRef]

- Ju-Long, D. Control problems of grey systems. Syst. Control Lett. 1982, 1, 288–294. [Google Scholar] [CrossRef]

- Ren, J.; Liang, H.; Dong, L.; Gao, Z.; He, C.; Pan, M.; Sun, L. Sustainable development of sewage sludge-to-energy in China: Barriers identification and technologies prioritization. Renew. Sustain. Energy Rev. 2017, 67, 384–396. [Google Scholar] [CrossRef]

- Li, G.-D.; Yamaguchi, D.; Nagai, M. A grey-based decision-making approach to the supplier selection problem. Math. Comput. Model. 2007, 46, 573–581. [Google Scholar] [CrossRef]

- Jin, J.; Yu, Z.; Mi, C. Commercial bank credit risk management based on grey incidence analysis. Grey Syst. Theory Appl. 2012, 2, 385–394. [Google Scholar] [CrossRef]

- Liu, S.; Forrest, J.; Yang, Y. A brief introduction to grey systems theory. Grey Syst. Theory Appl. 2012, 2, 89–104. [Google Scholar] [CrossRef]

- Rahimnia, F.; Moghadasian, M.; Mashreghi, E. Application of grey theory approach to evaluation of organizational vision. Grey Syst. Theory Appl. 2011, 1, 33–46. [Google Scholar] [CrossRef]

- Terjesen, S.; Bosma, N.; Stam, E. Advancing public policy for high-growth, female, and social entrepreneurs. Public Adm. Rev. 2016, 76, 230–239. [Google Scholar] [CrossRef]

- Henrekson, M.; Johansson, D. Gazelles as job creators: A survey and interpretation of the evidence. Small Bus. Econ. Group 2010, 35, 227–244. [Google Scholar] [CrossRef]

- Autio, E.; Rannikko, H. Retaining winners: Can policy boost high-growth entrepreneurship? Res. Policy 2016, 45, 42–55. [Google Scholar] [CrossRef]

- Dvouletý, O.; Lukeš, M. Report on Policies on Business Start-Ups and Self-Employment; CUPESSE: Heidelberg, Germany, 2017; doi:10.13140/RG.2.2.2, 0256. [Google Scholar]

- Assaf, T. The Kingdom of Saudi Arabia: Status of the Entrepreneurship Ecosystem; WAMDA: Amman, Jordan, 2017; p. 55.

| Research Area | Paper Quantity | Research Area | Paper Quantity |

|---|---|---|---|

| Business and Economics | 277 | Energy fuels | 14 |

| Environmental Science and Ecology | 42 | Operations Research and Management Science | 13 |

| Public Administration | 35 | Social Sciences | 13 |

| Engineering | 27 | Urban Studies | 10 |

| Geography | 15 | Sociology | 9 |

| Publication | Paper Quantity |

|---|---|

| Journal of Business Venturing | 43 |

| Energy Policy | 11 |

| Strategic Management Journal | 11 |

| Entrepreneurship Policy and Practice | 8 |

| Journal of Management Studies | 8 |

| Journal of International Business Studies | 6 |

| Journal of Small Business Management | 6 |

| Management Decision | 6 |

| Asia Pacific Journal of Management | 5 |

| Entrepreneurship and Regional Development | 5 |

| Enablers |

|---|

| E1: The VC firm is willing to provide necessary human resources support [74,75] |

| E2: Venture capitalists deeply understand the sustainable business models [9,75,77,78] |

| E3: Top management support [75] |

| E4: Venture capitalists are morally committed to sustainability [9,80,81,82] |

| E5: Innovation in the business model [9,83,84] |

| E6: VC investments in sustainable start-ups can reduce financial risks [85,86,87,88] |

| E7: VC investments in sustainable start-ups can create new demand [9,89,90] |

| E8: SMEs and other VC firms credible collaborations and networking [9,78,91] |

| E9: Government policies and regulations for sustainable investments [79,92,93,94] |

| E10: Government use of international standards for sustainable investments [38,95,96] |

| No | Organizational Level | Experience in Organization and Industry | Organization Information | Founded In | Number of Employees (2017) |

|---|---|---|---|---|---|

| 1 | Executive management | 9/20 | Venture Capital and Private Equity, Privately Owned | 2009 | 20 |

| 2 | Executive management | 2/10 | Venture Capital and Private Equity, Government Owned | 1971 | 230 |

| 3 | Executive management | 7/19 | Corporate Venture Capital and Private Equity, Independently Managed | 1986 | 40 |

| 4 | Executive management | 6/14 | Corporate Venture Capital and Private Equity, Directly Managed | 2012 | 53 |

| Linguistic Terms | Values |

|---|---|

| No influence (N) | 0 |

| Very low influence (VL) | 1 |

| Low influence (L) | 2 |

| High influence (H) | 3 |

| Very high influence (VH) | 4 |

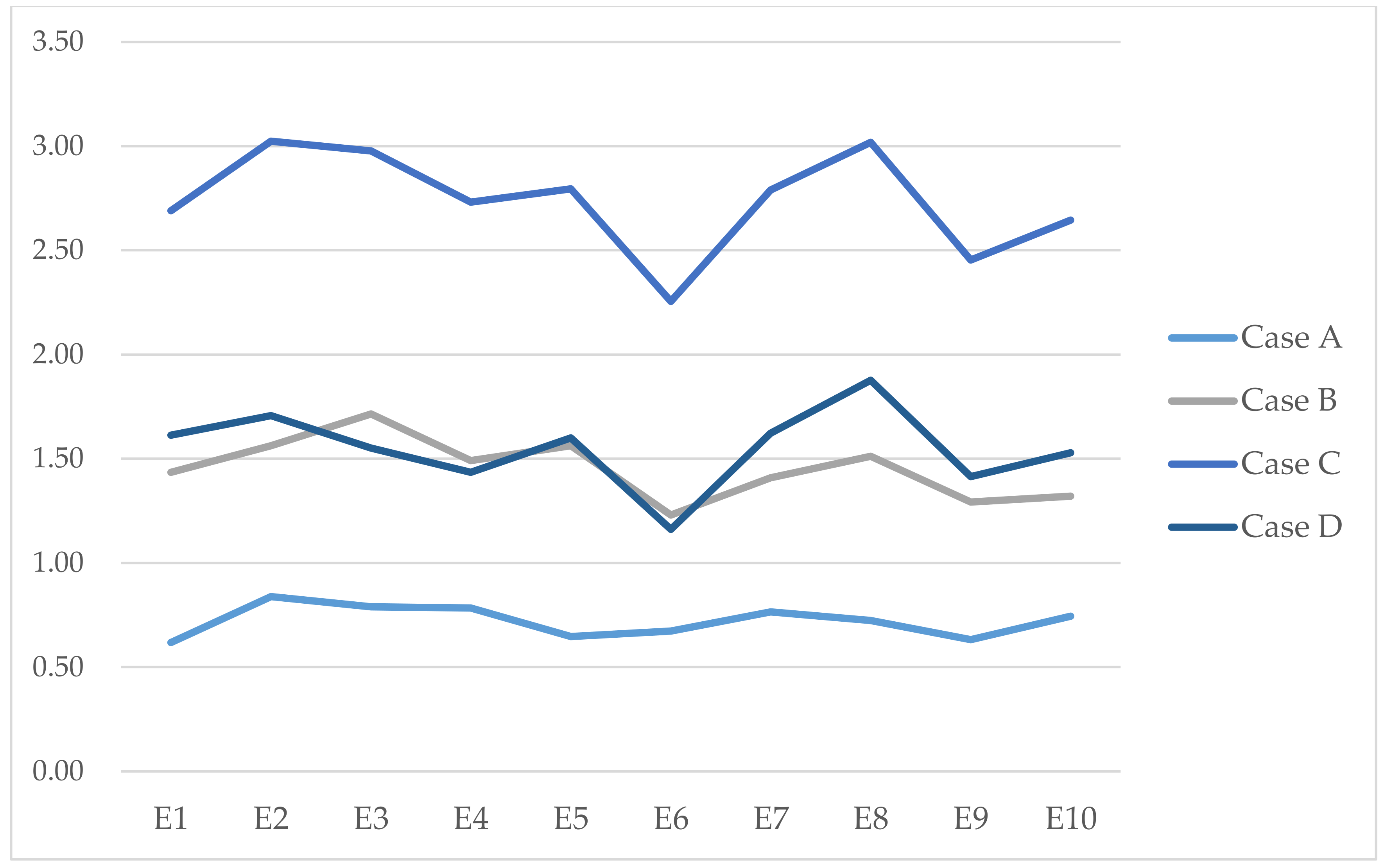

| E1 | E2 | E3 | E4 | E5 | E6 | E7 | E8 | E9 | E10 | |

|---|---|---|---|---|---|---|---|---|---|---|

| E1 | 0.6020 | 0.7168 | 0.7168 | 0.6427 | 0.7478 | 0.5340 | 0.7270 | 0.7816 | 0.5095 | 0.4470 |

| E2 | 0.8251 | 0.7339 | 0.8415 | 0.7779 | 0.8860 | 0.6241 | 0.8553 | 0.9245 | 0.5886 | 0.5164 |

| E3 | 0.8079 | 0.8243 | 0.7151 | 0.7476 | 0.8598 | 0.6107 | 0.8437 | 0.8979 | 0.5757 | 0.5051 |

| E4 | 0.7476 | 0.7912 | 0.7767 | 0.6094 | 0.8325 | 0.5787 | 0.8033 | 0.8687 | 0.5524 | 0.4847 |

| E5 | 0.6757 | 0.6956 | 0.6958 | 0.6224 | 0.6384 | 0.5236 | 0.7341 | 0.7595 | 0.4996 | 0.4383 |

| E6 | 0.4832 | 0.5124 | 0.5058 | 0.4500 | 0.5195 | 0.3330 | 0.5100 | 0.5385 | 0.3721 | 0.3255 |

| E7 | 0.7021 | 0.7225 | 0.7225 | 0.6335 | 0.7537 | 0.5383 | 0.6454 | 0.8018 | 0.5138 | 0.4508 |

| E8 | 0.7560 | 0.7923 | 0.7791 | 0.7044 | 0.8268 | 0.5811 | 0.8050 | 0.7477 | 0.5683 | 0.5004 |

| E9 | 0.8095 | 0.8336 | 0.8631 | 0.7242 | 0.8838 | 0.6684 | 0.8759 | 0.9155 | 0.5288 | 0.5432 |

| E10 | 0.7720 | 0.8097 | 0.8329 | 0.7025 | 0.8521 | 0.6365 | 0.8449 | 0.8827 | 0.6142 | 0.4487 |

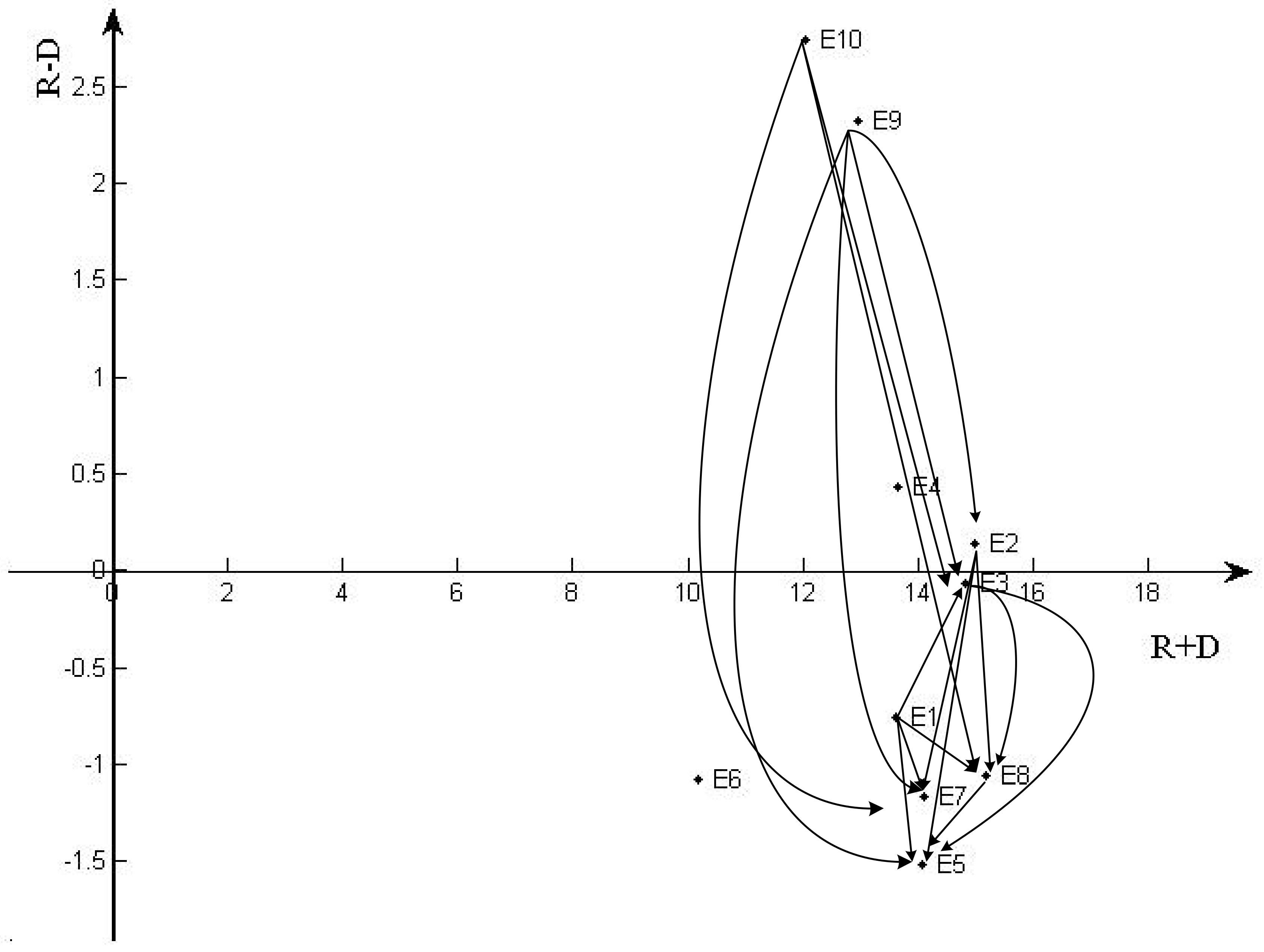

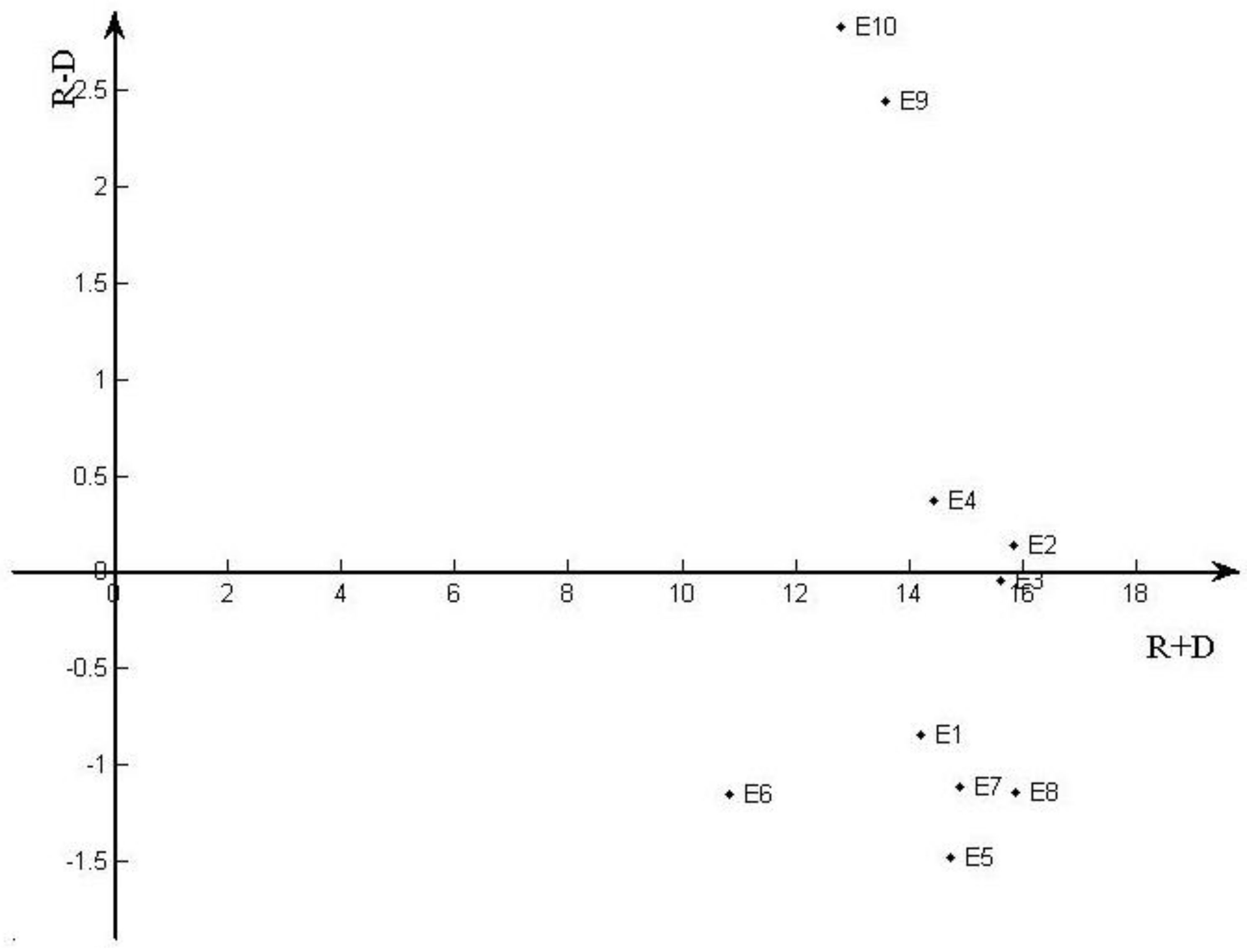

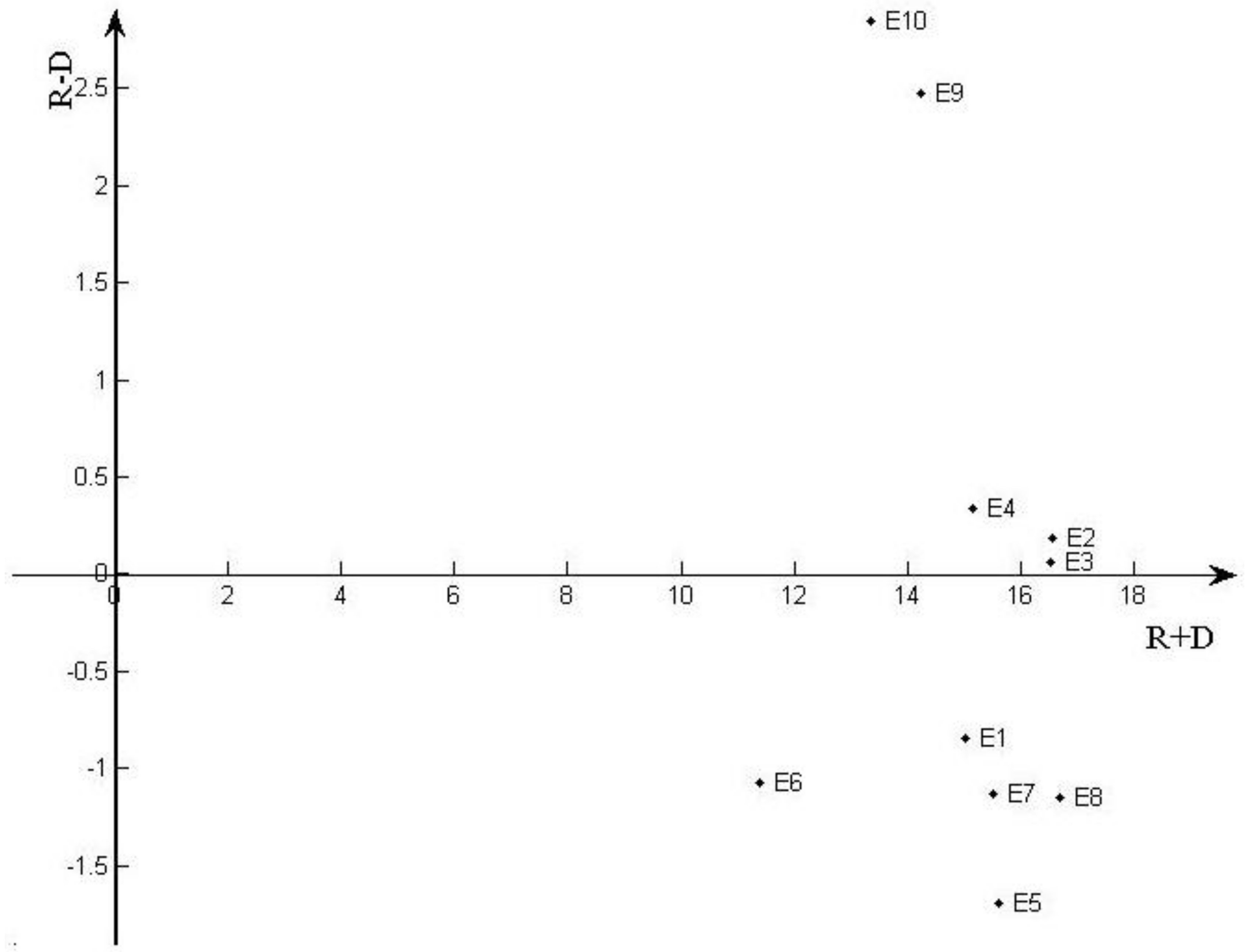

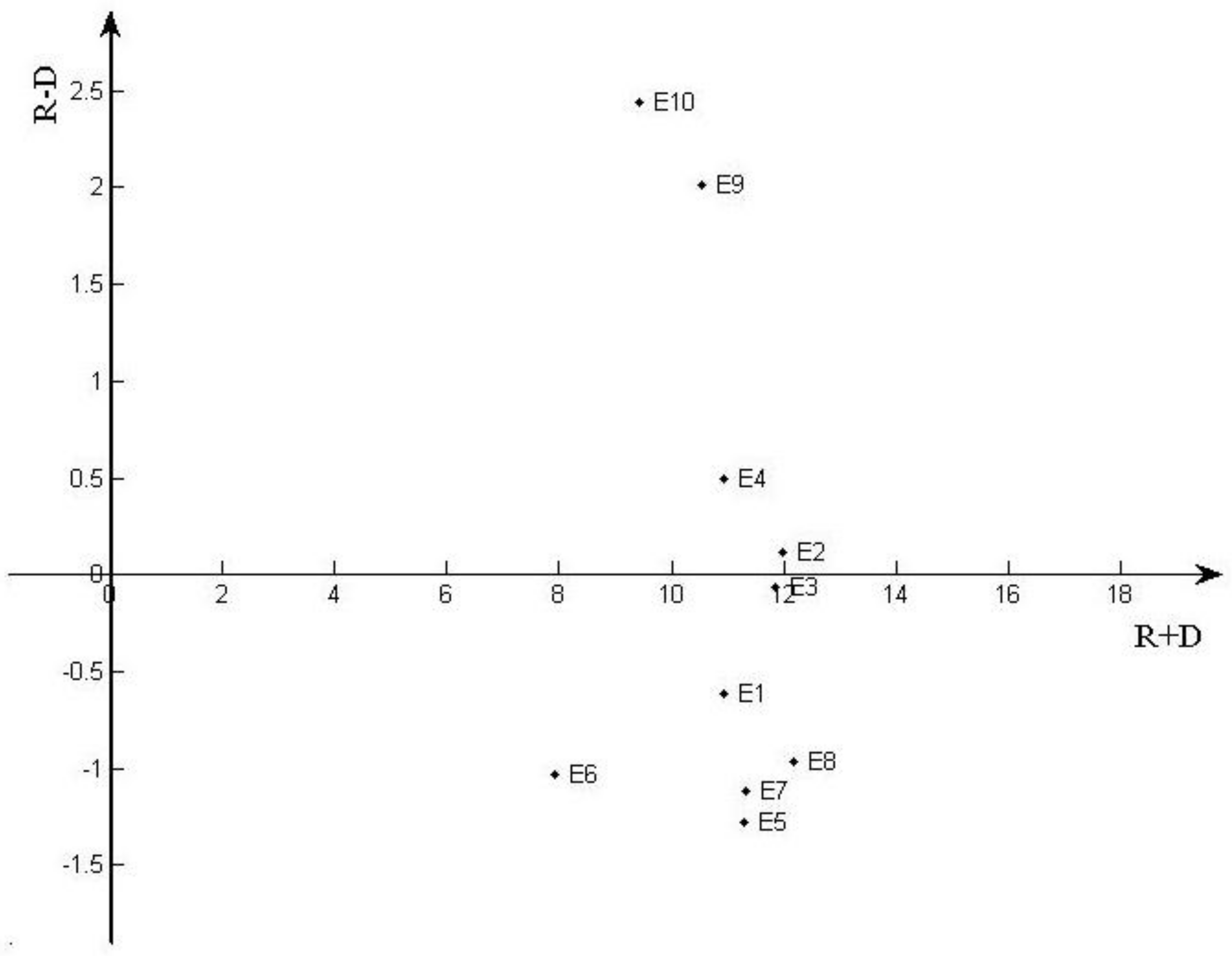

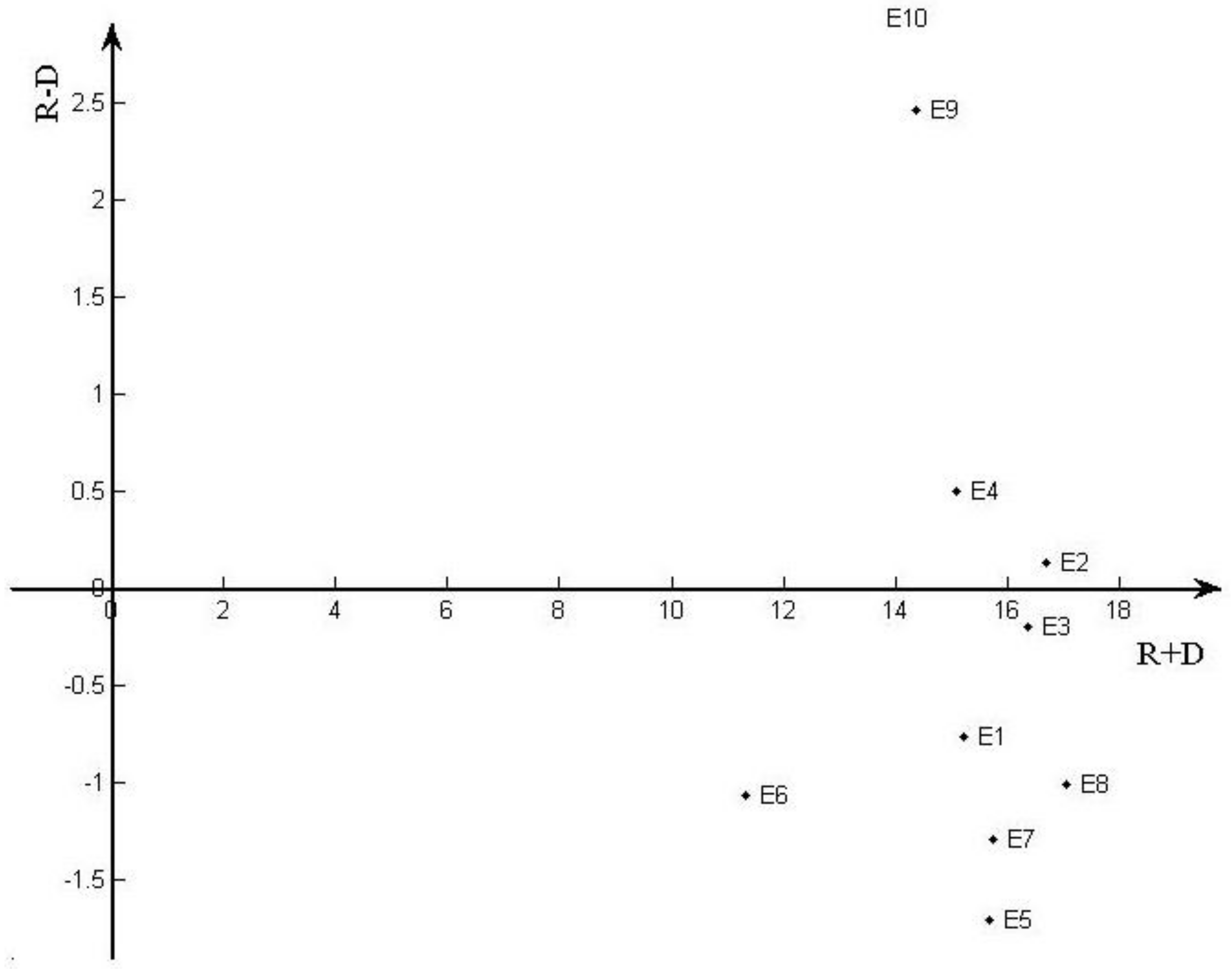

| Enabler | R Sum | D Sum | R + D | R-D |

|---|---|---|---|---|

| E1 | 6.4252 | 7.1811 | 13.6063 | −0.7559 |

| E2 | 7.5734 | 7.4324 | 15.0058 | 0.1411 |

| E3 | 7.3878 | 7.4492 | 14.8370 | −0.0615 |

| E4 | 7.0454 | 6.6147 | 13.6601 | 0.4307 |

| E5 | 6.2831 | 7.8006 | 14.0837 | −1.5174 |

| E6 | 4.5501 | 5.6283 | 10.1784 | −1.0782 |

| E7 | 6.4843 | 7.6446 | 14.1289 | −1.1602 |

| E8 | 7.0610 | 8.1185 | 15.1795 | −1.0575 |

| E9 | 7.6461 | 5.3230 | 12.9691 | 2.3230 |

| E10 | 7.3962 | 4.6602 | 12.0564 | 2.7360 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Antarciuc, E.; Zhu, Q.; Almarri, J.; Zhao, S.; Feng, Y.; Agyemang, M. Sustainable Venture Capital Investments: An Enabler Investigation. Sustainability 2018, 10, 1204. https://doi.org/10.3390/su10041204

Antarciuc E, Zhu Q, Almarri J, Zhao S, Feng Y, Agyemang M. Sustainable Venture Capital Investments: An Enabler Investigation. Sustainability. 2018; 10(4):1204. https://doi.org/10.3390/su10041204

Chicago/Turabian StyleAntarciuc, Elena, Qinghua Zhu, Jaber Almarri, Senlin Zhao, Yunting Feng, and Martin Agyemang. 2018. "Sustainable Venture Capital Investments: An Enabler Investigation" Sustainability 10, no. 4: 1204. https://doi.org/10.3390/su10041204

APA StyleAntarciuc, E., Zhu, Q., Almarri, J., Zhao, S., Feng, Y., & Agyemang, M. (2018). Sustainable Venture Capital Investments: An Enabler Investigation. Sustainability, 10(4), 1204. https://doi.org/10.3390/su10041204