Policies and Predictions for a Low-Carbon Transition by 2050 in Passenger Vehicles in East Asia: Based on an Analysis Using the E3ME-FTT Model

,

,

Abstract

:1. Introduction

- (1)

- (2)

- The existing studies have either taken one particular representative car model or used a representative agent to examine the response of agents to a set of policy incentives. In the real world, consumers are diverse and do not respond to policy incentives collectively.

2. Policy Context

2.1. China

2.2. Japan

2.3. Korea

- (1)

- Substituting fossil fuel cars with EVs requires a reduction in the cost of batteries (which depend on international technology actions) and building a nationwide charging infrastructure.

- (2)

- Green Car Developments: Current heavy fossil fuel dependence of transport should be reduced by diversifying energy sources. NEVs offer a promising alternative to conventional vehicles in short distance trips in urban areas. Wireless electricity technology could facilitate the introduction of electric vehicles by solving their current battery limitations. Fuel cell technology could be a long-term option in future alternative fuel vehicle developments. Legal support and economic incentives should be provided for the development of these types of green vehicles.

- (3)

- Non-Motorized Transportation: Non-motorized forms of transport provide zero carbon emissions. Bicycles are used extensively in many European and Asian cities, but their modal share in Korean cities is minimal due to limited infrastructure and low public reception. Bicycles should be promoted for short distance commuting by providing adequate infrastructure and by increasing safety.

2.4. Taiwan

3. Methodology

3.1. Theoretical Background

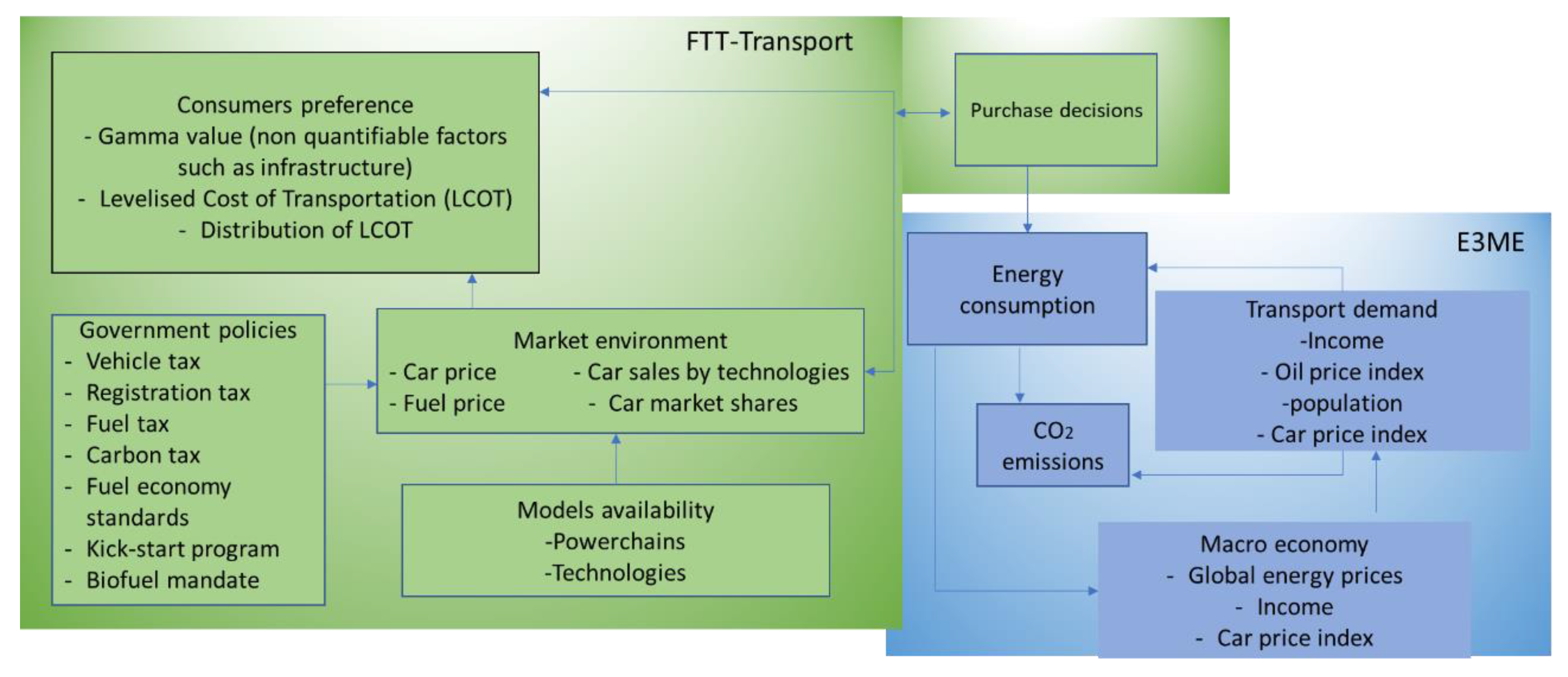

3.2. Structure of FTT: Transportation

3.3. The Levelized Cost of Transportation (LCOT)

- is a registration vehicle tax, in $/vehicle, paid at purchase time,

- is the capital cost of cars, in $/vehicle

- is the carbon tax based on fuel economy , in $/vehicle/(gCO2/km)

- is a tax on fuel consumption, in $/L

- is the fuel consumption, in L/vehicle

- is the vehicle maintenance cost in $/vehicle

- is a road tax in $/vehicle

3.3.1. The Generalized Cost as a Comparison Measure

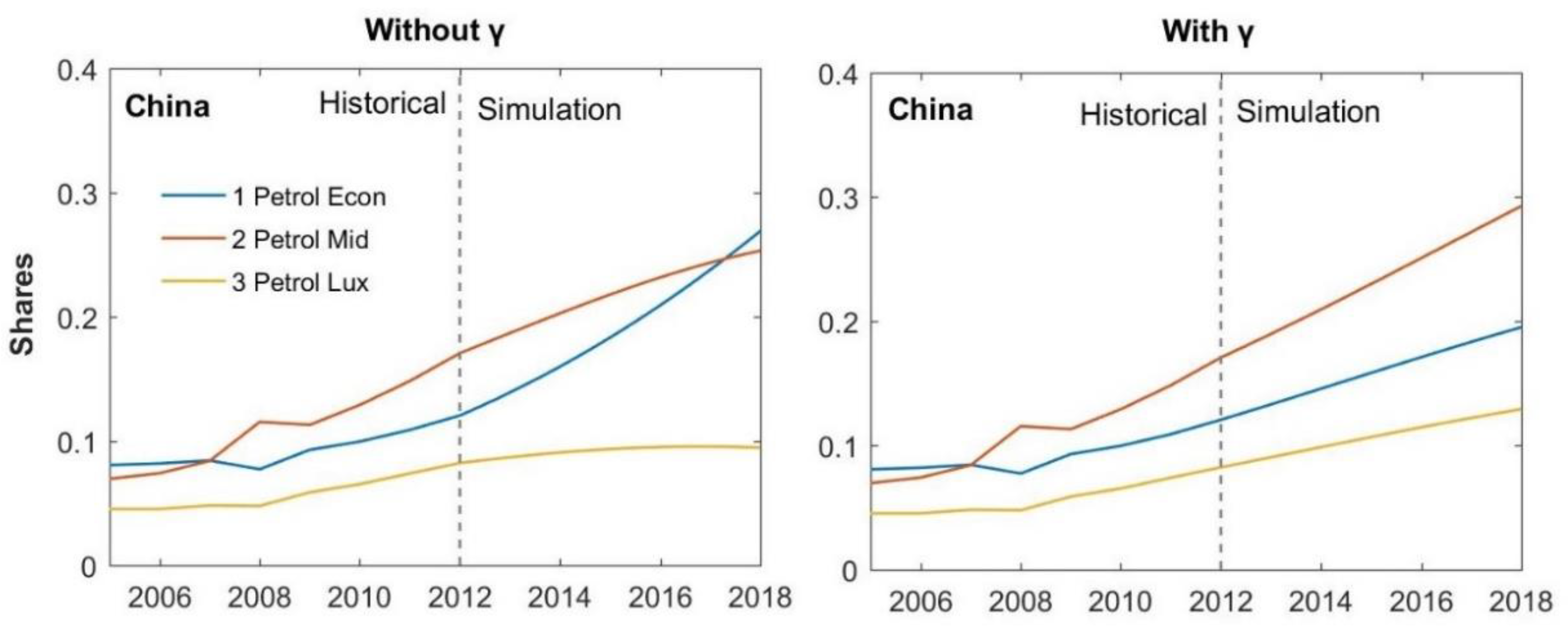

3.3.2. The Determination of Intangibles (γ)

3.3.3. Technology Learning

3.4. Energy Consumption and Emissions

3.5. Linkage between FTT: Transport and E3ME

4. Policy Assumptions

5. Data Overview

6. Results

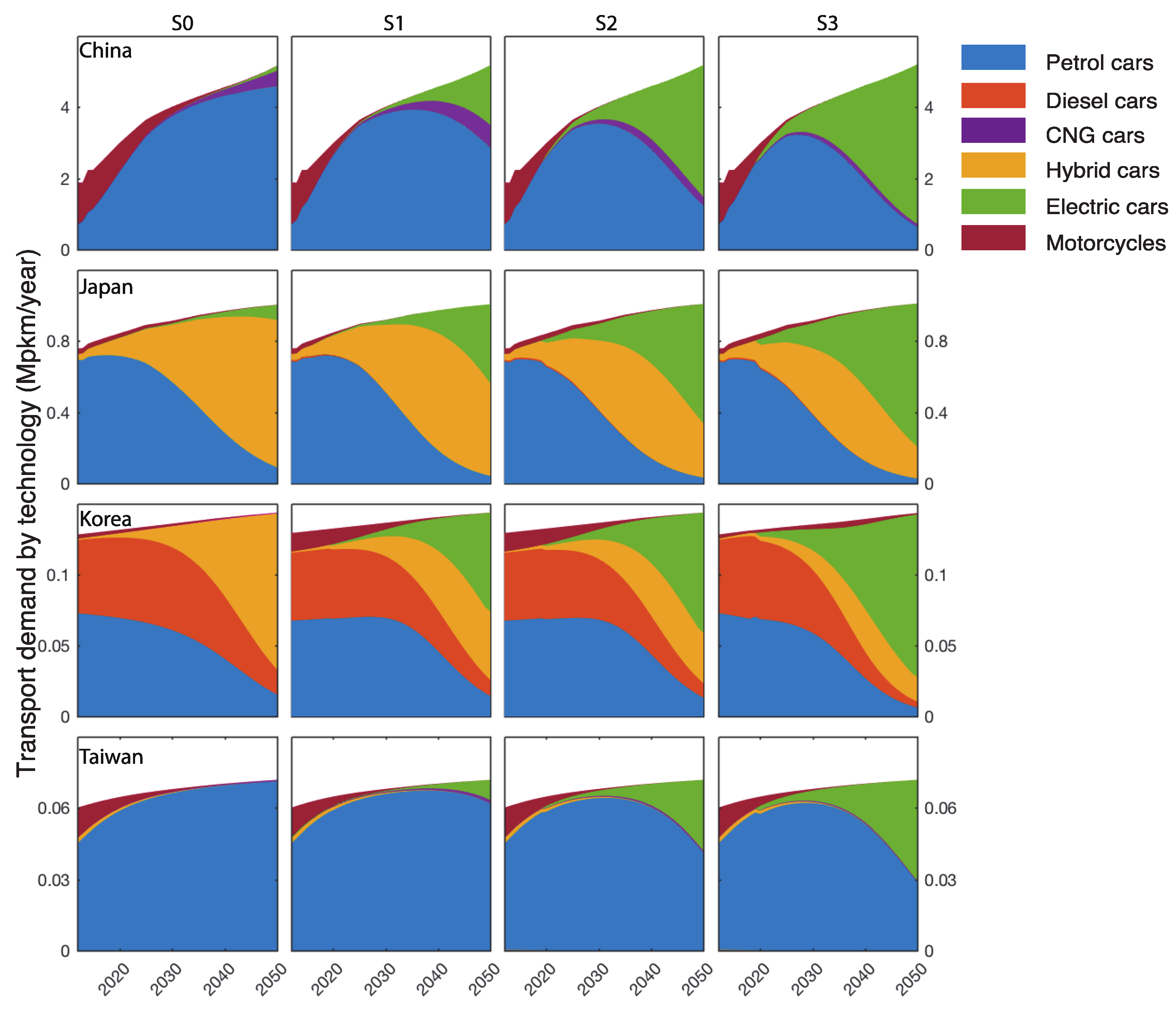

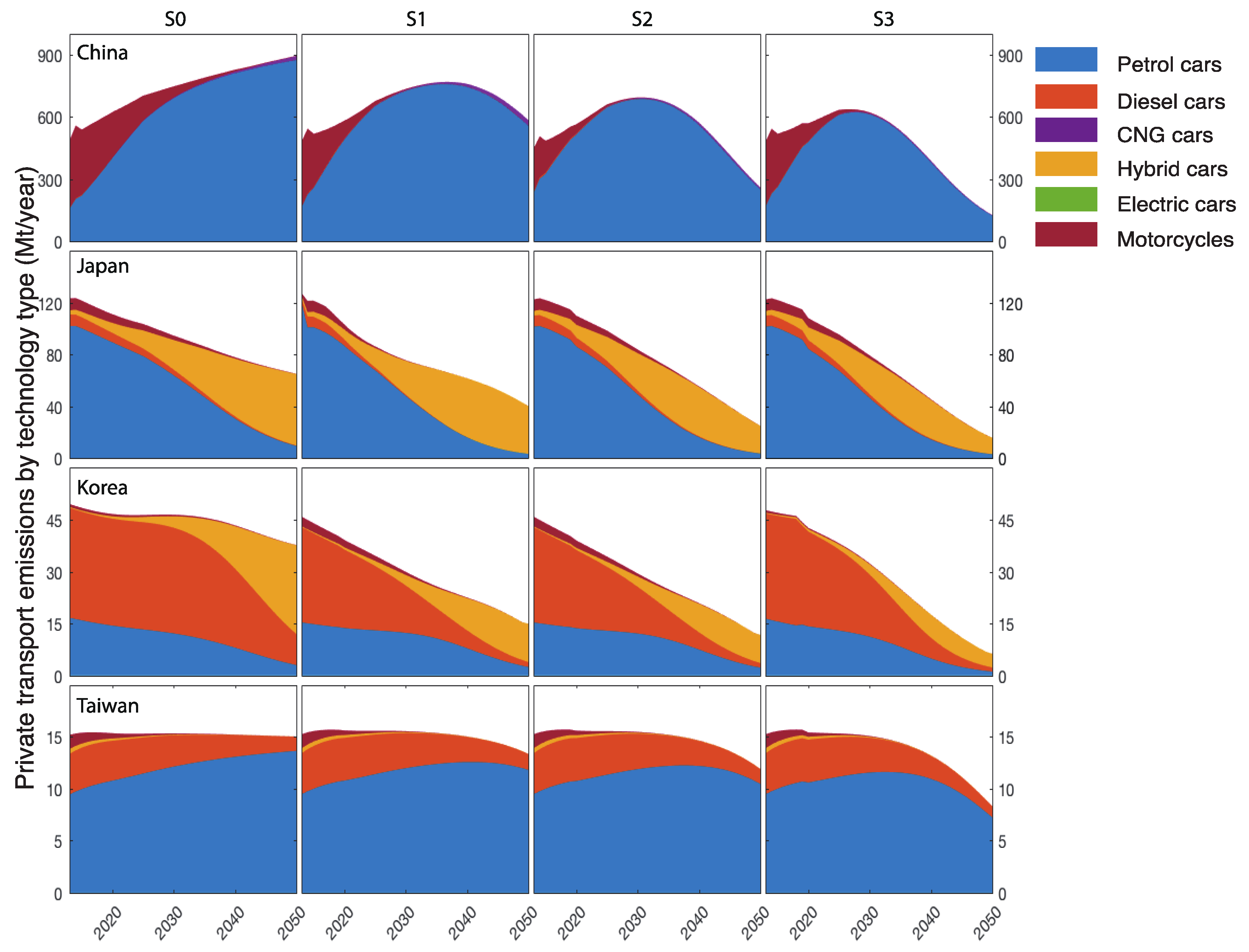

6.1. China

6.2. Japan

6.3. Korea

6.4. Taiwan

7. Policy Implications and Conclusions

8. Limitations and Recommendations

- (1)

- In this research, we have identified the available technologies, although new technologies will emerge in the future. However, it is impossible for this model to predict technologies that have not penetrated into the market, for example, fuel cell vehicles.

- (2)

- The non-pecuniary cost is represented by a γ parameter, which is found by calculating the difference between the historical shares and future shares. Our projections from 2012 to 2020 follow the trend from 2004 to 2012. However, γ parameters for EVs in Taiwan and South Korea may carry a degree of uncertainty, because our basis to determine the γ parameter is not sufficient, based on the fact that there is currently a limited number of EVs on the road. A better calibration can be achieved with the EV market shares data obtained from recent years (2012–2017).

- (3)

- Autonomous vehicles (AVs) represent a disruptive technology that could potentially impact on the vehicle size and transport demand for passenger cars.

Author Contributions

Acknowledgments

Conflicts of Interest

Appendix A. Initial Parameters

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Technology | Engine Size | Prices of Cars (USD/vehicle) | Standard Deviation of Price (USD/vehicle) | Fuel Cost (USD/km) | Discount Rate | Energy Use (MJ/vkm) | Learning Rate |

|---|---|---|---|---|---|---|---|

| Petrol | Econ | 9400.00 | 6249.00 | 0.07 | 0.15 | 2.05 | 1% |

| Mid | 21,036.00 | 12,005.00 | 0.08 | 0.15 | 2.26 | 1% | |

| Lux | 40,667.00 | 20,083.00 | 0.10 | 0.15 | 2.74 | 1% | |

| Adv Petrol | Econ | 9400.00 | 6249.00 | 0.05 | 0.15 | 1.64 | 5% |

| Mid | 21,036.00 | 12,005.00 | 0.06 | 0.15 | 1.81 | 5% | |

| Lux | 40,667.00 | 20,083.00 | 0.08 | 0.15 | 2.19 | 5% | |

| Diesel | Econ | 9400.00 | 1000.00 | 0.05 | 0.15 | 1.85 | 1% |

| Mid | 22,000.00 | 5631.20 | 0.06 | 0.15 | 2.12 | 1% | |

| Lux | 40,300.00 | 4404.40 | 0.07 | 0.15 | 2.40 | 1% | |

| Adv Diesel | Econ | 9400.00 | 1000.00 | 0.04 | 0.15 | 2.95 | 5% |

| Mid | 22,000.00 | 5631.20 | 0.05 | 0.15 | 1.70 | 5% | |

| Lux | 40,300.00 | 4404.40 | 0.06 | 0.15 | 1.92 | 5% | |

| CNG | Econ | 9635.00 | 1965.00 | 0.04 | 0.15 | 1.50 | 1% |

| Mid | 13,953.00 | 2654.00 | 0.05 | 0.15 | 1.70 | 1% | |

| Lux | 33,710.00 | 2654.00 | 0.06 | 0.15 | 2.09 | 1% | |

| Hybrid | Econ | 31,252.91 | 1654.00 | 0.02 | 0.15 | 0.68 | 5% |

| Mid | 41,018.00 | 1654.00 | 0.02 | 0.15 | 0.85 | 5% | |

| Lux | 47,584.00 | 1571.00 | 0.02 | 0.15 | 0.92 | 5% | |

| Electric | Econ | 13,250.00 | 3127.62 | 0.00 | 0.15 | 0.54 | 10% |

| Mid | 27,072.75 | 4372.41 | 0.00 | 0.15 | 0.76 | 10% | |

| Lux | 42,423.52 | 1492.71 | 0.00 | 0.15 | 0.94 | 10% | |

| Bikes | Econ | 1373.00 | 1859.00 | 0.02 | 0.15 | 0.72 | 1% |

| Lux | 4989.00 | 3031.00 | 0.05 | 0.15 | 1.44 | 1% | |

| Adv Bikes | Adv Econ | 1373.00 | 1859.00 | 0.00 | 0.15 | 0.00 | 5% |

| Adv Lux | 4989.00 | 3031.00 | 0.00 | 0.15 | 0.00 | 5% |

| Technology | Engine Size | Prices of Cars (USD/vehicle) | Standard Deviation of Price (USD/vehicle) | Fuel Cost (USD/km) | Discount Rate | Energy Use (MJ/vkm) | Learning Rate |

|---|---|---|---|---|---|---|---|

| Petrol | Econ | 12,973.05 | 4044.80 | 0.064 | 0.150 | 2.052 | 1% |

| Mid | 22,197.47 | 9597.81 | 0.068 | 0.150 | 2.260 | 1% | |

| Lux | 31,879.83 | 17,485.23 | 0.077 | 0.150 | 2.740 | 1% | |

| Adv Petrol | Econ | 12,973.05 | 4044.80 | 0.051 | 0.150 | 1.642 | 5% |

| Mid | 22,197.47 | 9597.81 | 0.054 | 0.150 | 1.808 | 5% | |

| Lux | 31,879.83 | 17,485.23 | 0.061 | 0.150 | 2.192 | 5% | |

| Diesel | Econ | N/A | N/A | N/A | N/A | N/A | N/A |

| Mid | N/A | N/A | N/A | N/A | N/A | N/A | |

| Lux | N/A | N/A | N/A | N/A | N/A | N/A | |

| Adv Diesel | Econ | N/A | N/A | N/A | N/A | N/A | N/A |

| Mid | N/A | N/A | N/A | N/A | N/A | N/A | |

| Lux | N/A | N/A | N/A | N/A | N/A | N/A | |

| CNG | Econ | N/A | N/A | N/A | N/A | N/A | N/A |

| Mid | N/A | N/A | N/A | N/A | N/A | N/A | |

| Lux | 27,472.00 | 0.00 | 0.070 | 0.150 | 2.093 | 1% | |

| Hybrid | Econ | 27,547.72 | 836.16 | 0.023 | 0.150 | 0.684 | 5% |

| Mid | 31,488.10 | 5548.62 | 0.028 | 0.150 | 0.848 | 5% | |

| Lux | 40,417.93 | 17,197.10 | 0.031 | 0.150 | 0.923 | 5% | |

| Electric | Econ | 12,448.00 | 1300.00 | 0.000 | 0.150 | 0.540 | 10% |

| Mid | 16,841.40 | 2592.98 | 0.000 | 0.150 | 0.756 | 10% | |

| Lux | 28,407.61 | 2647.72 | 0.000 | 0.150 | 0.936 | 10% | |

| Bikes | Econ | 4516.00 | 2292.00 | 0.046 | 0.150 | 0.720 | 1% |

| Lux | 12,357.00 | 4541.00 | 0.057 | 0.150 | 1.440 | 1% | |

| Adv Bikes | Adv Econ | 4516.00 | 2292.00 | 0.037 | 0.150 | 0.000 | 5% |

| Adv Lux | 12,357.00 | 4541.00 | 0.046 | 0.150 | 0.000 | 5% |

| Technology | Engine Size | Prices of Cars (USD/vehicle) | Standard Deviation of Price (USD/vehicle) | Fuel Cost (USD/km) | Discount Rate | Energy Use (MJ/vkm) | Learning Rate |

|---|---|---|---|---|---|---|---|

| Petrol | Econ | 17,842.45 | 30,920.21 | 0.079 | 0.15 | 2.05 | 1% |

| Mid | 19,342.74 | 5601.90 | 0.103 | 0.15 | 2.26 | 1% | |

| Lux | 38,942.42 | 29,216.44 | 0.139 | 0.15 | 2.74 | 1% | |

| Adv Petrol | Econ | 17,842.45 | 30,920.21 | 0.045 | 0.15 | 1.64 | 5% |

| Mid | 19,342.74 | 5601.90 | 0.059 | 0.15 | 1.81 | 5% | |

| Lux | 38,942.42 | 29,216.44 | 0.079 | 0.15 | 2.19 | 5% | |

| Diesel | Econ | N/A | N/A | N/A | N/A | N/A | N/A |

| Mid | 22,294.36 | 10,372.06 | 0.078 | 0.15 | 2.12 | 1% | |

| Lux | 29,919.85 | 15,199.82 | 0.093 | 0.15 | 2.40 | 1% | |

| Adv Diesel | Econ | N/A | N/A | N/A | N/A | N/A | N/A |

| Mid | 22,294.36 | 10,372.06 | 0.042 | 0.15 | 1.70 | 5% | |

| Lux | 29,919.85 | 15,199.82 | 0.050 | 0.15 | 1.92 | 5% | |

| CNG | Econ | N/A | N/A | N/A | N/A | N/A | N/A |

| Mid | N/A | N/A | N/A | N/A | N/A | N/A | |

| Lux | N/A | N/A | N/A | N/A | N/A | N/A | |

| Hybrid | Econ | 23,080.00 | 1000.00 | 0.040 | 0.15 | 0.68 | 5% |

| Mid | 30,655.62 | 3111.79 | 0.052 | 0.15 | 0.85 | 5% | |

| Lux | 35,031.11 | 10,048.45 | 0.103 | 0.15 | 0.92 | 5% | |

| Electric | Econ | 10,455.00 | 1000.00 | 0.004 | 0.15 | 0.67 | 10% |

| Mid | 12,272.00 | 100.00 | 0.005 | 0.15 | 0.81 | 10% | |

| Lux | 30,460.00 | 1000.00 | 0.008 | 0.15 | 0.93 | 10% | |

| Bikes | Econ | 2071.00 | 831.00 | 0.026 | 0.15 | 0.72 | 1% |

| Lux | 6306.00 | 2366.00 | 0.032 | 0.15 | 1.44 | 1% | |

| Adv Bikes | Adv Econ | 2071.00 | 831.00 | 0.026 | 0.15 | 0.00 | 5% |

| Adv Lux | 6306.00 | 2366.00 | 0.032 | 0.15 | 0.00 | 5% |

| Technology | Engine Size | Prices of Cars (USD/vehicle) | Standard Deviation of Price (USD/vehicle) | Fuel Cost (USD/km) | Discount Rate | Energy Use (MJ/vkm) | Learning Rate |

|---|---|---|---|---|---|---|---|

| Petrol | Econ | 12,936.18 | 2872.35 | 0.068 | 0.15 | 1.98 | 0.01 |

| Mid | 21,320.53 | 3746.18 | 0.069 | 0.15 | 2.02 | 0.01 | |

| Lux | 27,991.15 | 15,787.11 | 0.095 | 0.15 | 2.77 | 0.01 | |

| Adv Petrol | Econ | 15,523.41 | 2872.35 | 0.061 | 0.15 | 1.59 | 0.05 |

| Mid | 25,584.64 | 3746.18 | 0.062 | 0.15 | 1.61 | 0.05 | |

| Lux | 33,589.37 | 15,787.11 | 0.085 | 0.15 | 2.22 | 0.05 | |

| Diesel | Econ | N/A | N/A | N/A | N/A | N/A | N/A |

| Mid | N/A | N/A | N/A | N/A | N/A | N/A | |

| Lux | 33,589.37 | 15,787.11 | 0.072 | 0.15 | 2.53 | 0.01 | |

| Adv Diesel | Econ | N/A | N/A | N/A | N/A | N/A | N/A |

| Mid | N/A | N/A | N/A | N/A | N/A | N/A | |

| Lux | 33,589.37 | 15,787.11 | 0.065 | 0.15 | 2.02 | 0.05 | |

| CNG | Econ | N/A | N/A | N/A | N/A | N/A | N/A |

| Mid | N/A | N/A | N/A | N/A | N/A | N/A | |

| Lux | N/A | N/A | N/A | N/A | N/A | N/A | |

| Hybrid | Econ | 19,513.46 | 2913.99 | 0.046 | 0.15 | 1.34 | 0.05 |

| Mid | 22,734.51 | 4844.60 | 0.057 | 0.15 | 1.67 | 0.05 | |

| Lux | 45,303.10 | 13,194.43 | 0.068 | 0.15 | 2.00 | 0.05 | |

| Electric | Econ | 18,984.94 | 190.13 | 0.000 | 0.15 | 0.21 | 0.1 |

| Mid | 31,287.74 | 1529.99 | 0.000 | 0.15 | 0.54 | 0.1 | |

| Lux | 40,650.00 | 2080.00 | 0.000 | 0.15 | 0.58 | 0.1 | |

| Bikes | Econ | 4516.00 | 2292.00 | 0.025 | 0.15 | 0.53 | 0.01 |

| Lux | 12,357.00 | 4541.00 | 0.026 | 0.15 | 0.77 | 0.01 | |

| Adv Bikes | Adv Econ | 4516.00 | 2292.00 | 0.000 | 0.15 | 0.53 | 0.05 |

| Adv Lux | 12,357.00 | 4541.00 | 0.000 | 0.15 | 0.77 | 0.05 |

Appendix B. Assumptions for the Policy Scenarios

| China | Vehicle Tax (USD) | EV Subsidies (USD) | Registration Tax (USD) | Fuel Tax (USD/L) | Carbon Tax ($/(gCO2/km)) | Fuel Economy Standard | Kick-Start Program | Biofuel Mandate |

|---|---|---|---|---|---|---|---|---|

| Baseline scenario | 0 | 0 | 0 | 0 | 0 | N/A | N/A | N/A |

| Scenario 1 | Up to 1200 | Up to 9000 | Up to 300 | 1.2 | 20 | N/A | 0.3% | N/A |

| Scenario 2 | Up to 1200 | Up to 12,000 | Up to 300 | 1.2 | 40 | 20 km/L | 1.5% | N/A |

| Scenario 3 | Up to 1200 | Up to 15,000 | Up to 300 | 1.2 | 40 | 20 km/L | 3% | 20% |

| Japan | Vehicle Tax (USD) | EV Subsidies (USD) | Registration Tax (USD) | Fuel Tax (USD/L) | Carbon Tax ($/(gCO2/km)) | Fuel Economy Standard | Kick-Start Program | Biofuel Mandate |

|---|---|---|---|---|---|---|---|---|

| Baseline scenario | 0 | 0 | 0 | 0 | 0 | N/A | N/A | N/A |

| Scenario 1 | Up to 1200 | Up to 9,000 | Up to 300 | 1.2 | 20 | N/A | 0.3% | N/A |

| Scenario 2 | Up to 1200 | Up to 12,000 | Up to 300 | 1.2 | 40 | 20 km/L | 1.5% | N/A |

| Scenario 3 | Up to 1200 | Up to 15,000 | Up to 300 | 1.2 | 40 | 20 km/L | 3% | 20% |

| Korea | Vehicle Tax (USD) | EV Subsidies (USD) | Registration Tax (USD) | Fuel Tax (USD/L) | Carbon Tax ($/(gCO2/km)) | Fuel Economy standard | Kick-Start Program | Biofuel Mandate |

|---|---|---|---|---|---|---|---|---|

| Baseline scenario | 0 | 0 | 0 | 0 | 0 | N/A | N/A | N/A |

| Scenario 1 | Up to 1200 | Up to 9000 | Up to 300 | 1.2 | 20 | N/A | 0.3% | N/A |

| Scenario 2 | Up to 1200 | Up to 12,000 | Up to 300 | 1.2 | 40 | 20 m/L | 1/5% | N/A |

| Scenario 3 | Up to 1200 | Up to 15,000 | Up to 300 | 1.2 | 40 | 20 m/L | 3% | 20% |

| Taiwan | Vehicle Tax (USD) | EV Subsidies (USD) | Registration Tax (USD) | Fuel Tax (USD/L) | Carbon Tax ($/(gCO2/km)) | Fuel Economy Standard | Kick-Start Program | Biofuel Mandate |

|---|---|---|---|---|---|---|---|---|

| Baseline scenario | 0 | 0 | 0 | 0 | 0 | N/A | N/A | N/A |

| Scenario 1 | Up to 1200 | Up to 9000 | Up to 300 | 1.2 | 20 | N/A | 0.3% | N/A |

| Scenario 2 | Up to 1200 | Up to 12,000 | Up to 300 | 1.2 | 40 | 20 km/L | 1.5% | N/A |

| Scenario 3 | Up to 1200 | Up to 15,000 | Up to 300 | 1.2 | 40 | 20 km/L | 3% | 20% |

Appendix C. Sensitivity Analysis

- Learning rates for the EVs. We did not vary the learning rate for conventional petrol and diesel cars because the learning for the mature technologies is insignificant;

- Consumer discount rates;

- All γi values simultaneously; (for all vehicle types);

- The fuel prices.

| Country | Variations in Key Parameters | Emissions | Technology Shares | |||||

|---|---|---|---|---|---|---|---|---|

| CO2 | Petrol Car | Diesel Car | Hybrid | CNG | EV | Motorcycles | ||

| China | Learning rate + 5% | −2.10% | −2.48% | −1.04% | 1.20% | 0.00% | 2.32% | 0.00% |

| Learning rate − 5% | 3.90% | 6.10% | 0.12% | 0.00% | 0.00% | −6.22% | 0.00% | |

| Discount rate + 10% | 1.80% | 1.38% | 0.00% | −1.04% | 2.45% | −2.80% | 0.00% | |

| Discount rate − 10% | −3.74% | −2.35% | −0.82% | 8.13% | -8.69% | 3.74% | −0.34% | |

| All Gamma values + 20% | 2.90% | 2.00% | 0.00% | 0.10% | −1.40% | −0.70% | 0.00% | |

| All Gamma values − 20% | 1.40% | 1.20% | 0.00% | 0.00% | −0.85% | −0.35% | 0.00% | |

| Fuel price + 20% | −5.90% | −6.61% | −0.01% | 3.07% | 3.40% | −0.55% | 0.70% | |

| Fuel price − 20% | 3.78% | 4.98% | 0.02% | 0.80% | −4.95% | −0.60% | −0.25% | |

| Japan | Learning rate + 5% | −3.45% | −4.67% | 0.00% | 3.57% | 0.00% | 1.10% | 0.00% |

| Learning rate − 5% | 0.95% | 2.00% | 0.00% | −0.45% | 0.00% | −1.55% | 0.00% | |

| Discount rate + 10% | 4.52% | 2.90% | 0.00% | −2.40% | 0.00% | −0.50% | 0.00% | |

| Discount rate − 10% | −3.56% | −3.10% | 0.00% | 2.10% | 0.00% | 1.00% | 0.00% | |

| All Gamma values + 20% | −2.22% | −2.37% | 0.00% | 2.39% | 0.00% | −0.02% | 0.00% | |

| All Gamma values − 20% | 0.02% | 0.01% | 0.00% | −0.02% | 0.00% | 0.00% | 0.00% | |

| Fuel price + 20% | −3.22% | −2.03% | 0.00% | 2.03% | 0.00% | 0.00% | 0.00% | |

| Fuel price − 20% | 3.31% | 3.77% | 0.00% | −3.55% | 0.00% | −0.22% | 0.00% | |

| Korea | Learning rate + 5% | −4.52% | −5.60% | 0.00% | 4.64% | 0.00% | 0.97% | 0.00% |

| Learning rate − 5% | 2.34% | 2.76% | −0.30% | −2.27% | 0.00% | −0.19% | 0.00% | |

| Discount rate + 10% | 4.80% | 3.60% | −2.00% | −1.70% | 0.00% | −0.50% | 0.60% | |

| Discount rate − 10% | −3.20% | 2.92% | 0.00% | −3.74% | 0.00% | 0.82% | 0.00% | |

| All Gamma values + 20% | 0.02% | 0.00% | 0.00% | 0.01% | 0.00% | 0.00% | 0.00% | |

| All Gamma values − 20% | 0.05% | 0.00% | −0.01% | 0.00% | 0.00% | 0.00% | 0.01% | |

| Fuel price + 20% | −0.31% | −0.11% | 0.00% | 0.00% | 0.00% | −0.06% | 0.17% | |

| Fuel price − 20% | 0.22% | 0.12% | 0.00% | 0.00% | 0.00% | −0.06% | −0.06% | |

| Taiwan | Learning rate + 5% | −0.02% | −0.01% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% |

| Learning rate − 5% | 0.01% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | |

| Discount rate + 10% | 1.20% | −1.10% | 0.00% | 0.00% | 0.00% | 0.00% | 1.10% | |

| Discount rate − 10% | −0.49% | −0.41% | 0.55% | 0.00% | 0.00% | 0.00% | −0.14% | |

| All Gamma values + 20% | 0.00% | −0.25% | 0.00% | 0.00% | 0.00% | 0.00% | 0.25% | |

| All Gamma values − 20% | −0.57% | 0.07% | 0.07% | 0.00% | 0.00% | 0.00% | −0.14% | |

| Fuel price + 20% | −5.21% | −6.00% | 0.00% | 0.54% | 0.00% | 1.76% | 3.70% | |

| Fuel price − 20% | 8.54% | 4.17% | 0.00% | 1.21% | 0.00% | −1.61% | −3.77% | |

| Country | Variations in Key Parameters | Emissions | Technology Shares | |||||

|---|---|---|---|---|---|---|---|---|

| CO2 | Petrol Car | Diesel Car | Hybrid | CNG | EV | Motorcycles | ||

| China | Learning rate + 5% | −1.64% | −3.16% | 0.00% | 0.16% | 0.00% | 2.99% | 0.00% |

| Learning rate − 5% | 1.54% | 2.74% | 0.00% | 0.00% | 0.00% | −2.73% | 0.00% | |

| Discount rate + 10% | 3.98% | 2.15% | 0.01% | −1.62% | 3.81% | −4.35% | 0.00% | |

| Discount rate − 10% | −4.10% | −2.08% | −1.00% | 1.74% | −2.84% | 4.55% | −0.37% | |

| All Gamma values + 20% | 1.85% | 1.88% | 0.00% | 0.09% | −1.32% | −0.68% | 0.02% | |

| All Gamma values − 20% | 1.10% | 1.35% | 0.00% | 0.00% | −0.95% | −0.47% | 0.08% | |

| Fuel price + 20% | −1.74% | −1.50% | 0.00% | 0.02% | 0.00% | 1.06% | 0.42% | |

| Fuel price − 20% | 1.98% | 1.83% | 0.00% | −0.02% | 0.00% | −1.65% | −0.15% | |

| Japan | Learning rate + 5% | −3.70% | −3.99% | 0.00% | 3.05% | 0.00% | 0.94% | 0.00% |

| Learning rate − 5% | 1.90% | 1.71% | 0.00% | −0.40% | 0.00% | −1.31% | 0.00% | |

| Discount rate + 10% | 3.80% | 4.20% | 0.00% | −3.70% | 0.00% | −0.50% | 0.00% | |

| Discount rate − 10% | −1.42% | −1.66% | 0.00% | 1.90% | 0.00% | −0.24% | 0.00% | |

| All Gamma values + 20% | −0.44% | −0.38% | 0.00% | 2.12% | 0.00% | −1.74% | 0.00% | |

| All Gamma values − 20% | 0.55% | 1.37% | 0.00% | 0.00% | 0.00% | −1.37% | 0.00% | |

| Fuel price + 20% | −5.86% | −1.26% | 0.00% | 7.00% | 0.00% | −5.74% | 0.00% | |

| Fuel price − 20% | 6.90% | 7.28% | 0.00% | −4.20% | 0.00% | −3.08% | 0.00% | |

| Korea | Learning rate + 5% | −1.85% | −8.06% | −0.21% | 6.53% | 0.00% | 1.83% | 0.00% |

| Learning rate − 5% | 3.61% | 3.35% | 0.02% | −2.65% | 0.00% | −0.72% | 0.00% | |

| Discount rate + 10% | 7.45% | 6.42% | 0.41% | −3.70% | 0.00% | −3.64% | 0.51% | |

| Discount rate − 10% | −4.33% | −3.15% | −1.96% | 5.58% | 0.00% | −0.27% | −0.20% | |

| All Gamma values + 20% | 1.33% | 1.64% | 0.00% | 0.08% | 0.00% | −1.73% | 0.01% | |

| All Gamma values − 20% | 0.39% | 0.24% | 0.00% | −2.45% | 0.00% | 2.21% | 0.00% | |

| Fuel price + 20% | −10.50% | −9.17% | 4.00% | −1.38% | 0.00% | 6.29% | 0.26% | |

| Fuel price − 20% | 12.45% | 11.50% | −5.02% | 1.73% | 0.00% | −8.12% | −0.09% | |

| Taiwan | Learning rate + 5% | −0.02% | −0.01% | 0.00% | 0.00% | 0.00% | 0.14% | −0.13% |

| Learning rate − 5% | 0.40% | 0.10% | 0.00% | 0.00% | 0.00% | −0.22% | 0.12% | |

| Discount rate + 10% | 1.60% | 0.16% | 0.00% | −0.37% | 0.00% | −0.86% | 1.07% | |

| Discount rate − 10% | −0.54% | −0.47% | 0.00% | 2.22% | 0.00% | −1.61% | −0.14% | |

| All Gamma values + 20% | −0.34% | −0.27% | 0.26% | 0.43% | 0.00% | −0.48% | 0.06% | |

| All Gamma values − 20% | −0.05% | −0.04% | 0.14% | −0.14% | 0.00% | 0.07% | −0.03% | |

| Fuel price + 20% | −7.98% | −8.53% | −3.31% | # | 0.00% | 3.21% | 5.22% | |

| Fuel price − 20% | 6.65% | 0.67% | 0.00% | 0.13% | 0.00% | −4.80% | 4.00% | |

| Country | Variations in Key Parameters | Emissions | Technology Shares | |||||

|---|---|---|---|---|---|---|---|---|

| CO2 | Petrol Car | Diesel Car | Hybrid | CNG | EV | Motorcycles | ||

| China | Learning rate + 5% | −4.80% | −3.74% | 0.00% | 0.00% | 0.00% | 3.74% | 0.00% |

| Learning rate − 5% | 3.41% | 2.63% | 0.00% | 0.00% | 0.00% | −2.63% | 0.00% | |

| Discount rate + 10% | 3.10% | 3.20% | 0.00% | 0.04% | 0.00% | −3.65% | 0.41% | |

| Discount rate − 10% | −4.77% | −5.35% | 0.00% | 0.00% | 0.00% | 5.09% | −0.42% | |

| All Gamma values + 20% | 1.60% | 1.11% | 0.00% | 2.26% | −2.24% | −1.35% | 0.22% | |

| All Gamma values − 20% | 2.04% | 0.91% | 0.00% | 0.00% | −0.67% | −0.24% | 0.00% | |

| Fuel price + 20% | −8.10% | −7.80% | 0.01% | 2.10% | −2.00% | 7.32% | 0.37% | |

| Fuel price − 20% | 4.90% | 3.21% | −0.01% | −2.60% | 1.33% | −1.80% | −0.13% | |

| Japan | Learning rate + 5% | −2.45% | −5.65% | 0.00% | 4.32% | 0.00% | 1.33% | 0.00% |

| Learning rate − 5% | 4.24% | 3.42% | 0.02% | −2.75% | 0.00% | −0.69% | 0.00% | |

| Discount rate + 10% | 5.21% | 3.43% | 0.00% | −4.21% | 0.00% | 0.77% | 0.00% | |

| Discount rate − 10% | −3.41% | −4.27% | 0.00% | 6.10% | 0.00% | −1.83% | 0.00% | |

| All Gamma values + 20% | −0.32% | −0.37% | 0.00% | 1.79% | 0.00% | −1.42% | 0.00% | |

| All Gamma values − 20% | −1.40% | −0.92% | 0.00% | −0.25% | 0.00% | 1.17% | 0.00% | |

| Fuel price + 20% | −4.50% | −4.05% | 0.10% | 6.10% | 0.00% | −2.15% | 0.00% | |

| Fuel price − 20% | 5.96% | 3.83% | 0.09% | 2.11% | 0.00% | −6.03% | 0.00% | |

| Korea | Learning rate + 5% | −2.91% | −4.12% | 0.12% | 2.10% | 0.00% | 1.30% | 0.60% |

| Learning rate − 5% | 4.28% | 1.86% | 0.01% | −0.23% | 0.00% | −1.29% | −0.35% | |

| Discount rate + 10% | 6.45% | 4.29% | 0.98% | 0.35% | 0.00% | −5.61% | 0.00% | |

| Discount rate − 10% | −4.96% | −4.19% | −0.63% | 6.76% | 0.00% | −0.70% | −1.24% | |

| All Gamma values + 20% | 2.85% | 2.16% | 0.00% | 0.11% | 0.00% | −2.29% | 0.02% | |

| All Gamma values − 20% | 2.80% | 0.32% | 0.00% | −3.24% | 0.00% | 2.92% | 0.00% | |

| Fuel price + 20% | −5.79% | -7.00% | 3.00% | −1.24% | 0.00% | 4.88% | 0.36% | |

| Fuel price − 20% | 12.41% | 11.34% | 0.01% | −3.96% | 0.00% | -7.26% | −0.13% | |

| Taiwan | Learning rate + 5% | −3.04% | −2.85% | 0.00% | 0.00% | 0.00% | 3.08% | −0.23% |

| Learning rate − 5% | 2.86% | 2.69% | 0.00% | 0.00% | 0.00% | −2.90% | 0.21% | |

| Discount rate + 10% | 3.14% | 0.27% | 0.00% | 0.67% | 0.00% | −1.50% | 0.56% | |

| Discount rate − 10% | −2.53% | −0.83% | 0.00% | 3.87% | 0.00% | −2.81% | −0.24% | |

| All Gamma values + 20% | −0.34% | −0.28% | 0.29% | 0.48% | 0.00% | −0.54% | 0.05% | |

| All Gamma values − 20% | −0.27% | −0.05% | 0.16% | −0.16% | 0.00% | 0.07% | −0.03% | |

| Fuel price + 20% | −6.55% | −8.44% | 0.00% | 4.33% | 0.00% | 4.11% | 4.38% | |

| Fuel price − 20% | 9.21% | 7.34% | 0.00% | −3.77% | 0.00% | −3.58% | 3.36% | |

| Country | Variations in Key Parameters | Emissions | Technology Shares | |||||

|---|---|---|---|---|---|---|---|---|

| CO2 | Petrol Car | Diesel Car | Hybrid | CNG | EV | Motorcycles | ||

| China | Learning rate + 5% | −6.24% | −6.58% | 0.00% | 0.00% | 0.00% | 6.59% | 0.00% |

| Learning rate − 5% | 4.43% | 4.41% | 0.00% | 0.00% | 0.00% | −4.41% | 0.00% | |

| Discount rate + 10% | 4.10% | 3.75% | 0.00% | 0.05% | 0.00% | −3.80% | 0.00% | |

| Discount rate − 10% | -8.14% | −4.69% | 0.00% | 0.00% | 0.00% | 5.01% | 0.00% | |

| All Gamma values + 20% | 0.91% | 0.74% | 0.00% | 0.03% | 0.00% | −0.88% | 0.11% | |

| All Gamma values − 20% | 0.81% | 0.70% | 0.00% | 0.03% | 0.00% | −0.73% | 0% | |

| Fuel price + 20% | −9.11% | −10.92% | 0.01% | 1.17% | −2.80% | 12.50% | 0.00% | |

| Fuel price − 20% | 5.09% | 2.75% | −0.01% | −2.07% | 1.06% | −1.73% | 0.00% | |

| Japan | Learning rate + 5% | −4.09% | −6.85% | 0.00% | 3.87% | 0.00% | 2.98% | 0.00% |

| Learning rate − 5% | 7.12% | 2.52% | 0.02% | −1.75% | 0.00% | −0.78% | 0.00% | |

| Discount rate + 10% | 6.47% | 4.12% | 0.00% | −5.05% | 0.00% | 0.93% | 0.00% | |

| Discount rate − 10% | −4.02% | −5.10% | 0.00% | 0.20% | 0.00% | 4.90% | 0.00% | |

| All Gamma values + 20% | −0.99% | −0.21% | 0.00% | 0.93% | 0.00% | −0.72% | 0.00% | |

| All Gamma values − 20% | −0.26% | −0.16% | 0.00% | 0.45% | 0.00% | −0.29% | 0.00% | |

| Fuel price + 20% | −5.34% | −5.36% | 0.00% | −1.45% | 0.00% | 6.8100% | 0.00% | |

| Fuel price − 20% | 4.58% | 3.41% | 0.08% | 1.88% | 0.00% | −5.37% | 0.00% | |

| Korea | Learning rate + 5% | −3.74% | −2.03% | 0.18% | 0.73% | 0.00% | 2.66% | 0.00% |

| Learning rate − 5% | 3.66% | 2.46% | 0.02% | 0.25% | 0.00% | −2.73% | 0.00% | |

| Discount rate +10% | 3.43% | 4.13% | 0.94% | −0.02% | 0.00% | −5.41% | 0.00% | |

| Discount rate − 10% | −4.65% | −3.33% | −0.50% | 5.37% | 0.00% | −1.41% | 0.00% | |

| All Gamma values + 20% | −0.05% | −0.03% | 0.24% | 0.59% | 0.00% | −0.80% | 0.00% | |

| All Gamma values − 20% | 0.34% | 0.04% | −0.29% | −0.97% | 0.00% | 0.98% | 0.25% | |

| Fuel price + 20% | −8.57% | -10.29% | 4.41% | −1.29% | 0.00% | 6.72% | 0.00% | |

| Fuel price − 20% | 15.22% | 17.92% | 0.02% | −6.25% | 0.00% | −11.48% | 0.00% | |

| Taiwan | Learning rate + 5% | −5.20% | −2.80% | 0.00% | 0.00% | 0.00% | 5.00% | −2.20% |

| Learning rate − 5% | 3.40% | 2.83% | 0.00% | 0.00% | 0.00% | −4.63% | 1.80% | |

| Discount rate + 10% | 1.90% | 0.59% | 0.00% | 0.94% | 0.00% | −1.53% | 0.00% | |

| Discount rate − 10% | −2.54% | −1.34% | 0.00% | 6.28% | 0.00% | −3.97% | 0.00% | |

| All Gamma values + 20% | −1.65% | −0.52% | 0.59% | 0.89% | 0.00% | −1.01% | 0.00% | |

| All Gamma values − 20% | −0.67% | −0.39% | 0.61% | 0.88% | 0.00% | −1.06% | 0.00% | |

| Fuel price + 20% | −4.87% | −5.45% | 0.00% | 0.51% | 0.00% | 4.39% | 0.54% | |

| Fuel price − 20% | 6.07% | 5.72% | 0.00% | −2.93% | 0.00% | −2.46% | −0.33% | |

References

- IPCC. Mitigation of Climate Change. Contribution of Working Group III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change; University of Cambridge: Cambridge, UK, 2014. [Google Scholar]

- Matsuhashi, K.; Ariga, T. Estimation of passenger car CO2 emissions with urban population density scenarios for low carbon transportation in Japan. IATSS Res. 2016, 39, 117–120. [Google Scholar] [CrossRef]

- Yan, X.; Crookes, R. Energy demand and emissions from road transportation vehicles in China. Prog. Energy Combust. Sci. 2010, 36, 651–676. [Google Scholar] [CrossRef]

- Kemp, R.; Schot, J.; Hoogma, R. Regime shifts to sustainability through processes of niche formation: The approach of strategic niche management. Technol. Anal. Strateg. Manag. 1998, 10, 175–198. [Google Scholar] [CrossRef]

- Ko, A.; Myung, C.; Park, S.; Kwon, S. Scenario-based CO2 emissions reduction potential and energy use in Republic of Korea’s passenger vehicle fleet. Transp. Res. Part A Policy Pract. 2014, 59, 346–356. [Google Scholar] [CrossRef]

- Paltsev, S.; Chen, Y.; Karplus, V.; Kishimoto, P.; Reilly, J.; Löschel, A.; von Graevenitz, K.; Koesler, S. Reducing CO2 from cars in the European Union. Transportation 2016, 45, 1–23. [Google Scholar] [CrossRef]

- Oshiro, K.; Masui, T. Diffusion of low emission vehicles and their impact on CO2 emission reduction in Japan. Energy Policy 2015, 81, 215–225. [Google Scholar] [CrossRef]

- Wang, H.; Ou, X.; Zhang, X. Mode, technology, energy consumption, and resulting CO2 emissions in China’s transport sector up to 2050. Energy Policy 2017, 109, 719–733. [Google Scholar] [CrossRef]

- Fullerton, D.; Gan, L.; Hattori, M. A model to evaluate vehicle emission incentive policies in Japan. Environ. Econ. Policy Stud. 2015, 17, 79–108. [Google Scholar] [CrossRef]

- Mercure, J.; Lam, A. The effectiveness of policy on consumer choices for private road passenger transport emissions reductions in six major economies. Environ. Res. Lett. 2015, 10, 064008. [Google Scholar] [CrossRef]

- Gong, H.; Wang, M.; Wang, H. New energy vehicles in China: Policies, demonstration, and progress. Mitig. Adapt. Strateg. Glob. Chang. 2013, 18, 207–228. [Google Scholar] [CrossRef]

- Kitano, T. Disguised Protectionism? Environmental Policy in the Japanese Car Market; Research Institute of Economy, Trade and Industry: Tokyo, Japan, 2013. [Google Scholar]

- Rutherford, D. Hybrids break into the Japanese market (July 2015 update). The International Council on Clean Transportation (ICCT). Available online: https://www.theicct.org/blog/staff/hybrids-break-japanese-market-july-2015-update (accessed on 28 July 2015).

- Iino, F.; Lim, A. Developing Asia’s Competitive Advantage in Green Products: Learning from the Japanese Experience. Available online: https://www.adb.org/publications/developing-asias-competitive-advantage-green-products-learning-japanese-experience (accessed on 28 July 2015).

- Rogers, E. Diffusion of Innovations; Simon and Schuster: New York, NY, USA, 2010. [Google Scholar]

- Arthur, W. Competing technologies, increasing returns, and lock-in by historical events. Econ. J. 1989, 99, 116–131. [Google Scholar] [CrossRef]

- Liao, F.; Molin, E.; van Wee, B. Consumer preferences for electric vehicles: A literature review. Transp. Rev. 2017, 37, 252–275. [Google Scholar] [CrossRef]

- Chanaron, J. Automobiles: A static technology, a “wait-and-see” industry? Int. J. Technol. Manag. 1998, 16, 595–630. [Google Scholar] [CrossRef]

- Mercure, J. FTT: Power: A global model of the power sector with induced technological change and natural resource depletion. Energy Policy 2012, 48, 799–811. [Google Scholar] [CrossRef]

- Anandarajah, G.; McDowall, W.; Ekins, P. Decarbonising road transport with hydrogen and electricity: Long term global technology learning scenarios. Int. J. Hydrog. Energy 2013, 38, 3419–3432. [Google Scholar] [CrossRef]

- Weiss, M.; Patel, M.; Junginger, M.; Perujo, A.; Bonnel, P.; van Grootveld, G. On the electrification of road transport—Learning rates and price forecasts for hybrid-electric and battery-electric vehicles. Energy Policy 2012, 48, 374–393. [Google Scholar] [CrossRef]

- Sagar, A.; van der Zwaan, B. Technological innovation in the energy sector: R&D, deployment, and learning-by-doing. Energy Policy 2006, 34, 2601–2608. [Google Scholar]

- Pollitt, H.; Mercure, J. The role of money and the financial sector in energy-economy models used for assessing climate and energy policy. Clim. Policy 2018, 18, 184–197. [Google Scholar] [CrossRef]

- Kaldor, N. A model of economic growth. Econ. J. 1957, 67, 591–624. [Google Scholar] [CrossRef]

- Mercure, J.; Pollitt, H.; Bassi, A.; Viñuales, J.; Edwards, N. Modelling complex systems of heterogeneous agents to better design sustainability transitions policy. Glob. Environ. Chang. 2016, 37, 102–115. [Google Scholar] [CrossRef]

- Lee, S.; Chewpreecha, U.; Pollitt, H.; Kojima, S. An economic assessment of carbon tax reform to meet Japan’s NDC target under different nuclear assumptions using the E3ME model. Environ. Econ. Policy Stud. 2018, 20, 411–429. [Google Scholar] [CrossRef]

| Country or Region | Target Year | Unadjusted Fleet Target/Measure (L/100km) | Structure | Test Cycle |

|---|---|---|---|---|

| EU | 2015 2021 | 5.6 4.09 | Weight-based average | NEDC |

| China | 2015 2020 (proposed) | 6.9 5 | Weight-class based per vehicle and corporate average | NEDC |

| US | 2016 2025 | 6.5 4.19 | FP-based corporate average | US combined |

| Japan | 2015 2020 | 5.95 4.93 | Weight-class based corporate average | JC08 |

| Brazil | 2017 | 5.32 | Weight-based corporate average | US combined |

| India | 2016 2021 | 5.6 4.87 | Weight-based corporate average | NEDC for low-powered vehicle |

| Korea | 2015 | 5.88 | Weight-based corporate average | US combined |

| Mexico | 2016 | 5.99 | FB-based corporate average | US combined |

| Criteria\Phase | Phase 1 | Phase 2 | |

|---|---|---|---|

| Target market | Private | Public/private | |

| Subsidy duration | 2010–2012 | 2013–2015 | |

| Subsidy scope | Plug-in hybrid electric vehicles (PHEVs) Battery electric vehicles (BEVs) | Plug-in hybrid electric vehicles (PHEVs) Battery electric vehicles (BEVs) Fuel cell electric vehicles (FCEVs) | |

| Subsidy standard | HEV | - | - |

| PHEV | 3000 RMB/kWh | 35,000 RMB (range ≥ 50 km) | |

| BEV | 3000 RMB/kWh | 35,000 RMB (80 ≤ range < 150 km) 50,000 RMB (150 ≤ range < 250 km) 60,000 RMB (range ≥ 250 km) | |

| Phase-out mechanism | Not specified | 10% reduction in 2014 | |

| Pilot cities | Six cities | 28 cities and regions | |

| Type\Year | 2011 | 2012 | 2013 | 2014 | 2015 |

|---|---|---|---|---|---|

| EV | 0.056% | 0.074% | 0.082% | 0.227% | 1.192% |

| PHEV | 0.006% | 0.006% | 0.017% | 0.152% | 0.374% |

| Total | 0.056% | 0.081% | 0.098% | 0.379% | 1.57% |

| Type\Year | 2011 | 2012 | 2013 | 2014 | 2015 |

|---|---|---|---|---|---|

| EV | 0.635% | 0.847% | 1.201% | 1.504% | 1.908% |

| PHEV | 0.118% | 0.378% | 0.662% | 0.936% | 1.354% |

| FCV | <0.001% | <0.001% | <0.001% | 0.003% | 0.015% |

| Total | 0.753% | 1.225% | 1.862% | 2.444% | 3.227% |

| Policy Incentives | Model Representation | Examples of the Real-World Policy |

|---|---|---|

| Vehicle tax | Added/subtracted to the capital cost at the time of car purchases | Acquisition tax, EV rebates |

| Annual registration tax | Added to the annual costs summed to get the LCOT | Road tax |

| Carbon tax | Same as vehicle tax, this is a tax on expected (not yet emitted) CO2 emissions. The tax is proportional to fuel economy in the unit of USD/(gCO2/km) | Acquisition tax based on fuel economy |

| Fuel tax | Added to the fuel cost | Fuel tax (e.g., petrol tax, diesel tax) |

| Biofuel mandate | Biofuel is a certain percentage of liquid fuels | Biofuel mandate |

| Phase out regulation | The sale of lower efficiency liquid fuel vehicles is banned | Fuel economy standards |

| Kick-start program | A certain percentage of EVs are bought by someone or some institution (e.g., public or private institutions) as a policy or strategy. | Government-financed purchases |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lam, A.; Lee, S.; Mercure, J.-F.; Cho, Y.; Lin, C.-H.; Pollitt, H.; Chewpreecha, U.; Billington, S. Policies and Predictions for a Low-Carbon Transition by 2050 in Passenger Vehicles in East Asia: Based on an Analysis Using the E3ME-FTT Model. Sustainability 2018, 10, 1612. https://doi.org/10.3390/su10051612

Lam A, Lee S, Mercure J-F, Cho Y, Lin C-H, Pollitt H, Chewpreecha U, Billington S. Policies and Predictions for a Low-Carbon Transition by 2050 in Passenger Vehicles in East Asia: Based on an Analysis Using the E3ME-FTT Model. Sustainability. 2018; 10(5):1612. https://doi.org/10.3390/su10051612

Chicago/Turabian StyleLam, Aileen, Soocheol Lee, Jean-François Mercure, Yongsung Cho, Chun-Hsu Lin, Hector Pollitt, Unnada Chewpreecha, and Sophie Billington. 2018. "Policies and Predictions for a Low-Carbon Transition by 2050 in Passenger Vehicles in East Asia: Based on an Analysis Using the E3ME-FTT Model" Sustainability 10, no. 5: 1612. https://doi.org/10.3390/su10051612

APA StyleLam, A., Lee, S., Mercure, J. -F., Cho, Y., Lin, C. -H., Pollitt, H., Chewpreecha, U., & Billington, S. (2018). Policies and Predictions for a Low-Carbon Transition by 2050 in Passenger Vehicles in East Asia: Based on an Analysis Using the E3ME-FTT Model. Sustainability, 10(5), 1612. https://doi.org/10.3390/su10051612