1. Introduction

When considering the link between investments and policy in China’s power market, China’s energy regulators have been characterized by overlapping jurisdictions. China’s electricity sector consists of a mix of state and locally owned enterprises [

1]. The last major structural change occurred in 2002 with the dismantling of the State Power Corporation, resulting in competition in power generation and openness in energy investment. The government requires certain generators to take a certain share in the market, forcing them to sign contracts with end-users or retailers in annual or sometimes monthly forms to compete with each other. However, the electricity sector is not totally liberalized. Only limited competition has been introduced in electricity generation, and retail pricing is still under administrative regulation. The end-users do not have the autonomy to purchase power, and subsidies on power generation interfere with the development of the pricing system [

2]. Where the price signal has a limited role in allocating resources and investment, the business decision and profitability of listed power companies will likewise be affected by industrial policy issued during China’s power market reform. Thus, the stock price volatility will in part depend on the nature and extent of market reform, as well as the interaction between power market reform and the stock market.

China started to combine green energy and industrial policy in its power market reform in 2001, signaled by the Tenth Five-Year Plan which included price support scheme for electricity from renewable sources and subsidies in the push for the broader use of greener energy. Total power consumption in China has grown rapidly, especially from 2002 to 2011, during which the average growth rate of power consumption was more than 10%. The rapid growth in energy consumption and heavy reliance on coal have created serious environmental problems, including local air pollution and depletion of water resources. As air pollution caused by “PM (Particulate Matter) 2.5”, or fine particulate matter, has become a social problem, curbs on coal use as well as the expansion of clean energy use are recognized as urgent tasks. China also set the goal of peaking its CO2 emissions around 2030 in the “Paris Agreement”, which took effect in November 2016. In this agreement, China’s energy policy is responding to these changes in domestic and international circumstances, and therefore, continued political stress was imposed to reduce CO2 emissions.

The electricity sector provides an attractive context for our study for several reasons. Firstly, at least during the period of our study, there are distinctive groups of listed companies occupying the majority of market share that has been defined by academic scholars, business practitioners, and policymakers. For example, China’s electric power installed capacity was 1.06 billion kilowatts, among which the five major power groups (Huaneng, Datang, Guodian, Huadian, and Zhongdiantou) were 514 million kilowatts. Other central SOEs (such as Sanxia, Huarun, Guokai, Guanghe, Guohe, etc.) and local power groups accounted for 22.5%. The above-mentioned power generation enterprises accounted for 71.41% of the national installed capacity and most of them are listed in power stock price index (PSPI), and the Shanghai A-share Composite Index (SHCI).

Secondly, the industry is characterized by a sustained large-scale investment and steadily increasing demand between 2006 and 2012. As a result, price, capacity, and quality of service varies insignificantly during this period. Robust empirical evidence suggests that power market reform has affected power generation enterprises through electricity generation efficiency and market penetration of renewable energy. The majority of the empirical studies on the power market reform have focused on spillover effect on electricity generation efficiency; spillover on stock price has been understudied. This is unsatisfactory since not only are large sums of capital investment not easily reversible but also power companies face limited government funding supports for capacity expansion. Government funding only accounts for 5.5%. Around 54% of the funds were raised by firms’ own funds and outside investors during our sample period, and the ratio is even higher for established power companies.

Thirdly, China’s government was to spend $1.7 trillion between 2011 and 2015, in the form of investment, assistance for state-owned enterprises and bank loans. The stock price volatility of listed companies provides an opportunity to identify the policy responses to renewable energy industry at the investment level.

Finally, the power industry is heavily regulated, and detailed data on pricing, capacity, and quality is available at the firm level. The power industry has also been the subject of extensive academic research, which provides a benchmark for the current study.

In sum, with a rising demand for power generation, policies on power generation and consumption are likely to have a key bearing on the financial markets. At the same time, sudden structural breaks may affect the dynamics of stock prices. This study aims to investigate the interdependence between China’s stock market and the China’s power market during 2006–2012 (a substantial slowdown in the increase of primary energy consumption since 2012, with year-on-year increase remaining at 1.0% in 2015, and 1.4% in 2016), with careful consideration paid to the possibility of structural shifts in the mean and variance processes. We identify the impact of China’s power market reform on listed power companies’ performances and capacities to attract investment and explore what kind of reforms would be more suitable for China’s power industry development. Therefore, in the following studies, we address two significant issues: characteristics of stock price volatility of the listed power companies with structural breaks; and the impact of power industrial policy reform on stock price volatility.

This paper proceeds as follows.

Section 2 reviews the main studies and results regarding structure breaks in the process of stock price fluctuation, and the factors affecting stock price volatility. In

Section 3, we discuss the data used as well as variable selection.

Section 4 introduces methodologies, including: (1) the iterative cumulative sums of squares (ICSS) method for determining the structure break of stock price volatility; (2) generalized autoregressive conditional heteroskedastic (GARCH) model for analyzing the characteristics of stock price volatility; and (3) autoregressive distributed Lag (ARDL) model for studying the impact of power industrial policy reform on stock price volatility. We present the results and analysis in

Section 5 with conclusion and discussion in

Section 5.1 and

Section 5.2, respectively.

2. Literature Review

Structural break in stock price fluctuation is an active topic. Many studies have attempted to identify the most important event that precipitates structural breaks, such as macroeconomic events, reform policies, and crisis events. Many scholars considered the macroeconomic situation to be the most important factor [

2,

3]. For example, Chihoun and Mi-Ok found that firms with SEO (Seasoned Equity Offerings) have sustainable development in operational structural change [

4]. Fama argued that capital expenses, industrial production, gross national product (GNP), money supply, inflation and interest rates have a strong positive influence on stock price fluctuations [

5]. By using the iterated cumulative sums of squares (ICSS) algorithm, Hammoudeh and Li studied the characteristics of stock market volatility in the Arabian Gulf region, and they found that structural changes were usually caused by the impact of international events, for instance, the Asian Financial Crisis. They suggested that international events were the major origins of structural changes [

6]. Wang and Tomoe tested stock return data from 1994 to 2006 of five new European Union (EU) members and argued that reform in emerging stock markets, exchange rate policies and the financial crisis led to volatility. They also pointed out that many former studies did not consider the structure of the volatility, which resulted in overestimating volatility [

7]. Babikir et al. measured the Johannesburg Stock Exchange All-Share Index and found that structural breaks mainly stem from international financial crises; they argued that the presence of a structural breakpoint should be considered in forecasting stock market volatility, especially in the long term [

8].

Significant attention has been paid to the characteristics of fluctuations in China’s stock prices and the influential factors. Chen and Huang (2002) illustrated that asymmetry features existed in fluctuations in China’s stock market, meaning that the impact of negative information on stock price fluctuation was greater than that of positive information [

9]. Wang and Zhang indicated that China’s stock market had a long memory consistently, which meant that some unexpected events had a long-lag influence on stock price fluctuations and current risks would affect future risks continuously [

10]. There are different opinions about various characteristics across different stages in China’s stock market. Song and Jiang suggested that Chinese stock market volatility had poor stability, and the stratification of stock price volatility was hard to distinguish [

11]. Schwert related stock market volatility to the time-varying volatility of a variety of macroeconomic variables, including money growth, industrial production growth, and other measures of economic activity [

12]. Wang and Gao concluded that there were weak correlations among the Chinese stock market, inflation, money supply, and stock price volatility [

13]. Moreover, Wen et al. argued that there were relationships between oil prices, economic growth, money supply, inflation and Chinese stock market volatility by using data from 2002 to 2010 based on the multi-factor EGARCH (1, 1)-M model [

14]. Dong and Wang found a negative relationship between stock market volatility and economic growth in China by using data from 1993 to 2007 based on the Wavelet Transform method [

15]. Beltratti illustrated that the stock price volatility of the S&P 500 Index was affected by the volatility of economic and policy variables, and a positive relationship existed between economic growth and price volatility. Of particular interest [

16], Li and Fu studied factors affecting China’s power stock price and found that coal prices had a significant impact on power stock price fluctuations since thermal power was the largest share of the power industry in China [

17]. Zhao (2016) studied the impact of financial crisis on electricity demand in north China, and found electricity consumption, which affected stock value of electric enterprises and economic growth, was highly correlated [

18].

In a study literature on the general economy of power market reforms, Meng (2016) [

19] and Mou (2014) [

20] analyzed the efficiency of China’s thermal power plants. Mou (2014) found that there were generation efficiency disparities and generation-hour arrangement unfairness across plants [

20]. Meng (2016) claimed that reform caused a downshift to the “natural” generation efficiency curve of the thermal power industry [

19]. Zhu and Yan et al. (2017) [

21] and Zhang (2018) [

22] analyzed the impacts of renewable electricity promotion. They found that market reform not only promoted the penetration but also increased the utilization ratio of renewables significantly. Shang and Wei et al. (2016) found that market-oriented reforms decoupled China’s CO

2 emissions from total electricity generation [

23].

In summary, although there is significant literature on stock price volatility and its influencing factors, only a few studies deal with the stock price fluctuations of power companies (Li and Fu [

17], Teng [

24], Ming [

25]). In addition, studies on the characteristics of China’s power stock price volatility that consider structural breaks and the impact of power regulation on price volatility are scarce. In the related literature on the general economy of power market reforms, the majority of the empirical studies on the power market reform have focused on companies’ generation efficiency and CO

2 emission, spillover effect on the stock market has been understudied [

26,

27]. The contributions of this paper are twofold: first, our analysis is one of the few studies that examine the stock price volatility characteristics of listed power companies in China; and, second, we address the relationship between China’s power market reform and the relevant stock price volatility.

4. Results and Discussion

4.1. Structural Breaks of Stock Price Fluctuation

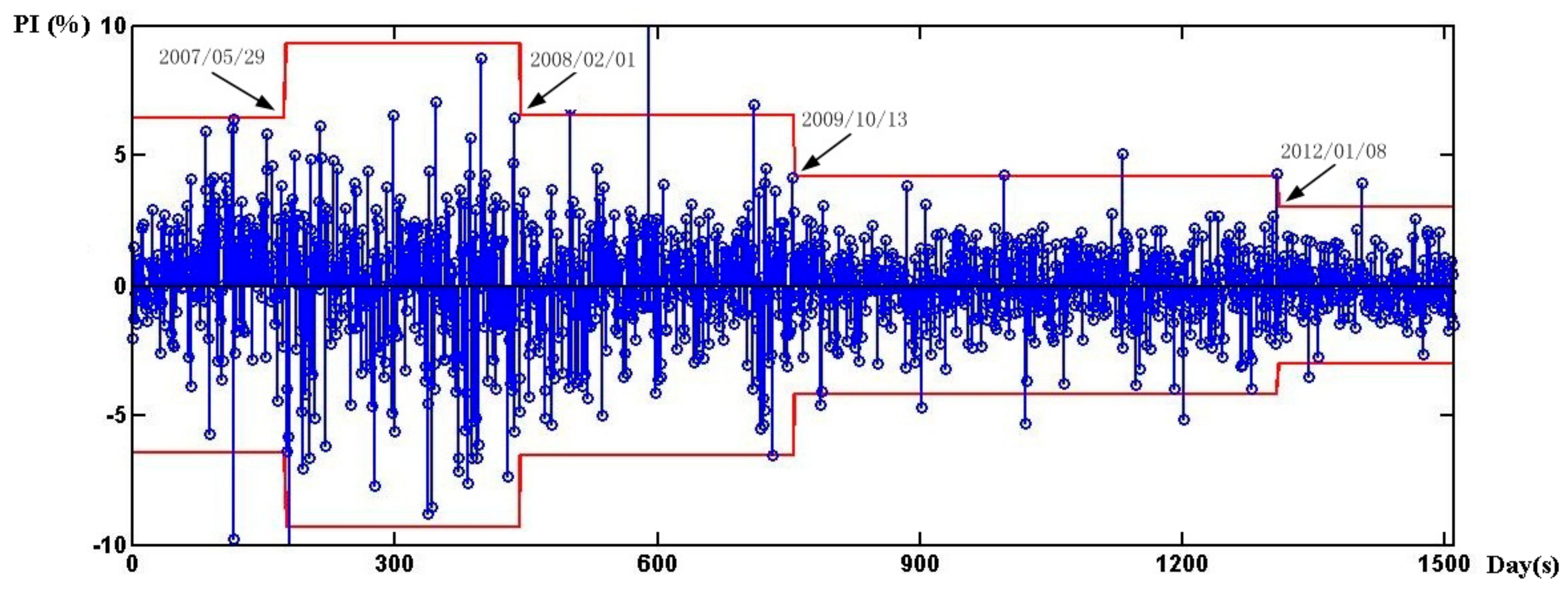

To better illustrate the characteristics of the fluctuation of the Power Stock Price Index (PSPI), we also analyzed structural breaks of the general stock price (Shanghai A-share Composite index: SHCI) and compared the structural break differences between these two stock prices. Results of these structural breaks for PSPI are shown in

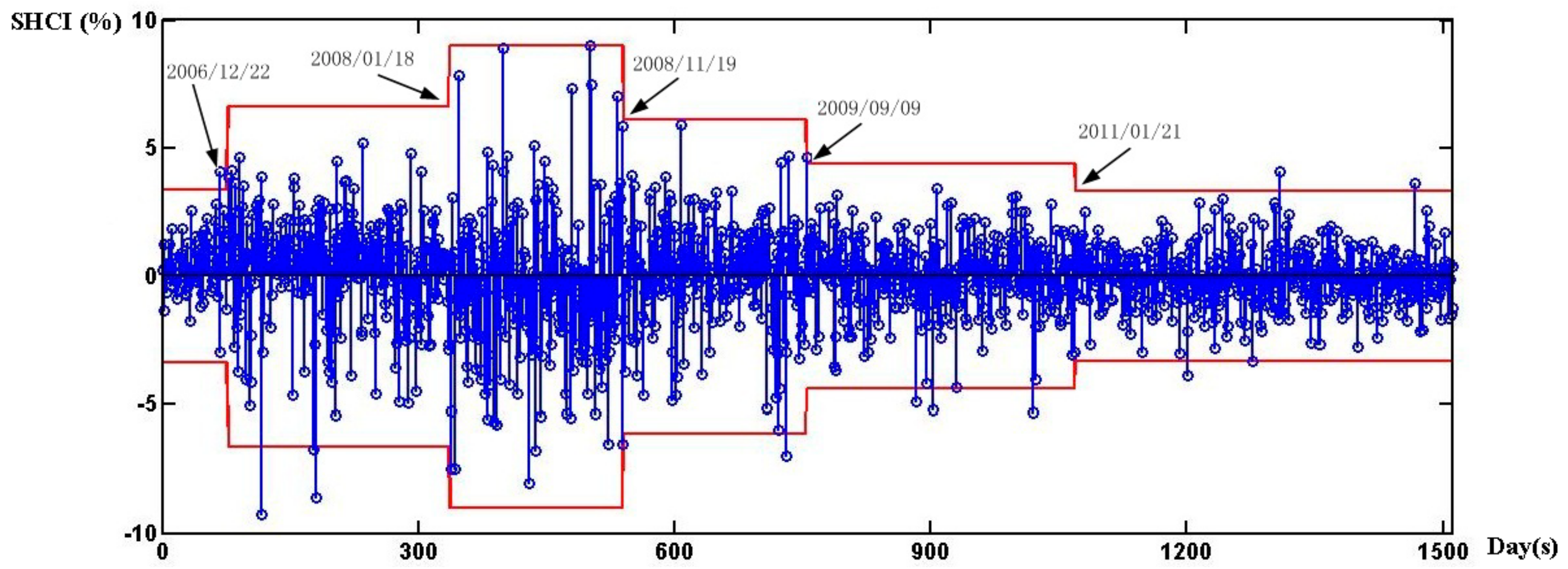

Figure 1. Results of the structural breaks for SHCI are shown in

Figure 2 (the x-coordinate 0 represents 30 August 2006, the x-coordinate 1500 refers to the 1500th day from the start date 0, since the trading day is inconsistent with calendar time). The blue line represents daily return of PSPI. The red line represents ±3 standard deviation bands in different sub-samples.

Figure 1 indicates the structure break dates for PSPI are 29 May 2007, 1 February 2008, 13 October 2009, and 18 January 2012, which divide the whole sample into five sub-samples.

Figure 2 indicates the structure break dates for SHCI are 22 December 2006, 18 January 2008, 19 November 2008, 9 September 2009, and 21 January 2011, which divide the whole sample into six sub-samples. Based on the results in

Figure 1 and

Figure 2, a few important findings are made.

Firstly, regarding the frequency of structural breaks, we found that frequency of structural breaks differs between the PSPI (four times) and SHCI (five times), which means that PSPI has experienced fewer structural changes than the SHCI. It also implies that the PSPI is exposed to volatility related to industry events or policy announcements apart from the common elements affecting the general stock market.

with

As the analysis is based on the identification of the break dates for the stock prices volatility, a further robust check is needed, given the uncertainty involved in the estimation of the break date. For that reason, we implement the approach proposed by Hawkins and Zamba (2005) [

42]. This approach has been recently implemented in economic data by Dergiades et al. (2017) [

43]. We follow a similar strategy to examine the in-control hypothesis and monitor changes in variance when the sample is updated with policy shock. We calculate

Gmax,n statistic based on Equations (11) and (12) and compare it to a critical limit introduced in Hawkins and Zamba (2005) [

42]. The results are shown in

Table 2.

Gmax,n statistic goes beyond the critical limit at the break dates estimated, which support our hypothesis that variance change may occur when policy announced. The break dates for the stock prices volatility out of control is consistent with what we derive with Iterative Cumulative Sum of Squares approach.

Secondly, from the time perspective of structural breaks, we found that a large difference exists between the PSPI and the SHCI, which means that events in the power industry have a greater impact on fluctuations in the PSPI compared with the macroeconomic environment. The specific date of breakpoints identified by the ICSS algorithm and the corresponding power industrial policies are shown in table.

Table 2 shows that, at the first break point on 29 May 2007, the document of

Management of Tariff and Facilities of Desulfurization for Coal-fired Power Units was issued, which implied the operational cost of power generation would increase and the risk of investment in power stock market would increase. As such, the fluctuation of the PSPI increased. At the second breakpoint on 1 February 2008, a policy restricting employees from increasing their share in power generation enterprises was issued. This policy would reduce the flow of funds into the CLPC; hence, the fluctuation of the PSPI took a downward trend. The third break of the PSPI took place on 13 October 2009, when the National Development and Reform Commission and State Electricity Regulatory Commission regulated the power trading price. The policy stipulated that the on-grid power price within a province must be consistent with the standard power price of the province; however, power trading prices across provinces or regions have relative flexibility. The last structure breakpoint is on 13 October 2009, when the State Electricity Regulatory Commission (SERC) issued the document,

Drawing the Roadmap for Deepened Reform for Power Development in the Twelfth Five-Year Plan Period. This document stipulates that the industry’s transmission and distribution businesses will be separated into two parts, and large power consumers will be permitted to purchase power directly from power generators; meanwhile, the market will decide the power price. The third and fourth power regulations in

Table 2 provided the signal that China’s power market would move in a more orderly and standardized direction, thus decreasing the anticipated risk of investment in this market. Accordingly, the fluctuation of the PSPI decreased.

In addition to the four power regulation policies presented in

Table 2, some other important power regulation policies (shown in

Table 3) were issued over this study period. Distinct from the policies in

Table 2, those in

Table 4 do not contribute to the structural breaks in China’s power stock price. Of the six policies in

Table 3, three relate to renewable energy development. Currently, the proportion of renewable energy generation contributes only about 2% of the total power. As such, the policies related to renewable energy do not have a very significant impact on the power stock market.

One in the six policies calls for shutting down small thermal power units. This measure can improve the operating efficiency of power generators; on the other hand, the work itself will increase operational costs in the short run. Hence, it does not have an important impact on power stock price fluctuation.

The policy of price intervention of coal used by power generation units should have an important effect on power stock price fluctuation. However, because it is only a “temporary” price intervention, the effect is not statistically significant.

The most recent policy issued by the National Energy Board on 18 June 2012, is the Proposals on Encouraging and Guiding Private Capital Flowing into Energy Fields. This document stipulated that private investment in energy sectors, such as in power plant construction and industrial upgrading fields, was stimulated. It is beyond any doubt that the introduction of private investment in power fields will promote China’s power industry. However, it is uncertain what impact it will have on China’s listed power firms’ performance. Hence, this policy has no significant effect on the power stock market.

4.2. Analysis of the Fluctuation Characteristics of PSPI

4.2.1. Descriptive Statistics Results

This analysis differs from the previous analysis as the sample is divided into several different sub-samples according to the detected breakpoints obtained by using the ICSS algorithm. Descriptive statistics for different sub-samples are reported in

Table 4, which shows that only the mean of the first sub-sample (31 August 2006 to 28 May 2007) is positive. These results indicate that, compared with the period from 31 August 2006 to 28 May 2007, returns on power stock index (or the change of power stock price volatility) decreased from 28 May 2007 to 15 November 2012.

Table 4 also shows that the full sample and all sub-samples are characterized by statistically significant kurtosis (exceeds 3), suggesting that they are leptokurtic, namely demonstrating a fatter tail and a higher peak (the Jarque–Bera test outcome in the sixth column). Meanwhile, the Jarque–Bera result (the sixth column in

Table 5) and Ljung–Box Q-statistic result (the seventh column in

Table 4) show that series autocorrelations for squared residuals at any reasonable level exist in the first through fourth sub-samples as well as in the full sample, which indicates that the GARCH model is suitable for these samples except the fifth sample.

The largest standard deviation emerges in the second sub-sample (from 5 May 2007 to 1 February 2008), meaning that, from 5 May 2007 to 1 February 2008, power stock price volatility is the greatest. This volatility occurred during this period because China’s interest rate was adjusted several times; meanwhile, originally non-tradable stocks, such as the stocks owned by state companies, were permitted to be listed and traded.

4.2.2. The Fluctuation Characteristics of the PSPI

Table 6 reports the results of the fluctuation characteristics of the PSPI based on the GARCH model. In terms of the model estimated with the full-sample, the value of

is the highest with 0.988. The value of

in sub-series 1 to 4 reduced by 34%, 22%, 9%, and 24%, respectively, compared with the value of the full sample, and the average value decline in sub-samples is 22.75%.

This result shows that power stock price fluctuation persistence stage is reduced typically when considering structural breaks, which is consistent with the conclusions of Kasman [

45]. Kasman argued that the value of

decreased by 29.2% while considering structural breaks. Christopher and William [

46], Malik [

47], and Rapach and Strauss [

48] also stated that, with structure breaks, the persistence of a volatility stage will be reduced.

4.3. The Impact of Power Market Reform on Power Stock Price Volatility

In this section, we first examine the long-term relationship between the variables. We then explore the magnitude of the policy impact on structural changes in the stock volatility. Finally, we examine the policy impact by type.

As previously discussed, to establish a long-term relationship between the variables, an

F-test should be applied to Equation (4). The

F-test results are displayed in

Table 7.

Table 7 shows

F statistics are higher than the Upper Bound value when it includes the dummy variable; and the

p value is 0.000, indicating that a level of significant co-integration exists between the explanatory variable and the explained variable, as well as between the control variables and the explained variable.

In the search for the optimal length of time for the level variables of coefficients, the lag selection criteria of the Schwarz Bayesian Criterion (SBC) is utilized (Rushdi et al. [

41]), and the order of lags is selected as 0. The results in

Table 7 imply that a long-term relationship exists between the variables. Then, to estimate the parameters of Equation (5), the ARDL co-integration results between power stock price fluctuations and other variables are reported in

Table 8.

Table 8 demonstrates that there is long co-integration between the power stock price (PS) and fund supply (FS), power generation (PG) and coal price (CP). The dummy policy variables (except the first one (D1)) have a significant negative impact on China’s listed power companies’ stock price volatility in the long term. This indicates that China’s power industrial policy reduced the volatility of the power stock price in this study’s period. Market-based regulation is a signal that the power industry will develop toward more orderly operations. Hence, investors have more confidence in the future development of the power industry, and the stability of the power stock market increased. This result is in line with that of Malik [

31], who argued that events, such as policy, are important factors affecting the volatility of the CLPC.

Furthermore, we found that the fourth dummy variable—the policy of deepening power market reform promulgated by the SERC—had the greatest impact on volatility. This implies that compared with the policy restricting employees’ investment behavior and reform of the power trading price, reforms affecting the entire power market have greater influences on the power stock market. This result aligns with our expectations: More important policies have a broader influence, and greater impacts will occur.

The co-integration of the control variables, power generation, coal price and stock price is statistically significant, meaning that they have a considerable impact on the power stock market. The negative correlation between power generation (PG) and power stock price indicates that greater the power output is, the lower the PS should be. This finding reveals that macroeconomic growth has a significant negative effect on China’s listed power companies’ (CLCP) stock returns in the long run. This seemingly odd result is caused by the strong speculation that occurs in China’s stock market (Dong and Wang [

15]) and is policy-driven (Narayan and Zheng [

49]), meaning that policies affect investors’ sentiments more highly than economic growth. Moreover, although China’s economic growth (power generation is an indicator of macroeconomic development) increased quickly in the period of this study, tightening policies during this period—such as raising the deposit reserve rate from 2.25% to 3.50% between 23 December 2008 and 8 June 2012, and strengthening the supervision of the power industry (over this period, more than 10 policies have been implemented to regulate power generators to develop energy savings and environmental protection)—jointly exerted negative impacts on changes in the power stock price.

The relationship between coal price (CP) and power stock price fluctuation is statistically significant with a negative value. This means the increase in coal price has a negative impact on power stock price fluctuation; coal price increase caused a decrease in generators’ anticipated profit, and thus reduced the fund flowed into power stock market.

The positive correlation between fund supply on the stock market (FS) and power stock price volatility could be easily understood. Increase in the money supply will lead to additions of money liquidity and nominal wealth; thus, stock prices are more volatile.

The short-run dynamic changes of the relationship between power stock price and other variables (results of ECM) are shown in

Table 9. The short-term impact of power market reform on power stock price volatility is similar to that in the long run, which strengthens the result that China’s power market reform reduced the stock price volatility of the listed power companies and the risk of investing in the power stock market. This implies that China’s power market reform favors the expansion of power companies’ ability to attract capital and promote power industrial development.

The only important difference between

Table 8 and

Table 9 is that the impact of the first policy (D1) on power stock price volatility becomes statistically significant in

Table 8.

Table 8 also indicates that the impacts of the control variables (PG, CP and FS) are consistent with the results in the long term. The most important difference between short term and long term is that the negative coefficient of dummy variable 1 is statistically significant in a short-run period. This indicates that the policy of

Measures of Price and Facility Operation of Desulfurization for Coal-fired Power Units issued by NDRC reduced the fluctuation of power stock price in a short run. This policy aims to encourage coal-fired power firms to invest and operate the facilities of desulfurization. Since this policy is signaled by compulsory administrative characteristics, it affects power stock price only in a short run.

In

Table 9, the coefficient of the error correction term is statistically significant at −0.154. This suggests that, when power stock price volatility is above or below its equilibrium level, it adjusts by almost 15.4% within the first year. The results support the notion that with the promulgation of a few power industrial policies, China’s power stock price volatility tended to shrink because these regulations increased investors’ confidence in the orderly development of China’s power market.

The ARDL co-integration approach has certain econometric advantages. It avoids the endogeneity problems and allows researchers to estimate the long-run and short-run parameters of the model simultaneously. However, it is important to stress that the application of the ARDL co-integration technique presumes the existence of a unique long-run relationship among the variables at hand [

43,

45], a fact quite restrictive for multivariate systems. Towards this direction and as a robustness test for the equilibrium relationship, we also applied the Johansen’s approach via the trace and the maximum eigenvalue tests. The results of the Johansen’s co-integration test on power stock price fluctuations and other variables are reported in

Table 10 and

Table 11. The trace test and the maximum eigenvalue test results indicate that there exist two cointegration equations between the explanatory variable and the explained variable, as well as six cointegration equations between the control variables and the explained variable, which is consistent with results in

Table 8 and

Table 9.

5. Conclusions and Discussion

5.1. Conclusions

Our research controls for possible exogenous shocks in three ways. Firstly, we estimate the effect of various policies along the timeline separately. Using all policy dummy variables in the GARCH model allows us to estimate the coefficient of each policy and observe the scale of policy effect. Secondly, by using the GARCH model, the model incorporates the influence of all past and recent informational shocks on volatility. When we use the policy dummy variables as explanatory variables of volatility, we separate the policy impacts from other effects in the past. Thirdly, we incorporate macroeconomic indicators such as CP, PG, and FS as explanatory variables into the process of estimation. The statistical significance of these economic variables further shows that the Chinese stock price is easily affected by macroeconomic shocks. Considering that macroeconomic factors are not the focus of this study, we do not demonstrate the relevant results for clarity. However, these tests can be regarded as alternative robustness tests.

As one of the important energy-intensive and emission-intensive sectors, China’s power industry has increasingly attracted the attention of researchers and policymakers regarding how to promote more environmentally friendly development. One effective measure to improve energy efficiency is implementing power market reform (Zhao and Ma [

50]; Du, et al. [

51]; Ma and He [

52]). However, the possible negative impact of policies on stock price volatility is a concern for the issue of relative policies.

The main objective of this study was to empirically examine the dynamics of interaction between China’s power market reform and relevant stock price volatility. This paper uses the ICSS algorithm to detect structural breakpoints in power stock price volatility and analyzes volatility characteristics of sub-samples based on the GARCH (1, 1) model. To identify the above result and quantitatively study the impact of power market reform on power stock price volatility, we conduct an ARDL co-integration analysis using relative monthly data from 30 August 2006 to 15 November 2012.

Our results indicate a few broad empirical patterns. We find that, from 30 August 2006 to 15 November 2012, four structural breaks of China’s power stock price volatility occurred, and three of them are related to the promulgation of power market reform policies. In addition, we find that the degree of power stock price fluctuations in each sub-sample decreases with time, indicating that China’s power market reform reduces power stock price fluctuations. These results demonstrate that power industrial policies have a statistically significant negative impact on power stock price volatility, meaning that China’s power industrial policy promote the development of the power stock market by reducing market risks. We give explanations for policies with extreme volatility one by one in

Section 5 along with the market conditions at that time. Moreover, Drawing the Roadmap for Deepened Reform for Power Development in the Twelfth Five-Year Plan Period had the most important impact on power stock price volatility in the long-run period with the coefficient of −1.451, and in the short-run period with the coefficient of −0.224. These results indicate that, compared to specific power regulation in

Table 3, overall strategic plan for industrial development is more important in terms of degree and scope of influence, thus has a greater impact on the power stock market.

5.2. Recommendation

Industrial policies in the power market aim to not only motivate the investment in renewable energy but also affect company’s value. Therefore, when formulating policies related to investment behavior, the government should focus on the links between different markets. Given our empirical analysis, we provide insights on further design for and implications of industrial policy on the electricity market. At least three implications of this study merit discussion.

Firstly, greater attention should be paid to policies promoting power market reforms in China. Based on our study, few power industrial policies issued between 2006 and 2012 have a significant effect on stock volatility, which implies market reform experience a decade of stagnation. Market-oriented reforms have proven to be beneficial to the stability of China’s power stock market and favorable for power industry development. We hope the new round of power sector reform could make a change.

Secondly, policies promoting the use of renewable energy by subsidizing retailing price and fixed investment is far from satisfactory. Our study indicates the recent policies related to renewable energy do not have a very significant impact on the power stock market. Our findings are consistent with the other scholar’s judgment. Rioux et al. (2017) [

53] showed that the increase in the share of renewable energy did not have a significant effect on total generation with coal. A substantial increase in renewables use in China’s energy system would require additional policy interventions.

Thirdly, according to our empirical analysis, the short-term impact of power market reform on power stock price volatility is similar to that in long run, which implies investors have paid considerable attention to the continuing implementation of the policy rather than publish. Therefore, the government should pay attention to clarifying the execution of the policy and providing further detailed information.

5.3. Limitations and Future Research

The paper has a few limitations that present opportunities for future research. First, our analysis is based on data from 30 August 2006 to 15 November 2012, in China. Future studies are required to determine whether the analysis can be expanded to a longer period or wider scope. Meanwhile, in addition to regulation reforms, the difference between detailed policy operation also contribute to the structure breaks of China’s stock price volatility; however, these factors have not been considered in this study.

We offer two speculations about generalizability. On the one hand, SOEs represent particularly strong policy executors that are known to be more aggressive to participate in policy experiments than other companies. The fact that the power market reform triggers different responses from SOEs and private enterprises present important fodder for future research. On the other hand, the power industry is unique in the sense that it is evolving toward deregulation of retailing price and the freedom to invest in renewable energy, which will enhance the profitability of enterprises and achieve dynamic competition in the power industry, in turn, may reduce the interactions between the industrial policy and stock price volatility. However, policies such as limiting the manufacturing development, upgrading the generation equipment, guidance for appropriate investment in thermal power plants continue to have impacts on stock price volatility. In sum, we believe that generalizability is an issue in this study as it is in any single industry study. Replication across industries is necessary before we can attempt to extend the implications of our study to a broader range of industry contexts.

In conclusion, this paper highlights the interaction between industrial policy and stock price volatility. Despite its limitations, it directs our attention to an understudied question in policy-making—how interaction varies within and across the market. We have taken great care to document and explain our methodology to enable replication across industries. We hope this effort spurs more empirical studies of competitive interaction among firms within industries.

{kind=link}

{kind=link}

{kind=link}

{kind=link}