1. Introduction

As carbon emissions accelerate global warming, the reduction of carbon emission is imperative. Then, there is a consensus that fatal and irreversible climate change can occur without appropriate global controls. Since the Kyoto Protocol, agreed to in 1997, governments have implemented various regulations to reduce carbon emissions, including tax policies. Here, an important regulatory policy is “cap-and-trade” (CAT) system, which was initiated from the 1970s and then introduced through the Kyoto Protocol (refer to [

1,

2,

3]). It sets up a limit on carbon emission amounts for developed countries at the national level, and again to assign an emission limit for each firm. It is a combination of international market mechanism and regulation, which implies that carbon emission rights can be traded as a commodity. Accordingly, if an individual firm under the CAT exceeds the predetermined carbon emission limit, the excess amount must be purchased from outside suppliers. Otherwise, the firm may sell the remaining amount. As a result, both academia and companies have been making efforts to decrease the carbon footprint against the CAT system.

Nonetheless, these efforts have so far focused on the issues of energy efficiency and use of eco-friendly materials from an engineering standpoint, or on the issues of designing international trade mechanisms for carbon emission with an economics perspective. Some examples of the engineering issues are the replacement of energy inefficient equipment and facilities, the redesign issues in product and packaging, the use of renewable energy sources, or organizing programs for energy savings (refer to [

4]). On the other hand, the policy effects on eco-friendly concerns have been studied in literature from an economic point of view. Then, these policy regulations can be roughly classified into those based on prices and those based on quantities. Here, price-based regulation refers primarily to imposing taxes on carbon emissions, while quantity-based regulation gives maximum exposure to emissions and allows companies to trade such emissions rights in the market (refer to [

4,

5,

6,

7]). It implies that there is a relatively small number of papers in literature to analyze operational efficiency and optimization modeling with eco-friendly carbon emissions.

This study aims to provide an optimization model for operational efficiency in individual firms with CAT carbon emissions regulation. More specifically, this study assumes that customers’ demand takes a probability distribution. Under this circumstance, our intention is to draw theoretical and policy implications for carbon emissions regulation by setting and analyzing a newsvendor model in which the decision maker is loss-averse for her risk preference.

The newsvendor model has been a classic problem in supply chain management since [

8]. More specifically, it is a stochastic inventory model where end customers’ demand is known to retailers only as a probability distribution. Thus, it is an expected-profit optimization model in a single-period selling season which aims to determine the optimal inventory level in demand-driven supply chain processes. In other words, such newsvendor problem effectively models the key trade-off relationship between underage and overage costs in inventory management and can be applied potentially for a variety of industrial decision-making situations. In addition, from an analytical perspective, the major advantage of the newsvendor model is that it is well established as an unconstrained mathematical optimization model. Then, it has simple but powerful managerial insights to obtain a closed-form optimal solution if there are no additional constraints such as budget or resource limits.

Due to the aforementioned reasons, various forms of basic newsvendor models have been extended and modified and also actively studied until now. In literature of stochastic inventory management, Refs. [

9,

10] examine many related studies in newsvendor models and provide excellent reviews. At first, Ref. [

9] classifies newsvendor models into 11 categories, one of which refers to different forms of objective and utility functions. Then, in this category, it points out that all the decision makers may not be risk-neutral. That is, some inventory managers may not target simply maximizing their expected profit. Instead, their goals might be maximizing the probability of achieving a target profit. Some alternative objectives can be an expected utility or risk tolerance factor. In summary, risk neutrality guarantees that it provides the best decision on average and it may be justified by the Law of Large Numbers. However, the outcomes actually observed are random. The first few outcomes may turn out to be very bad and cause unacceptable losses. Ref. [

11] conducts two experiments and provides empirical evidence suggesting that the risk preferences of inventory manager may be very different depending on the product characteristics and risk attitude. They also present several descriptive models of newsvendor decision-making including loss aversion. As a result, these models cause the optimal solutions deviated from those with risk neutrality, which is called as “Decision Bias”. Meanwhile, in order to select an appropriate risk measure, an axiomatic approach has been studied in literature to categorize typical risk measures in risk-averse newsvendor models and discuss the validity of risk measures (refer to [

12,

13,

14]).

In this work, we focus on loss aversion as a benchmark risk preference to analyze our newsvendor problems with CAT regulations. In literature, the theory of loss aversion originated from the prospect theory suggested by [

15]. It implies that, for the same amount of gains and losses, loss-averse decision makers are more averse to the loss, compared with the gain. Then, loss aversion is also closely related to well-known endowment effects in psychology and behavioral economics, or divestiture aversion in social psychology. Accordingly, it is not uncommon to find such loss-averse attitude under uncertainty in practical decision-making situations. For example, Ref. [

16] studied decision-making under uncertainty based on their questionnaires from US and Canadian CEOs. As a result, they show that managers’ decision-making is a good harmony with loss aversion, as pointed out by [

17].

The purpose of this study is to establish and analyze loss-averse newsvendor models with CAT. Through these newsvendor models, we will analyze how loss aversion affects the optimal solution with CAT. To this end, the authors used a “kinked” piecewise linear and concave utility function to reflect loss aversion in the existing newsvendor models. Then, the key research questions are as follows: (1) How to consider loss aversion in newsvendor models with CAT? (2) How to identify the existence of a unique optimal solution in the corresponding optimization model and analyze the impacts of model parameters on the optimal solution? (3) In particular, what are the joint effects of loss aversion and stockout costs to the optimal solution with CAT? For this, we analyze the newsvendor model to provide implications and insights through analytical results and computational study. With the authors’ best knowledge, this paper is the first attempt to consider a newsvendor problem of CAT regulations with any other risk attitude rather than risk neutrality, which is an important contribution to the literature of stochastic modeling with CAT carbon emissions regulation.

The remainder of this paper is organized as follows.

Section 2 corresponds to the theoretical background. Then, we review various studies related to operational efficiency and optimization models with carbon emissions regulation. In particular, we examine the well-known newsvendor models and loss aversion in literature for modeling CAT regulation used in this study. In

Section 3, we present two research models for this study. After that, in

Section 4, we analyze each of the models. Then, we show the existence and uniqueness of the optimal solution in the two models, respectively. We also provide a sensitivity analysis on the effects of parameter changes on the optimal solution through comparative static analysis, respectively. Next, in

Section 5, we conduct numerical experiments to reconfirm our analytical results. Finally, in

Section 6, we summarize our major results and contributions of the study, and then presents the future directions of the study.

3. Problem Formulation

Let us consider a loss-averse newsvendor with the CAT emission regulation. Initially, the newsvendor orders x units of products at a purchasing cost c and then resells them at an increased price p. For a CAT problem setting, let us denote a as the base carbon emission amount with zero production quantity and b as the additional carbon emission amount per unit product. In addition, we also denote K and as the initial permissible carbon emission cap and unit trading value with carbon emission cap. That is, when the newsvendor determines to produce x amount, which is a decision variable of the model, the total initial emission amount is equal to . If , the total emission amount exceeds the initial permissible emission cap and then the newsvendor needs to buy the extra emission from emission suppliers with the unit trading value . On the contrary, if , the newsvendor may sell the remaining amount to emission buyers with the same unit value .

For the balance of the newsvendor’s demand and supply in our model, we assume that demand

D is only known as a nonnegative probability distribution where its cumulative distribution function,

, and probability density function,

. Due to this intrinsic randomness in the model, a rational decision maker may face a mismatch between the predetermined ordering quantity and post-realized demand. If realized demand is smaller than the ordering amount, the leftovers

are disposed at the unit cost

. Here, the sign of

may either positive or negative. When it is negative, it implies a positive salvage value with the same absolute value. On the other hand, if the demand is larger than the ordering amount, it means that stockout has occurred for the difference,

. Then, we consider each of two cases separately in the following

Section 4 at which we provide two models of how to deal with stockout items, a lost-sale model and stockout penalty model. First, in a lost-sale model, it is assumed that we just lose a sales opportunity for the excess demand

. Second, in a stockout penalty model, the unit shortage penalty cost

s is incurred for the excess demand due to the reasons such as the costs of emergency delivery option or backordering and loss of goodwill and so on. Finally, in order to formulate the model meaningfully, we need to have the conditions (1)

,

and

; (2)

to prevent trivial solutions with CAT regulations and classic newsvendor models, respectively.

Then, the newsvendor has a payoff function

as follows:

where

. In Equation (

1), the first term means the revenue of the newsvendor. As the initial inventory is simply assumed to be zero, the newsvendor’s on-hand inventory is

x. Then, the newsvendor can sell no more than his on-hand inventory even if the realized demand is larger than his on-hand inventory. Then, the second term is the cost of purchasing

x units for his product. Next, the third and fourth terms mean disposal costs and stockout penalty costs, respectively. In the last, the fifth term is the trading value with carbon emission cap to reflect the CAT system. In the last, nonnegative production level is assumed with

.

Then, for modeling the loss aversion of the newsvendor, we introduce a following utility function

in our newsvendor problem with CAT, which is also consistent with [

11,

17], as follows:

where

is a (fixed) loss aversion coefficient. That is, an optimization model for loss-averse decision maker can be considered as a special case of the expected-utility optimization problem where the utility function is piecewise linear and concave, and also has a kinked point at a threshold (i.e., zero in our model) utility level. Finally, our objective function for a loss-averse newsvendor is to maximize the expected utility of profit, instead of the expected profit in a risk-neutral newsvendor problem, which is given as follows:

Thus, in a mathematical perspective, our objective given in Equation (

3) is an unconstrained stochastic optimization model only except a nonnegativity condition for production amount,

. Here, bigger

means that the newsvendor is more loss-averse. If

as the lowest possible value of a loss aversion coefficient, then the utility function reduces to a linear function and the kinked point does not exist. Thus, when

, it is equivalent to a risk-neutral newsvendor with CAT emissions regulation, which was studied at [

27]. From that sense, this work is a direct extension of [

27] when the newsvendor is loss-averse.

In the last, for clarification of our problem, let us categorize the model parameters into three types. The fist type is

, a loss aversion coefficient. The second type includes

s,

p,

c and

, which are in the first four terms in Equation (

1) to specify the basic newsvendor problem. The third type covers

a,

b,

K and

, which are in the fifth term in Equation (

1) to represent the CAT system. From now on, let us denote the second and third types of the model parameters as

newsvendor and

CAT parameters.

4. Analytical Results

Now, we begin our analysis with the risk-neutral models studied at [

27]. These risk-neutral models lay a theoretical foundation for our loss-averse models as the preliminary results.

Lemma 1. When (i.e., the newsvendor is risk-neutral), is concave for all x and there exists a unique optimal order quantity where and denote the loss-averse optimal solution with λ and risk-neutral optimal solution.

Proof. When

, the newsvendor problem corresponds to a risk-neutral case with CAT emissions regulation, which is equivalent to Model 2 in [

27]. □

In Lemma 1, the proof idea is that the second-order derivatives of is nonpositive, which is a sufficient condition for concavity of the model.

Lemma 2. For a risk-neutral newsvendor with cap-and-trade emissions regulation, higher values of s and p leads to increased . In comparison, higher values of c and decrease . For the CAT parameters, the values of b and β decrease . However, a and K do not affect .

Proof. The proof for Lemma 2 is based on supermodularity and implicit function theorem. For its detailed proof, please refer to [

27]. □

In summary, the inclusion of CAT regulation terms and shortage penalty costs does not lead to structural changes of the optimal solution when the newsvendors are risk-neutral. That is, when we add CAT terms with the CAT parameters, they do not affect the impacts of the newsvendor parameters (i.e., s, c, p, ) by themselves in risk-neutral newsvendor models. However, in loss-averse newsvendor models, the impacts of newsvendor and CAT parameters on the optimal solution jointly affect the optimal solution more dynamically, especially with shortage costs, which we will see as follows.

4.1. Model 1: Loss-Averse Newsvendor Model with No Shortage Costs

Now, let us resume our analysis with the loss-averse newsvendor models with these preliminary results. Then, we will show how the the results of risk-neutral and loss-averse newsvendors models can be different each other. The first step is to analyze concavity of the newsvendor’s expected utility with loss aversion.

Proposition 1. When , is concave for all x and there exists a unique optimal order quantity .

Proof. In model 1, the value of

s is fixed as zero. Then, the profit function in Equation (

1) can be re-described as follows:

Then, by mapping the newsvenror’s profit function at Equation (

4) into his utility function at Equation (

2), the expected utility function for the loss-averse newsvendor can be expressed as follows:

with

because the condition

holds true only when

while

,

. Thus,

Then, by Leibniz’s integral rule, we take the first derivative of

with respect to

x as follows:

Next, we similarly take the second derivative of

with respect to

x and the sign of the second derivative is shown to be nonpositive as follows:

because

from Lemma 1 and

. □

Next, we will conduct a sensitivity analysis of model parameters on the optimal solution through comparative static analysis. The main idea of the proof is implicit function theorem in literature.

Proposition 2. For a loss-averse newsvendor with cap-and-trade emissions regulation, is a decreasing function of λ. In addition, higher value of p leads increased . In comparison, higher values of c and decrease . For the CAT parameters, the value of K increases . However, the values of a and b decrease . Finally, the impact of β is indeterminate.

Proof. First, for the impact of the loss-averse coefficient on the optimal solution

, we use implicit function theorem and then

As

from Proposition 1, we need to show that

. By taking the derivative of Equation (

6) with respect to

, we can obtain the mixed second derivative of the expected utility as follows:

Next, for the impact of

p, we need to show that Equation (

6) is nondecreasing in

p. Since the first term of the right-hand side

in Equation (

6) is nondecreasing in

p from Lemma 2, it is sufficient to prove that the second term of the right-hand side

in Equation (

6) is nondecreasing in

p, which can be easily proved because

is a nondecreasing function and

is nonincreasing in

p. Then, for the impacts of

c and

, the proofs are similar to that of the impact of

c.

For the CAT parameters, first let us consider a, b and K. Then, is not a function of a, b and K from Lemma 2. Again in this case, we only need to show that is a nonincreasing function of a and b and nondecreasing function of K. Then, it can be shown straightforward from the definition of . In the last, for , the impact of in may change depending on the value of x. Thus, we cannot derive a monotone direction for the impact of on the optimal solution. □

4.2. Model 2: Loss-Averse Newsvendor Model with Shortage Costs

Next, we consider a loss-averse newsvendor model with a stockout penalty cost. Thus, our definition for the profit function returns to Equation (

1). Then, we analyze a stockout penalty model in a similar way that was done with the lost-sale model.

Proposition 3. When with a stockout penalty cost, is concave for all x and there exists a unique optimal order quantity .

Proof. Our profit function in Equation (

1) can be re-represented as follows:

Then,

with

and

because the condition

holds true when

and also

when

. Thus,

Then, we take the first derivative of

with respect to

x as follows:

Thus,

where

. Similarly, we take the second derivative of

with respect to

x and the sign of the second derivative is shown to be nonpositive as follows:

because

from Lemma 1 and

. □

Proposition 4. For a loss-averse newsvendor with stockout penalty cost and cap-and-trade emissions regulation, is a decreasing (or increasing) function of λ if (or ). In addition, higher value of s leads to increased while higher value of decreases . In comparison, the impacts of p and c are indeterminate. Finally, for the CAT parameters, the impacts of a, b, K and β are also indeterminate.

Proof. Similar to Proposition 2, it is sufficient to analyze for the impact of on the optimal solution. In fact, . Thus, nonnegative (or nonpositive) means that is nonincreasing (or nondecreasing) in .

Next, for the impact of s, we need to show that is nonincreasing in s because is not a function of s. Then, from the definition of , it is straightforward to show that is nonincreasing in s. Then, for the impact of , is not a function of . Thus, following from Proposition 2, the introduction of shortage costs does not affect the impact of on the optimal solution, regardless of without or with shortage costs. On the other hand, the impacts of p and c in may differ from the values of x. Thus, the impacts of p and c on the optimal solution are not given monotonously.

For the CAT parameters of a, b, K, , the impacts of the parameters are not monotone due to the complexity of the problem in by the introduction of shortage costs. □

As a summary of the analytical results in this section, we discuss the results from each model in

Section 4.1 and

Section 4.2 separately as follows. When there is no shortage costs, our sensitivity analysis at Proposition 2 shows that the impacts of newsvendor parameters on the optimal solution is the same as in those on the optimal solution regardless of risk preferences, risk neutrality and loss aversion. On the other hand, the impacts of CAT parameters on the optimal solution changes in a loss-averse newsvendor problem, compared with a corresponding risk-neutral problem. It implies that loss aversion significantly affects the optimal policy of newsvendors’ decision-making with CAT regulations.

Next, when we additionally include shortage penalty costs in a loss-averse newsvendor problem with CAT consideration, it increases the structural complexity of the model. That is, for most of the model parameters, the directions of the impacts are mixed and the impacts on the optimal solution are not monotone, especially with CAT terms. Thus, it shows big differences in the analytical results between the existing risk-neutral and loss-averse models.

In the last, please note that our analytical results allow any arbitrary probability distributions for random demand, so the demand distribution is not limited to a specific distribution. These general results add to the applicability and value of the model as do in the risk-neutral models.

5. Numerical Experiments

In this section, we conduct our numerical experiments to reconfirm our key analytical results and to develop insights in our study. For all the numerical examples considered, we apply Monte Carlo simulation for the original analytical problem. In all examples, the sample size is given as 1000. The base values of the model parameters and random variable given are follows: (1) for newsvendor parameters, , , c = 400, ; (2) for CAT parameters, , , , and (3) for random demand, D takes a normal distribution with mean and variance .

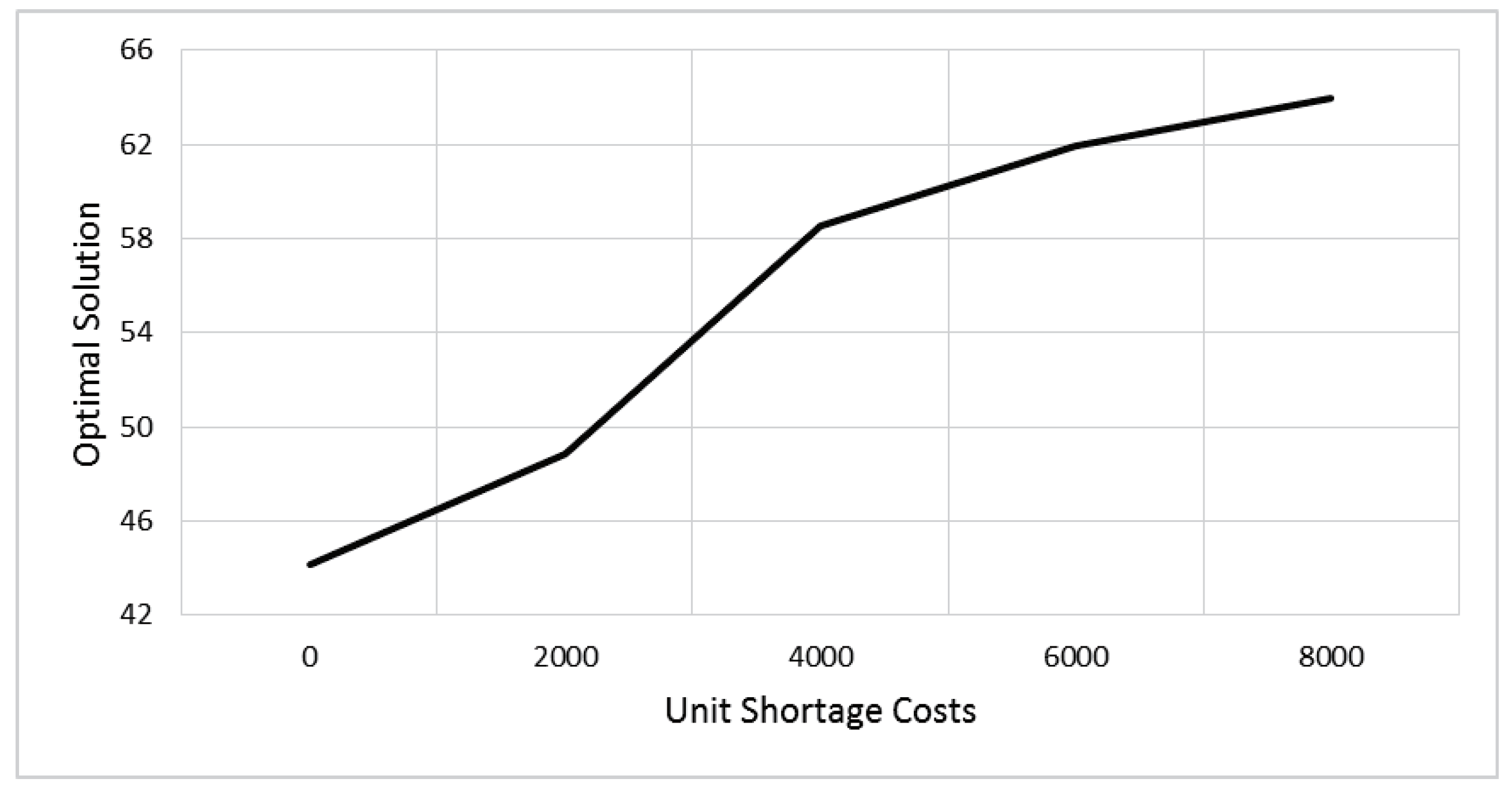

In

Figure 1, we redefine

as the degree of loss aversion. Then, we add

and five values of unit shortage costs,

, to see the impact of shortage costs numerically. The results show that increased shortage costs lead to higher optimal solution, which is to confirm the analytical result proved in Proposition 4. It is intuitive that loss-averse newsvendor with CAT system faces more risk for potential loss with higher shortage costs, leading to lower optimal solution.

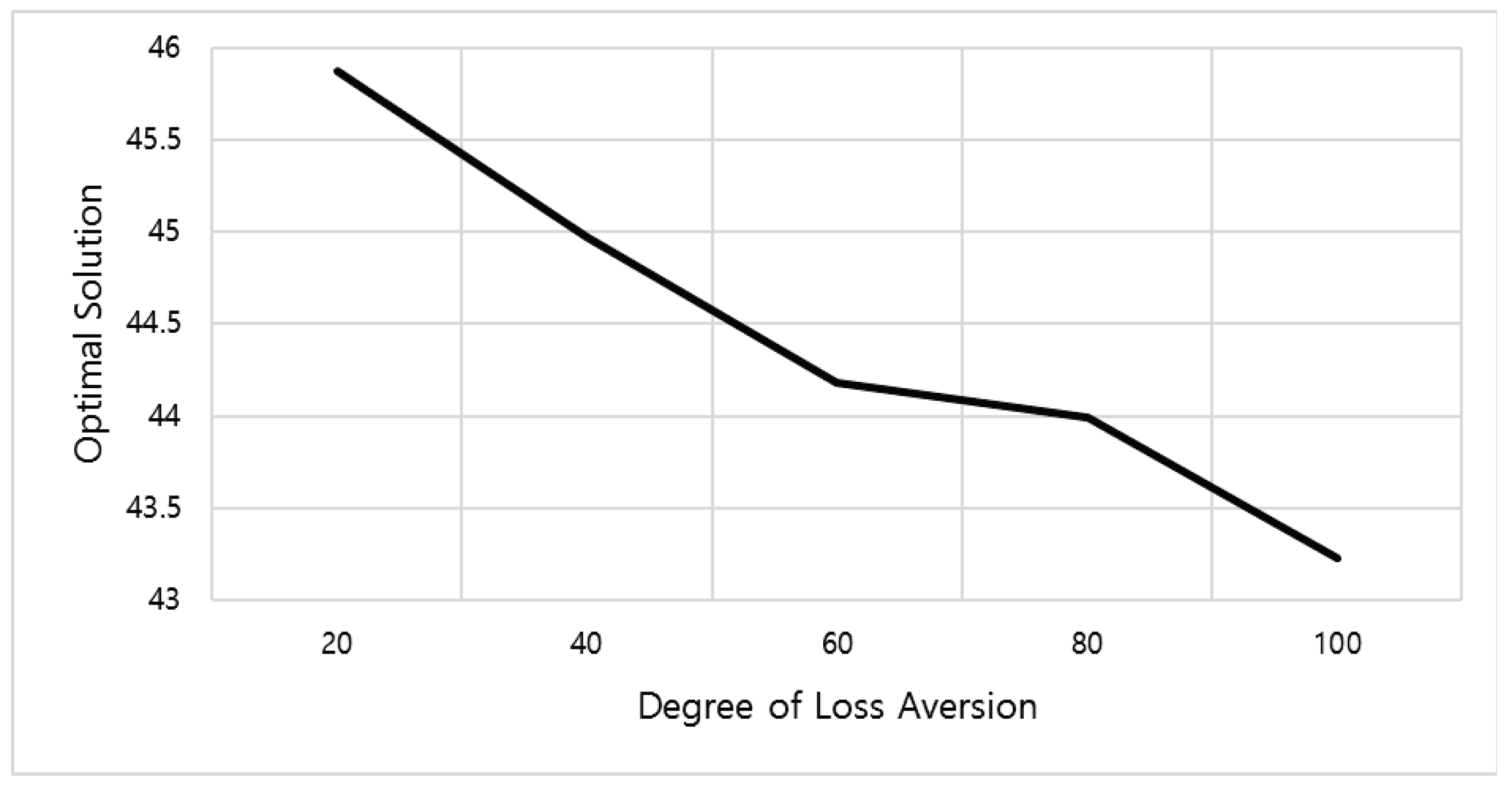

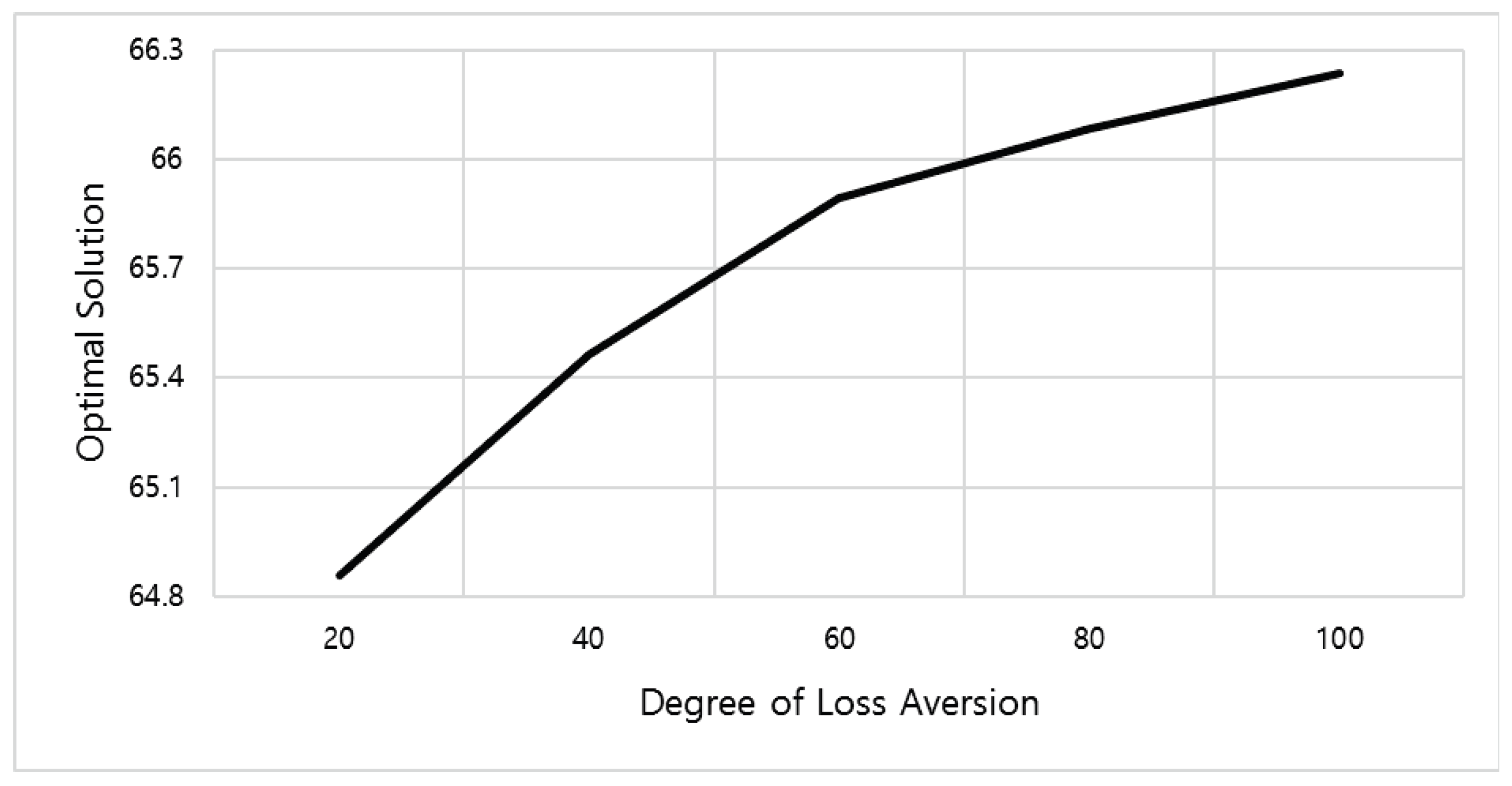

Figure 2 and

Figure 3 imply that the direction of the impact of the degree of loss aversion with a CAT system may change in different values of

. As

is a nonincreasing function of

s, a sufficiently high

s may cause a negative

, leading to the positive impact of loss aversion on the optimal solution. Then, in order to verify this, we use two values of

to represent the cases with low shortage costs and high shortage costs, respectively. Then, we also use five values of

to see the impact of loss aversion numerically. As a result, the impact of loss aversion with a CAT system has a negative slope when unit shortage cost is low in

Figure 2. On the other hand, the sign of the slope changes to be positive when unit shortage cost is sufficiently high in

Figure 3. In conclusion, the impacts of shortage costs and loss aversion with CAT system jointly affect the optimal solution, which is also consistent with the results in SCM (Supply Chain Management) literature (refer to [

17]).

6. Conclusions

We apply a newsvendor analysis for loss-averse inventory managers with a CAT emissions regulation. We use a simple “kinked” piecewise linear and concave utility function to reflect loss aversion to study the newsvendor models. Then, we analyze the two models in a lost-sale and stockout penalty costs models. More specifically, we show that our objective functions are concave to derive the existence and uniqueness of the optimal solution. After then, through a comparative static analysis, we conduct a sensitivity analysis of how the model (newsvendor and CAT) parameters affect the optimal solution. As a result, the analytical results we obtain from the two models are very different. In conclusion, with loss-averse newsvendor models, the inclusion of CAT regulation terms and shortage penalty costs adds more structural complexity in the optimal solution. However, it is not with risk-neutral solutions in literature.

For future direction of the study, the following topics can be considered. First, this study considers a stochastic demand model with an individual firm. Similarly done in literature of risk-neutral newsvendor models, it can be extended in the scope of SCM studies. Then, it is possible to study the issues of SCM coordination by the contract among SCM agents in centralized and decentralized models, accordingly. Second, when the greening efforts and investment are included in the model as an additional decision variable, the results of the model can be enriched by considering the cost factors such as the increase in demand and the cost factors such as the investment cost.

{kind=link}

{kind=link}

{kind=link}