Spatial Distribution Pattern of the Headquarters of Listed Firms in China

Abstract

:1. Introduction

2. Literature Review

3. Data and Methodology

3.1. Data

3.2. Spatial Autocorrelation Model

3.2.1. Global Moran’s I Statistic

3.2.2. Getis-Ord Gi* Statistic

3.3. Kernel Density Estimation

3.4. Apriori Algorithm

4. Results and Analysis

4.1. Temporal Growth of Listed Firms in China

4.2. Spatial Analysis in Different Periods

4.2.1. Global Moran’s I Statistic

4.2.2. Getis-Ord Gi* Statistic in Different Periods

4.3. Spatial Patterns in Different Sectors

4.3.1. Global Moran’s I Statistics in the Top Five Sectors

4.3.2. Getis-Ord Gi* Statistics in the Top Five Sectors

4.3.3. Kernel Density Estimation with Different Radius

4.4. Spatial Association Analysis of Industry Sectors

4.4.1. Rules of Spatial Association

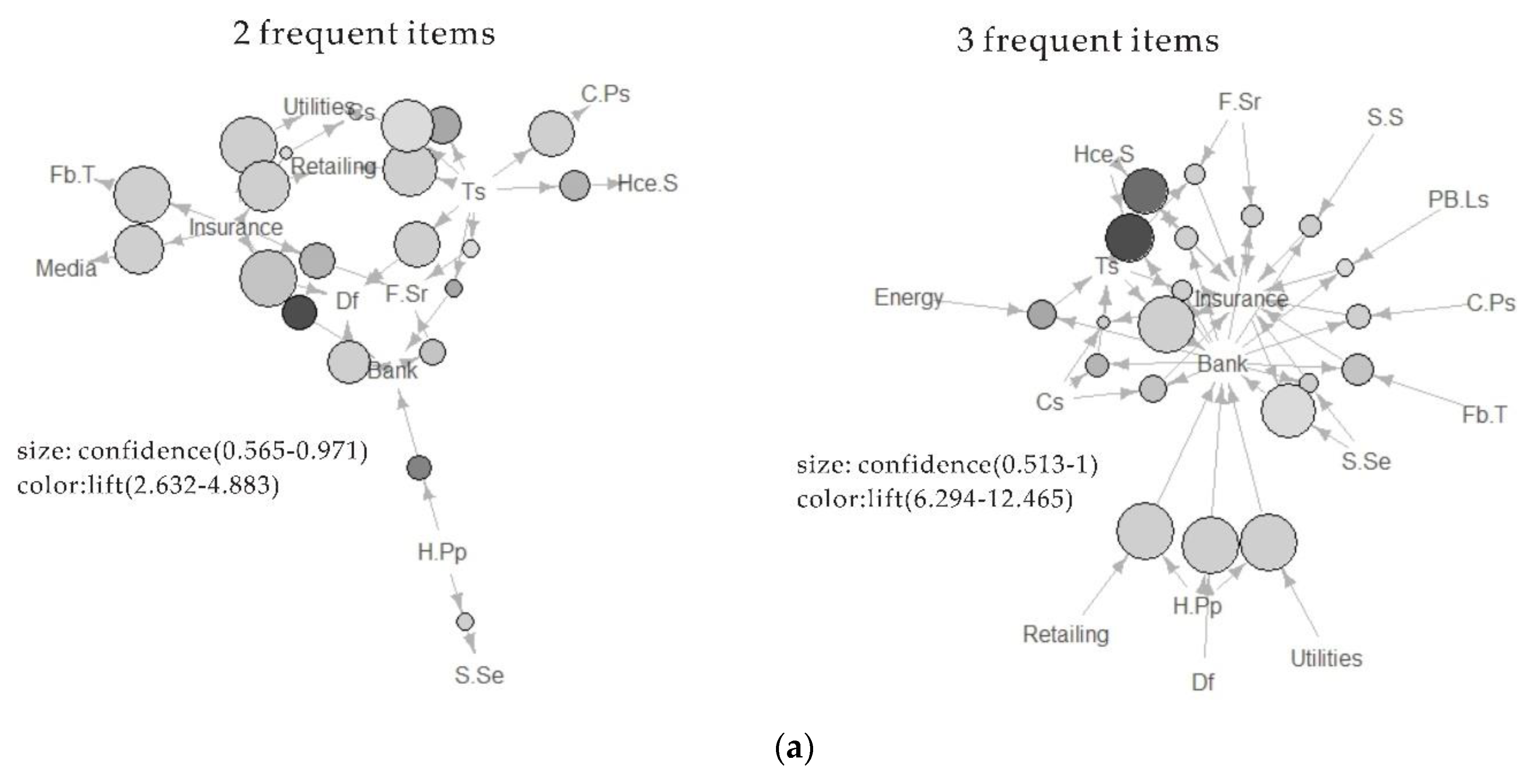

4.4.2. Frequent Itemsets

5. Conclusions and Policy Implications

- (1)

- The headquarters of listed firms in China agglomerate around megacities, especially Beijing, Shanghai, and Shenzhen, and are concentrated in certain regions along the Pacific coast, notably the Pearl River Delta region in the south, the Yangtze River Delta region in the southeast, and the Bohai Rim region in the northeast.

- (2)

- Headquarters belonging to firms in different sectors show different clustering patterns. Headquarters of listed companies classified as consumer discretionary and information technology display a higher degree of agglomeration than those in materials and health care. This enables them to obtain clustering benefits or take advantage of technology diffusion and knowledge spillover. Being close to raw materials or located in industrial parks with specific industrial facilities, the headquarters of materials firms show more dispersed location patterns than other sectors.

- (3)

- The service industries, especially insurance II and consumer service II, show strong correlations with other industries at all distance thresholds. This is so they can provide professional services to clients conveniently and quickly.

Author Contributions

Funding

Conflicts of Interest

References

- Gao, B.; Chan, W.K.; Li, H. On the increasing inequality in size distribution of China’s listed companies. China Econ. Rev. 2015, 36, 25–41. [Google Scholar] [CrossRef]

- Cho, Y.; Honorati, M. Entrepreneurship programs in developing countries: A meta regression analysis. Labour Econ. 2014, 28, 110–130. [Google Scholar] [CrossRef] [Green Version]

- Wang, C.; Madsen, J.B.; Steiner, B. Industry diversity, competition and firm relatedness: The impact on employment before and after the 2008 global financial crisis. Reg. Stud. 2016, 51, 1801–1814. [Google Scholar] [CrossRef]

- Giovanni, J.D.; Levchenko, A.A.; Mejean, I. Firms, Destinations, and Aggregate Fluctuations; National Bureau of Economic Research: Cambridge, MA, USA, 2014. [Google Scholar]

- Acemoglu, D.; Carvalho, V.M.; Ozdaglar, A.; Tahbaz-Salehi, A. The network origins of aggregate fluctuations. Econometrica. 2012, 80, 1977–2016. [Google Scholar] [CrossRef]

- Mai, Y.; Meng, L.; Ye, Z. Regional variation in the capital structure adjustment speed of listed firms: Evidence from China. Econ. Model. 2017, 64, 288–294. [Google Scholar] [CrossRef]

- Chen, G.; Firth, M.; Xu, L. Does the type of ownership control matter? Evidence from China’s listed companies. J. Bank. Financ. 2009, 33, 171–181. [Google Scholar] [CrossRef]

- Pan, F.; Brooker, D. Going global? Examining the geography of Chinese firms’ overseas listings on international stock exchanges. Geoforum. 2014, 52, 1–11. [Google Scholar] [CrossRef]

- Goyal, P.; Rahman, Z.; Kazmi, A.A. Corporate sustainability performance and firm performance research literature review and future research agenda. Manag. Decis. 2013, 51, 361–379. [Google Scholar] [CrossRef]

- Zahid, M.; Ghazali, Z.; Rahman, H.U. Corporate sustainability practices among Malaysian REITs and property listed companies. Int. J. Econ. Financ. Issues 2016, 6, 688–693. [Google Scholar] [CrossRef]

- Csomós, G. The command and control centers of the United States (2006/2012): An analysis of industry sectors influencing the position of cities. Geoforum. 2013, 50, 241–251. [Google Scholar] [CrossRef]

- Lyons, D.I.; Salmon, S. World cities in a world-system: World cities, multinational corporations, and urban hierarchy: The case of the United States. In World Cities in A World-System; Knox, P.L., Taylor, P.J., Eds.; Cambridge University Press: Cambridge, MA, USA, 1995; pp. 98–114. [Google Scholar]

- Card, D.; Hallock, K.F.; Moretti, E. The geography of giving the effect of corporate headquarters on local charities. J. Public Econ. 2010, 94, 222–234. [Google Scholar] [CrossRef]

- Davis, J.C.; Henderson, J.V. The agglomeration of headquarters. Reg. Sci. Urban Econ. 2008, 38, 445–460. [Google Scholar] [CrossRef]

- Pan, F.; Xia, Y. Location and agglomeration of headquarters of publicly listed firms within China’s urban system. Urban Geogr. 2014, 35, 757–779. [Google Scholar] [CrossRef]

- Rice, M.D.; Lyons, D.I. Geographies of corporate decision-making and control development, applications, and future directions in headquarters location research. Geogr. Compass 2010, 4, 320–334. [Google Scholar] [CrossRef]

- Rice, M.D.; Lyons, D.I.; O’Hagan, S.B. Fast-growing firms as elements of change in Canada’s headquarters city system. Urban Geogr. 2014, 36, 844–863. [Google Scholar] [CrossRef]

- Lain, K. Differentiated markets: Shanghai, Beijing and Hong Kong in China’s financial centre network. Urban Stud. 2011, 49, 1275–1296. [Google Scholar]

- Jiang, Y.; Shen, J. Measuring the urban competitiveness of Chinese cities in 2000. Cities 2010, 27, 307–314. [Google Scholar] [CrossRef]

- Jan, N. Mumbai as a global city: Theoretical essay. In International Handbook of Globalization and World Cities; Derudder, B., Hoyler, M., Taylor, P.J., Witlox, F., Eds.; Edward Elgar Publishing: Cheltenham, UK, 2012; pp. 447–454. [Google Scholar]

- Ellison, G.; Glaeser, E.L.; Kerr, W.R. What Causes Industry Agglomeration? Evidence from Coagglomeration Patterns; National Bureau of Economic Research: Cambridge, MA, USA, 2007; Volume 100, pp. 1195–1213. [Google Scholar]

- Wang, J.; Pan, F.; Guo, J. The spatial pattern of the headquarters of listed enterprises in Shanghai. Geogr. Res. 2015, 34, 1920–1932. (in Chinese). [Google Scholar]

- Goodwin, W. The management center in the United States. Geogr. Rev. 1965, 55, 1–16. [Google Scholar] [CrossRef]

- Semple, R.K.; Phipps, A.G. The spatial evolution of corporate headquarters within an urban system. Urban Geogr. 1982, 3, 258–279. [Google Scholar] [CrossRef]

- Semple, R.K.; Green, M.B.; Martz, D.J.F. Perspectives on corporate headquarters relocation in the United States. Urban Geogr. 2013, 6, 370–391. [Google Scholar] [CrossRef]

- Taylor, M.J.; Thrift, N. Large corporations and concentrations of capital in Australia. Econ. Geogr. 1980, 56, 261–280. [Google Scholar] [CrossRef]

- Bel, G.; Fageda, X. Getting there fast: Globalization, intercontinental flights and location of headquarters. J. Econ. Geogr. 2008, 8, 471–495. [Google Scholar] [CrossRef]

- Naughton, B. China’s economic policy today: The new state activism. Eurasian Geogr. Econ. 2011, 52, 313–329. [Google Scholar] [CrossRef]

- Pan, F.; Guo, J.; Zhang, H.; Liang, J. Building a “headquarters economy”: The geography of headquarters within Beijing and its implications for urban restructuring. Cities 2015, 42, 1–12. [Google Scholar] [CrossRef]

- Tonts, M.; Taylor, M. Corporate location, concentration and performance: Large company headquarters in the Australian urban system. Urban Stud. 2010, 47, 2641–2664. [Google Scholar] [CrossRef]

- Céline, B.-O.; Rachel, G. Changes in the intrametropolitan location of producer services in le-de-France (1978–1997): Do information technologies promote a more dispersed spatial pattern? Urban Geogr. 2013, 25, 550–578. [Google Scholar]

- Tonts, M.; Taylor, M. The shifting geography of corporate headquarters in Australia: A longitudinal analysis. Reg. Stud. 2013, 47, 1507–1522. [Google Scholar] [CrossRef]

- Birkinshaw, J.; Braunerhjelm, P.; Holm, U.; Terjesen, S. Why do some multinational corporations relocate their headquarters overseas? Strateg. Manag. J. 2006, 27, 681–700. [Google Scholar] [CrossRef] [Green Version]

- Birkinshaw, J.; Ambos, T.C.; Bouquet, C. Boundary spanning activities of corporate HQ executives insights from a longitudinal study. J. Manag. Stud. 2017, 54, 422–454. [Google Scholar] [CrossRef]

- Meyer, K.E.; Benito, G.R.G. Where do MNEs locate their headquarters? At home! Glob. Strateg. J. 2016, 6, 149–159. [Google Scholar] [CrossRef]

- Pan, F.; Xia, Y.; Liu, Z. The relocation of headquarters of public listed firms in China: A regional perspective study. Acta Geogr. Sinica. 2013, 68, 449–463. (In Chinese) [Google Scholar]

- Noyelle, T.J.; Stanback, T.M. The Economic Transformation of American Cities; Rowman & Allanheld: Totowa, NJ, USA, 1984. [Google Scholar]

- Rice, M.D. Regional and sectoral growth in Canada’s emerging economy. Can. J. Reg. Sci. 2004, 27, 237–254. [Google Scholar]

- Rice, M.D.; Pooler, J.A. Subsidiary headquarters: The urban geography of the “second tier” of corporate decision-making activity in North America. Urban Geogr. 2013, 30, 289–311. [Google Scholar] [CrossRef]

- Li, J.; Jiang, F.; Shen, J. Institutional distance and the quality of the headquarters–subsidiary relationship: The moderating role of the institutionalization of headquarters’ practices in subsidiaries. Int. Bus. Rev. 2016, 25, 589–603. [Google Scholar] [CrossRef]

- Xu, D.; Shenkar, O. Institutional distance and the multinational enterprise. Acad. Manag. Rev. 2002, 27, 608–618. [Google Scholar] [CrossRef]

- Huang, Q.; Chand, S. Spatial spillovers of regional wages: Evidence from Chinese provinces. China Econ. Rev. 2015, 32, 97–109. [Google Scholar] [CrossRef]

- Wang, X.; Du, L. Carbon emission performance of China’s power industry: Regional disparity and spatial analysis. J. Ind. Ecol. 2017, 21, 1323–1332. [Google Scholar] [CrossRef]

- Fallah Ghalhari, G.A.; Dadashi Roudbari, A.A.; Asadi, M. Identifying the spatial and temporal distribution characteristics of precipitation in Iran. Arab. J. Geosci. 2016, 9, 595. [Google Scholar] [CrossRef]

- Wubuli, A.; Xue, F.; Jiang, D.; Yao, X.; Upur, H.; Wushouer, Q. Socio-demographic predictors and distribution of pulmonary tuberculosis (TB) in Xinjiang, China: A spatial analysis. PLoS ONE 2015, 10, e0144010. [Google Scholar] [CrossRef] [PubMed]

- Peng, J.; Chen, X.; Liu, Y.; Lü, H.; Hu, X. Spatial identification of multifunctional landscapes and associated influencing factors in the Beijing-Tianjin-Hebei region, China. Appl. Geogr. 2016, 74, 170–181. [Google Scholar] [CrossRef]

- Jiang, G.; Ma, W.; Qu, Y.; Zhang, R.; Zhou, D. How does sprawl differ across urban built-up land types in China? A spatial-temporal analysis of the Beijing metropolitan area using granted land parcel data. Cities 2016, 58, 1–9. [Google Scholar] [CrossRef]

- Dehnad, K. Density Estimation for Statistics and Data Analysis by Bernard Silverman; Chapman & Hall/CRC: London, UK, 1998; Volume 39, pp. 296–297. [Google Scholar]

- Liao, S.-H.; Chen, Y.-J.; Deng, M.-Y. Mining customer knowledge for tourism new product development and customer relationship management. Expert Syst. Appl. 2010, 37, 4212–4223. [Google Scholar] [CrossRef]

- Bryson, A.; Forth, J.; Zhou, M. Same or different the CEO labour market in China’s public listed companies. Econ. J. 2014, 124, 90–108. [Google Scholar] [CrossRef] [Green Version]

- Ma, X.; Delios, A.; Lau, C. Beijing or Shanghai the strategic location choice of large mnes’ host-country headquarters in China. J. Int. Bus. Stud. 2013, 44, 953–961. [Google Scholar] [CrossRef]

- Karreman, B.; Knaap, B.V.D. The geography of equity listing and financial centre competition in mainland china and Hong Kong. J. Econ. Geogr. 2012, 12, 899–922. [Google Scholar] [CrossRef]

- Potter, A.; Watts, H.D. Evolutionary agglomeration theory: Increasing returns, diminishing returns, and the industry life cycle. J. Econ. Geogr. 2010, 11, 417–455. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Distance Method | p-Value | z-Score | Variance | Moran Index | Period |

|---|---|---|---|---|---|

| Euclidean | 0.000000 | 7.235523 | 0.000146 | 0.0846 | I |

| Euclidean | 0.000001 | 4.992633 | 0.000146 | 0.0575 | II |

| Euclidean | 0.000000 | 7.743269 | 0.000146 | 0.0907 | III |

| Euclidean | 0.000001 | 4.840777 | 0.000118 | 0.0498 | IV |

| Euclidean | 0.000000 | 6.143428 | 0.000145 | 0.0711 | All |

| Types of Clusters | Intensity of Clusters | Periods | Number of Cities | Percentage |

|---|---|---|---|---|

| Hot spots | Primary | Period I | 3 | 0.76% |

| Period II | 3 | 0.76% | ||

| Period III | 3 | 0.76% | ||

| Period IV | 1 | 0.25% | ||

| All | 3 | 0.76% | ||

| Secondary | Period I | 13 | 3.29% | |

| Period II | 12 | 3.04% | ||

| Period III | 8 | 2.04% | ||

| Period IV | 6 | 1.52% | ||

| All | 8 | 2.04% | ||

| Cold spots | Secondary | Period I | 47 | 11.9% |

| Period II | 32 | 8.1% | ||

| Period III | 27 | 6.84% | ||

| Period IV | 49 | 12.4% | ||

| All | 33 | 8.35% |

| Distance Method | p-Value | z-Score | Variance | Moran Index | Industry |

|---|---|---|---|---|---|

| Euclidean | 0.000000 | 7.79356 | 0.000169 | 0.0988 | Industrial |

| Euclidean | 0.000000 | 14.3722 | 0.000186 | 0.1936 | Materials |

| Euclidean | 0.000077 | 3.95275 | 0.000141 | 0.0444 | Information Technology |

| Euclidean | 0.000000 | 8.12152 | 0.000165 | 0.1016 | Consumer Discretionary |

| Euclidean | 0.002054 | 3.08225 | 0.000164 | 0.0369 | Health Care |

| Types of Clusters | Intensity of Clusters | Industry | Number of Cities | Percentage |

|---|---|---|---|---|

| Hot spots | Primary | Industrials | 3 | 0.76% |

| Materials | 6 | 1.52% | ||

| Information Technology | 2 | 0.51% | ||

| Consumer Discretionary | 2 | 0.51% | ||

| Health Care | 2 | 0.51% | ||

| Secondary | Industrials | 7 | 1.77% | |

| Materials | 32 | 8.1% | ||

| Information Technology | 3 | 0.76% | ||

| Consumer Discretionary | 8 | 2.03% | ||

| Health Care | 20 | 5.06% | ||

| Cold spots | Secondary | Industrials | 35 | 8.86% |

| Materials | 134 | 33.92% | ||

| Information Technology | 10 | 2.53% | ||

| Consumer Discretionary | 35 | 8.86% | ||

| Health Care | 77 | 19.5% |

| Radius | Rules | Support | Confidence | Lift | Count |

|---|---|---|---|---|---|

| 5 km | {Insurance II} ⇒ {Banks} | 0.066 | 0.754 | 4.883 | 52 |

| {Household…Personal Products} ⇒ {Banks} | 0.013 | 0.667 | 4.320 | 10 | |

| {Telecommunication Services II} ⇒ {Banks} | 0.043 | 0.596 | 3.865 | 34 | |

| {Telecommunication Services II} ⇒ {Consumer Services II} | 0.057 | 0.789 | 3.706 | 45 | |

| {Telecommunication Services II} ⇒ {Health Care Equipment Services} | 0.052 | 0.719 | 3.460 | 41 | |

| 10 km | {Insurance II} ⇒ {Consumer Services II} | 0.135 | 0.986 | 1.629 | 616 |

| {Insurance II} ⇒ {Banks} | 0.132 | 0.963 | 1.562 | 602 | |

| {Telecommunication Services II} ⇒ {Food…Staples Retailing II} | 0.192 | 0.969 | 1.547 | 875 | |

| {Telecommunication Services II} ⇒ {Consumer Services II} | 0.183 | 0.922 | 1.525 | 833 | |

| {Telecommunication Services II} ⇒ {Health Care Equipment Services} | 0.197 | 0.993 | 1.522 | 897 | |

| 30 km | {Insurance II} ⇒ {Consumer Services II} | 0.161 | 0.970 | 1.748 | 723 |

| {Telecommunication Services II} ⇒ {Health Care Equipment Services} | 0.243 | 0.978 | 1.668 | 1087 | |

| {Telecommunication Services II} ⇒ {Consumer Services II} | 0.228 | 0.919 | 1.655 | 1022 | |

| {Telecommunication Services II} ⇒ {Food Staples Retailing II} | 0.235 | 0.947 | 1.654 | 1053 | |

| {Insurance II} ⇒ {Banks} | 0.153 | 0.922 | 1.652 | 687 | |

| 50 km | {Insurance II} ⇒ {Consumer Services II} | 0.135 | 0.986 | 1.629 | 616 |

| {Insurance II} ⇒ {Banks} | 0.132 | 0.963 | 1.562 | 602 | |

| {Telecommunication Services II} ⇒ {Food Staples Retailing II} | 0192 | 0969 | 1547 | 875 | |

| {Telecommunication Services II} ⇒ {Consumer Services II} | 0183 | 0922 | 1525 | 833 | |

| {Telecommunication Services II} ⇒ {Health Care Equipment Services} | 0197 | 0993 | 1522 | 897 |

| Full Name | For Short | Full Name | For Short | Full Name | For Short |

|---|---|---|---|---|---|

| Banks | Bank | Utilities II | Utilities | Retailing | Retailing |

| Diversified Financials | Df | Media II | Media | Transportation | Transportation |

| Food & Staples Retailing II | F.Sr | Software and Services | S.S | Telecommunication Services II | Ts |

| Real Estate | Re | Consumer Services II | Cs | Materials II | Materials |

| Capital Goods | Cg | Energy II | Energy | Insurance II | Insurance |

| Household and Personal Products | H.Pp | Food, Beverage and Tobacco | Fb.T | Health Care Equipment and Services | Hce.S |

| Consumer Durables and Apparel | Cd.A | Automobiles and Components | A.C | Semiconductors and Semiconductor Equipment | S.Se |

| Pharmaceuticals, Biotechnology and Life Sciences | PB.Ls | Commercial and Professional Services | C.Ps | Technology Hardware and Equipment | Th.E |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhang, L.; Zhang, H.; Yang, H. Spatial Distribution Pattern of the Headquarters of Listed Firms in China. Sustainability 2018, 10, 2564. https://doi.org/10.3390/su10072564

Zhang L, Zhang H, Yang H. Spatial Distribution Pattern of the Headquarters of Listed Firms in China. Sustainability. 2018; 10(7):2564. https://doi.org/10.3390/su10072564

Chicago/Turabian StyleZhang, Ling, Hui Zhang, and Hao Yang. 2018. "Spatial Distribution Pattern of the Headquarters of Listed Firms in China" Sustainability 10, no. 7: 2564. https://doi.org/10.3390/su10072564

APA StyleZhang, L., Zhang, H., & Yang, H. (2018). Spatial Distribution Pattern of the Headquarters of Listed Firms in China. Sustainability, 10(7), 2564. https://doi.org/10.3390/su10072564