Approaches on the Screening Methods for Materiality in Sustainability Reporting

Abstract

:1. Introduction

- What are the various approaches toward defining and understanding materiality from the perspectives of different stakeholders?

- How can one avoid “re-inventing the wheel” and screen out the most important material topics using publicly available resources and by which screening methods?

- Will different screening methods (with various degrees of complexity) yield relatively consistent results in screening material topics for selected industries?

2. Research Framework

3. Research Findings

3.1. Research Question 1—Approaches toward Materiality

3.1.1. Materiality in GRI

3.1.2. Materiality in IIRC

3.1.3. Materiality in SASB

3.1.4. Materiality in ESG Reporting of SSE

3.1.5. Different Perspectives toward Materiality

3.2. Research Question 2—Screening Methods for Preliminary Assessment of Materiality

3.2.1. Approach 1: Directly Accessible—SASB Materiality Map™

3.2.2. Approach 2: Directly Accessible—GRI Sustainability Topics for Sectors

3.2.3. Approach 3: Desktop Research—GRI Sustainability Disclosure Database

3.2.4. Approach 4: Desktop Research—Modeling from a Life Cycle Perspective

3.2.5. (Dis)advantages of the Proposed Screening Methods

3.3. Research Question 3—Comparing the Selected Screening Methods

3.3.1. Case Selection, Data Collection and Analysis Method

Case Selection

- The apparel industry in Hong Kong and Italy is selected to observe the discrepancy between concerned topics by companies and GRI Topics (which should be focused on theoretically).

- The energy industry is selected with a broader geographical scope (i.e., entire Asia) to observe the consistency obtained from the GRI Topics and the concerned topics reported by the industry in Asia.

Data Collection

Analysis Method

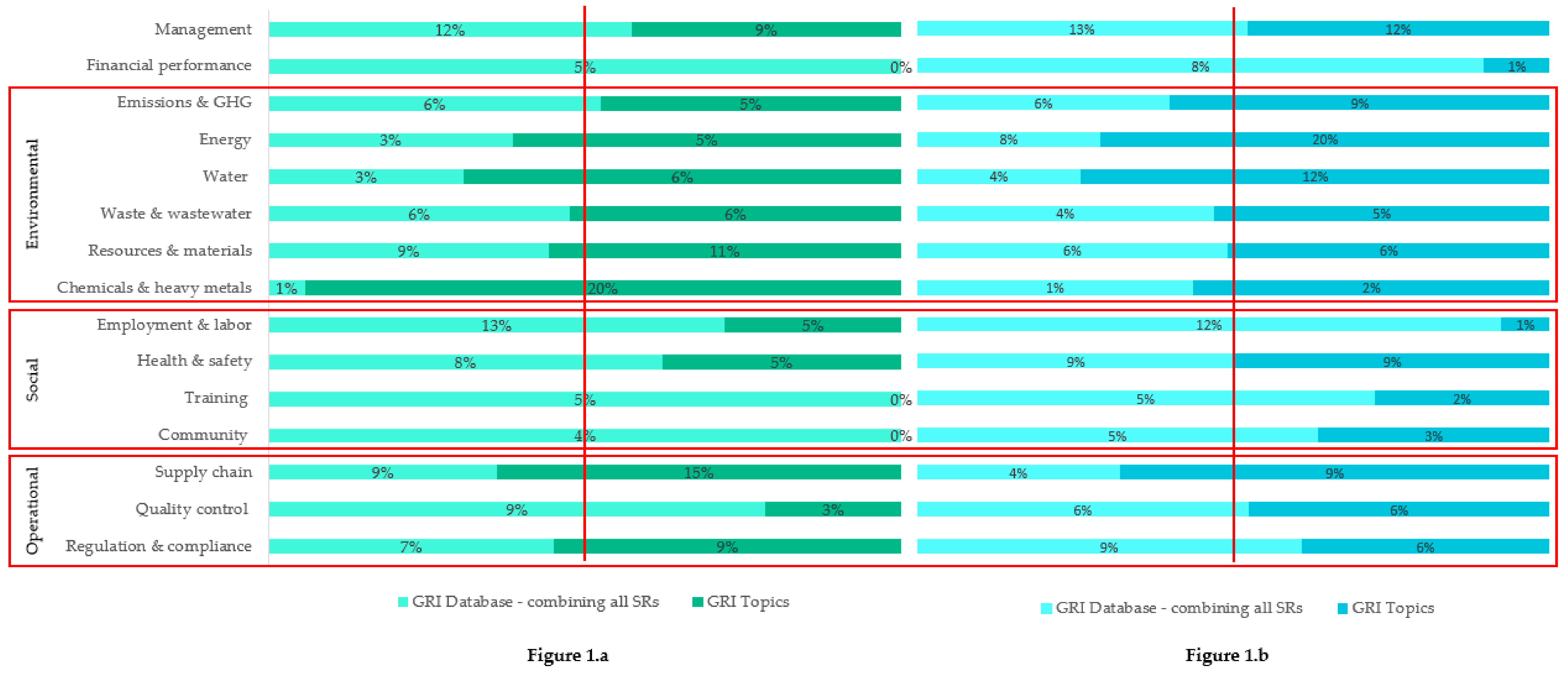

3.3.2. Comparison of GRI Database versus GRI Topics—Apparel Industry

- SRs from GRI Database indicate that the dominant material topics the industry chooses to disclose include: employment & labor, management and quality control; whereas GRI Topics considers chemicals & heavy metals, supply chain and resources & materials as the most material (Table 2). None of the most material topics align and all differ statistically.

- The two-sample proportional test shows that, statistically at a p-value of 0.1, nine out of 15 themes require similar amounts of sustainability disclosure by both GRI Database and GRI Topics, mostly on environmental topics (Table 2).

- Both approaches agree on the amounts of information disclosure on the topic relating to management. Economic information has only been disclosed by the industry and not included in GRI Topics.

- GRI Topics requires more disclosure on all environmental themes than that disclosed by the industry, except for emissions & GHG. Specifically, GRI Topics requires the highest degree of disclosure on chemicals & heavy metals (20% of total sustainability disclosure), whereas it receives the lowest amount of attention in companies’ SRs from GRI Database.

- Compared to environmental themes, reversed patterns are observed for social themes, as the industry discloses more information on all four social themes, with only health & safety results in similar proportion although statistically insignificant.

- Compared to management, economic, environmental and social themes, which show a clear pattern, the operational theme shows a more diverse result; industry tends to pay more attention to product quality whereas GRI Topics focuses more on the supply chain issues.

3.3.3. Comparison of GRI Database versus GRI Topics—Energy Industry

- SRs from GRI Database indicate that the dominant material topics the industry chooses to disclose include: management, employment & labor and regulation & compliance; whereas GRI Topics considers management, energy and water the most material (Table 2). While management topic aligns, the remaining two topics differ statistically.

- The two-sample proportional test shows that, statistically at a p-value of 0.1, 10 out of 15 themes require similar amounts of sustainability disclosure by both GRI Database and GRI Topics, including four environmental and five social themes other than management (Table 2).

- Similar findings on the disclosure on management and economic information can be found for the apparel industry.

- GRI Topics requires more disclosure on all environmental themes than those disclosed by the industry, with energy and water related topics showing statistical significance.

- Similar to the apparel industry, a reversed pattern for social themes is obtained compared to environmental aspects, as the industry discloses more information on all social themes than GRI Topics. However, only employment & labor topic shows statistical significance.

- For operational themes, GRI Topics, like the apparel industry, also focuses more on supply chain issues, whereas the other two topics do not show significant differences.

3.3.4. Implications

4. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

| Sustainability Reporting Initiatives | Targeting Audience and Managerial Focus | Disclosure Requirement | Definition and Approach toward Materiality |

|---|---|---|---|

| Global Reporting Initiatives (GRI) | Various audience; external feedback from stakeholders needs [1] | Voluntary | Approached from perspective of all stakeholders |

| Sustainable Stock Exchanges Initiatives (SASB) | Mainly targeting regulators; focus on internal management [1] | Voluntary | Approached from perspective of investors |

| International Integrated Reporting Council (IIRC) | Mainly targeting investors, focus on internal management [1] | Voluntary | Approached from perspective of investors |

| Sustainable Stock Exchanges Initiative (SSE) | Various audience and focus depending on individual reporting guidelines of individual stock exchange | Depending on individual stock exchange | Various approaches by each stock exchange. Mostly with investors, asset owners, shareholders mostly included |

| Approach | Method | Platform | Sectors Covered | Topics Covered | Advantages | Disadvantages | Licensing |

|---|---|---|---|---|---|---|---|

| Directly accessible | SASB Materiality Map™ | Online interactive tool | 10 sectors with over 70 sub-sectors | Covering SASB topics | Easy to use, quick to perform analysis and free; Solid and robust identification process of material topics, involving both objective Heat Map score and subjective Industry Working Group score. | Fixed output; Screened material topics only for SASB topics thus over-simplification if following other reporting guidelines. | Free to use, a licensing agreement with SASB needed |

| GRI Sustainability Topics for Sectors | PDF tables | 52 business sectors | 1612 Proposed Topics | Easy to use, quick to perform analysis and free; Transparent identification process of material topics and clearly stated in the report based on 616 references. | Not representative for certain industries within a specific geographical context. | N/A | |

| With desktop research | GRI Sustainability Disclosure Database | Online database | 38 business sectors | Not applicable (N/A) | Constantly evolving/adding new reports; Tailored to including targeting companies within a specific region, during a certain period. | Not directly usable; Further information processing/data analysis needed (e.g., content analysis). | Free to download reports listed on the database |

| SLCA and ELCA screening | Database and/or modeling software | N/A | N/A | Constantly evolving and adding new dataset; Science-based method with an extra layer of robustness and objectivity added; Fitting for those reporting entities following GRI guidelines with a broader stakeholder definition, including supply chain partners. | Time-consuming; Further expertise knowledge on ELCA/SLCA need; Extra cost involved. | Extra licensing and cost involved |

References

- Ortar, L. From flexibility to specificity: Practical lessons from comparing materiality in sustainability reports of the world’s largest financial institutions. Int. J. Corp. Strategy Soc. Responsib. 2016, 1, 44–64. [Google Scholar] [CrossRef]

- Calabrese, A.; Costa, R.; Rosati, F. A feedback-based model for CSR assessment and materiality analysis. Account. Forum 2015, 39, 312–327. [Google Scholar] [CrossRef] [Green Version]

- Mehra, S.J.B. Materiality Analysis: Evolution and Importance. Master Thesis, Purdue University, West Lafayette, IN, USA, 2017. [Google Scholar]

- Moneva, J.M.; Archel, P.; Correa, C. Gri and the camouflaging of corporate unsustainability. Account. Forum 2006, 30, 121–137. [Google Scholar] [CrossRef]

- Gao, S.S.; Heravi, S.; Xiao, J.Z. Determinants of corporate social and environmental reporting in Hong Kong: A research note. Account. Forum 2005, 29, 233–242. [Google Scholar] [CrossRef]

- Monteiro, S.; Aibar-Guzmán, B. Determinants of environmental disclosure in the annual reports of large companies operating in portugal. Corp. Soc. Responsib. Environ. Manag. 2010, 17, 185–204. [Google Scholar] [CrossRef]

- Bae, S.; Masud, M.; Kim, J. A cross-country investigation of corporate governance and corporate sustainability disclosure: A signaling theory perspective. Sustainability 2018, 10, 2611. [Google Scholar] [CrossRef]

- Chen, L.; Tang, O.; Feldmann, A. Applying Gri reports for the investigation of environmental management practices and company performance in Sweden, China and India. J. Clean. Prod. 2015, 98, 36–46. [Google Scholar] [CrossRef]

- Ali, W.; Frynas, J.G.; Mahmood, Z. Determinants of Corporate Social Responsibility (CSR) disclosure in developed and developing countries: A literature review. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 273–294. [Google Scholar] [CrossRef]

- Hu, M.; Loh, L. Board governance and sustainability disclosure: A cross-sectional study of Singapore-listed companies. Sustainability 2018, 10, 2578. [Google Scholar] [CrossRef]

- Said, R.; Yuserrie, H.Z.; Hasnah, H. The relationship between corporate social responsibility disclosure and corporate governance characteristics in Malaysian public listed companies. Soc. Responsib. J. 2009, 5, 212–226. [Google Scholar] [CrossRef]

- Gavana, G.; Gottardo, P.; Moisello, A. Earnings management and CSR disclosure. Family vs. Non-family firms. Sustainability 2017, 9, 2327. [Google Scholar] [CrossRef]

- Gavana, G.; Gottardo, P.; Moisello, A. Do customers value Csr disclosure? Evidence from Italian family and non-family firms. Sustainability 2018, 10, 1642. [Google Scholar] [CrossRef]

- De Villiers, C.; van Staden, C.J. Shareholders’ requirements for corporate environmental disclosures: A cross country comparison. Br. Account. Rev. 2010, 42, 227–240. [Google Scholar] [CrossRef]

- Unerman, J.; Bennett, M. Increased stakeholder dialogue and the internet: Towards greater corporate accountability or reinforcing capitalist hegemony? Account. Organ. Soc. 2004, 29, 685–707. [Google Scholar] [CrossRef]

- Adams, C.A. The ethical, social and environmental reporting-performance portrayal gap. Account. Audit. Account. J. 2004, 17, 731–757. [Google Scholar] [CrossRef]

- Norris, C.B.; Dettling, J.; Couture, J.M.; Norris, G.A.; Parent, J.; Schenck, R.; Huizen, D. Assessing the Materiality of Various Sustainability Issues in the Agrifood Sector with Lca-Based Tools: 3 Case Studies. In Proceedings of the 9th International Conference on Life Cycle Assessment in the Agri-Food Sector (LCA Food 2014), San Francisco, CA, USA, 8–10 October 2014. [Google Scholar]

- KPMG. The Kpmg Survey of Corporate Responsibility Reporting 2013. Available online: https://assets.kpmg.com/content/dam/kpmg/pdf/2015/08/kpmg-survey-of-corporate-responsibility-reporting-2013.pdf (accessed on 31 May 2018).

- KPMG. The Road Ahead—The Kpmg Survey of Corporate Responsibility Reporting 2017. Available online: https://home.kpmg.com/content/dam/kpmg/campaigns/csr/pdf/CSR_Reporting_2017.pdf (accessed on 31 May 2018).

- BMW. BMW Group Sustainable Value Report-2016. Available online: https://www.bmwgroup.com/content/dam/bmw-group-websites/bmwgroup_com/ir/downloads/en/2016/BMW-Group-SustainableValueReport-2016--EN.pdf (accessed on 31 May 2018).

- Schneider-Electric. Financial and Sustainable Development Annual Report. 2016. Available online: https://www.schneider-electric.com/ww/en/documents/finance/2017/03/2016-annual-report-tcm50-288816.pdf#page=53 (accessed on 31 May 2018).

- Manes-Rossi, F.; Tiron-Tudor, A.; Nicolò, G.; Zanellato, G. Ensuring more sustainable reporting in Europe using non-financial disclosure—De facto and de jure evidence. Sustainability 2018, 10, 1162. [Google Scholar] [CrossRef]

- Global Reporting Initiative. Materiality: What Topics should Organizations Include in Their Reports? Available online: https://www.globalreporting.org/resourcelibrary/Materiality.pdf (accessed on 11 June 2018).

- International Federation of Accountants. Materiality in <Integrated Reporting> Guidance for the Preparation of Integrated Reports. 2015. Available online: http://integratedreporting.org/wp-content/uploads/2015/11/1315_MaterialityinIR_Doc_4a_Interactive.pdf (accessed on 31 May 2018).

- Sustainability Accounting Standards Board Our Process. Available online: https://www.sasb.org/approach/our-process/ (accessed on 31 May 2018).

- Sustainability Accounting Standards Board. Why Is it Important? Available online: https://www.sasb.org/about-the-sasb/ (accessed on 31 May 2018).

- The Sustainable Stock Exchanges (SSE) Initiative. List of Partner Exchanges. Available online: http://www.sseinitiative.org/sse-partner-exchanges/list-of-partner-exchanges/ (accessed on 31 May 2018).

- The Sustainable Stock Exchanges (SSE) Initiative. ESG Guidance. Available online: http://www.sseinitiative.org/esg-guidance/ (accessed on 31 May 2018).

- Singapore Stock Exchange. Sgx-st Listing Rules Practice Note 7.6 Sustainability Reporting Guide. 2016. Available online: http://rulebook.sgx.com/net_file_store/new_rulebooks/s/g/SGX_Mainboard_Practice_Note_7.6_July_20_2016.pdf (accessed on 31 May 2018).

- Financial Services Council, Australian Council of Superannuation Investors. ESG Reporting Guide for Australian Companies 2015. Available online: https://www.acsi.org.au/images/stories/ACSIDocuments/ESG_Reporting_Guide_Final_2015 single_page.pdf (accessed on 31 May 2018).

- Shenzhen Stock Exchange Social Responsibility Instructions to Listed Companies 2011. Available online: http://www.szse.cn/main/en/RulesandRegulations/SZSERules/GeneralRules/10636.shtml (accessed on 31 May 2018).

- Masud, M.; Hossain, M.; Kim, J. Is Green Regulation Effective or a Failure: Comparative Analysis between Bangladesh Bank (BB) Green Guidelines and Global Reporting Initiative Guidelines. Sustainability 2018, 10, 1267. [Google Scholar] [CrossRef]

- Global Reporting Initiative. Defining What Matters: Do Companies and Investors Agree on What Is Material? 2016. Available online: https://www.globalreporting.org/resourcelibrary/GRI-DefiningMateriality2016.pdf (accessed on 31 May 2018).

- Sustainability Accounting Standards Board. SASB Materiality Map. Available online: https://www.sasb.org/materiality/sasb-materiality-map/ (accessed on 31 May 2018).

- Global Reporting Initiative. Sustainability Topics for Sectors. Available online: https://www.globalreporting.org/Pages/default.aspx (accessed on 31 May 2018).

- Sustainability Topics for Sectors. What Do Stakeholders Want to Know? Available online: https://www.globalreporting.org/resourcelibrary/References.pdf (accessed on 31 May 2018).

- Global Reporting Initiative. Gri’s Sustainability Disclosure Database. Available online: http://database.globalreporting.org/about-this-site (accessed on 31 May 2018).

- Turker, D.; Altuntas, C. Sustainable supply chain management in the fast fashion industry: An analysis of corporate reports. Eur. Manag. J. 2014, 32, 837–849. [Google Scholar] [CrossRef]

- Kleindorfer, P.R.; Singhal, K.; Wassenhove, L.N. Sustainable operations management. Prod. Oper. Manag. 2005, 14, 482–492. [Google Scholar] [CrossRef]

- Guthrie, J.; Abeysekera, I. Content analysis of social, environmental reporting: What is new? J. Hum. Resour. Cost. Account. 2006, 10, 114–126. [Google Scholar] [CrossRef]

- Hsu, C.W.; Lee, W.H.; Chao, W.C. Materiality analysis model in sustainability reporting: A case study at lite-on technology corporation. J. Clean. Prod. 2013, 57, 142–151. [Google Scholar] [CrossRef]

- Norris, C.B.; Norris, C.A. Can conducting a social LCA helps meeting major social responsibility standards requirements? In Proceedings of the 4th SocSem—Social-lca.cirad.fr, Montpellier, France, 21 November 2014. [Google Scholar]

- Norris, G.; Norris, C.B. Sustainable Brands. Social materiality: The Importance of a Life Cycle-Based Approach. 2014. Available online: http://www.sustainablebrands.com/news_and_views/supply_chain/greg_norris/social_materiality_importance_life_cycle-based_approach (accessed on 31 May 2018).

- Global Reporting Initiative. The Sustainability Topics for Sectors: What Do Stakeholders Want to Know? 2013. Available online: https://www.globalreporting.org/resourcelibrary/sustainability-topics.pdf (accessed on 31 May 2018).

- Mieras, E. Business Decision Making: Materiality Assessment vs. Hotspot Analysis. Available online: https://www.pre-sustainability.com/news/business-decision-making-materiality-assessment-vs.-hotspot-analysis (accessed on 31 May 2018).

- Cantele, S.; Tsalis, T.; Nikolaou, I. A new framework for assessing the sustainability reporting disclosure of water utilities. Sustainability 2018, 10, 433. [Google Scholar] [CrossRef]

- Global Reporting Initiative. Gri Reports List. Available online: https://www.globalreporting.org/services/Analysis/Reports_List/Pages/default.aspx (accessed on 31 May 2018).

- Masud, M.A.; Mi Bae, S.; Kim, J.D. Analysis of environmental accounting and reporting practices of listed banking companies in Bangladesh. Sustainability 2017, 10, 1717. [Google Scholar] [CrossRef]

- Beck, A.C.; Campbell, D.; Shrives, P.J. Content analysis in environmental reporting research: Enrichment and rehearsal of the method in a British–German context. Br. Account. Rev. 2010, 42, 207–222. [Google Scholar] [CrossRef]

| Sustainable Business Category | Content Theme | Keywords Selected |

|---|---|---|

| Management | Management | Management, governance |

| Economic | Financial performance | Cash, fiscal, economic, financial |

| Environment | Emissions & GHG | Emission, greenhouse gas (GHG), carbon |

| Energy | Energy, energy(in)efficiency, energy-saving, energy-use | |

| Water | Freshwater, water, groundwater, base saving, atershed | |

| Waste & wastewater | Waste, wastewater, disposal, landfill, recycle | |

| Resources & materials | Material, resource, package | |

| Chemicals & heavy metals | Chemical, metal, pesticide, chromium, cobalt, copper, lead, mercury, nickel, zinc | |

| Social | Employment & labor | Employ, labor |

| Health & safety | Health, safety, injury | |

| Training | Train, educate | |

| Community | Community, volunteer, donate | |

| Operational | Supply chain | Supplier, sourcing |

| Quality control | Quality, complaint | |

| Regulation & compliance | Compliance, regulate, specification, standard, law |

| Theme | Industry | Absolute Word Counts | Proportional Word Counts | p-Value (Two Sample Proportional Test) | ||

|---|---|---|---|---|---|---|

| GRI Database | GRI Topics | GRI Database | GRI Topics | |||

| Management | Apparel | 533 | 7 | 12% (#2, A) | 9% | 0.515 |

| Energy | 5163 | 12 | 13% (#1, E) | 12% (#2, E) | 0.864 | |

| Financial performance | Apparel | 237 | 0 | 5% | 0% | 0.065 * |

| Energy | 3419 | 1 | 8% | 1% | 0.011 ** | |

| Emissions & GHG | Apparel | 250 | 4 | 6% | 5% | 1 |

| Energy | 2370 | 9 | 6% | 9% | 0.295 | |

| Energy | Apparel | 142 | 4 | 3% | 5% | 0.531 |

| Energy | 3391 | 21 | 8% | 20% (#1, E) | <0.001 ** | |

| Water | Apparel | 126 | 5 | 3% | 6% | 0.130 |

| Energy | 1660 | 12 | 4% | 12% (#2, E) | <0.001 ** | |

| Waste & wastewater | Apparel | 257 | 5 | 6% | 6% | 1 |

| Energy | 1746 | 5 | 4% | 5% | 0.971 | |

| Resources & materials | Apparel | 404 | 9 | 9% | 11% (#3, A) | 0.594 |

| Energy | 2289 | 6 | 6% | 6% | 1 | |

| Chemicals % heavy metals | Apparel | 54 | 16 | 1% | 20% (#1, A) | <0.001 ** |

| Energy | 612 | 2 | 1% | 2% | 1 | |

| Employment & labor | Apparel | 585 | 4 | 13% (#1, A) | 5% | 0.054 * |

| Energy | 4743 | 1 | 12% (#2, E) | 1% | 0.001 ** | |

| Health & safety | Apparel | 372 | 4 | 8% | 5% | 0.406 |

| Energy | 3590 | 9 | 9% | 9% | 1 | |

| Training | Apparel | 208 | 0 | 5% | 0% | 0.091 * |

| Energy | 2060 | 2 | 5% | 2% | 0.222 | |

| Community | Apparel | 193 | 0 | 4% | 0% | 0.109 |

| Energy | 2049 | 3 | 5% | 3% | 0.447 | |

| Supply chain | Apparel | 383 | 12 | 9% | 15% (#2, A) | 0.060 * |

| Energy | 1679 | 9 | 4% | 9% | 0.036 ** | |

| Quality control | Apparel | 413 | 2 | 9% (#3, A) | 3% | 0.064 * |

| Energy | 2611 | 6 | 6% | 6% | 0.963 | |

| Regulation & compliance | Apparel | 325 | 7 | 7% | 9% | 0.743 |

| Energy | 3665 | 6 | 9% (#3, E) | 6% | 0.339 | |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wu, S.R.; Shao, C.; Chen, J. Approaches on the Screening Methods for Materiality in Sustainability Reporting. Sustainability 2018, 10, 3233. https://doi.org/10.3390/su10093233

Wu SR, Shao C, Chen J. Approaches on the Screening Methods for Materiality in Sustainability Reporting. Sustainability. 2018; 10(9):3233. https://doi.org/10.3390/su10093233

Chicago/Turabian StyleWu, Susie Ruqun, Changliang Shao, and Jiquan Chen. 2018. "Approaches on the Screening Methods for Materiality in Sustainability Reporting" Sustainability 10, no. 9: 3233. https://doi.org/10.3390/su10093233

APA StyleWu, S. R., Shao, C., & Chen, J. (2018). Approaches on the Screening Methods for Materiality in Sustainability Reporting. Sustainability, 10(9), 3233. https://doi.org/10.3390/su10093233