An Optimal Management Strategy of Carbon Forestry with a Stochastic Price

Abstract

:1. Introduction

2. Methods

3. Results

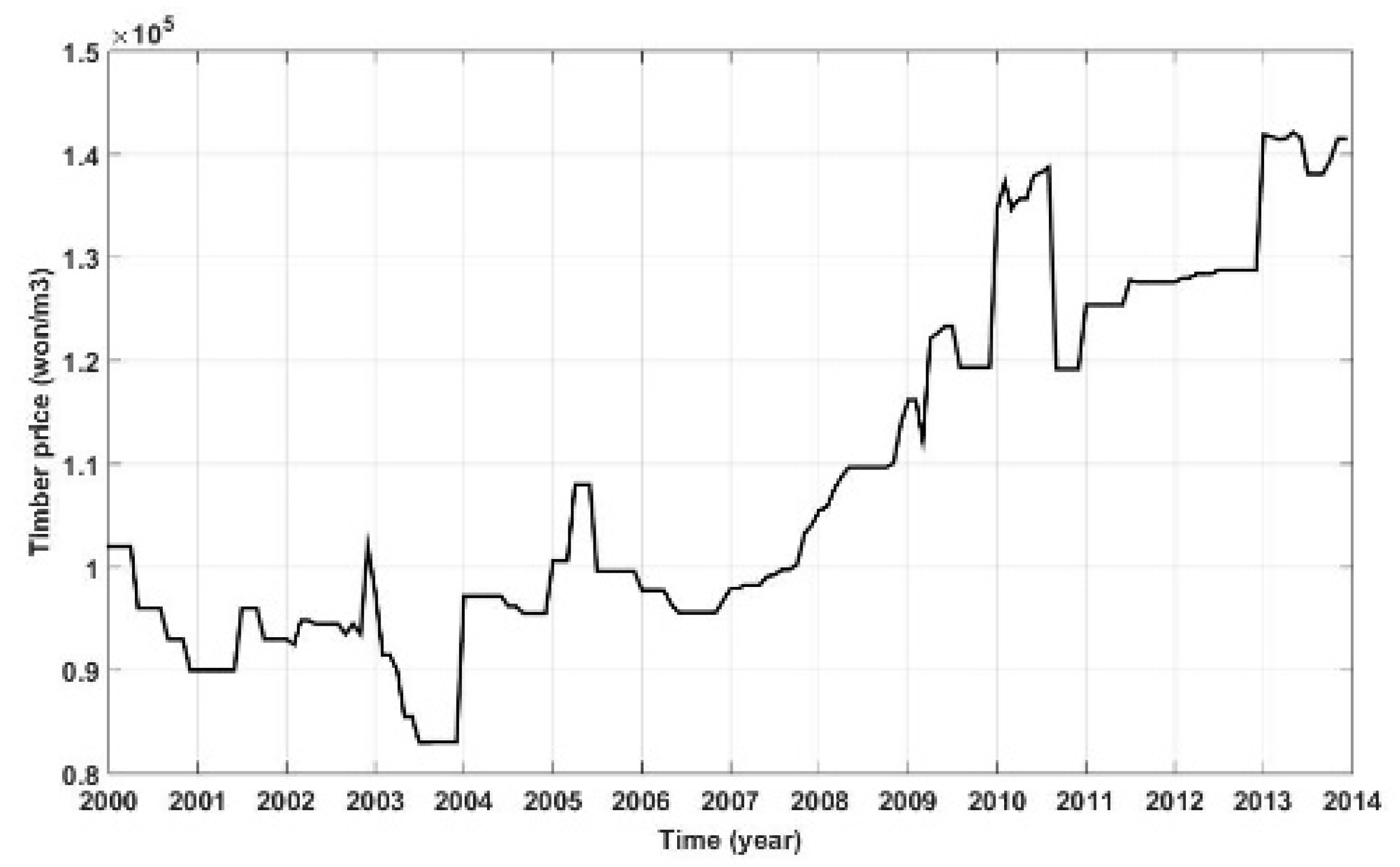

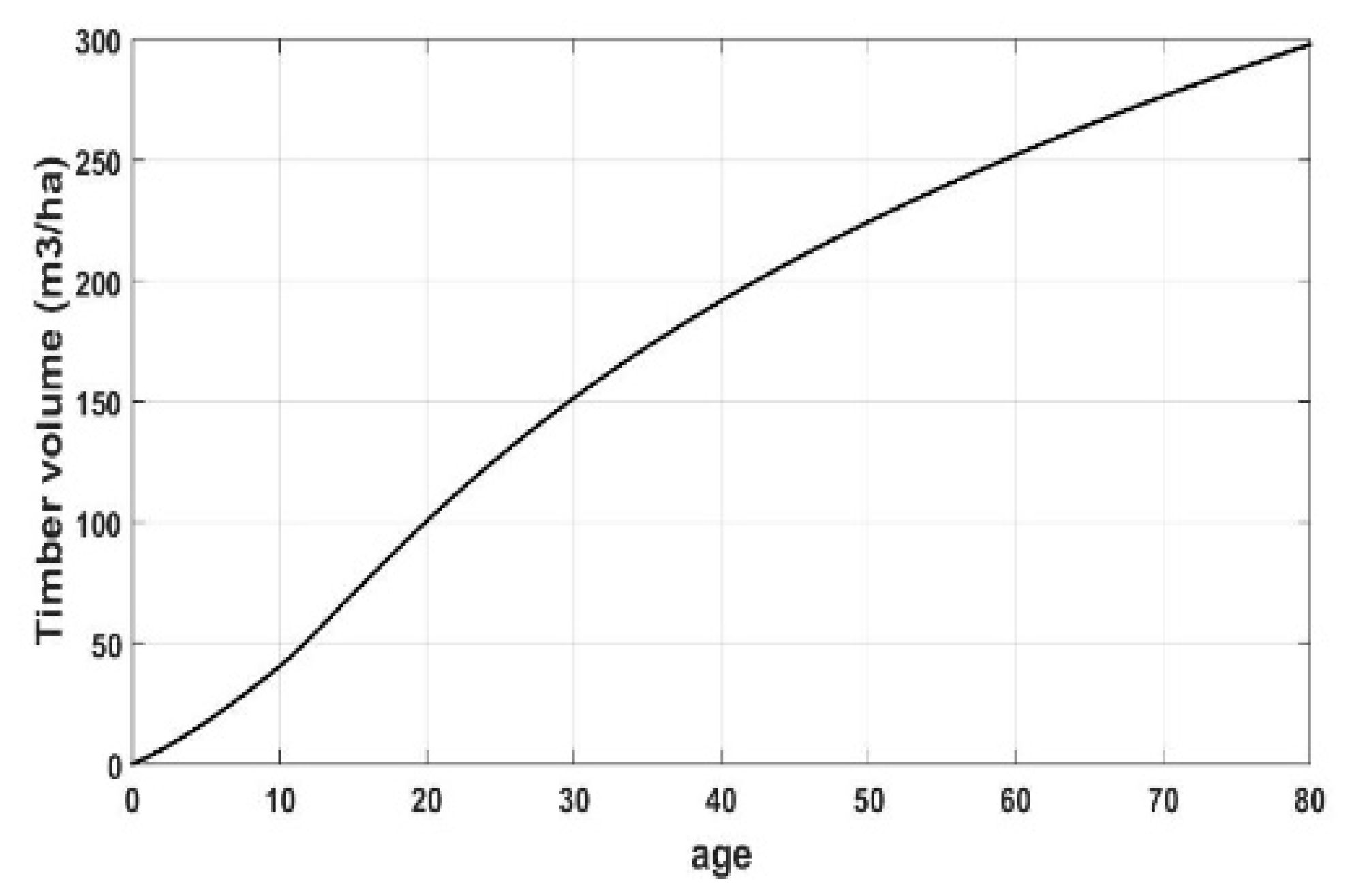

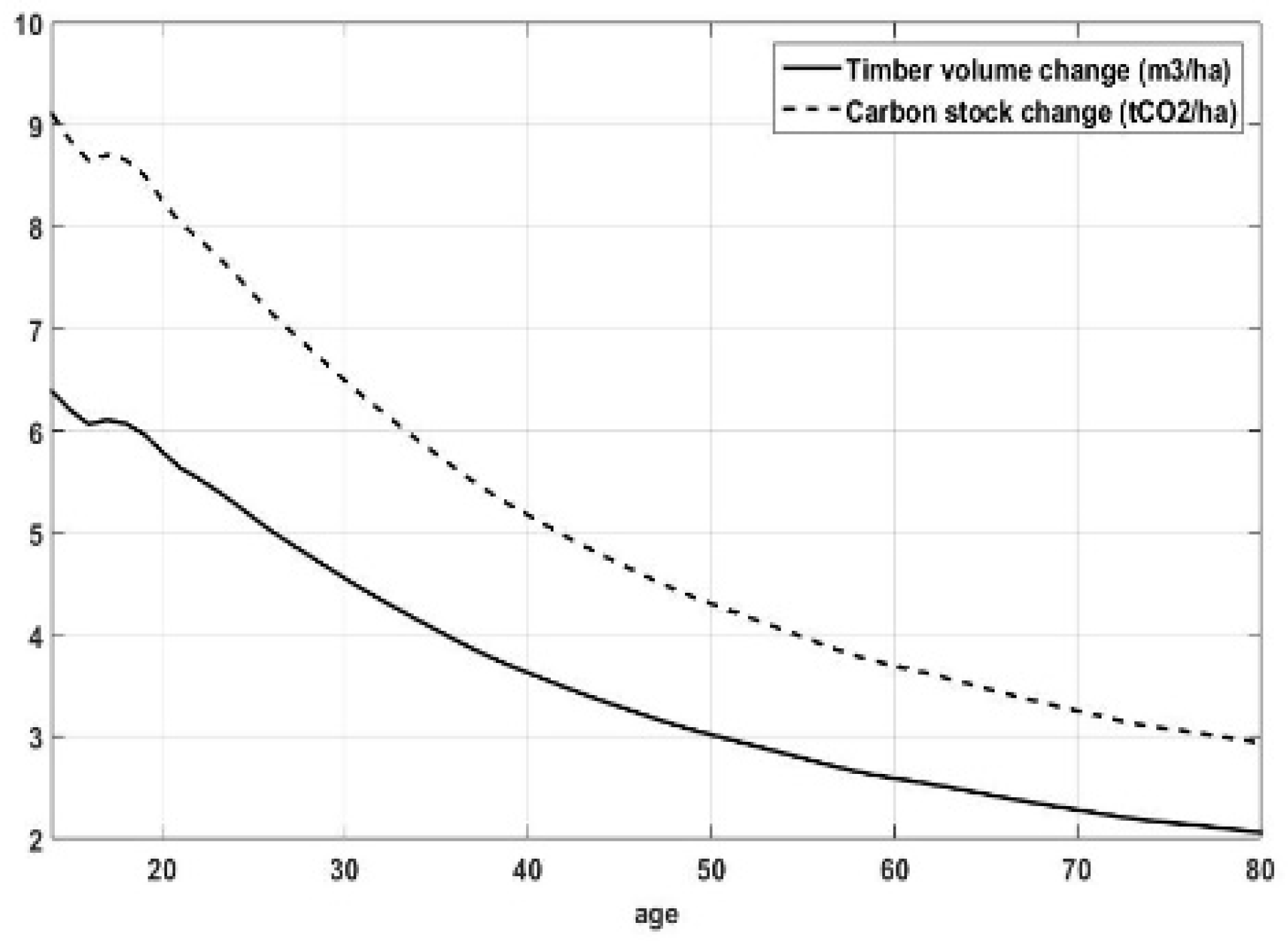

3.1. Data Description

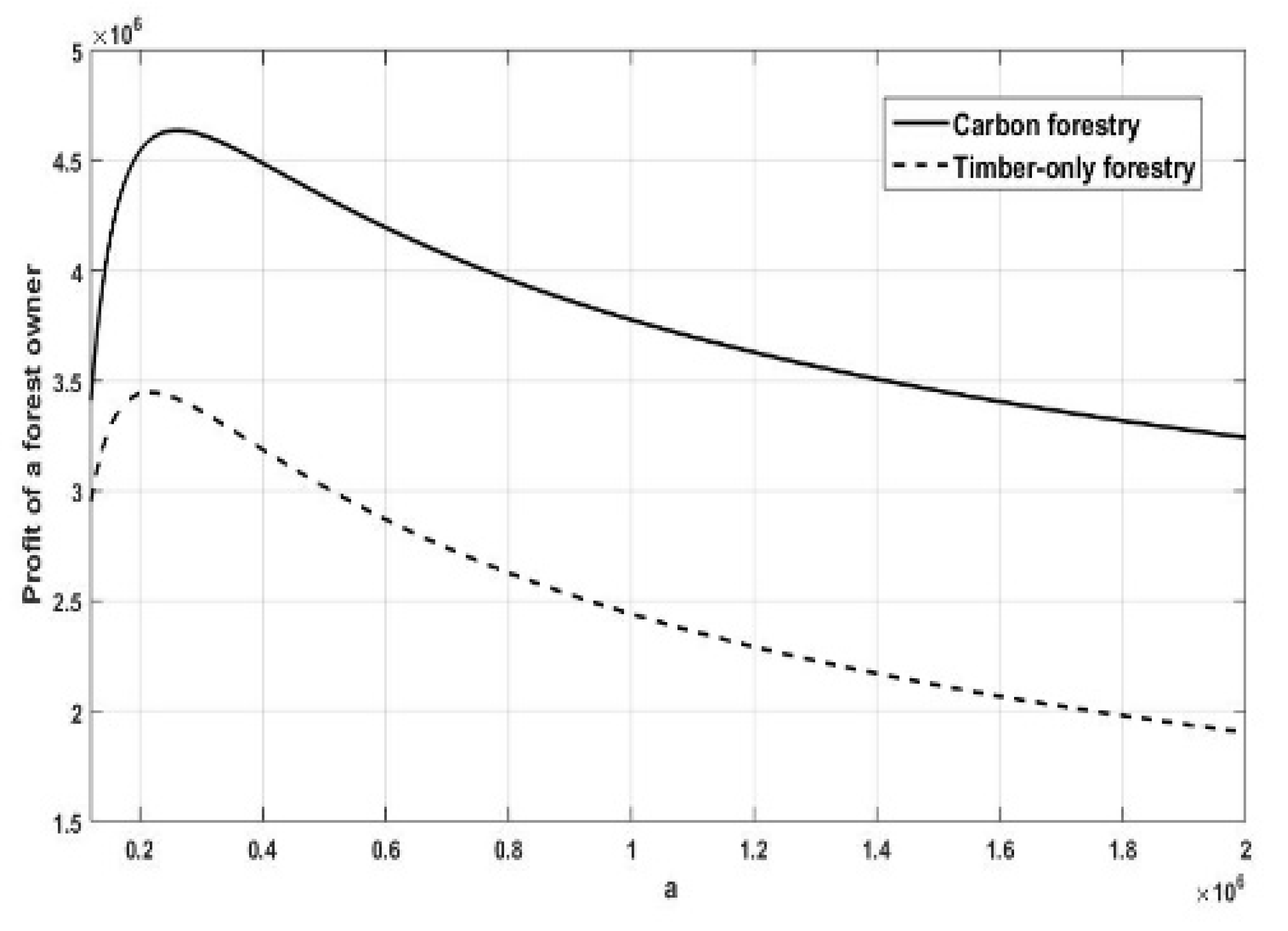

3.2. Empirical Result

4. Discussion

Author Contributions

Funding

Conflicts of Interest

References

- Edenhofer, O.; Pichs-Madruga, R.; Sokona, Y.; Farahani, E.; Kadner, S.; Seyboth, K.; Adler, A.; Baum, I.; Brunner, S.; Eickemeier, P.; et al. IPCC, 2014: Summary for Policymakers. In Climate Change 2014: Mitigation of Climate Change. Contribution of Working Group III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change; Cambridge University Press: Cambridge, UK; New York, NY, USA, 2014; pp. 7–8. ISBN 978-1-107-05821-7. [Google Scholar]

- Kim, E.G.; Park, S.B.; Kim, D.H. A Review on the New Zealand Forest Emissions Trading Scheme. Korean J. For. Econ. 2008, 16, 1–19. [Google Scholar]

- Lee, S.-M.; Kim, K.-D.; Song, S.-H. Optimal Forest Management Schemes with Carbon Storage Value Included. J. Rural Dev. 2011, 34, 59–81. [Google Scholar]

- Min, K.-T. An Analysis of Forest Cutting Age with Consideration of Forest Carbon Sequestration. J. Rural Dev. 2011, 34, 43–54. [Google Scholar]

- Jang, H.S.; Park, H.J.; Choi, Y.T. Real Option Analysis of A/R CDM Project Considering CER Price Uncertainty. J. Econ. Stud. 2010, 28, 143–161. [Google Scholar]

- Brazee, R.; Mendelsohn, R. Timber Harvesting with Fluctuating Prices. For. Sci. 1998, 34, 359–372. [Google Scholar]

- Englin, J.; Callaway, J.M. Global Climate Change and Optimal Forest Management. Nat. Resour. Model. 1993, 7, 191–202. [Google Scholar] [CrossRef]

- Chladná, Z. Determination of Optimal Rotation Period under Stochastic Wood and Carbon Prices. For. Policy Econ. 2007, 9, 1031–1045. [Google Scholar] [CrossRef]

- Guthrie, G.; Kumareswaran, D. Carbon Subsidies, Taxes and Optimal Forest Management. Environ. Resour. Econ. 2009, 43, 275–293. [Google Scholar] [CrossRef]

- Tee, J.; Scarpa, R.; Marsh, D.; Guthrie, G. Forest valuation under the New Zealand Emissions Trading Scheme: A Real Options Binomial Tree with Stochastic Carbon and Timber Prices. Land Econ. 2014, 90, 44–60. [Google Scholar] [CrossRef]

- Chang, F.R. On the Elasticities of Harvesting Rules. J. Econ. Dyn. Control 2005, 29, 469–485. [Google Scholar] [CrossRef]

- Harrison, J.M. Brownian Motion and Stochastic Flow Systems; John Wiley & Sons Inc.: New York, NY, USA, 1985; pp. 89–91. ISBN 10: 0471819395. [Google Scholar]

- Koo, G.-B.; Bae, S.-W.; Ryu, S.-H.; Lee, C.-Y.; Kim, K.-W.; Park, B.-W.; Hong, S.-C.; Noh, E.-W.; Hong, K.-N.; Han, S.-U. Economic Tree Species ④ Larix kaemferi, 55; Korea Forest Research Institute: Seoul, Korea, 2012; ISBN 978-89-8176-900-0. [Google Scholar]

- Kim, Y.-H.; Jeon, E.-J.; Shin, M.-Y.; Chung, I.-B.; Lee, S.-T.; Seo, K.-W.; Pho, J.-K. A study on the Baseline Carbon Stock for Major Species in Korea for Conducting Carbon Offset Projects based on Forest Management Projects. J. Korean Soc. For. Sci. 2014, 103, 439–445. [Google Scholar] [CrossRef]

- Shin, S.-W. The Statistical Yearbook of Forestry 2001, 31; Korea Forest Service: Daejeon, Korea, 2001; p. 322. ISBN 11-1400000-000001-10. [Google Scholar]

- Kim, B.-I. The Statistical Yearbook of Forestry 2002, 32; Korea Forest Service: Deajeon, Korea, 2002; p. 328. ISBN 11-1400000-000001-10. [Google Scholar]

- Choi, J.-S. The Statistical Yearbook of Forestry 2003, 33; Korea Forest Service: Deajeon, Korea, 2003; p. 330. ISBN 11-1400000-000001-10. [Google Scholar]

- Cho, Y.-H. The Statistical Yearbook of Forestry 2004, 34; Korea Forest Service: Deajeon, Korea, 2004; p. 314. ISBN 11-1400000-000001-10. [Google Scholar]

- Cho, Y.-H. The Statistical Yearbook of Forestry 2005, 35; Korea Forest Service: Deajeon, Korea, 2005; p. 342. ISBN 11-1400000-000001-10. [Google Scholar]

- Suh, S.-J. The Statistical Yearbook of Forestry 2006, 36; Korea Forest Service: Deajeon, Korea, 2006; p. 350. ISBN 11-1400000-000001-10. [Google Scholar]

- Suh, S.-J. The Statistical Yearbook of Forestry 2007, 37; Korea Forest Service: Deajeon, Korea, 2007; p. 352. ISBN 11-1400000-000001-10. [Google Scholar]

- Ha, Y.-J. The Statistical Yearbook of Forestry 2008, 38; Korea Forest Service: Deajeon, Korea, 2008; p. 356. ISBN 11-1400000-000001-10. [Google Scholar]

- Chung, K.-S. The Statistical Yearbook of Forestry 2009, 39; Korea Forest Service: Deajeon, Korea, 2009; p. 352. ISBN 11-1400000-000001-10. [Google Scholar]

- Chung, K.-S. The Statistical Yearbook of Forestry 2010, 40; Korea Forest Service: Deajeon, Korea, 2010; p. 352. ISBN 11-1400000-000001-10. [Google Scholar]

- Lee, D.-K. The Statistical Yearbook of Forestry 2011, 41; Korea Forest Service: Deajeon, Korea, 2011; p. 360. ISBN 11-1400000-000001-10. [Google Scholar]

- Lee, D.-K. The Statistical Yearbook of Forestry 2012, 42; Korea Forest Service: Deajeon, Korea, 2012; p. 364. ISBN 11-1400000-000001-10. [Google Scholar]

- Shin, W.-S. The Statistical Yearbook of Forestry 2013, 43; Korea Forest Service: Deajeon, Korea, 2013; p. 356. ISBN 11-1400000-000001-10. [Google Scholar]

- Tsay, R.S. Analysis of Financial Time Series; John Wiley & Sons: New York, NY, USA, 2005; pp. 56–61. [Google Scholar]

- Goo, G.-J.; Son, Y.-M.; Lee, K.-H.; Kwon, S.-D.; Pyo, J.-K.; Lim, S.-S.; Yoon, H.-J. Volume·Biomass and Stand Yield Table; Korea Forest Service & Korea Forest Research Institute: Seoul, Korea, 2012; p. 195. ISBN 978-89-8176-875-1. [Google Scholar]

- Korea Forest Service. Available online: http://www.forest.go.kr/newkfsweb/html/HtmlPage.do?pg=/fcm/UI_FCS_122030.html&mn=KFS_02_10_12_20_30&orgId=fcm (accessed on 13 September 2018).

- Park, K.-G. KEI Focus: The State and the Issue of Emission Trading Scheme, 3; Korea Environment Institute: Sejong, Korea, 2015. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Basic Wood Density (D) (tdm/m3) | Biomass Expansion Factor (BEF) | Root-Shot Ratio (R) | Carbon Faction (CF) |

|---|---|---|---|

| 0.45 | 1.34 | 0.29 | 0.5 |

| Parameter | Estimates |

|---|---|

| The drift rate, | 0.02 |

| The volatility rate, | 0.09 |

| The negative growth rate of , | 0.018 |

| The growth rate of , | 0.196 |

| The sequestration factor, | 1.4261 |

| The discount rate, | 0.05 |

| The offset credit price, | 10,000 won |

| The initial timber volume, | 64.5 m3/ha |

| The initial change of timber volume, | 6.38 m3/ha/year |

| The initial price of timber, | 102,000 won |

| The harvesting cost, | 62,500 won/m3 |

| The penalty, | 0 won |

| Variable | Coefficient | Std. Error |

|---|---|---|

| AGE | 5.133933 | 0.110198 |

| AGE2 | −0.002411 | 0.004242 |

| AGE3 | −0.000203 | 0.026278 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yoo, S.; Cho, Y.-s.; Park, H. An Optimal Management Strategy of Carbon Forestry with a Stochastic Price. Sustainability 2018, 10, 3290. https://doi.org/10.3390/su10093290

Yoo S, Cho Y-s, Park H. An Optimal Management Strategy of Carbon Forestry with a Stochastic Price. Sustainability. 2018; 10(9):3290. https://doi.org/10.3390/su10093290

Chicago/Turabian StyleYoo, Sora, Yong-sung Cho, and Hojeong Park. 2018. "An Optimal Management Strategy of Carbon Forestry with a Stochastic Price" Sustainability 10, no. 9: 3290. https://doi.org/10.3390/su10093290

APA StyleYoo, S., Cho, Y. -s., & Park, H. (2018). An Optimal Management Strategy of Carbon Forestry with a Stochastic Price. Sustainability, 10(9), 3290. https://doi.org/10.3390/su10093290