Managing Procurement for a Firm with Two Ordering Opportunities under Supply Disruption Risk

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

2. Literature Review

- (1)

- The authors study how a firm should take full advantage of multiple ordering opportunities and different procurement strategies to mitigate supply disruption and demand risks and improve the reliability of the supply chain;

- (2)

- Beside the supply risk and demand risk, the authors also consider the uncertainty of the emergency procurement price at selling season in this model and explore the impacts of random supply, demand, and emergency procurement price on the firm’s procurement strategy and supply chain performance;

- (3)

- Under the constantly changing operational environment, the authors investigate how a firm should adjust the procurement strategy to maintain the sustainability of the supply chain and even improve supply chain performance.

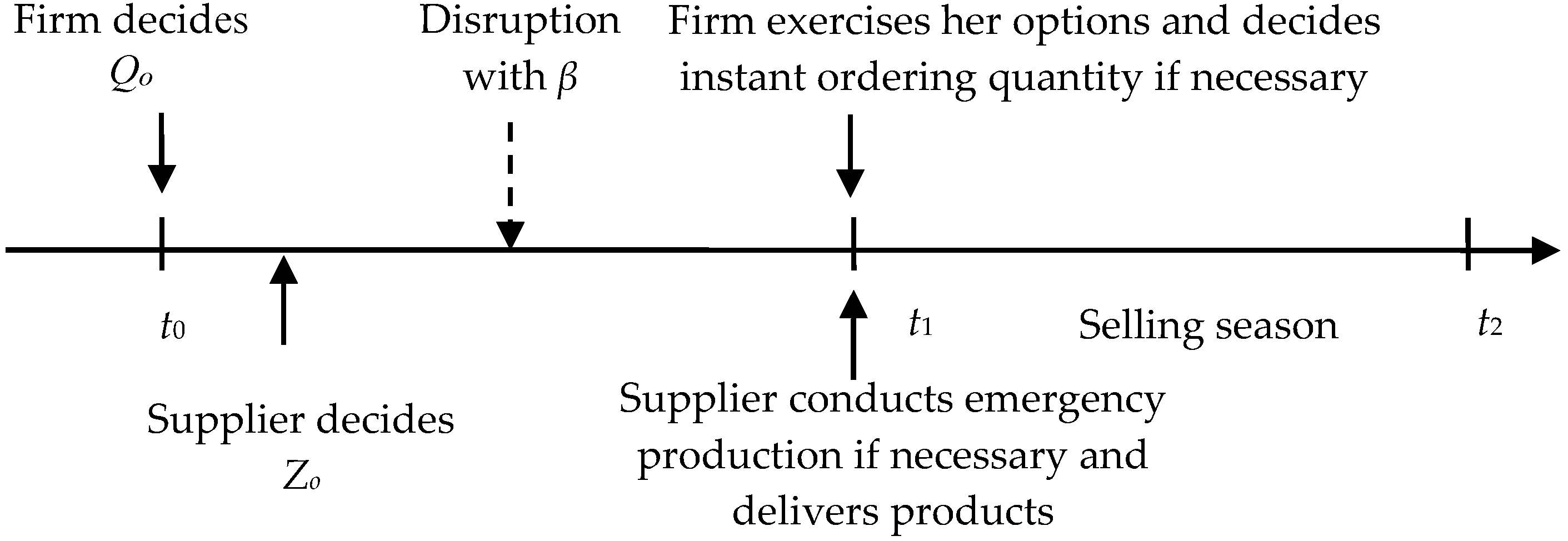

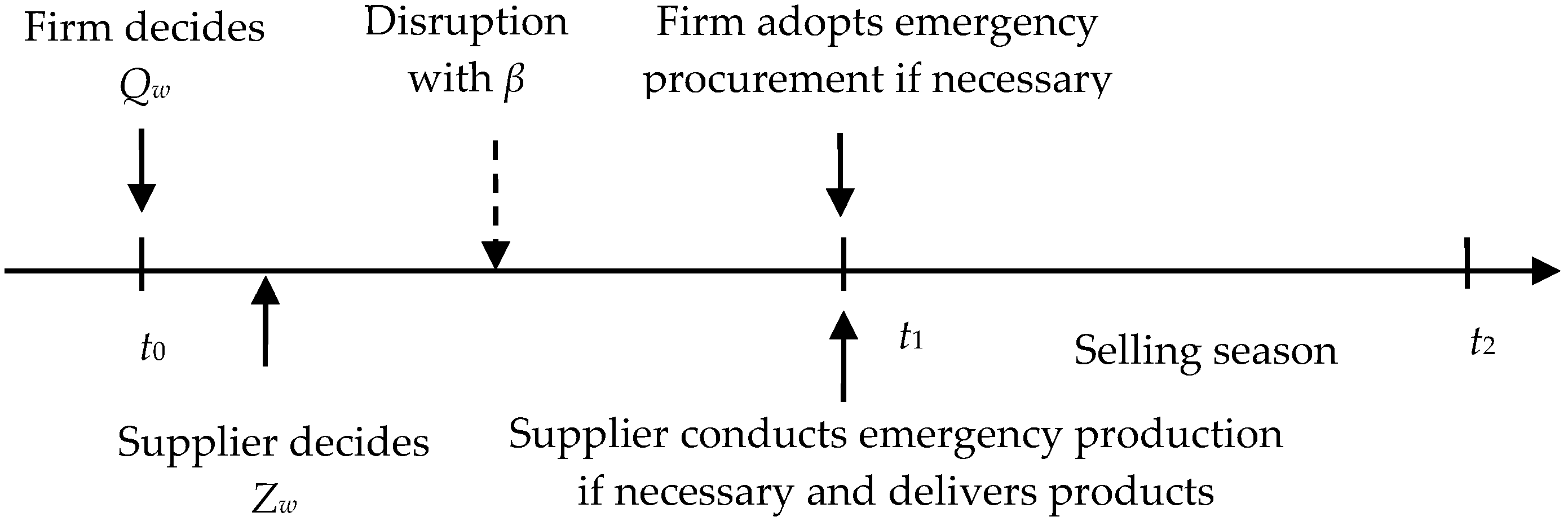

3. Model Descriptions

| C | Supplier’s production cost per unit |

| S | Product’s salvage value per unit |

| ce | Supplier’s emergency production cost per unit |

| β | Probability of disruption occurrence |

| ζ, f(·), F(·) μ | Random market demand and its PDF, CDF and mean value |

| co | Option price per unit |

| w | Option exercise price or wholesale price per unit |

| r | Product’s retail price per unit |

| P, g(p), G(p) | Random emergency procurement price and its PDF and CDF, P ∈ [A, B] |

| , | The profit, and expected profit of j under i strategy, i = {O, W}, O = option purchase strategy, W = procurement commitment strategy, j = {S, R}, S = supplier, R = firm |

| Decision variables | |

| Zi | Supplier’s production quantity under i strategy |

| Qi | Firm’s (option) order quantity under i strategy |

- (1)

- , which ensures the salvage value is lower than the production cost;

- (2)

- and , which ensure the supplier and the firm both have positive profits under the OP strategy;

- (3)

- , which represents the emergency production cost is higher than the normal production cost;

- (4)

- , which ensures the firm can achieve positive profit through instant ordering;

- (5)

- , which denotes the emergency purchase price is higher than the option purchase price;

- (6)

- , which ensures the supplier has a positive profit if he produces.

4. Model Analyses

4.1. Option Purchase Strategy

4.1.1. Supplier’s Production Decision

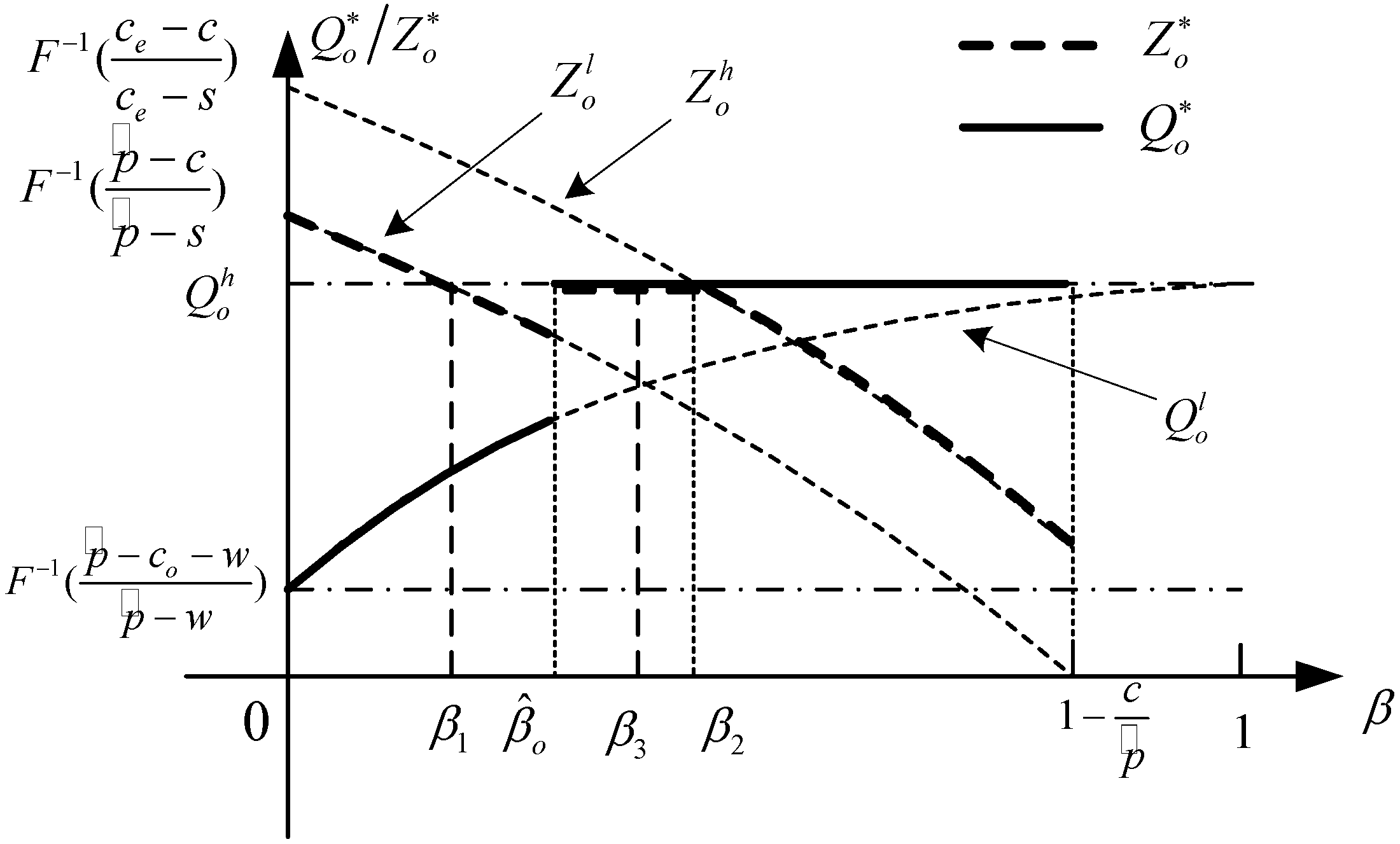

4.1.2. Firm’s Procurement Decision

- (i)

- when , then , ;

- (ii)

- when , , ;

4.2. Procurement Commitment Strategy

4.2.1. Supplier’s Production Decision

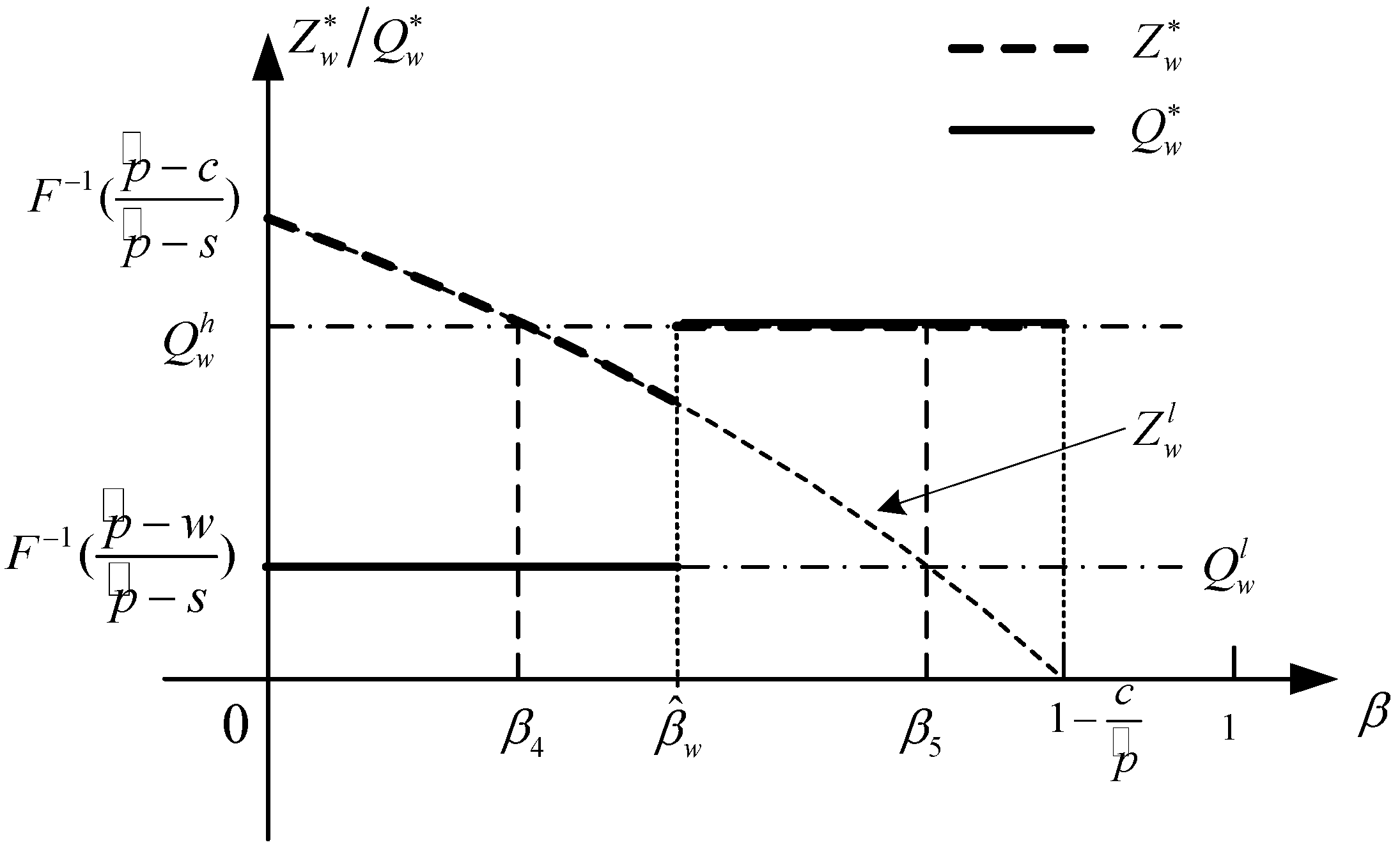

4.2.2. Firm’s Procurement Decision

- (i)

- if, then, ;

- (ii)

- if, then, wheresatisfies,satisfiesandcan be formulated as:

5. Comparisons

5.1. Optimal Decisions and Profits of the Supplier and Firm under the Two Types of Strategies

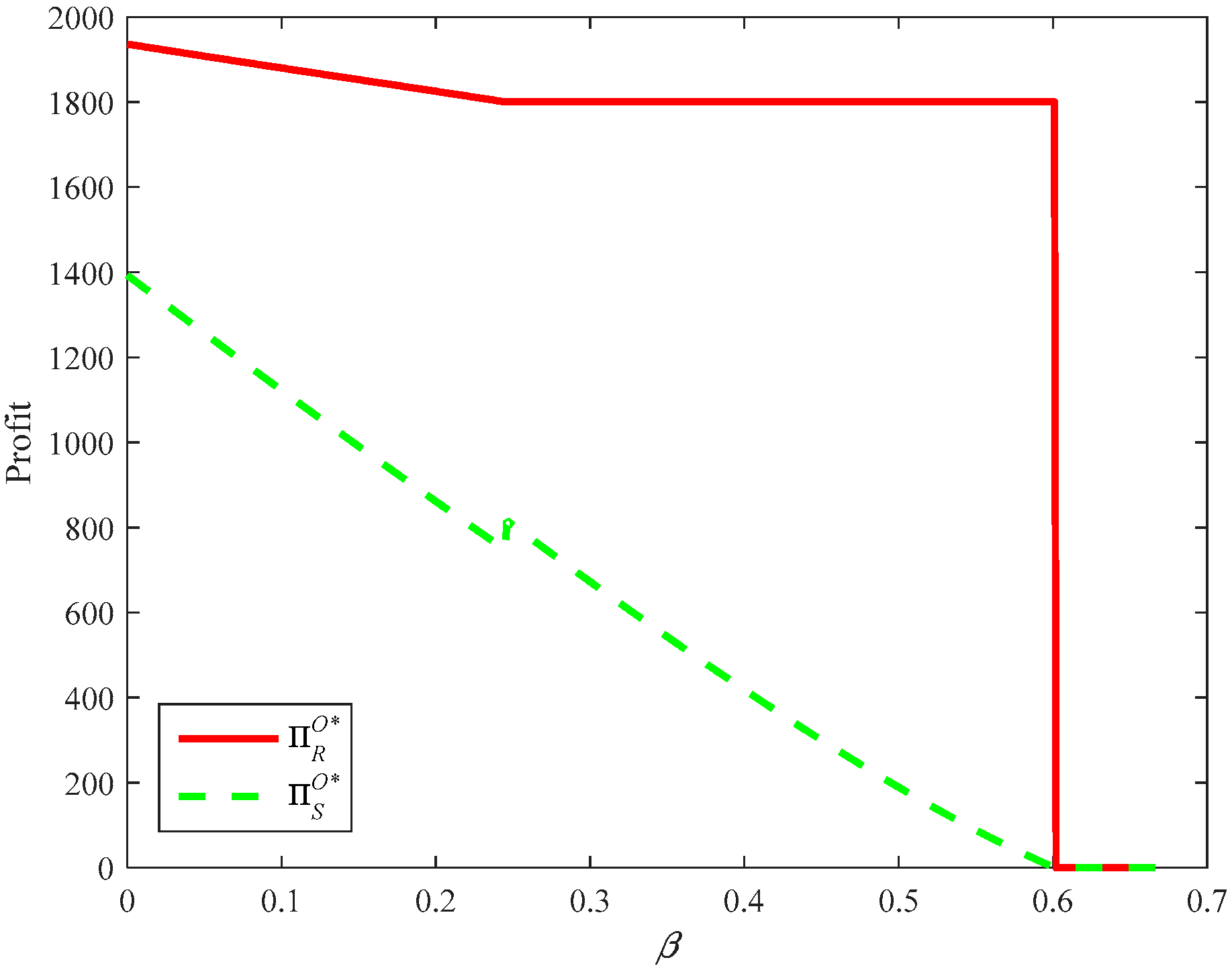

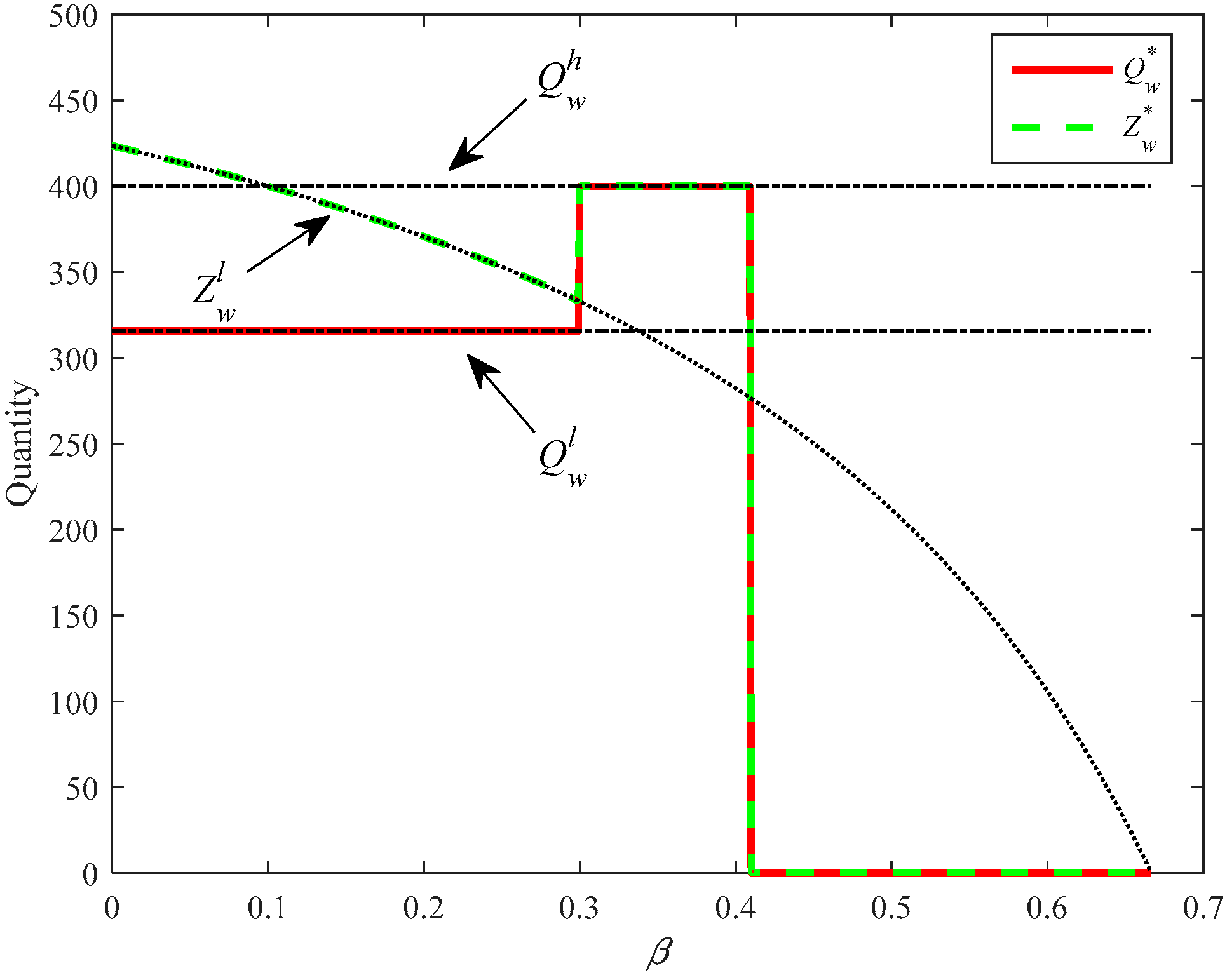

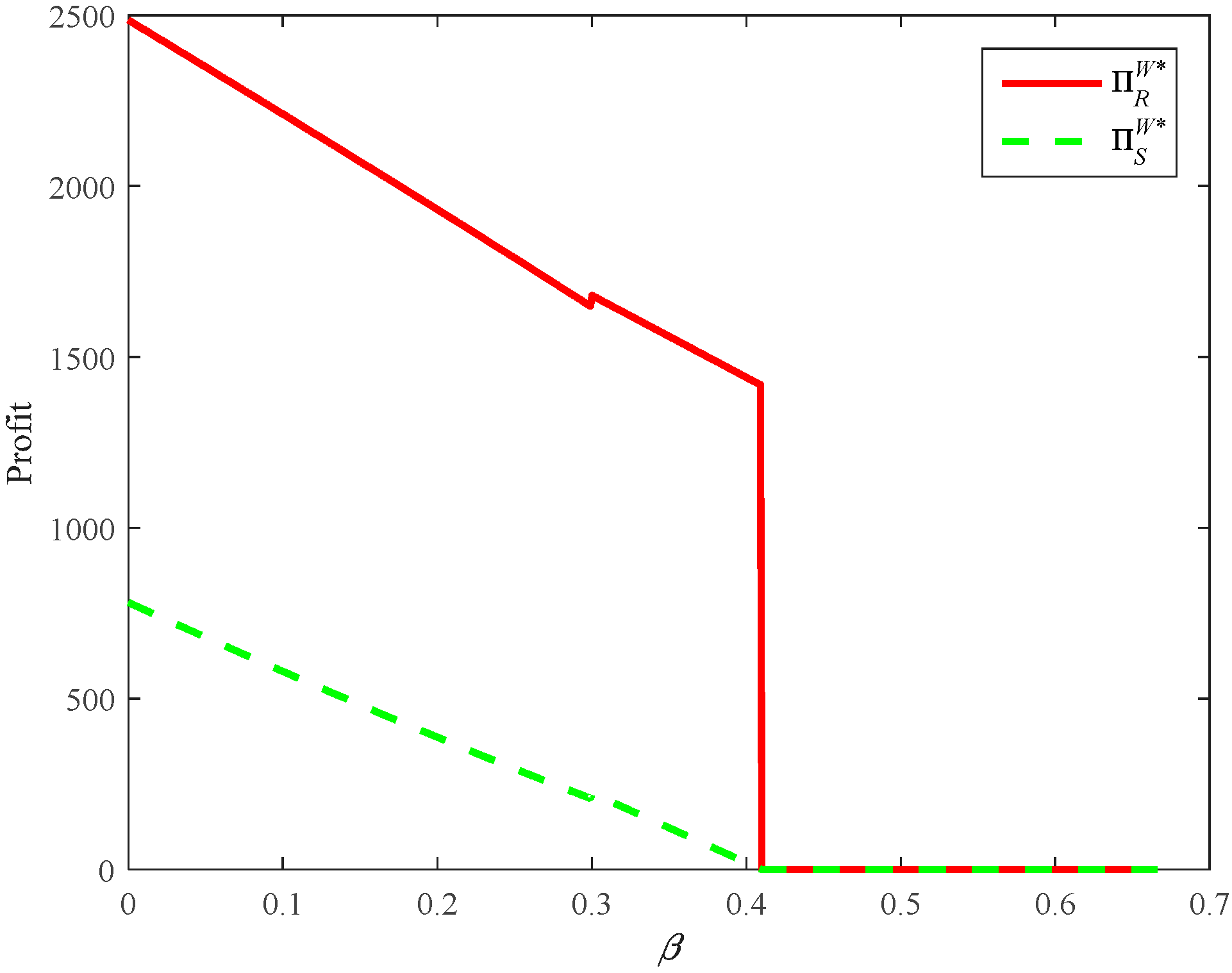

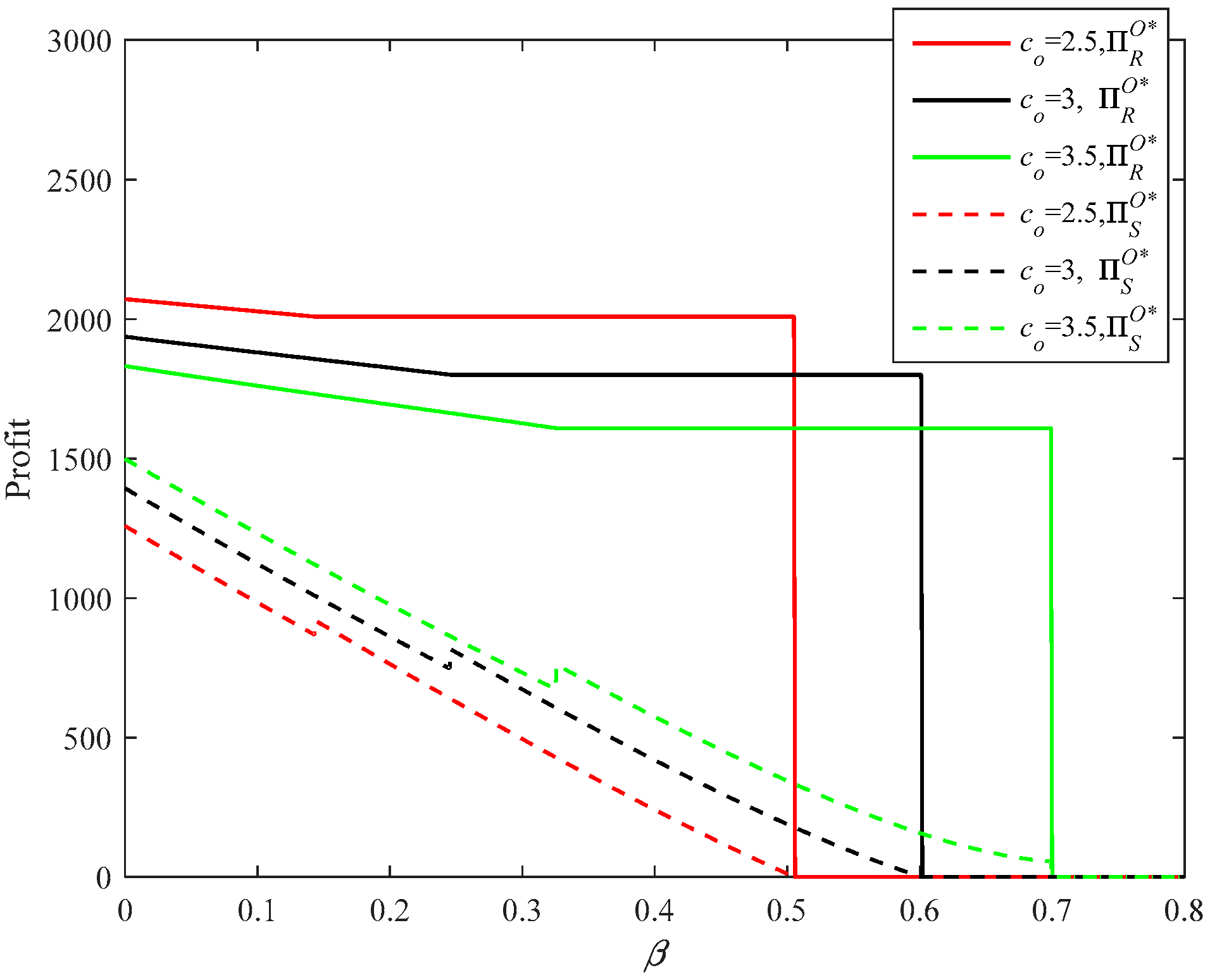

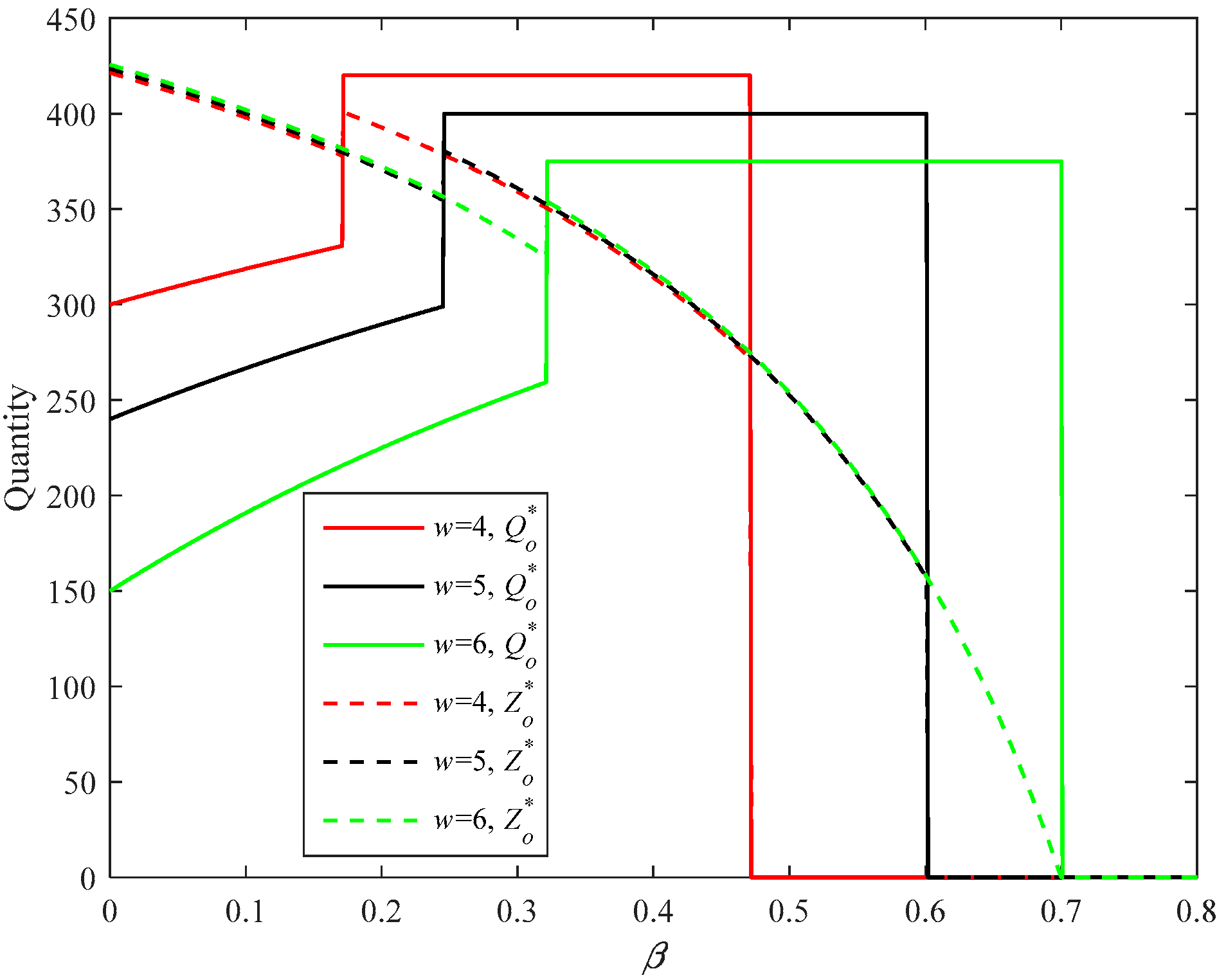

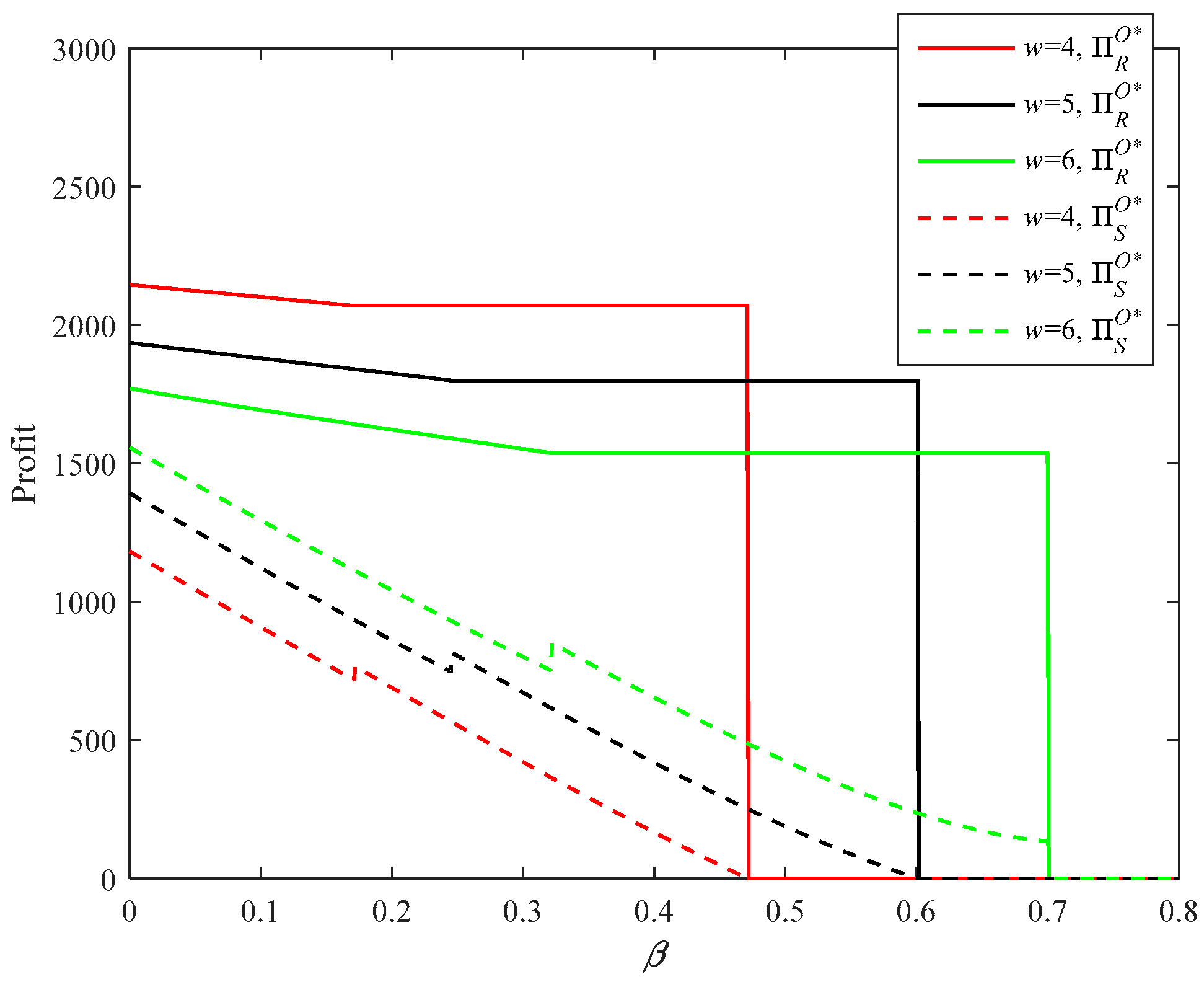

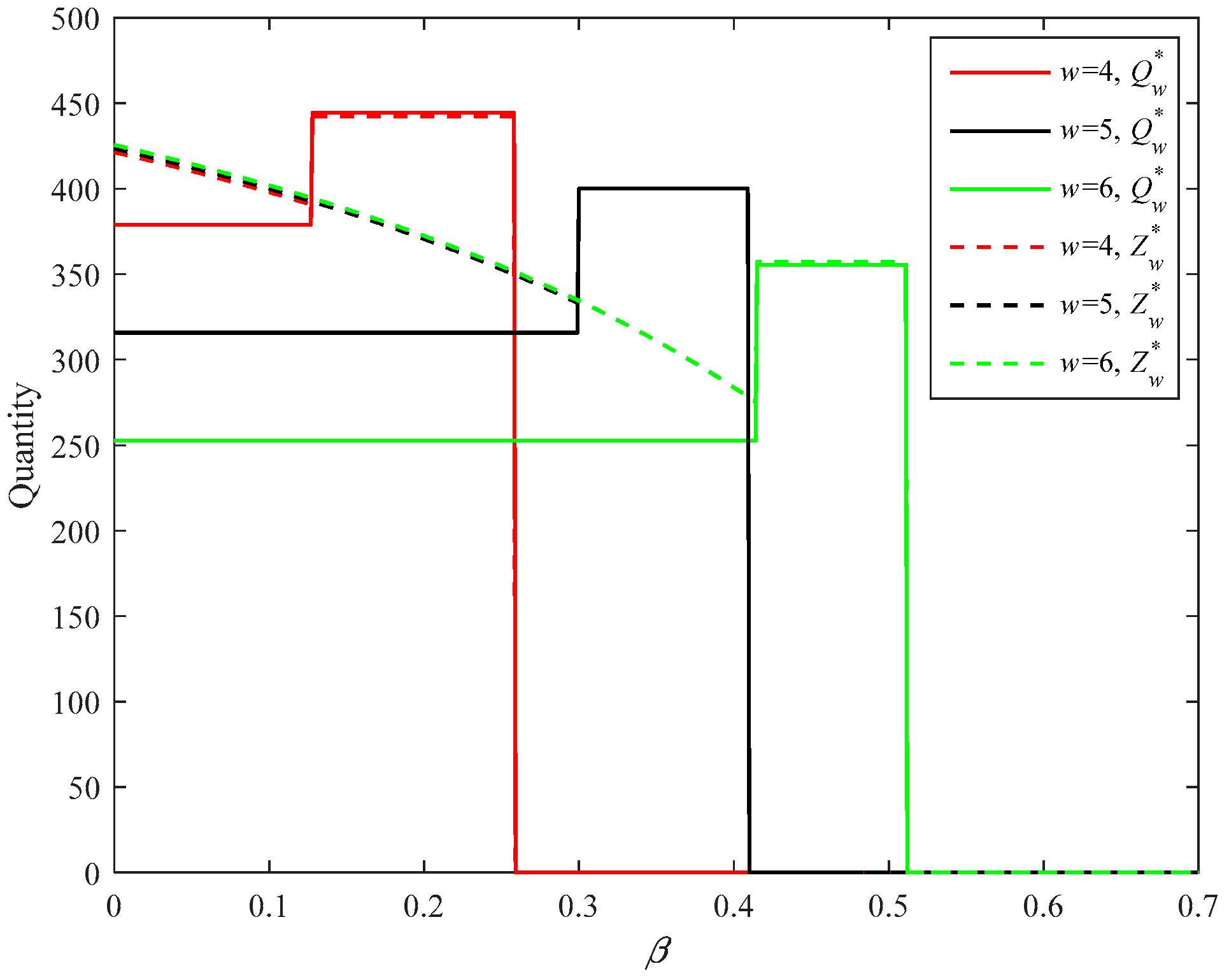

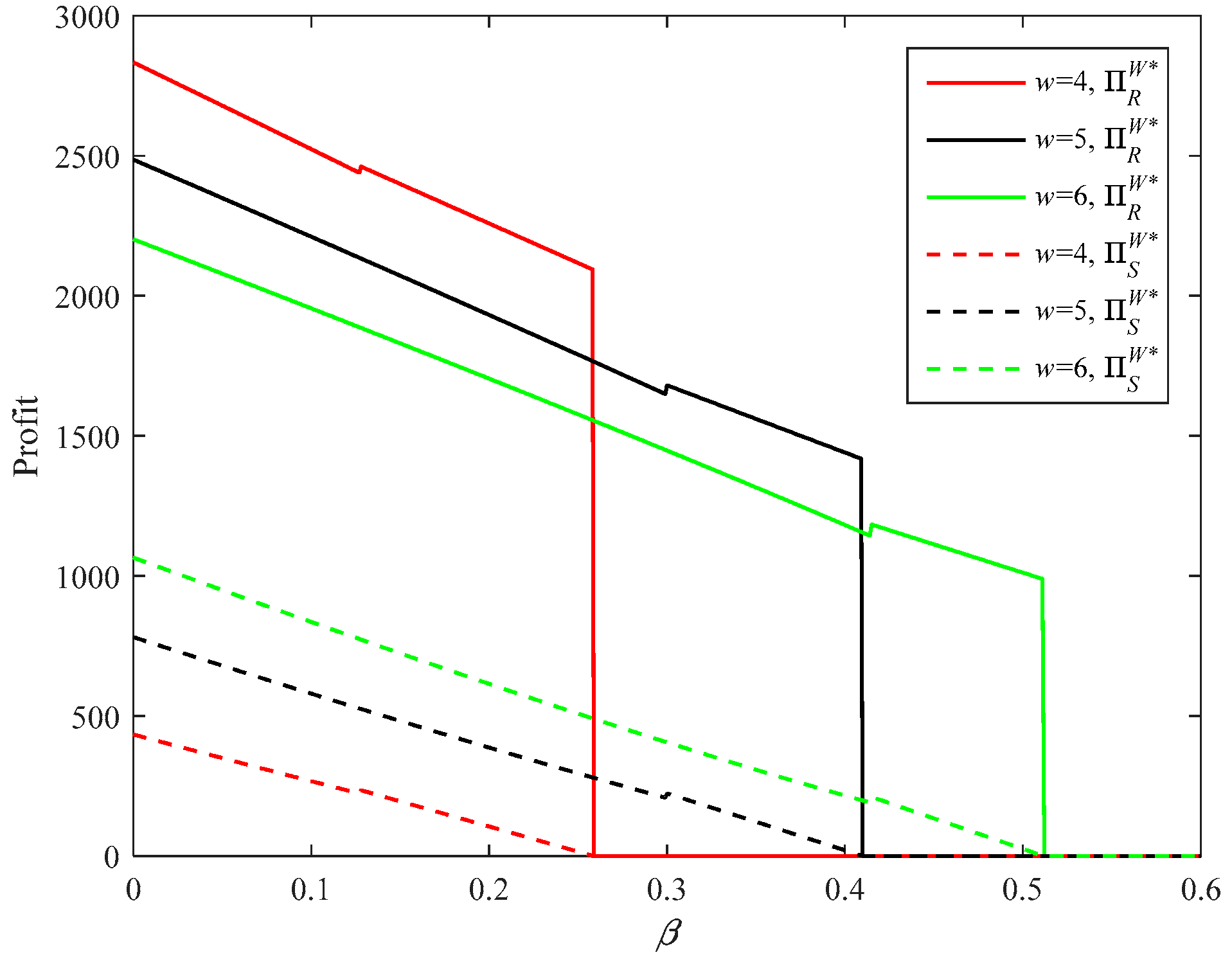

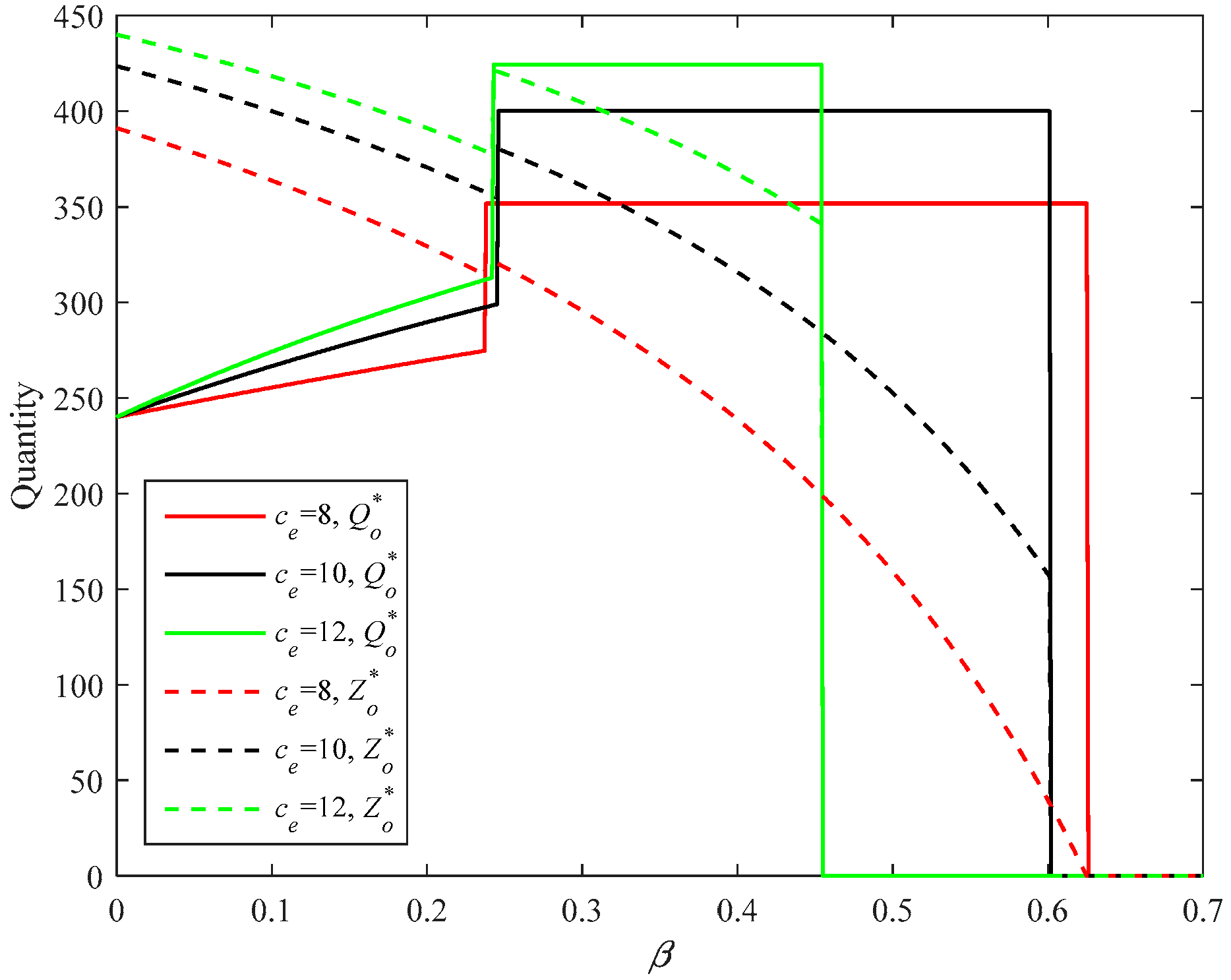

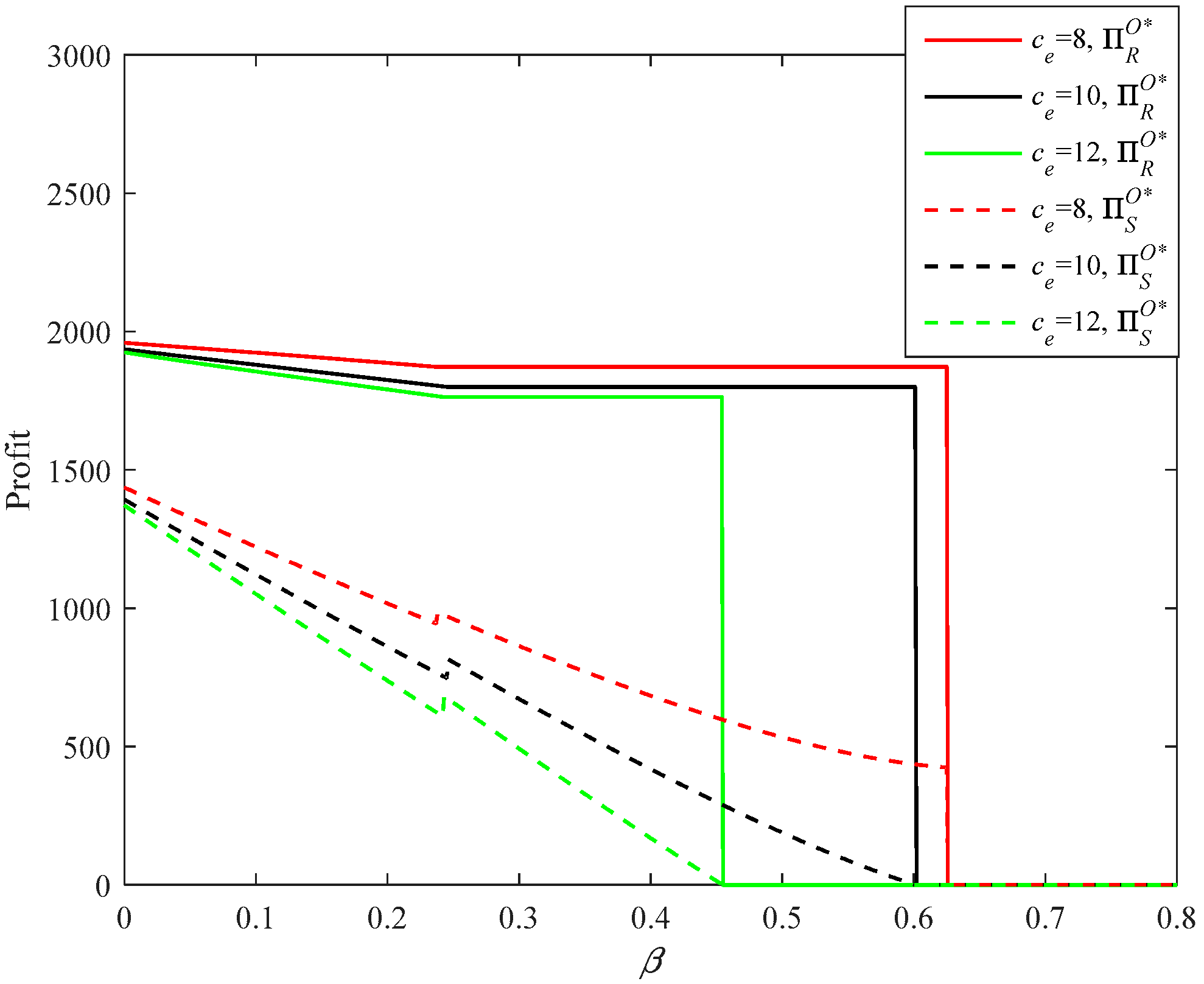

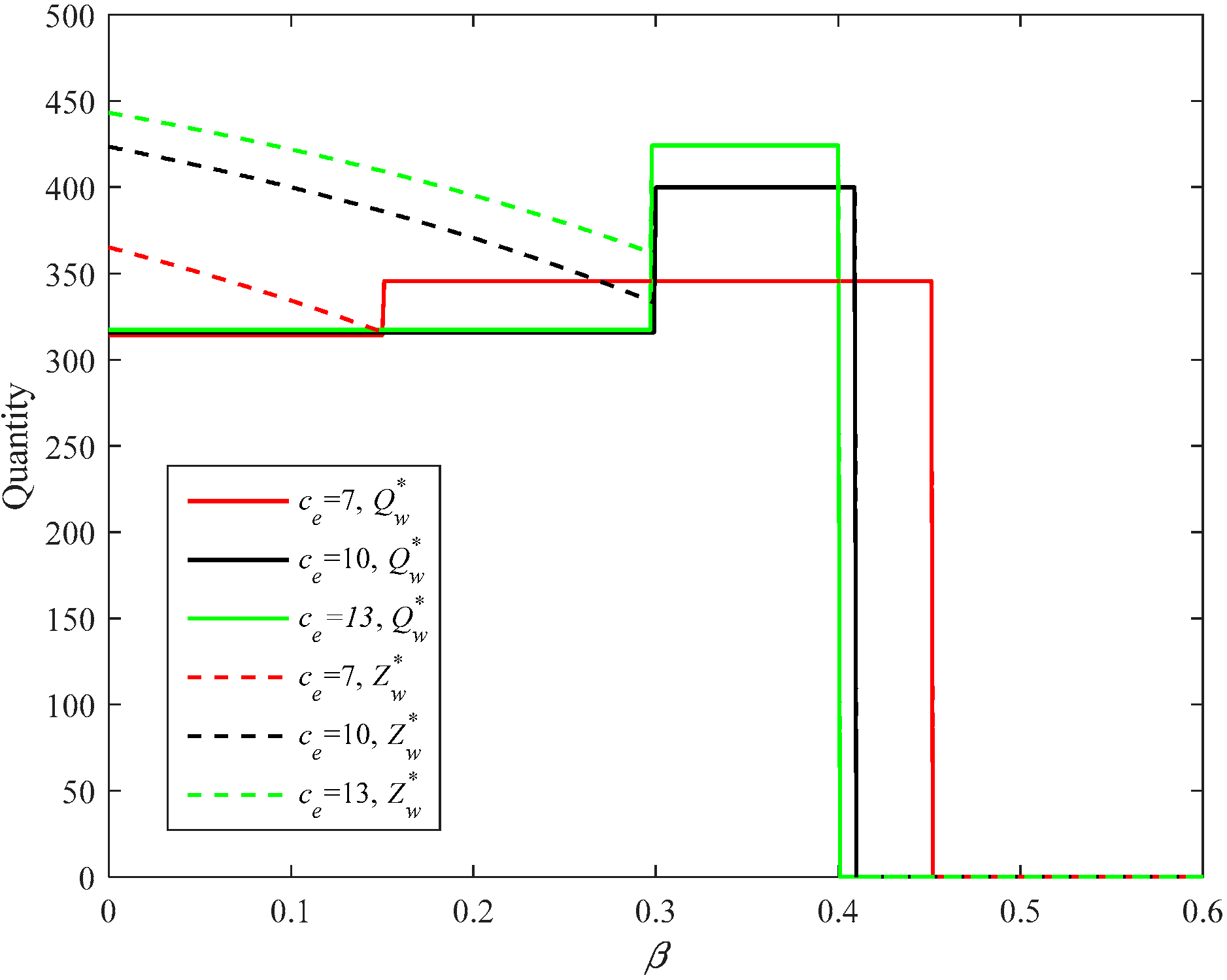

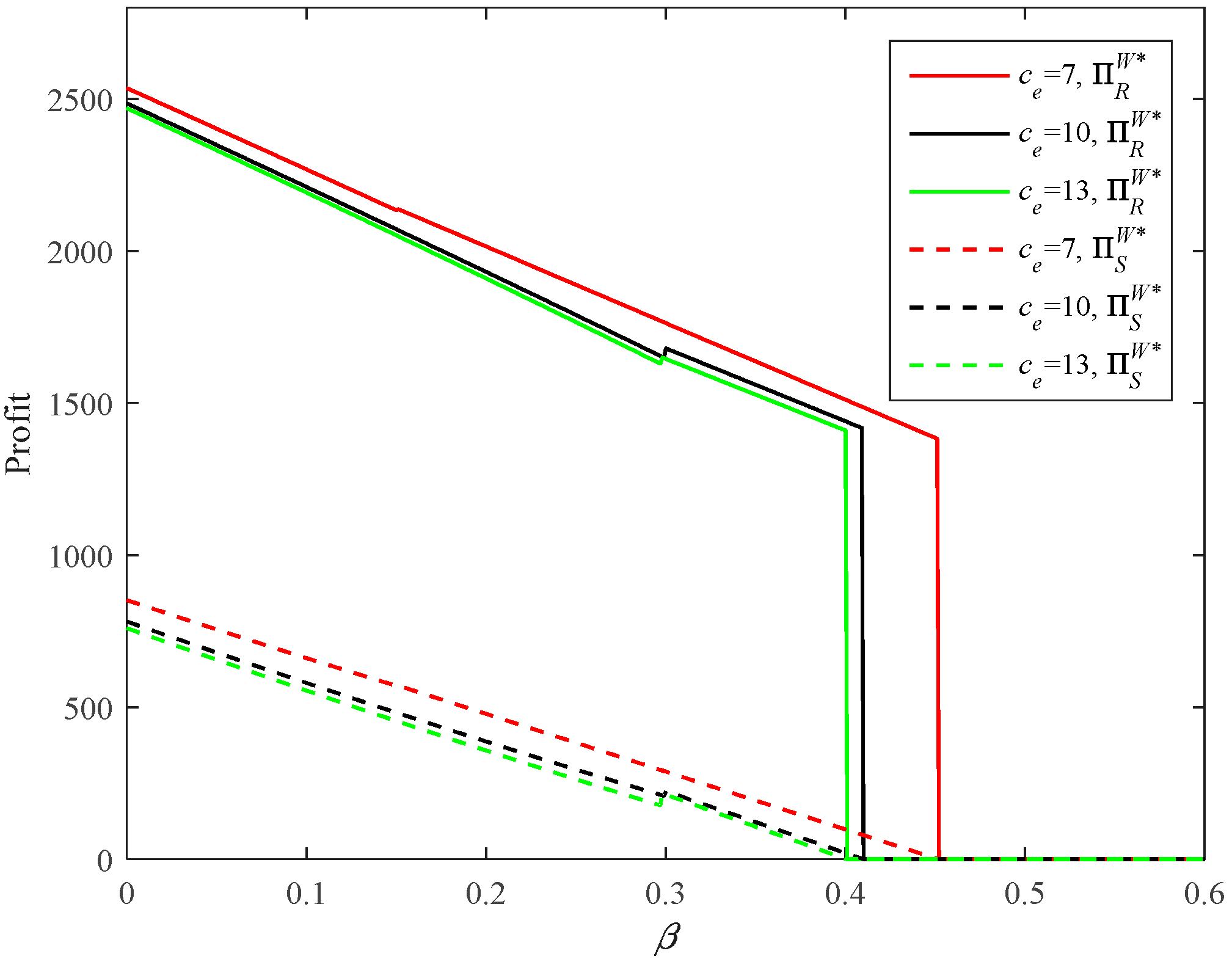

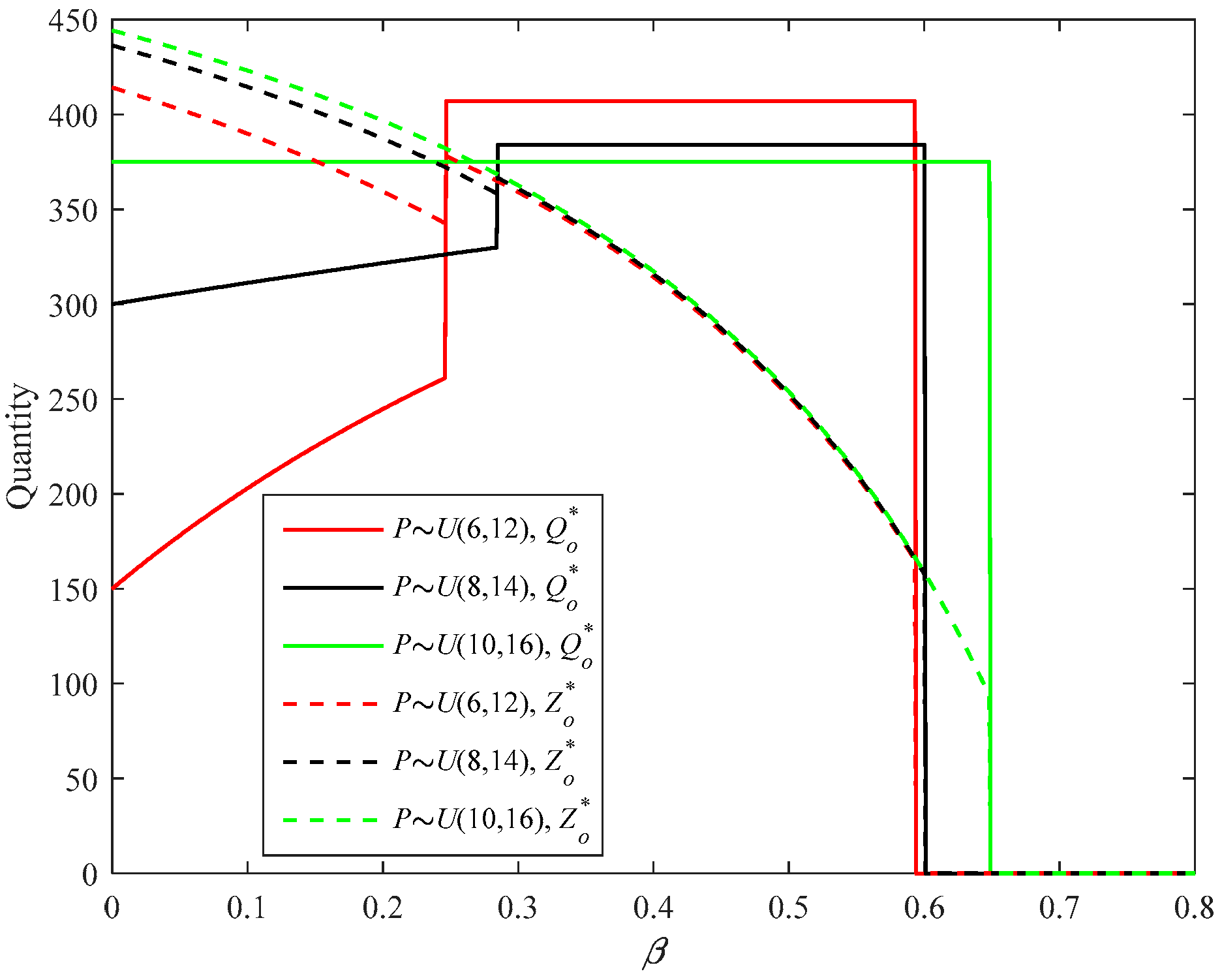

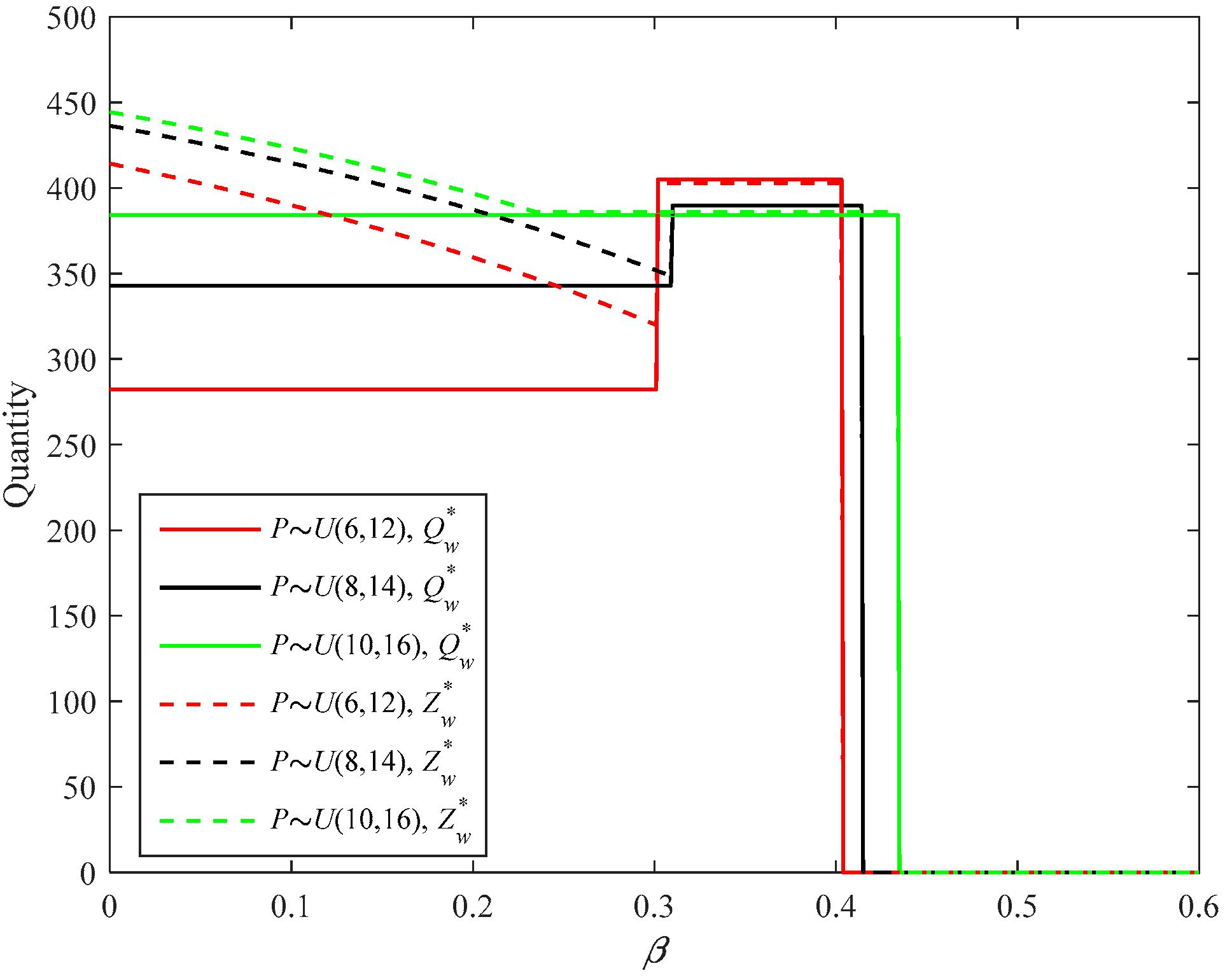

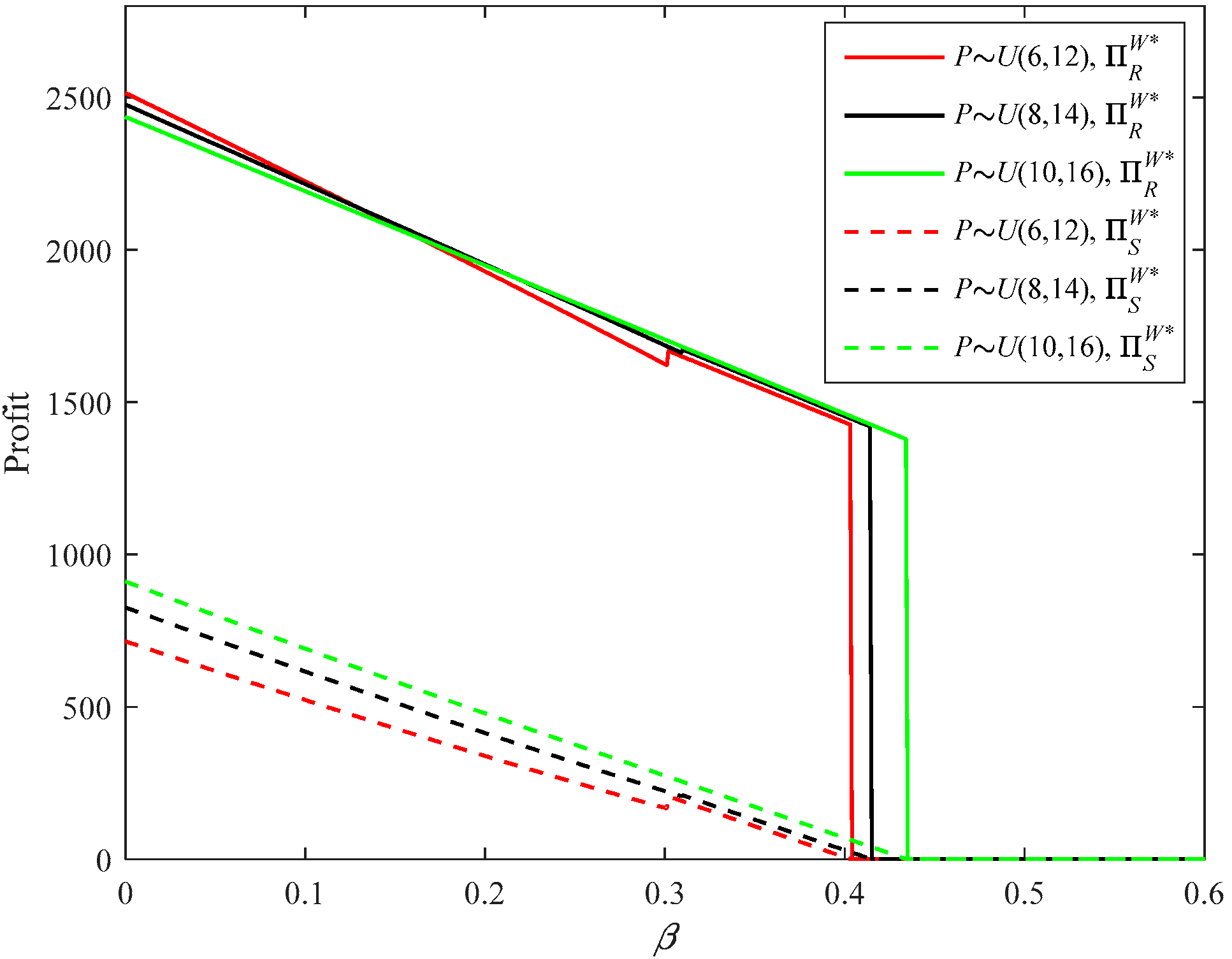

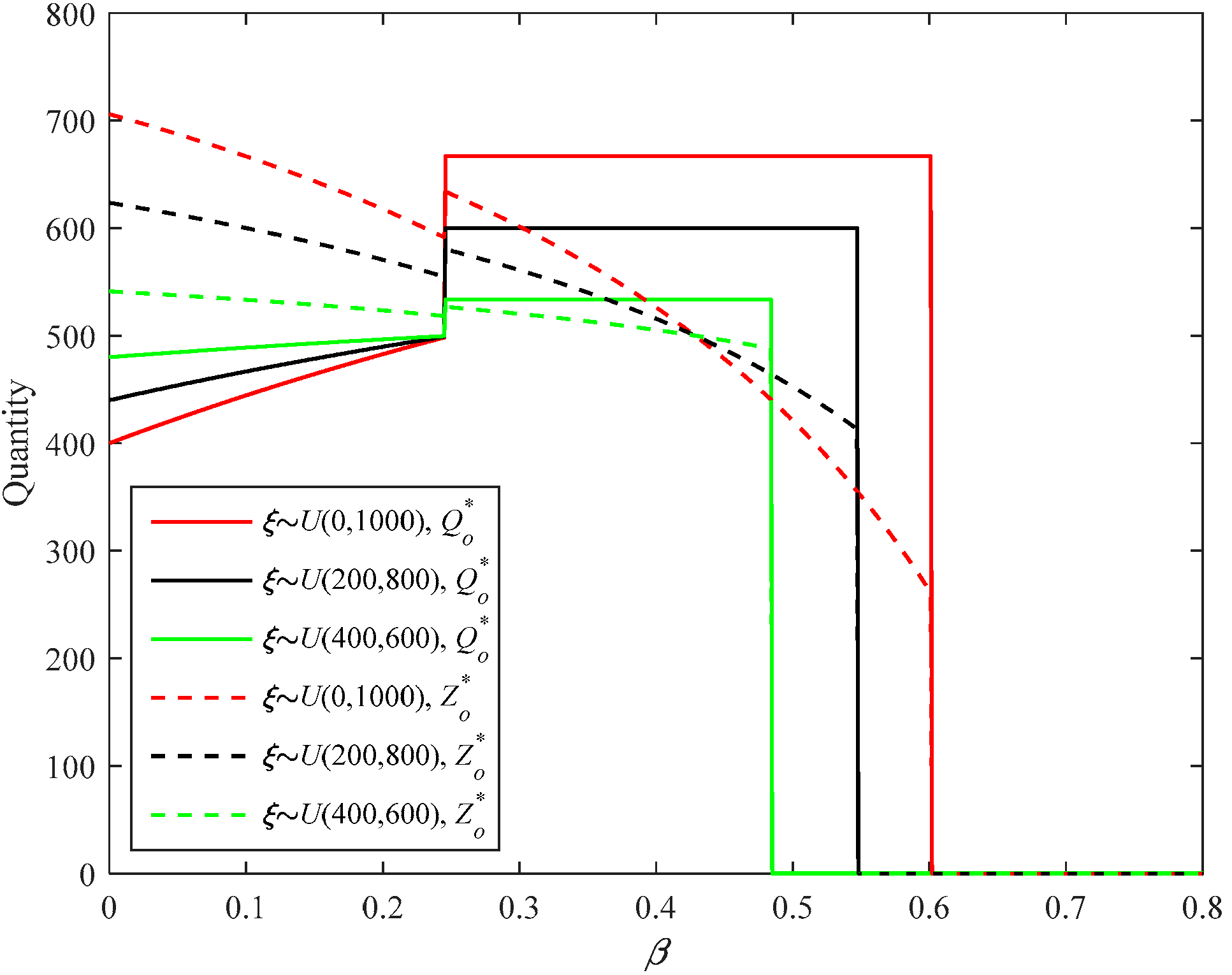

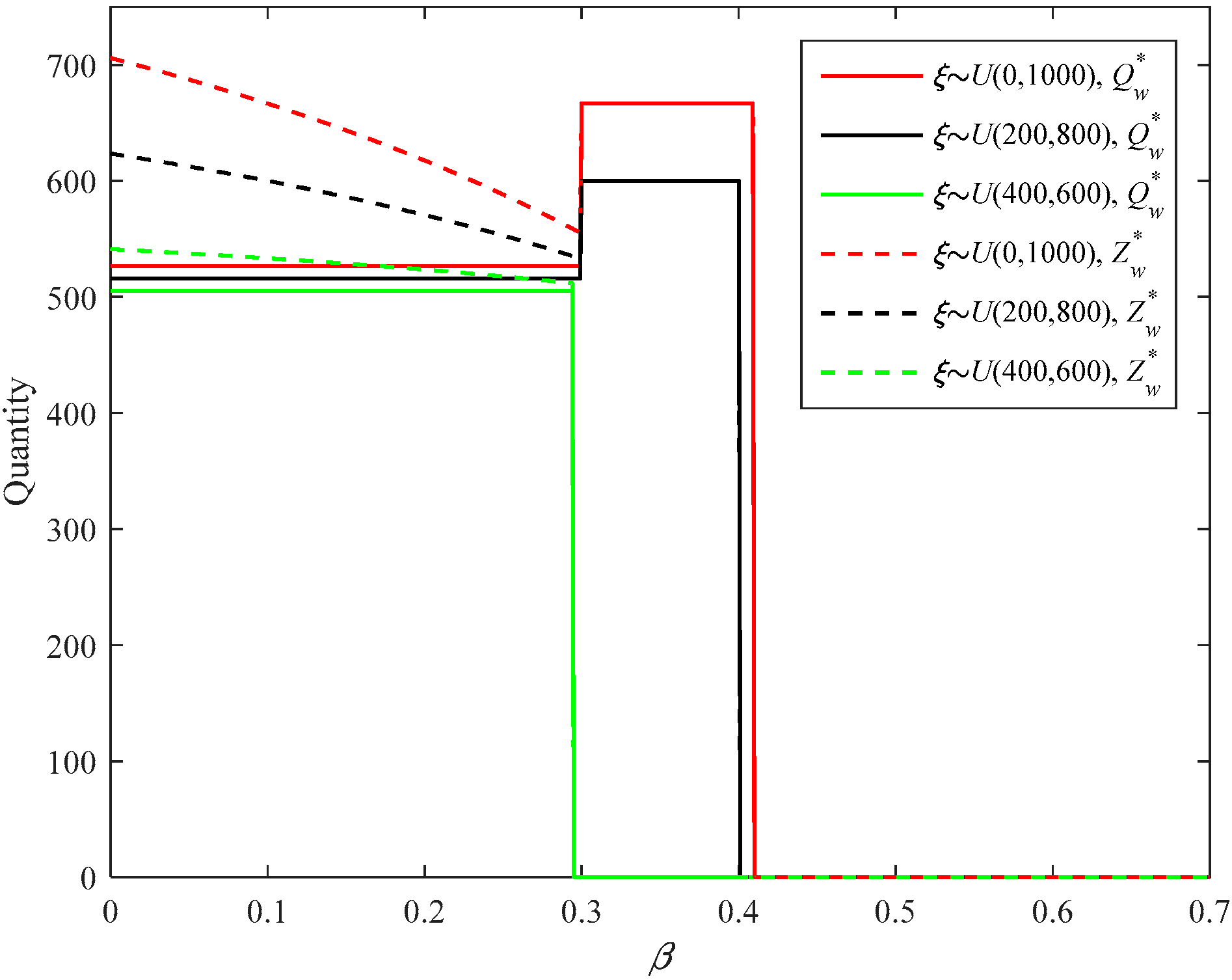

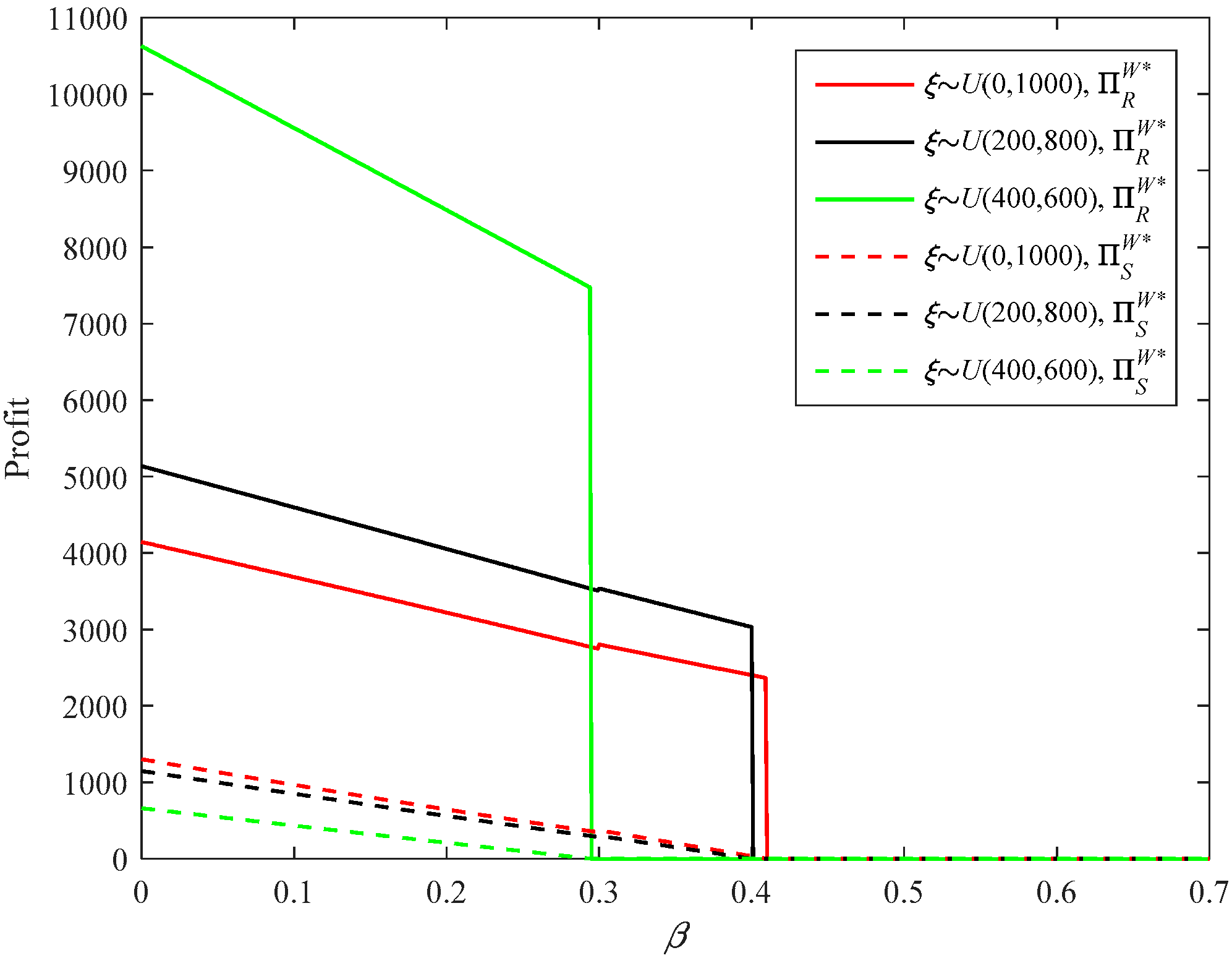

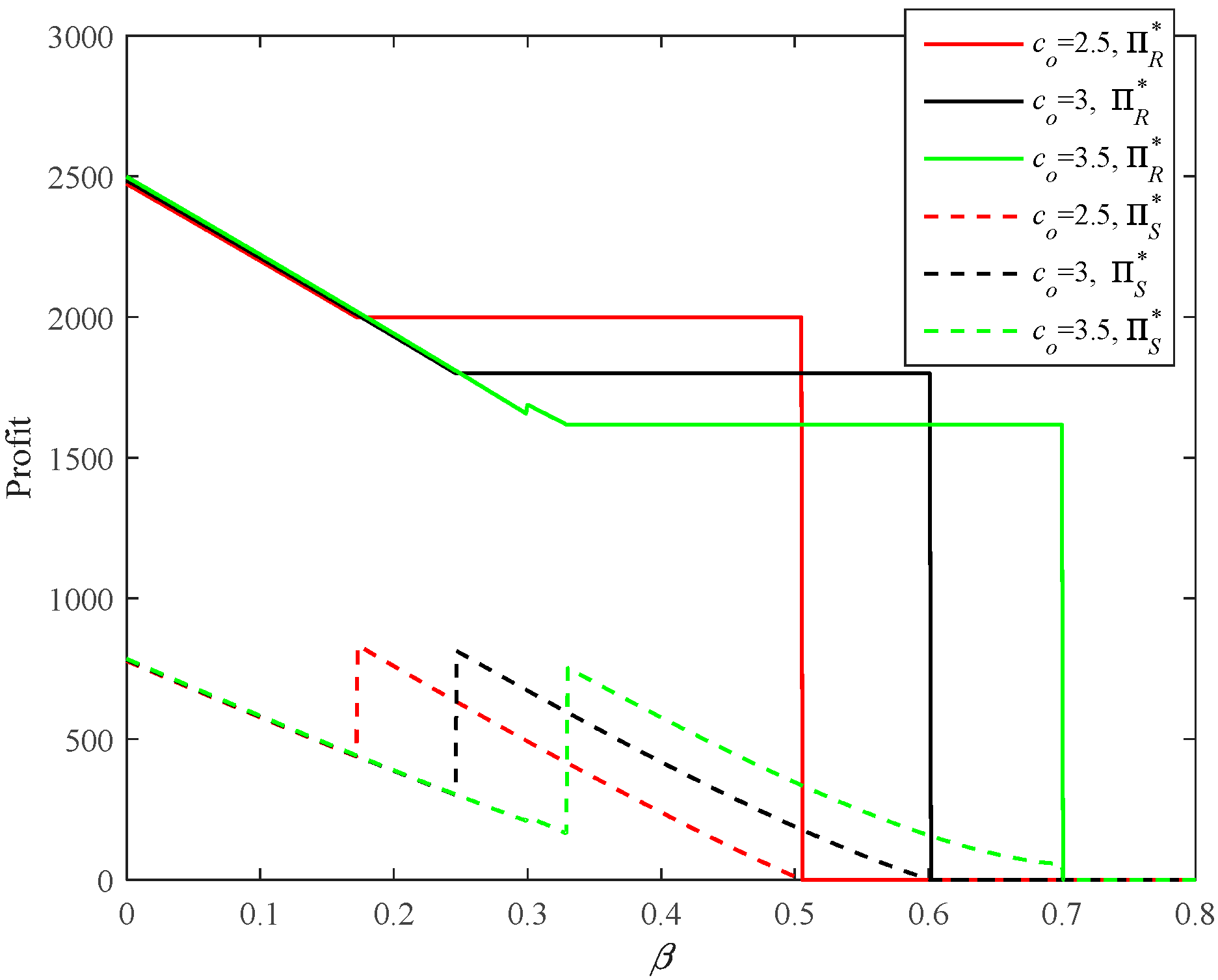

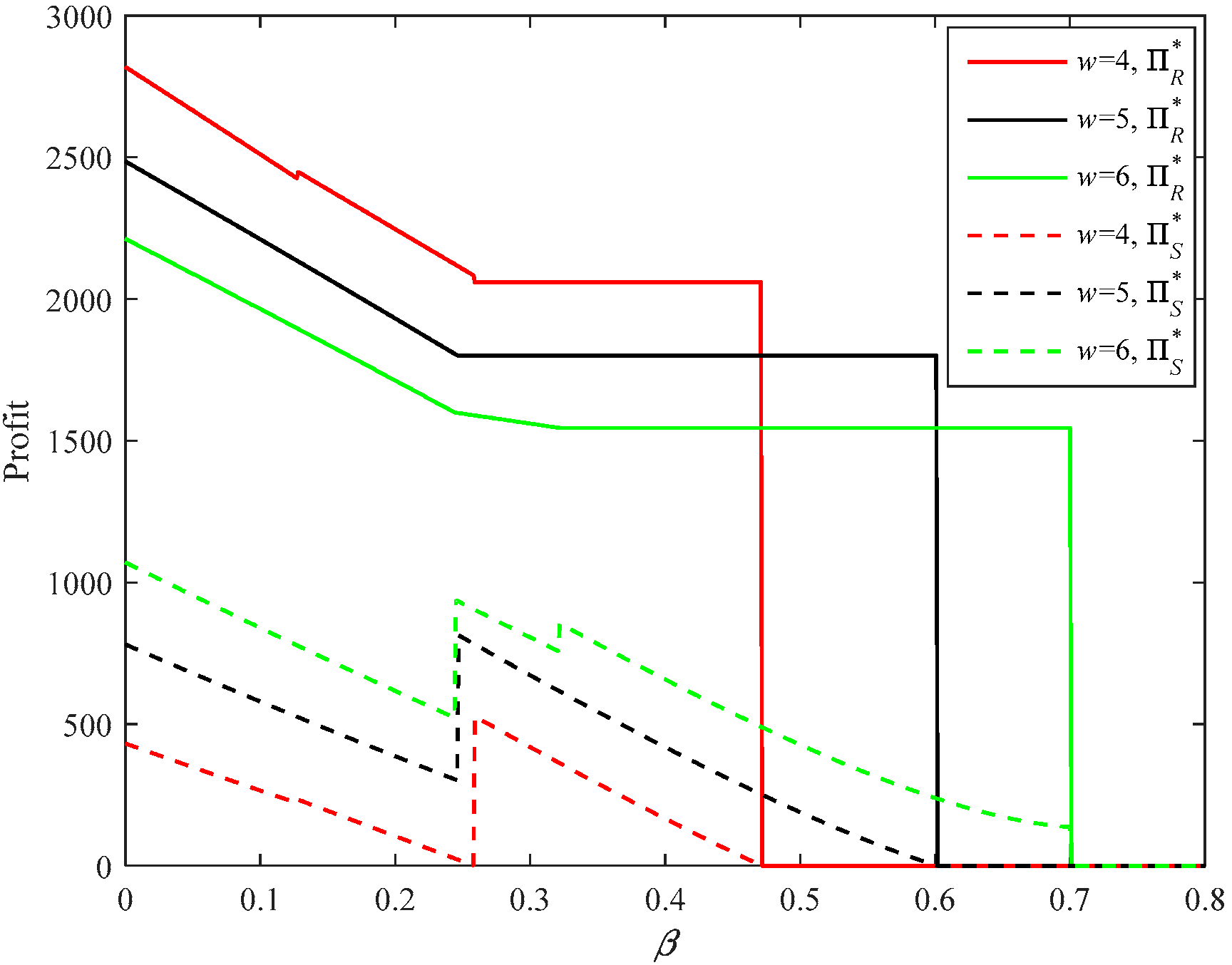

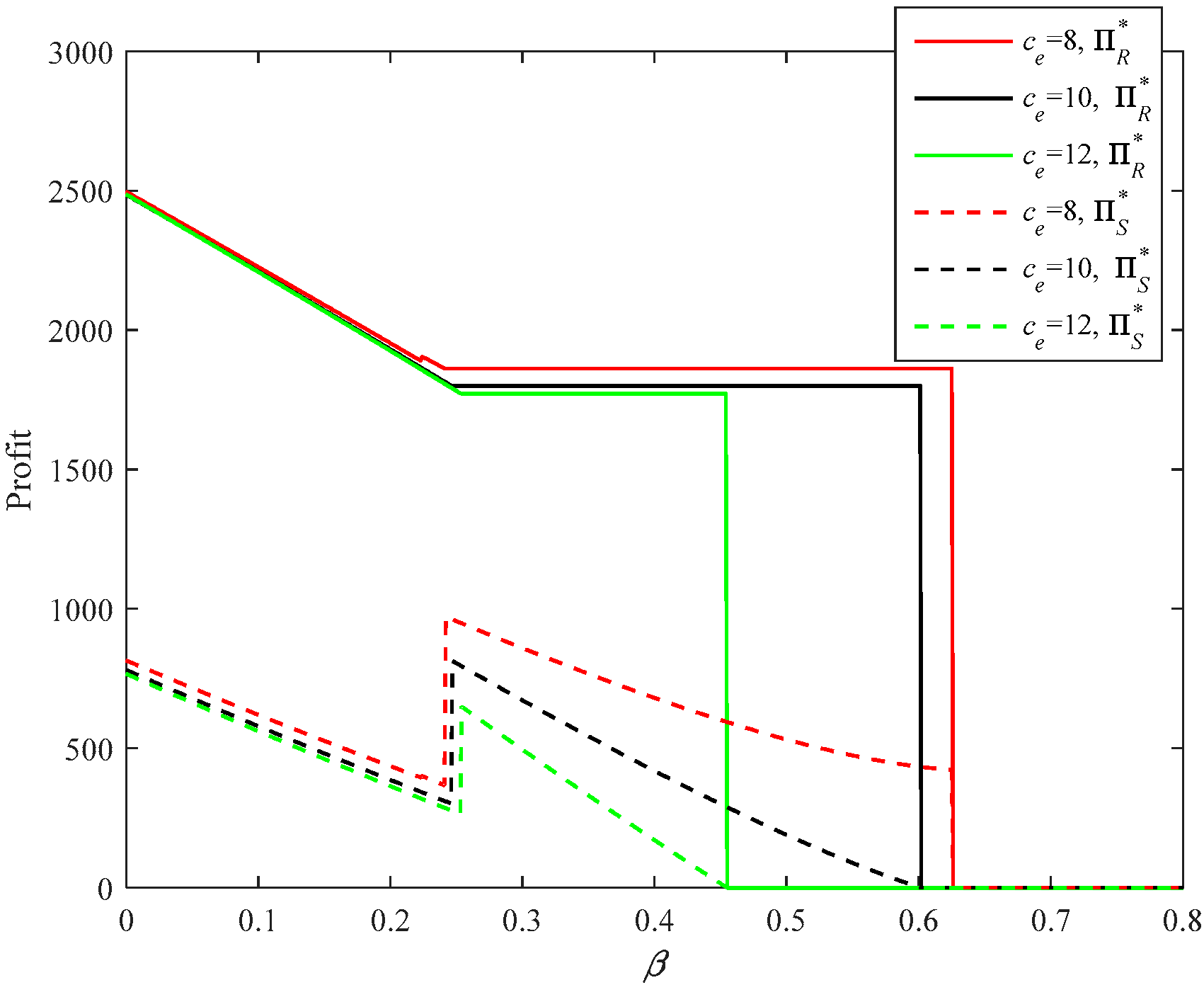

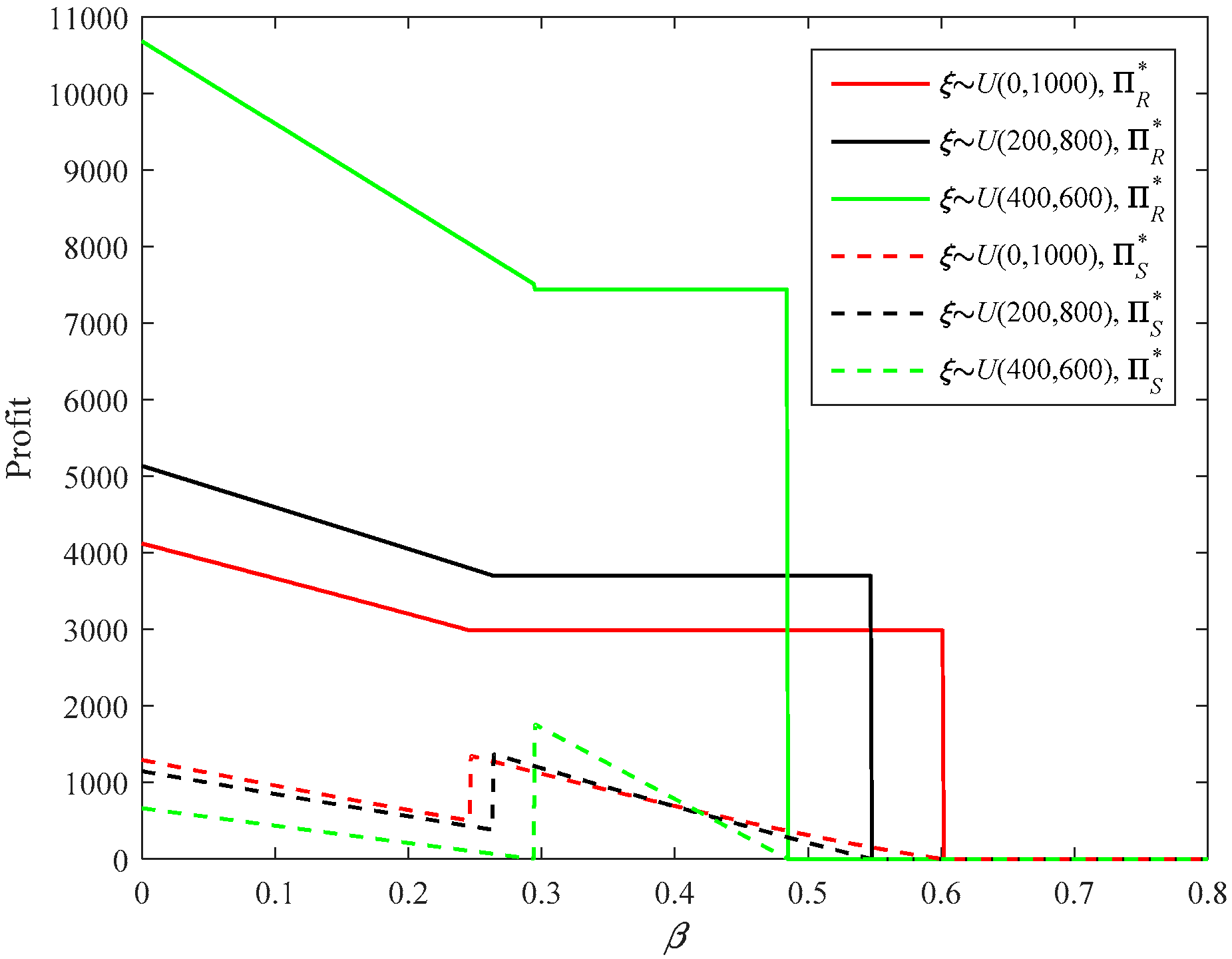

5.1.1. Impact of β

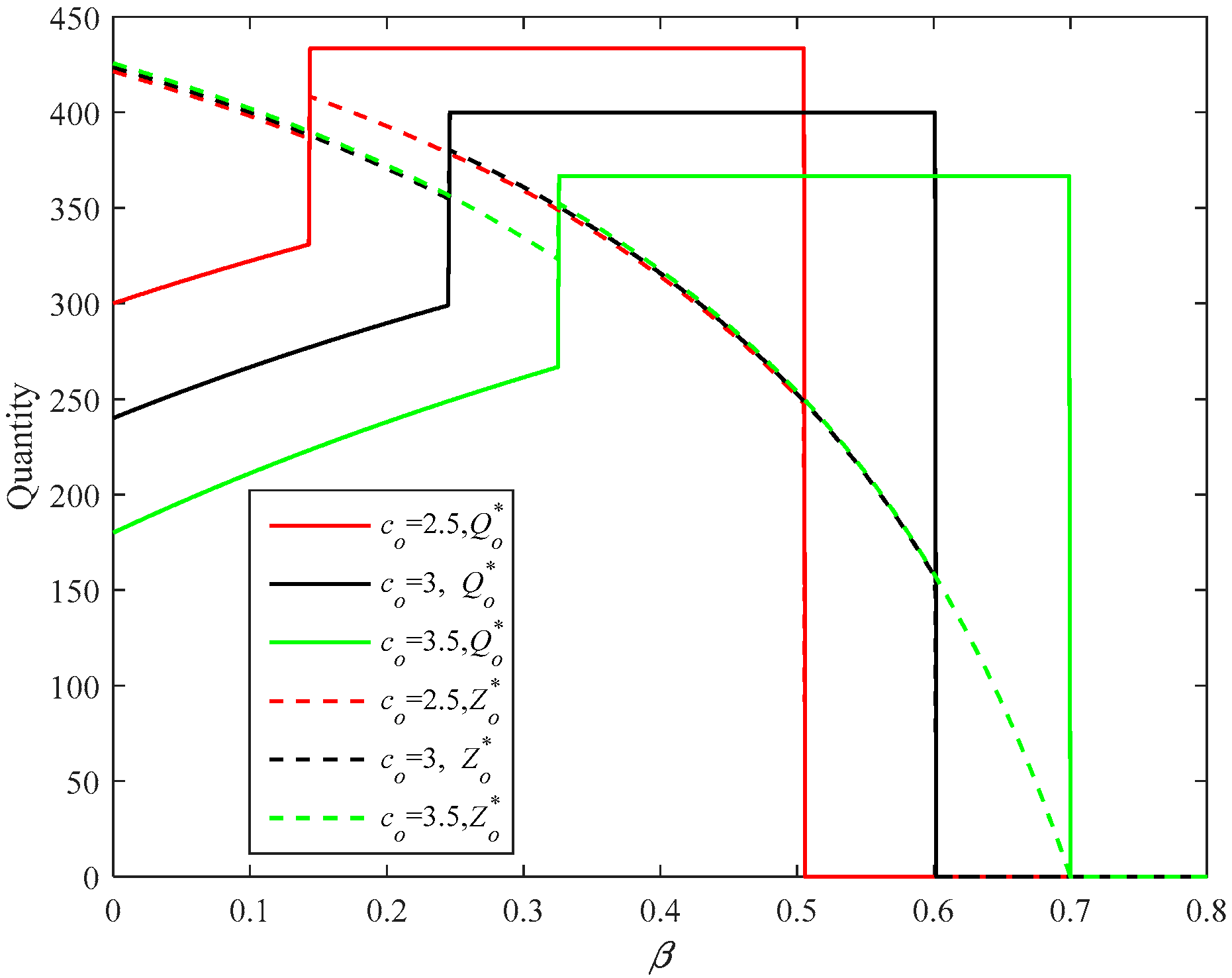

5.1.2. Impacts of co, w, and ce

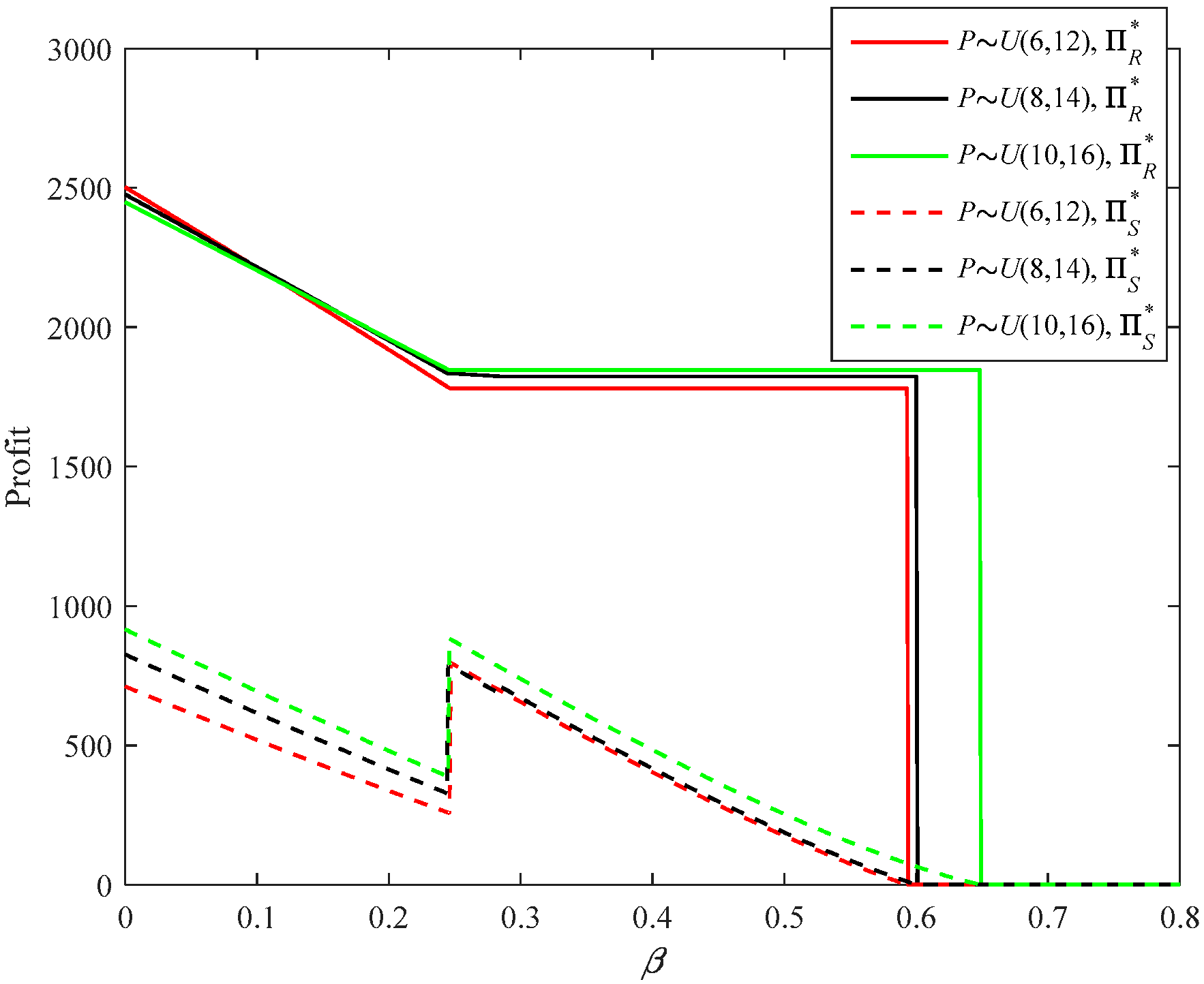

5.1.3. Impacts of P and ζ

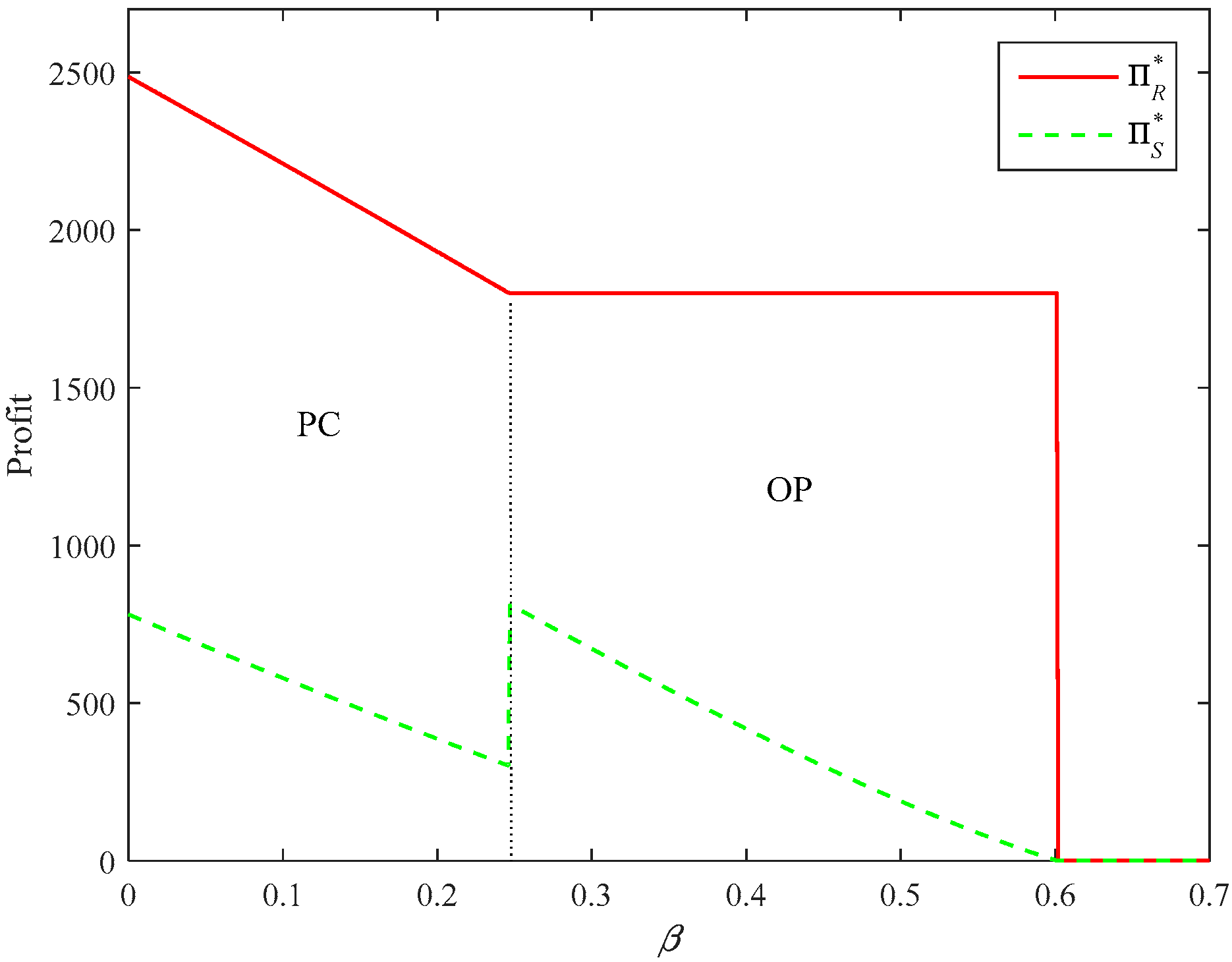

5.2. Firm’s Strategy Selection Decision

6. Conclusions

- (1)

- Under both types of strategies, the firm’s procurement quantity can be represented by two newsvendor solutions and her procurement strategy follows a “threshold” principle. That is to say, when the disruption risk is less than the threshold, the firm’s optimal procurement quantity takes the lower newsvendor solution, otherwise, it takes the higher newsvendor solution. Moreover, when the disruption risk is relatively low, the supplier tends to produce more products than the ordered or option reserved. Using the OP strategy, the firm tends to reserve more options to deal with the increasing supply risk. Generally speaking, the disruption risk has a negative impact on the supplier’s and firm’s profits.

- (2)

- A lower option price or option exercise price benefits the firm, while it damages the supplier. The increase of the emergency production cost will damage both the supplier’s and the firm’s profits under both strategies. When the option price or the option exercise price is relatively high, the supplier has an incentive to cooperate with the firm in a risky operational environment under both types of strategies.

- (3)

- Under two types of strategies, a higher mean value (MV) of emergency procurement price is beneficial to the supplier. However, it is counterintuitive that a lower MV of emergency procurement price is not always beneficial to the firm. Concerning the uncertainty of demand, a higher market demand variability is harmful to the firm and supplier, while it could be beneficial to the supplier under the PC strategy.

- (4)

- Accompanying the increase in the disruption risk, the firm first chooses the PC strategy and then changes to the OP strategy. When the option price and market demand variability increases, the firm is more likely to choose the OP strategy with the increase of the disruption risk. A higher option price and market demand variability can impel the supplier to cooperate with the firm even in a risky operational environment.

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

- (1)

- If , the optimal solution must be obtained when . Then, can be derived.

- (2)

- If , the optimal solution must be obtained when . Then, can be derived.

- (3)

- If , the optimal solution must be obtained when . Then, can be derived.

References

- Hu, X.; Gurnani, H.; Wang, L. Managing risk of supply disruptions: Incentives for capacity restoration. Prod. Oper. Manag. 2013, 22, 137–150. [Google Scholar] [CrossRef]

- Hu, B.; Kostamis, D. Managing supply disruptions when sourcing from reliable and unreliable suppliers. Prod. Oper. Manag. 2015, 24, 808–820. [Google Scholar] [CrossRef]

- Hendricks, K.B.; Singhal, V.R. Association between supply chain glitches and operating performance. Manag. Sci. 2005, 51, 695–711. [Google Scholar] [CrossRef]

- Barbosa-Póvoa, A.P.; da Silva, C.; Carvalho, A. Opportunities and challenges in sustainable supply chain: An operations research perspective. Eur. J. Oper. Res. 2018, 268, 399–431. [Google Scholar] [CrossRef]

- Tokui, J.; Kawasaki, K.; Miyagawa, T. The economic impact of supply chain disruptions from the Great East-Japan earthquake. Jpn. World Econ. 2017, 41, 59–70. [Google Scholar] [CrossRef] [Green Version]

- Tomlin, B. On the value of mitigation and contingency strategies for managing supply chain disruption risks. Manag. Sci. 2006, 52, 639–657. [Google Scholar] [CrossRef]

- Wang, Y.; Gilland, W.; Tomlin, B. Mitigating supply risk: Dual sourcing or process improvement? Manuf. Serv. Oper. Manag. 2010, 12, 489–510. [Google Scholar] [CrossRef]

- Dong, L.; Tomlin, B. Managing disruption risk: The interplay between operations and insurance. Manag. Sci. 2012, 58, 1898–1915. [Google Scholar] [CrossRef]

- Li, Y.; Zhen, X.; Qi, X.; Cai, G. Penalty and financial assistance in a supply chain with supply disruption. Omega 2016, 61, 167–181. [Google Scholar] [CrossRef] [Green Version]

- Zhen, X.; Li, Y.; Cai, G.G.; Shi, D. Transportation disruption risk management: Business interruption insurance and backup transportation. Trans. Res. Part E 2016, 90, 51–68. [Google Scholar] [CrossRef]

- Feng, C.; Wang, Z.; Jiang, Z. Retailer’s procurement strategy under endogenous supply stability. Sustainability 2017, 9, 2261. [Google Scholar] [CrossRef]

- Kumar, M.; Basu, P.; Avittathur, B. Pricing and sourcing strategies for competing retailers in supply chains under disruption risk. Eur. J. Oper. Res. 2018, 265, 533–543. [Google Scholar] [CrossRef]

- Nagali, V.; Hwang, J.; Sanghera, D.; Gaskins, M.; Pridgen, M.; Thurston, T.; Shoemaker, G. Procurement risk management (PRM) at Hewlett-Packard company. Interfaces 2008, 38, 51–60. [Google Scholar] [CrossRef]

- Chen, J.Y.; Dada, M.; Hu, Q. Designing supply contracts: Buy-now, reserve, and wait-and-see. IIE Trans. 2016, 48, 881–900. [Google Scholar] [CrossRef]

- Ma, L.; Zhao, Y.; Xue, W.; Cheng, T.C.E.; Yan, H. Loss-averse newsvendor model with two ordering opportunities and market information updating. Int. J. Prod. Econ. 2012, 140, 912–921. [Google Scholar] [CrossRef]

- Chen, X.; Shen, Z.J. An analysis of a supply chain with options contracts and service requirements. IIE Trans. 2012, 44, 805–819. [Google Scholar] [CrossRef]

- Yu, H.; Zeng, A.Z.; Zhao, L. Single or dual sourcing: Decision-making in the presence of supply chain disruption risks. Omega 2009, 37, 788–800. [Google Scholar] [CrossRef]

- Kim, M.; Jim, C. Global Supply Chain Rattled by Japan Quake, Tsunami. 2011. Available online: http://www.reuters.com/article/2011/03/14/japan-quake-supplychain-idUSL3E7EE05V20110314 (accessed on 20 June 2018).

- Fang, Y.; Shou, B. Managing supply uncertainty under supply chain Cournot competition. Eur. J. Oper. Res. 2015, 243, 156–176. [Google Scholar] [CrossRef]

- Tomlin, B. Disruption-management strategies for short life-cycle products. Nav. Logist. Res. 2009, 56, 318–347. [Google Scholar] [CrossRef]

- Tang, C.S. Perspectives in supply chain risk management. Int. J. Prod. Econ. 2006, 103, 451–488. [Google Scholar] [CrossRef]

- Snyder, L.V.; Atan, Z.; Peng, P.; Rong, Y.; Schmitt, A.J.; Sinsoysal, B. OR/MS models for supply chain disruptions: A review. IIE Trans. 2016, 48, 89–109. [Google Scholar] [CrossRef]

- Yan, R.; Lu, B.; Wu, J. Contract coordination strategy of supply chain with substitution under supply disruption and stochastic demand. Sustainability 2016, 8, 676. [Google Scholar] [CrossRef]

- Zhao, M.; Freeman, N.K. Robust sourcing from suppliers under ambiguously correlated major disruption risks. Prod. Oper. Manag. 2018. [Google Scholar] [CrossRef]

- Yin, Z.; Wang, C. Strategic cooperation with a backup supplier for the mitigation of supply disruptions. Int. J. Prod. Res. 2017. [Google Scholar] [CrossRef]

- Wang, C.; Yin, Z. Using backup supply with responsive pricing to mitigate disruption risk for a risk-averse firm. Int. J. Prod. Res. 2018. [Google Scholar] [CrossRef]

- He, B.; Huang, H.; Yuan, K. The comparison of two procurement strategies in the presence of supply disruption. Comput. Ind. Eng. 2015, 85, 296–305. [Google Scholar] [CrossRef]

- Bolandifar, E.; Feng, T.; Zhang, F. Simple contracts to assure supply under noncontractible capacity and asymmetric cost information. Manuf. Serv. Oper. Manag. 2018, 20, 217–231. [Google Scholar] [CrossRef]

- Hwang, W.; Bakshi, N.; DeMiguel, V. Wholesale price contracts for reliable supply. Prod. Oper. Manag. 2018. [Google Scholar] [CrossRef]

- Xu, H. Managing production and procurement through option contracts in supply chains with random yield. Int. J. Prod. Econ. 2010, 126, 306–313. [Google Scholar] [CrossRef]

- Li, J.C.; Zhou, Y.W.; Huang, W. Production and procurement strategies for seasonal product supply chain under yield uncertainty with commitment-option contracts. Int. J. Prod. Econ. 2017, 183, 208–222. [Google Scholar] [CrossRef]

- Köle, H.; Bakal, I.S. Value of information through options contract under disruption risk. Comput. Ind. Eng. 2017, 103, 85–97. [Google Scholar] [CrossRef]

- Xia, Y.; Ramachandran, K.; Gurnani, H. Sharing demand and supply risk in a supply chain. IIE Trans. 2011, 43, 451–469. [Google Scholar] [CrossRef]

- Xue, K.; Li, Y.; Zhen, X.; Wang, W. Managing the disruption risk: Option contract or order commitment contract? Ann. Oper. Res. 2018. [Google Scholar] [CrossRef]

- Li, X.; Li, Y. On the loss-averse dual-sourcing problem under supply disruption. Comput. Oper. Res. 2016. [Google Scholar] [CrossRef]

- Mizgier, K.J.; Wagner, S.M.; Holyst, J.A. Modeling defaults of companies in multi-stage supply chain networks. Int. J. Prod. Econ. 2012, 135, 14–23. [Google Scholar] [CrossRef]

- Mizgier, K.J.; Wagner, S.M.; Jüttner, M.P. Disentangling diversification in supply chain networks. Int. J. Prod. Econ. 2015, 162, 115–124. [Google Scholar] [CrossRef]

- Wagner, S.M.; Mizgier, K.J.; Papageorgiou, S. Operational disruptions and business cycles. Int. J. Prod. Econ. 2017, 183, 66–78. [Google Scholar] [CrossRef]

- Tang, S.Y.; Gurnani, H.; Gupta, D. Managing disruptions in decentralized supply chains with endogenous supply process reliability. Prod. Oper. Manag. 2014, 23, 1198–1211. [Google Scholar] [CrossRef]

- Latour, A. Trial by Fire: A Blaze in Albuquerque Sets Off Major Crisis for Cell-Phone Giants. 2001. Available online: https://www.wsj.com/articles/SB980720939804883010 (accessed on 20 June 2018).

- He, Y. Supply risk sharing in a closed-loop supply chain. Int. J. Prod. Econ. 2017, 183, 39–52. [Google Scholar] [CrossRef]

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Xue, K.; Xu, Y.; Feng, L. Managing Procurement for a Firm with Two Ordering Opportunities under Supply Disruption Risk. Sustainability 2018, 10, 3293. https://doi.org/10.3390/su10093293

Xue K, Xu Y, Feng L. Managing Procurement for a Firm with Two Ordering Opportunities under Supply Disruption Risk. Sustainability. 2018; 10(9):3293. https://doi.org/10.3390/su10093293

Chicago/Turabian StyleXue, Kelei, Ya Xu, and Lipan Feng. 2018. "Managing Procurement for a Firm with Two Ordering Opportunities under Supply Disruption Risk" Sustainability 10, no. 9: 3293. https://doi.org/10.3390/su10093293

APA StyleXue, K., Xu, Y., & Feng, L. (2018). Managing Procurement for a Firm with Two Ordering Opportunities under Supply Disruption Risk. Sustainability, 10(9), 3293. https://doi.org/10.3390/su10093293