Performance Measurement for Sustainability: Does Firm Ownership Matter

Abstract

:1. Introduction

2. Literature Review

2.1. The Role of Performance Measurement Systems in Organizations

2.2. The Role of Outcome-Based Compensation Systems in Organizations

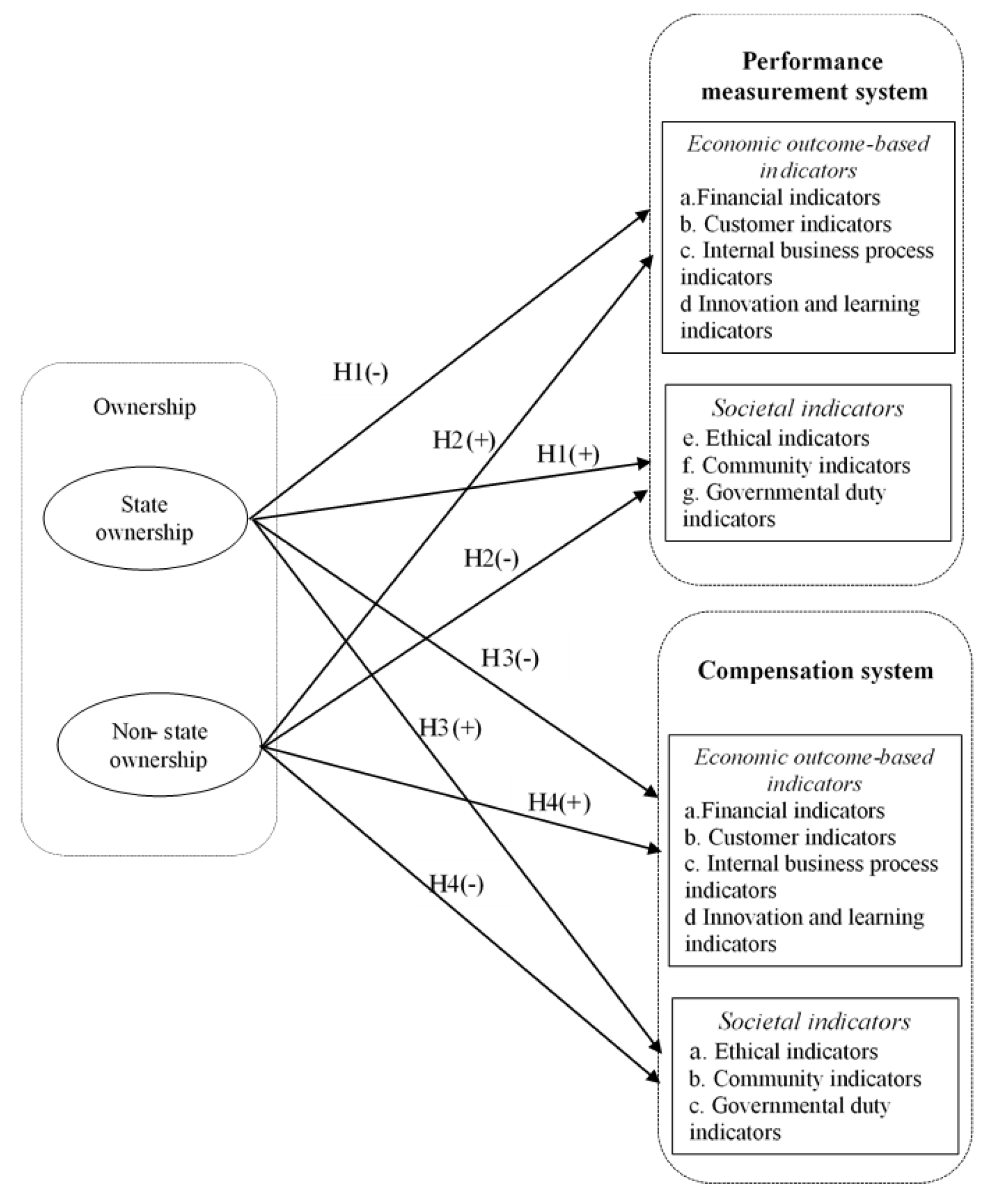

3. Hypothesis Development

3.1. Ownership Differences and the Impact on the Design of Performance Measurement Systems

3.2. Ownership Differences and the Relationship with the Presence of Outcome-Based Compensation Systems

4. Research Methodology

4.1. Data Collection

4.2. Measurement of Variables

- (i)

- State-owned enterprises include the following types: (1) enterprises with 100% of state capital operating under the control of the central or local governmental agencies; (2) limited companies under the management of the central or local government; (3) joint stock companies with domestic capital, of which the government shares more than 50% charter capital.

- (ii)

- Non-state-owned enterprises are enterprises set up by domestic capital. The capital may be owned by private shareholders, being one individual or a group of individuals (like a family) or the government when the capital of the government is equal to or less than 50% of the registered capital. There are the following types of non-state enterprises: (1) private enterprises; (2) cooperative name companies; (3) private limited companies; (4) joint stock companies without capital of state; (5) joint stock companies with 50% and less than 50% of charter capital shared by the government.

4.3. Method of Analysis

5. Results

5.1. The Measurement Models

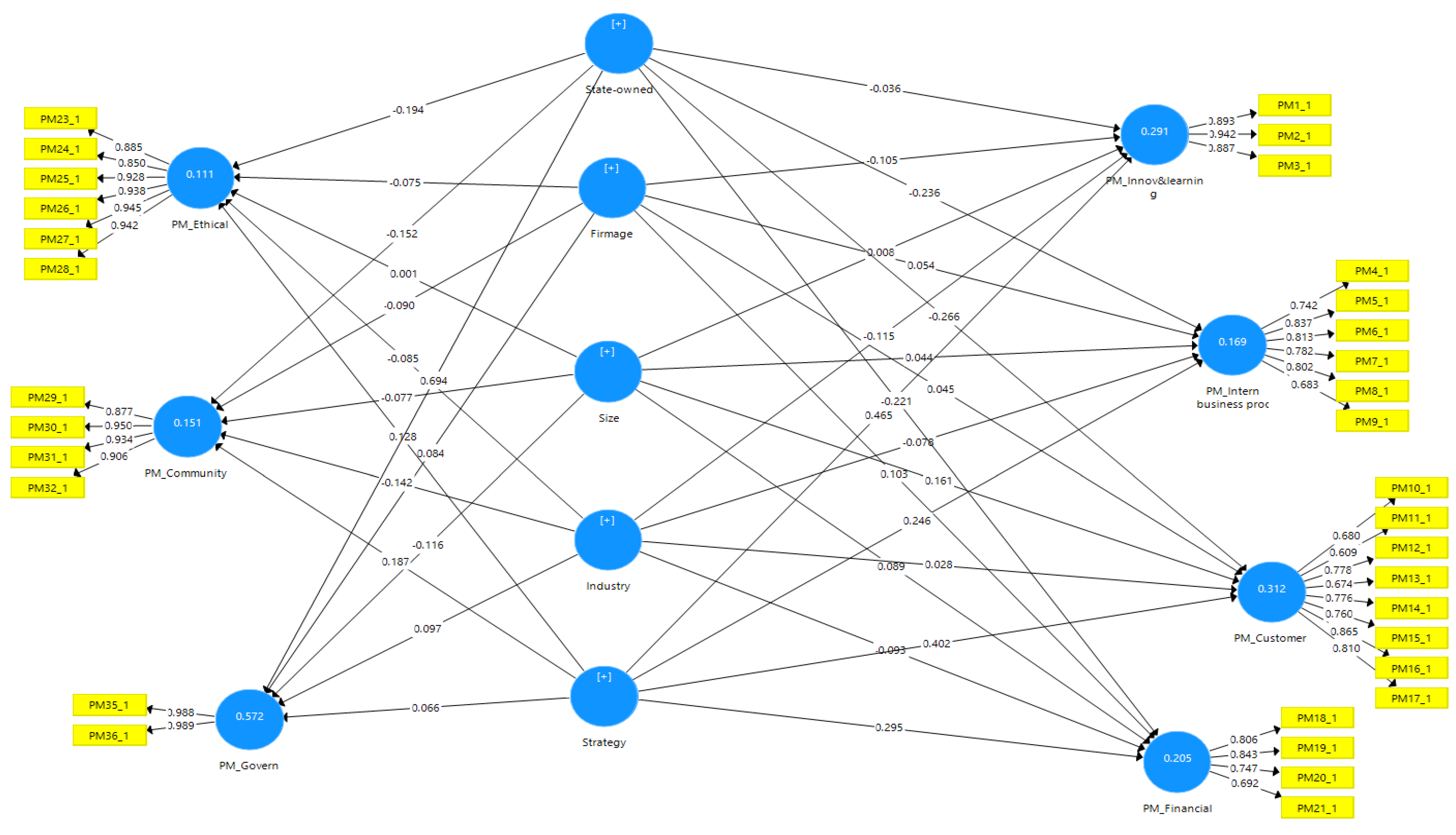

5.2. Structural Model

5.2.1. Ownership Differences and the Relationship with the Design of Performance Measurement Systems (Hypotheses H1 and H2)

5.2.2. Ownership Differences and the Relationship with the Compensation Systems (Hypotheses H3 and H4)

5.3. Additional Analyses

6. Conclusions, Limitations, and Future Research

Author Contributions

Funding

Conflicts of Interest

Appendix A. Measurements of the Constructs

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Main Constructs | Indicators | Codes | |

|---|---|---|---|

| PMS | Compensation Systems | ||

| Economic value-based indicators | |||

| Innovation and learning perspective PM_Innov&learning CO_Innov&learning | 1. Number of new product launches | PM1_1 | CO1_1 |

| 2. Number of new patterns | PM2_1 | CO2_1 | |

| 3. Time to market new products | PM3_1 | CO3_1 | |

| Internal business perspective PM_Intern buss proc CO_Intern buss proc | 4. Labor efficiency variance | PM4_1 | CO4_1 |

| 5. Rate of material scrap loss | PM5_1 | CO5_1 | |

| 6. Material efficiency variance | PM6_1 | CO6_1 | |

| 7. Manufacturing lead time | PM7_1 | CO7_1 | |

| 8. Ratio of good output to total output | PM8_1 | CO8_1 | |

| 9. Percent defective products shipped | PM9_1 | CO9_1 | |

| Customer perspective PM_Customer CO_Customer | 10. Survey of customer satisfaction | PM10_1 | CO10_1 |

| 11. Number of customer complaints | PM11_1 | CO11_1 | |

| 12. Market share | PM12_1 | CO12_1 | |

| 13. Percent shipments returned due to poor quality | PM13_1 | CO13_1 | |

| 14. On-time delivery | PM14_1 | CO14_1 | |

| 15. Warranty repair cost | PM15_1 | CO15_1 | |

| 16. Customer response time | PM16_1 | CO16_1 | |

| 17. Cycle time from order to delivery | PM17_1 | CO17_1 | |

| Financial perspective PM_Financial CO_Financial | 18. Operating income | PM18_1 | CO18_1 |

| 19. Sales growth | PM19_1 | CO19_1 | |

| 20. Return on investment | PM20_1 | CO20_1 | |

| 21. Production costs | PM21_1 | CO21_1 | |

| Societal indicators | |||

| Ethical indicators PM_Ethical CO_Ethical | 22. Code of ethics | PM22_1 | CO22_1 |

| 23. The amount of litigation involving corporate lawbreaking | PM23_1 | CO23_1 | |

| 24. The number of fines resulting from illegal activities (e.g., illegally comply with regimes, and policies such as tax, budget remittance, insurance, etc.) 25. Number of managers and employees convicted of illegal activities | PM24_1 | CO24_1 | |

| PM25_1 | CO25_1 | ||

| 26. Number of fines, number of product recalls, pollution performance measured against industry standard (e.g., number of fines, litigation from pollution, toxic waste) | PM26_1 | CO26_1 | |

| 27. Amount of litigation, number of fines from false advertising | PM27_1 | CO27_1 | |

| 28. Number of fines, amount of litigation from public controversy | PM28_1 | CO28_1 | |

| Community indicators PM_Community CO_Community | 29. Number of giving programs for community welfare as % of earnings | PM29_1 | CO29_1 |

| 30. Number of community programs | PM30_1 | CO31_1 | |

| 31. Cost of community programs | PM31_1 | CO32_1 | |

| 32. Outcomes of community programs | PM32_1 | CO33_1 | |

| Governmental duty indicators PM_Govern CO_Govern | 33. Number of completed services or products assigned by government | PM35_1 | CO35_1 |

| 34. Total value of completed services or products assigned by government | PM36_1 | CO36_1 | |

Appendix B. The Measurement of Strategy

| Types of Strategy | Codes |

|---|---|

| Low cost | |

| 1. Low-cost products/services | ST1_1 |

| 2. Low price | ST2-1 |

| Innovation | |

| 3. Being first to market with new products/services | ST4_1 |

| 4. Extensive range of products/services | ST5_1 |

| 5. Rapid volume or product/service mix changes | ST6_1 |

| 6. Experimenting with new products/services | ST7_1 |

| Customer focus | |

| 7. Providing high-quality products/services | ST7_1 |

| 8. Accurately meeting delivery agreement | ST8_1 |

| 9. Providing effective after-sales services and support | ST9_1 |

| 10. Providing fast delivery of products/services | ST10_1 |

| 11. Superior customer services | ST11_1 |

Appendix C. Outer Loadings of the Measurement Models

| Firmage | Industry | PM_ Community | PM_ Customer | PM_ Ethical | PM_ Financial | PM_ Govern | PM_Intern_ Business_Proc | PM_Innov&Learning | Size | State-Owned | Strategy | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| PM10_1 | −0.014 | −0.076 | 0.208 | 0.68 | 0.209 | 0.414 | −0.036 | 0.407 | 0.405 | 0.129 | −0.221 | 0.313 |

| PM11_1 | 0.056 | −0.126 | 0.149 | 0.609 | 0.469 | 0.281 | −0.128 | 0.279 | 0.107 | 0.206 | −0.154 | 0.174 |

| PM12_1 | −0.077 | −0.238 | 0.412 | 0.778 | 0.362 | 0.531 | −0.173 | 0.437 | 0.412 | 0.149 | −0.358 | 0.482 |

| PM13_1 | −0.069 | −0.146 | 0.188 | 0.674 | 0.481 | 0.408 | −0.109 | 0.409 | 0.266 | 0.161 | −0.173 | 0.245 |

| PM14_1 | −0.047 | −0.071 | 0.335 | 0.776 | 0.27 | 0.493 | −0.063 | 0.504 | 0.273 | 0.175 | −0.288 | 0.324 |

| PM15_1 | −0.149 | −0.037 | 0.375 | 0.76 | 0.344 | 0.344 | −0.038 | 0.468 | 0.423 | 0.08 | −0.224 | 0.383 |

| PM16_1 | 0.006 | −0.028 | 0.297 | 0.865 | 0.224 | 0.383 | −0.158 | 0.461 | 0.408 | 0.258 | −0.267 | 0.404 |

| PM17_1 | −0.073 | −0.031 | 0.341 | 0.81 | 0.293 | 0.404 | −0.176 | 0.597 | 0.443 | 0.098 | −0.331 | 0.418 |

| PM18_1 | −0.001 | −0.099 | 0.171 | 0.353 | 0.152 | 0.806 | −0.044 | 0.374 | 0.213 | 0.137 | −0.282 | 0.217 |

| PM19_1 | −0.02 | −0.11 | 0.231 | 0.449 | 0.196 | 0.843 | −0.073 | 0.406 | 0.205 | 0.155 | −0.312 | 0.315 |

| PM1_1 | −0.172 | −0.136 | 0.351 | 0.42 | 0.249 | 0.246 | −0.103 | 0.383 | 0.893 | 0.075 | −0.214 | 0.468 |

| PM20_1 | 0.015 | −0.126 | 0.301 | 0.512 | 0.314 | 0.747 | 0.156 | 0.466 | 0.32 | 0.082 | −0.084 | 0.291 |

| PM21_1 | −0.008 | −0.298 | 0.252 | 0.411 | 0.21 | 0.692 | −0.058 | 0.583 | 0.288 | 0.047 | −0.234 | 0.278 |

| PM23_1 | −0.091 | −0.23 | 0.462 | 0.415 | 0.885 | 0.271 | −0.171 | 0.358 | 0.276 | 0.036 | −0.266 | 0.203 |

| PM24_1 | −0.107 | −0.141 | 0.41 | 0.344 | 0.85 | 0.262 | −0.089 | 0.305 | 0.161 | −0.043 | −0.177 | 0.188 |

| PM25_1 | −0.152 | −0.136 | 0.396 | 0.365 | 0.928 | 0.248 | −0.081 | 0.358 | 0.301 | −0.002 | −0.256 | 0.176 |

| PM26_1 | −0.16 | −0.174 | 0.429 | 0.442 | 0.938 | 0.286 | −0.152 | 0.402 | 0.3 | −0.02 | −0.316 | 0.162 |

| PM27_1 | −0.174 | −0.165 | 0.537 | 0.405 | 0.945 | 0.228 | −0.134 | 0.309 | 0.351 | 0 | −0.254 | 0.201 |

| PM28_1 | −0.216 | −0.183 | 0.545 | 0.355 | 0.942 | 0.219 | −0.184 | 0.352 | 0.355 | −0.019 | −0.291 | 0.203 |

| PM29_1 | −0.131 | −0.229 | 0.877 | 0.333 | 0.464 | 0.268 | −0.133 | 0.289 | 0.367 | −0.09 | −0.275 | 0.187 |

| PM2_1 | −0.184 | −0.22 | 0.417 | 0.424 | 0.311 | 0.295 | −0.137 | 0.494 | 0.942 | −0.015 | −0.222 | 0.448 |

| PM30_1 | −0.248 | −0.214 | 0.95 | 0.328 | 0.465 | 0.267 | −0.112 | 0.273 | 0.408 | −0.102 | −0.278 | 0.23 |

| PM31_1 | −0.155 | −0.224 | 0.934 | 0.376 | 0.497 | 0.254 | −0.096 | 0.315 | 0.464 | −0.065 | −0.245 | 0.23 |

| PM32_1 | −0.202 | −0.208 | 0.906 | 0.439 | 0.445 | 0.327 | −0.082 | 0.379 | 0.499 | −0.047 | −0.27 | 0.288 |

| PM35_1 | 0.273 | 0.375 | −0.103 | −0.133 | −0.137 | −0.018 | 0.988 | −0.077 | −0.124 | −0.092 | 0.715 | −0.146 |

| PM36_1 | 0.259 | 0.387 | −0.123 | −0.169 | −0.161 | −0.027 | 0.989 | −0.086 | −0.122 | −0.07 | 0.747 | −0.182 |

| PM3_1 | −0.215 | −0.186 | 0.52 | 0.448 | 0.319 | 0.343 | −0.1 | 0.582 | 0.887 | 0.009 | −0.232 | 0.469 |

| PM4_1 | −0.038 | −0.109 | 0.261 | 0.357 | 0.216 | 0.421 | 0.051 | 0.742 | 0.485 | 0.041 | −0.187 | 0.191 |

| PM5_1 | −0.031 | −0.213 | 0.339 | 0.412 | 0.322 | 0.535 | −0.08 | 0.837 | 0.523 | 0.04 | −0.241 | 0.216 |

| PM6_1 | −0.013 | −0.182 | 0.376 | 0.477 | 0.253 | 0.544 | 0.03 | 0.813 | 0.485 | 0.007 | −0.202 | 0.232 |

| PM7_1 | −0.036 | −0.116 | 0.146 | 0.499 | 0.261 | 0.461 | −0.016 | 0.782 | 0.398 | 0.103 | −0.228 | 0.272 |

| PM8_1 | −0.046 | −0.161 | 0.221 | 0.485 | 0.25 | 0.445 | −0.154 | 0.802 | 0.363 | 0.086 | −0.319 | 0.332 |

| PM9_1 | −0.114 | −0.145 | 0.281 | 0.558 | 0.47 | 0.366 | −0.159 | 0.683 | 0.296 | 0.065 | −0.277 | 0.195 |

| ST10_1 | −0.042 | −0.1 | 0.237 | 0.552 | 0.152 | 0.297 | −0.134 | 0.391 | 0.415 | 0.114 | −0.265 | 0.798 |

| ST11_1 | −0.183 | −0.132 | 0.272 | 0.456 | 0.168 | 0.318 | −0.273 | 0.233 | 0.432 | 0.164 | −0.303 | 0.796 |

| ST1_1 | −0.126 | −0.049 | 0.122 | 0.294 | 0.148 | 0.241 | 0 | 0.302 | 0.322 | −0.03 | −0.119 | 0.66 |

| ST2_1 | −0.147 | −0.03 | 0.143 | 0.202 | 0.167 | 0.208 | −0.023 | 0.299 | 0.351 | −0.01 | −0.118 | 0.628 |

| ST3_1 | −0.259 | −0.146 | 0.267 | 0.252 | 0.259 | 0.223 | −0.123 | 0.23 | 0.47 | 0.021 | −0.222 | 0.745 |

| ST4_1 | −0.094 | −0.08 | 0.198 | 0.29 | 0.111 | 0.274 | −0.051 | 0.136 | 0.387 | 0.09 | −0.132 | 0.773 |

| ST5_1 | −0.157 | −0.074 | 0.212 | 0.309 | 0.138 | 0.207 | 0.033 | 0.094 | 0.39 | 0.033 | −0.082 | 0.786 |

| ST6_1 | −0.16 | −0.163 | 0.247 | 0.255 | 0.147 | 0.285 | −0.09 | 0.154 | 0.377 | 0.011 | −0.203 | 0.791 |

| ST7_1 | −0.11 | −0.07 | 0.073 | 0.387 | 0.108 | 0.338 | −0.197 | 0.211 | 0.293 | 0.119 | −0.27 | 0.779 |

| ST8_1 | −0.153 | −0.036 | 0.136 | 0.398 | 0.161 | 0.335 | −0.206 | 0.287 | 0.367 | 0.074 | −0.265 | 0.836 |

| ST9_1 | −0.101 | −0.141 | 0.208 | 0.481 | 0.16 | 0.248 | −0.208 | 0.251 | 0.435 | 0.104 | −0.266 | 0.778 |

| firmage | 1 | 0.107 | −0.204 | −0.067 | −0.166 | −0.007 | 0.269 | −0.06 | −0.21 | 0.239 | 0.308 | −0.18 |

| large_size | 0.239 | −0.001 | −0.083 | 0.205 | −0.008 | 0.138 | −0.081 | 0.077 | 0.025 | 1 | 0.012 | 0.091 |

| manufacturing | 0.107 | 1 | −0.238 | −0.128 | −0.189 | −0.21 | 0.385 | −0.2 | −0.199 | −0.001 | 0.414 | −0.125 |

| state_owned | 0.308 | 0.414 | −0.291 | −0.351 | −0.288 | −0.309 | 0.74 | −0.319 | −0.246 | 0.012 | 1 | −0.279 |

| Firmage | Industry | Non-State Owned | PM_ Community | PM_ Customer | PM_ Ethical | PM_ Financial | PM_ Govern | PM_Intern_ Business_Proc | PM_Innov &Learning | Size | Strategy | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| PM10_1 | −0.014 | −0.076 | 0.154 | 0.208 | 0.683 | 0.206 | 0.414 | −0.036 | 0.406 | 0.406 | 0.129 | 0.313 |

| PM11_1 | 0.056 | −0.126 | 0.108 | 0.149 | 0.612 | 0.47 | 0.283 | −0.128 | 0.273 | 0.107 | 0.206 | 0.174 |

| PM12_1 | −0.077 | −0.238 | 0.218 | 0.412 | 0.778 | 0.361 | 0.53 | −0.173 | 0.436 | 0.412 | 0.149 | 0.482 |

| PM13_1 | −0.069 | −0.146 | 0.106 | 0.189 | 0.676 | 0.479 | 0.408 | −0.109 | 0.406 | 0.266 | 0.161 | 0.245 |

| PM14_1 | −0.047 | −0.071 | 0.23 | 0.334 | 0.775 | 0.269 | 0.492 | −0.063 | 0.507 | 0.273 | 0.175 | 0.324 |

| PM15_1 | −0.149 | −0.037 | 0.092 | 0.376 | 0.757 | 0.344 | 0.343 | −0.038 | 0.468 | 0.423 | 0.08 | 0.383 |

| PM16_1 | 0.006 | −0.028 | 0.214 | 0.297 | 0.866 | 0.223 | 0.384 | −0.158 | 0.46 | 0.408 | 0.258 | 0.404 |

| PM17_1 | −0.073 | −0.031 | 0.173 | 0.342 | 0.807 | 0.292 | 0.404 | −0.176 | 0.598 | 0.442 | 0.098 | 0.418 |

| PM18_1 | −0.001 | −0.099 | 0.272 | 0.173 | 0.353 | 0.152 | 0.811 | −0.044 | 0.375 | 0.213 | 0.137 | 0.217 |

| PM19_1 | −0.02 | −0.11 | 0.323 | 0.232 | 0.449 | 0.196 | 0.85 | −0.073 | 0.407 | 0.204 | 0.155 | 0.315 |

| PM1_1 | −0.172 | −0.136 | 0.151 | 0.353 | 0.418 | 0.247 | 0.246 | −0.103 | 0.383 | 0.896 | 0.075 | 0.468 |

| PM20_1 | 0.015 | −0.126 | 0.09 | 0.301 | 0.512 | 0.312 | 0.749 | 0.156 | 0.464 | 0.319 | 0.082 | 0.291 |

| PM21_1 | −0.008 | −0.298 | 0.177 | 0.251 | 0.41 | 0.209 | 0.679 | −0.058 | 0.583 | 0.287 | 0.047 | 0.278 |

| PM23_1 | −0.091 | −0.23 | −0.004 | 0.462 | 0.415 | 0.887 | 0.271 | −0.171 | 0.353 | 0.275 | 0.036 | 0.203 |

| PM24_1 | −0.107 | −0.141 | −0.071 | 0.41 | 0.343 | 0.856 | 0.264 | −0.089 | 0.302 | 0.16 | −0.043 | 0.188 |

| PM25_1 | −0.152 | −0.136 | 0.008 | 0.396 | 0.364 | 0.926 | 0.249 | −0.081 | 0.355 | 0.301 | −0.002 | 0.176 |

| PM26_1 | −0.16 | −0.174 | 0.035 | 0.429 | 0.442 | 0.934 | 0.286 | −0.152 | 0.398 | 0.3 | −0.02 | 0.162 |

| PM27_1 | −0.174 | −0.165 | −0.046 | 0.536 | 0.406 | 0.945 | 0.228 | −0.134 | 0.305 | 0.351 | 0 | 0.201 |

| PM28_1 | −0.216 | −0.183 | −0.062 | 0.545 | 0.355 | 0.943 | 0.219 | −0.184 | 0.349 | 0.354 | −0.019 | 0.203 |

| PM29_1 | −0.131 | −0.229 | 0.002 | 0.873 | 0.332 | 0.466 | 0.267 | −0.133 | 0.288 | 0.366 | −0.09 | 0.187 |

| PM2_1 | −0.184 | −0.22 | 0.108 | 0.417 | 0.423 | 0.31 | 0.292 | −0.137 | 0.494 | 0.942 | −0.015 | 0.448 |

| PM30_1 | −0.248 | −0.214 | −0.042 | 0.95 | 0.326 | 0.467 | 0.266 | −0.112 | 0.271 | 0.407 | −0.102 | 0.23 |

| PM31_1 | −0.155 | −0.224 | −0.022 | 0.935 | 0.375 | 0.5 | 0.254 | −0.096 | 0.314 | 0.463 | −0.065 | 0.23 |

| PM32_1 | −0.202 | −0.208 | −0.004 | 0.908 | 0.437 | 0.447 | 0.328 | −0.082 | 0.379 | 0.498 | −0.047 | 0.288 |

| PM35_1 | 0.273 | 0.375 | −0.35 | −0.103 | −0.133 | −0.137 | −0.017 | 0.988 | −0.074 | −0.124 | −0.092 | −0.146 |

| PM36_1 | 0.259 | 0.387 | −0.377 | −0.122 | −0.168 | −0.161 | −0.025 | 0.989 | −0.084 | −0.122 | −0.07 | −0.182 |

| PM3_1 | −0.215 | −0.186 | 0.063 | 0.521 | 0.446 | 0.319 | 0.342 | −0.1 | 0.582 | 0.884 | 0.009 | 0.469 |

| PM4_1 | −0.038 | −0.109 | 0.088 | 0.262 | 0.356 | 0.215 | 0.419 | 0.051 | 0.739 | 0.485 | 0.041 | 0.191 |

| PM5_1 | −0.031 | −0.213 | 0.111 | 0.339 | 0.41 | 0.321 | 0.532 | −0.08 | 0.835 | 0.521 | 0.04 | 0.215 |

| PM6_1 | −0.013 | −0.182 | 0.136 | 0.376 | 0.475 | 0.252 | 0.541 | 0.03 | 0.816 | 0.484 | 0.007 | 0.232 |

| PM7_1 | −0.036 | −0.116 | 0.152 | 0.147 | 0.496 | 0.259 | 0.458 | −0.016 | 0.789 | 0.397 | 0.103 | 0.272 |

| PM8_1 | −0.046 | −0.161 | 0.192 | 0.221 | 0.483 | 0.248 | 0.44 | −0.154 | 0.805 | 0.362 | 0.086 | 0.332 |

| PM9_1 | −0.114 | −0.145 | 0.146 | 0.281 | 0.557 | 0.468 | 0.364 | −0.159 | 0.672 | 0.295 | 0.065 | 0.195 |

| ST10_1 | −0.042 | −0.1 | 0.155 | 0.237 | 0.55 | 0.151 | 0.295 | −0.134 | 0.391 | 0.414 | 0.114 | 0.798 |

| ST11_1 | −0.183 | −0.132 | 0.121 | 0.272 | 0.455 | 0.168 | 0.319 | −0.273 | 0.235 | 0.432 | 0.164 | 0.796 |

| ST1_1 | −0.126 | −0.049 | 0.103 | 0.124 | 0.293 | 0.149 | 0.24 | 0 | 0.304 | 0.323 | −0.03 | 0.66 |

| ST2_1 | −0.147 | −0.03 | 0.108 | 0.144 | 0.201 | 0.167 | 0.206 | −0.023 | 0.3 | 0.351 | −0.01 | 0.628 |

| ST3_1 | −0.259 | −0.146 | 0.018 | 0.268 | 0.25 | 0.261 | 0.223 | −0.123 | 0.23 | 0.47 | 0.021 | 0.745 |

| ST4_1 | −0.094 | −0.08 | 0.031 | 0.198 | 0.289 | 0.114 | 0.276 | −0.051 | 0.136 | 0.388 | 0.09 | 0.773 |

| ST5_1 | −0.157 | −0.074 | 0.001 | 0.212 | 0.308 | 0.14 | 0.209 | 0.033 | 0.096 | 0.39 | 0.033 | 0.786 |

| ST6_1 | −0.16 | −0.163 | 0.056 | 0.248 | 0.253 | 0.15 | 0.285 | −0.09 | 0.155 | 0.376 | 0.011 | 0.792 |

| ST7_1 | −0.11 | −0.07 | 0.209 | 0.074 | 0.386 | 0.107 | 0.339 | −0.197 | 0.21 | 0.294 | 0.119 | 0.779 |

| ST8_1 | −0.153 | −0.036 | 0.166 | 0.137 | 0.396 | 0.161 | 0.334 | −0.206 | 0.288 | 0.367 | 0.074 | 0.836 |

| ST9_1 | −0.101 | −0.141 | 0.164 | 0.209 | 0.481 | 0.16 | 0.247 | −0.208 | 0.251 | 0.436 | 0.104 | 0.778 |

| Non-state-owned | 0.037 | −0.123 | 1 | −0.019 | 0.225 | −0.027 | 0.291 | −0.368 | 0.183 | 0.118 | −0.001 | 0.141 |

| firmage | 1 | 0.107 | 0.037 | −0.205 | −0.066 | −0.166 | −0.007 | 0.269 | −0.059 | −0.21 | 0.239 | −0.18 |

| large_size | 0.239 | −0.001 | −0.001 | −0.082 | 0.208 | −0.008 | 0.139 | −0.081 | 0.077 | 0.025 | 1 | 0.091 |

| manufacturing | 0.107 | 1 | −0.123 | −0.238 | −0.128 | −0.189 | −0.206 | 0.386 | −0.2 | −0.199 | −0.001 | −0.125 |

| CO_ Customer | CO_ Financial | CO_Intern_ Business_Proc | CO_ Community | CO_ Ethical | CO_ Govern | CO_Innov &Learning | Firmage | Industry | Size | State-owned | Strategy | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| CO10_1 | 0.727 | 0.597 | 0.513 | 0.303 | 0.281 | −0.076 | 0.495 | −0.103 | −0.127 | 0.044 | −0.283 | 0.359 |

| CO11_1 | 0.667 | 0.316 | 0.447 | 0.158 | 0.549 | −0.158 | 0.236 | 0.007 | −0.098 | 0.137 | −0.201 | 0.266 |

| CO12_1 | 0.8 | 0.535 | 0.538 | 0.416 | 0.366 | −0.192 | 0.406 | −0.041 | −0.233 | 0.092 | −0.395 | 0.399 |

| CO13_1 | 0.721 | 0.393 | 0.54 | 0.174 | 0.507 | −0.151 | 0.313 | −0.072 | −0.19 | 0.127 | −0.244 | 0.241 |

| CO14_1 | 0.785 | 0.598 | 0.555 | 0.315 | 0.228 | −0.109 | 0.246 | −0.068 | −0.088 | 0.114 | −0.301 | 0.295 |

| CO15_1 | 0.742 | 0.402 | 0.545 | 0.365 | 0.358 | −0.026 | 0.407 | −0.139 | −0.051 | 0.002 | −0.21 | 0.368 |

| CO16_1 | 0.874 | 0.485 | 0.6 | 0.314 | 0.261 | −0.225 | 0.48 | −0.065 | −0.083 | 0.124 | −0.351 | 0.41 |

| CO17_1 | 0.823 | 0.479 | 0.623 | 0.273 | 0.31 | −0.13 | 0.425 | −0.065 | −0.033 | 0.049 | −0.295 | 0.397 |

| CO18_1 | 0.452 | 0.839 | 0.449 | 0.161 | 0.132 | −0.016 | 0.238 | −0.04 | −0.009 | 0.141 | −0.314 | 0.194 |

| CO19_1 | 0.458 | 0.844 | 0.425 | 0.14 | 0.179 | −0.043 | 0.182 | −0.064 | −0.043 | 0.061 | −0.321 | 0.248 |

| CO1_1 | 0.453 | 0.322 | 0.444 | 0.396 | 0.281 | −0.186 | 0.93 | −0.18 | −0.142 | 0.07 | −0.289 | 0.468 |

| CO20_1 | 0.586 | 0.813 | 0.581 | 0.334 | 0.339 | 0.069 | 0.369 | 0.023 | −0.1 | 0.051 | −0.223 | 0.286 |

| CO21_1 | 0.519 | 0.732 | 0.645 | 0.286 | 0.237 | −0.125 | 0.339 | −0.054 | −0.225 | 0.033 | −0.3 | 0.263 |

| CO23_1 | 0.448 | 0.33 | 0.436 | 0.482 | 0.903 | −0.155 | 0.328 | −0.082 | −0.231 | −0.003 | −0.304 | 0.265 |

| CO24_1 | 0.405 | 0.259 | 0.375 | 0.415 | 0.856 | −0.11 | 0.196 | −0.104 | −0.169 | −0.09 | −0.246 | 0.235 |

| CO25_1 | 0.391 | 0.253 | 0.403 | 0.403 | 0.92 | −0.076 | 0.31 | −0.11 | −0.177 | 0.027 | −0.289 | 0.24 |

| CO26_1 | 0.463 | 0.288 | 0.431 | 0.469 | 0.943 | −0.157 | 0.332 | −0.129 | −0.213 | 0.018 | −0.35 | 0.219 |

| CO27_1 | 0.394 | 0.185 | 0.364 | 0.581 | 0.935 | −0.115 | 0.327 | −0.11 | −0.186 | 0.048 | −0.258 | 0.235 |

| CO28_1 | 0.362 | 0.189 | 0.394 | 0.577 | 0.948 | −0.16 | 0.34 | −0.139 | −0.212 | 0.047 | −0.292 | 0.243 |

| CO29_1 | 0.313 | 0.282 | 0.358 | 0.891 | 0.477 | −0.123 | 0.393 | −0.108 | −0.263 | −0.076 | −0.271 | 0.247 |

| CO2_1 | 0.47 | 0.334 | 0.546 | 0.456 | 0.33 | −0.193 | 0.953 | −0.192 | −0.232 | 0.025 | −0.269 | 0.429 |

| CO30_1 | 0.33 | 0.25 | 0.316 | 0.952 | 0.493 | −0.071 | 0.437 | −0.17 | −0.26 | −0.064 | −0.245 | 0.27 |

| CO31_1 | 0.377 | 0.289 | 0.375 | 0.948 | 0.505 | −0.047 | 0.486 | −0.142 | −0.235 | −0.023 | −0.223 | 0.289 |

| CO32_1 | 0.416 | 0.246 | 0.386 | 0.932 | 0.504 | −0.044 | 0.498 | −0.149 | −0.238 | −0.014 | −0.243 | 0.337 |

| CO35_1 | −0.167 | −0.038 | −0.095 | −0.063 | −0.138 | 0.992 | −0.18 | 0.254 | 0.356 | −0.135 | 0.669 | −0.136 |

| CO36_1 | −0.185 | −0.044 | −0.105 | −0.087 | −0.143 | 0.993 | −0.194 | 0.273 | 0.357 | −0.119 | 0.719 | −0.174 |

| CO3_1 | 0.468 | 0.322 | 0.595 | 0.514 | 0.327 | −0.146 | 0.909 | −0.204 | −0.181 | 0.013 | −0.255 | 0.427 |

| CO4_1 | 0.466 | 0.53 | 0.769 | 0.299 | 0.33 | −0.01 | 0.548 | −0.06 | −0.12 | 0.008 | −0.246 | 0.179 |

| CO5_1 | 0.538 | 0.561 | 0.871 | 0.375 | 0.377 | −0.051 | 0.499 | −0.008 | −0.215 | 0.041 | −0.278 | 0.197 |

| CO6_1 | 0.581 | 0.608 | 0.874 | 0.425 | 0.356 | −0.047 | 0.509 | −0.046 | −0.235 | 0.031 | −0.301 | 0.256 |

| CO7_1 | 0.638 | 0.566 | 0.848 | 0.291 | 0.397 | −0.092 | 0.447 | −0.083 | −0.204 | 0.048 | −0.326 | 0.3 |

| CO8_1 | 0.642 | 0.546 | 0.839 | 0.268 | 0.276 | −0.167 | 0.435 | −0.057 | −0.152 | 0.062 | −0.339 | 0.323 |

| CO9_1 | 0.605 | 0.39 | 0.707 | 0.237 | 0.462 | −0.107 | 0.382 | −0.026 | −0.109 | 0.096 | −0.21 | 0.201 |

| ST10_1 | 0.568 | 0.312 | 0.4 | 0.289 | 0.218 | −0.126 | 0.407 | −0.042 | −0.1 | 0.114 | −0.265 | 0.806 |

| ST11_1 | 0.405 | 0.263 | 0.261 | 0.353 | 0.221 | −0.265 | 0.421 | −0.183 | −0.132 | 0.164 | −0.303 | 0.799 |

| ST1_1 | 0.267 | 0.096 | 0.245 | 0.158 | 0.188 | −0.03 | 0.262 | −0.126 | −0.049 | −0.03 | −0.119 | 0.644 |

| ST2_1 | 0.15 | 0.052 | 0.218 | 0.193 | 0.195 | −0.034 | 0.262 | −0.147 | −0.03 | −0.01 | −0.118 | 0.611 |

| ST3_1 | 0.233 | 0.192 | 0.209 | 0.3 | 0.282 | −0.092 | 0.428 | −0.259 | −0.146 | 0.021 | −0.222 | 0.744 |

| ST4_1 | 0.256 | 0.198 | 0.144 | 0.207 | 0.142 | −0.045 | 0.353 | −0.094 | −0.08 | 0.09 | −0.132 | 0.773 |

| ST5_1 | 0.237 | 0.183 | 0.145 | 0.275 | 0.188 | 0.051 | 0.371 | −0.157 | −0.074 | 0.033 | −0.082 | 0.788 |

| ST6_1 | 0.263 | 0.274 | 0.189 | 0.265 | 0.196 | −0.072 | 0.357 | −0.16 | −0.163 | 0.011 | −0.203 | 0.795 |

| ST7_1 | 0.334 | 0.29 | 0.159 | 0.038 | 0.117 | −0.163 | 0.288 | −0.11 | −0.07 | 0.119 | −0.27 | 0.779 |

| ST8_1 | 0.399 | 0.34 | 0.246 | 0.154 | 0.198 | −0.202 | 0.345 | −0.153 | −0.036 | 0.074 | −0.265 | 0.837 |

| ST9_1 | 0.458 | 0.258 | 0.242 | 0.26 | 0.215 | −0.203 | 0.408 | −0.101 | −0.141 | 0.104 | −0.266 | 0.782 |

| firmage | −0.089 | −0.044 | −0.059 | −0.153 | −0.123 | 0.266 | −0.206 | 1 | 0.107 | 0.239 | 0.308 | −0.178 |

| large_size | 0.111 | 0.087 | 0.057 | −0.047 | 0.01 | −0.128 | 0.039 | 0.239 | −0.001 | 1 | 0.012 | 0.093 |

| manufacturing | −0.15 | −0.123 | −0.215 | −0.268 | −0.217 | 0.359 | −0.198 | 0.107 | 1 | −0.001 | 0.414 | −0.127 |

| state_owned | −0.38 | −0.362 | −0.352 | −0.264 | −0.318 | 0.7 | −0.291 | 0.308 | 0.414 | 0.012 | 1 | −0.282 |

| CO_ Customer | CO_ Financial | CO_Intern_ Business_Proc | CO_ Cmmunity | CO_ Ethical | CO_ Govern | CO_Innov &Learning | Non-State-Owned | Firmage | Industry | Size | Strategy | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| CO10_1 | 0.727 | 0.595 | 0.511 | 0.302 | 0.28 | −0.076 | 0.496 | 0.175 | −0.103 | −0.127 | 0.044 | 0.359 |

| CO11_1 | 0.663 | 0.314 | 0.448 | 0.158 | 0.549 | −0.158 | 0.235 | 0.08 | 0.007 | −0.098 | 0.137 | 0.266 |

| CO12_1 | 0.798 | 0.53 | 0.539 | 0.415 | 0.366 | −0.192 | 0.406 | 0.247 | −0.041 | −0.233 | 0.092 | 0.399 |

| CO13_1 | 0.719 | 0.385 | 0.543 | 0.176 | 0.506 | −0.151 | 0.312 | 0.142 | −0.072 | −0.19 | 0.127 | 0.241 |

| CO14_1 | 0.787 | 0.596 | 0.56 | 0.315 | 0.227 | −0.109 | 0.246 | 0.239 | −0.068 | −0.088 | 0.114 | 0.295 |

| CO15_1 | 0.744 | 0.397 | 0.549 | 0.366 | 0.358 | −0.026 | 0.407 | 0.103 | −0.139 | −0.051 | 0.002 | 0.368 |

| CO16_1 | 0.874 | 0.478 | 0.602 | 0.315 | 0.26 | −0.225 | 0.48 | 0.223 | −0.065 | −0.083 | 0.124 | 0.41 |

| CO17_1 | 0.824 | 0.476 | 0.626 | 0.274 | 0.309 | −0.13 | 0.425 | 0.192 | −0.065 | −0.033 | 0.049 | 0.397 |

| CO18_1 | 0.453 | 0.856 | 0.45 | 0.161 | 0.132 | −0.016 | 0.238 | 0.353 | −0.04 | −0.009 | 0.141 | 0.194 |

| CO19_1 | 0.458 | 0.855 | 0.427 | 0.14 | 0.178 | −0.043 | 0.182 | 0.316 | −0.064 | −0.043 | 0.061 | 0.248 |

| CO1_1 | 0.454 | 0.322 | 0.442 | 0.397 | 0.281 | −0.186 | 0.931 | 0.199 | −0.18 | −0.142 | 0.07 | 0.468 |

| CO20_1 | 0.587 | 0.808 | 0.58 | 0.333 | 0.339 | 0.069 | 0.369 | 0.195 | 0.023 | −0.1 | 0.051 | 0.285 |

| CO21_1 | 0.52 | 0.709 | 0.645 | 0.285 | 0.237 | −0.125 | 0.339 | 0.23 | −0.054 | −0.225 | 0.033 | 0.263 |

| CO23_1 | 0.447 | 0.324 | 0.433 | 0.482 | 0.904 | −0.155 | 0.328 | 0.037 | −0.082 | −0.231 | −0.003 | 0.265 |

| CO24_1 | 0.403 | 0.258 | 0.373 | 0.415 | 0.858 | −0.11 | 0.196 | −0.028 | −0.104 | −0.169 | −0.09 | 0.235 |

| CO25_1 | 0.389 | 0.249 | 0.401 | 0.403 | 0.919 | −0.076 | 0.31 | 0.042 | −0.11 | −0.177 | 0.027 | 0.24 |

| CO26_1 | 0.461 | 0.282 | 0.429 | 0.469 | 0.94 | −0.157 | 0.332 | 0.08 | −0.129 | −0.213 | 0.018 | 0.219 |

| CO27_1 | 0.392 | 0.18 | 0.361 | 0.581 | 0.935 | −0.115 | 0.326 | −0.03 | −0.11 | −0.186 | 0.048 | 0.235 |

| CO28_1 | 0.361 | 0.182 | 0.392 | 0.577 | 0.948 | −0.16 | 0.34 | −0.029 | −0.139 | −0.212 | 0.047 | 0.243 |

| CO29_1 | 0.313 | 0.273 | 0.355 | 0.887 | 0.478 | −0.123 | 0.393 | 0.002 | −0.108 | −0.263 | −0.076 | 0.247 |

| CO2_1 | 0.47 | 0.325 | 0.543 | 0.456 | 0.329 | −0.193 | 0.953 | 0.129 | −0.192 | −0.232 | 0.025 | 0.429 |

| CO30_1 | 0.33 | 0.243 | 0.314 | 0.952 | 0.494 | −0.071 | 0.436 | −0.067 | −0.17 | −0.26 | −0.064 | 0.27 |

| CO31_1 | 0.378 | 0.283 | 0.375 | 0.949 | 0.506 | −0.047 | 0.486 | −0.063 | −0.142 | −0.235 | −0.023 | 0.289 |

| CO32_1 | 0.417 | 0.244 | 0.387 | 0.934 | 0.506 | −0.044 | 0.498 | −0.033 | −0.149 | −0.238 | −0.014 | 0.337 |

| CO35_1 | −0.166 | −0.035 | −0.097 | −0.062 | −0.138 | 0.992 | −0.18 | −0.347 | 0.254 | 0.356 | −0.135 | −0.136 |

| CO36_1 | −0.184 | −0.042 | −0.107 | −0.086 | −0.143 | 0.993 | −0.194 | −0.376 | 0.273 | 0.357 | −0.119 | −0.174 |

| CO3_1 | 0.468 | 0.315 | 0.599 | 0.515 | 0.327 | −0.146 | 0.908 | 0.12 | −0.204 | −0.181 | 0.013 | 0.427 |

| CO4_1 | 0.467 | 0.526 | 0.759 | 0.298 | 0.33 | −0.01 | 0.547 | 0.112 | −0.06 | −0.12 | 0.008 | 0.179 |

| CO5_1 | 0.538 | 0.551 | 0.864 | 0.373 | 0.377 | −0.051 | 0.499 | 0.093 | −0.008 | −0.215 | 0.041 | 0.197 |

| CO6_1 | 0.581 | 0.601 | 0.872 | 0.424 | 0.355 | −0.047 | 0.508 | 0.172 | −0.046 | −0.235 | 0.031 | 0.256 |

| CO7_1 | 0.639 | 0.56 | 0.854 | 0.292 | 0.396 | −0.092 | 0.447 | 0.193 | −0.083 | −0.204 | 0.048 | 0.3 |

| CO8_1 | 0.643 | 0.538 | 0.848 | 0.268 | 0.275 | −0.167 | 0.435 | 0.248 | −0.057 | −0.152 | 0.062 | 0.323 |

| CO9_1 | 0.604 | 0.377 | 0.704 | 0.237 | 0.461 | −0.107 | 0.381 | 0.082 | −0.026 | −0.109 | 0.096 | 0.201 |

| ST10_1 | 0.568 | 0.305 | 0.403 | 0.289 | 0.217 | −0.126 | 0.407 | 0.155 | −0.042 | −0.1 | 0.114 | 0.805 |

| ST11_1 | 0.405 | 0.261 | 0.264 | 0.353 | 0.221 | −0.265 | 0.422 | 0.121 | −0.183 | −0.132 | 0.164 | 0.799 |

| ST1_1 | 0.267 | 0.094 | 0.248 | 0.159 | 0.188 | −0.029 | 0.262 | 0.103 | −0.126 | −0.049 | −0.03 | 0.644 |

| ST2_1 | 0.15 | 0.05 | 0.218 | 0.195 | 0.196 | −0.034 | 0.262 | 0.108 | −0.147 | −0.03 | −0.01 | 0.611 |

| ST3_1 | 0.234 | 0.188 | 0.213 | 0.301 | 0.283 | −0.092 | 0.428 | 0.018 | −0.259 | −0.146 | 0.021 | 0.744 |

| ST4_1 | 0.256 | 0.198 | 0.144 | 0.207 | 0.143 | −0.045 | 0.353 | 0.031 | −0.094 | −0.08 | 0.09 | 0.773 |

| ST5_1 | 0.237 | 0.182 | 0.149 | 0.276 | 0.189 | 0.051 | 0.371 | 0.001 | −0.157 | −0.074 | 0.033 | 0.788 |

| ST6_1 | 0.263 | 0.271 | 0.19 | 0.265 | 0.196 | −0.072 | 0.357 | 0.056 | −0.16 | −0.163 | 0.011 | 0.795 |

| ST7_1 | 0.334 | 0.292 | 0.162 | 0.038 | 0.116 | −0.163 | 0.288 | 0.209 | −0.11 | −0.07 | 0.119 | 0.779 |

| ST8_1 | 0.4 | 0.337 | 0.249 | 0.154 | 0.198 | −0.202 | 0.345 | 0.166 | −0.153 | −0.036 | 0.074 | 0.837 |

| ST9_1 | 0.457 | 0.253 | 0.245 | 0.261 | 0.215 | −0.203 | 0.409 | 0.164 | −0.101 | −0.141 | 0.104 | 0.782 |

| Non−state owned | 0.236 | 0.342 | 0.197 | −0.044 | 0.014 | −0.364 | 0.162 | 1 | 0.037 | −0.123 | −0.001 | 0.14 |

| firmage | −0.089 | −0.044 | −0.06 | −0.154 | −0.122 | 0.266 | −0.206 | 0.037 | 1 | 0.107 | 0.239 | −0.178 |

| large_size | 0.11 | 0.089 | 0.058 | −0.046 | 0.01 | −0.128 | 0.039 | −0.001 | 0.239 | −0.001 | 1 | 0.093 |

| manufacturing | −0.149 | −0.115 | −0.216 | −0.267 | −0.217 | 0.359 | −0.198 | −0.123 | 0.107 | 1 | −0.001 | −0.127 |

Appendix D. Discriminant Validity (Fornell–Larcker Criterion) of the Measurements of the Models

| Firmage | Industry | PM_ Community | PM_ Customer | PM_ Ethical | PM_ Financial | PM_ Govern | PM_Intern_ Business_Proc | PM_Innov &Learning | Size | State-Owned | Strategy | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Firmage | 1 | |||||||||||

| Industry | 0.107 | 1 | ||||||||||

| PM_Community | −0.204 | −0.238 | 0.917 | |||||||||

| PM_Customer | −0.067 | −0.128 | 0.403 | 0.748 | ||||||||

| PM_Ethical | −0.166 | −0.189 | 0.509 | 0.424 | 0.916 | |||||||

| PM_Financial | −0.007 | −0.21 | 0.305 | 0.553 | 0.274 | 0.774 | ||||||

| PM_Govern | 0.269 | 0.385 | −0.115 | −0.153 | −0.151 | −0.023 | 0.988 | |||||

| PM_Intern_ business_proc | −0.06 | −0.2 | 0.343 | 0.603 | 0.381 | 0.593 | −0.083 | 0.778 | ||||

| PM_innov&learning | −0.21 | −0.199 | 0.475 | 0.475 | 0.324 | 0.326 | −0.124 | 0.538 | 0.908 | |||

| Size | 0.239 | −0.001 | −0.083 | 0.205 | −0.008 | 0.138 | −0.081 | 0.077 | 0.025 | 1 | ||

| State-owned | 0.308 | 0.414 | −0.291 | −0.351 | −0.288 | −0.309 | 0.74 | −0.319 | −0.246 | 0.012 | 1 | |

| Strategy | −0.18 | −0.125 | 0.257 | 0.479 | 0.206 | 0.358 | −0.166 | 0.316 | 0.509 | 0.091 | −0.279 | 0.763 |

| Firmage | Industry | Non-State Owned | PM_ Community | PM_ Customer | PM_ Ethical | PM_ Financial | PM_ Govern | PM_Intern_ Business_Proc | PM_Innov &Learning | Size | Strategy | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Firmage | 1 | |||||||||||

| Industry | 0.107 | 1 | ||||||||||

| Non-State-owned | 0.037 | −0.123 | 1 | |||||||||

| PM_Community | −0.205 | −0.238 | −0.019 | 0.917 | ||||||||

| PM_Customer | −0.066 | −0.128 | 0.225 | 0.402 | 0.748 | |||||||

| PM_Ethical | −0.166 | −0.189 | −0.027 | 0.511 | 0.423 | 0.916 | ||||||

| PM_Financial | −0.007 | −0.206 | 0.291 | 0.305 | 0.553 | 0.274 | 0.775 | |||||

| PM_Govern | 0.269 | 0.386 | −0.368 | −0.114 | −0.153 | −0.151 | −0.021 | 0.988 | ||||

| PM_Intern_ business_proc | −0.059 | −0.2 | 0.183 | 0.342 | 0.6 | 0.375 | 0.59 | −0.08 | 0.778 | |||

| PM_innov&learning | −0.21 | −0.199 | 0.118 | 0.475 | 0.473 | 0.322 | 0.324 | −0.124 | 0.537 | 0.908 | ||

| Size | 0.239 | −0.001 | −0.001 | −0.082 | 0.208 | −0.008 | 0.139 | −0.081 | 0.077 | 0.025 | 1 | |

| Strategy | −0.18 | −0.125 | 0.141 | 0.257 | 0.477 | 0.207 | 0.357 | −0.166 | 0.317 | 0.509 | 0.091 | 0.763 |

| CO_ Customer | CO_ Financial | CO_Intern_ Business_Proc | CO_ Community | CO_ Ethical | CO_ Govern | CO_Innov &Learning | Firmage | Industry | Size | State-Owned | Strategy | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| CO_Customer | 0.77 | |||||||||||

| CO_Financial | 0.625 | 0.808 | ||||||||||

| CO_Intern_ business_proc | 0.709 | 0.656 | 0.820 | |||||||||

| CO_community | 0.386 | 0.286 | 0.386 | 0.931 | ||||||||

| CO_ethical | 0.448 | 0.275 | 0.438 | 0.532 | 0.918 | |||||||

| CO_govern | −0.178 | −0.042 | −0.101 | −0.076 | −0.142 | 0.992 | ||||||

| CO_innov&learning | 0.498 | 0.35 | 0.568 | 0.488 | 0.335 | −0.189 | 0.931 | |||||

| firmage | −0.089 | −0.044 | −0.059 | −0.153 | −0.123 | 0.266 | −0.206 | 1 | ||||

| industry | −0.15 | −0.123 | −0.215 | −0.268 | −0.217 | 0.359 | −0.198 | 0.107 | 1 | |||

| size | 0.111 | 0.087 | 0.057 | −0.047 | 0.01 | −0.128 | 0.039 | 0.239 | −0.001 | 1 | ||

| State-owned | −0.38 | −0.362 | −0.352 | −0.264 | −0.318 | 0.7 | −0.291 | 0.308 | 0.414 | 0.012 | 1 | |

| strategy | 0.452 | 0.308 | 0.305 | 0.308 | 0.261 | −0.157 | 0.474 | −0.178 | −0.127 | 0.093 | −0.282 | 0.763 |

| CO_ Customer | CO_ Financial | CO_Intern_ Business_Proc | CO_ Community | CO_ Ethical | CO_ Govern | CO_Innov &Learning | Non-State Owned | Firmage | Industry | Size | Strategy | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| CO_Customer | 0.77 | |||||||||||

| CO_Financial | 0.621 | 0.809 | ||||||||||

| CO_Intern_ business_proc | 0.712 | 0.647 | 0.819 | |||||||||

| CO_community | 0.388 | 0.279 | 0.384 | 0.931 | ||||||||

| CO_ethical | 0.445 | 0.269 | 0.435 | 0.533 | 0.918 | |||||||

| CO_govern | −0.177 | −0.039 | −0.103 | −0.075 | −0.142 | 0.992 | ||||||

| CO_innov&learning | 0.498 | 0.345 | 0.565 | 0.489 | 0.335 | −0.189 | 0.931 | |||||

| Non-state owned | 0.236 | 0.342 | 0.197 | −0.044 | 0.014 | −0.364 | 0.162 | 1 | ||||

| firmage | −0.089 | −0.044 | −0.06 | −0.154 | −0.122 | 0.266 | −0.206 | 0.037 | 1 | |||

| industry | −0.149 | −0.115 | −0.216 | −0.267 | −0.217 | 0.359 | −0.198 | −0.123 | 0.107 | 1 | ||

| size | 0.11 | 0.089 | 0.058 | −0.046 | 0.01 | −0.128 | 0.039 | −0.001 | 0.239 | −0.001 | 1 | |

| strategy | 0.452 | 0.305 | 0.308 | 0.308 | 0.261 | −0.157 | 0.474 | 0.14 | −0.178 | −0.127 | 0.093 | 0.763 |

References

- Otley, D.T. The contingency theory of management accounting achievement and prognosis. Account. Organ. Soc. 1980, 5, 413–428. [Google Scholar] [CrossRef]

- Chenhall, R.H. Theorizing contingencies in management control systems research. In Handbook of Management Accounting; Chapman, C.S., Hopwood, A.G., Shields, M.D., Eds.; Elsevier: Amsterdam, The Netherlands, 2007; Volume 1, pp. 163–205. [Google Scholar]

- Merchant, K.; Van der Stede, W.A. Management Control. Systems: Performance Measurement, Evaluation and Incentives; Prentice Hall, Pearson Education Limited: England, UK, 2007. [Google Scholar]

- Malmi, T.; Brown, D.A. Management control system as a package—Opportunities, challenges and research directions. Manag. Account. Res. 2008, 19, 287–300. [Google Scholar] [CrossRef]

- Abernethy, M.A.; Bouwens, J.; Van Lent, L. Leadership and control system design. Manag. Account. Res. 2010, 21, 2–16. [Google Scholar] [CrossRef]

- Jansen, E.P. The Effec of Leadership Style on the Information receivers’ reaction to management accounting change. Manag. Account. Res. 2011, 22, 105–124. [Google Scholar] [CrossRef]

- Nguyen, T.T.; Mia, L.; Winata, L.; Chong, V.K. Effect of transformational-Leadership style and management control system on managerial performance. J. Bus. Res. 2017, 70, 202–213. [Google Scholar] [CrossRef]

- O’Connor, N.G.; Deng, J.; Luo, Y. Political constraints, organization design and performance measurement in China’s State-owned enterprises. Account. Organ. Soc. 2006, 31, 157–177. [Google Scholar] [CrossRef]

- Warfield, T.D.; Wild, J.J.; Wild, K.L. Managerial ownership, accounting choices, and informativeness of earnings. J. Account. Econ. 1995, 20, 61–91. [Google Scholar] [CrossRef]

- Firth, M. The diffusion of managerial accounting procedures in the People’s Republic of China and the influence of foreign partnered joint ventures. Account. Organ. Soc. 1996, 21, 629–654. [Google Scholar] [CrossRef]

- Yan, A.; Gray, B. Antecedents and effects of parent control in international joint ventures. J. Manag. Stud. 2001, 38, 393–416. [Google Scholar] [CrossRef]

- Van der Stede, W.A. The effect of national culture on management control. and incentive system design in multi-business firms: Evidence of intracorporate isomorphism. Eur. Account. Rev. 2003, 12, 263–285. [Google Scholar] [CrossRef]

- Wong, M.C.; Luk, S.T.; Li, S.C. Equity Onwership and Management Control. in Sino-Foreign Joint Venture Hotels. Serv. Ind. J. 2005, 25, 117–133. [Google Scholar] [CrossRef]

- Li, P.; Tang, G. Performance measurement design within its organizational context—Evidence from China. Manag. Account. Res. 2009, 20, 193–207. [Google Scholar] [CrossRef]

- Carker, M.; Siverbo, S. Management control. in public sector joint ventures. Manag. Account. Res. 2011, 22, 330–348. [Google Scholar] [CrossRef]

- Sharma, P. An overview of the field of family business studies: Current status and direction for the future. Fam. Bus. Rev. 2004, 17, 1–36. [Google Scholar] [CrossRef]

- Chu, W. Family ownership and firm performance: Influence of family management, family control, and firm size. Asia Pac. J. Manag. 2011, 28, 833–851. [Google Scholar] [CrossRef]

- Speckbacher, G.; Wentges, P. The impact of family control. on the use of performance measures in strategic target. setting and incentive compensation: A research note. Manag. Account. Res. 2012, 23, 34–46. [Google Scholar] [CrossRef]

- Liang, X.; Wang, L.; Cui, Z. Chinese private firms and internationalization: effects of family involvement in management and family ownership. Fam. Bus. Rev. 2014, 27, 126–141. [Google Scholar] [CrossRef]

- Helsen, Z.; Lybaert, N.; Steijvers, T. Management control. systems in family firms: A review of the literature and directions for the future. J. Econ. Surv. 2017, 31, 410–435. [Google Scholar] [CrossRef]

- Jensen, M.C.; Meckling, W.H. Theory of the firm: managerial behavior, agency costs and ownership structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Eisenhardt, K.M. Agency theory: An. assessment and review. Acad. Manag. 1989, 14, 57–74. [Google Scholar]

- Baiman, S. Agency research in managerial accounting: A second look. Account. Organ. Soc. 1990, 15, 341–371. [Google Scholar] [CrossRef]

- Bouckva, M. Management accounting and agency theory. Procedia Econ. Financ. 2015, 25, 5–13. [Google Scholar] [CrossRef]

- Lambert, R.A. Agency theory and management accounting. In Handbook of Management Accounting; Chapman, C.S., Hopwood, A.G., Shields, M.D., Eds.; Elsevier: Amsterdam, The Netherlands, 2007; pp. 247–268. [Google Scholar]

- Ronen, J.; Balachandran, K.R. Agency theory: An. approach to incentive problems in management accounting. Asian Rev. Account. 1995, 3, 127–151. [Google Scholar] [CrossRef]

- Brickley, J.A.; Smith, C.W.; Zimmweman, J.L. Management fads and organizational architecture. J. Appl. Corp. Financ. 1997, 10, 23–39. [Google Scholar] [CrossRef]

- Guo, S. Economic transition in china and vietnam: A comparative perspective. Asian Profile 2004, 32, 393–411. [Google Scholar]

- An, D.V.; Duc, L.M. Economic Reforms in China and Vietnam: A Brief. Comparison; Central Institute for Economic Management: Ha Noi, Vietnam, 2007. [Google Scholar]

- Vu, K.M. Economic reform and performance: A comparative study of china and vietnam. China Int. J. 2009, 7, 189–226. [Google Scholar] [CrossRef]

- Flamholtz, E.; Das, T.; Tsui, A. Toward an integrative framework of organizational control. Account. Organ. Soc. 1985, 10, 35–50. [Google Scholar] [CrossRef]

- Anthony, R.; Govindarajan, V. Managemnent Control. Systems, 12th ed.; McGraw Hill: New York, NY, USA, 2007. [Google Scholar]

- Abernethy, M.A.; Chua, W. Field Study of control system "redesign": the impact of institutional process. on strategic choice. Contemp. Account. Res. 1996, 13, 569–606. [Google Scholar] [CrossRef]

- Neely, A.; Grefory, M.; Platts, K. Performance measurement system design: A literature review and research agenda. Int. J. Oper. Prod. Manag. 2005, 25, 1228–1263. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Norton, D.P. The balanced scorecard: Measure that drive performance. Harv. Bus. Rev. 1992, 70, 172–180. [Google Scholar]

- Atkinson, A.A.; Waterhouse, J.H.; Wells, R.B. A Stakeholder Approach to Strategic Performance Measurement. Sloan Manag. Rev. 1997, 38, 25–37. [Google Scholar]

- Bititci, U.S.; Carrie, A.S.; Mcdevitt, L. Integrated performance measurement systems: A development guide. Int. J. Oper. Prod. Manag. 1997, 17, 522–534. [Google Scholar] [CrossRef]

- Atkinson, A.A. Strategic performance measurement and incentive compensation. Eur. Manag. J. 1998, 16, 552–561. [Google Scholar] [CrossRef]

- Gates, S. Aligning Strategic Performance Measures and Results; The Conference Board: New York, NY, USA, 1999. [Google Scholar]

- Ittner, C.D.; Larcker, D.F.; Randall, T. Performance implications of strategic performance measurement in financial services firms. Account. Organ. Soc. 2003, 28, 715–741. [Google Scholar] [CrossRef] [Green Version]

- Maisel, L.S. Performance Measurement Practices Survey Results; American Institute of Certified Public Accountants: Ewing, NJ, USA, 2001. [Google Scholar]

- Johnson, C.C.; Beiman, I. Balanced Scorecard: for State-Owned Enterprises: Driving Performance and Corporate Governance; Asian Development Bank: Mandaluyong, The Philippines, 2007. [Google Scholar]

- Poister, T.H. Measuring Performance in Public and Nonprofit Organizations; Jossey Bass: San Francisco, CA, USA; John Wiley & Sons, Inc.: Hoboken, NJ, USA, 2003. [Google Scholar]

- Sturesson, J.; McIntyre, S.; Jones, N.C. State-Owned Enterprises: Catalysts for Public Value Creation. 2015. Available online: https://www.pwc.com/gx/en/psrc/publications/assets/pwc-state-owned-enterprise-psrc.pdf (accessed on 28 April 2015).

- Neely, A.; Bourne, M.; Kennerley, M. Performance measurement system design: Developing and testing a process-based approach. Int. J. Oper. Prod. Manag. 2000, 20, 1119–1145. [Google Scholar] [CrossRef]

- Caputo, F.; Veltri, S.; Ventureli, A. Sustainability strategy and management control systems in family firms. Evidence from a case study. Sustainability 2017, 9, 977. [Google Scholar] [CrossRef]

- Hosoda, M. Management control. systems and corporate social responsibility: Perspectives from a japanese small company. Corp. Gov. Int. J. Bus. Soc. 2018, 18, 68–80. [Google Scholar] [CrossRef]

- Husgafvel, R.; Pajunen, N.; Virtanen, K.; Paavola, I.L.; Päällysaho, M.; Inkinen, V.; Ekroos, A.; Dahl, O.; Heiskanen, K. Social sustainability performance indicators-experiences from process industry. Int. J. Sustain. Eng. 2015, 8, 14–25. [Google Scholar] [CrossRef]

- Senger, J. Designing a Non-for-Profit Compensation System; John Wiley & Sons, Inc.: Hoboken, NJ, USA, 2005. [Google Scholar]

- Milkovich, G.T.; Newan, J.M.; Gerhart, B. Compensation, 11th ed.; McGraw-Hill Education: New York, NY, USA, 2013. [Google Scholar]

- Booner, S.E.; Sprinkle, G.B. The effects of monetary incentives on effort and task performance: theories, evidence, and a framework for research. Account. Organ. Soc. 2002, 27, 303–345. [Google Scholar] [CrossRef]

- Packwood, E.C. Using variable pay programs to support. organization goals. In The Compensation Handbook-A State-Of-The-Art Guide to Compensation Strategy and Design, 5th ed.; Berger, L.A., Berger, D.R., Eds.; The McGraw-Hill Companies, Inc.: New York, NY, USA, 2008. [Google Scholar]

- Shiels, M.; Young, S.M. Antecedents and consequences of participative budegeting: Evidence on the effects of asymetrical information. J. Manag. Account. Res. 1993, 5, 265–280. [Google Scholar]

- Chow, C.W.; Shields, M.D.; Wu, A. The importance of national culture in the design of and preference for management controls for multi-national operations. Account. Organ. Soc. 1999, 24, 441–461. [Google Scholar] [CrossRef] [Green Version]

- O’Connor, A. Private Equity Compensation and Incentives; O’Connor, A., Private Equity International (PEI), Eds.; Hobbs the Printers: London, UK, 2012; p. 324. [Google Scholar]

- OECD. State-Owned Enterprises in Asia: National Practices for Performance Evaluation and Management; OECD: Paris, France, 2016. [Google Scholar]

- Phan, V.T.; Nguyen, V.T. Problems and prospects of state enterprise reform, 1996–2000. In State-owned Enterprises Reform in Vietnam: Lessons from Asia; Yuen, N.C., Freeman, N.J., Frank, H., Eds.; Institute of Southeast Asian Studies: Singapore, 1996; pp. 3–18. [Google Scholar]

- Nguyen, T.H. Strategic Management in Vietnam State-Owned Enterprises (SOEs). Int. J. Bus. Manag. 2016, 11, 197–204. [Google Scholar]

- Boyne, G.A. Public and private management: What’s the difference? J. Manag. Stud. 2002, 39, 97–122. [Google Scholar] [CrossRef]

- Nguyen, T.V. Managing change in vietnamese state-owned enterprises: What is the best strategy? Hum. Resour. Manag. Rev. 2003, 13, 423–438. [Google Scholar] [CrossRef]

- Painter, M. The politics of economic restructuring in vietnam: The case of state-owned enterprises "reform". Contemp. Southeast. Asia 2003, 25, 20–43. [Google Scholar] [CrossRef]

- Helden, J.V.; Reichard, C. Commonalities and differences in public and private sector performance management practices: A literature review. In Performance Measurement and Management Control: Contemporary Issues (Studies in Managerial and Financial Accounting); Marc, J., Verbeeten, E.F., Sally, K., Widener, S.K., Eds.; Emerald Group Publishing Limited: Bingely, UK, 2016; Volume 31, pp. 309–351. [Google Scholar]

- Nguyen, L.D. Organizational characteristics and employee overall satisfaction: A comparison of state-owned and non state-owned enterprises in vietnam. South. East. Asian J. Manag. 2011, 5, 135–158. [Google Scholar] [CrossRef]

- O’Connor, N.G.; Chow, C.W.; Wu, A. The adoption of western management accounting/controls in china’s state-owned enterprises during economic transition. Account. Organ. Soc. 2004, 29, 349–375. [Google Scholar] [CrossRef]

- Bedford, D.S.; Malmi, T. Configurations of control: An. exploratory analysis. Manag. Account. Res. 2015, 27, 2–26. [Google Scholar] [CrossRef]

- Thomsen, S.; Pedersen, T. Ownership structure and economic performance in the largest European companies. Strateg. Manag. J. 2000, 21, 689–705. [Google Scholar] [CrossRef]

- Lan, M.T. Public management and strategic management in vietnam state-owned enterprises (SOEs). Int. Bus. Res. 2016, 9, 58–65. [Google Scholar] [CrossRef]

- Goldeng, E.; Grünfeld, L.A.; Benito, G.R.G. The performance differential between private and state owned enterprises: The roles of ownership, management and market structure. J. Manag. Stud. 2008, 45, 1244–1273. [Google Scholar] [CrossRef]

- Kornai, J.; Maskin, E.; Roland, G. Understanding the soft budget constraint. J. Econ. Lit. 2003, 41, 1095–1136. [Google Scholar] [CrossRef]

- Kornai, J. The soft budget constraint: An introductory study to volume iv of the life’s work series. Acta Oecon. 2014, 41, 25–79. [Google Scholar] [CrossRef]

- Nhiem, P.T.; Harvie, C.; Hoa, T.V. Vietnam’s Economic Transition: Policies, Issues and Prospects; The ICFAI Univeristy Press: Dehradun, Uttarakhand, India, 2006. [Google Scholar]

- Tran, N.M.; Nonneman, W.; Jorissen, A. Privatization of vietnamese firms and its effects on firms performance. Asian Econ. Financ. Rev. 2015, 5, 202–217. [Google Scholar] [CrossRef]

- Kokko, A.; Sjoholm, F. Some alternative scenarios for the role of the state in Vietnam. Pac. Rev. 2000, 13, 257–277. [Google Scholar] [CrossRef]

- Nartisa, I.; Putans, R.; Muravska, T. Strategic planning and management in public and private sector organizations in Europe: Comparative analysis and opportunities for improvement. Eur. Integr. Stud. 2012, 6, 240–248. [Google Scholar]

- Baldwin, J.N. Public versus private: Not that different, not that consequential. Public Pers. Manag. 1987, 16, 181–193. [Google Scholar] [CrossRef]

- Waller, W.; Chow, C. Self-selection and effort effects of standard-based employment contracts: A framework and some empirical evidence. Account. Rev. 1985, 60, 458–476. [Google Scholar]

- Banker, R.D.; Lee, S.; Potter, G.S. A field study of the impact of a performance-based incentive plan. J. Account. Econ. 1996, 21, 195–226. [Google Scholar] [CrossRef] [Green Version]

- Smith, M. Research Methods in Accounting; SAGE Publications Ltd.: London, UK, 2003. [Google Scholar]

- Dillman, D.A. Mail and Internet Surveys: The Tailored Design Method, 2nd ed.; Wiley, P., Ed.; John Wiley & Sons: Hoboken, NJ, USA, 2007. [Google Scholar]

- Brislin, R.W. Back-translation for cross-cultural research. J. Cross Cult. Psychol. 1970, 1, 185–216. [Google Scholar] [CrossRef]

- Hoque, Z.; James, W. Linking balanced scorecard measures to size and market factors: Impact on organizational performance. J. Manag. Account. Res. 2000, 12, 1–17. [Google Scholar] [CrossRef]

- Chenhall, R.H. Integrative strategic performance measurement systems, strategic alignment of manufacturing, learning and strategic outcomes: An exploratory study. Account. Organ. Soc. 2005, 30, 395–422. [Google Scholar] [CrossRef]

- Chenhall, R.H.; Langfield-Smith, K. The relationship between strategic priorities, management techniques and management accounting: An empirical investigation using a system approach. Account. Organ. Soc. 1998, 23, 243–264. [Google Scholar] [CrossRef]

- Ringle, C.M.; Wende, S.; Becker, J. SmartPLS 3.2.8. 2018. Available online: https://www.smartpls.com (accessed on 14 May 2019).

- Nitzl, C. The use of partial least square structural equation modelling (pls-sem) in management accounting research: directions for future theory development. J. Account. Lit. 2016, 37, 19–35. [Google Scholar] [CrossRef]

- Hair, J.R.; Joseph, F.; Hult, G.T.M.; Ringle, C.; Sarstedt, M. A Primer on Partial Least Squares Structual Equation Modeling (PLS-SEM), 2nd ed.; SAGE Publication: Thousand Oaks, CA, USA, 2013. [Google Scholar]

- Hair, J.F.; Ringle, C.M.; Sarstedt, M. PLS-SEM: Indeed a silver bullet. J. Mark. Theory Pract. 2011, 19, 139–151. [Google Scholar] [CrossRef]

- Hair, J.R.; Joseph, F.; Sarstedt, M.; Ringle, C.M.; Gudergan, S.P. Advanced Issues in Partial Least Squares Equation Modeling; SAGE Publications, Inc.: Thousand Oaks, CA, USA, 2017. [Google Scholar]

- Hoozée, S.; Ngo, Q.H. The impact of managers’ participation in costing system design on their perceived contributions to process improvement. Eur. Account. Rev. 2017, 27, 747–770. [Google Scholar] [CrossRef]

- Parwoll, M.; Wagner, R. The Impact of MissingVvalues on PLS Model Fit. In Challenges at the Interface of Data Analysis, Computer Science, and Optimization; Gaul, W., Geyer-Schulz, A., Schmidt-Thieme, B., Kunze, J., Eds.; Springer: Berlin, Germany, 2012; pp. 537–544. [Google Scholar]

- Podsakoff, P.M.; Mackenzie, S.B.; Podsakoff, N.P. Sources of method bias in social science research and recommendations on how to control it. Annu. Rev. Psychol. 2012, 63, 539–569. [Google Scholar] [CrossRef]

- Harman, H.H. Modern Factor Analysis; The University of Chicago Press: Chicago, IL, USA, 1967. [Google Scholar]

- Hulland, J. Use of partial least squares (PLS) in strategic management research: A review of four recent studies. Strateg. Manag. J. 1999, 20, 195–204. [Google Scholar] [CrossRef]

- Chin, W.W. The partial least squares approach to structural equation modeling. In Modern Methods for Business Research; Marcoulides, G.A., Ed.; Lawrence Erlbaum Associates: Mahwah, NJ, USA, 1998; pp. 295–336. [Google Scholar]

- Fornerll, C.; Larcker, D.F. Structural equation models with unobservable variables and measurement error: algebra and statistics. J. Mark. Res. 1981, 18, 382–388. [Google Scholar] [CrossRef]

- Hesenler, J.; Ringle, C.M.; Sarstedt, M. A new criterion for assessing discriminant validity in variance-based structural equation modeling. J. Acad. Mark. Sci. 2015, 43, 115–135. [Google Scholar]

- Pan, Y.; Jackson, R.T. Ethnic difference in the relationship between acute inflammation and serum ferritin in us adult males. Epidemiol. Infect. 2008, 136, 421–431. [Google Scholar] [CrossRef] [PubMed]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis, 7th ed.; Pearson Education: Harlow, UK, 2014. [Google Scholar]

- Rogerson, P.A. Statistical Methods for Geography; Sage: London, UK, 2001. [Google Scholar]

- Cohen, J. Statistical Power Analysis for the Behavioral Sciences; Lawrence Erlbaum Associates: New York, NY, USA, 1988. [Google Scholar]

- Tenenhaus, M.; Vinzi, V.E.; Chatelin, Y.M.; Lauro, C. PLS path modeling. Comput. Stat. Data 2005, 48, 159–205. [Google Scholar] [CrossRef]

- Dyllick, T.; Hockerts, K. Beyond the business case for corporate sustainability. Bus. Strategy Environ. 2002, 11, 130–141. [Google Scholar] [CrossRef]

- Guo, M.; Hu, Y.; Zhang, Y.; Tian, F. State-Owned Shareholding and CSR: Do Multiple Financing Methods Matter?—Evidence from China. Sustainability 2019, 11, 1292. [Google Scholar] [CrossRef]

- Zhu, Q.; Liu, J.; Lai, K.H. Corporate social responsibility practices and performance improvement among chinese national state-owned enterprises. Int. J. Prod. Econ. 2016, 17, 417–426. [Google Scholar] [CrossRef]

- Yu, Y.; Choi, Y.; Zhang, N. Strategic corporate sustainability performance of chinesestate-owned listed firms: A meta-frontier generalizeddirectional distance function approach. Soc. Sci. J. 2015, 52, 300–310. [Google Scholar] [CrossRef]

- Xu, S.; Liu, D.; Huang, J. Corporate social responsibility, the cost of equity capital and ownership structure: an. analysis of Chinese listed firms. Aust. J. Manag. 2015, 40, 245–276. [Google Scholar] [CrossRef]

- Kuo, L.; Yeh, C.C.; Yu, H.C. Disclosure of corporate social responsibility and environmental management: Evidence from China. Corp. Soc. Responsib. Environ. Manag. 2012, 19, 273–287. [Google Scholar] [CrossRef]

- Van der Stede, W.A.; Young, S.M.; Chen, C.X. Assessing the quality of evidence in empirical management accounting research: The case of survey studies. Account. Organ. Soc. 2005, 30, 655–684. [Google Scholar] [CrossRef]

- DiMaggio, P.J.; Powell, W.W. The iron cage revisited: Instutional isomorphism and collective rationally in organizational fields. Am. Sociol. Rev. 1983, 48, 147–160. [Google Scholar] [CrossRef]

- Yan, A.; Gray, B. Bargaining power, management control., and performance in united states-China joint ventures: A comparative case study. Acad. Manag. J. 1994, 37, 1487–1517. [Google Scholar]

| Panel A: Companies’ Background | |

|---|---|

| Firm age | |

| Mean | 27.53 years |

| Max | 110 years |

| Min | 3 years |

| Assets (million VND) | |

| ≤20 | 0.7% |

| 20–50 | 14.3% |

| 50–100 | 10.7% |

| >100 | 74.3% |

| Firm size (the number of employees) | |

| <50 | 0% |

| 50–100 | 5.7% |

| 100–200 | 27.1% |

| 200–300 | 17.9% |

| >300 | 49.3% |

| Sector | |

| Agriculture, forestry, and fishing | 7.1% |

| Mining and quarrying | 2.9% |

| Manufacturing | 43.6% |

| Electricity, gas, steam, and air conditioning supply | 5.0% |

| Water supply; sewerage, waste management, and remediation activities | 7.9% |

| Construction | 7.1% |

| Wholesale and retail trade; repair of motor vehicles and motorcycles | 3.6% |

| Transportation and storage | 12.1% |

| Accommodation and food service activities | 1.4% |

| Information and communication | 4.3% |

| Real estate activities | 0.7% |

| Administration and support service activities | 3.6% |

| Arts, entertainment, and recreation | 0.7% |

| Has there been a change in ownership since the establishment of the firm? | |

| Yes | 57.9% |

| No | 42.1% |

| Panel B: Respondent position | |

| CEOs | 12.9% |

| Top managers | 12.9% |

| Middle managers | 74.3% |

| SOE PMSs | Non-SOE PMSs | |||||

|---|---|---|---|---|---|---|

| Cronbach’s Alpha | CR | AVE | Cronbach’s Alpha | CR | AVE | |

| Firm age | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| Industry | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| PM_Community | 0.937 | 0.955 | 0.841 | 0.937 | 0.955 | 0.841 |

| PM_Customer | 0.887 | 0.910 | 0.560 | 0.887 | 0.910 | 0.560 |

| PM_Ethical | 0.961 | 0.969 | 0.838 | 0.961 | 0.969 | 0.838 |

| PM_Financial | 0.777 | 0.856 | 0.599 | 0.777 | 0.857 | 0.601 |

| PM_Govern | 0.976 | 0.988 | 0.976 | 0.976 | 0.988 | 0.976 |

| PM_Innov&learning | 0.893 | 0.933 | 0.824 | 0.893 | 0.934 | 0.824 |

| PM_Intern business proc | 0.870 | 0.902 | 0.606 | 0.870 | 0.902 | 0.605 |

| Size | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| State-owned | 1.000 | 1.000 | 1.000 | |||

| Non-state-owned | 1.000 | 1.000 | 1.000 | |||

| Strategy | 0.928 | 0.938 | 0.582 | 0.928 | 0.938 | 0.582 |

| SOE Compensations | Non-SOE Compensations | |||||

|---|---|---|---|---|---|---|

| Cronbach’s Alpha | CR | AVE | Cronbach’s Alpha | CR | AVE | |

| CO_Community | 0.948 | 0.963 | 0.867 | 0.948 | 0.963 | 0.866 |

| CO_Customer | 0.901 | 0.920 | 0.592 | 0.901 | 0.920 | 0.592 |

| CO_Ethical | 0.962 | 0.970 | 0.843 | 0.962 | 0.970 | 0.843 |

| CO_Financial | 0.822 | 0.883 | 0.653 | 0.822 | 0.883 | 0.655 |

| CO_Govern | 0.984 | 0.992 | 0.985 | 0.984 | 0.992 | 0.985 |

| CO_Innov&learning | 0.923 | 0.951 | 0.867 | 0.923 | 0.951 | 0.867 |

| CO_Intern buss proc | 0.902 | 0.925 | 0.672 | 0.902 | 0.924 | 0.671 |

| Firm age | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| Industry | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| Size | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| State-owned | 1.000 | 1.000 | 1.000 | |||

| Non-state-owned | 1.000 | 1.000 | 1.000 | |||

| Strategy | 0.928 | 0.938 | 0.582 | 0.928 | 0.938 | 0.582 |

| Construct | Performance Measurement Systems | Outcome-Based Compensation Systems | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SOEs | Non-SOEs | SOEs | Non-SOEs | |||||||||

| β | p | f2 | B | p | f2 | β | p | f2 | β | p | f2 | |

| Financial | −0.221 | 0.027 | 0.044 | 0.230 | 0.006 | 0.065 | −0.340 | 0.000 | 0.103 | 0.304 | 0.000 | 0.110 |

| Customer | −0.266 | 0.000 | 0.074 | 0.160 | 0.037 | 0.034 | −0.298 | 0.000 | 0.089 | 0.172 | 0.039 | 0.038 |

| Intern buss proc | −0.236 | 0.003 | 0.048 | 0.126 | 0.144 | 0.018 | −0.277 | 0.001 | 0.068 | 0.140 | 0.112 | 0.022 |

| Innov & learning | −0.036 | 0.661 | 0.001 | 0.042 | 0.546 | 0.002 | −0.108 | 0.202 | 0.012 | 0.093 | 0.201 | 0.011 |

| Ethical | −0.194 | 0.039 | 0.031 | −0.067 | 0.430 | 0.005 | −0.221 | 0.018 | 0.041 | −0.039 | 0.664 | 0.002 |

| Community | −0.152 | 0.097 | 0.02 | −0.071 | 0.359 | 0.006 | −0.101 | 0.280 | 0.009 | −0.112 | 0.161 | 0.014 |

| Govern | 0.694 | 0.000 | 0.813 | −0.338 | 0.000 | 0.165 | 0.654 | 0.000 | 0.653 | −0.340 | 0.000 | 0.167 |

| Construct | Performance Measurement Systems | Outcome-Based Compensation Systems | ||||||

|---|---|---|---|---|---|---|---|---|

| State-Owned | Non-State Owned | State-Owned | Non-State Owned | |||||

| R2 | Q2 | R2 | Q2 | R2 | Q2 | R2 | Q2 | |

| Financial | 0.205 | 0.100 | 0.219 | 0.100 | 0.189 | 0.101 | 0.191 | 0.101 |

| Customer | 0.312 | 0.137 | 0.285 | 0.137 | 0.282 | 0.135 | 0.246 | 0.135 |

| Intern buss proc | 0.169 | 0.084 | 0.144 | 0.084 | 0.181 | 0.099 | 0.146 | 0.099 |

| Innov & learning | 0.291 | 0.214 | 0.291 | 0.214 | 0.266 | 0.204 | 0.266 | 0.204 |

| Ethical | 0.111 | 0.068 | 0.088 | 0.068 | 0.141 | 0.095 | 0.108 | 0.095 |

| Community | 0.151 | 0.109 | 0.139 | 0.109 | 0.164 | 0.122 | 0.169 | 0.122 |

| Govern | 0.572 | 0.515 | 0.334 | 0.515 | 0.528 | 0.477 | 0.330 | 0.477 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Luong, T.C.T.; Jorissen, A.; Paeleman, I. Performance Measurement for Sustainability: Does Firm Ownership Matter. Sustainability 2019, 11, 4436. https://doi.org/10.3390/su11164436

Luong TCT, Jorissen A, Paeleman I. Performance Measurement for Sustainability: Does Firm Ownership Matter. Sustainability. 2019; 11(16):4436. https://doi.org/10.3390/su11164436

Chicago/Turabian StyleLuong, Thi Cam Tu, Ann Jorissen, and Ine Paeleman. 2019. "Performance Measurement for Sustainability: Does Firm Ownership Matter" Sustainability 11, no. 16: 4436. https://doi.org/10.3390/su11164436

APA StyleLuong, T. C. T., Jorissen, A., & Paeleman, I. (2019). Performance Measurement for Sustainability: Does Firm Ownership Matter. Sustainability, 11(16), 4436. https://doi.org/10.3390/su11164436