Artificial Intelligence Based Commercial Risk Management Framework for SMEs

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

2. Nature and Implications of Commercial Risk for SMEs and General Definitions: Risk, Risk Assessment and Management

2.1. Uncontrolled Risk in Commercial Processes as One of the Factors Destroying SMEs Competitiveness and SDG Objectives

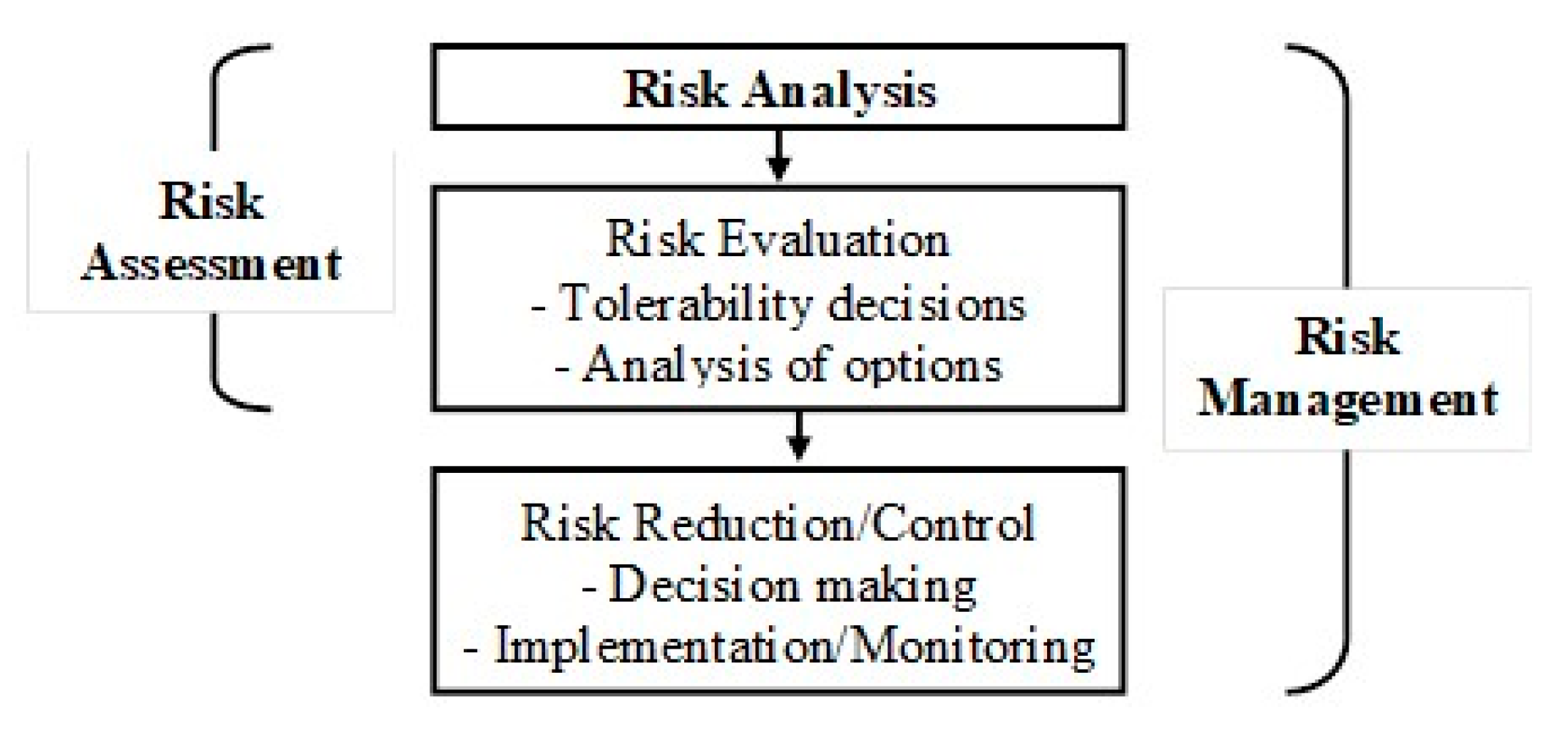

2.2. General Definitions: Risk, Risk Assessment and Management

- What can happen?

- How likely is it that it will happen?

- If it does happen, what are the consequences?

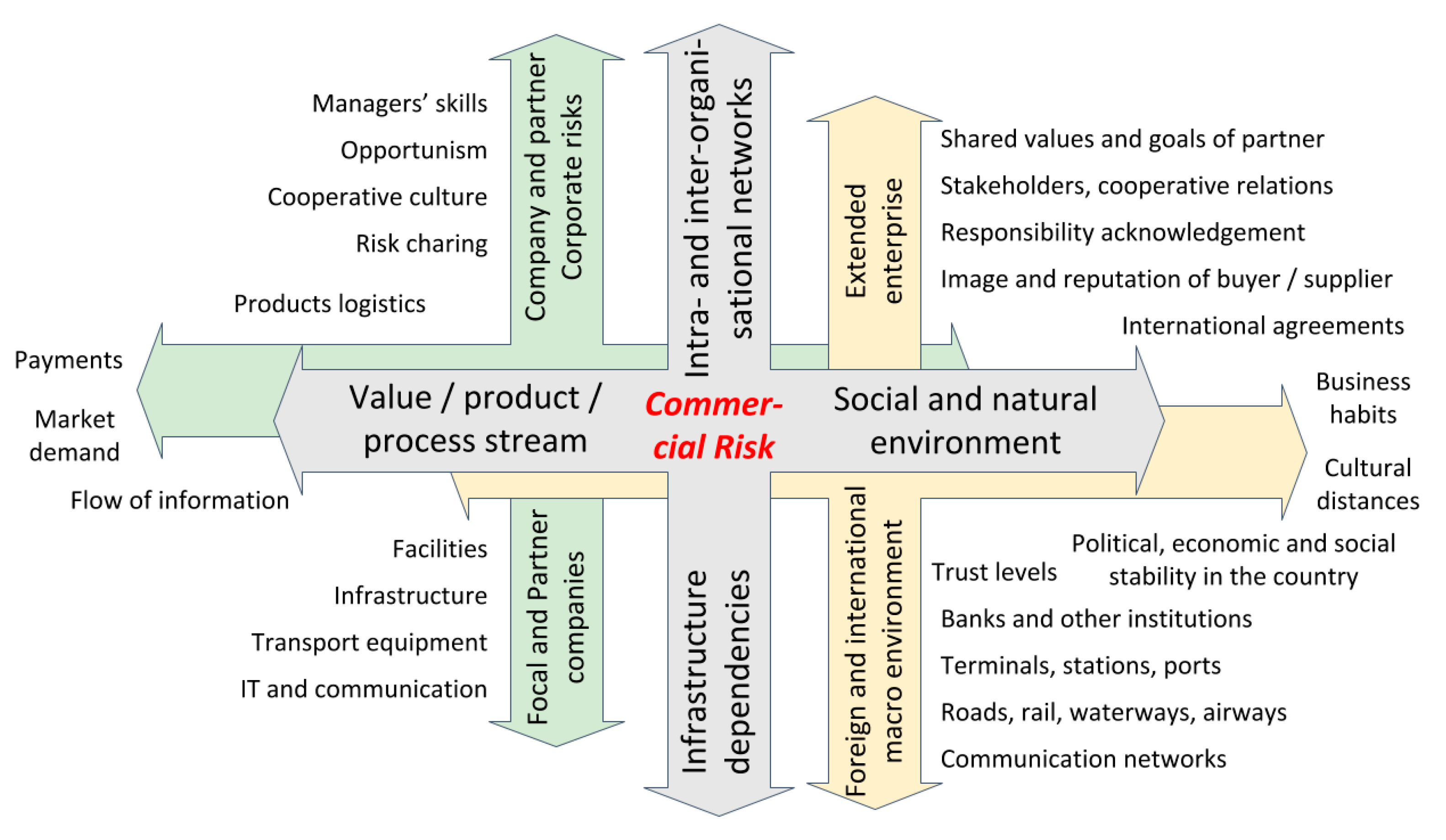

2.3. Ecosystem Perspective Approach to Commercial Risk Management Framework

3. AI Solutions for Commercial Risk Management

3.1. Existing AI Solutions, Their Applicability, and Availability

- -

- First, it is highly desirable for decision-makers to be aware of the full range of the possible risk in order to make informed and balanced decisions.

- -

- Second, point risk estimates frequently are very uncertain because of the accumulation of the effects of rare data, expert judgments or/and various conservative assumptions.

3.2. Risk Assessment Workflow Using Machine Learning

4. Discussion on Recommendations for CRMF and AI Applicability

5. Conclusions

- Commercial risk is a substantial issue for SMEs, affecting their performance and international competitiveness. Insufficient performance does not allow SMEs to achieve SDG defined state of the business. Unassessed and unmanaged commercial risk results in business shortages.

- The given theoretical approach of risk management framework could be extended considering expected implications in policy, further research, and business levels dealing with commercial risk and AI applications.

- Though there are many risk definitions, the commercial risk here is perceived as the assessed probability of an event with negative commercial consequences. The factors of risk, i.e., events having negative commercial consequences, are found in a broad range of analytical levels around commercial processes, including product/process/value stream, commercial infrastructure, intra- and inter-organizational relationships/networks, social and natural environment. The latter analytical level covers those factors that are certain company invariant and define their groups based on sector, home country, etc.

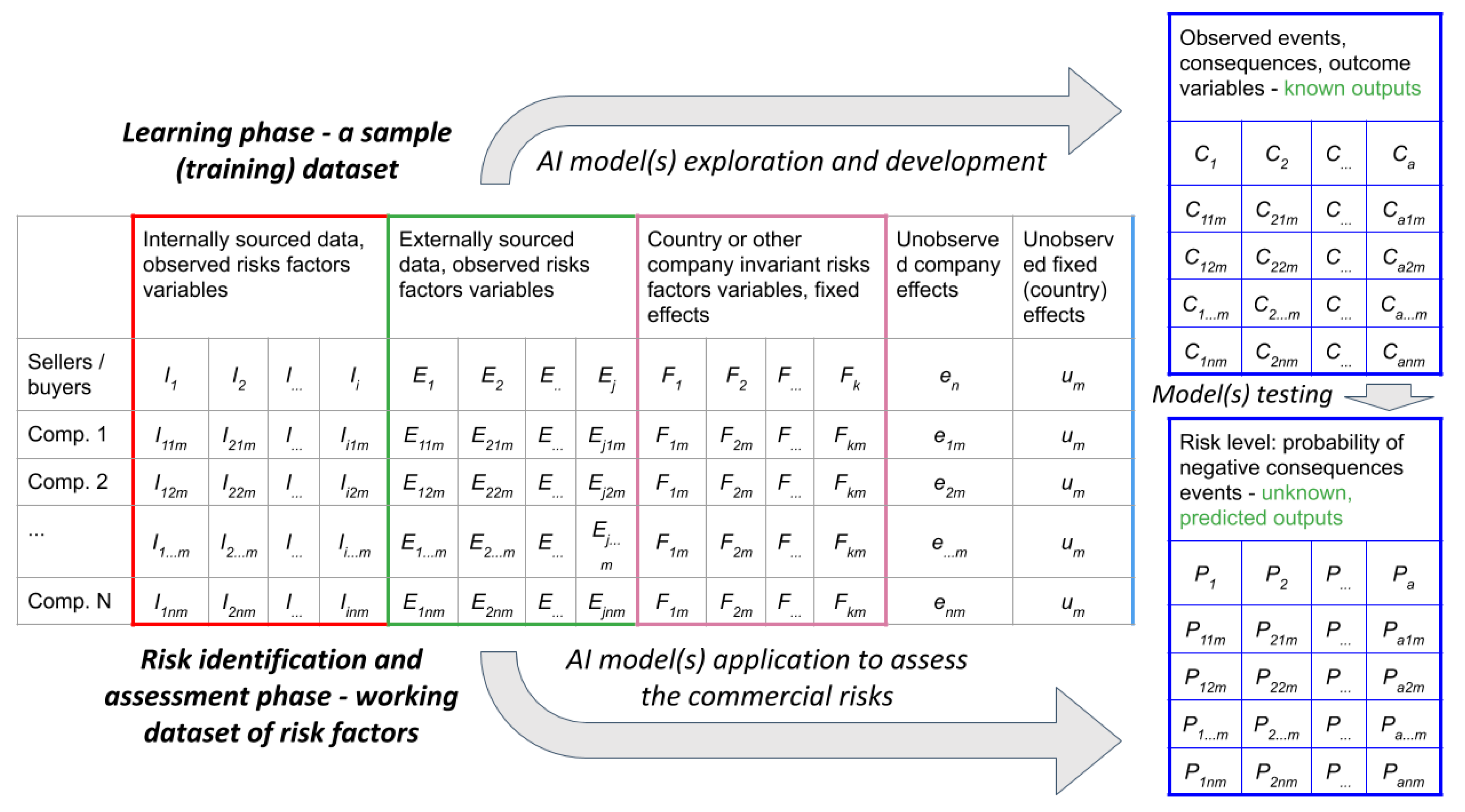

- The calculation of negative event probability is done applying the statistical analysis of selected certain risk event factors. The statistical analysis of selected risk factors is applied to the artificial intelligence development approach, i.e., by learning machines to apply historical patterns for new data evaluation and respective potential risk assessments.

- CRMF is conceptualized as external to the certain business ecosystem-level services provider. SMEs as CRMF’s services users would get risk assessments of potential and/or existent commercial partners—suppliers or buyers. Such services would help SMEs reduce costs for human resource development, data collection, data processing and AI-based risk assessment solution maintenance.

- Observing a variety of financial data, it would be difficult for machine learning techniques to identify the risky case. However, this task becomes easier in the finance domain considering the relevant features.

- Proposed CRMF based SME support solutions development is expected to include data from various sources. Internal business data defining selected risk factors are shared by SMEs themselves. External data, collected and structured (maybe analyzed) by private or public bodies, also defining selected risk factors are associated with particular SMEs. State or industry level indicators, whose values are invariant to the certain SME and define their environmental or other fixed characteristics, are also used to assess the probability of events with negative consequences for the business.

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Stein, P.; Ardic, O.P.; Hommes, M. Closing the Credit Gap for Formal and Informal Micro, Small, and Medium Enterprises; International Finance Corporation: Washington, DC, USA, 2014. [Google Scholar]

- European Commission. Commission Outlines European Approach to Artificial Intelligence. Available online: https://ec.europa.eu/growth/content/commission-outlines-european-approach-artificial-intelligence_en (accessed on 1 May 2019).

- Bughin, J.; Seong, J.; Manyika, J.; Hämäläinen, L.; Windhagen, E.; Hazan, E. Notes from the AI Frontier: Tackling Europe’s Gap in Digital and AI; McKinsey&Company: New York, NY, USA, 2019. [Google Scholar]

- European Commission. Artificial Intelligence for Europe; European Commission: Brussels, Belgium, 2018. [Google Scholar]

- Boobier, T. Advanced Analytics and AI; John Wiley & Sons: Chichester, West Sussex, UK, 2018; ISBN 978-1-119-39030-5. [Google Scholar]

- Brustbauer, J. Enterprise risk management in SMEs: Towards a structural model. Int. Small Bus. J. 2016, 34, 70–85. [Google Scholar] [CrossRef]

- Yang, S.; Ishtiaq, M.; Anwar, M. Enterprise Risk Management Practices and Firm Performance, the Mediating Role of Competitive Advantage and the Moderating Role of Financial Literacy. J. Risk Finan. Manag. 2018, 11, 35. [Google Scholar] [Green Version]

- Gao, L. Long-Term Contracting: The Role of Private Information in Dynamic Supply Risk Management. Prod. Operat. Manag. 2015, 24, 1570–1579. [Google Scholar] [CrossRef]

- Verbano, C.; Venturini, K. Managing Risks in SMEs: A Literature Review and Research Agenda. J. Technol. Manag. Innov. 2013, 8, 186–197. [Google Scholar] [CrossRef]

- Leopoulos, V.N.; Kirytopoulos, K.A.; Malandrakis, C. Risk management for SMEs: Tools to use and how. Prod. Plann. Control 2006, 17, 322–332. [Google Scholar] [CrossRef]

- Bharati, P.; Chaudhury, A. SMEs and Competitiveness: The Role of Information Systems; Social Science Research Network: Rochester, NY, USA, 2015. [Google Scholar]

- Belas, J.; Machacek, J.; Bartos, P.; Hlawiczka, R.; Hudakova, M. Business Risks and the Level of Entrepreneurial Optimism among SME in the Czech and Slovak Republic. JOC 2014, 6, 30–41. [Google Scholar] [CrossRef] [Green Version]

- Morsing, M.; Perrini, F. CSR in SMEs: Do SMEs matter for the CSR agenda? Bus. Ethics Eur. Rev. 2009, 18, 1–6. [Google Scholar] [CrossRef]

- Lawrence, S.R.; Collins, E.; Pavlovich, K.; Arunachalam, M. Sustainability practices of SMEs: The case of NZ. Bus. Strategy Environ. 2006, 15, 242–257. [Google Scholar] [CrossRef]

- Castka, P.; Balzarova, M.A.; Bamber, C.J.; Sharp, J.M. How can SMEs effectively implement the CSR agenda? A UK case study perspective. Corp. Soc. Responsib. Environ. Manag. 2004, 11, 140–149. [Google Scholar] [CrossRef]

- Moore, S.B.; Manring, S.L. Strategy development in small and medium sized enterprises for sustainability and increased value creation. J. Clean. Prod. 2009, 17, 276–282. [Google Scholar] [CrossRef]

- United Nations SDG Accelerator for SMEs. Available online: http://www.sdg-accelerator.org/ (accessed on 23 April 2019).

- Tsai, W.-H.; Chou, W.-C. Selecting management systems for sustainable development in SMEs: A novel hybrid model based on DEMATEL, ANP, and ZOGP. Expert Syst. Appl. 2009, 36, 1444–1458. [Google Scholar] [CrossRef]

- Hillary, R. Environmental management systems and the smaller enterprise. J. Clean. Prod. 2004, 12, 561–569. [Google Scholar] [CrossRef]

- Brammer, S.; Hoejmose, S.; Marchant, K. Environmental Management in SMEs in the UK: Practices, Pressures and Perceived Benefits. Bus. Strategy Environ. 2012, 21, 423–434. [Google Scholar] [CrossRef]

- Biondi, V.; Iraldo, F.; Meredith, S. Achieving sustainability through environmental innovation: The role of SMEs. Int. J. Technol. Manag. 2002, 24, 612–626. [Google Scholar] [CrossRef]

- Zorpas, A. Environmental management systems as sustainable tools in the way of life for the SMEs and VSMEs. Bioresour. Technol. 2010, 101, 1544–1557. [Google Scholar] [CrossRef] [PubMed]

- Kerr, I.R. Leadership strategies for sustainable SME operation. Bus. Strategy Environ. 2006, 15, 30–39. [Google Scholar] [CrossRef]

- Burke, S.; Gaughran, W.F. Developing a framework for sustainability management in engineering SMEs. Robot. Comput.-Integr. Manuf. 2007, 23, 696–703. [Google Scholar] [CrossRef]

- Johnson, M.P. Sustainability Management and Small and Medium-Sized Enterprises: Managers’ Awareness and Implementation of Innovative Tools. Corp. Soc. Responsib. Environ. Manag. 2015, 22, 271–285. [Google Scholar] [CrossRef]

- Johnson, M.P.; Schaltegger, S. Two Decades of Sustainability Management Tools for SMEs: How Far Have We Come? J. Small Bus. Manag. 2016, 54, 481–505. [Google Scholar] [CrossRef]

- Bos-Brouwers, H.E.J. Corporate sustainability and innovation in SMEs: Evidence of themes and activities in practice. Bus. Strategy Environ. 2010, 19, 417–435. [Google Scholar] [CrossRef]

- Klewitz, J.; Hansen, E.G. Sustainability-oriented innovation of SMEs: A systematic review. J. Clean. Prod. 2014, 65, 57–75. [Google Scholar] [CrossRef]

- Halme, M.; Korpela, M. Responsible Innovation Toward Sustainable Development in Small and Medium-Sized Enterprises: A Resource Perspective. Bus. Strategy Environ. 2014, 23, 547–566. [Google Scholar] [CrossRef]

- Martinez-Conesa, I.; Soto-Acosta, P.; Palacios-Manzano, M. Corporate social responsibility and its effect on innovation and firm performance: An empirical research in SMEs. J. Clean. Prod. 2017, 142, 2374–2383. [Google Scholar] [CrossRef]

- Bayarçelik, E.B.; Taşel, F.; Apak, S. A Research on Determining Innovation Factors for SMEs. Procedia—Soc. Behav. Sci. 2014, 150, 202–211. [Google Scholar] [CrossRef] [Green Version]

- Weber, O.; Scholz, R.W.; Michalik, G. Incorporating Sustainability Criteria into Credit Risk Management. Available online: https://onlinelibrary.wiley.com/doi/abs/10.1002/bse.636 (accessed on 30 July 2019).

- OECD Unlocking the Potential of SMEs for the SDGs. Available online: https://oecd-development-matters.org/2017/04/03/unlocking-the-potential-of-smes-for-the-sdgs/ (accessed on 23 April 2019).

- Nunoo, J.; Andoh, F.K. Sustaining Small and Medium Enterprises through Financial Service Utilization: Does Financial Literacy Matter? In Proceedings of the Agricultural and Applied Economics Association (AAEA)—Annual Meeting, Seattle, WA, USA, 2–14 August 2012. [Google Scholar]

- Fatoki, O.; Oni, O. Financial Literacy Studies in South Africa: Current Literature and Research Opportunities. Mediterr. J. Soc. Sci. 2014, 5, 409. [Google Scholar] [CrossRef]

- Eniola, A.A.; Entebang, H. Financial literacy and SME firm performance. Int. J. Res. Stud. Manag. 2016, 5, 31–43. [Google Scholar] [CrossRef]

- Eniola, A.A.; Entebang, H. SME Managers and Financial Literacy. Glob. Bus. Rev. 2017, 18, 559–576. [Google Scholar] [CrossRef]

- Dahmen, P.; Rodriguez, E. Financial Literacy and the Success of Small Businesses: An Observation from a Small Business Development Center. Numeracy 2014, 7, 3. [Google Scholar] [CrossRef] [Green Version]

- Tauringana, V.; Korutaro Nkundabanyanga, S.; Kasozi, D.; Nalukenge, I. Lending terms, financial literacy and formal credit accessibility. Int J. Soc. Econ. 2014, 41, 342–361. [Google Scholar]

- Joo, S.-H.; Grable, J.E. Improving Employee Productivity: The Role of Financial Counseling and Education. J. Employ. Couns. 2000, 37, 2–15. [Google Scholar] [CrossRef]

- Drexler, A.; Fischer, G.; Schoar, A. Keeping It Simple: Financial Literacy and Rules of Thumb. Am. Econ. J. Appl. Econ. 2014, 6, 1–31. [Google Scholar] [CrossRef] [Green Version]

- Bayrakdaroğlu, A.; Şan, F.B. Financial Literacy Training as a Strategic Management Tool among Small—Medium Sized Businesses Operating in Turkey. Procedia—Soc. Behav. Sci. 2014, 150, 148–155. [Google Scholar] [CrossRef]

- Gibb, A.A. SME Policy, Academic Research and the Growth of Ignorance, Mythical Concepts, Myths, Assumptions, Rituals and Confusions. Int. Small Bus. J. 2000, 18, 13–35. [Google Scholar] [CrossRef]

- SDG Compass-A Guide for Business Action to Advance the Sustainable Development Goals. Available online: https://sdgcompass.org/ (accessed on 31 July 2019).

- Verboven, H.; Vanherck, L. Sustainability management of SMEs and the UN Sustainable Development Goals. uwf 2016, 24, 165–178. [Google Scholar] [CrossRef]

- Aven, T. On how to define, understand and describe risk. Reliab. Eng. Sys. Saf. 2010, 95, 623–631. [Google Scholar] [CrossRef]

- ISO 31000 Risk Management. Available online: http://www.iso.org/cms/render/live/en/sites/isoorg/home/standards/popular-standards/iso-31000-risk-management.html (accessed on 16 June 2019).

- Kaplan, S.; Garrick, B.J. On the Quantitative Definition of Risk. Risk Anal. 1981, 1, 11–27. [Google Scholar] [CrossRef]

- Haimes, Y.Y. On the Complex Definition of Risk: A Systems-Based Approach. Risk Anal. 2009, 29, 1647–1654. [Google Scholar] [CrossRef] [PubMed]

- ISO Guide 73:2009. Available online: http://www.iso.org/cms/render/live/en/sites/isoorg/contents/data/standard/04/46/44651.html (accessed on 16 June 2019).

- Risk Management. Available online: https://www.iaea.org/publications/6201/risk-management-a-tool-for-improving-nuclear-power-plant-performance (accessed on 17 June 2019).

- Lockamy, A. Benchmarking supplier risks using Bayesian networks. Benchmarking 2011, 18, 409–427. [Google Scholar] [CrossRef]

- Heckmann, I.; Comes, T.; Nickel, S. A critical review on supply chain risk—Definition, measure and modeling. Omega 2015, 52, 119–132. [Google Scholar] [CrossRef]

- Schwab, L.; Gold, S.; Reiner, G. Exploring financial sustainability of SMEs during periods of production growth: A simulation study. Int. J. Prod. Econ. 2019, 212, 8–18. [Google Scholar] [CrossRef]

- Gerasimova, E.B.; Redin, D.V. Analyzing and Managing Financial Sustainability of the Company in Turbulent Environment. Mediterr. J. Soc. Sci. 2015, 6, 138. [Google Scholar] [CrossRef]

- Peck, H. Drivers of supply chain vulnerability: An integrated framework. Int. J. Phys. Dist. Log. Manag. 2005, 35, 210–232. [Google Scholar] [CrossRef]

- Banks, E.; Dunn, R. Practical Risk Management: An Executive Guide to Avoiding Surprises and Losses, 1st ed.; Wiley: Chichester, UK, 2007. [Google Scholar]

- Pilinkienė, V.; Mačiulis, P. Comparison of Different Ecosystem Analogies: The Main Economic Determinants and Levels of Impact. Procedia—Soc. Behav. Sci. 2014, 156, 365–370. [Google Scholar] [CrossRef] [Green Version]

- Moore, J.F. Predators and prey: A new ecology of competition. Harvard Bus. Rev. 1999, 71, 75–86. [Google Scholar]

- Fan, H.; Li, G.; Sun, H.; Cheng, T.C.E. An information processing perspective on supply chain risk management: Antecedents, mechanism, and consequences. Int. J. Prod. Econ. 2017, 185, 63–75. [Google Scholar] [CrossRef]

- Yaprak, A.; Yosun, T.; Cetindamar, D. The influence of firm-specific and country-specific advantages in the internationalization of emerging market firms: Evidence from Turkey. Int. Bus. Rev. 2018, 27, 198–207. [Google Scholar] [CrossRef]

- Bhaumik, S.K.; Driffield, N.; Zhou, Y. Country specific advantage, firm specific advantage and multinationality—Sources of competitive advantage in emerging markets: Evidence from the electronics industry in China. Int. Bus. Rev. 2016, 25, 165–176. [Google Scholar] [CrossRef]

- Zhu, Y.; Xie, C.; Sun, B.; Wang, G.-J.; Yan, X.-G. Predicting China’s SME Credit Risk in Supply Chain Financing by Logistic Regression, Artificial Neural Network and Hybrid Models. Sustainability 2016, 8, 433. [Google Scholar] [CrossRef]

- López-Robles, J.R.; Otegi-Olaso, J.R.; Porto Gómez, I.; Cobo, M.J. 30 years of intelligence models in management and business: A bibliometric review. Int. J. Inf. Manag. 2019, 48, 22–38. [Google Scholar] [CrossRef]

- Li, K.; Niskanen, J.; Kolehmainen, M.; Niskanen, M. Financial innovation: Credit default hybrid model for SME lending. Expert Syst. Appl. 2016, 61, 343–355. [Google Scholar] [CrossRef]

- Zhang, Q.; Wang, J.; Lu, A.; Wang, S.; Ma, J. An improved SMO algorithm for financial credit risk assessment—Evidence from China’s banking. Neurocomputing 2018, 272, 314–325. [Google Scholar] [CrossRef]

- Aziz, S.; Dowling, M. Machine Learning and AI for Risk Management. In Disrupting Finance: FinTech and Strategy in the 21st Century; Lynn, T., Mooney, J.G., Rosati, P., Cummins, M., Eds.; Springer International Publishing: Cham, Switzerland, 2019; pp. 33–50. ISBN 978-3-030-02330-0. [Google Scholar]

- Kungas, P. Business Credit Scoring Moves towards Big Data Era. Available online: https://www.linkedin.com/pulse/business-credit-scoring-verge-big-data-peep-k%C3%BCngas/ (accessed on 24 April 2019).

- Scoriff Scoriff. Available online: https://scoriff.co.uk/about/ (accessed on 25 April 2019).

- Abrahamsson, M. Uncertainty in Quantitative Risk Analysis—Characterisation and Methods of Treatment; Lunds tekniska högskola, Lunds universitet: Lund, Brandteknik, 2002; p. 88. ISSN 1402-3504. [Google Scholar]

- IEC 31010:2019 |IEC Webstore. Available online: https://webstore.iec.ch/publication/59809 (accessed on 17 June 2019).

- Hendershot, D.C. Risk guidelines as a risk management tool. Process. Saf. Prog. 1996, 15, 213–218. [Google Scholar] [CrossRef]

- Soffer, T.; Cohen, A. Privacy Perception of Adolescents in a Digital World. Bull. Sci. Technol. Soc. 2014, 34, 145–158. [Google Scholar] [CrossRef]

- Hyndman, R.J.; Athanasopoulos, G. Forecasting: Principles and Practice, 2nd ed.; OTexts: Heathmont, Victoria, Australia, 2018; ISBN 978-0-9875071-1-2. [Google Scholar]

- Lombardía, M.J.; López-Vizcaíno, E.; Rueda, C. Mixed generalized Akaike information criterion for small area models. J. R. Stat. Soc. Ser. Stat. Soc. 2017, 180, 1229–1252. [Google Scholar] [CrossRef]

- World Economic Forum. WEF_Future of Jobs_2018. 2018. Available online: http://www3.weforum.org/docs/WEF_Future_of_Jobs_2018.pdf (accessed on 15 June 2019).

- European Commission. Digital Opportunity Traineeships: Boosting Digital Skills on the Job. Available online: https://ec.europa.eu/digital-single-market/en/digital-opportunity-traineeships-boosting-digital-skills-job (accessed on 15 June 2019).

- European Commission. The Digital Skills and Jobs Coalition. Available online: https://ec.europa.eu/digital-single-market/en/digital-skills-jobs-coalition (accessed on 15 June 2019).

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Žigienė, G.; Rybakovas, E.; Alzbutas, R. Artificial Intelligence Based Commercial Risk Management Framework for SMEs. Sustainability 2019, 11, 4501. https://doi.org/10.3390/su11164501

Žigienė G, Rybakovas E, Alzbutas R. Artificial Intelligence Based Commercial Risk Management Framework for SMEs. Sustainability. 2019; 11(16):4501. https://doi.org/10.3390/su11164501

Chicago/Turabian StyleŽigienė, Gerda, Egidijus Rybakovas, and Robertas Alzbutas. 2019. "Artificial Intelligence Based Commercial Risk Management Framework for SMEs" Sustainability 11, no. 16: 4501. https://doi.org/10.3390/su11164501

APA StyleŽigienė, G., Rybakovas, E., & Alzbutas, R. (2019). Artificial Intelligence Based Commercial Risk Management Framework for SMEs. Sustainability, 11(16), 4501. https://doi.org/10.3390/su11164501