The Mediating Role of Business Strategies between Management Control Systems Package and Firms Stability: Evidence from SMEs in Malaysia

Abstract

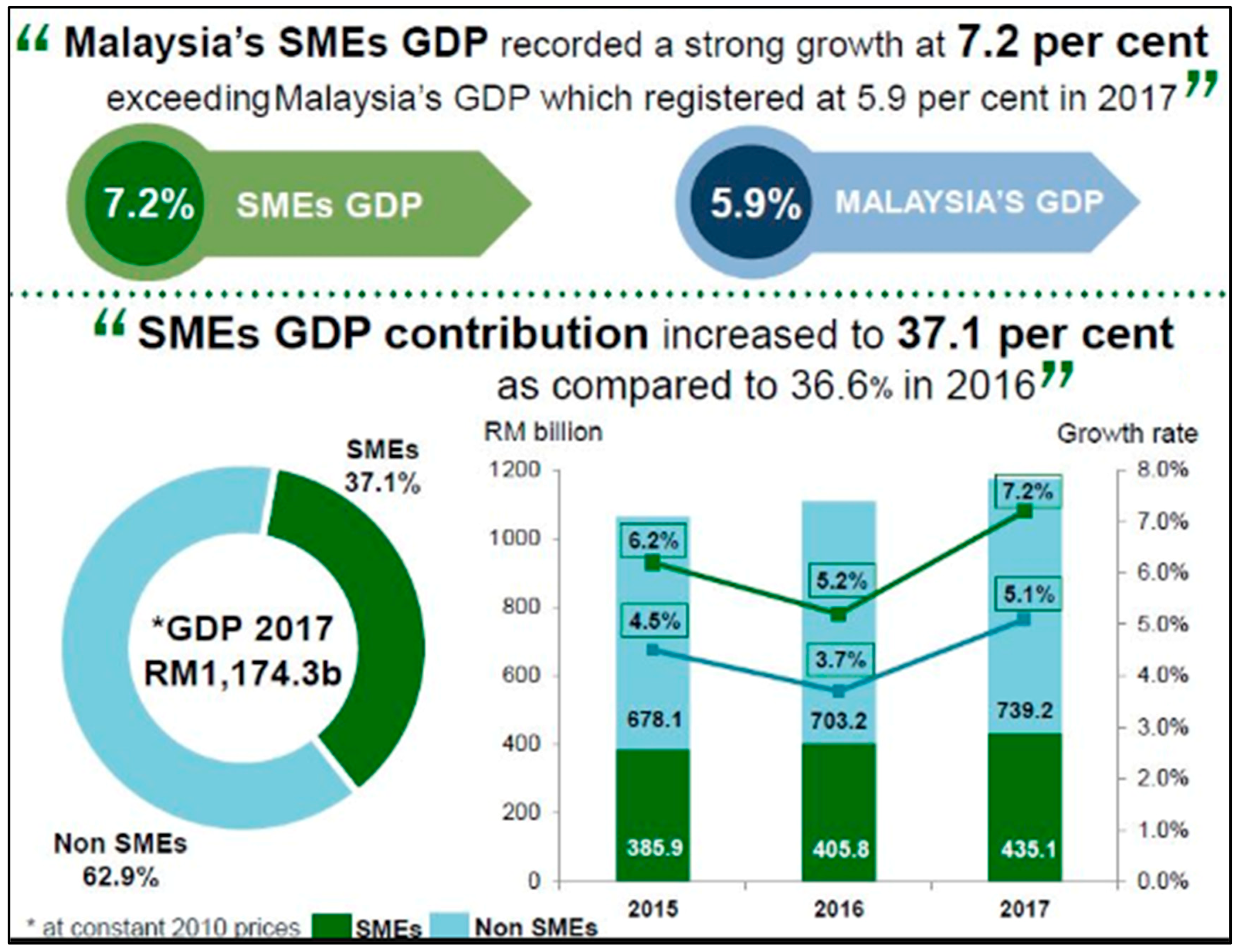

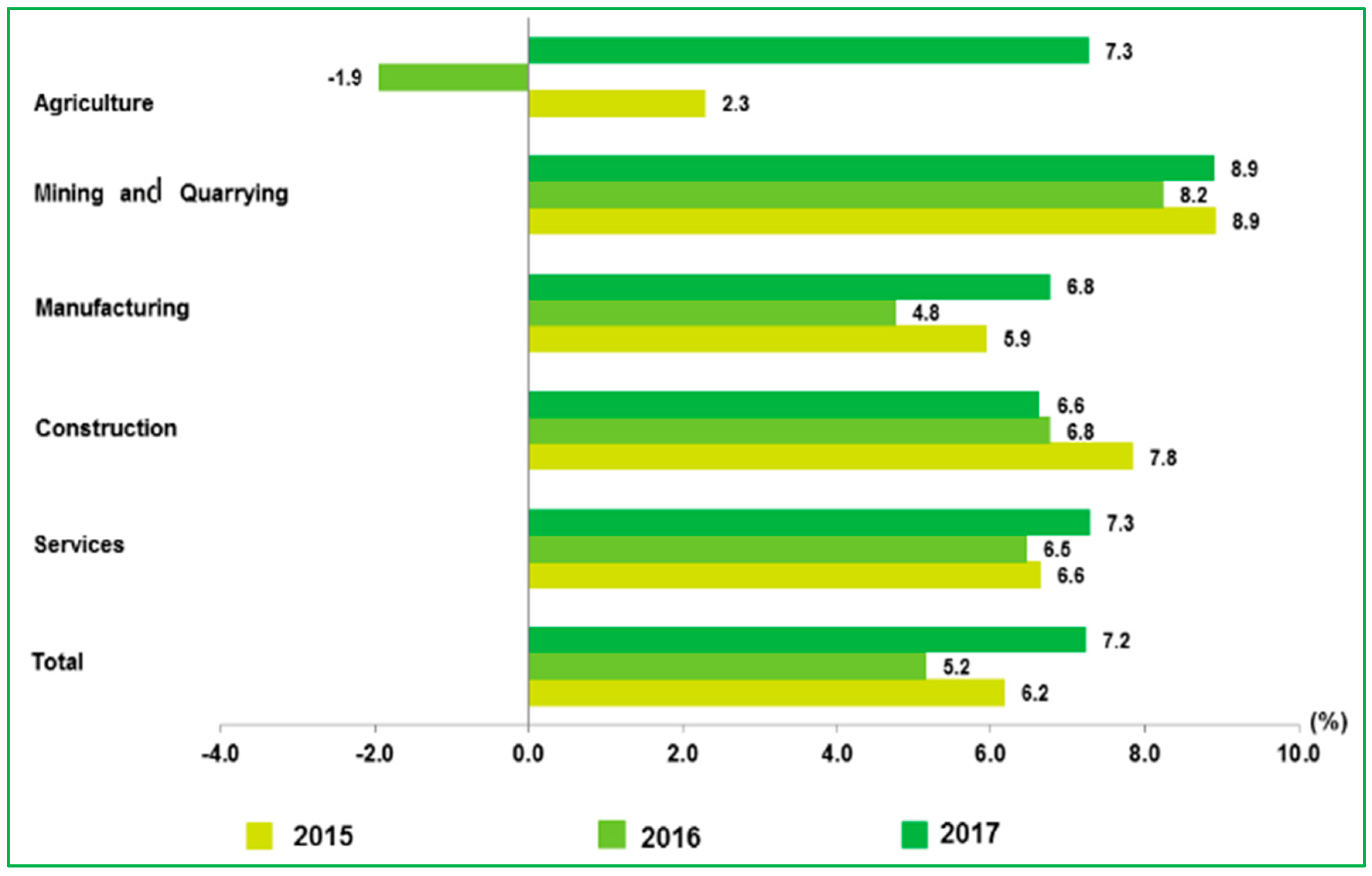

:1. Introduction

2. Literature Review and Hypothesis Development

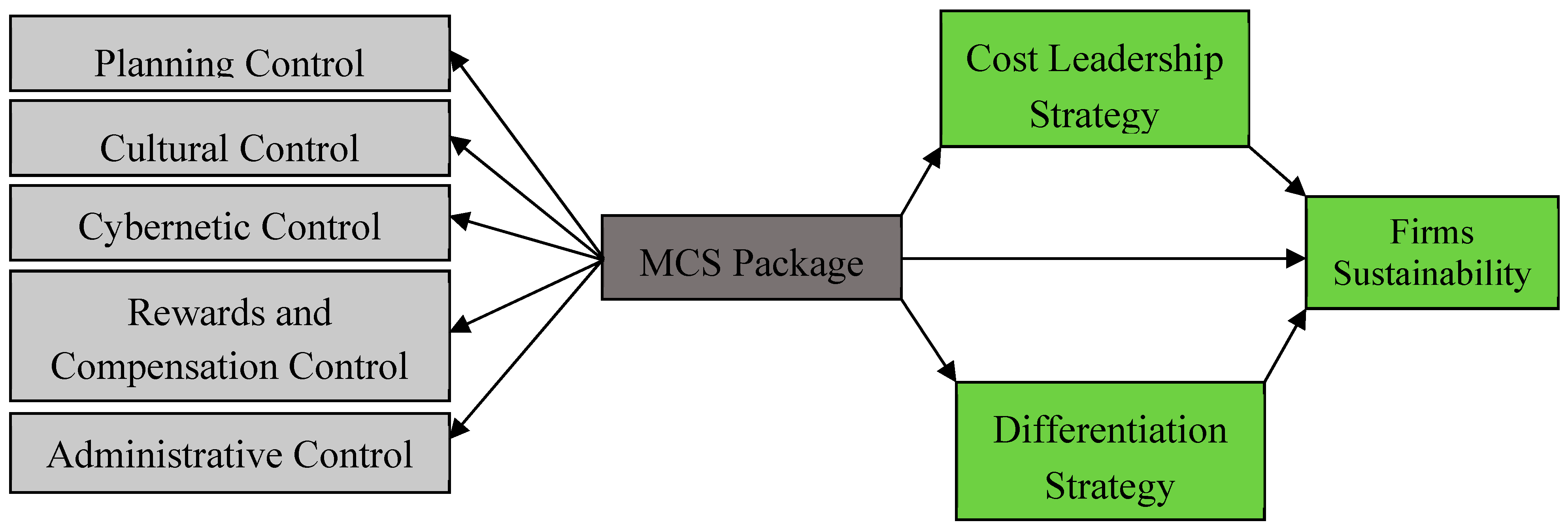

2.1. MCS as a Package (MCSP)

2.2. Business Strategies

2.3. MCS Package, Business Strategies, and Firm Sustainability

3. Methodology

3.1. Research Questionnaire

3.2. Population and Sampling

3.3. Sample Size

3.4. Statistical Analysis Results

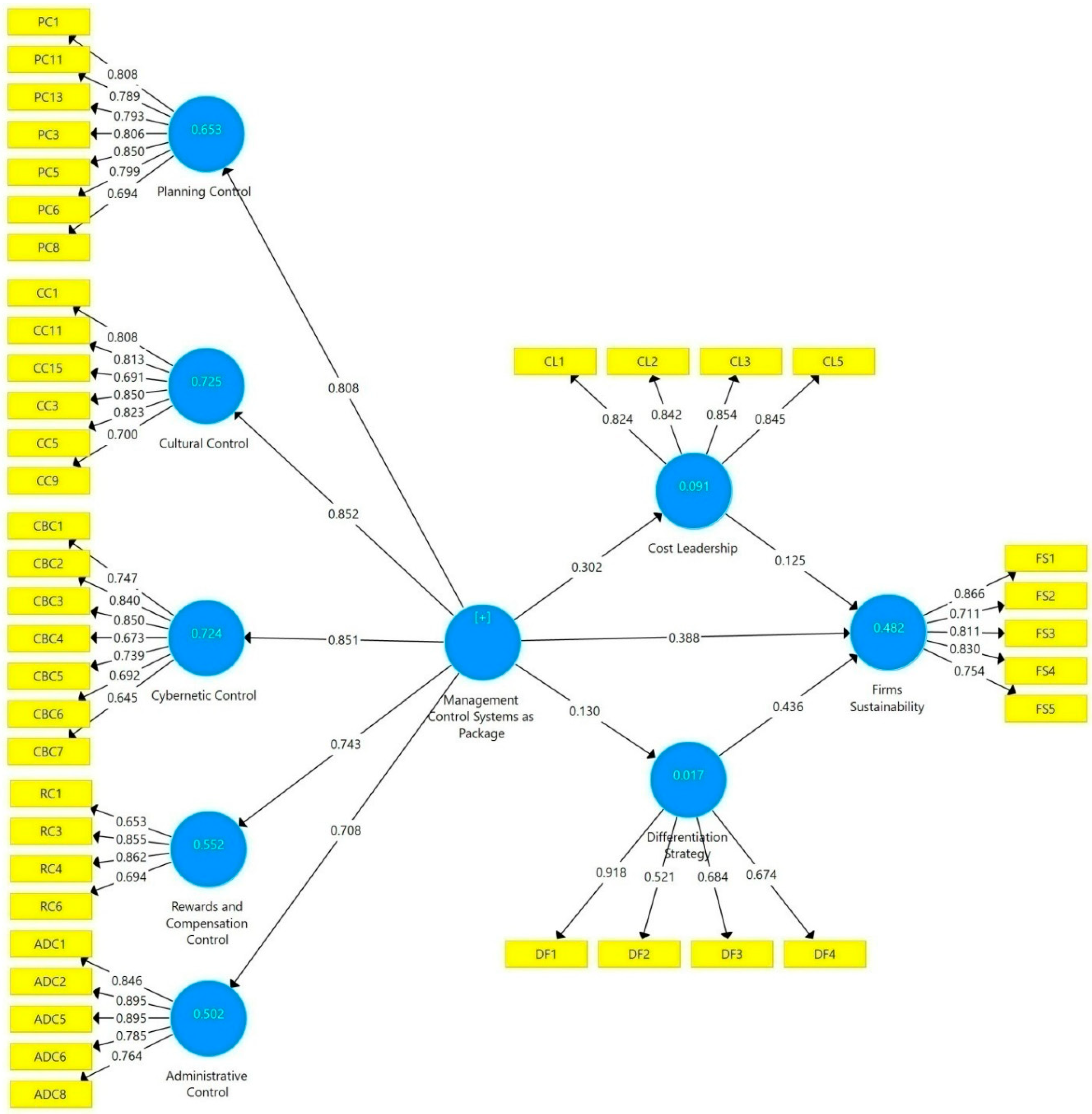

3.4.1. Measurement Model (Outer Model)

Convergent Validity

Discriminant Validity

3.4.2. The Structural Model and Hypotheses Testing

3.5. Mediation Analysis (Indirect Relationship)

3.6. The Predictive Relevance of the Theoretical Model

4. Discussion

5. Conclusions

5.1. Theoretical Contribution

5.2. Practical Contribution

6. Future Directions

Author Contributions

Funding

Conflicts of Interest

References

- Heinicke, A. Performance measurement systems in small and medium-sized enterprises and family firms: A systematic literature review. J. Manag. Control 2018, 28, 457–502. [Google Scholar] [CrossRef]

- Nasir, W.M.N.b.W.M.; Mamun, A.A.; Breen, J. Strategic Orientation and Performance of SMEs in Malaysia. SAGE Open 2017, 7, 2158244017712768. [Google Scholar] [CrossRef]

- SMEinfo. Here’s Why SME Matters in Malaysia. 2018. Available online: https://smeinfo.com.my/profile-of-smes (accessed on 23 August 2018).

- Chenhall, R.H.; Langfield-Smith, K. Performance measurement and reward systems, trust, and strategic change. J. Manag. Account. Res. 2003, 15, 117–143. [Google Scholar] [CrossRef]

- Lavia López, O.; Hiebl, M.R. Management accounting in small and medium-sized enterprises: Current knowledge and avenues for further research. J. Manag. Account. Res. 2015, 27, 81–119. [Google Scholar] [CrossRef]

- Garengo, P.; Biazzo, S.; Bititci, U.S. Performance measurement systems in SMEs: A review for a research agenda. Int. J. Manag. Rev. 2005, 7, 25–47. [Google Scholar] [CrossRef] [Green Version]

- Pešalj, B.; Pavlov, A.; Micheli, P. The use of management control and performance measurement systems in SMEs: A levers of control perspective. Int. J. Oper. Prod. Manag. 2018, 11, 2169–2191. [Google Scholar] [CrossRef]

- Malagueño, R.; Lopez-Valeiras, E.; Gomez-Conde, J. Balanced scorecard in SMEs: Effects on innovation and financial performance. Small Bus. Econ. 2018, 51, 221–244. [Google Scholar] [CrossRef]

- Cooper, D.J.; Ezzamel, M.; Qu, S.Q. Popularizing a management accounting idea: The case of the balanced scorecard. Contemp. Account. Res. 2017, 34, 991–1025. [Google Scholar] [CrossRef]

- Massaro, M.; Moro, A.; Aschauer, E.; Fink, M. Trust, control and knowledge transfer in small business networks. Rev. Manag. Sci. 2017, 13, 1–35. [Google Scholar] [CrossRef]

- Gschwantner, S.; Hiebl, M.R. Management control systems and organizational ambidexterity. J. Manag. Control 2016, 27, 371–404. [Google Scholar] [CrossRef] [Green Version]

- Chalmeta, R.; Palomero, S.; Matilla, M. Methodology to develop a performance measurement system in small and medium-sized enterprises. Int. J. Comput. Integr. Manuf. 2012, 25, 716–740. [Google Scholar] [CrossRef]

- Taticchi, P.; Balachandran, K.; Tonelli, F. Performance measurement and management systems: State of the art, guidelines for design and challenges. Meas. Bus. Excell. 2012, 16, 41–54. [Google Scholar] [CrossRef]

- Akroyd, C.; Maguire, W. The roles of management control in a product development setting. Qual. Res. Account. Manag. 2011, 8, 212–237. [Google Scholar] [CrossRef]

- Tsamenyi, M.; Sahadev, S.; Qiao, Z.S. The relationship between business strategy, management control systems and performance: Evidence from China. Adv. Account. 2011, 27, 193–203. [Google Scholar] [CrossRef]

- Ussahawanitchakit, P. Management Control Systems and Firm Sustainability: Evidence from textile and apparel businesses in Thailand. Asian Acad. Manag. J. 2017, 22, 185–208. [Google Scholar] [CrossRef]

- Henri, J.F. Management control systems and strategy: A resource-based perspective. Account. Organ. Soc. 2006, 31, 529–558. [Google Scholar] [CrossRef]

- Goyal, P.; Rahman, Z.; Kazmi, A. Corporate sustainability performance and firm performance research: Literature review and future research agenda. Manag. Decis. 2013, 51, 361–379. [Google Scholar] [CrossRef]

- Rehman, S.U.; Mohamed, R.; Ayoup, H. The mediating role of organizational capabilities between organizational performance and its determinants. J. Glob. Entrep. Res. 2019, 9, 30. [Google Scholar] [CrossRef]

- Malmi, T.; Brown, D.A. Management control systems as a package—Opportunities, challenges and research directions. Manag. Account. Res. 2008, 19, 287–300. [Google Scholar] [CrossRef]

- Statista. Direct Contribution of Travel and Tourism to GDP in Selected Asia Pacific Countries in 2017; Statista: Hamburg, Germany, 2018. [Google Scholar]

- Hussain, H.I.; Grabara, J.; Razimi, M.S.A.; Sharif, S.P. Sustainability of Leverage Levels in Response to Shocks in Equity Prices: Islamic Finance as a Socially Responsible Investment. Sustainability 2019, 11, 3260. [Google Scholar] [CrossRef]

- Susanto, F.; Arafah, W.; Husin, Z. Ambidextrous sustainability and manufacturing industry performance: The role of potential non-economic benefits as mediation pathways. Pol. J. Manag. Stud. 2017, 16, 278–289. [Google Scholar] [CrossRef]

- Hussain, H.I.; Salem, M.A.; Rashid, A.Z.A.; Kamarudin, F. Environmental Impact of Sectoral Energy Consumption on Economic Growth in Malaysia: Evidence from ARDL Bound. Testing Approach. Ekoloji 2019, 28, 199–210. [Google Scholar]

- Salem, M.A.; Shawtari, F.; Shamsudin, M.F.; Hussain, H.B.I. The consequences of integrating stakeholder engagement in sustainable development (environmental perspectives). Sustain. Dev. 2018, 26, 255–268. [Google Scholar] [CrossRef]

- Rehman, S.-U.; Mohamed, R.; Ayoup, H. Management Control System (MCS) as a Package Elements Influence on Organizational Performance in the Pakistani context Pakistan. J. Humanit. Soc. Sci. 2018, 6, 280–295. [Google Scholar]

- Rehman, S.-U.; Mohamed, R.; Ayoup, H. Cybernetic Controls, and Rewards and Compensation Controls Influence on Organizational Performance. Mediating Role of Organizational Capabilities in Pakistan. Int. J. Acad. Manag. Sci. Res. (IJAMSR) 2018, 2, 1–10. [Google Scholar]

- Meyer, N.; Molefe, K.; De Jongh, J. Managerial challenges within SMEs: The case of a developing region. Pol. J. Manag. Stud. 2018, 18, 185–196. [Google Scholar] [CrossRef]

- Barney, J.B.; Arikan, A.M. The resource-based view: Origins and implications. Handb. Strateg. Manag. 2001, 10, 124188. [Google Scholar]

- Sirmon, D.G.; Hitt, M.A.; Ireland, R.D.; Gilbert, B.A. Resource orchestration to create competitive advantage: Breadth, depth, and life cycle effects. J. Manag. 2011, 37, 1390–1412. [Google Scholar] [CrossRef]

- Haseeb, M.; Hussain, H.I.; Ślusarczyk, B.; Jermsittiparsert, K. Industry 4.0: A solution towards technology challenges of sustainable business performance. Soc. Sci. 2019, 8, 154. [Google Scholar] [CrossRef]

- Maelah, R.; Yadzid, N.H.N. Budgetary control, corporate culture and performance of small and medium enterprises (SMEs) in Malaysia. Int. J. Glob. Small Bus. 2018, 10, 77–99. [Google Scholar] [CrossRef]

- Tehseen, S.; Qureshi, Z.H.; Ramayah, T. Impact of network competence on firm’s performances among Chinese and Indian entrepreneurs: A multigroup analysis. Int. J. Entrep. 2018, 1–14. [Google Scholar]

- Bianchi, C.; Glavas, C.; Mathews, S. SME international performance in Latin America: The role of entrepreneurial and technological capabilities. J. Small Bus. Enterp. Dev. 2017, 24, 176–195. [Google Scholar] [CrossRef]

- Gray, D.; Jones, K.F. Using organisational development and learning methods to develop resilience for sustainable futures with SMEs and micro businesses: The case of the “business alliance”. J. Small Bus. Enterp. Dev. 2016, 23, 474–494. [Google Scholar] [CrossRef]

- Azarloo, M.; Eshghiaraghi, M.; Salehi, S.Y.; Habibpoor, V.; Jahangiri, M. Factors Affecting Technological Entrepreneurship and Innovation in Small and Medium Enterprises (SMEs) and its Role in Countries’ Economic Development. EDII Inst. Repos. 2017. [Google Scholar]

- Ngoma, M.; Ernest, A.; Nangoli, S.; Christopher, K. Internationalisation of SMEs: Does entrepreneurial orientation matter? World J. Entrep. Manag. Sustain. Dev. 2017, 13, 96–113. [Google Scholar] [CrossRef]

- Mahmood, R.; Hanafi, N. Learning orientation and business performance of women-owned SMEs in Malaysia: The mediating effect of competitive advantage. Br. J. Arts Soc. Sci. 2013, 11, 150–161. [Google Scholar]

- Welbourne, T.M.; Pardo-del-Val, M. Relational capital: Strategic advantage for small and medium-size enterprises (SMEs) through negotiation and collaboration. Group Decis. Negot. 2009, 18, 483–497. [Google Scholar] [CrossRef]

- Appiah Fening, F.; Pesakovic, G.; Amaria, P. Relationship between quality management practices and the performance of small and medium size enterprises (SMEs) in Ghana. Int. J. Qual. Reliab. Manag. 2008, 25, 694–708. [Google Scholar] [CrossRef]

- Madden, K.; Scaife, W.; Crissman, K. How and why small to medium size enterprises (SMEs) engage with their communities: An. Australian study. Int. J. Nonprofit Volunt. Sect. Mark. 2006, 11, 49–60. [Google Scholar] [CrossRef]

- Oly Ndubisi, N.; Iftikhar, K. Relationship between entrepreneurship, innovation and performance: Comparing small and medium-size enterprises. J. Res. Mark. Entrep. 2012, 14, 214–236. [Google Scholar] [CrossRef]

- North, D.; Smallbone, D. Innovative activity in SMEs and rural economic development: Some evidence from England. Eur. Plan. Stud. 2000, 8, 87–106. [Google Scholar] [CrossRef]

- Dini, P.; Lombardo, G.; Mansell, R.; Razavi, A.R.; Moschoyiannis, S.; Krause, P.; Nicolai, A.; Rivera León, L. Beyond interoperability to digital ecosystems: Regional innovation and socio-economic development led by SMEs. Int. J. Technol. Learn. Innov. Dev. 2008, 1, 410–426. [Google Scholar] [CrossRef]

- Syed, A.A.S.G.; Ahmadani, M.M.; Shaikh, N.; Shaikh, F.M. Impact analysis of SMEs sector in economic development of Pakistan: A case of Sindh. J. Asian Bus. Strategy 2012, 2, 44–53. [Google Scholar]

- Smallbone, D.; Welter, F.; Isakova, N.; Slonimski, A. The contribution of small and medium enterprises to economic development in Ukraine and Belarus: Some policy perspectives. MOST: Econ. Policy Transit. Econ. 2001, 11, 253–273. [Google Scholar] [CrossRef]

- Armeanu, D.; Istudor, N.; Lache, L. The role of SMEs in assessing the contribution of entrepreneurship to GDP in the Romanian business environment. Amfiteatru Econ. J. 2015, 17, 195–211. [Google Scholar]

- Abdullah, N.H.; Shamsuddin, A.; Wahab, E.; Hamid, N.A. Preliminary qualitative findings on technology adoption of Malaysian SMEs. In Proceedings of the 2012 IEEE Colloquium on Humanities, Science and Engineering (CHUSER), Kota Kinabalu, Malaysia, 3–4 December 2012. [Google Scholar]

- Tan, K.; Eze, U.; Chong, S. Factors influencing internet-based information and communication technologies adoption among Malaysian small and medium enterprises. Int. J. Manag. Enterp. Dev. 2009, 6, 397–418. [Google Scholar] [CrossRef]

- Ismail, H.B.; Talukder, D.; Panni, M.F.A.K. Technology dimension of CRM: The orientation level and its impact on the business performance of SMEs in Malaysia. Int. J. Electron. Cust. Relatsh. Manag. 2007, 1, 16–29. [Google Scholar] [CrossRef]

- Mahmud, N.; Hilmi, M.F. TQM and Malaysian SMEs performance: The mediating roles of organization learning. Procedia Soc. Behav. Sci. 2014, 130, 216–225. [Google Scholar] [CrossRef]

- Hameed, W.U.; Basheer, M.F.; Iqbal, J.; Anwar, A.; Ahmad, H.K. Determinants of Firm’s open innovation performance and the role of R & D department: An empirical evidence from Malaysian SME’s. J. Glob. Entrep. Res. 2018, 8, 29. [Google Scholar]

- Hameed, W.; Naveed, F. Coopetition-Based Open-Innovation and Innovation Performance: Role of Trust and Dependency Evidence from Malaysian High. Tech. SMEs. Pakistan J. Commer. Soc. Sci. 2019, 13, 209–230. [Google Scholar]

- Statistics. Percentage share of SMEs DGP and Malaysian GDP in 2017; Department of Statistics: Kaula Lumpur, Malaysia, 2017.

- Wirtenberg, J.; Lipsky, D.; Abrams, L.; Conway, M.; Slepian, J. The future of organization development: Enabling sustainable business performance through people. Organ. Dev. J. 2007, 25, 11. [Google Scholar]

- Samy, M.; Odemilin, G.; Bampton, R. Corporate social responsibility: A strategy for sustainable business success. An. analysis of 20 selected British companies. Corporate Governance Int. J. Bus. Soc. 2010, 10, 203–217. [Google Scholar] [CrossRef]

- Wang, C.-J. Do ethical and sustainable practices matter? Effects of corporate citizenship on business performance in the hospitality industry. Int. J. Contemp. Hosp. Manag. 2014, 26, 930–947. [Google Scholar] [CrossRef]

- Fujii, H.; Iwata, K.; Kaneko, S.; Managi, S. Corporate environmental and economic performance of Japanese manufacturing firms: Empirical study for sustainable development. Bus. Strategy Environ. 2013, 22, 187–201. [Google Scholar] [CrossRef]

- Schaper, M. The challenge of environmental responsibility and sustainable development: Implications for SME and entrepreneurship academics. Radic. Chang. World: Will SMEs Soar Crash 2002, 541–553. [Google Scholar]

- Bourlakis, M.; Maglaras, G.; Aktas, E.; Gallear, D.; Fotopoulos, C. Firm size and sustainable performance in food supply chains: Insights from Greek SMEs. Int. J. Prod. Econ. 2014, 152, 112–130. [Google Scholar] [CrossRef] [Green Version]

- Taylor, N.; Barker, K.; Simpson, M. Achieving ‘sustainable business’: A study of perceptions of environmental best practice by SMEs in South. Yorkshire. Environ. Plan. C Gov. Policy 2003, 21, 89–105. [Google Scholar] [CrossRef]

- Bianchi, C.; Cosenz, F.; Marinković, M. Designing dynamic performance management systems to foster SME competitiveness according to a sustainable development perspective: Empirical evidences from a case-study. Int. J. Bus. Perform. Manag. 2015, 16, 84–108. [Google Scholar] [CrossRef]

- Hirvonen, S.; Laukkanen, T. The Moderating Effect of the Market. Orientation Components on the Brand Orientation–Brand Performance Relationship. In Celebrating America’s Pastimes: Baseball, Hot Dogs, Apple Pie and Marketing? Springer: Berlin/Heidelberg, Germany, 2016; pp. 185–186. [Google Scholar]

- Antony, J.P.; Bhattacharyya, S. Measuring organizational performance and organizational excellence of SMEs–Part. 1: A conceptual framework. Meas. Bus. Excell. 2010, 14, 3–11. [Google Scholar] [CrossRef]

- Antony, J.P.; Bhattacharyya, S. Measuring organizational performance and organizational excellence of SMEs–Part. 2: An empirical study on SMEs in India. Meas. Bus. Excell. 2010, 14, 42–52. [Google Scholar] [CrossRef]

- Waseem-Ul-Hameed, S.N.; Azeem, M.; Aljumah, A.I.; Adeyemi, R.A. Determinants of E-Logistic Customer Satisfaction: A Mediating Role of Information and Communication Technology (ICT). Int. J. Chain Manag. 2018, 7, 105–111. [Google Scholar]

- Taylor, S.A.; Baker, T.L. An. assessment of the relationship between service quality and customer satisfaction in the formation of consumers’ purchase intentions. J. Retail. 1994, 70, 163–178. [Google Scholar] [CrossRef]

- Wallin Andreassen, T.; Lindestad, B. Customer loyalty and complex services: The impact of corporate image on quality, customer satisfaction and loyalty for customers with varying degrees of service expertise. Int. J. Serv. Ind. Manag. 1998, 9, 7–23. [Google Scholar] [CrossRef]

- Matzler, K.; Hinterhuber, H.H. How to make product development projects more successful by integrating Kano’s model of customer satisfaction into quality function deployment. Technovation 1998, 18, 25–38. [Google Scholar] [CrossRef]

- Kristensen, K.; Martensen, A.; Gronholdt, L. Customer satisfaction measurement at post Denmark: Results of application of the European customer satisfaction index methodology. Total Qual. Manag. 2000, 11, 1007–1015. [Google Scholar] [CrossRef]

- Olusola, O. Intinsic motivation, job satisfaction and self-efficacy as predictors of job performance of industrial workers in ijebu zone of ogun state. J. Int. Soc. Res. 2011, 4, 569–577. [Google Scholar]

- Devi, S.; Kamyabi, Y. The impact of advisory services on Iranian SME performance: An. empirical investigation of the role of professional accountants. South African J. Bus. Manag. 2012, 43, 61–72. [Google Scholar]

- Gharakhani, D.; Mousakhani, M. Knowledge management capabilities and SMEs’ organizational performance. J. Chin. Entrep. 2012, 4, 35–49. [Google Scholar] [CrossRef]

- Johannessen, J.-A.; Olsen, B.; Olaisen, J. Aspects of innovation theory based on knowledge-management. Int. J. Inf. Manag. 1999, 19, 121–139. [Google Scholar] [CrossRef]

- Simons, R. The role of management control systems in creating competitive advantage: New perspectives. Account. Organ. Soc. 1990, 15, 127–143. [Google Scholar] [CrossRef]

- Otley, D.T.; Berry, A.J. Control., organisation and accounting. Account. Organ. Soc. 1980, 5, 231–244. [Google Scholar] [CrossRef]

- Chenhall, R.H. Management control systems design within its organizational context: Findings from contingency-based research and directions for the future. Account. Organ. Soc. 2003, 28, 127–168. [Google Scholar] [CrossRef]

- Alvesson, M.; Kärreman, D. Interfaces of control. Technocratic and socio-ideological control in a global management consultancy firm. Account. Organ. Soc. 2004, 29, 423–444. [Google Scholar] [CrossRef]

- Ali, M. Effect of Firm Size on the Relationship between Strategic Planning Dimensions and Performance of Manufacturing Firms in Kenya. Ph.D. Thesis, Jomo Kenyatta University of Agriculture and Technology, Juja, Kenya, 2017. [Google Scholar]

- Bonner, S.E.; Sprinkle, G.B. The effects of monetary incentives on effort and task performance: Theories, evidence, and a framework for research. Account. Organ. Soc. 2002, 27, 303–345. [Google Scholar] [CrossRef]

- Chhillar, P. Management control systems and corporate governance: A theoretical review. Asia-Pac. Manag. Account. J. 2013, 10, 103–128. [Google Scholar]

- Lundell, T.; Forzelius, M. Developing a Framework for Management Control. Systems in Start-ups: How Management Control. Systems can Be Used in Fast-Growing Technology Start-Ups to Support Controlled Growth. Master’s Thesis, Linköping University, Department of Management and Engineering (IEI), Linköping, Sweden, 2017. [Google Scholar]

- Peljhan, D.; Tekavčič, M. The impact of management control systems-strategy interaction on performance management: A case study. Organizacija 2008, 41, 184. [Google Scholar] [CrossRef]

- Jordao, R.V.D.; Souza, A.A.; Avelar, E.A. Organizational culture and post-acquisition changes in management control systems: An. analysis of a successful Brazilian case. J. Bus. Res. 2014, 67, 542–549. [Google Scholar] [CrossRef]

- Simons, R. Levers of Control: How Managers Use Innovative Control Systems to Drive Strategic Renewal; Harvard Business Press: Brighton, MA, USA, 1994. [Google Scholar]

- Shields, M.D. Research in management accounting by North. Americans in the 1990s. J. Manag. Account. Res. 1997, 9, 3–62. [Google Scholar]

- Langfield-Smith, K. Management control systems and strategy: A critical review. Account. Organ. Soc. 1997, 22, 207–232. [Google Scholar] [CrossRef]

- Swenson, C. Empirical evidence on municipal tax policy and firm growth. Int. J. Public Policy Adm. Res. 2016, 3, 1–13. [Google Scholar] [CrossRef]

- Galliers, R.D. Towards a flexible information architecture: Integrating business strategies, information systems strategies and business process redesign. Inf. Syst. J. 1993, 3, 199–213. [Google Scholar] [CrossRef]

- Basili, V.; Heidrich, J.; Lindvall, M.; Munch, J.; Regardie, M.; Trendowicz, A. GQM^+ strategies--aligning business strategies with software measurement. In Proceedings of the First International Symposium on Empirical Software Engineering and Measurement (ESEM 2007), Madrid, Spain, 20–21 September 2007. [Google Scholar]

- Ashley, C.; Haysom, G. From philanthropy to a different way of doing business: Strategies and challenges in integrating pro-poor approaches into tourism business. Dev. South. Afr. 2006, 23, 265–280. [Google Scholar] [CrossRef]

- Prikladnicki, R.; Audy, J.L.N.; Damian, D.; de Oliveira, T.C. Distributed Software Development: Practices and challenges in different business strategies of offshoring and onshoring. In Proceedings of the International Conference on Global Software Engineering (ICGSE 2007), Munich, Germany, 27–30 August 2007. [Google Scholar]

- Lin, C.; Tsai, H.-L.; Wu, J.-C. Collaboration strategy decision-making using the Miles and Snow typology. J. Bus. Res. 2014, 67, 1979–1990. [Google Scholar] [CrossRef]

- Jabarullah, N.H.; Shabbir, M.S.; Abbas, M.; Siddiqi, A.F.; Berti, S. Using random inquiry optimization method for provision of heat and cooling demand in hub systems for smart buildings. Sustain. Cities Soc. 2019, 47, 101475. [Google Scholar] [CrossRef]

- Dropulić, I. The effect of contingency factors on management control systems: A study of manufacturing companies in Croatia. Econ. Res.-Ekon. Istraživanja 2013, 1, 369–382. [Google Scholar] [CrossRef]

- Auzair, S.M.; Langfield-Smith, K. The effect of service process type, business strategy and life cycle stage on bureaucratic MCS in service organizations. Manag. Account. Res. 2005, 16, 399–421. [Google Scholar] [CrossRef]

- Elbashir, M.Z.; Collier, P.A.; Sutton, S.G. The role of organizational absorptive capacity in strategic use of business intelligence to support integrated management control systems. Account. Rev. 2011, 86, 155–184. [Google Scholar] [CrossRef]

- Chenhall, R.H.; Kallunki, J.-P.; Silvola, H. Exploring the relationships between strategy, innovation, and management control systems: The roles of social networking, organic innovative culture, and formal controls. J. Manag. Account. Res. 2011, 23, 99–128. [Google Scholar] [CrossRef]

- Porter, M.E. Competitive Strategy: Techniques for Analyzing Industries and Competitors; Simon and Schuster: New York, NY, USA, 1980. [Google Scholar]

- Kim, E.; Nam, D.-I.; Stimpert, J.L. Testing the applicability of Porter’s generic strategies in the digital age: A study of Korean cyber malls. J. Bus. Strateg. 2004, 21, 19–45. [Google Scholar]

- Parnell, J.A. Strategic clarity, business strategy and performance. J. Strategy Manag. 2010, 3, 304–324. [Google Scholar] [CrossRef]

- Maldonado-Guzman, G.; Marin-Aguilar, J.; Garcia-Vidales, M. Innovation and performance in Latin-American small family firms. Asian Econ. Financ. Rev. 2018, 8, 1008–1020. [Google Scholar]

- Junqueira, E.; Dutra, E.V.; Filho, H.Z.; Gonzaga, R. The Effect of Strategic Choices and Management Control. Systems on Organizational Performance. Rev. Contab. Finanças 2016. [Google Scholar] [CrossRef]

- Sampe, F. The influence of organizational learning on performance in Indonesian SMEs. Ph.D. Thesis, Southern Cross University, Lismore, Australia, 2012. [Google Scholar]

- Arshed, N.; Hassan, M.S.; Grant, K.A.; Aziz, O. Are Karachi Stock Exchange Firms Investment Promoting? Evidence of Efficient Market. Hypothesis Using Panel Cointegration. Asian Dev. Policy Rev. 2019, 7, 52–65. [Google Scholar] [CrossRef]

- Ramamurthy, K. Role of environmental, organizational and technological factors in information technology implementation in advanced manufacturing: An. innovation adoption-diffusion perspective. Ph.D. Thesis, University of Pittsburgh, Pittsburgh, PA, USA, 1991. [Google Scholar]

- Narver, J.C.; Slater, S.F. The effect of a market orientation on business profitability. J. Mark. 1990, 54, 20–35. [Google Scholar] [CrossRef]

- Sekaran, U.; Bougie, R. Research Methods for Business: A Skill Building Approach; John Wiley & Sons: Hoboken, NJ, USA, 2016. [Google Scholar]

- Comrey, A.L.; Lee, H.B. A First Course in Factor Analysis; Psychology Press: East Sussex, England, UK, 1992. [Google Scholar]

- Bamgbade, J.A.; Kamaruddeen, A.M.; Nawi, M. Factors influencing sustainable construction among construction firms in Malaysia: A preliminary study using PLS-SEM. Rev. Tec. De La Fac. De Ing. Univ. Del Zulia (Tech. J. Fac. Eng. TJFE) 2015, 38, 132–142. [Google Scholar]

- Opara, B.C. Analysis of Nigeria firms, export marketing configuration in the global market. Int. J. Manag. Sustain. 2014, 3, 448–456. [Google Scholar]

- Hair, J.F.; Ringle, C.M.; Sarstedt, M. Partial least squares structural equation modeling: Rigorous applications, better results and higher acceptance. Long Range Plan. 2013, 46, 1–12. [Google Scholar] [CrossRef]

- Zhou, T. Understanding continuance usage of mobile sites. Ind. Manag. Data Syst. 2013, 113, 1286–1299. [Google Scholar] [CrossRef]

- Hayduk, L.A.; Littvay, L. Should researchers use single indicators, best indicators, or multiple indicators in structural equation models? BMC Med Res. Methodol. 2012, 12, 159. [Google Scholar] [CrossRef]

- Hair, J.F.; Sarstedt, M.; Pieper, T.M.; Ringle, C.M. Applications of partial least squares path modeling in management journals: A review of past practices and recommendations for future applications. Long Range Plan. 2012, 45, 320–340. [Google Scholar] [CrossRef]

- Nunnally, J.C. Psychometric Theory; McGraw-Hill: New York, NY, USA, 1978; Volume 226. [Google Scholar]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Chin, W.W. How to Write Up and Report PLS Analyses. In Handbook of Partial Least Squares; Springer: Berlin/Heidelberg, Germany, 2010; pp. 655–690. [Google Scholar]

- Memon, M.A.; Cheah, J.; Ramayah, T.; Ting, H.; Chuah, F. Mediation Analysis Issues and Recommendations. J. Appl. Struct. Equ. Modeling 2018, 2, 1–9. [Google Scholar]

- Preacher, K.J.; Hayes, A.F. Asymptotic and resampling strategies for assessing and comparing indirect effects in multiple mediator models. Behav. Res. Methods 2008, 40, 879–891. [Google Scholar] [CrossRef] [PubMed]

- Preacher, K.J.; Hayes, A.F. SPSS and SAS procedures for estimating indirect effects in simple mediation models. Behav. Res. Methods Instrum. Comput. 2004, 36, 717–731. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Baron, R.M.; Kenny, D.A. The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. J. Personal. Soc. Psychol. 1986, 51, 1173. [Google Scholar] [CrossRef]

- MacKinnon, D.P.; Fairchild, A.J.; Fritz, M.S. Mediation analysis. Annu. Rev. Psychol. 2007, 58, 593–614. [Google Scholar] [CrossRef] [PubMed]

- Zhao, X.; Lynch, J.G., Jr.; Chen, Q. Reconsidering Baron and Kenny: Myths and truths about mediation analysis. J. Consum. Res. 2010, 37, 197–206. [Google Scholar] [CrossRef]

- Cohen, J. Statistical Power Analysis for the Behavioral Sciences, 2nd ed.; Erlbaum: Hillsdale, NJ, USA, 1988. [Google Scholar]

- Mahmoud, O. Managerial Judgement versus Financial Techniques in Strategic Investment Decisions: An Empirical Study on the Syrian Coastal Region. Firms. Int. J. Bus. Econ. Manag. 2016, 3, 31–43. [Google Scholar] [CrossRef]

- Duréndez, A.; Ruíz-Palomo, D.; García-Pérez-de-Lema, D.; Diéguez-Soto, J. Management control systems and performance in small and medium family firms. Eur. J. Fam. Bus. 2016, 6, 10–20. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| States | %Age | States | %Age | States | %Age | States | %Age |

|---|---|---|---|---|---|---|---|

| Selangor | 19.8 | Penang | 7.4 | Kelantan | 5.1 | Terengganu | 3.2 |

| Kuala Lumpur | 14.7 | Sarawak | 6.7 | Pahang | 4.1 | Perlis | 0.8 |

| Johor | 10.8 | Sabah | 6.2 | Negeri Sembilan | 3.6 | Labuan | 0.3 |

| Perak | 8.3 | Kedah | 5.4 | Malacca | 3.5 | Putrajaya | 0.1 |

| First-Order Constructs | Second-Order Constructs | Items | Factor Loadings | AVE | CR | R2 | Cronbach’s Alpha |

|---|---|---|---|---|---|---|---|

| Planning | PC1 | 0.808 | 0.628 | 0.922 | 0.901 | ||

| PC11 | 0.789 | ||||||

| PC13 | 0.793 | ||||||

| PC3 | 0.806 | ||||||

| PC5 | 0.85 | ||||||

| PC6 | 0.799 | ||||||

| PC8 | 0.694 | ||||||

| Cultural | CC1 | 0.808 | 0.613 | 0.904 | 0.873 | ||

| CC11 | 0.813 | ||||||

| CC15 | 0.691 | ||||||

| CC3 | 0.85 | ||||||

| CC5 | 0.823 | ||||||

| CC7 | 0.7 | ||||||

| Cybernetic | CBC1 | 0.747 | 0.554 | 0.896 | 0.866 | ||

| CBC2 | 0.84 | ||||||

| CBC3 | 0.85 | ||||||

| CBC4 | 0.673 | ||||||

| CBC5 | 0.739 | ||||||

| CBC6 | 0.692 | ||||||

| CBC7 | 0.645 | ||||||

| Rewards and Compensation | RC1 | 0.653 | 0.596 | 0.853 | 0.767 | ||

| RC3 | 0.855 | ||||||

| RC4 | 0.862 | ||||||

| RC6 | 0.694 | ||||||

| Administrative | ADC1 | 0.846 | 0.704 | 0.922 | 0.893 | ||

| ADC2 | 0.895 | ||||||

| ADC5 | 0.895 | ||||||

| ADC6 | 0.785 | ||||||

| ADC8 | 0.764 | ||||||

| MCS package | Planning | 0.808 | 0.631 | 0.894 | 0.943 | ||

| Cultural | 0.852 | ||||||

| Cybernetic | 0.851 | ||||||

| Rewards and Compensation | 0.743 | ||||||

| Administrative | 0.708 | ||||||

| Cost Leadership | CL1 | 0.824 | 0.708 | 0.906 | 0.091 | 0.862 | |

| CL2 | 0.842 | ||||||

| CL4 | 0.854 | ||||||

| CL5 | 0.845 | ||||||

| Differentiation Strategy | DF1 | 0.918 | 0.509 | 0.799 | 0.017 | 0.764 | |

| DF2 | 0.521 | ||||||

| DF3 | 0.684 | ||||||

| DF4 | 0.674 | ||||||

| Firms Sustainability | FS1 | 0.866 | 0.634 | 0.896 | 0.482 | 0.858 | |

| FS2 | 0.711 | ||||||

| FS3 | 0.811 | ||||||

| FS4 | 0.83 | ||||||

| FS5 | 0.754 |

| Variables | MCSP | CL | DF | FS |

|---|---|---|---|---|

| Management control system package (MCSP) | 0.794 | |||

| Cost leadership (CL) | 0.302 | 0.841 | ||

| Differentiation strategy (DS) | 0.130 | 0.482 | 0.714 | |

| Firm stability (FS) | 0.482 | 0.453 | 0.546 | 0.796 |

| Hypotheses | Paths | Original Sample | Sample Mean | Std. Dev. | t-Values | p-Values | Results |

|---|---|---|---|---|---|---|---|

| H1 | MCSP --> FS | 0.388 | 0.384 | 0.040 | 9.718 | 0.000 | Accepted |

| H2 | MCSP --> DF | 0.130 | 0.134 | 0.064 | 2.025 | 0.021 | Accepted |

| H3 | MCSP --> CL | 0.302 | 0.301 | 0.061 | 4.975 | 0.000 | Accepted |

| H4 | DF --> FS | 0.436 | 0.442 | 0.062 | 7.078 | 0.000 | Accepted |

| H5 | CL --> FS | 0.125 | 0.127 | 0.058 | 2.149 | 0.016 | Accepted |

| Hypotheses | Paths | Original Sample | Sample Mean | Std. Dev. | t-Values | p-Values | Results |

|---|---|---|---|---|---|---|---|

| H6 | MCSP-> DF-> FS | 0.057 | 0.059 | 0.030 | 1.891 | 0.029 | Accepted |

| H7 | MCSP-> CL-> FS | 0.038 | 0.038 | 0.019 | 1.962 | 0.025 | Accepted |

| Total | R2 | SSO | SSE | Q2( = 1–SSE/SSO) |

|---|---|---|---|---|

| Cost leadership | 0.091 | 1536.000 | 1443.221 | 0.060 |

| Differentiation strategy | 0.017 | 1536.000 | 1532.626 | 0.002 |

| Firm sustainability | 0.482 | 1920.000 | 1396.124 | 0.273 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Haseeb, M.; Lis, M.; Haouas, I.; WW Mihardjo, L. The Mediating Role of Business Strategies between Management Control Systems Package and Firms Stability: Evidence from SMEs in Malaysia. Sustainability 2019, 11, 4705. https://doi.org/10.3390/su11174705

Haseeb M, Lis M, Haouas I, WW Mihardjo L. The Mediating Role of Business Strategies between Management Control Systems Package and Firms Stability: Evidence from SMEs in Malaysia. Sustainability. 2019; 11(17):4705. https://doi.org/10.3390/su11174705

Chicago/Turabian StyleHaseeb, Muhammad, Marcin Lis, Ilham Haouas, and Leonardus WW Mihardjo. 2019. "The Mediating Role of Business Strategies between Management Control Systems Package and Firms Stability: Evidence from SMEs in Malaysia" Sustainability 11, no. 17: 4705. https://doi.org/10.3390/su11174705

APA StyleHaseeb, M., Lis, M., Haouas, I., & WW Mihardjo, L. (2019). The Mediating Role of Business Strategies between Management Control Systems Package and Firms Stability: Evidence from SMEs in Malaysia. Sustainability, 11(17), 4705. https://doi.org/10.3390/su11174705