Solutions for SMEs Challenged by CSR: A Multiple Cases Approach in the Food Industry within the DACH-Region

Abstract

:1. Introduction

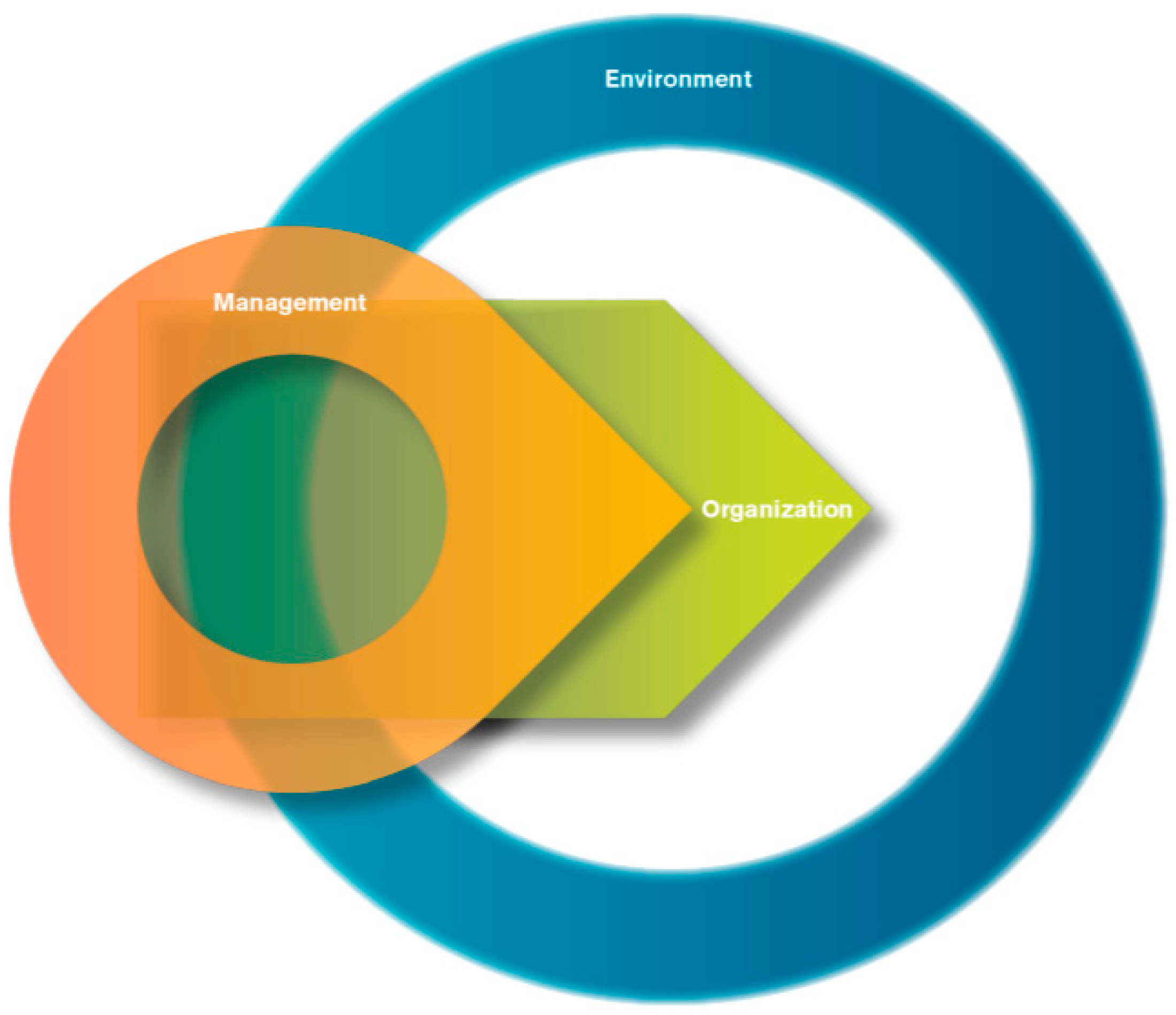

2. The St. Galler Management Model in Relation to CSR Challenges Faced by SMEs

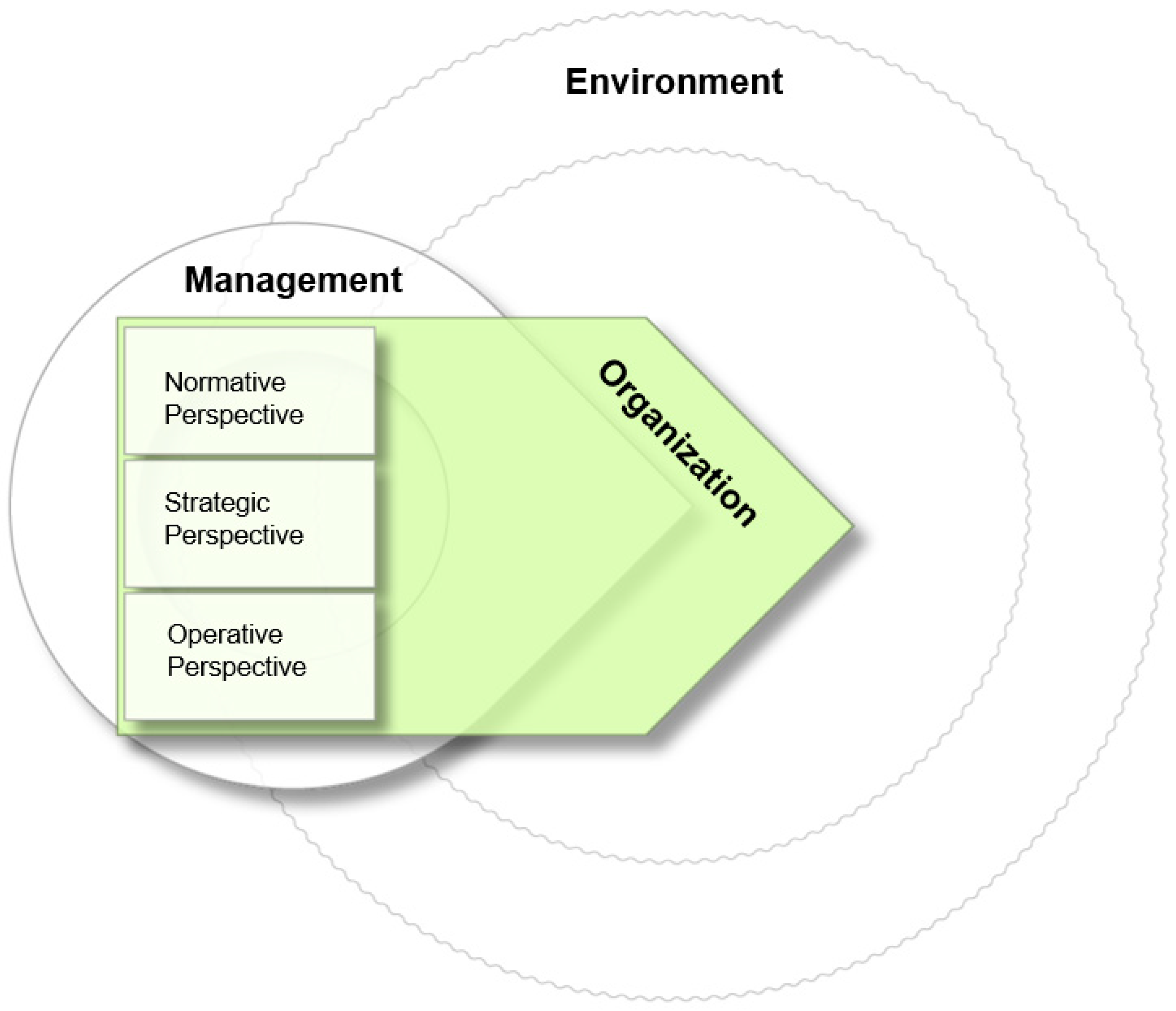

2.1. The Organization Dimension and Its Management Levels

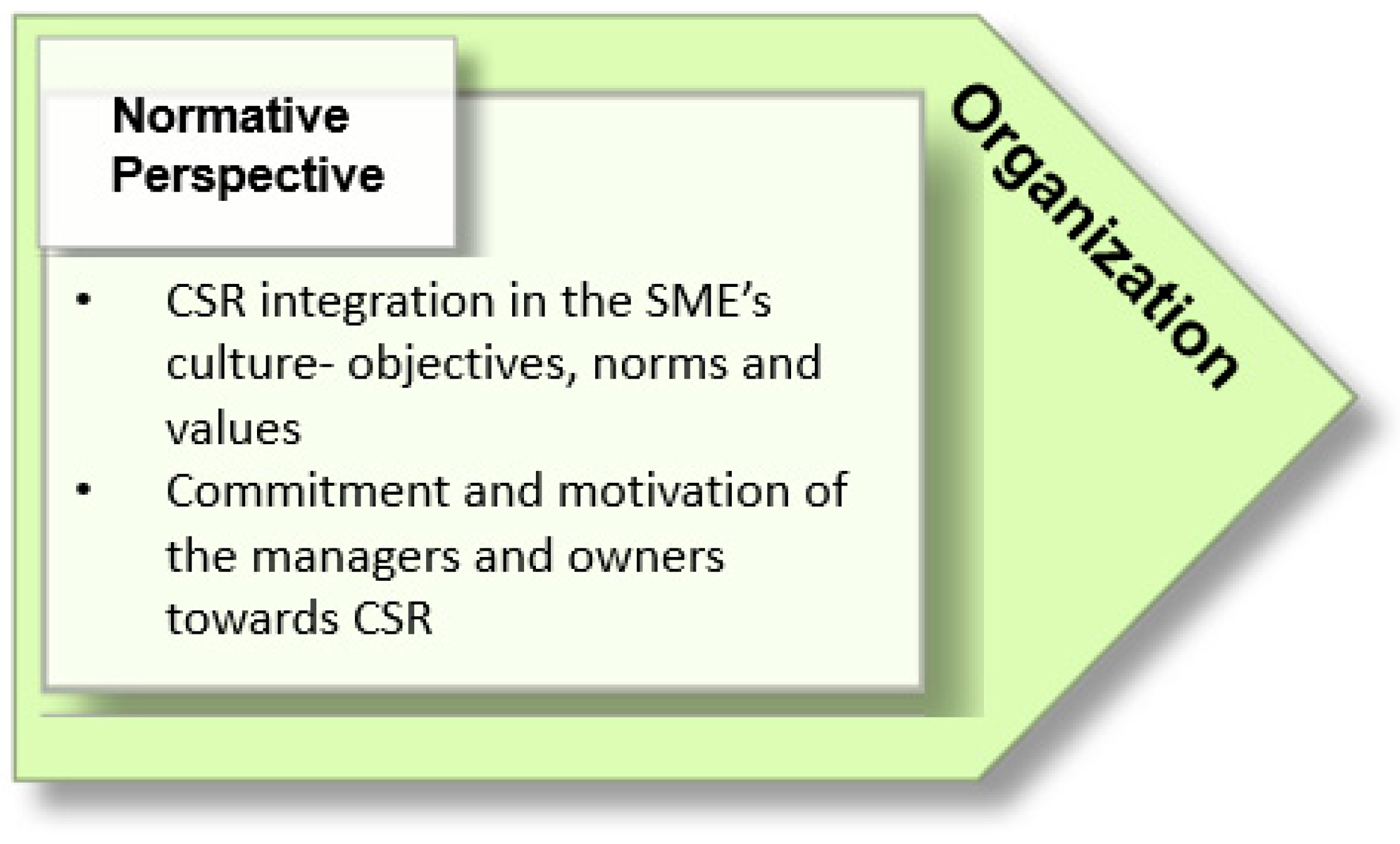

2.2. CSR Challenges at the Normative Management Level

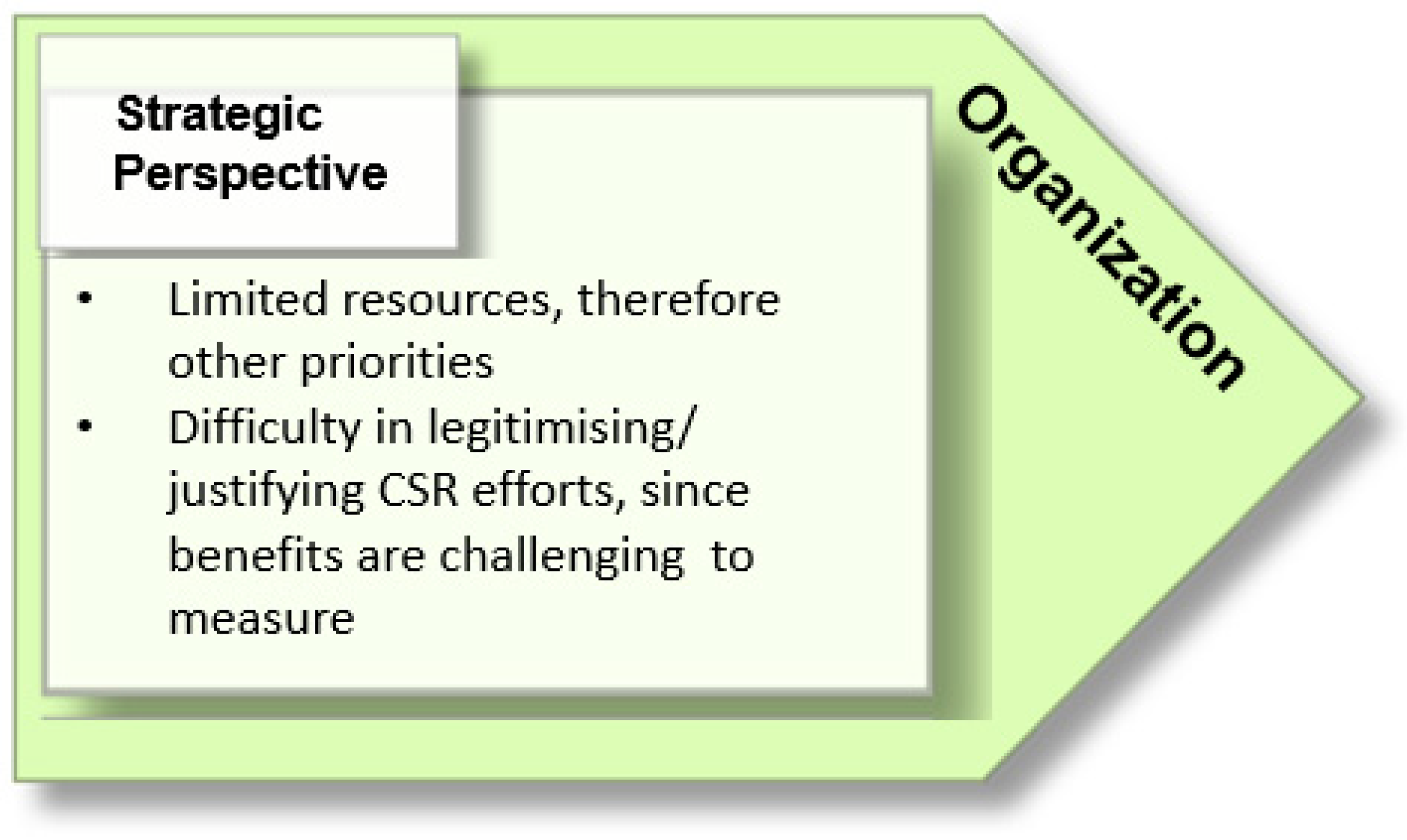

2.3. CSR Challenges at the Strategic Management Level

2.4. CSR Challenges at the Operative Management Level

3. Research Methodology

3.1. Research Approach

3.2. Research Design

3.3. Case Selection and Sample Description

3.4. Data Collection and Analysis

3.5. Ethical Considerations

4. Results

4.1. The Organization Dimension

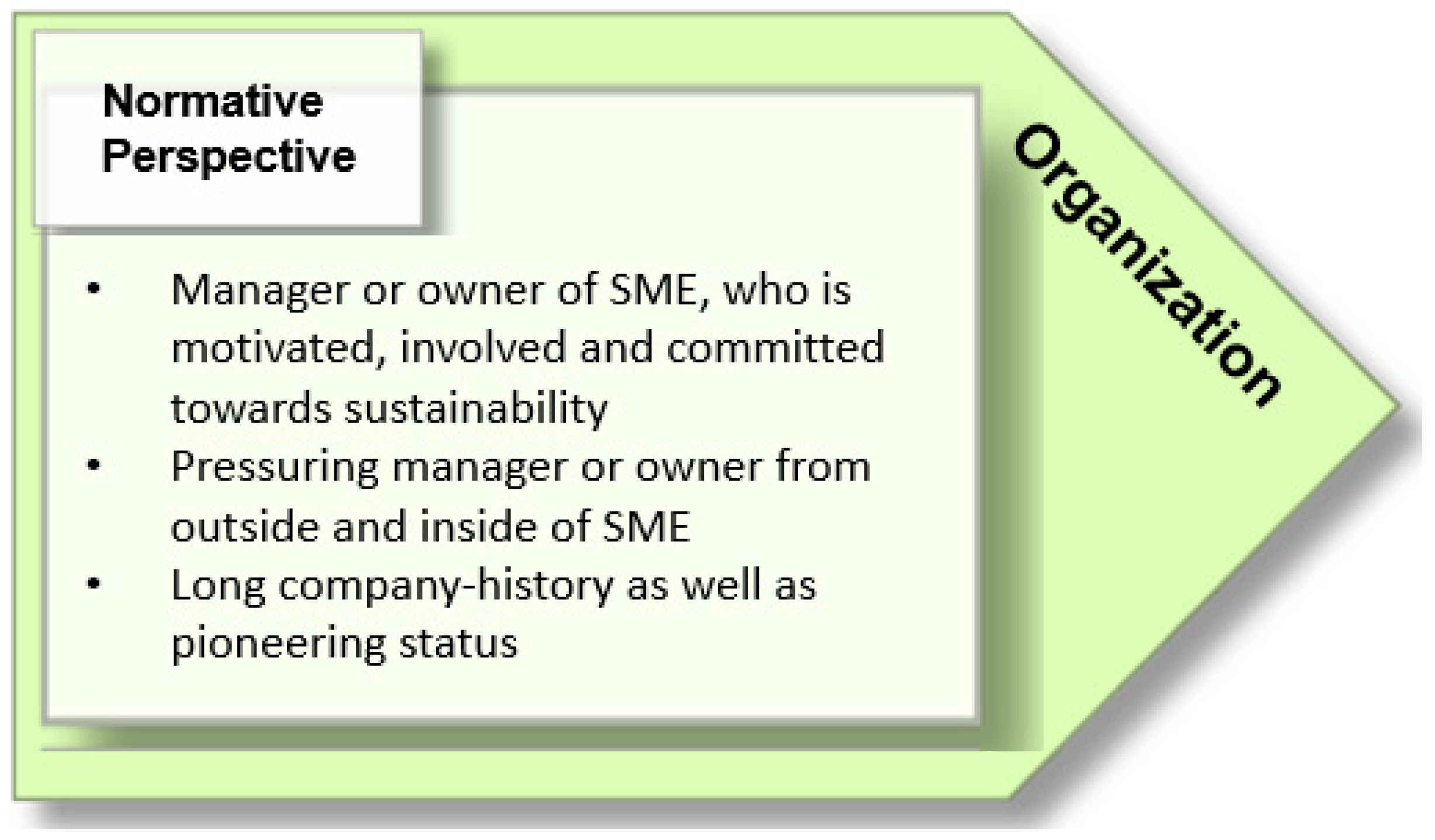

4.1.1. The Normative Management Level

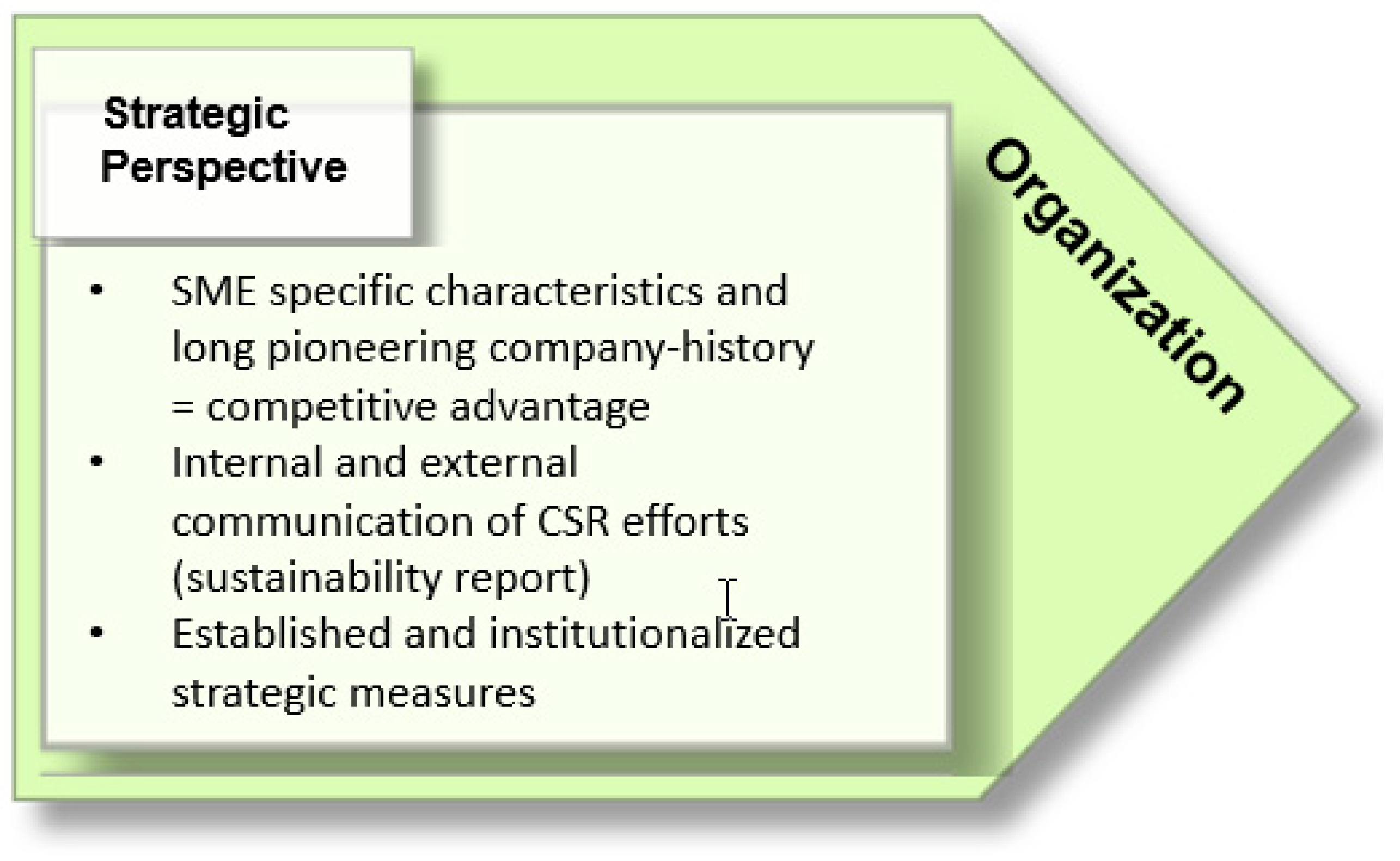

4.1.2. The Strategic Management Level

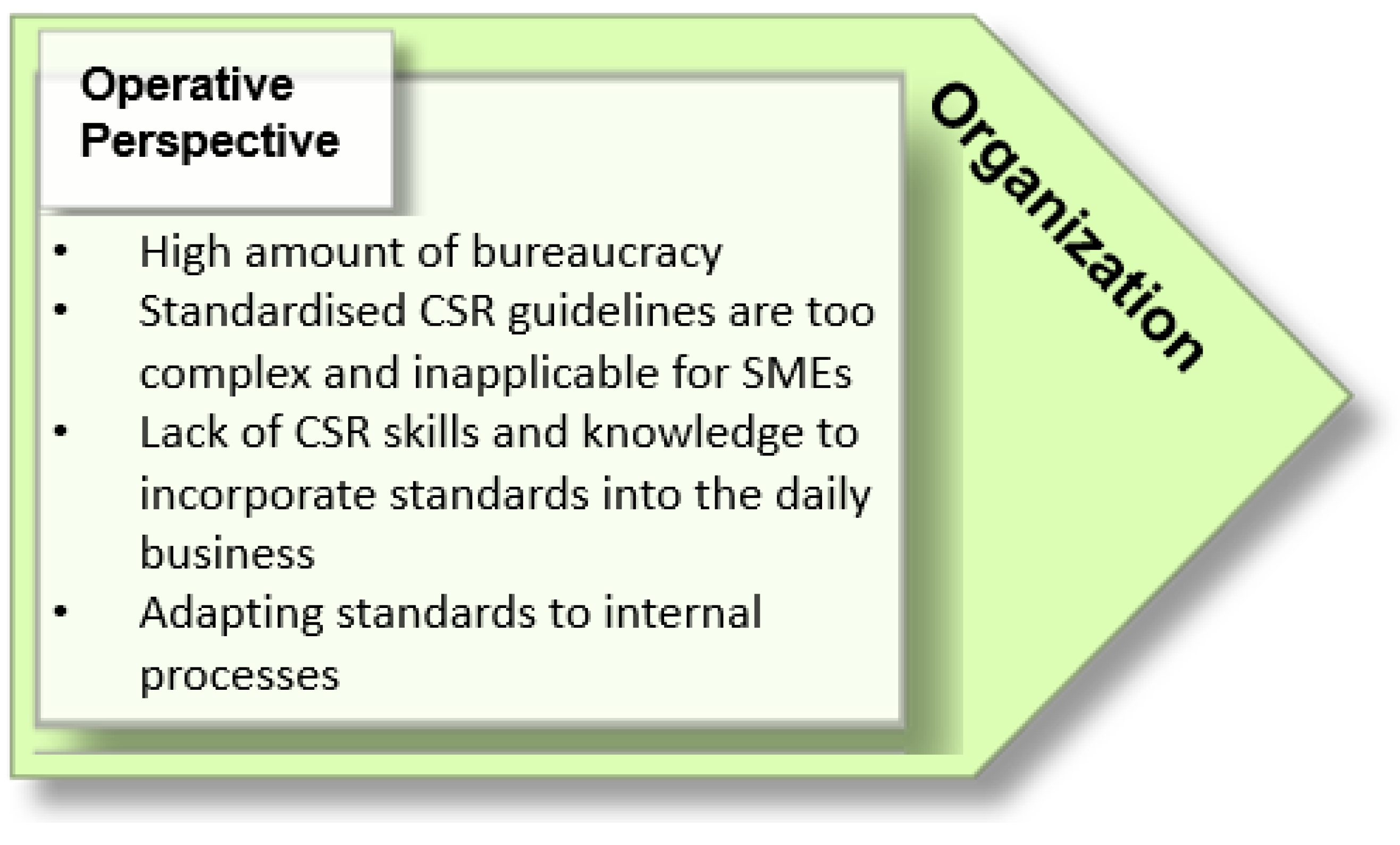

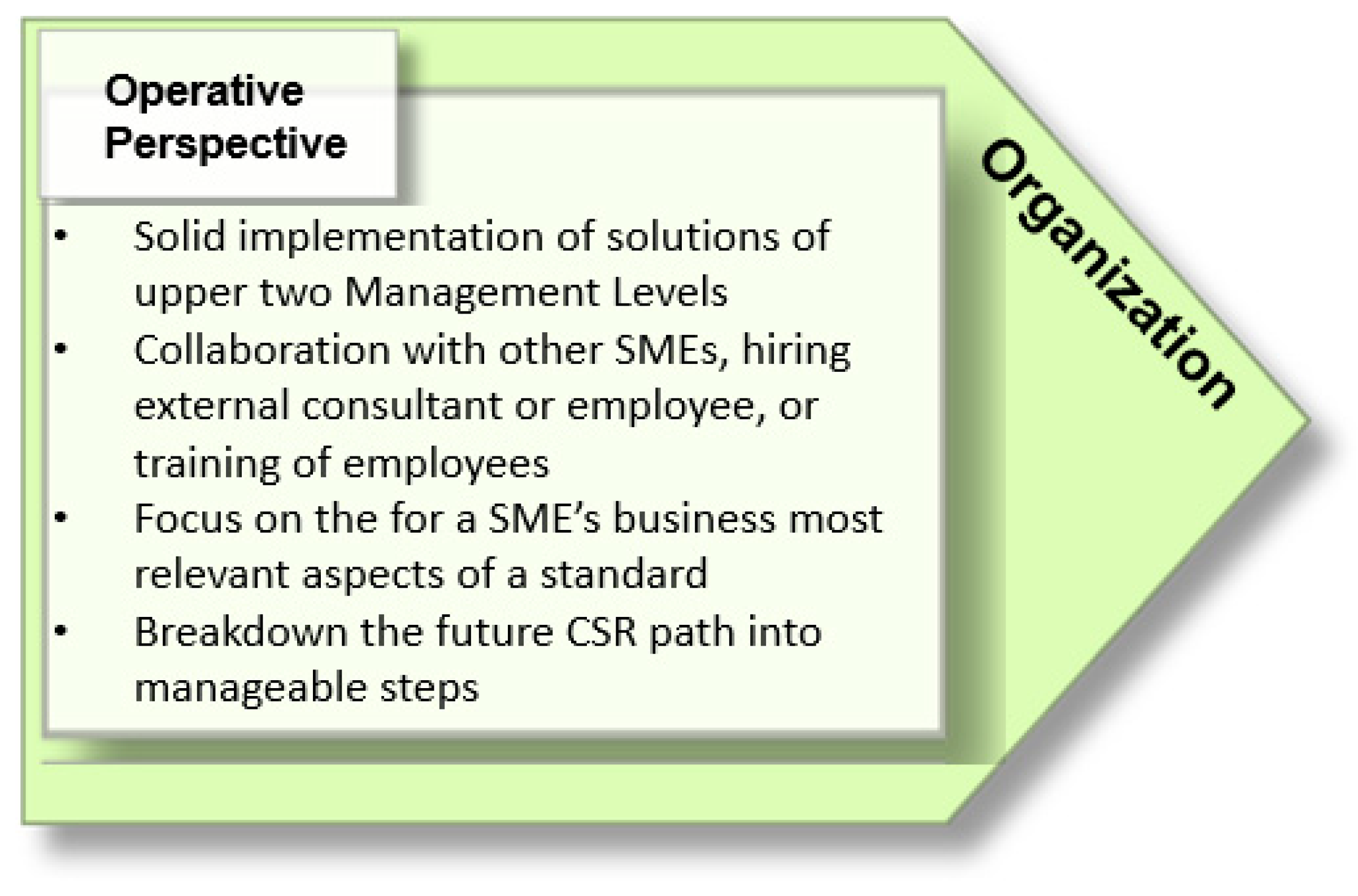

4.1.3. The Operative Management Level

5. Discussion of Findings of the Organization Dimension

5.1. The Normative Management Level

5.2. The Strategic Management Level

5.3. The Operative Management Level

6. Conclusions and Future Research

Author Contributions

Funding

Conflicts of Interest

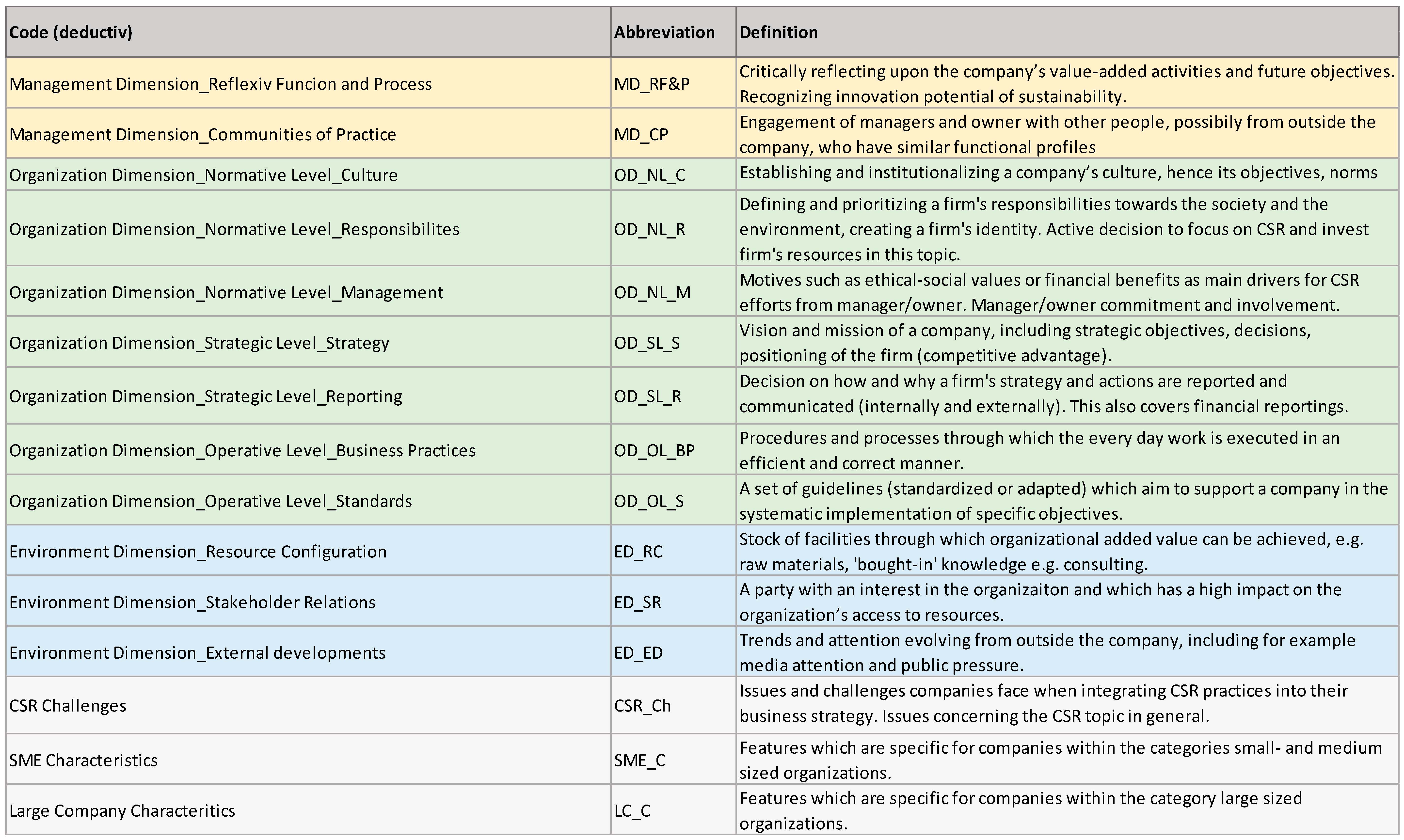

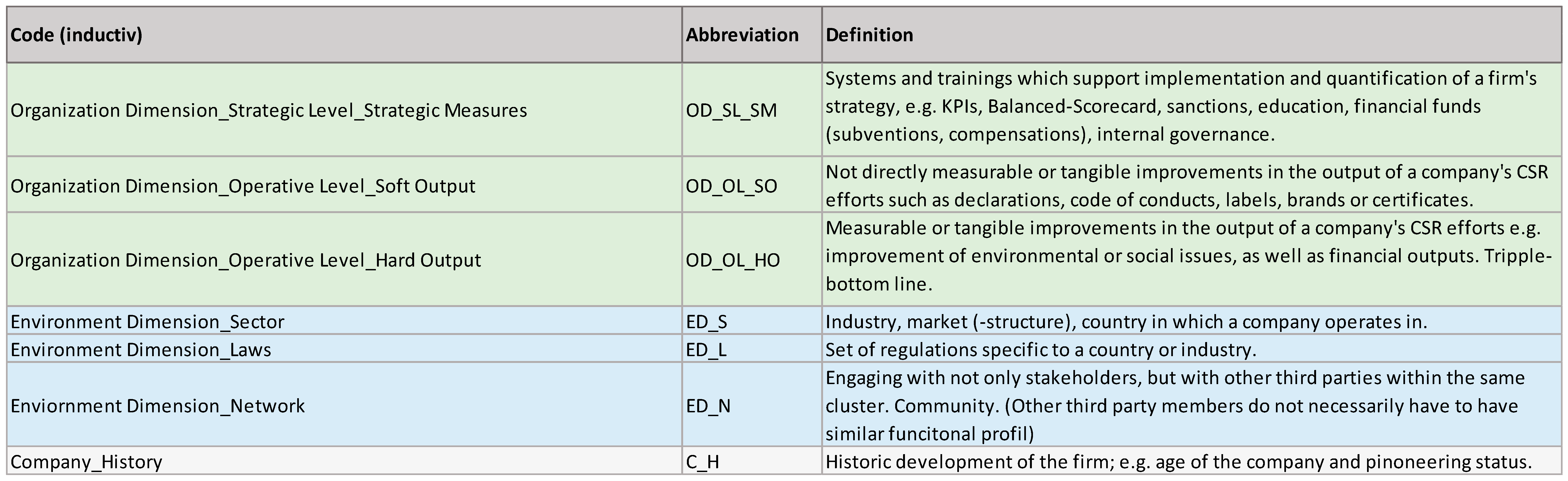

Appendix A.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Interviewee | Company/Organization | Position | Country | Description |

|---|---|---|---|---|

| SME 1 | (Anonymous) | Project Manager Sustainability | Switzerland | Chocolate producer, and a subsidiary of a Swiss retailer |

| SME 2 | Jucker Farm AG | Manager Marketing and Communications | Switzerland | An agritourism company and agriculture producer and distributor |

| SME 3 | Holle baby food GmbH | Sustainability and Marketing Manager | Switzerland | A manufacturer of organic baby food |

| SME 4 | Kärntnermilch reg. GmbH | Environmental Manager | Austria | Dairy producer |

| SME 5 | Naturata AG | Quality and Environmental Manager | Germany | Manufacturer of biologically produced groceries |

| Expert 1 | Swiss Business Council for Sustainable Development (öbu) | CEO | Switzerland | Swiss network for sustainable economies (>360 members) |

| Expert 2 | BHP—Brugger und Partner AG | Senior Consultant | Switzerland | Consulting company with a core competence in ‘Corporate Social Responsibility’ |

| Expert 3 | Centre for Corporate Responsibility and Sustainability (CCRS), University Zurich | Director of the CCRS | Switzerland | Associated institute at the University of Zurich, focusing on exploring the role of the private sector in sustainable development on the local and global level, Jury member of the Zürcher Kantonalbank (ZKB)-KMU Award |

| Expert 4 | Eartheffect GmbH | CEO | Switzerland | Company offering workshops, educational programs and consulting on sustainability |

| Expert 5 | E2 Management Consulting AG | CEO | Switzerland | Consulting company, which develops and implements environmental and sustainability management for companies,Former managing director of öbu |

| Expert 6 | (Anonymous) | Project Manager | Austria | Economic platform for CSR and sustainable development, Organizer of a nation-wide CSR award |

| Expert 7 | Regionalwert AG Freiburg | CEO and Founder | Germany | A citizen shareholder company that channels citizens’ money to build up regional sustainable enterprises |

Appendix B. Interview Questionnaires

Appendix B.1. Interview Questions for Experts in the Field

Appendix B.1.1. Introductory Questions

- Why do you think that a few SMEs are successful in their CSR practices whilst others are not?

- How do the characteristics of SMEs influence their success in their CSR practices?

Appendix B.1.2. Challenges on Different Management Levels

- Normative Management Level

- ○

- CSR integration into the mindset of the management/owner(s)?

- ○

- No evident relation between CSR and the company’s activities

- ○

- Lack of consideration and understanding of the CSR topic

- ○

- CSR integration in the SME’s culture

- Strategic Management Level

- ○

- Limited resources, therefore other priorities

- ○

- Owner-operated, leading to difficulty in legitimizing/justifying CSR efforts due to difficulty in measuring benefits of efforts

- ○

- Limited external attention and pressure

- ○

- No demand for formal CSR strategy due to e.g., personal relationships with stakeholders

- Operative Management Level

- ○

- Lack of CSR skills and knowledge

- ○

- High amount of bureaucracy

- ○

- Standardized CSR strategies are too complex and inapplicable for SMEs

- ○

- Incorporating standards into the daily business, adaption to internal processes

- Why do you think some SMEs face these challenges whilst others do not? (cause of challenges)

- How can SMEs overcome these challenges?

- What is key to avoid these challenges?

- What is the role of the manager/owner of an SME when integrating CSR practices into the culture, strategy and into the daily business of the company?

Appendix B.1.3. Adapted CSR Standards

- How do you judge the development of adapted CSR standards to better suit SMEs characteristics?

- Why do you think there are still so many SMEs which, despite the creation of the adapted CSR standards, do not implement CSR practices?

- Do you think that the challenges which SMEs face on the Normative (challenges they face when implementing CSR practices in the firm’s culture) and on the Strategic Management Level (challenges they face when implementing CSR practices in the firm’s strategy) differ when focusing on adapted CSR standards compared to non-adapted standards?

- Do you think there are any challenges on the Operative Management Level for SMEs focusing on adapted CSR standards? If so, elaborate which ones and how these could be overcome or avoided.

Appendix B.2. Interview Questions for SMEs

Appendix B.2.1. Introductory Questions

- What does sustainability stand for within XYZ?

- Why do you think that XYZ is so successful in its CSR practices?

- Does the fact that XYZ is a SME have any influence on its success in its CSR practices?

Appendix B.2.2. Challenges on Different Management Levels

- Did XYZ face any challenges integrating CSR practices into the company’s

- ○

- culture (norms, values and objectives)?

- ○

- strategy (strategic measures, procedures, allocation and prioritization of resources, shareholder relationship)?

- ○

- daily business?

- Elaborate which ones and their causes.

- How did XYZ overcome these challenges?

- Normative Management Level

- ○

- CSR integration into the mindset of the management/owner(s)?

- ○

- No evident relation between CSR and the company’s activities

- ○

- Lack of consideration and understanding of the CSR topic

- ○

- CSR integration in the SME’s culture

- Strategic Management Level

- ○

- Limited resources, therefore other priorities

- ○

- Owner-operated, leading to difficulty in legitimizing/justifying CSR efforts due to difficulty in measuring benefits of efforts

- ○

- Limited external attention and pressure

- ○

- No demand for formal CSR strategy due to e.g., personal relationships with stakeholders

- Operative Management Level

- ○

- Lack of CSR skills and knowledge

- ○

- High amount of bureaucracy

- ○

- Standardized CSR strategies are too complex and inapplicable for SMEs

- ○

- Incorporating standards into the daily business, adaption to internal processes

- What is the role of the manager/owner of XYZ when integrating CSR practices into the culture, strategy and into the daily business of the company?

Appendix B.2.3. Adapted CSR Standards

- Why does XYZ implement adapted CSR standards? Why not?… only if XYZ implements adapted CSR standards:

- Were there any challenges implementing these adapted CSR standards in the daily business of XYZ?

- How did XYZ overcome these challenges?

Appendix C.

References

- Brammer, S.; Hoejmose, S.; Marchant, K. Environmental Management in SMEs in the UK: Practices, Pressures and Perceived Benefits. Bus. Strategy Environ. 2012, 21, 423–434. [Google Scholar] [CrossRef]

- Perrini, F.; Russo, A.; Tencati, A. CSR strategies of SMEs and large firms. Evidence from Italy. J. Bus. Ethics 2007, 74, 285–300. [Google Scholar] [CrossRef]

- Jenkins, H. Small business champions for corporate social responsibility. J. Bus. Ethics 2006, 67, 241–256. [Google Scholar] [CrossRef]

- European Union. Regulation (EC) no. 178/2002 of the European Parliament and of the Council of 28. January 2002. Off. J. Eur. Communities 2002, 131, 1–24. [Google Scholar]

- European Union. Directive 2014/.../eu of the European Parliament and of the Council of Amending Directive 2013/34/EU as Regards Disclosure of Non-Financial and Diversity Information by Certain Large Undertakings and Group; European Union: Brussels, Belgium, 2014. [Google Scholar]

- Brand, F.S.; Berger, V.; Hetze, K.; Schmidt, J.; Weber, M.; Winistörfer, H.; Daub, C. Overcoming current practical challenges in sustainability and integrated reporting: Insights from a Swiss field study. Sustain. Manag. Forum 2018, 26, 35–46. [Google Scholar] [CrossRef]

- Muller, P.; Julius, J.; Herr, D.; Koch, L.; Peycheva, V.; McKiernan, S. Annual Report on European SMEs 2016/2017: Focus on self-employment; European Commission: Brussels, Belgium, 2017. [Google Scholar]

- Kromjong, L.; Rajpal, S.; Thorns, M.; Verkouw, R. Small Business Big Impact-SME Sustainability Reporting from Vision to Action; Global Reporting Initiative: Amsterdam, The Netherlands, 2016. [Google Scholar]

- European Commission. Commission Recommendation of 6 May 2003 concerning the definition of micro, small, and medium-sized enterprises (2003/361/EC). Off. J. Eur. Union 2003, 124, 36–41. [Google Scholar]

- Stubblefield Loucks, E.; Martens, M.L.; Cho, C.H. Engaging small-and medium-sized businesses in sustainability. Sustain. Account. Manag. Policy J. 2010, 1, 178–200. [Google Scholar] [CrossRef]

- Halila, F. Networks as a means of supporting the adoption of organizational innovation in SMEs: The case of environmental management systems (EMSs) based on ISO 14001. Corp. Soc. Responsib. Environ. Manag. 2007, 14, 167–181. [Google Scholar] [CrossRef]

- Jenkins, H. A Critique of Conventional CSR Theory: An SME Perspective. J. Gen. Manag. 2004, 29, 37–57. [Google Scholar] [CrossRef]

- Gibb, A.A. SME Policy, Academic Research and the Growth of Ignorance, Mythical Concepts, Myths, Assumptions, Rituals and Confusions. Int. Small Bus. J. 2000, 18, 13–35. [Google Scholar] [CrossRef]

- Castka, P.; Balzaro, M.A.; Bamber, C.J. How Can SMEs Effectively Implement the CSR Agenda? A UK Case Study Perspective. Corp. Soc. Responsib. Environ. Manag. 2004, 11, 140–149. [Google Scholar] [CrossRef]

- European Commission. Promoting a European Framework for Corporate Social Responsibility. Green Paper; Directorate-General for Employment and Social Affairs of the European Commission: Luxembourg, 2001. [Google Scholar]

- Russo, A.; Tencati, A. Formal vs. Informal CSR strategies: Evidence from Italian Micro, Small, Medium-sized, and large firms. J. Bus. Ethics 2009, 85, 339–353. [Google Scholar] [CrossRef]

- Rüegg-Stürm, J.; Grand, S. Das St. Galler Management-Modell. 3. Überarbeitete Und Weiterentwickelte Auflage; Haupt: Bern, Switzerland, 2017. [Google Scholar]

- United Nations. Guide to Corporate Responsibility-Shaping a Sustainable Future; The United Nations Global Compact: New York, NY, USA, 2014; pp. 1–48. [Google Scholar]

- Bonini, S.; Görner, S.; Jones, A. How Companies Manage Sustainability: McKinsey Global Survey Results; McKinsey & Company: New York, NY, USA, 2010. [Google Scholar]

- Knopf, J.; Mayer-Scholl, B. Tips and Tricks for Advisors–Corporate Social Responsibility for Small and Medium-Sized Enterprises; European Commission: Brussels, Belgium, 2013. [Google Scholar]

- Ulrich, H.; Krieg, W. Das St. Galler Management-Modell; Haupt Verlag: Bern, Switzerland, 1972. [Google Scholar]

- European Commission. European SMEs and Social and Environmental Responsibility (4). Observatory of the European SMEs; Office for Official Publications of the European Communities: Luxembourg, 2002. [Google Scholar]

- Santos, M. CSR in SMEs: Strategies, practices, motivations and obstacles. Soc. Responsib. J. 2011, 7, 490–508. [Google Scholar] [CrossRef]

- Worthington, I.; Ram, M.; Jones, T. Giving something back: A study of corporate social responsibility in UK South Asian small enterprises. Bus. Ethics A Eur. Rev. 2006, 15, 95–108. [Google Scholar] [CrossRef]

- Graafland, J.; Van de Ven, B.; Stoffele, N. Strategies and Instruments for Organising CSR by Small and Large Businesses in the Netherlands. J. Bus. Ethics 2003, 47, 45–60. [Google Scholar] [CrossRef]

- Bianchi, R.; Noci, G. “Greening”-SMEs’ Competitiveness. Small Bus. Econ. 1998, 11, 269–281. [Google Scholar] [CrossRef]

- Carroll, A. The pyramid of corporate social responsibility. Bus. Horiz. 1991, 34, 42. [Google Scholar] [CrossRef]

- Quinn, J.J. Personal ethics and business ethics: The ethical attitudes of owner/managers of small business. J. Bus. Ethics 1997, 16, 119–127. [Google Scholar] [CrossRef]

- Tang, Z.; Hull, C.E.; Rothenberg, S. How Corporate Social Responsibility Engagement Strategy Moderates the CSR-Financial Performance Relationship. J. Manag. Stud. 2012, 49, 1274–1303. [Google Scholar] [CrossRef]

- Porter, M.E. Harvard’s Porter Compares Small Business to Big Business; Bloomberg Markets: New York, NY, USA, 2018; Available online: https://www.bloomberg.com/news/videos/2018-02-13/harvard-s-porter-compares-small-business-to-big-business-video (accessed on 13 February 2018).

- Biondi, V.; Frey, M.; Iraldo, F. EMSs and SMEs: Motivations, opportunities and barriers related to EMAs and ISO 14001 implementation. Greener Manag. Int. 2000, 29, 55–69. [Google Scholar] [CrossRef]

- Heras, I.; Arana, G. Alternative models for environmental management in SMEs: The case Ekoscan vs. ISO 14001. J. Clean. Prod. 2010, 18, 726–735. [Google Scholar] [CrossRef]

- European Commission. EMAS “Easy” for Small and Medium Enterprises; The European Eco-Management and Audit Scheme [EMAS]; European Commission: Brussels, Belgium, 2007; pp. 1–36. [Google Scholar]

- International Organization for Standardization [ISO]. ISO 14001:2015-Environmental Management Systems-A Practical Guide for SMEs; ISO: Geneva, Switzerland, 2007; pp. 1–12. [Google Scholar]

- Miles, M.B.; Huberman, A.M.; Saldaña, J. Qualitative Data Analysis: A Methods Sourcebook; Sage Publications: London, UK, 2013. [Google Scholar]

- Guthrie, G. Basic Research Methods—An Entry to Social Science Research; SAGE Publications Ltd.: Thousand Oaks, CA, USA, 2010. [Google Scholar]

- Yin, R.K. (Ed.) Case Study Research: Design and Methods, 5th ed.; Sage Publications Ltd.: London, UK, 2014. [Google Scholar]

- Ritchie, J.; Lewis, J. Qualitative Research Practice: A Guide for Social Science Students and Researchers; Sage Publications Ltd.: London, UK, 2011. [Google Scholar]

- Kim, Y. Consumer Responses to the Food Industry’s Proactive and Passive Environmental CSR, Factoring in Price as CSR Trade off. J. Bus. Ethics 2017, 140, 307–321. [Google Scholar] [CrossRef]

- Maloni, M.; Brown, M. Corporate social responsibility in the supply chain: An application in the food industry. J. Bus. Ethics 2006, 68, 35–52. [Google Scholar] [CrossRef]

- Chen, Y.-H.; Wen, X.-W.; Luo, M.-Z. Corporate Social Responsibility Spillover and Competition Effects on the Food Industry. Aust. Econ. Pap. 2016, 55, 1–13. [Google Scholar] [CrossRef]

- FoodDrink Europe. Data & Trends: EU Food and Drink Industry; FoodDrink Europe: Brussels, Belgium, 2017. [Google Scholar]

- Blažková, I.; Dvouletý, O. Investigating the differences in entrepreneurial success through the firm-specific factors: Microeconomic evidence from the Czech food industry. J. Entrep. Emerg. Econ. 2019, 11, 154–176. [Google Scholar] [CrossRef]

- Hirsch, S.; Gschwandtner, A. Profit persistence in the food industry: Evidence from five European countries. Eur. Rev. Agric. Econ. 2013, 40, 741–759. [Google Scholar] [CrossRef]

- RobecoSAM. Country Sustainability Ranking. 2017. Available online: www.robecosam.com/en/sustainability-insights/about-sustainability/country-sustainability-ranking/ (accessed on 20 August 2019).

- Yale University. Environmental Performance Index, Country Rankings 2014. 2018. Available online: https://issuu.com/yaleepi/docs/2014_epi_report (accessed on 20 August 2019).

- Hofstede Insights. Compare Countries. 2018. Available online: https://www.hofstede-insights.com/product/compare-countries/ (accessed on 20 August 2019).

- Dyllick, T.; Muff, K. Clarifying the Meaning of Sustainable Business: Introducing a Typology from Business-As-Usual to True Business Sustainability. Organ. Environ. 2016, 29, 156–174. [Google Scholar] [CrossRef]

- Fossey, E.; Harvey, C.; McDermott, F.; Davidson, L. Understanding and evaluating qualitative Re-search. Aust. New Zealand J. Psychiatry 2002, 36, 717–732. [Google Scholar] [CrossRef] [PubMed]

- Wilson, J. (Ed.) Essentials of Business Research: A Guide to Doing Your Research Project, 2nd ed.; Sage Publications: London, UK, 2014. [Google Scholar]

- Saunders, M.; Lewis, P.; Tornhill, A. (Eds.) Research Methods for Business Students, 7th ed.; Pearson: London, UK, 2016. [Google Scholar]

- Braun, V.; Clarke, V. Successful Qualitative Research. A practical guide for Beginners; Sage Publications Ltd.: London, UK, 2013. [Google Scholar]

- Porter, M.E.; van der Linde, C. Green and competitive. Harv. Bus. Rev. 1995, 73, 120–134. [Google Scholar]

- Global Reporting Initiative. New GRI Booklet Gives SMEs a Helping Hand; Global Reporting Initiative: Amsterdam, The Netherlands, 2014. [Google Scholar]

| Interviewee. | Statement |

|---|---|

| Expert 1 | Regarding the challenges which many of the case companies claimed to have faced, expert 1 emphasized that “by having an intrinsic motivation to integrate sustainability topics into the management system, into the culture and whatever […] If that is the case, they will not avoid the difficulties, but they are willing to tackle them” |

| Expert 2 | Expert 2 claimed that challenges, such as the limited resources of SMEs or the lack of CSR skills and knowledge within the company, “are only functions of how someone within the organization, namely the owner or the management, perceives the relevance of sustainability”. |

| Expert 6 | “The commitment has to be there from the top management level. […]. This differentiates successful from not successful companies; it has to be established at the top levels. Furthermore, I think it is really important that thereafter it is lived.” |

| Expert 7 | “The manager or owner has to be determined and committed to hold on to sustainability practices, even when the balance sheet and the income statement speak another language.” |

| Interviewee | Statement |

|---|---|

| Expert 2 | “If you have a reward system which is not congruent with your goals, you won’t get anywhere. Whatever is rewarded, is what will be done in the end.” |

| Expert 3 | Only once these strategic measures are successfully established and the tasks implemented, monitored and measured, then “it’s a value you can integrate much better into the financial reporting”. |

| Expert 6 | Expert 6 while referring to the credibility of a firm stated that this “can only be achieved if CSR is not only being executed internally within the company, but when it is being talked about towards the outside. I personally, think this is the goal.” |

| Expert 7 | When talking about the reasoning behind the establishment of sustainability reports, expert 7 elaborated that these reports reflect the “business success, which goes beyond the standard balance sheet”. |

| Interviewee. | Statement |

|---|---|

| Expert 2 | Expert 2 when referring to standardized CSR guidelines: “If you are a SME your influence, your leverage is limited, hence you don’t have to fulfil everything”. “Do not play it by the book, play it in a way that it really makes sense for your organization […]”. |

| Expert 3 | Explaining the reason behind the creation of adapted CSR standards; rating agencies are “mostly focused on selling these to certain institutions.” |

| Expert 6 | Regarding how CSR is executed in companies: “It is only bureaucratic if I execute it bureaucratically”. Further expert 6 explained that key was to quantify the stage at which the company is with its CSR efforts and to break down the future path into “possible and manageable” steps. |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Elford, A.C.; Daub, C.-H. Solutions for SMEs Challenged by CSR: A Multiple Cases Approach in the Food Industry within the DACH-Region. Sustainability 2019, 11, 4758. https://doi.org/10.3390/su11174758

Elford AC, Daub C-H. Solutions for SMEs Challenged by CSR: A Multiple Cases Approach in the Food Industry within the DACH-Region. Sustainability. 2019; 11(17):4758. https://doi.org/10.3390/su11174758

Chicago/Turabian StyleElford, Angélique Catharina, and Claus-Heinrich Daub. 2019. "Solutions for SMEs Challenged by CSR: A Multiple Cases Approach in the Food Industry within the DACH-Region" Sustainability 11, no. 17: 4758. https://doi.org/10.3390/su11174758

APA StyleElford, A. C., & Daub, C. -H. (2019). Solutions for SMEs Challenged by CSR: A Multiple Cases Approach in the Food Industry within the DACH-Region. Sustainability, 11(17), 4758. https://doi.org/10.3390/su11174758