Corporate Social Responsibility Practices in China: Trends, Context, and Impact on Company Performance

Abstract

:1. Introduction

2. Methodological Approach

3. CSR in China: Performance, Trend, and Context

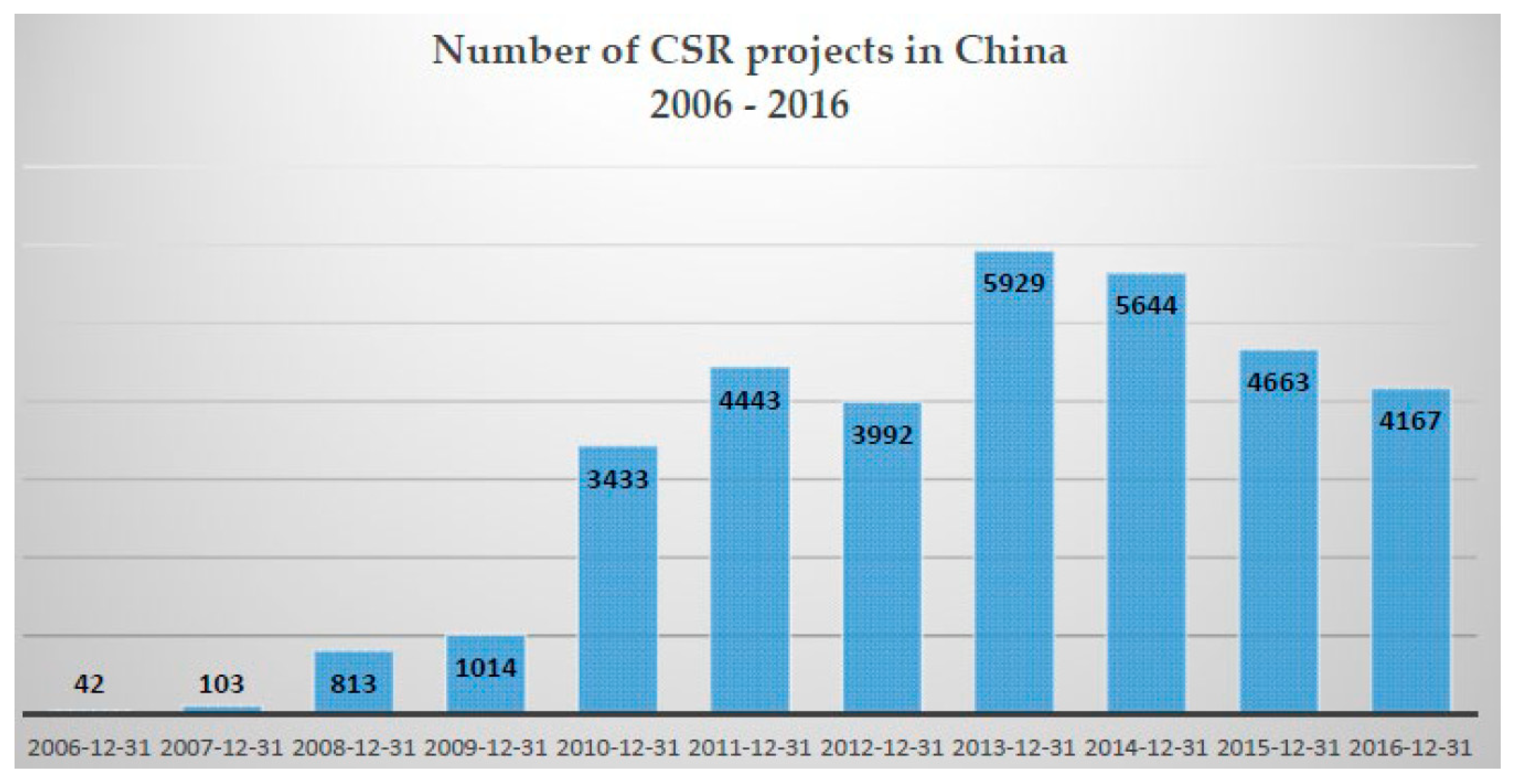

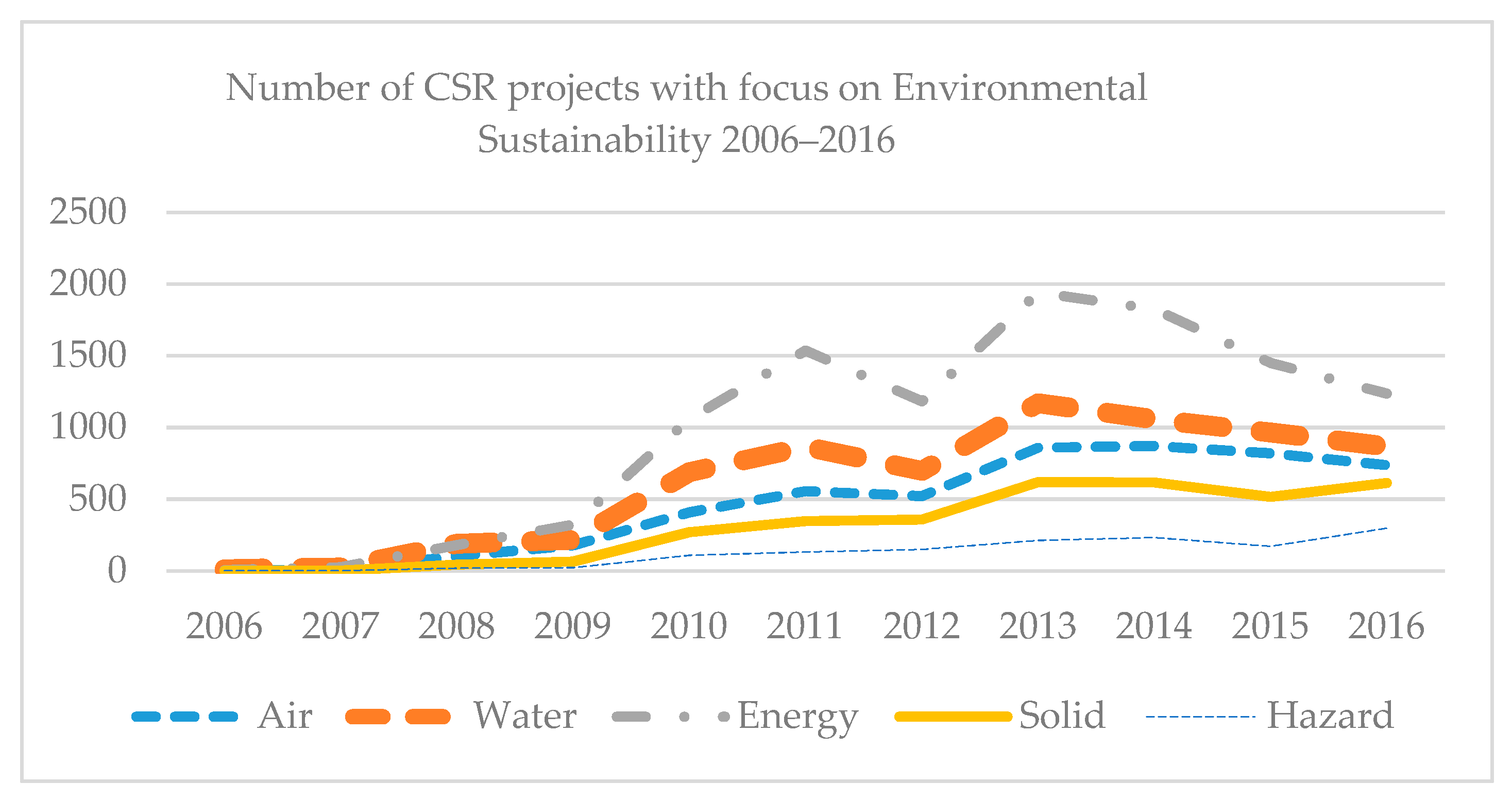

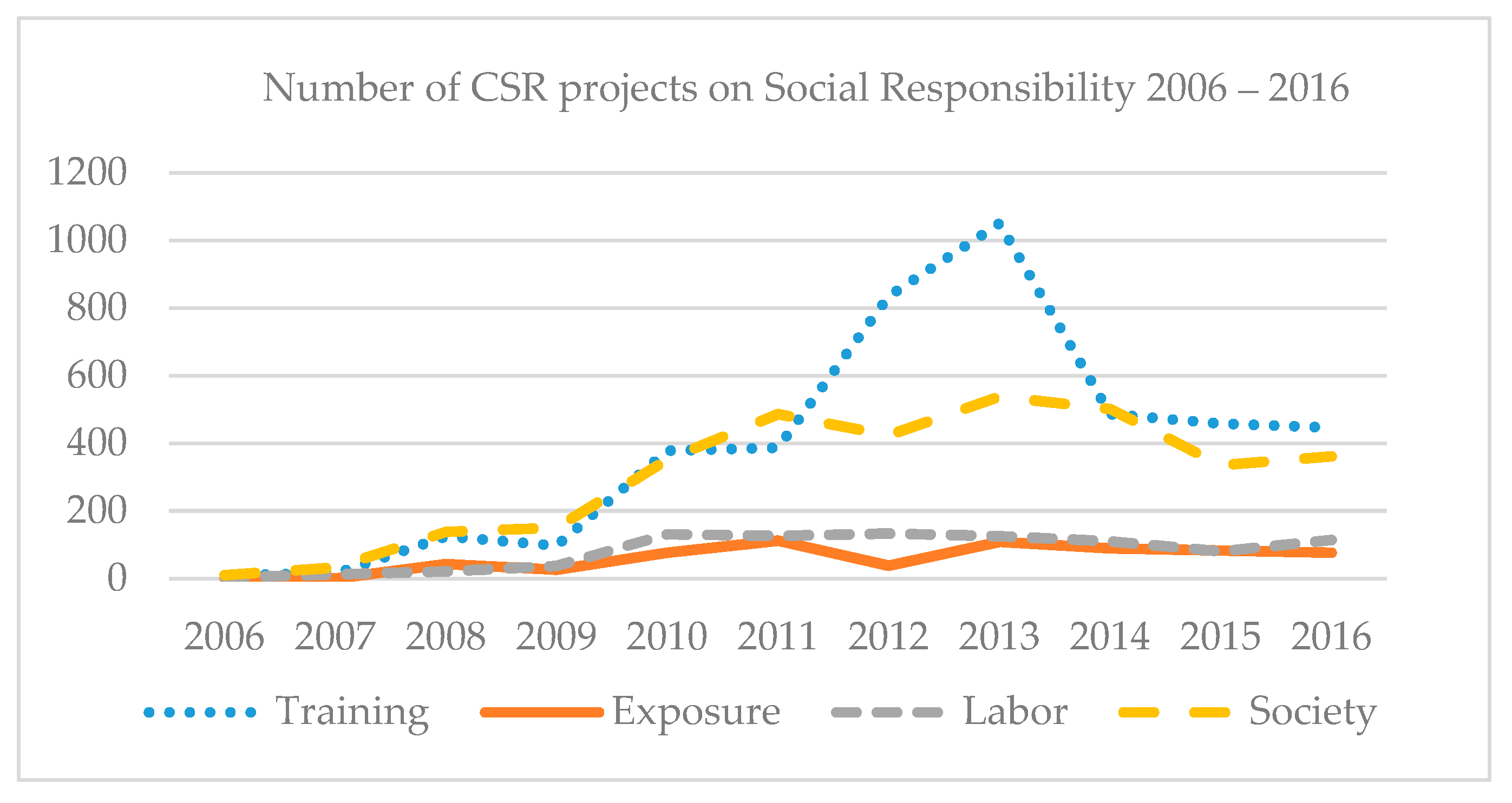

3.1. Trends and Numbers of CSR Projects

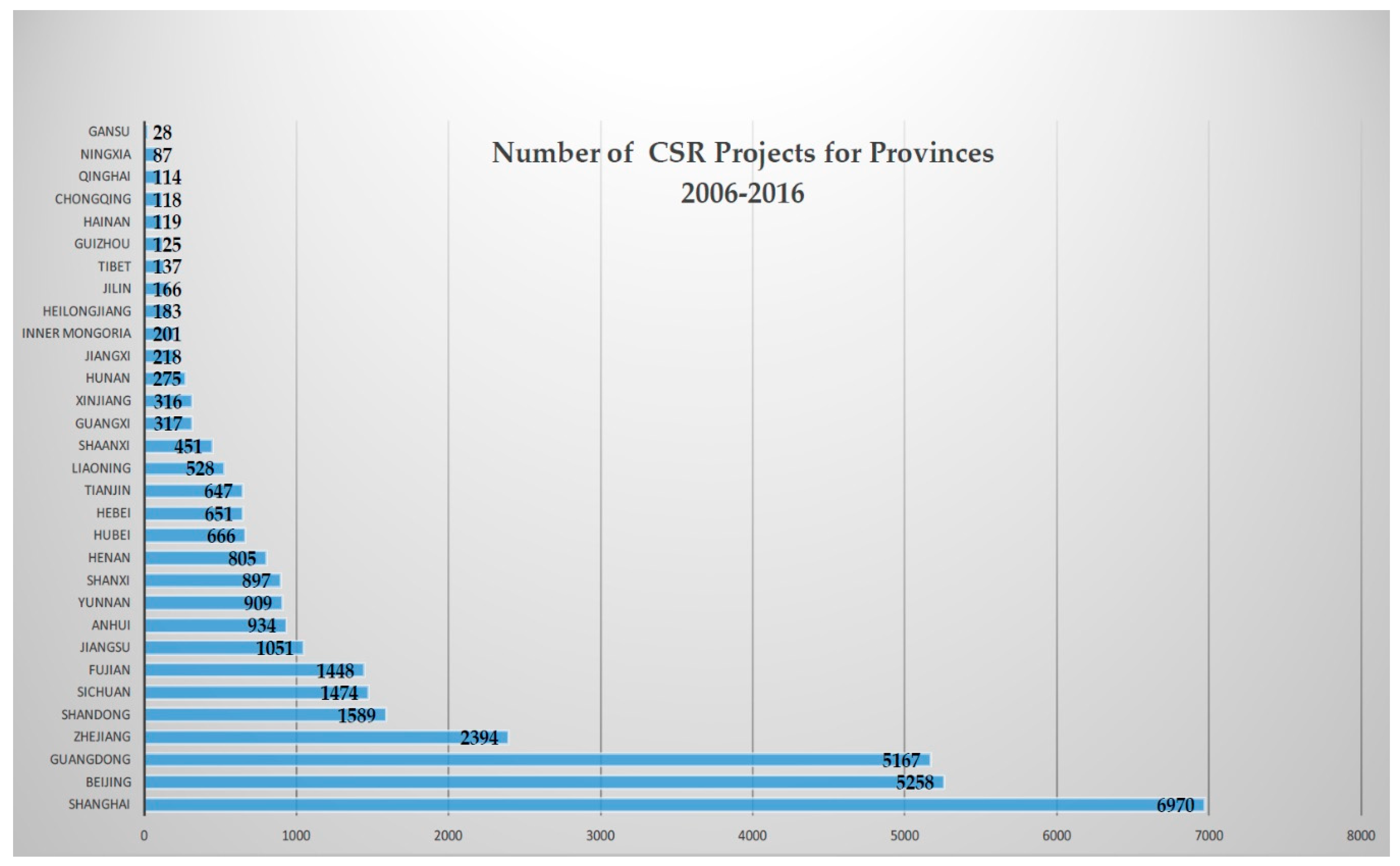

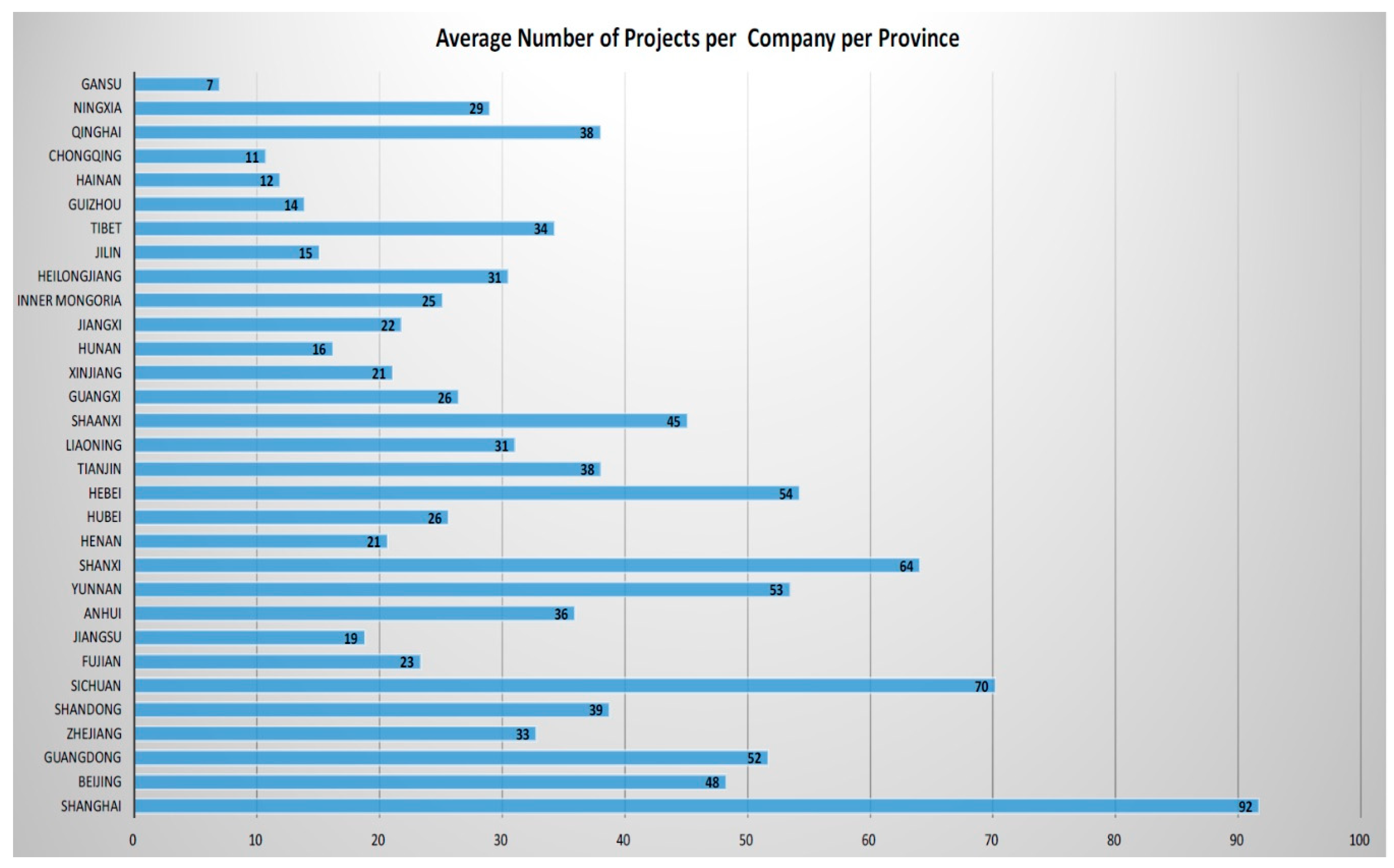

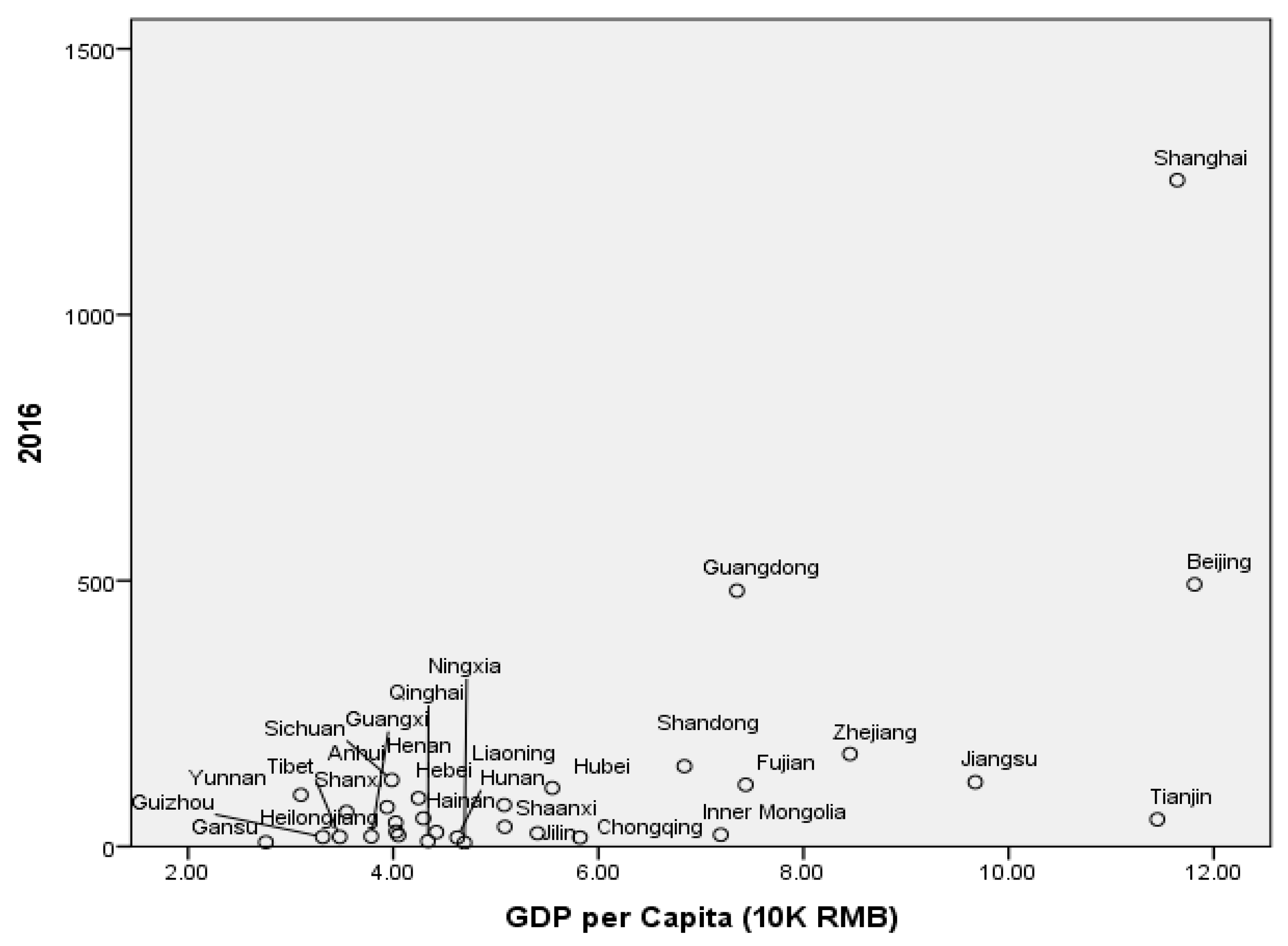

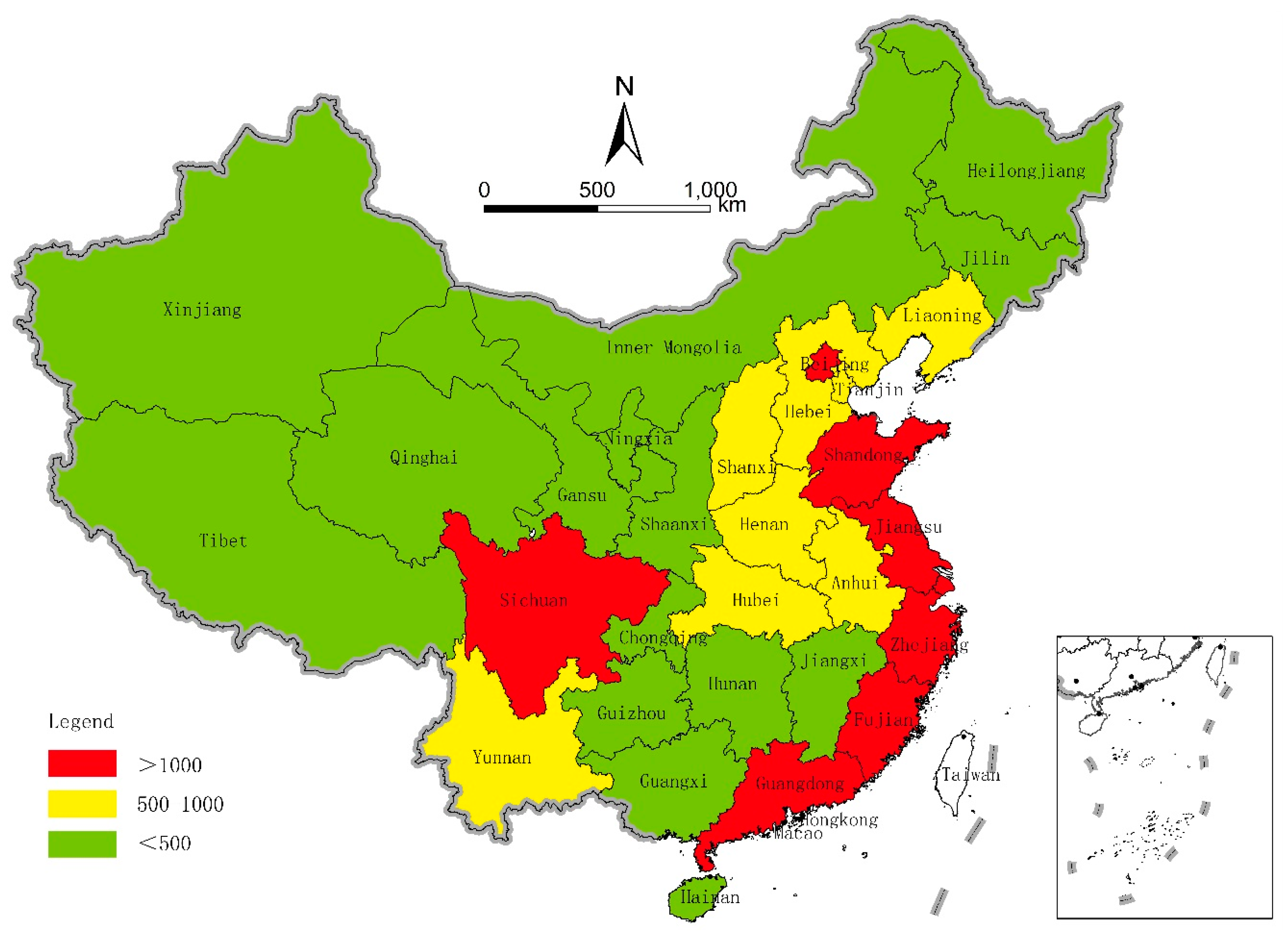

3.2. Context Analysis of CSR Projects

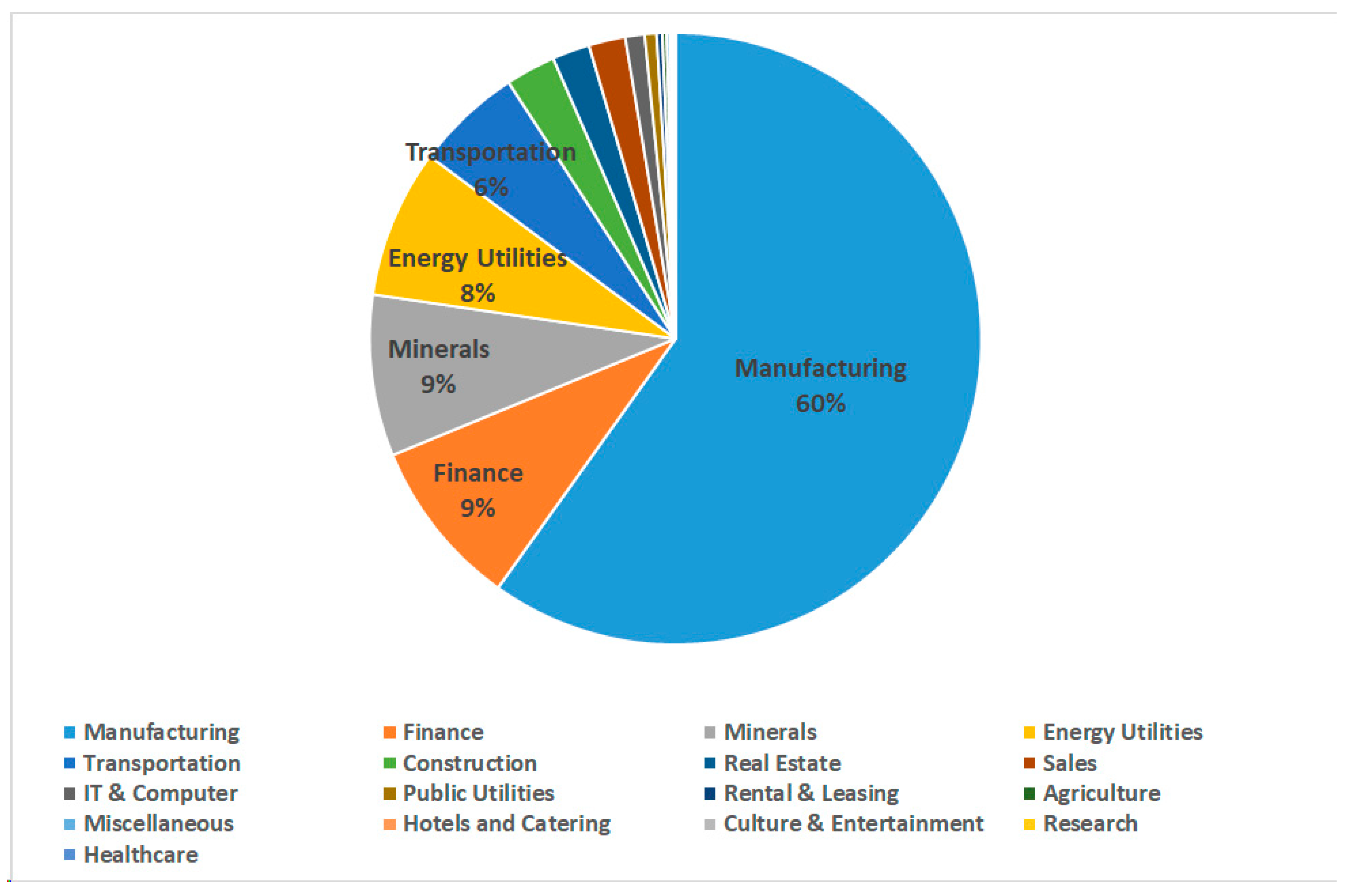

4. CSR on Corporate Performance

4.1. Test of Hypothesis 1

- For each company i in year t, we count the number of CSR projects, NumCSRi,t, to measure the extent of participation. A larger value of NumCSRi,t indicates a greater initiative in CSR and sustainability.

- For each company i in year t, we use to represent the total asset.

- For each company i in year t, we use to present the annual revenue from main business.

- For each company i in year t, we use to present the effective tax rate.

- For each company i in year t, we use to present the number of employees.

4.2. Test of Hypothesis 2

- CP1: environmentally sound products and packaging

- CP2: non-polluting production

- CP3: production energy efficiency

- CP4: safe and healthy work environments

- CP5: waste reduction.

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Hamann, R. Mining companies’ role in sustainable development: The ‘why’ and ‘how’ of corporate social responsibility from a business perspective. Dev. S. Afr. 2003, 20, 237–254. [Google Scholar] [CrossRef]

- Rasche, A.; Morsing, M.; Moon, J. The changing role of business in global society: CSR and beyond. In Corporate Social Responsibility: Strategy, Communication and Governance; Cambridge University Press: Cambridge, UK, 2017; pp. 1–28. [Google Scholar]

- Elkington, J. Towards the sustainable corporation: Win-win-win business strategies for sustainable development. Calif. Manag. Rev. 1994, 36, 90–100. [Google Scholar] [CrossRef]

- Laszlo, C.; Cescau, P. Sustainable Value: How the World’s Leading Companies are Doing Well by Doing Good; Routledge: Abingdon, UK, 2017. [Google Scholar]

- Thorlakson, T.; de Zegher, J.F.; Lambin, E.F. Companies’ contribution to sustainability through global supply chains. Proc. Natl. Acad. Sci. USA 2018, 115, 2072–2077. [Google Scholar] [CrossRef] [PubMed]

- Ritala, P.; Huotari, P.; Bocken, N.; Albareda, L.; Puumalainen, K. Sustainable business model adoption among S&P 500 firms: A longitudinal content analysis study. J. Clean. Prod. 2018, 170, 216–226. [Google Scholar]

- Lin, L.W. Corporate social responsibility in China: Window dressing or structural change. Berkeley J. Int. Law 2010, 28, 64. [Google Scholar]

- Gray, R.; Kouhy, R.; Lavers, S. Corporate social and environmental projecting: A review of the literature and a longitudinal study of UK disclosure. Account. Audit. Account. J. 1995, 8, 47–77. [Google Scholar] [CrossRef]

- Global Projecting Initiative (GRI). Sustainability Projecting Guidelines; GRI: Amsterdam, The Netherlands, 2011. [Google Scholar]

- Qiu, Y.; Shaukat, A.; Tharyan, R. Environmental and social disclosures: Link with corporate financial performance. Br. Account. Rev. 2016, 48, 102–116. [Google Scholar] [CrossRef] [Green Version]

- Klynveld Peat Marwick Goerdeler (KPMG). The KPMG Survey of Corporate Social Responsibility Reporting; KPMG: London, UK, 2011; Available online: https://www.kpmg.de/docs/Survey-corporate-responsibility-reporting-2011.pdf (accessed on 7 January 2019).

- Van Marrewijk, M. Concepts and definitions of CSR and corporate sustainability: Between agency and communion. J. Bus. Ethics 2003, 44, 95–105. [Google Scholar] [CrossRef]

- O’Riordan, L.; Fairbrass, J. Corporate social responsibility (CSR): Models and theories in stakeholder dialogue. J. Bus. Ethics 2008, 83, 745–758. [Google Scholar] [CrossRef]

- Tang, Y.; Ma, Y.; Wong, C.W.; Miao, X. Evolution of government policies on guiding corporate social responsibility in China. Sustainability 2018, 10, 741. [Google Scholar] [CrossRef]

- Babiak, K.; Trendafilova, S. CSR and environmental responsibility: Motives and pressures to adopt green management practices. Corp. Soc. Responsib. Environ. Manag. 2011, 18, 11–24. [Google Scholar] [CrossRef]

- Hens, L.; Block, C.; Cabello-Eras, J.J.; Sagastume-Gutierez, A.; Garcia-Lorenzo, D.; Chamorro, C.; Vandecasteele, C. On the evolution of “Cleaner Production” as a concept and a practice. J. Clean. Prod. 2018, 172, 3323–3333. [Google Scholar] [CrossRef]

- Fresner, J. Cleaner production as a means for effective environmental management. J. Clean. Prod. 1998, 6, 171–179. [Google Scholar] [CrossRef]

- Yüksel, H. An empirical evaluation of cleaner production practices in Turkey. J. Clean. Prod. 2008, 16, S50–S57. [Google Scholar] [CrossRef]

- Tseng, M.L.; Lin, Y.H.; Chiu, A.S.F.; Liao, J.C.H. Using FANP approach on selection of competitive priorities based on cleaner production implementation: A case study in PCB manufacturer, Taiwan. Clean Technol. Environ. Policy 2008, 10, 17–29. [Google Scholar] [CrossRef]

- Tseng, M.L.; Lin, Y.H.; Chiu, A.S.F. Fuzzy AHP-based study of cleaner production implementation in Taiwan PWB manufacturer. J. Clean. Prod. 2009, 17, 1249–1256. [Google Scholar] [CrossRef]

- Pimenta, H.C.D.; Gouvinhas, R.P. Cleaner Production as a Corporate Sustainability Tool: An Exploratory Discussion. 2011. Available online: http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.663.948&rep=rep1&type=pdf (accessed on 9 January 2019).

- Zeng, S.X.; Meng, X.H.; Yin, H.T.; Tam, C.M.; Sun, L. Impact of cleaner production on business performance. J. Clean. Prod. 2010, 18, 975–983. [Google Scholar] [CrossRef]

- Deegan, C.; Gordon, B. A study of the environmental disclosure practices of Australian corporations. Account. Bus. Res. 1996, 26, 187–199. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Li, Y.; Richardson, G.D.; Vasvari, F.P. Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Account. Organ. Soc. 2008, 33, 303–327. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Li, Y.; Richardson, G.D.; Vasvari, F.P. Does it really pay to be green? Determinants and consequences of proactive environmental strategies. J. Account. Public Policy 2011, 30, 122–144. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Fang, X.; Li, Y.; Richardson, G. The relevance of environmental disclosures: Are such disclosures incrementally informative? J. Account. Public Policy 2013, 32, 410–431. [Google Scholar] [CrossRef]

- López-Gamero, M.D.; Molina-Azorín, J.F.; Claver-Cortés, E. The whole relationship between environmental variables and firm performance: Competitive advantage and firm resources as mediator variables. J. Environ. Manag. 2009, 90, 3110–3121. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Molina-Azorín, J.F.; Claver-Cortés, E.; Pereira-Moliner, J.; Tarí, J.J. Environmental practices and firm performance: An empirical analysis in the Spanish hotel industry. J. Clean. Prod. 2009, 17, 516–524. [Google Scholar] [CrossRef]

- Wagner, M. How to reconcile environmental and economic performance to improve corporate sustainability: Corporate environmental strategies in European paper industry. J. Environ. Manag. 2005, 76, 105–118. [Google Scholar] [CrossRef] [PubMed]

- Sarkis, J.; Dijkshoorn, J. Relationships between solid waste management performance and environmental practice adoption in Welsh small and medium-sized enterprises (SMEs). Int. J. Prod. Res. 2007, 45, 4989–5015. [Google Scholar] [CrossRef]

- Aupperle, K.E.; Carroll, A.B.; Hatfield, J.D. An empirical examination of the relationship between corporate social responsibility and profitability. Acad. Manag. J. 1985, 28, 446–463. [Google Scholar]

- McGuire, J.B.; Sundgren, A.; Schneeweis, T. Corporate social responsibility and firm financial performance. Acad. Manag. J. 1988, 31, 854–872. [Google Scholar]

- McWilliams, A.; Siegel, D. Corporate social responsibility: A theory of the firm perspective. Acad. Manag. Rev. 2001, 26, 117–127. [Google Scholar] [CrossRef]

- Barnett, M.L. Stakeholder influence capacity and the variability of financial returns to corporate social responsibility. Acad. Manag. Rev. 2007, 32, 794–816. [Google Scholar] [CrossRef]

- Tixier, M. Will sustainable management be a clear differentiator for tour operators? Anatolia 2009, 20, 461–466. [Google Scholar] [CrossRef]

- Tziner, A. Corporative social responsibility (CSR) activities in the workplace: A comment on Aguinis and Glavas (2013). Revista de Psicología del Trabajo y de las Organizaciones 2013, 29, 91–93. [Google Scholar] [CrossRef] [Green Version]

- Cheng, B.; Ioannou, I.; Serafeim, G. Corporate social responsibility and access to finance. Strateg. Manag. J. 2014, 35, 1–23. [Google Scholar] [CrossRef]

- Warshawsky, D.N. Food waste, sustainability, and the corporate sector: Case study of a US food company. Geogr. J. 2016, 182, 384–394. [Google Scholar] [CrossRef]

- Yuan, X. Correction of Corporation Value Assessment Model Based on Corporate Social Responsibility. Agric. Sci. Technol. 2017, 18, 736–739. [Google Scholar]

- Hategan, C.D.; Sirghi, N.; Curea-Pitorac, R.I.; Hategan, V.P. Doing well or doing good: The relationship between corporate social responsibility and profit in Romanian companies. Sustainability 2018, 10, 1041. [Google Scholar] [CrossRef]

- Hawn, O.; Chatterji, A.K.; Mitchell, W. Do investors actually value sustainability? New evidence from investor reactions to the Dow Jones Sustainability Index (DJSI). Strateg. Manag. J. 2018, 39, 949–976. [Google Scholar] [CrossRef]

- Platonova, E.; Asutay, M.; Dixon, R.; Mohammad, S. The impact of corporate social responsibility disclosure on financial performance: Evidence from the GCC Islamic banking sector. J. Bus. Ethics 2018, 151, 451–471. [Google Scholar] [CrossRef]

- Halme, M.; Rintamäki, J.; Knudsen, J.S.; Lankoski, L.; Kuisma, M. When Is There a Sustainability Case for CSR? Pathways to Environmental and Social Performance Improvements. Bus. Soc. 2018. [Google Scholar] [CrossRef]

- Presley, A.; Presley, T.; Blum, M. Sustainability and company attractiveness: A study of American college students entering the job market. Sustain. Account. Manag. Policy J. 2018, 9, 470–489. [Google Scholar] [CrossRef]

- Dragomir, V.D. How do we measure corporate environmental performance? A critical review. J. Clean. Prod. 2018, 196, 1124–1157. [Google Scholar] [CrossRef]

- Chen, Y.C.; Hung, M.; Wang, Y. The effect of mandatory CSR disclosure on firm profitability and social externalities: Evidence from China. J. Account. Econ. 2018, 65, 169–190. [Google Scholar] [CrossRef]

- Feng, Y.; Chen, H.H.; Tang, J. The Impacts of Social Responsibility and Ownership Structure on Sustainable Financial Development of China’s Energy Industry. Sustainability 2018, 10, 301. [Google Scholar] [CrossRef]

- Anser, M.K.; Zhang, Z.; Kanwal, L. Moderating effect of innovation on corporate social responsibility and firm performance in realm of sustainable development. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 799–806. [Google Scholar] [CrossRef]

- Li, K. Reaction to News in the Chinese Stock Market: A Study on Xiong’an New Area Strategy. J. Behav. Exp. Financ. 2018, 19, 36–38. [Google Scholar] [CrossRef]

- Yu, A.; Gallagher, T.; Zhao, C.; Zhao, Y. Selecting Evaluation Indices for Cleaner Production of Plantation Logging in Southern China with Fuzzy Clustering Methods. Croat. J. Forest Eng. 2016, 37, 71–87. [Google Scholar]

- Khalili, N.R.; Cheng, W.; McWilliams, A. A methodological approach for the design of sustainability initiatives: In pursuit of sustainable transition in China. Sustain. Sci. 2017, 12, 933–956. [Google Scholar] [CrossRef]

- Jensen, M.C.; Meckling, W.H. Theory of the firm: Managerial behavior, agency costs and ownership structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef] [Green Version]

- Mohammadi, M.A.D.; Mardani, A.; Khan, A.; Azli, M.N.; Streimikiene, D. Corporate sustainability disclosure and market valuation in a Middle Eastern Nation: Evidence from listed firms on the Tehran Stock Exchange: Sensitive industries versus non-sensitive industries. Economic Research-Ekonomska Istraživanja 2018, 31, 1488–1511. [Google Scholar] [CrossRef]

- Jorion, P. Financial Risk Manager Handbook, 4th ed.; John Wiley & Sons: Hoboken NJ, USA, 2007; ISBN 978-0470904015. [Google Scholar]

- Gao, W.; Ng, L.; Wang, Q. Does geographic dispersion affect firm valuation? J. Corp. Finan. 2008, 14, 674–687. [Google Scholar] [CrossRef]

- Almazan, A.; Motta, A.D.; Titman, S.; Uysal, V. Financial structure, acquisition opportunities, and firm locations. J. Finan. 2010, 65, 529–563. [Google Scholar] [CrossRef]

- Garcia, D.; Norli, Ø. Geographic dispersion and stock return. J. Financ. Econ. 2012, 106, 547–565. [Google Scholar] [CrossRef]

- Shi, G.; Sun, J.; Luo, R. Geographic dispersion and earnings management. J. Account. Public Policy 2015, 34, 490–508. [Google Scholar] [CrossRef]

- Brealey, R.A.; Myers, S.C.; Allen, F. Principles of Corporate Finance, 12th ed.; 2012; ISBN 978-1259004650. Available online: https://s3.amazonaws.com/academia.edu.documents/31182842/DE001125555EA654126BCC12572DF00423B78.pdf?AWSAccessKeyId=AKIAIWOWYYGZ2Y53UL3A&Expires=1547172506&Signature=AyPzFn87mDigb7okd5e2YuYLVZw%3D&response-content-disposition=inline%3B%20filename%3DCorporate_finance.pdf (accessed on 11 January 2019).

- Hua, M.; A Personal Account of Life inside a Chinese Mining Company. China Dialogue. 2013. Available online: https://www.chinadialogue.net/article/show/single/en/6334-A-personal-account-of-life-inside-a-Chinese-mining-company (accessed on 7 January 2019).

- Al Mamun, M.; Sohag, K.; Shahbaz, M.; Hammoudeh, S. Financial markets, innovations and cleaner energy production in OECD countries. Energy Econ. 2018, 72, 236–254. [Google Scholar] [CrossRef] [Green Version]

- Lee, M.D.P. A review of the theories of corporate social responsibility: Its evolutionary path and the road ahead. Int. J. Manag. Rev. 2008, 10, 53–73. [Google Scholar] [CrossRef]

- Gatti, L.; Vishwanath, B.; Seele, P.; Cottier, B. Are we moving beyond voluntary CSR? Exploring theoretical and managerial implications of mandatory CSR resulting from the New Indian Companies Act. J. Bus. Ethics 2018, 1–12. Available online: https://doi.org/10.1007/s10551-018-3783-8 (accessed on 11 January 2019). [CrossRef]

- Chuang, S.P.; Huang, S.J. The effect of environmental corporate social responsibility on environmental performance and business competitiveness: The mediation of green information technology capital. J. Bus. Ethics 2018, 150, 991–1009. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Reference | Finding | Link |

|---|---|---|

| Aupperle, K. E., Carroll, A. B., & Hatfield, J. D. (1985). An Empirical Examination of the Relationship between Corporate Social Responsibility and Profitability. Academy of Management Journal, 28(2), 446–463. [31] | Using an elaborate, forced-choice instrument administered to corporate CEOs, did not find any relationship between social responsibility and profitability. Specifically, varying levels of social orientation were not found to correlate with performance differences | Published: 30 November 2017 https://doi.org/10.5465/256210 |

| McGuire, J. B., Sundgren, A., & Schneeweis, T. (1988). Corporate Social Responsibility and Firm Financial Performance. Academy of Management Journal, 31(4), 854–872. [32] | Firm’s prior performance, assessed by both stock-market returns and accounting-based measures, is related to corporate social responsibility | Published: 30 November 2017 https://doi.org/10.5465/256342 |

| McWilliams, A., & Siegel, D. (2001). Corporate Social Responsibility: A Theory of the Firm Perspective. Academy of Management Review, 26(1), 117–127. [33] | There is an ‘ideal’ level of CSR, which managers can determine via cost-benefit analysis, and a neutral relationship between CSR and financial performance | Published: 1 January 2001 https://doi.org/10.5465/amr.2001.4011987 |

| Barnett, M. L. (2007). Stakeholder Influence Capacity and the Variability of Financial Returns to Corporate Social Responsibility. Academy of Management Review, 32(3), 794–816. [34] | The impact of CSR on corporate social performance varies from one firm to another. Situational contingencies affect the relationship between CSR and firm financial performance | Published: 1 July 2007 https://journals.aom.org/doi/abs/10.5465/AMR.2007.25275520 |

| Tixier, M. (2009). Will Sustainable Management be a Clear Differentiator for Tour Operators? Anatolia, 20(2), 461–466. [35] | Studying the tourism industry revealed that CSR helps specialty tour operators attract customers and increase profitability in tourism business | Published: 25 June 2012 https://www.tandfonline.com/doi/abs/10.1080/13032917.2009.10518923?journalCode=rana20 |

| Tziner, A. (2013). Corporative Social Responsibility (CSR) Activities in the Workplace: A Comment on Aguinis and Glavas (2013). Revista de Psicología del Trabajo y de las Organizaciones, 29(2). [36] | CSR could improve employees’ productivity and thus increase firm’s profitability | Published: 2013 https://www.redalyc.org/html/2313/231328684007/ |

| Cheng, B., Ioannou, I., & Serafeim, G. (2014). Corporate Social Responsibility and Access to Finance. Strategic Management Journal, 35(1), 1–23. [37] | Corporations with better CSR performance have better access to finance and hence lower cost | Published: 05 April 2013 https://onlinelibrary.wiley.com/doi/abs/10.1002/smj.2131 |

| Warshawsky, D. N. (2016). Food Waste, Sustainability, and the Corporate Sector: Case Study of a US Food Company. The Geographical Journal, 182(4), 384–394. [38] | CSR (food waste management) generates some financial benefits in the U.S. food industry. However, it is not considered as important as corporate profitability | Published: 17 September 2015 https://rgs-ibg.onlinelibrary.wiley.com/doi/abs/10.1111/geoj.12156 |

| Yuan, X. (2017). Correction of Corporation Value Assessment Model Based on Corporate Social Responsibility. Agricultural Science & Technology, 18(4). [39] | Because the value and cost of CSR is difficult to access under the current accounting system, its impact on profitability is hard to measure | Published: April 2017 https://search.proquest.com/docview/1961708060?pq-origsite=gscholar |

| Hategan, C. D., Sirghi, N., Curea-Pitorac, R. I., & Hategan, V. P. (2018). Doing Well or Doing Good: The Relationship between Corporate Social Responsibility and Profit in Romanian Companies. Sustainability, 10(4), 1041. [40] | Companies that implement CSR are more profitable in economic terms | Published: 1 April 2018 https://www.mdpi.com/2071-1050/10/4/1041 |

| Hawn, O., Chatterji, A. K., & Mitchell, W. (2018). Do Investors Actually Value Sustainability? New Evidence from Investor Reactions to the Dow Jones Sustainability Index (DJSI). Strategic Management Journal, 39(4), 949–976. [41] | Firms may gain at least limited benefits from reliable CSR activities | Published: 12 December 2017 https://onlinelibrary.wiley.com/doi/abs/10.1002/smj.2752 |

| Platonova, E., Asutay, M., Dixon, R., & Mohammad, S. (2018). The Impact of Corporate Social Responsibility Disclosure on Financial Performance: Evidence from the GCC Islamic Banking Sector. Journal of Business Ethics, 151(2), 451–471. [42] | CSR disclosure has a significant positive relationship with the financial performance | Published: August 2018 https://link.springer.com/article/10.1007/s10551-016-3229-0 |

| Halme, M., Rintamäki, J., Knudsen, J. S., Lankoski, L., & Kuisma, M. (2018). When Is There a Sustainability Case for CSR? Pathways to Environmental and Social Performance Improvements. Business & Society, 0007650318755648. [43] | Integrating social responsibility into the core business results in improving social performance | Published: 21 March 2018 https://journals.sagepub.com/doi/abs/10.1177/0007650318755648 |

| Presley, A., Presley, T., & Blum, M. (2018). Sustainability and Company Attractiveness: A Study of American College Students Entering the Job Market. Sustainability Accounting, Management and Policy Journal. [44] | Sustainability performance is an important factor in determining the attractiveness of a company to potential applicants | Published: 2018 https://www.emeraldinsight.com/doi/abs/10.1108/SAMPJ-03-2017-0032 |

| Voicu, D. Dragomir. (2018). How Do We Measure Corporate Environmental Performance? A Critical Review. Journal of Cleaner Production 196, 1124–1157. [45] | A critical review of 172 papers is provided and new definition is given for corporate goals and reducing and preventing environmental harm | Published: 2018 https://doi.org/10.1016/j.jclepro.2018.06.014 |

| Chen, Y.C., Hung, M. and Wang, Y. (2018). The Effect of Mandatory CSR Disclosure on Firm Profitability and Social Externalities: Evidence from China. Journal of Accounting and Economics, 65(1), pp.169–190. [46] | Although the CSR reporting mandate in 2008 does not require firms to spend on CSR, they experience a decrease in profitability subsequent to the mandate | Published: 2018 https://doi.org/10.1016/j.jacceco.2017.11.009 |

| Feng, Y., Chen, H.H. and Tang, J. (2018). The Impacts of Social Responsibility and Ownership Structure on Sustainable Financial Development of China’s Energy Industry. Sustainability (2071–1050), 10(2). [47] | Chinese energy companies should pay more attention to improving corporate social responsibility to maintain good economic performance and develop sustainable competitive advantage | Published: 2018 https://www.mdpi.com/2071-1050/10/2/301 |

| Anser, M.K., Zhang, Z. and Kanwal, L. (2018). Moderating Effect of Innovation on Corporate Social Responsibility and Firm Performance in Realm of Sustainable Development. Corporate Social Responsibility and Environmental Management, 25(5), pp.799–806. [48] | Significant direct relationship exists among CSR, innovation, and firm performance while moderating effect of innovation is absent between CSR and firm performance | Published: 2018 https://doi.org/10.1002/csr.1495 |

| Panel A. Environmental Sustainability | |||||

| Air | Water | Energy | Solid | Hazard | |

| Number | 5070 | 6753 | 10,765 | 3451 | 1349 |

| Percentage | 16.30% | 21.70% | 34.60% | 11.10% | 4.30% |

| Panel B. Social Responsibility | |||||

| Training | Exposure | Labor | Society | ||

| Number | 4286 | 651 | 892 | 3327 | |

| Percentage | 13.80% | 2.10% | 2.90% | 10.70% | |

| EPS | Overall | High-CSR Regions | Mid-CSR Regions | Low-CSR Regions |

|---|---|---|---|---|

| NumCSR | 0.13 * | 0.14 * | 0.12 * | 0.07 |

| Size | 0.15 * | 0.18 * | −0.09 | 0.26 * |

| Revenue | 0.36 * | 0.42 * | 0.18 * | 0.03 |

| Tax | −0.05 * | −0.03 | −0.13 * | −0.03 |

| Employment | −0.43 * | −0.50 * | −0.08 | −0.12 * |

| NCF | Overall |

|---|---|

| CP1 | −0.01 |

| CP2 | 0.10 * |

| CP3 | 0.27 * |

| CP4 | −0.02 |

| CP5 | −0.22 * |

| NCF | Manufactures | Finance | Minerals | Energy Utilities | Transportation | Other |

|---|---|---|---|---|---|---|

| CP1 | −0.18 * | 0.04 | 0.18 * | −0.11 | −0.19 | −0.09 |

| CP2 | 0.04 | −0.07 | −0.10 | −0.08 | 0.00 | −0.03 |

| CP3 | 0.20 * | 0.40 * | 0.17 | 0.82 * | 0.64 * | 0.58 |

| CP4 | 0.02 | 0.13 | 0.11 | −0.11 | −0.08 | 0.01 |

| CP5 | 0.07 | −0.14 | −0.09 | −0.49 * | −0.10 | −0.45 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, K.; Khalili, N.R.; Cheng, W. Corporate Social Responsibility Practices in China: Trends, Context, and Impact on Company Performance. Sustainability 2019, 11, 354. https://doi.org/10.3390/su11020354

Li K, Khalili NR, Cheng W. Corporate Social Responsibility Practices in China: Trends, Context, and Impact on Company Performance. Sustainability. 2019; 11(2):354. https://doi.org/10.3390/su11020354

Chicago/Turabian StyleLi, Kun, Nasrin R. Khalili, and Weiquan Cheng. 2019. "Corporate Social Responsibility Practices in China: Trends, Context, and Impact on Company Performance" Sustainability 11, no. 2: 354. https://doi.org/10.3390/su11020354

APA StyleLi, K., Khalili, N. R., & Cheng, W. (2019). Corporate Social Responsibility Practices in China: Trends, Context, and Impact on Company Performance. Sustainability, 11(2), 354. https://doi.org/10.3390/su11020354