Relationship between Corporate Sustainability and Compliance with State-Owned Enterprises in Central-Europe: A Case Study from Hungary

Abstract

:1. Introduction

2. Key Aspects of Corporate Compliance

- the objectives pursued in setting up the business in question;

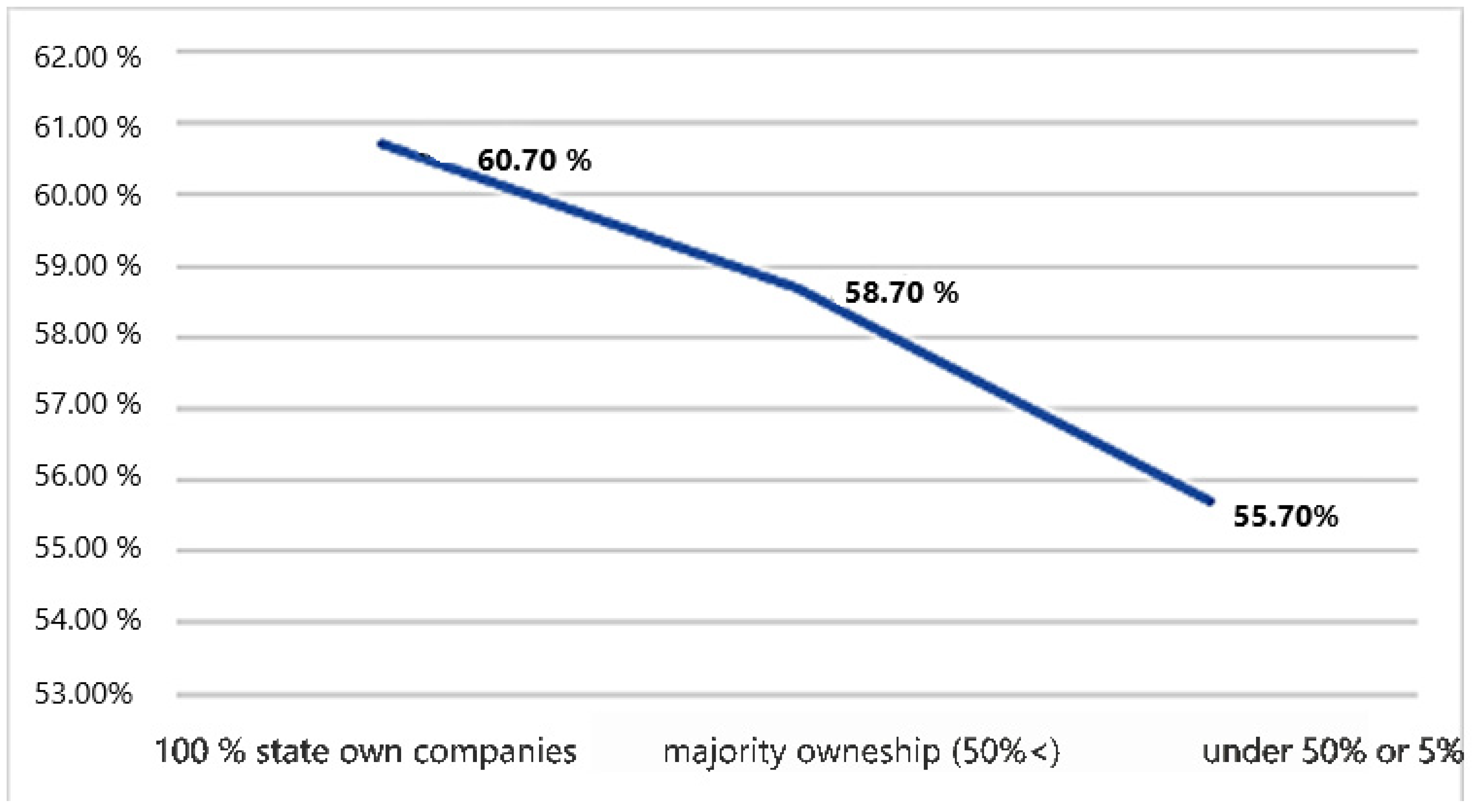

- ownership, sometimes at the governmental level, together with regulators at the policy (sector) level;

- compliance with standards;

- meeting the expectations of the public service users;

- compliance with the organization’s short-, medium- and long-term strategic objectives;

- it also represents compliance with corporate values for managers and employees.

3. Overview of the Compliance Environment for Hungarian State-Owned Enterprises

- to carry out the activities in the course of their operation and management in a regular, economic, efficient and effective manner;

- to comply with clearing obligations and protect resources from loss, damage and improper use.

- control environment,

- an integrated risk management system,

- control activities,

- information and communication system, and

- monitoring system design, operation and development.

4. Materials and Methods

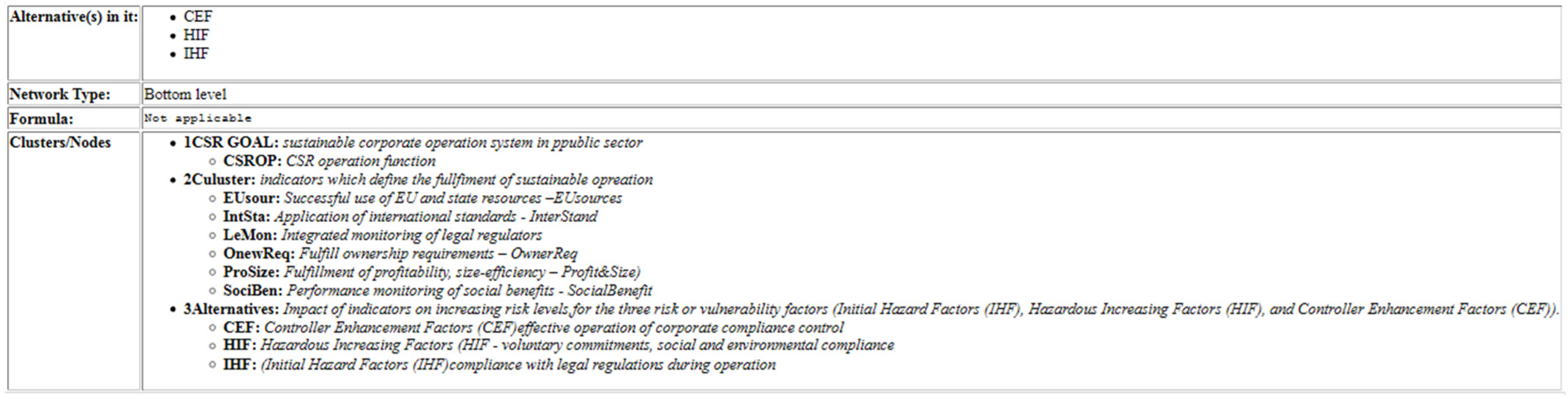

- 1. Goal: CSR operation;

- 2. Alternatives: IHFs, HIFs and CEFs;

- 3. Aspects: a, b, c, d, e, f:

- a-

- Integrated monitoring of legal regulators (LeMon),

- b-

- Fulfillment of profitability, size-efficiency (ProSize),

- c-

- Fulfill ownership requirements (OwnReq),

- d-

- Application of international standards (IntSta),

- e-

- Performance monitoring of social benefits (SociBen), and

- f-

- Successful use of EU and state resources (EUsour).

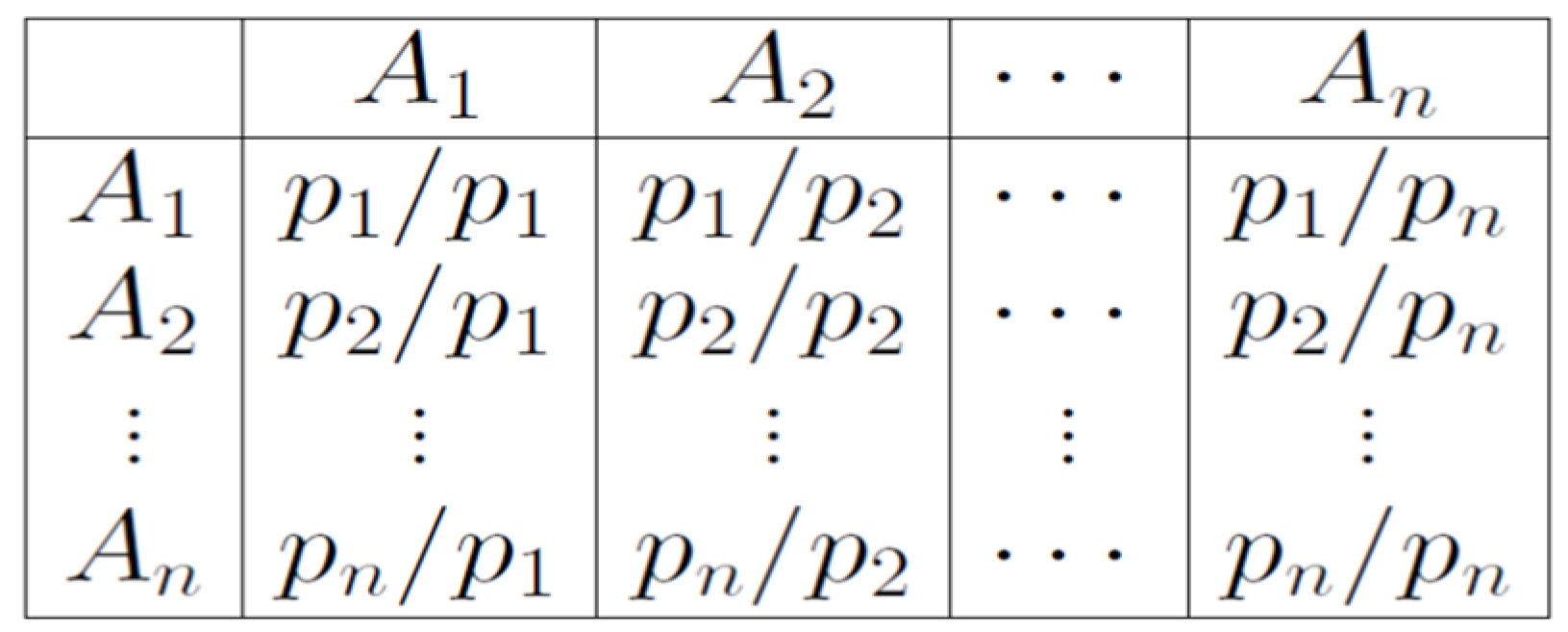

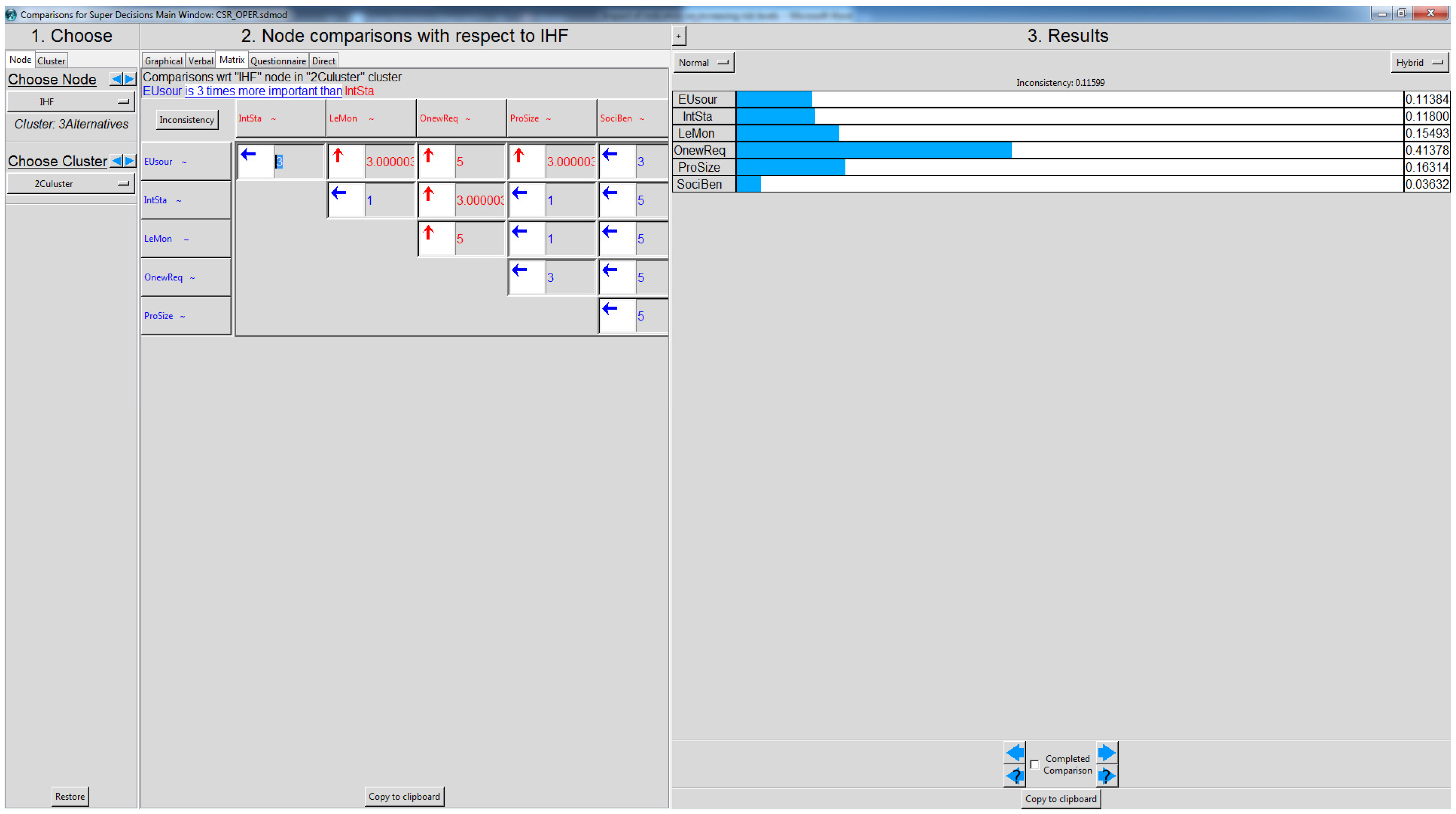

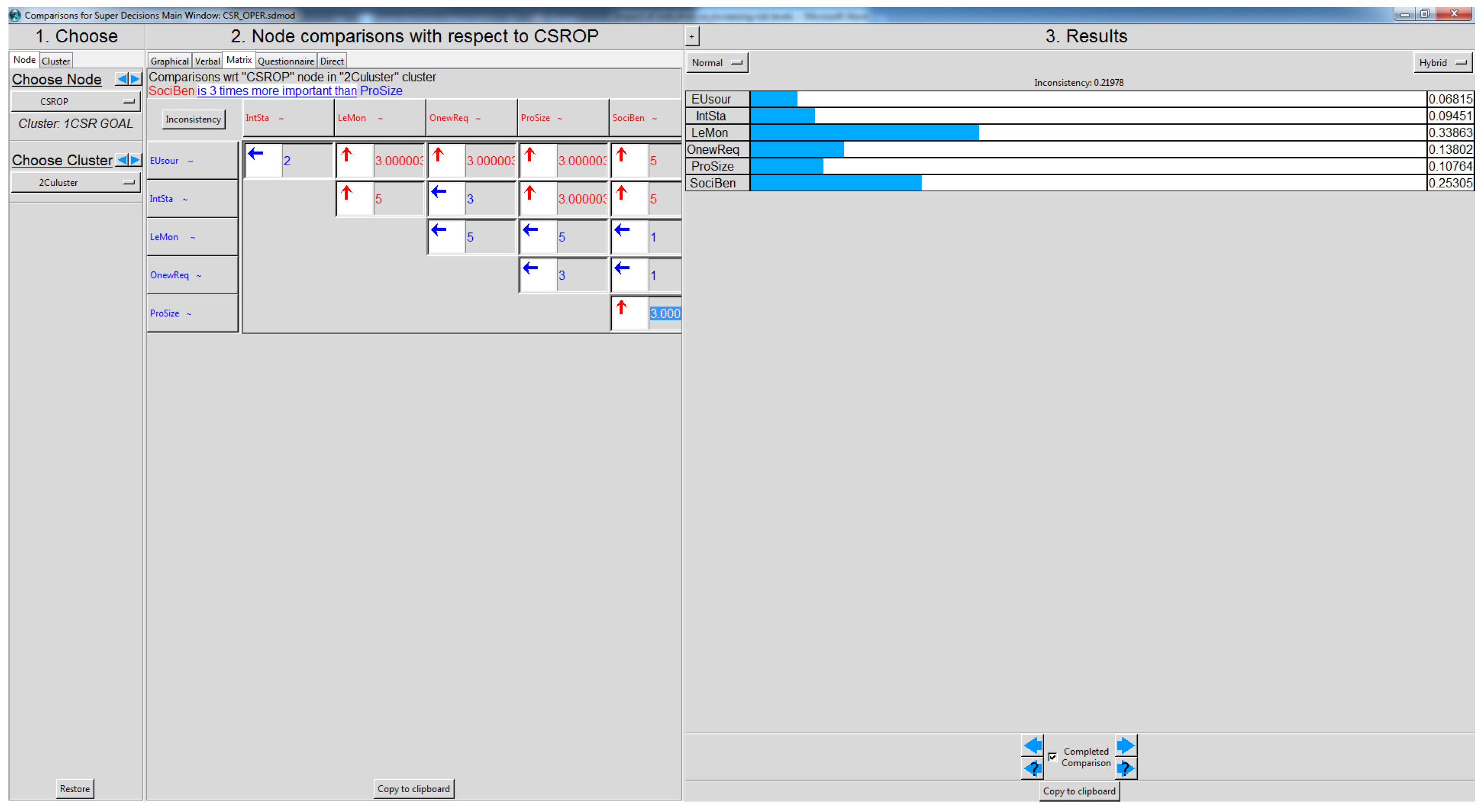

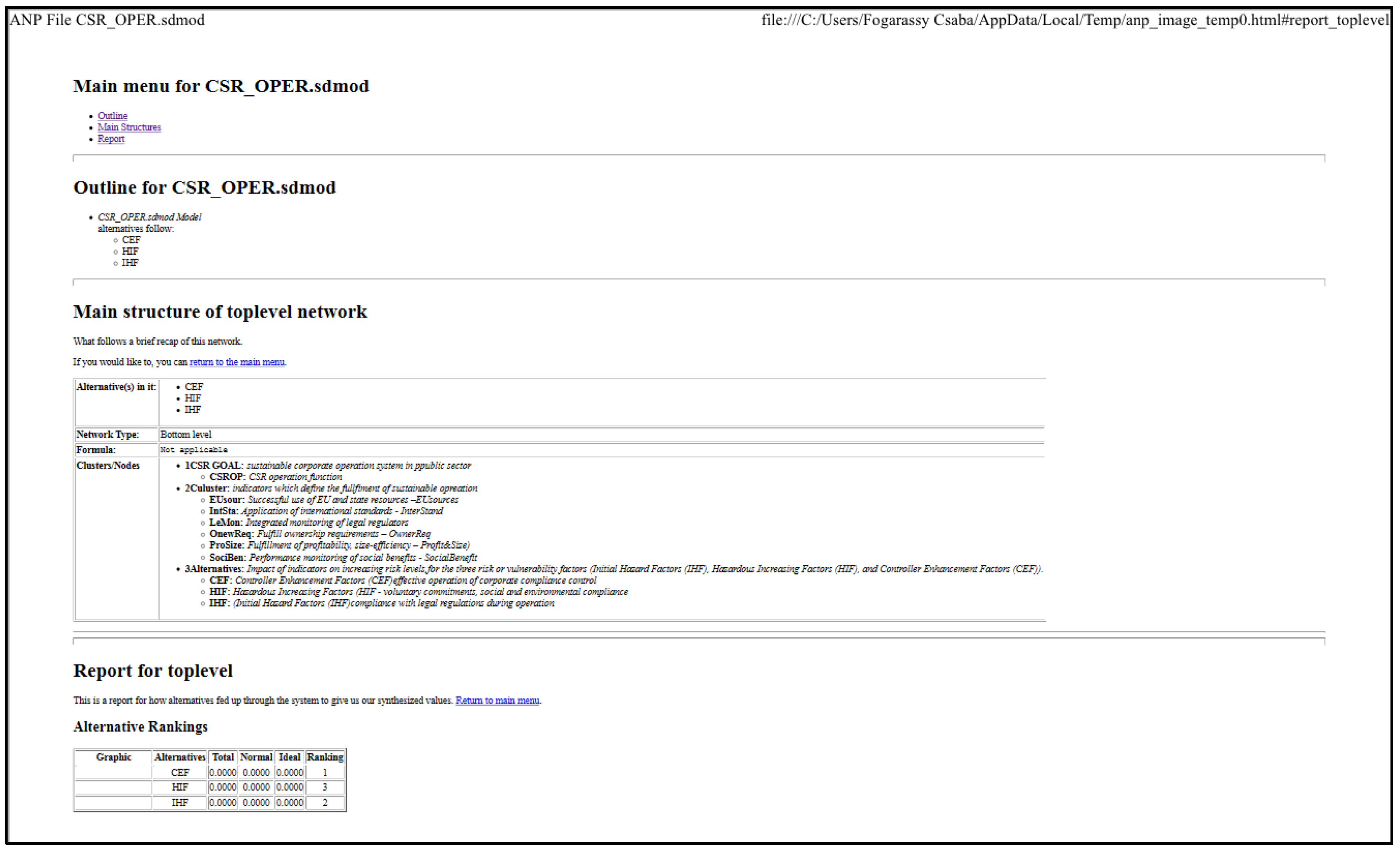

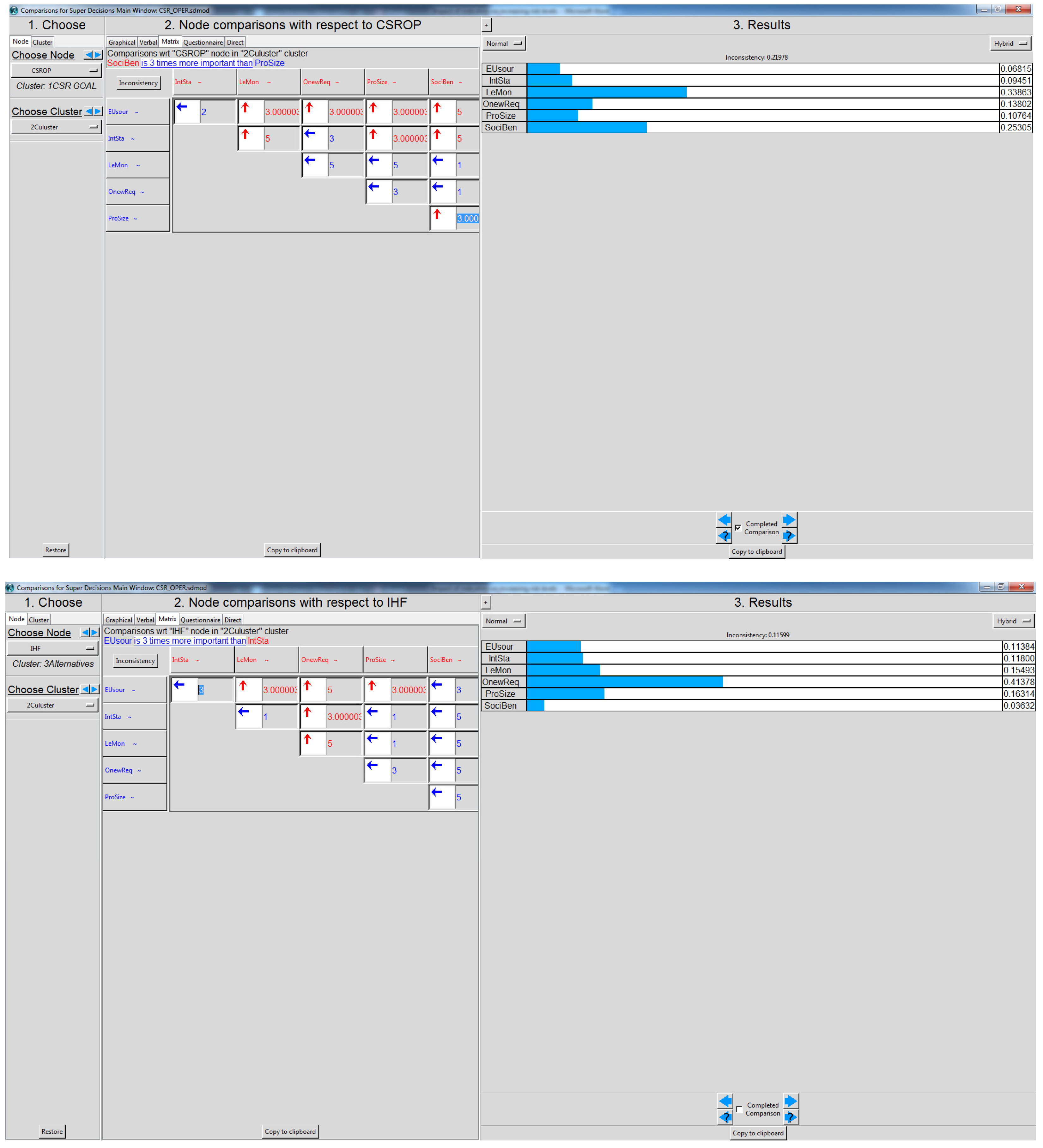

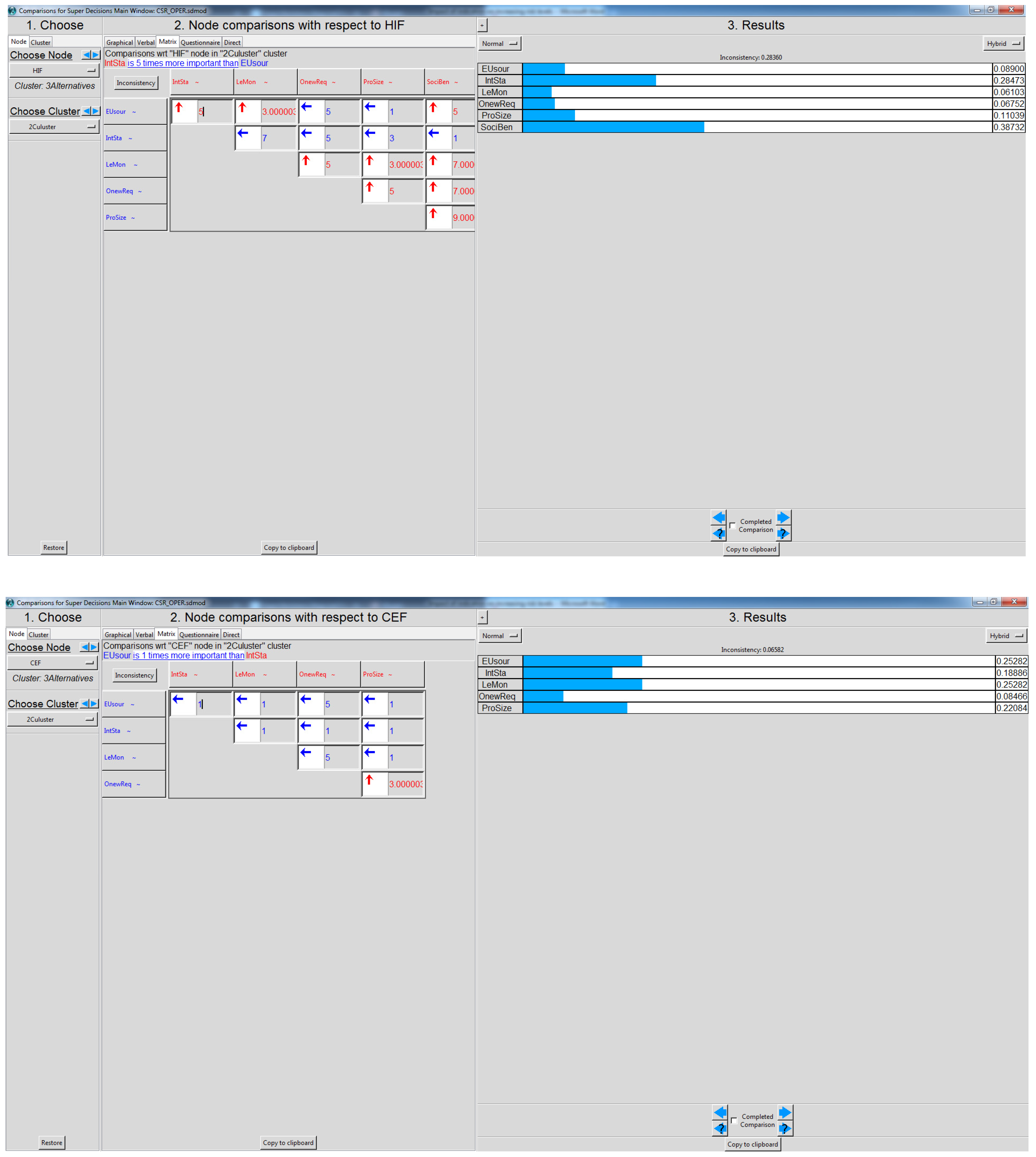

4.1. Creating the Test Matrix, Determining the Weights of the Aspects—The Weighting of the Selected Indicators (a, b, c, d, e, f) Based on the Three Groups of Factors (IHFs, HIFs and CEFs) (Table 1)

4.2. The Process of Evaluating Alternatives According to the Criteria Given

4.3. Summary of Weighting and Ratings

- 1CSR GOAL

- 2Clusters

- 3Alternatives

5. Results and Discussions

5.1. Reasons for Inducing Sustainability Deficit and Their Inductive Analysis

- Integrated monitoring of legal regulators;

- Fulfilment of profitability, size-efficiency;

- Fulfilled ownership requirements;

- Application of international standards;

- Performance monitoring of social benefits;

- Successful use of EU and state resources.

5.2. The Results of Analytic Hierarchy Process (AHP) Comparative Analysis

6. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

References

- Greenlee, E.J. The University of Pennsylvania Law Review: 150 Years of History. Univ. Pa. Law Rev. 2002, 150, 1875–1904. [Google Scholar] [CrossRef]

- World Commission on Environment and Development (Ed.) Our Common Future; Oxford University Press: Oxford, UK, 1987; ISBN 978-0-19-282080-8. [Google Scholar]

- Oded, S. Inducing corporate compliance: A compound corporate liability regime. Int. Rev. Law Econ. 2011, 31, 272–283. [Google Scholar] [CrossRef]

- Springett, D. Business conceptions of sustainable development: A perspective from critical theory. Bus. Strategy Environ. 2003, 12, 71–86. [Google Scholar] [CrossRef]

- Abbott, W.F.; Monsen, R.J. On the measurement of corporate social responsibility: Self-reported disclosures as a method of measuring corporate social involvement. Acad. Manag. J. 1979, 22, 501–515. [Google Scholar]

- Atkinson, G. Measuring corporate sustainability. J. Environ. Plan. Manag. 2000, 43, 235–252. [Google Scholar] [CrossRef]

- Figge, F.; Hahn, T. Sustainable Value Added—Measuring corporate contributions to sustainability beyond eco-efficiency. Ecol. Econ. 2004, 48, 173–187. [Google Scholar] [CrossRef]

- Shrivastava, P. Ecocentric Management for a Risk Society. Acad. Manag. Rev. 1995, 20, 118. [Google Scholar] [CrossRef]

- Montiel, I. Corporate social responsibility and corporate sustainability: separate pasts, common futures. Organ. Environ. 2008, 21, 245–269. [Google Scholar] [CrossRef]

- Husted, B.W.; Allen, D.B. Corporate social responsibility in the multinational enterprise: Strategic and institutional approaches. J. Int. Bus. Stud. 2006, 37, 838–849. [Google Scholar] [CrossRef]

- Kapsalis, V.C.; Kyriakopoulos, G.L.; Aravossis, K.G. Investigation of Ecosystem Services and Circular Economy Interactions under an Inter-organizational Framework. Energies 2019, 12, 1734. [Google Scholar] [CrossRef]

- Chen, R. An Integrated Sustainable Business and Development System: Thoughts and Opinions. Sustainability 2014, 6, 6862–6871. [Google Scholar] [CrossRef] [Green Version]

- Aravossis, K.G.; Kapsalis, V.C.; Kyriakopoulos, G.L.; Xouleis, T.G. Development of a Holistic Assessment Framework for Industrial Organizations. Sustainability 2019, 11, 3946. [Google Scholar] [CrossRef]

- Horvath, B.; Mallinguh, E.; Fogarassy, C. Designing Business Solutions for Plastic Waste Management to Enhance Circular Transitions in Kenya. Sustainability 2018, 10, 1664. [Google Scholar] [CrossRef]

- Taliento, M.; Favino, C.; Netti, A. Impact of Environmental, Social, and Governance Information on Economic Performance: Evidence of a Corporate ‘Sustainability Advantage’ from Europe. Sustainability 2019, 11, 1738. [Google Scholar] [CrossRef]

- Horvath, B.; Khazami, N.; Ymeri, P.; Fogarassy, C. Investigating the current business model innovation trends in the biotechnology industry. J. Bus. Econ. Manag. 2019, 20, 63–85. [Google Scholar] [CrossRef]

- Sharma, S.K.; Sengupta, A.; Panja, S.C. Mapping Corruption Risks in Public Procurement: Uncovering Improvement Opportunities and Strengthening Controls. Public Perform. Manag. Rev. 2019, 42, 947–975. [Google Scholar] [CrossRef]

- Bank, D. Double dependent market economy and corporate social responsibility in Hungary. Corvinus J. Sociol. Soc. Policy 2017, 8, 25–47. [Google Scholar] [CrossRef]

- Gibbs, D. Sustainability entrepreneurs, ecopreneurs and the development of a sustainable economy. Greener Manag. Int. 2006, 55, 63–78. [Google Scholar] [CrossRef]

- Fogarassy, C.; Nguyen, H.H.; Oláh, J.; Popp, J. Transition management applications to accelerate sustainable food consumption – comparative analysis between Switzerland and Hungary. J. Int. Stud. 2018, 11, 31–43. [Google Scholar] [CrossRef]

- Ntanos, S.; Kyriakopoulos, G.; Chalikias, M.; Arabatzis, G.; Skordoulis, M.; Galatsidas, S.; Drosos, D. A Social Assessment of the Usage of Renewable Energy Sources and Its Contribution to Life Quality: The Case of an Attica Urban Area in Greece. Sustainability 2018, 10, 1414. [Google Scholar] [CrossRef]

- University of Liechtenstein; Seidel, S.; Bharati, P.; University of Massachusetts Boston; Fridgen, G.; University of Bayreuth; Watson, R.T.; University of Georgia; Albizri, A.; Northern State University; et al. The Sustainability Imperative in Information Systems Research. Commun. Assoc. Inf. Syst. 2017, 40, 40–52. [Google Scholar] [CrossRef]

- Carter, C.R.; Rogers, D.S. A framework of sustainable supply chain management: Moving toward new theory. Int. J. Phys. Distrib. Logist. Manag. 2008, 38, 360–387. [Google Scholar] [CrossRef]

- Haugh, T. Nudging Corporate Compliance. Am. Bus. Law J. 2017, 54, 683–741. [Google Scholar] [CrossRef]

- Hauschka, C.E.; Moosmayer, K.; Lösler, T. (Eds.) Corporate Compliance: Handbuch der Haftungsvermeidung im Unternehmen; überarbeitete und erweiterte Auflage; C.H. Beck: München, Germany, 2016; ISBN 978-3-406-66297-3. [Google Scholar]

- Strategic Developent Plan (SDP) fog the INTOSAI Framework of Professiomal Promouncements (IFPP). Abu Dhaby. 2018. Available online: https://www.issai.org/wp-content/uploads/2019/08/sdp_ifpp_2016.pdf (accessed on 13 October 2019).

- Steinberg, R. Governance, Risk Management, and Compliance: It Can’t Happen to Us–Avoiding Corporate Disaster While Driving Success; Wiley: Hoboken, NJ, USA, 2011; ISBN 978-1-118-02430-0. [Google Scholar]

- Mitra, S.; Hossain, M.; Marks, B.R. Corporate ownership characteristics and timeliness of remediation of internal control weaknesses. Manag. Audit. J. 2012, 27, 846–877. [Google Scholar] [CrossRef]

- Spira, L.F.; Page, M. Risk management: The reinvention of internal control and the changing role of internal audit. Account. Audit. Account. J. 2003, 16, 640–661. [Google Scholar] [CrossRef]

- Organisation for Economic Co-operation and Development. OECD Guidelines on Corporate Governance of State-Owned Enterprises; OECD Publishing: Paris, France, 2015; ISBN 978-92-64-25025-3. [Google Scholar]

- Elbardan, H.; Ali, M.; Ghoneim, A. The dilemma of internal audit function adaptation: The impact of ERP and corporate governance pressures. J. Enterp. Inf. Manag. 2015, 28, 93–106. [Google Scholar] [CrossRef]

- Cuervo-Cazurra, A.; Inkpen, A.; Musacchio, A.; Ramaswamy, K. Governments as owners: State-owned multinational companies. J. Int. Bus. Stud. 2014, 45, 919–942. [Google Scholar] [CrossRef] [Green Version]

- Dewenter, K.L.; Malatesta, P.H. State-Owned and Privately Owned Firms: An Empirical Analysis of Profitability, Leverage, and Labor Intensity. Am. Econ. Rev. 2001, 91, 320–334. [Google Scholar] [CrossRef]

- Boros, A. OECD Guidelines on Corporate Governance of State-Owned Enterprises; OECD: Paris, France, 2015; ISBN 978-92-64-24412-2. [Google Scholar]

- Lentner, C. Excerpts on new Hungarian state finances from legal, economic and international aspect. Prav. Vjesn. 2018, 34, 9–36. [Google Scholar] [CrossRef]

- Johnson, R.A.; Greening, D.W. The Effects of Corporate Governance and Institutional Ownership Types on Corporate Social Performance. Acad. Manag. J. 1999, 42, 564–576. [Google Scholar]

- Gadinis, S.; Miazad, A. The Hidden Power of Compliance. SSRN Electron. J. 2018, 103, 2135. [Google Scholar] [CrossRef]

- Crisóstomo, V.L.; Girão, A.M.C. Analysis of the compliance of Brazilian firms with good corporate governance practices. Rev. AMBIENTE CONTÁBIL—Univ. Fed. Rio Gd. Norte—ISSN 2176-9036 2019, 11. [Google Scholar] [CrossRef] [Green Version]

- Pospisil, R. Performance audit in public institutions in the Czech Republic. Audit. Financ. J. 2017, 15, 430. [Google Scholar] [CrossRef]

- Rezaee, Z. What the COSO report means for internal auditors. Manag. Audit. J. 1995, 10, 5–9. [Google Scholar] [CrossRef]

- Galewska, E. (Ed.) European Information Law: Good Governance in the Public Sector; Research Center for Legal and Economic Issues of Electronic Communication: Warschau, Poland, 2010; ISBN 978-83-928515-0-9. [Google Scholar]

- Bird, R.C.; Park, S.K. The Domains of Corporate Counsel in an Era of Compliance: The Domains of Corporate Counsel in an Era of Compliance. Am. Bus. Law J. 2016, 53, 203–249. [Google Scholar] [CrossRef]

- Domokos, L.; Holman, M. The Methodological Renewal of the State Audit Office of Hungary in Light of the Protection of Public Funds. Polgári Szle 2017, 13, 83–98. [Google Scholar] [CrossRef] [Green Version]

- Warnier, M.; Oey, M.; Timmer, R.; Brazier, F.; Overeinder, B. Enforcing integrity of agent migration paths by distribution of trust. Int. J. Intell. Inf. Database Syst. 2009, 3, 382. [Google Scholar] [CrossRef]

- Grunig, J.E. A New Measure of Public Opinion on Corporate Social Responsibility. Acad. Manag. J. 1979, 22, 738–764. [Google Scholar] [CrossRef]

- Schwebel, S.M. The Compliance Process and the Future of International Law. Proc. ASIL Annu. Meet. 1981, 75, 178–185. [Google Scholar] [CrossRef]

- Gramling, A.; Schneider, A. Effects of reporting relationship and type of internal control deficiency on internal auditors’ internal control evaluations. Manag. Audit. J. 2018, 33, 318–335. [Google Scholar] [CrossRef]

- Premuroso, R.F.; Houmes, R. Financial statement risk assessment following the COSO framework: An instructional case study. Int. J. Account. Inf. Manag. 2012, 20, 26–48. [Google Scholar] [CrossRef]

- Adizes, I.; Weston, J.F. Comparative Models of Social Responsibility. Acad. Manag. J. 1973, 16, 112–128. [Google Scholar]

- Pederin, I. Hrvatska u europskim savezima u pismima Franje Račkoga i Josipa Jurja Strossmayera Louisu Legeru. Croat. Slavica Iadert. 2017, 5, 366–384. [Google Scholar] [CrossRef]

- Sutcliffe, P. The Standards Programme of IFAC’s Public Sector Committee. Public Money Manag. 2003, 23, 29–36. [Google Scholar] [CrossRef]

- Lentner, C. The New Hungarian Public Finance System—In a Historical, Institutional and Scientific Context. Public Financ. Q. 2015, 60, 447–461. [Google Scholar]

- Pulay, G. Preventing corruption by strengthening organisational integrity. Public Financ. Q. 2014, 59, 133–149. [Google Scholar]

- Pulay, G.; Lucza, A. Objective Corruption Risks—Subjective Controls. Integrity of Publicly Owned Business Associations, Methodology and Results of the Integrity Survey. Public Financ. Q. 2018, 63, 490–510. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Alternatives | Initial Hazard Factors (IHFs) (p1…p6) | Hazardous Increasing Factors(HIFs) (p1…p6) | Control Enhancement Factors (CEFs) (p1…p6) | |

|---|---|---|---|---|

| Indicators | ||||

| a1/p1 | a2/p1 | a3/p1 | |

| b1/p2 | b2/p2 | b3/p2 | |

| c1/p3 | c2/p3 | c3/p3 | |

| d1/p4 | d2/p4 | d3/p4 | |

| e1/p5 | e2/p5 | e3/p5 | |

| f1/p6 | f2/p6 | f3/p6 | |

| Index | The Value of the Index in 2016 (%) | The Value of the Index in 2017 (%) | The Value of the Index in 2018 (%) |

|---|---|---|---|

| Initial Hazard Factors (IHFs) | 48.4 | 41.4 | 41.6 |

| Hazardous Increasing Factors (HIFs) | 35.2 | 25.0 | 27.8 |

| Control Enhancement Factors (CEFs) | 60.0 | 49.8 | 46.6 |

| Factors Qualifying for IHFs in 2016 | Factors Qualifying for IHFs in 2017 | Factors Qualifying for IHFs in 2018 |

|---|---|---|

| Carrying out public tasks and pursuing other activities. | Carrying out public and service tasks and carrying out other activities. The blending of the objectives and conditions of the Community mission and the operation of a competitive market has contributed to an increased vulnerability to integrity. | The mixed activity also involved other initial hazards. |

| It affects the operation of business associations and the initial hazard to corruption - the contents of the memorandum and articles of association, the management agreement, the operation contract, the public service delegation contract, and the technical and financial requirements relating to the performance of the tasks, and - related ownership reporting. If these required clear and stringent requirements, the initial risk of corruption was less. | More complicated and more complex legal environment. | The initial hazard of public service and high-balance sheet companies was almost double that of smaller, non-public service companies. |

| As regards public service charges, the majority of the state-owned public service companies, which are entrusted with public service tasks, lack licensing or equity. | The operation of the public service and the size of the plant enhance the influence of each other. |

| Factors Qualifying for HIFs in 2016 | Factors Qualifying for HIFs in 2017 | Factors Qualifying for HIFs in 2018 |

|---|---|---|

| He has been a recipient of EU funding for the past three years, having been involved as a contracting authority, tenderer and in both ways in public procurement. Maintenance obligation, environmental compliance. | He has received EU funding for the past three years and is now subject to public procurement obligations. Recruitment of an external expert/consultant for the activity, such as obtaining a grant or conducting a public procurement. Environmental compliance: the use of an environmental monitoring system is required to fulfill the application criteria. | Larger companies’ overdue debts pose a greater risk. It was identified as a significant difference factor from a member company of the group: using a service or providing a service. Supporting other organizations or companies and employing or subcontracting external environmental consultants or experts. |

| There was a significantly higher proportion of public service, public-service and other companies increasing the risk of corruption. | The risk of companies using a restricted procedure in the field of public procurement was greater than that of firms not in the scope of public procurement. The continuous additional cost of defects in construction is a significant cost during maintenance. | Lack of approval by the supervisory board of the internal control plan was more often a risk-increasing factor for smaller companies. |

| Increasing the risk of corruption when a company is involved in a public procurement procedure is because it uses a significant amount of public money. | The vulnerability of public service companies has already exceeded that of non-public service providers with a subsidy amount of EUR 3 million. | |

| Public service companies have a higher HIFs index, mainly because (in the absence of competence) they subcontract their core tasks more frequently, have recourse to a restricted procedure in their procurement and receive more state aid than non-public service companies. The use of the restricted procedure was accompanied by a higher incidence of other public procurement risk factors, such as several public tenders awarded to the same tenderer and the fact that the company was the successful tenderer with which the company was previously contracted. |

| Factors Qualifying for CEFs in 2016 | Factors Qualifying for CEFs in 2017 | Factors Qualifying for CEFs in 2018 |

|---|---|---|

| The relationship between size and hazard has not been studied in detail. | In terms of control structure, the largest differences were found between the total assets, the size of the balance sheet, the reporting activity and the internal control function. | The absolute value of the control structure was significantly influenced by the plant size. |

| Higher risk was associated with higher levels of control. For assets with a balance sheet total of more than EUR 2 million, the level of controls is above average. | There was a significant difference in the intensity of the control factors for companies below and above the balance sheet total of EUR 2 million. Larger companies had better controls. | |

| If the management (director/chief executive/executive) of a company did not or regularly inform the supervisory board of the decisions taken by the management and their implementation, this was also related to the lower level of control in place. | The intensity of the soft controls is only moderate in the larger companies, but very low in the smaller companies. | |

| If a company did not have a risk-based internal control plan, it had a below average control system, which was also significantly lower than companies with an internal control plan based on risk analysis. | If a company received an EU subsidy, it increased the CEFs index by an average of 6.3 percentage points (index of EU subsidized companies: 51.1%, of non-subsidized companies: 44.8%). |

| Areas of Application of Integrity Controls 2016 | Areas of Application of Integrity Controls 2017 | Areas of Application of Integrity Controls 2018 |

|---|---|---|

| - Asset management, management of public funds; - Corporate governance, supervision; - Activities, provision of public services; - Organizational structure; - Purchases, public procurement; - Legal environment; - Internal regulation; - Human resource management; - Internal controls, risk management; - Special anti-corruption systems and procedures. | - Responsible management (provision of ownership, legal environment, role of the supervisory board, reporting to the owner, decision-making power of the owner, corporate governance, establishment of the organizational structure, management information system); - Public service tasks, external relations (public service tasks, public service provision, fee setting, support to and from outside organizations, risks of contractual partners, outsourcing, disclosure, publicity); - Management (resource and asset management, EU support, partner contracts, group of companies, management efficiency); - Compliance, audits (internal regulations, public procurement, tendering, auditing, external and internal audits); - Organizational culture, ethical behavior (integrity culture in internal rules, private benefits, staff selection, conflict of interest, benchmarking, ethics, media appearance). | Beyond the areas named in the 2017 analysis: - External relations: Participation in, or provision of, external aid, accounting for subsidies, measurement of customer satisfaction and social utility, disclosure of data of public interest. - External and internal audits: auditing, audits by external bodies, quality of internal audits, utilization, environmental and financial risk analysis and risk management. - Organizational culture: human resources management, conflict of interest management and employee selection, remuneration system, performance evaluation, ethical procedures. |

| Alternatives | Initial Hazard Factors (IHFs) | Hazardous Increasing Factors (HIFs) | Control Enhancement Factors (CEFs) | |

|---|---|---|---|---|

| Indicators | ||||

| 5/7 (0.71) | 1/7 (0.14) | 7/7 (1.0) | |

| 5/7 (0.71) | 5/7 (0.71) | 7/7 (1.0) | |

| 7/7 (1.0) | 3/7 (0.42) | 5/7 (0.71) | |

| 5/7 (0.71) | 7/7 (1.0) | 7/7 (1.0) | |

| 3/9 (0.33) | 9/9 (1.0) | 5/9 (0.55) | |

| 3/7 (0.42) | 5/7 (0.71) | 7/7 (1.0) | |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Boros, A.; Fogarassy, C. Relationship between Corporate Sustainability and Compliance with State-Owned Enterprises in Central-Europe: A Case Study from Hungary. Sustainability 2019, 11, 5653. https://doi.org/10.3390/su11205653

Boros A, Fogarassy C. Relationship between Corporate Sustainability and Compliance with State-Owned Enterprises in Central-Europe: A Case Study from Hungary. Sustainability. 2019; 11(20):5653. https://doi.org/10.3390/su11205653

Chicago/Turabian StyleBoros, Anita, and Csaba Fogarassy. 2019. "Relationship between Corporate Sustainability and Compliance with State-Owned Enterprises in Central-Europe: A Case Study from Hungary" Sustainability 11, no. 20: 5653. https://doi.org/10.3390/su11205653

APA StyleBoros, A., & Fogarassy, C. (2019). Relationship between Corporate Sustainability and Compliance with State-Owned Enterprises in Central-Europe: A Case Study from Hungary. Sustainability, 11(20), 5653. https://doi.org/10.3390/su11205653