The Application of Material Flow Cost Accounting in Waste Reduction

Abstract

:1. Introduction

2. Literature Review

2.1. Material Flow Management

2.2. Material Flow Cost Accounting

2.3. ISO 14051 Based MFCA

2.3.1. Implementation Step 1: Engaging Management and Determining Roles and Responsibilities (Clause 6.2, 6.3, ISO 14051:2011)

2.3.2. Implementation Step 2: Scope and Boundary of The Process and Establishing A Material Flow Model (Clauses 6.4, 6.5, ISO 14051:2011)

2.3.3. Implementation Step 3: Cost Allocation (Clauses 5.3, 6.8, ISO 14051:2011)

- Material cost: cost for a substance that enters and/or leaves a quantity center;

- Energy cost: cost for electricity, fuel, steam, heat, and compressed air;

- System cost: Cost of labor, cost of depreciation and maintenance, and cost of transport;

- Waste management cost: cost of handling waste generated in a quantity center.

2.3.4. Implementation Step 4: Interpreting and Communication MFCA Results (Clauses 6.9, 6.10, ISO 14051:2011)

2.3.5. Implementation Step 5: Improving Production Practices and Reducing Material Loss through MFCA Results (Clause 6.11, ISO 14051:2011)

3. Research Method

4. Case Analysis

4.1. Company Profile

4.2. Decision for Implementing MFCA

4.3. The Initial Stage of Establishing a Project Group

- Finance department integrates the construction and cost information to construct a material flow model, compile reports, and document findings for future reference. It also provides valuable assistance in the implementation process, from preliminary planning to the compilation of an MFCA balance sheet. In the preparatory stage of MFCA implementation, a scope and time period must first be specified;

- Environmental-safety department provides the information regarding the environmental effects of wastes, including types of the waste and waste-treatment activities;

- Plant affairs department identifies types and methods of the energy application and quantifies the consumption of the energy, including the energy loss in each quantity center (QC);

- Manufacturing and technical department analyzes the material balance in a material flow model and assists in providing the missing information.

4.4. Scope Specification

- Product with the highest unit price;

- Product or production line associated with the maximum material input;

- Product or production line associated with the maximum energy consumption;

- The simplest product variety;

- Production line with a discernible scope;

- Process that easily generates wastes.

4.5. Quantity Center Selection

4.6. Cost Classification in MFCA

- Material Cost:

- (1)

- Direct materials: Direct materials refer to materials inputted at the beginning of the process and remain in the final product. The direct materials of Company T include glass, BM resist, R resist, G resist, and B resist;

- (2)

- Indirect and auxiliary materials: Indirect materials are added during an intermediary process. Auxiliary materials, such as detergents and solvents, are not directly required for manufacturing products, but are essential to the process. Auxiliary materials vary in type and account for less than 10% of the total cost. We therefore eliminated auxiliary materials in the current analysis.

- Energy Cost (Water & Electricity cost):

- 3.

- System Cost:

- 4.

- Waste-Management Cost:

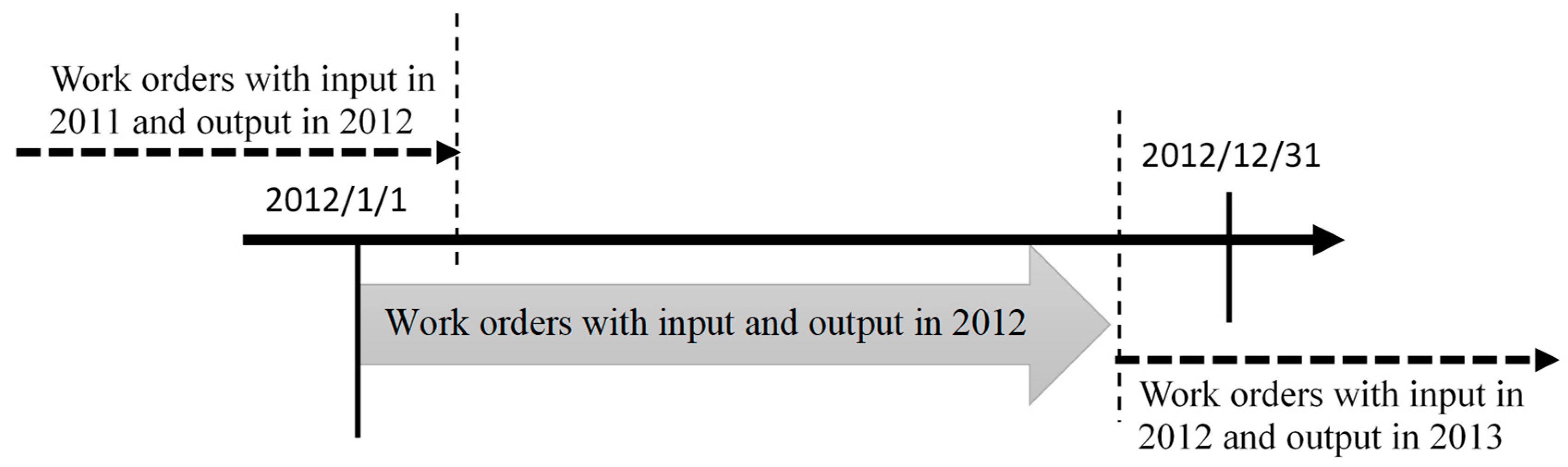

4.7. Specification of a Time Period

4.8. Summary of Material Flow

4.9. Determination of Material Balance

4.10. Quantification of Material Loss and Details (Material Balance Sheet for Each Quantity Center)

4.11. Calculation of Material Flow Cost

- (1)

- Standard-order bill of material: A standard-order bill of material is the accounting evidence and also consists of the amount of materials used in each quantity center, hours of labor, and other manufacture quantities of input materials required to produce a piece of color filter without any substantial loss ring costs;

- (2)

- Production-order bill of material: It is almost impossible that no loss is incurred during the production process. Therefore, production-management staff adopt a standard-order bill of material as the basis for adjusting input quantity according to the status of a production line. Adjustments are most commonly made to yields. On a production-order bill of material, the quantity of usage is also the basis for calculating material stock and the quantity of materials to be purchased. Cost accounting is based on the data provided on a production-order bill of material, which documents the production start time, actual usage in each quantity center, and the amount of loss. In the case of actual usage, cost is calculated by multiplying the bill of material-based input quantities in each quantity center by the standard unit price. Standard unit price is the unit price of the most recently approved order. The actual cost of each quantity center is summarized in Table 2. In the following section, adjustments to figures in the table are simulated. After a work order has been completed and inventoried, a work order record sheet is completed, as displayed in Table 3.

4.12. Summary of Energy and System Costs

4.13. Waste-Treatment Cost Calculation

4.14. Development of Improvement Plans

4.15. Improvement Implementation

5. Conclusion and Recommendations

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| The calculation steps are as follows |

|---|

| Material_ Resist 1: Standard Unit Price $3200 × Quantity of Usage $0.8 = Monetary Amount $2560 |

| Labor_Direct labor: Standard Unit Price $125 × Quantity of Usage $4 = Monetary Amount $500 |

| Labor_Indirect labor: Standard Unit Price $165 × Quantity of Usage $3 = Monetary Amount $495 |

| Manufacturing Costs_Depreciation expense: Standard Unit Price $10,000 × Quantity of Usage $30 = Monetary Amount $300,000 |

| Manufacturing Costs_Consumables: Standard Unit Price $800 × Quantity of Usage $4 = Monetary Amount $3200 |

| Manufacturing Costs_Other costs: Standard Unit Price $600 × Quantity of Usage $4 = Monetary Amount $2400 |

| Manufacturing_Electricity: Standard Unit Price $4500 × Quantity of Usage $4 = Monetary Amount $18,000 |

| The total cost of QC2 is $327,155 |

| The calculation steps are as follows | |||

|---|---|---|---|

| Step1 Monetary Input/Input Quantity = Average Unit Price Step2 last Cumulative Input Quantity + Input Quantity = Cumulative Input Quantity Step3 Cumulative Input Quantity × Average Unit Price = Cumulative Monetary Input | |||

| Work Section | Step1 Average Unit Price | Step2 Cumulative Input Quantity | Step3 Cumulative Monetary Input |

| QC2 BM | $698,425/53,260 = $13.11 | 0 + 53,260 = 53,260 | 53,260 × $13.11 = $698,239 |

| QC3 BM | $2,916,395/222,398 = $13.11 | 53,260 + 222,398 = 275,658 | 275,658 × $13.11 = $3,613,876 |

| QC4 POL/ITO | $3,950,633/301,265 = $13.11 | 275,658 + 301,265 = 576,923 | 576,923 × $13.11 = $7,563,460 |

| QC5 PS | $4,590,404/350,053 = $13.11 | 576,923 + 350,053 = 926,976 | 926,976 × $13.11 = $12,152,655 |

| QC6 INS | $ 4,523,001/344,913 = $ 13.11 | 926,976 + 344,913 = 1,271,889 | 1,271,889 × $13.11 = $16,674,464 |

| Tap Water Monetary Input Subtotal: $ 698,425 + $,2,916,395 + 3,950,633 + $4,590,404 + $4,523,001 = 16,678,858 | |||

References

- Stotz, P.M.; Bey, N. Integrating Sustainability in the Development and Operation of High-volume Production Lines. In Proceedings of the 25th CIRP Life Cycle Engineering (LCE) Conference, Copenhagen, Denmark, 30 April–2 May 2018. [Google Scholar]

- Cheng, L.C. The Study of Accounting Statements of Environmental Costs. Master’s Thesis, Business Administration National Sun Yat-sen University, Kaohsiung, Taiwan, 2017. [Google Scholar]

- Fakoya, M.B.; van der Poll, H.M. Integrating ERP and MFCA systems for improved waste-reduction decisions in a brewery in South Africa. J. Clean. Prod. 2013, 40, 136–140. [Google Scholar] [CrossRef]

- Daian, G.; Ozarska, B. Wood waste management practices and strategies to increase sustainability standards in the Australian wooden furniture manufacturing sector. J. Clean. Prod. 2009, 17, 1594–1602. [Google Scholar] [CrossRef]

- Van Hoof, B.; Lyon, T.P. Cleaner production in small firms taking part in Mexico’s Sustainable Supplier Program. J. Clean. Prod. 2013, 41, 270–282. [Google Scholar] [CrossRef]

- Wagner, B.; Enzler, S. Material Flow Management: Improving Cost Efficiency and Environmental Performance; Springer: Berlin, Germany, 2005; pp. 8–12. [Google Scholar]

- Christ, K.L.; Burritt, R.L. ISO 14051: A new era for MFCA implementation and research. Rev. Contab. Span. Account. Rev. 2016, 19, 1–9. [Google Scholar] [CrossRef] [Green Version]

- Schaltegger, S.; Windolph, S.E.; Herzig, C. From Knowledge to Application: Dissemination of Sustainability Management Tools in Large German Companies; Centre for Sustainability Management, Leuphana University: Lueneburg, Germany, 2011. [Google Scholar]

- Onishi, Y.; Kokubu, K.; Nakajima, M. Implementing material flow cost accounting in a pharmaceutical company. In Environmental Management Accounting for Cleaner Production; Schaltegger, S., Bennett, M., Burritt, R.L., Jasch, C., Eds.; Springer: Dordrecht, The Netherlands, 2009; pp. 395–409. [Google Scholar]

- Kasemset, C.; Chernsupornchai, J.; Pala-ud, W. Application of MFCA in waste reduction: Case study on a small textile factory in Thailand. J. Clean. Prod. 2015, 108, 1342–1351. [Google Scholar] [CrossRef]

- Sulong, F.; Sulaiman, M.; Norhayati, M.A. Material Flow Cost Accounting (MFCA) enablers and barriers: The case of a Malaysian small and medium-sized enterprise (SME). J. Clean. Prod. 2015, 108, 1365–1374. [Google Scholar] [CrossRef]

- Tang, C.S.; Zhou, S. Research advances in environmentally and socially sustainable operations. Eur. J. Oper. Res. 2012, 223, 585–594. [Google Scholar] [CrossRef]

- Energy Research Centre of the Netherlands. Resource Efficiency: What Does It Mean and Why Is It Relevant? 2013. Available online: https://www.ecn.nl/docs/library/report/2013/o13004.pdf (accessed on 30 August 2018).

- International Organization for Standardization (ISO). Environmental Management—Material Flow Cost Accounting—General Framework (ISO 14051:2011); ISO: Geneva, Switzerland, 2011. [Google Scholar]

- Seuring, S.; Müller, M. Integrated chain management in Germany—Identifying schools of thought based on a literature review. J. Clean. Prod. 2007, 15, 699–710. [Google Scholar] [CrossRef]

- Sygulla, R.; Bierer, A.; Götze, U. Material Flow Cost Accounting—Proposals for Improving the Evaluation of Monetary Effects of Resource Saving. In Proceedings of the 44th CIRP Conference on Manufacturing Systems, Madison, WI, USA, 31 May–3 June 2011. [Google Scholar]

- Kokubu, K.; Kitada, H. Material flow cost accounting and existing management perspectives. J. Clean. Prod. 2015, 108, 1279–1288. [Google Scholar] [CrossRef]

- Mahmood, H.; Furqan, M.; Bagais, O. Environmental Accounting of Financial Development and Foreign Investment: Spatial Analyses of East Asia. Sustainability 2019, 11, 13. [Google Scholar] [CrossRef]

- Masud, M.A.K.; Bae, S.M.; Kim, J.D. Analysis of Environmental Accounting and Reporting Practices of Listed Banking Companies in Bangladesh. Sustainability 2017, 9, 1717. [Google Scholar] [CrossRef]

- Nakajima, M. On the differences between material flow cost accounting and traditional cost accounting: In reply to the questions and misunderstandings on material flow cost accounting. Kansai Univ. Rev. Bus. Commer. 2004, 6, 1–20. [Google Scholar]

- Wan, Y.K.; Ng, R.T.; Ng, D.K.; Tan, R.R. Material flow cost accounting (MFCA)–based approach for prioritisation of waste recovery. J. Clean. Prod. 2015, 104, 602–614. [Google Scholar] [CrossRef]

- Dunuwila, P.; Rodrigo, V.H.L.; Goto, N. Sustainability of natural rubber processing can be improved: A case study with crepe rubber manufacturing in Sri Lanka. Resour. Conserv. Recycl. 2018, 133, 417–427. [Google Scholar] [CrossRef]

- Kokubu, K. Practice of Material Flow Cost Accounting; Japan Environmental Management Association for Industry: Tokyo, Japan, 2008. [Google Scholar]

- Chompu-Inwai, R.; Jaimjit, B.; Premsuriyanunt, P. A combination of Material Flow Cost Accounting and design of experiments techniques in an SME: The case of a wood products manufacturing company in northern Thailand. J. Clean. Prod. 2015, 108, 1352–1364. [Google Scholar] [CrossRef]

- Jasch, C. How to perform an environmental management cost assessment in one day. J. Clean. Prod. 2006, 14, 1194–12133. [Google Scholar] [CrossRef]

- Chetty, N.S. The case study method for research in small-and medium-sized firms. Int. Small Bus. J. 1996, 15, 73–85. [Google Scholar] [CrossRef]

- Yin, R.K. Case Study Research: Design and Methods, 2nd ed.; Sage Publications: Thousand Oaks, CA, USA, 1994. [Google Scholar]

- Gustafsson, A.; Johnson, M.D. Measuring and managing the satisfaction-loyalty performance links at Volvo. J. Target. Meas. Anal. Mark. 2002, 10, 249–258. [Google Scholar] [CrossRef]

- Gosman, M.L.; Kohlbeck, M.J. Effects of the existence and identity of major customers on supplier profitability: Is Wal-Mart different? J. Manag. Account. Res. 2009, 21, 179–201. [Google Scholar] [CrossRef]

- Banker, R.D.; Potter, G.; Srinivasan, D. An empirical investigation of an incentive plan that includes nonfinancial performance measures. Account. Rev. 2000, 75, 65–92. [Google Scholar] [CrossRef]

- Rieckhof, N.R.; Bergmann, A.; Guenther, E. Interrelating material flow cost accounting with management control systems to introduce resource efficiency into strategy. J. Clean. Prod. 2015, 108, 1262–1278. [Google Scholar] [CrossRef]

- Strobel, M.; Redmann, C. Flow cost accounting, an accounting approach based on the actual flows of materials. In Environmental Management Accounting: Informational and Institutional Developments; Bennett, M., Bouma, J.J., Walters, T., Eds.; Kluwer: Dordrecht, The Netherlands, 2002; pp. 67–82. [Google Scholar]

- Schönborn, G.; Berlin, C.; Pinzone, M.; Hanisch, C.; Lanz, M. Why social sustainability counts: The impact of corporate social sustainability culture on financial success. Sustain. Prod. Consum. 2019, 17, 1–10. [Google Scholar] [CrossRef]

- China Productivity Center myMKC.com. MFCA Practice “Business and the Environment” of Sustainable Development 2017. Available online: https://mymkc.com/article/content/22738 (accessed on 20 September 2018).

- Strazza, C.; Borghi, A.D.; Borghi, M.D. Resource productivity enhancement as means for promoting cleaner production: Analysis of co-incineration in cement plants through a life cycle approach. J. Clean. Prod. 2011, 19, 1615–1621. [Google Scholar] [CrossRef]

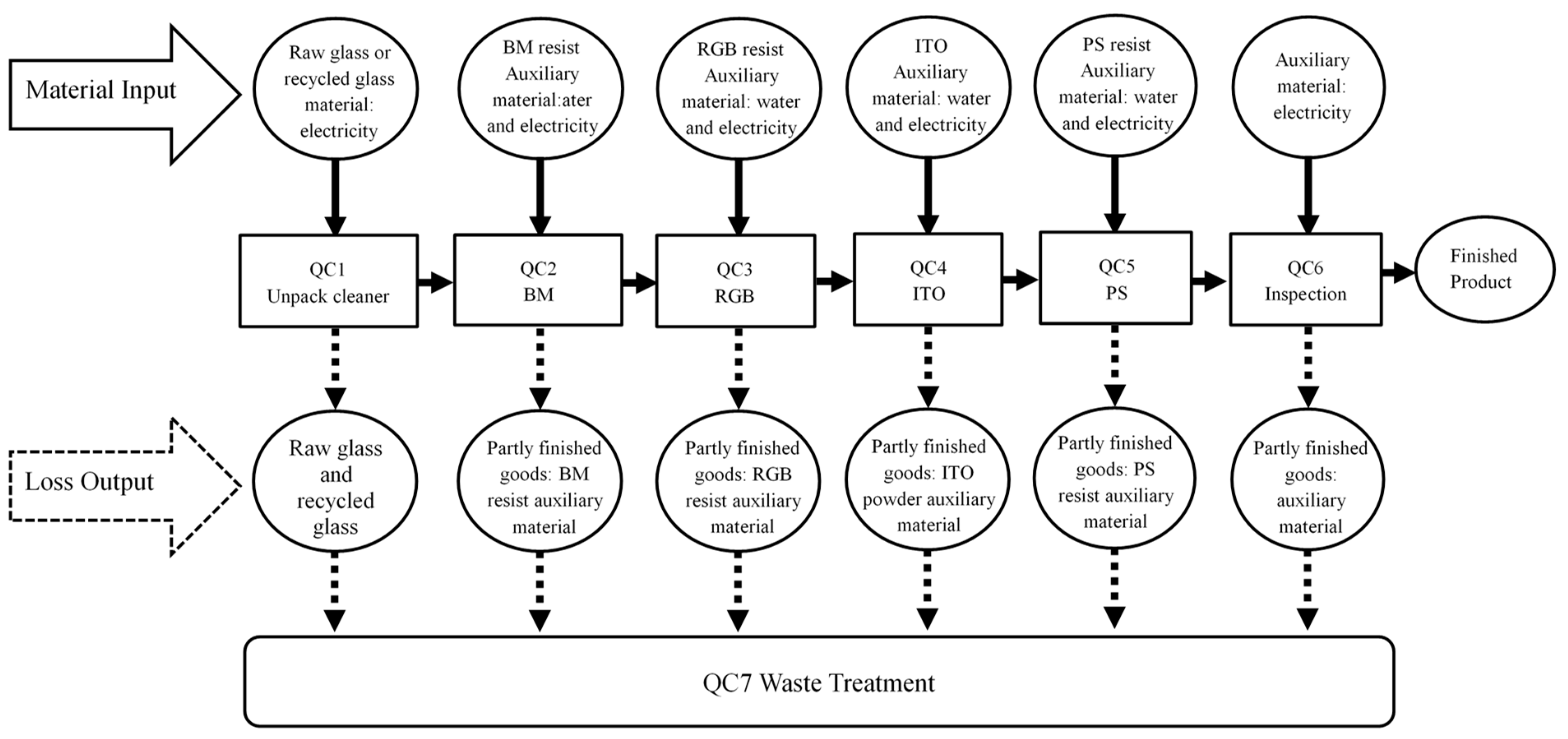

| QC | Process | Input | Output | Loss |

| QC1: Unpacked Cleaner | Automated robot arm inputted material into the production line for production | Raw and recycled glass | Raw and recycled glass | Defective raw glass and recycled glass |

| Electricity | Electricity | |||

| QC2: BM processes | Coat a glass substrate with BM resist and project a photomask pattern onto the glass substrate, which is then exposed to photoresist agent and engraved to form a BM pattern. The primary function of a color filter was to enhance contrast and prevent light leakage and photoelectric flow | Raw and recycled glass | Partly finished BM goods | Defective raw glass and recycled glass |

| BM resist | Defective BM resist | |||

| BM resist (switch outlet) | ||||

| Auxiliary material | Auxiliary material (including switch to cleaning and repair and maintenance) | |||

| Electricity | Electricity | |||

| Water | Water | |||

| QC3: RGB processes | Expose R resist to an R-patterned photomask after it has been coated, and then use a developing agent to remove the unexposed part and thereby reveal the R pattern. Oven-dry the R resist to ensure that the pattern is drug resistant, and then repeat this process for the G and B resists. The colors red, green, and blue were separated by a BM. The primary function of the RGB resist was to transform black and white images into color images | Partly finished BM goods | Partly finished RGB goods | Defective raw glass and recycled glass |

| Defective BM resist | ||||

| Defective RGB resist | ||||

| R resist | R resist (switch outlet) | |||

| G resist | G resist (switch outlet) | |||

| B resist | B resist (switch outlet) | |||

| Auxiliary material | Auxiliary material (including switch to cleaning and repair and maintenance) | |||

| Electricity | Electricity | |||

| Water | Water | |||

| QC4: POL and ITO processes | Grind the coated RGB glass substrate using a polyamide to flatten the photoresist layer. The purpose of the ITO process was to spread a layer of ITO film onto the flattened glass substrate to form a transparent conducting layer. | Partly finished RGB goods | Partly finished ITO goods | Defective raw glass and recycled glass |

| Defective BM resist | ||||

| Defective RGB resist | ||||

| ITO target | Defect ITO target | |||

| Auxiliary material | Auxiliary material | |||

| Electricity | Electricity | |||

| Water | Water | |||

| QC5: PS processes | Subject the coated PS resist to light exposure, image- developing, and oven-drying to obtain substrate gap control for the required thickness to enhance contrast | Partly finished ITO goods | Partly finished PS goods | Defective raw glass and recycled glass |

| Defective BM resist | ||||

| Defective RGB resist | ||||

| Defective ITO target | ||||

| Defective PS resist | ||||

| PS resist | PS resist (switch outlet) | |||

| Auxiliary material | Auxiliary material (including switch to cleaning and repair and maintenance) | |||

| Electricity | Electricity | |||

| Water | Water | |||

| QC 6: Inspection | Manually perform a visual inspection using an inspection machine | Partly finished PS goods | Finished goods | Defective raw glass and recycled glass |

| Defective BM resist | ||||

| Defective RGB resist | ||||

| Defective ITO target | ||||

| Defective PS resist | ||||

| Auxiliary material | Auxiliary material | |||

| Electricity | Electricity | |||

| QC | Process | Input | Treatment Method | |

| QC 7: Waste treatment | Because waste at the output end are worthless (e.g., waste gas and wastewater discharge) or not within the scope of analysis (e.g., externally recycled materials), this QC describes input items and treatment methods | Scrapped glass | Outsource glass waste recycling treatment plants | |

| Partly finished goods that have been scrapped | Outsource ITO recycling treatment plants and outsource glass waste recycling treatment plants | |||

| Output from a manufacturing process | Plant air-pollution control treatment, wastewater and recycled water treatment system, outsourced incineration treatment, outsourced recycling treatment, and external wastewater treatment (wastewater control) | |||

| Item | QC 1 | QC 2 | QC 3 | QC 4 | Total | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Type | Name | Unit | Standard Unit Price | Quantity of Usage | Monetary Amount | Quantity of Usage | Monetary Amount | Quantity of Usage | Monetary Amount | Quantity of Usage | Monetary Amount | Quantity of Usage | Monetary Amount |

| Material | Glass | Piece | 2800 | 303 | 848,400 | - | - | 303 | 848,400 | ||||

| Resist 1 | Kg | 3200 | - | 0.8 | 2560 | - | 0.8 | 2560 | |||||

| Resist 2 | Kg | 1800 | 0.7 | 1260 | - | - | 0.7 | 1260 | |||||

| Resist 3 | Kg | 1500 | - | - | - | 0.8 | 1200 | 0.8 | 1200 | ||||

| ITO | Kg | 21,000 | - | - | 0.2 | 4200 | - | 0.2 | 4200 | ||||

| Labor | Direct labor | Hour | 125 | 3.5 | 438 | 4 | 500 | 2 | 250 | 3.5 | 438 | 13 | 1625 |

| Indirect labor | Hour | 165 | 3 | 495 | 3 | 495 | 3 | 495 | 3 | 495 | 12 | 1980 | |

| Manufacturing Costs | Depreciation expense | Area/Square | 10,000 | 10 | 100,000 | 30 | 300,000 | 20 | 200,000 | 20 | 200,000 | 80 | 800,000 |

| Consumables | Hour | 800 | 3.5 | 2800 | 4 | 3200 | 2 | 1600 | 3.5 | 2800 | 13 | 10,400 | |

| Other costs | Hour | 600 | 3.5 | 2100 | 4 | 2400 | 2 | 1200 | 3.5 | 2100 | 13 | 7800 | |

| Electricity | KWH | 4500 | 3.5 | 15,750 | 4 | 18,000 | 2 | 9000 | 3.5 | 15,750 | 13 | 58,500 | |

| Total | 971,243 | 327,155 | 216,745 | 222,783 | 1,737,925 | ||||||||

| [Work Order: A001] | MFCA Terms | Realistic Standard | Yield | Ideal Standard | Consumption Quantity | Order Difference | Loss | ||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Type | Name | Unit | Standard Unit Price | Standard Usage | Standard Monetary Amount | Yield | Usage in Order | Actual Quantity of Usage | Monetary Amount Equivalent of Actual Amount of Usage | Monetary Difference | NG Quantity |

| Material | Glass | Piece | 2800 | 300 | 840,000 | 99% | 303 | 303 | 848,400 | 8400 | 3.0 |

| Resist 1 | Kg | 3200 | 0.3 | 960 | 98% | 0.306 | 0.8 | 2560 | 1600 | 0.5 | |

| Resist 2 | Kg | 1800 | 0.6 | 1080 | 99% | 0.606 | 0.7 | 1260 | 180 | 0.1 | |

| Resist 3 | Kg | 1500 | 0.6 | 900 | 97% | 0.618 | 0.8 | 1200 | 300 | 0.2 | |

| ITO | Kg | 21,000 | 0.1 | 2100 | 85% | 0.115 | 0.2 | 4200 | 2100 | 0.1 | |

| Labor | Direct labor | Hour | 125 | 10 | 1250 | 80% | 12 | 13 | 1625 | 375 | 3.0 |

| Indirect labor | Hour | 165 | 11 | 1815 | 80% | 13.2 | 12 | 1980 | 165 | 1.0 | |

| Manufacturing Costs | Depreciation expense | Area/Square | 10,000 | 80 | 800,000 | 100% | 80 | 80 | 80,000 | - | 0.0 |

| Consumables | Hour | 800 | 11 | 8800 | 100% | 11 | 13 | 10,400 | 1600 | 2.0 | |

| Other costs | Hour | 600 | 12.5 | 7500 | 100% | 12.5 | 13 | 7800 | 300 | 0.5 | |

| Electricity | KWH | 4500 | 10 | 45,000 | 100% | 10 | 13 | 58,500 | 13,500 | 3.0 | |

| Total | 1,709,405 | 1,737,925 | 28,520 | ||||||||

| QC | Quantity of Material Input (INPUT) | Usage of Positive Products in Each Resist | Quantity of Resist Lost | Quantity of Losses | Input Cost and Cost of Losses |

|---|---|---|---|---|---|

| QC1: Unpacked Cleaner | Quantity of glass inputted in QC1 is the total quantity of glass inputted in 2012 (because QC1 only has glass input and no other material input, and the input of a piece of glass produces a piece of glass filter, which is characteristic of the company’s product) | Quantity of glass lost = quantity of defective glass at a station | Quantity × unit price = input and loss costs | ||

| QC2: BM Processes | Quantity of positive products in QC1 OUTPUT + Total quantity of new materials input in QC2 | Sum of the quantity of glass positive products × the realistic-standard quantity of resist usage in each work order | Total number of resist input − the value for the usage of each resist positive product | Quantity of glass lost = quantity of defective glass at a station | Quantity × unit price = input and loss costs |

| QC3: RGB Processes | Quantity of positive products in QC2 OUTPUT + Total quantity of new materials input in QC3 | Sum of the quantity of glass positive products × the realistic-standard quantity of resist usage in each work order | Total number of resist input − the value for the usage of each resist positive product | Quantity of glass lost = quantity of defective glass at a station | Quantity × unit price = input and loss costs |

| QC4: POL Processes and ITO Processes | Quantity and monetary amount of each material used in the QC thereafter | ||||

| QC5: PS Processes | Quantity and monetary amount of each material used in the QC thereafter | ||||

| QC 6: Inspection | Quantity and monetary amount of each material used in the QC thereafter | ||||

| QC 7: Waste Treatment | Quantity and monetary amount of each material used in the QC thereafter | ||||

| Energy | Usage | Unit Cost | Input Cost of Each QC | Cost of Losses in Each QC |

|---|---|---|---|---|

| Tap water | Data regarding tap-water consumption were obtained from the quantity and monetary amount indicated by the Taiwan Water Corporation, but these data excluded the consumption of pure water | Unit cost of tap water = total monetary amount for 2012/total water consumption | Cost allocation and calculation for QCs that have inputted water resources = Total quantity of glass input at a station (including the number of times stripped glass was reworked) × the unit cost of tap water | = Total quantity of glass input at a station (including the number of times stripped glass was reworked) × the unit cost of tap water |

| Electricity | The plant owned by Company T supplied electricity to its two plant buildings; therefore, electricity consumed by the plant was allocated according to the ratio of electricity consumption by the two plant buildings. Subsequently, total electricity consumption was allocated to each QC, and costs were calculated as follows: Total electricity consumption = (amount of electricity consumption by a production line + amount of electricity allocated to plant buildings) in 2012 | Unit cost of electricity = (monetary amount for a production line indicated by the Taiwan Power Company + the monetary amount allocated to plant buildings) in 2012/total electricity consumption | Cost allocation and calculation of QCs that have inputted electricity = total quantity of glass input at a station (including the number of times stripped glass was reworked) × the unit cost of electricity | = Total quantity of defective glass at a station (including the number of times stripped glass was reworked) × the unit cost of electricity × the number of stations passed |

| Item | Work Section | Input Quantity | Monetary Input | Average Unit Price | Cumulative Input Quantity | Cumulative Monetary Input |

|---|---|---|---|---|---|---|

| Tap Water | QC1 INC | |||||

| QC2 BM | 53,260 | 698,425 | 13.11 | 53,260 | 698,425 | |

| QC3 RGB | 222,398 | 2,916,395 | 13.11 | 275,658 | 3,614,820 | |

| QC4 POL/ITO | 301,265 | 3,950,633 | 13.11 | 576,923 | 7,565,453 | |

| QC5 PS | 350,053 | 4,590,404 | 13.11 | 926,976 | 12,155,857 | |

| QC6 INS | 344,913 | 4,523,001 | 13.11 | 1,271,889 | 16,678,858 | |

| Tap Water Subtotal | 1,271,889 | 16,678,858 | 13.11 | |||

| Electricity | QC1 INC | 2,905,791 | 4,217,049 | 1.45 | 2,905,791 | 4,217,049 |

| QC2 BM | 20,315,148 | 29,482,497 | 1.45 | 23,220,939 | 33,699,546 | |

| QC3 RGB | 55,192,669 | 80,098,737 | 1.45 | 78,413,608 | 113,798,283 | |

| QC4 POL/ITO | 93,347,887 | 135,471,756 | 1.45 | 171,761,495 | 249,270,039 | |

| QC5 PS | 108,138,933 | 156,937,362 | 1.45 | 279,900,428 | 406,207,401 | |

| QC6 INS | 109,630,206 | 159,101,582 | 1.45 | 389,530,634 | 565,308,983 | |

| Electricity Subtotal | 389,530,634 | 565,308,983 | 1.45 | |||

| Total | 390,802,523 | 581,987,841 | 1.49 | |||

| Cost | Calculation Method | Unit Cost | Input Cost of Each QC | Cost of Losses in Each QC |

|---|---|---|---|---|

| System Cost | System cost = total production costs for a work order that has both input and output in 2012 − (Material cost + energy cost + waste treatment cost) | Unit cost of system cost = system cost/(the quantity of glass input at a station + the number of times stripped glass was reworked at each station) | Cost allocation and calculation for each QC = quantity of glass input at a station (including the number of times stripped glass was reworked) × the unit cost of the system | = Quantity of defective glass at a station (including the number of times stripped glass was reworked) × the unit cost of the system × the number of stations passed |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Huang, S.Y.; Chiu, A.A.; Chao, P.C.; Wang, N. The Application of Material Flow Cost Accounting in Waste Reduction. Sustainability 2019, 11, 1270. https://doi.org/10.3390/su11051270

Huang SY, Chiu AA, Chao PC, Wang N. The Application of Material Flow Cost Accounting in Waste Reduction. Sustainability. 2019; 11(5):1270. https://doi.org/10.3390/su11051270

Chicago/Turabian StyleHuang, Shaio Yan, An An Chiu, Po Chi Chao, and Ni Wang. 2019. "The Application of Material Flow Cost Accounting in Waste Reduction" Sustainability 11, no. 5: 1270. https://doi.org/10.3390/su11051270

APA StyleHuang, S. Y., Chiu, A. A., Chao, P. C., & Wang, N. (2019). The Application of Material Flow Cost Accounting in Waste Reduction. Sustainability, 11(5), 1270. https://doi.org/10.3390/su11051270