Carbon Emissions, Firm Size, and Corporate Governance Structure: Evidence from the Mining and Agricultural Industries in Indonesia

Abstract

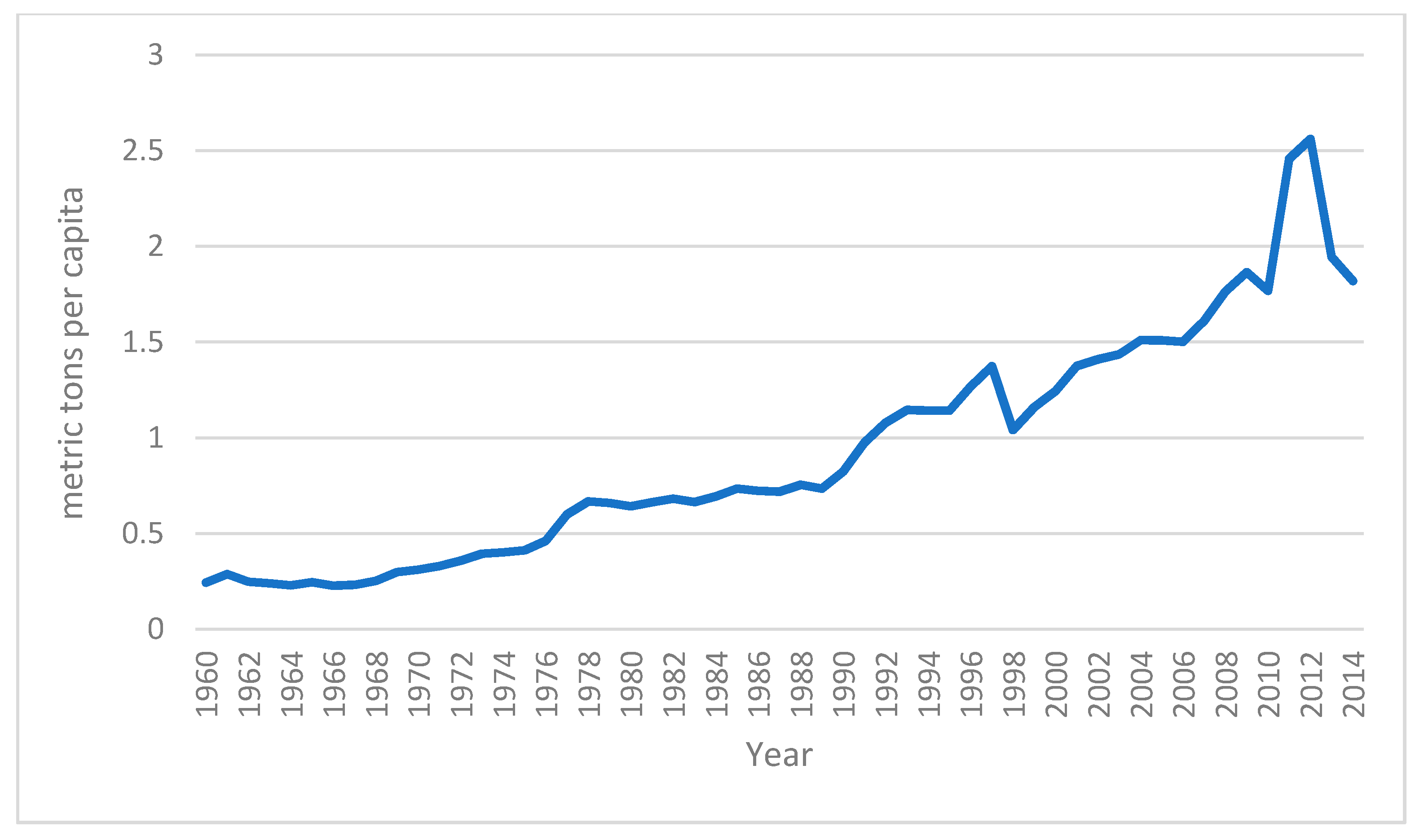

:1. Introduction

2. Theoretical Background and Hypothesis Development

2.1. Theoretical Background

2.1.1. Stakeholder Theory

2.1.2. Legitimacy Theory

2.2. Hypothesis Development

3. Data and Research Methodology

4. Results and Analysis

5. Conclusions and Suggestions

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

| Category | Items | Notes |

|---|---|---|

| 1. Climate Change (CC): Risks and Opportunities | CC1 | Assessment/Description of risks (regulations, both special and general) relating to climate change and actions seized or to be seized as a risk management step. |

| CC2 | Assessment/Description of financial, business, and opportunities implications for climate change both now and in the future. | |

| 2. Greenhouse Gases (GHG): Accounting for Greenhouse Gas Emissions | GHG1 | Describe the methods utilized in calculating greenhouse gas (GHG) emissions. |

| GHG2 | Continuity of external verification of the quantity of greenhouse gas (GHG) emissions. | |

| GHG3 | Total greenhouse gas emissions—metric tons of CO2—that are produced. | |

| GHG4 | Disclosure of scope 1, 2 and 3 directly on greenhouse gas emissions. | |

| GHG5 | Disclosure of the greenhouse gas emissions that come from resources (e.g., electricity, coal). | |

| GHG6 | Disclosure of greenhouse gas emissions that come from the facilities or segment level. | |

| GHG7 | Comparison of greenhouse gas emissions with the prior year. | |

| 3. Energy Consumption (EC) | EC1 | Total energy devoured. |

| EC2 | The quantity of energy used that comes from renewable resources. | |

| EC3 | Disclosures based on type, facility, or segment. | |

| 4. Reduction and Cost (RC) | RC1 | Explain the planning or strategies in reducing greenhouse gas emissions. |

| RC2 | Specifications of the level of reduction of greenhouse gas emissions and the targets per year. | |

| RC3 | Emission reductions and costs are borne or to be provided. | |

| RC4 | Costs of future emissions included in capital planning. | |

| 5. Accountability of Cost and Carbon Emission (ACC) | ACC1 | Indications where the board of the committee or executive body has responsibility for activities concomitant to climate change. |

| ACC2 | Describe the mechanism made by the board or other executive bodies by reviewing the sustainability of the company concerning climate change. |

References

- Martinez, L.H. Post industrial revolution human activity and climate change: Why the United States must implement mandatory limits on industrial greenhouse gas emmissions. J. Land Use Environ. Law 2005, 403–421. [Google Scholar]

- IPCC—Intergovernmental Panel on Climate Change. Climate Change 2007: Synthesis Report. 2007. Available online: http://www.ipcc.ch/pdf/assessmentreport/ar4/wg2/ar4_wg2_full_report.pdf (accessed on 2 April 2019).

- Freedman, M.; Jaggi, B. Global Warming Disclosures: Impact of Kyoto Protocol across Countries. J. Int. Financ. Manag. Account. 2011, 22, 46–90. [Google Scholar] [CrossRef]

- World Development Indicators. Indonesia’s CO2 Emissions (Metric Tons per Capita). Available online: https://data.worldbank.org/indicator/EN.ATM.CO2E.PC?end=2014&locations=ID&start=1960&vie=chart (accessed on 3 April 2019).

- Ministry of Energy and Mineral Resources. Transport Sector, Assessment of Greenhouse Emissions; Ministry of Energy and Mineral Resources: Jakarta, Indonesia, 2012. (In Indonesia)

- National Development Planning Agency. One Year Report on the Implementation of National Action Plan for Greenhouse Gases and Regional Action Plan for Greenhouse Gases; BAPPENAS: Jakarta, Indonesia, 2012. Available online: http://ranradgrk.bappenas.go.id/rangrk/admincms/downloads/publications/Laporan_Satu_Tahun_Pelaksanaan_RAN-GRK_RAD-GRK.pdf (accessed on 3 April 2019). (In Indonesia)

- PEACE. Indonesia and Climate Change: Current Status and Policy. 2007. Available online: http://siteresources.worldbank.org/INTINDONESIAINBAHASA/Resources/Environment/ClimateChange_Full_BH.pdf (accessed on 3 April 2019). (In Indonesia).

- Gonzalez-Gonzalez, J.M.; Zamora Ramírez, C. Voluntary carbon disclosure by Spanish companies: An empirical analysis. Int. J. Clim. Chang. Strateg. Manag. 2016, 8, 57–79. [Google Scholar] [CrossRef]

- Jaggi, B.; Freedman, M.; Martin, C. Global warming, Kyoto Protocol, and the need for corporate pollution disclosures in India: A case study. Int. J. Bus. Hum. Technol. 2011, 1, 60–67. [Google Scholar]

- Berthelot, S.; Robert, A.-M. Climate Change Disclosures: An Examination of Canadian Oil and Gas Firms. Issues Soc. Environ. Account. 2011, 5, 106–123. [Google Scholar] [CrossRef] [Green Version]

- Brammer, S.; Pavelin, S. Voluntary Environmental Disclosures by Large UK Companies. J. Bus. Financ. Account. 2006, 33, 1168–1188. [Google Scholar] [CrossRef]

- Luo, L.; Lan, Y.-C.; Tang, Q. Corporate Incentives to Disclose Carbon Information: Evidence from the CDP Global 500 Report. J. Int. Financ. Manag. Account. 2012, 23, 93–120. [Google Scholar] [CrossRef]

- Prado-Lorenzo, J.; Rodríguez-Domínguez, L.; Gallego-Álvarez, I.; García-Sánchez, I. Factors influencing the disclosure of greenhouse gas emissions in companies world-wide. Manag. Decis. 2009, 47, 1133–1157. [Google Scholar] [CrossRef]

- Lu, Y.; Abeysekera, I.; Cortese, C. Corporate social responsibility reporting quality, board characteristics and corporate social reputation. Pac. Account. Rev. 2015, 27, 95–118. [Google Scholar] [CrossRef]

- Deegan, C. Organizational legitimacy as a motive for sustainability reporting. Sustain. Account. Account. 2007, 127–149. [Google Scholar] [CrossRef]

- Hermawan, A.; Aisyah, I.S.; Gunardi, A.; Putri, W.Y. Going green: Determinants of carbon emission disclosure in manufacturing companies in Indonesia. Int. J. Energy Econ. Policy 2018, 8, 55–61. [Google Scholar]

- Aguilar-Fernández, M.; Otegi-Olaso, J. Firm Size and the Business Model for Sustainable Innovation. Sustainability 2018, 10, 4785. [Google Scholar] [CrossRef]

- Al-Tuwaijri, S.A.; Christensen, T.E.; Hughes, K. The relations among environmental disclosure, environmental performance, and economic performance: A simultaneous equations approach. Account. Organ. Soc. 2004, 29, 447–471. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Li, Y.; Richardson, G.D.; Vasvari, F.P. Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Account. Organ. Soc. 2008, 33, 303–327. [Google Scholar] [CrossRef]

- De Villiers, C.; van Staden, C.J. Where firms choose to disclose voluntary environmental information. J. Account. Public Policy 2011, 30, 504–525. [Google Scholar] [CrossRef]

- Hackston, D.; Milne, M.J. Some determinants of social and environmental disclosures in New Zealand companies. Account. Audit. Account. 1996, 9, 77–108. [Google Scholar] [CrossRef]

- Patten, D.M. Intra-industry environmental disclosures in response to the Alaskan oil spill: A note on legitimacy theory. Account. Organ. Soc. 1992, 17, 471–475. [Google Scholar] [CrossRef]

- Patten, D.M. The relation between environmental performance and environmental disclosure: A research note. Account. Organ. Soc. 2002, 27, 763–773. [Google Scholar] [CrossRef]

- Arvidsson, S. Communication of Corporate Social Responsibility: A Study of the Views of Management Teams in Large Companies. J. Bus. Eth. 2010, 96, 339–354. [Google Scholar] [CrossRef]

- Badulescu, A.; Badulescu, D.; Saveanu, T.; Hatos, R. The Relationship between Firm Size and Age, and Its Social Responsibility Actions—Focus on a Developing Country (Romania). Sustainability 2018, 10, 805. [Google Scholar] [CrossRef]

- Gangi, F.; Meles, A.; Monferrà, S.; Mustilli, M. Does Corporate Social Responsibility Help the Survivorship of SMEs and Large Firms? Glob. Financ. J. 2018, in press. Available online: https://www.sciencedirect.com/science/article/pii/S1044028317304106 (accessed on 3 April 2019).

- Kassinis, G.; Vafeas, N. Corporate boards and outside stakeholders as determinants of environmental litigation. Strateg. Manag. J. 2002, 23, 399–415. [Google Scholar] [CrossRef] [Green Version]

- Coles, J.; Daniel, N.; Naveen, L. Boards: Does one size fit all? J. Financ. Econ. 2008, 87, 329–356. [Google Scholar] [CrossRef]

- Dalton, D.R.; Daily, C.M. What’s wrong with having friends on the board? Across Board 1999, 36, 28–32. [Google Scholar]

- De Villiers, C.; Naiker, V.; van Staden, C.J. The Effect of Board Characteristics on Firm Environmental Performance. J. Manag. 2011, 37, 1636–1663. [Google Scholar] [CrossRef]

- Yanto, H.; Hasan, I.; Fam, S.F.; Raeni, R. Strengthening PROPER Implementation to Improve Transparency in Managing Carbon Emission among Indonesian Manufacturing Companies. Int. J. Bus. Manag. Sci. 2017, 7, 219–236. [Google Scholar]

- Ajinkya, B.; Bhojraj, S.; Sengupta, P. The Association between Outside Directors, Institutional Investors and the Properties of Management Earnings Forecasts. J. Account. Res. 2005, 43, 343–376. [Google Scholar] [CrossRef]

- Bushee, B.J.; Noe, C.F. Corporate Disclosure Practices, Institutional Investors, and Stock Return Volatility. J. Account. Res. 2000, 38, 171. [Google Scholar] [CrossRef] [Green Version]

- Chung, K.H.; Zhang, H. Corporate Governance and Institutional Ownership. J. Financ. Quant. Anal. 2011, 46, 247–273. [Google Scholar] [CrossRef]

- Gillan, S.L.; Starks, L.T. Corporate Governance, Corporate Ownership, and the Role of Institutional Investors: A Global Perspective. J. Appl. Financ. 2003, 13, 4–22. [Google Scholar] [CrossRef]

- Karamanou, I.; Vafeas, N. The Association between Corporate Boards, Audit Committees, and Management Earnings Forecasts: An Empirical Analysis. J. Account. Res. 2005, 43, 453–486. [Google Scholar] [CrossRef]

- Darmadi, S.; Sodikin, A. Information disclosure by family-controlled firms. Asian Rev. Account. 2013, 21, 223–240. [Google Scholar] [CrossRef]

- Baysinger, B.D.; Butler, H.N. Corporate Governance and the Board of Directors: Performance Effects of Changes in Board Composition. J. Law Econ. Organ. 1985, 1, 101–124. [Google Scholar] [CrossRef]

- Goodstein, J.; Gautam, K.; Boeker, W. The effects of board size and diversity on strategic change. Strateg. Manag. J. 1994, 15, 241–250. [Google Scholar] [CrossRef]

- Eng, L.L.; Mak, Y.T. Corporate governance and voluntary disclosure. J. Account. Public Policy 2003, 22, 325–345. [Google Scholar] [CrossRef]

- WRI Indonesia. Making Big Ideas Happen; World Resources Institute: Jakarta, Indonesia, 2018; Available online: http://www.wri-indonesia.org/ (accessed on 3 April 2019).

- Herold, D.M.; Lee, K.-H. The influence of internal and external pressures on carbon management practices and disclosure strategies. Aust. J. Environ. Manag. 2018, 26, 63–81. [Google Scholar] [CrossRef]

- Herold, D.M.; Farr-Wharton, B.; Lee, K.-H.; Groschopf, W. The interaction between institutional and stakeholder pressures: Advancing a framework for categorising carbon disclosure strategies. Bus. Strat. Dev. 2018. [Google Scholar] [CrossRef]

- Adams, C.A.; Hill, W.-Y.; Roberts, C.B. Corporate Social Reporting Practices in Western Europe: Legitimating Corporate Behavior? Br. Account. Rev. 1998, 30, 1–21. [Google Scholar] [CrossRef]

- Deegan, C.; Gordon, B. A Study of the Environmental Disclosure Practices of Australian Corporations. Account. Bus. Res. 1996, 26, 187–199. [Google Scholar] [CrossRef]

- Halme, M.; Huse, M. The influence of corporate governance, industry and country factors on environmental reporting. Scand. J. Manag. 1997, 13, 137–157. [Google Scholar] [CrossRef]

- Yu, G.; Kwon, K.-M.; Lee, J.; Jung, H. Exploration and Exploitation as Antecedents of Environmental Performance: The Moderating Effect of Technological Dynamism and Firm Size. Sustainability 2016, 8, 200. [Google Scholar] [CrossRef]

- Oxford Business Group. The Report: Indonesia 2008; Oxford Business Group: Oxford, UK, 2008; Available online: https://books.google.co.id/books?id=uW2XV5i1OvYC&printsec=frontcover&hl=id#v=onepage&q&f=false (accessed on 3 April 2019).

- Brown, J.L. The Spread of Aggressive Corporate Tax Reporting: A Detailed Examination of the Corporate-Owned Life Insurance Shelter. Account. Rev. 2011, 86, 23–57. [Google Scholar] [CrossRef] [Green Version]

- Choi, B.B.; Lee, D.; Psaros, J. An analysis of Australian company carbon emission disclosures. Pac. Account. Rev. 2013, 25, 58–79. [Google Scholar] [CrossRef]

| Year | Total | Mining | Agricultural | ||

|---|---|---|---|---|---|

| N | # | % | # | % | |

| 2011 | 44 | 33 | 75% | 11 | 25% |

| 2012 | 51 | 36 | 70.59% | 15 | 29.41% |

| 2013 | 52 | 36 | 69.23% | 16 | 30.77% |

| 2014 | 53 | 36 | 67.92% | 17 | 32.08% |

| 2015 | 52 | 36 | 69.23% | 16 | 30.77% |

| 2016 | 53 | 37 | 69.81% | 16 | 30.19% |

| Total | 305 | 214 | 70.16% | 91 | 29.84% |

| Variables | Mean | Minimum | P25 | P50 | P75 | Maximum |

|---|---|---|---|---|---|---|

| CED | 3.089 | 0.000 | 0.000 | 0.000 | 0.000 | 17.000 |

| BOARDSIZE | 9.610 | 4.000 | 7.000 | 10.000 | 12.000 | 20.000 |

| %INDCOM | 0.374 | 0.000 | 0.333 | 0.333 | 0.500 | 0.667 |

| %INDDIR | 0.098 | 0.000 | 0.000 | 0.000 | 0.200 | 0.667 |

| MINING | 0.702 | 0.000 | 0.000 | 1.000 | 1.000 | 1.000 |

| FIRMSIZE | 22.204 | 15.993 | 21.295 | 22.230 | 23.396 | 25.196 |

| PROFIT | 2.384 | −70.470 | −1.420 | 2.560 | 8.210 | 45.730 |

| LEVERAGE | 0.492 | 0.006 | 0.313 | 0.471 | 0.646 | 2.998 |

| Variables | [1] | [2] | [3] | [4] | [5] | [6] | [7] |

|---|---|---|---|---|---|---|---|

| [1] CED | 1.000 | ||||||

| [2] BOARDSIZE | 0.384 *** | 1.000 | |||||

| (0.000) | |||||||

| [3] %INDCOM | −0.185 *** | −0.085 | 1.000 | ||||

| (0.001) | (0.140) | ||||||

| [4] %INDDIR | −0.196 *** | −0.218 *** | 0.219 *** | 1.000 | |||

| (0.001) | (0.000) | (0.000) | |||||

| [5] MINING | 0.076 | −0.178 *** | −0.023 | 0.004 | 1.000 | ||

| (0.185) | (0.002) | (0.693) | (0.944) | ||||

| [6] FIRMSIZE | 0.472 *** | 0.564 *** | 0.015 | −0.105 * | −0.160 *** | 1.000 | |

| (0.000) | (0.000) | (0.798) | (0.066) | (0.005) | |||

| [7] PROFIT | 0.137 ** | 0.174 *** | −0.069 | −0.105 * | −0.054 | 0.104 * | 1.000 |

| (0.017) | (0.002) | (0.228) | (0.067) | (0.347) | (0.069) | ||

| [8] LEVERAGE | −0.026 | 0.040 | 0.023 | 0.034 | 0.052 | 0.108 * | −0.357 *** |

| (0.645) | (0.483) | (0.684) | (0.558) | (0.370) | (0.061) | (0.000) |

| Variables | Mining Firms | Agricultural Firms | Coef. | t-Value |

|---|---|---|---|---|

| CED | 3.397 | 2.363 | 1.035 | 1.328 |

| BOARDSIZE | 9.271 | 10.407 | −1.136 *** | −3.140 |

| PINDCOM | 0.372 | 0.379 | −0.007 | −0.395 |

| PINDDIR | 0.098 | 0.097 | 0.001 | 0.071 |

| FIRMSIZE | 22.050 | 22.568 | −0.518 *** | −2.815 |

| PROFITABILITY | 1.963 | 3.376 | −1.413 | −0.942 |

| LEVERAGE | 0.502 | 0.469 | 0.032 | 0.898 |

| Variables | Predicted | Carbon Emissions Disclosure (CED) | |||||

|---|---|---|---|---|---|---|---|

| Sign | (1) | (2) | (3) | (4) | (5) | (6) | |

| MINING | + | 2.370 *** | 2.384 *** | ||||

| (3.53) | (3.53) | ||||||

| BOARDSIZE | + | 0.212 * | 0.223 * | 0.261 ** | 0.273 ** | ||

| (1.67) | (1.76) | (2.09) | (2.19) | ||||

| %INDCOM | – | −7.250 *** | −7.690 *** | −7.001 *** | −7.444 *** | ||

| (−3.18) | (−3.35) | (−3.26) | (−3.42) | ||||

| %INDDIR | – | −3.864 * | −5.052 ** | −3.568 * | −4.819 ** | ||

| (−1.94) | (−2.30) | (−1.78) | (−2.20) | ||||

| FIRMSIZE | + | 2.238 *** | 2.244 *** | 1.954 *** | 1.879 *** | 2.031 *** | 1.953 *** |

| (9.38) | (9.47) | (7.45) | (7.07) | (7.97) | (7.51) | ||

| PROFIT | + | 0.025 | 0.020 | 0.008 | 0.016 | 0.008 | 0.016 |

| (1.04) | (0.85) | (0.32) | (0.63) | (0.32) | (0.65) | ||

| LEVERAGE | – | −3.709 *** | −3.875 *** | −3.369 ** | −3.176 ** | −3.709 *** | −3.505 *** |

| (−2.67) | (−2.98) | (−2.52) | (−2.39) | (−2.76) | (−2.61) | ||

| CONSTANT | −44.914 *** | −44.900 *** | −37.659 *** | −36.342 *** | −41.474 *** | −40.164 *** | |

| (−9.08) | (−9.00) | (−7.61) | (−7.23) | (−8.48) | (−8.04) | ||

| Year-dummies | Included | Included | Included | Included | Included | Included | |

| Robust SE | No | Yes | No | Yes | No | Yes | |

| r2 | 0.260 | 0.262 | 0.306 | 0.312 | 0.335 | 0.342 | |

| N | 315 | 315 | 305 | 305 | 305 | 305 | |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nasih, M.; Harymawan, I.; Paramitasari, Y.I.; Handayani, A. Carbon Emissions, Firm Size, and Corporate Governance Structure: Evidence from the Mining and Agricultural Industries in Indonesia. Sustainability 2019, 11, 2483. https://doi.org/10.3390/su11092483

Nasih M, Harymawan I, Paramitasari YI, Handayani A. Carbon Emissions, Firm Size, and Corporate Governance Structure: Evidence from the Mining and Agricultural Industries in Indonesia. Sustainability. 2019; 11(9):2483. https://doi.org/10.3390/su11092483

Chicago/Turabian StyleNasih, Mohammad, Iman Harymawan, Yuanita Intan Paramitasari, and Azizah Handayani. 2019. "Carbon Emissions, Firm Size, and Corporate Governance Structure: Evidence from the Mining and Agricultural Industries in Indonesia" Sustainability 11, no. 9: 2483. https://doi.org/10.3390/su11092483

APA StyleNasih, M., Harymawan, I., Paramitasari, Y. I., & Handayani, A. (2019). Carbon Emissions, Firm Size, and Corporate Governance Structure: Evidence from the Mining and Agricultural Industries in Indonesia. Sustainability, 11(9), 2483. https://doi.org/10.3390/su11092483