The Role of Port Development Companies in Transitioning the Port Business Ecosystem; The Case of Port of Amsterdam’s Circular Activities

Abstract

:1. Introduction

2. CE Activities in European Ports

3. The Port as a Business Ecosystem and the Role of the PDC in Transitioning This Ecosystem; A Review

3.1. The Port Business Ecosystem and the PDC

3.2. The Strategy and Business Model of the PDC

4. The Transition Towards CE; the Case of Port of Amsterdam

4.1. Research Questions and Methods

4.2. Amsterdam’s Port Business Ecosystem and PDC

4.3. Circular Activities in Amsterdam’s Port Complex

4.4. Synergies and Complementarities of CE Activities in Amsterdam

4.5. CE in the Strategy of the PDC

4.6. PoA’s Emerging Ecosystem Approach

4.7. Implications of the Circularity Transition for the Business Model of PoA

- Paid option on a plot of land in the port. If a company is not yet able to sign a long-term rental or long-term lease contract, it can take a paid option (25% of the normal price) on the plot of land it is looking to develop. The company cannot start physically developing the plot, but it can make plans and start the permitting procedure in the knowledge that the land will not be rented out or leased to a third party.

- Start-up discounts. A new company does not start generating revenue until its activity is (environmentally) permitted, designed, built, commissioned and up and running. The Port of Amsterdam can provide temporary discounts to new tenants to reduce OPEX until a new activity is operational and revenue streams have started flowing.

- Delayed payment. For companies that plan to scale up processing capacity (i.e., in the case of phased increase in production from, say, 100 tons per day to 600 tons per day), the initial revenue streams may not be enough to sustain full lease payments. For these parties, PoA offers delayed payment of the land rental or lease fees. Like the above-mentioned growth agreement, this method reduces OPEX for the activity in the startup and/or growth phase of the operation. The delayed payment is paid back to Port of Amsterdam at a later date or spread out across the duration of the land rental or land lease contract. To ensure that this incentive tool adheres to is EU state-aid regulation, PoA charges a market conform interest over the amount for which payment is delayed.

- Subordinated loans. Port of Amsterdam occasionally provides new companies and activities with subordinated loans, in partnership with local investment funds. These loans provide the funding to get a new activity built and operational. Like with the other mechanisms, the interest is market-based to adhere to EU legislation. One of the reasons for partnering with public investment funds is their expertise in due diligence and contractual agreements.

5. Conclusions

- Our population-level assessment of CE activities in European Core and Comprehensive ports shows that ports in Europe do indeed attract CE activities. However, there are huge differences between the ports, and large ports in linear activities do not automatically also attract circular activities. Furthermore, there are important regional disparities in Europe regarding the speed of the CE transition in ports.

- Amsterdam is a frontrunner in the CE transition in ports, with over 20 circular activities across five segments and substantial growth in CE activity over the past couple of years.

- A circular and renewable industry business ecosystem has emerged in Port of Amsterdam and continues to evolve. Three types of synergies between the companies in this ecosystem can be distinguished. The vast majority of CE companies benefit from a logistics infrastructure and services because other firms in the ecosystem provide logistics services, enabled by logistics infrastructure. Almost all CE companies also benefit from input–output synergy that arises through sales to or purchases from other firms in the port business ecosystem. Finally, less than 20% of Amsterdam’s CE companies also benefit from industrial ecology synergies, in which the exchange of (by)products is enabled by dedicated infrastructure.

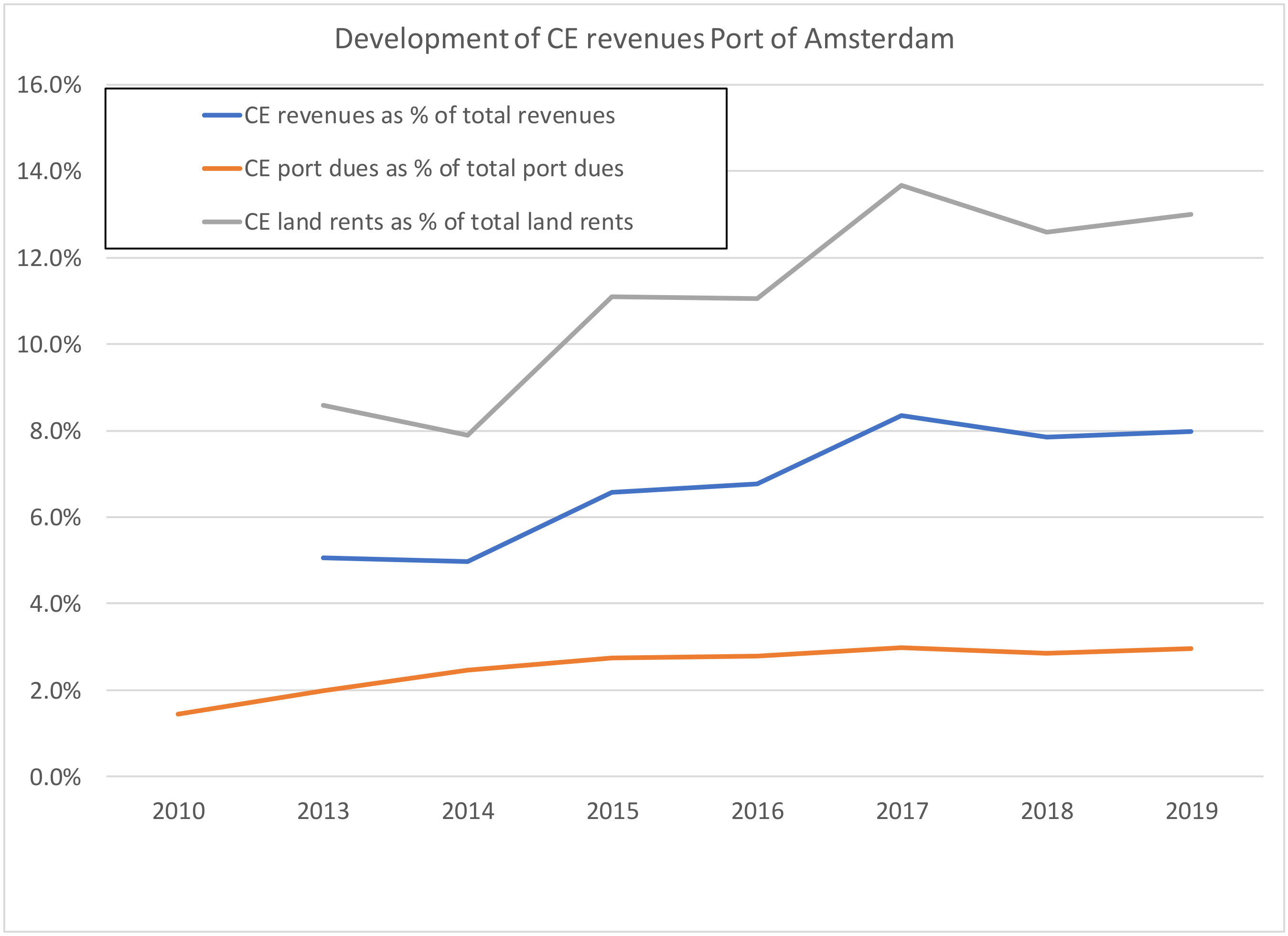

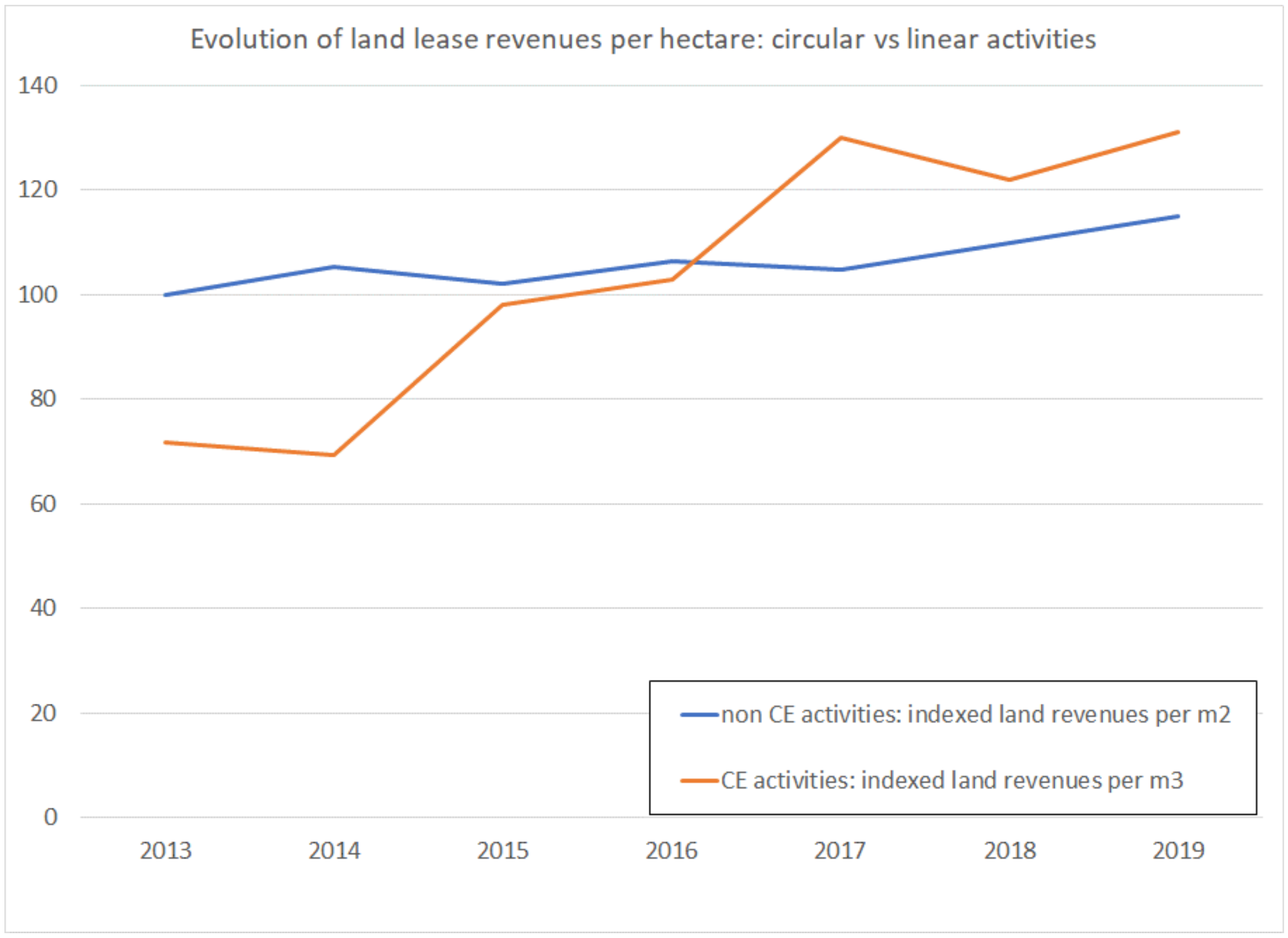

- The spatial scale of the CE value chains varies between segments but is in general less international than linear value chains; resources (in the form of waste) are often confined to the hinterland of the port, and often transported to the port by truck. Outputs of CE activities, either in the form of new products or in the form of sorted waste, are in some cases traded internationally, but often mainly reach continental markets within the European trading bloc. Amsterdam’s maritime circular volumes amount to about 2.5 million tons, around 3% of total volumes, while CE activities account for around 11.5% of the total land use in Amsterdam’s port.

- PoA, the government-owned landlord port development company, gives developing CE activities a central place in its strategy. Circularity is mentioned frequently in PoA’s long-term vision, its five-year corporate strategy and its recent annual reports. PoA also reports land use for CE activities and has allocated a part of the port area for CE activities. PoA’s focus on CE is in line with the ambitions and policies of its shareholder, the municipality of Amsterdam, which also includes the challenge to shift to a circular economy in its shareholder policy.

- PoA takes on new and active roles in advancing the circular business ecosystem. Most notable are PoA’s active role in developing industrial ecology synergies through investments in infrastructure to better connect the companies in the ecosystem and its role in nurturing and attracting new companies through an incubator facility as well capital provision (through loans and in one specific case equity).

- The transition towards CE goes hand in hand with a transition of PoA’s business model, with an increasing focus on new services that create synergy and a decreasing importance of the share of port dues in the total revenue mix.

Author Contributions

Funding

Conflicts of Interest

References

- Sullivan, A.; White, D.D.; Larson, K.L.; Wutich, A. Towards Water Sensitive Cities in the Colorado River Basin: A Comparative Historical Analysis to Inform Future Urban Water Sustainability Transitions. Sustainability 2017, 9, 761. [Google Scholar] [CrossRef] [Green Version]

- Nasi, M.H.A.; Genovese, A.; Acquaye, A.A.; Koh, S.C.L.; Yamoah, F. Comparing linear and circular supply chains: A case study from the construction industry. Int. J. Prod. Econ. 2017, 183, 443–457. [Google Scholar] [CrossRef]

- Bocken, N.M.P.; de Pauw, I.; Bakker, C.; van der Grinten, B. Product design and business model strategies for a circular economy. J. Ind. Prod. Eng. 2016, 33, 308–320. [Google Scholar] [CrossRef] [Green Version]

- Graedel, T.E.; Allwood, J.; Birat, J.P.; Rech, B.K.; Sibley, S.F.; Sonnemann, G.; Buchert, M.; Gaheluken, C. Recycling Rates of Metals—A Status Report; A Report of the Working Group on the Global Metal Flows to International Resource Panel; United Nations Environment Programme: Nairobi, Kenya, 2011. [Google Scholar]

- De Langen, P.; Sornn-Friese, H. Ports and the Circular Economy. In Green Ports. Inland and Seaside Sustainable Strategies; Bergqvist, R., Monios, J., Eds.; Elsevier: Amsterdam, The Netherlands, 2018. [Google Scholar]

- Carpenter, A.; Lozano, R.; Samalisto, K.; Astner, L. Securing a port’s future through Circular Economy: Experiences from the Port of Gävle in contributing to sustainability. Mar. Pollut. Bull. 2018, 128, 539–547. [Google Scholar] [CrossRef] [PubMed]

- De Langen, P.W.; Heij, C. Corporatisation and performance: A literature review and an analysis of the performance effects of the corporatisation of port of Rotterdam authority. Transp. Rev. 2014, 34, 396–414. [Google Scholar] [CrossRef]

- De Langen, P.W.; van der Lugt, L.M. Institutional reforms of port authorities in The Netherlands; the establishment of port development companies. Transp. Bus. Manag. 2017, 22, 108–113. [Google Scholar] [CrossRef]

- Ezzat, A.M. Sustainable Development of Seaport Cities through Circular Economy: A Comparative Study with Implications to Suez Canal Corridor Project. Eur. J. Sustain. Dev. 2016, 5, 509–522. [Google Scholar] [CrossRef] [Green Version]

- Kringelum, L.T.B. Transcending Organizational Boundaries: Exploring Intra-and Inter-Organizational Processes of Business Model Innovation in a Port Authority. Ph.D. Thesis, Aalborg Universitetsforlag, Aalborg, Denmark, 2017. [Google Scholar]

- Kringelum, L.T.B. Reviewing the challenges of port authority business model Innovation. World Rev. Intermodal Transp. Res. 2019, 8, 265–291. [Google Scholar]

- Duriau, V.J.; Reger, R.K.; Pfarrer, M.D. A Content Analysis of the Content Analysis Literature in Organization Studies. Research Themes, Data Sources, and Methodological Refinements. Organ. Res. Methods 2007, 10, 5–34. [Google Scholar] [CrossRef] [Green Version]

- Puig, M.; Wooldridge, C.; Darbra, R.M. Identification and selection of Environmental Performance Indicators for sustainable port development. Mar. Pollut. Bull. 2014, 81, 124–130. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Li, Y.; Richardson, G.D.; Vasvan, F. Revising the relation between environmental performance and environmental disclosure: An empirical analysis. Accounting, Organ. Soc. 2008, 33, 303–327. [Google Scholar] [CrossRef]

- Santos, S.; Rodrigues, L.L.; Branco, M.C. Online sustainability communication practices of European seaports. J. Clean. Prod. 2016, 112, 2935–2942. [Google Scholar] [CrossRef]

- Lewandowski, M. Designing the Business Models for Circular Economy—Towards the Conceptual Framework. Sustainability 2016, 8, 43. [Google Scholar] [CrossRef] [Green Version]

- Van der Lugt, L.M.; de Langen, P.W. Value creation and value capture in the port’s business. In Port Management, Cases in Port Geography, Operations and Policy; Petitt, S., Beresford, A., Eds.; Kogan Page: London, UK, 2018; pp. 13–27. [Google Scholar]

- Martins, N.O. Ecosystems, strong sustainability and the classical circular economy. Ecol. Econ. 2016, 129, 32–39. [Google Scholar] [CrossRef]

- Valkokari, K. Business, innovation, and knowledge ecosystems: How they differ and how to survive and thrive within them. Technol. Innov. Manag. Rev. 2015, 5, 17–24. [Google Scholar] [CrossRef]

- Cennamo, C.; Gawer, A.; Jacobides, M.G. Towards a theory of ecosystems. Strateg. Manag. J. 2018, 39, 2255–2276. [Google Scholar]

- Power, T.; Jerjian, G. Ecosystem: Living the 12 Principles of Networked Business; Financial Times Management: London, UK, 2001. [Google Scholar]

- Bichou, K.; Gray, R. A critical review of conventional terminology for classifying seaports. Transp. Res. Part A Policy Pract. 2005, 39, 75–92. [Google Scholar] [CrossRef]

- Dhanaraj, C.; Parkhe, A. Orchestrating innovation networks. Acad. Manag. Rev. 2006, 31, 659–669. [Google Scholar] [CrossRef] [Green Version]

- Gulati, R.; Puranam, P.; Tushman, M. Meta-organization design: Rethinking design in interorganizational and community contexts. Strateg. Manag. J. 2012, 33, 571–586. [Google Scholar] [CrossRef]

- De Langen, P.W.; Visser, E.J. Collective action regimes in seaport clusters: The case of the Lower Mississippi port cluster. Transp. Geogr. 2004, 13, 173–186. [Google Scholar] [CrossRef]

- Helfat, C.E.; Raubitschek, R.S. Dynamic and integrative capabilities for profiting from innovation in digital platform-based ecosystems. Res. Policy 2018, 47, 1391–1399. [Google Scholar] [CrossRef]

- Iansiti, M.; Levien, R. Strategy as Ecology. Harv. Bus. Rev. 2004, 82, 68–78. [Google Scholar] [PubMed]

- van der Lugt, L.; De Langen, P.W.; Hagdorn, L. Beyond the landlord: Worldwide empirical analysis of port authority strategies. Int. J. Shipp. Transp. Logist. 2015, 7, 570–596. [Google Scholar]

- De Langen, P.W. The Performance of Seaport Clusters; a Framework to Analyze Cluster Performance and an Application to the Seaport Clusters of Durban, Rotterdam and the Lower Mississippi 2004 (No. ERIM PhD Series; EPS-2004-034-LIS). Available online: https://www.erim.eur.nl/smartporterasmus/publications/books/detail/2597-the-performance-of-seaport-clusters-a-framework-to-analyze-cluster-performance-and-an-application-to-the-seaport-clusters-of-durban-rotterdam-and-the-lower-mississippi/ (accessed on 20 February 2020).

- Verhoeven, P. A review of port authority functions: Towards a renaissance? Marit. Policy Manag. 2010, 37, 247–270. [Google Scholar] [CrossRef]

- Teece, D.J. Explicating dynamic capabilities: The nature and microfoundations of (sustainable) enterprise performance. Strateg. Manag. J. 2007, 28, 1319–1350. [Google Scholar] [CrossRef] [Green Version]

- Gerring, J. What is a case study and what is it good for? Am. Political Sci. Rev. 2004, 98, 341–354. [Google Scholar] [CrossRef] [Green Version]

- Eisenhardt, K.M. Building theories from case study research. Acad. Manag. Rev. 1989, 14, 532–550. [Google Scholar] [CrossRef]

- Ridder, H.-G. The theory contribution of case study research designs. Bus. Res. 2017, 10, 281–305. [Google Scholar] [CrossRef] [Green Version]

- Piekkari, R.; Welsh, C.; Paavilainen, E. The Case Study as Disciplinary Convention. Evidence from International Business Journal. Organ. Res. Methods 2009, 12, 567–589. [Google Scholar] [CrossRef]

- Lopez, F.J.D.; Bastein, T.; Tukker, A. Business model innovation for resource-efficiency, circularity and cleaner production: What 143 cases tell us. Ecol. Econ. 2019, 155, 20–35. [Google Scholar] [CrossRef]

- Flick, U. An Introduction to Qualitative Research, 5th ed.; Sage: London, UK, 2019. [Google Scholar]

- Port of Amsterdam. Circular Companies in Port of Amsterdam. Available online: https://myport.portofamsterdam.com/en/portle/service/industries?f%5B0%5D=services%3A41). (accessed on 20 February 2020).

- Port of Amsterdam. Feiten en Cijfers 2018. Available online: https://www.portofamsterdam.com/sites/poa/files/media/pdf-nl/feiten-en-cijfers-2018-port-of-amsterdam.pdf (accessed on 20 February 2020).

- Gemeente Amsterdam. Uitvoeringsplan. 2016. Available online: https://www.amsterdam.nl/bestuur-organisatie/volg-beleid/afval-en-schoon/ (accessed on 19 March 2020).

- Port of Amsterdam. Visie 2030, Port of Amsterdam, Port of Partnerships. 2015. Available online: https://www.portofamsterdam.com/nl/havenbedrijf/visie-2030 (accessed on 15 February 2020).

- Jonsson, D. Sustainable infrasystem synergies: A conceptual framework. Urban Technol. 2000, 7, 81–104. [Google Scholar] [CrossRef]

- Van den Heuvel, F.; Van Donselaar, K.; De Langen, P.; Fransoo, J. Co-Location Synergies: Specialised Versus Diverse Logistics Concentration Areas. Tijdschr. Voor Econ. Soc. Geogr. 2016, 107, 331–346. [Google Scholar] [CrossRef]

- Williams, J. Circular cities. Urban Stud. 2019, 56, 2746–2762. [Google Scholar] [CrossRef]

- Sheffi, Y. Logistics Clusters: Delivering Value and Driving Growth; MIT Press: Cambridge, MA, USA, 2012. [Google Scholar]

- Port of Amsterdam. Corporate Information. 2020. Available online: https://www.portofamsterdam.com/en/business/settlement/port-amsterdam-perfect-hub-circular-economy (accessed on 27 March 2020).

- Hollen, R.M.A.; van den Bosch, F.A.J.; Volberda, H.W. Strategic levers of port authorities for industrial ecosystem development. Marit. Econ. Logist. 2015, 17, 79–96. [Google Scholar] [CrossRef]

- Lozano, R.; Fobbe, L.; Carpenter, A.; Sammalisto, K. Analysing sustainability changes in seaports: Experiences from the Gävle Port Authority. Sustain. Dev. 2019, 27, 409–418. [Google Scholar] [CrossRef]

- Bahers, J.B.; Tanguy, A.; Pincetl, S. Metabolic relationships between cities and hinterland: A political-industrial ecology of energy metabolism of Saint-Nazaire metropolitan and port area (France). Ecol. Econ. 2020, 167, 106–447. [Google Scholar] [CrossRef]

- Mahoney, J.; Rueschemeyer, D. Comparative Historical Analysis in the Social Sciences; Cambridge University Press: Cambridge, UK, 2003. [Google Scholar]

- Zhang, Q.; Zheng, S.; Geerlings, H.; El Makhloufi, A. Port governance revisited: How to govern and for what purpose? Transp. Policy 2019, 77, 46–57. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

| Country | Number of Ports in Database | Number of Ports With at Least 1 New CE Activity | % Ports With at Least 1 New CE Activity | Average Number of New CE Activities in Ports |

|---|---|---|---|---|

| Belgium | 4 | 4 | 100% | 3.8 |

| Slovenia | 1 | 1 | 100% | 3.0 |

| The Netherlands | 12 | 7 | 58% | 2.3 |

| Latvia | 3 | 1 | 33% | 1.0 |

| Finland | 15 | 4 | 27% | 0.6 |

| Sweden | 25 | 6 | 24% | 0.4 |

| France | 26 | 6 | 23% | 0.6 |

| Ireland | 5 | 1 | 20% | 0.6 |

| Germany | 20 | 4 | 20% | 0.4 |

| Denmark | 22 | 4 | 18% | 0.4 |

| Croatia | 7 | 1 | 14% | 0.1 |

| Estonia | 8 | 1 | 13% | 0.1 |

| Greece | 25 | 2 | 8% | 0.2 |

| Italy | 39 | 1 | 3% | 0.0 |

| Bulgaria | 2 | 0 | 0% | 0.0 |

| Cyprus | 2 | 0 | 0% | 0.0 |

| Lithuania | 1 | 0 | 0% | 0.0 |

| Malta | 4 | 0 | 0% | 0.0 |

| Poland | 4 | 0 | 0% | 0.0 |

| Portugal | 13 | 0 | 0% | 0.0 |

| Romania | 5 | 0 | 0% | 0.0 |

| Spain | 37 | 0 | 0% | 0.0 |

| Port | Number of CE Initiatives |

|---|---|

| Amsterdam | 8 |

| Nantes-St Nazaire | 6 |

| Antwerp | 5 |

| Oostende | 5 |

| Helsinki | 5 |

| Delfzijl/Eemshaven | 5 |

| Zeebrugge | 4 |

| Thessaloniki | 4 |

| Rotterdam | 4 |

| Copenhagen-Malmö | 3 |

| Le Havre | 3 |

| Marseille | 3 |

| Hamburg | 3 |

| Dublin | 3 |

| Ventspils | 3 |

| Moerdijk | 3 |

| Koper | 3 |

| Aalborg | 3 |

| Categories of CE Activities | Number of Companies | Of Which Full Transformation |

|---|---|---|

| Recycling of plastics and rubber | 5 | 3 |

| Demolition waste recycling | 2 | 0 |

| Recycling of food and agricultural residues | 7 | 7 |

| Metals recycling | 4 | 0 |

| General waste processing | 3 | 1 |

| Example CE in Amsterdam | Number of Firms Benefitting from This Synergy Effect | |

|---|---|---|

| Logistics infrastructure and services synergy | Scrap recycling company exports scrap in containers overseas, using the container terminal in Amsterdam. | 20 |

| Input Output Synergy | Oils and fats recycling company sources its fats from a nearby waste collection company. | 20 |

| Industrial ecology synergy | A producer of bioelectricity uses dedicated electricity connection to put the electricity in the grid. | 4 |

| Segment | Spatial Scale Inputs | Spatial Scale Outputs |

|---|---|---|

| Recycling of plastics and rubber | Mainly continental. There are no substantial overseas import flows of plastics waste; there are overseas imports of used car tires from small niche markets such as Iceland. | Mainly continental, even though some products, such as fuels and tiles made from plastics, are traded internationally. |

| Demolition waste recycling | Continental, and mainly local. Demolition waste is not traded internationally. | Continental. The demolition waste is generally sorted by waste companies and further processed by other firms in Amsterdam’s CE ecosystem. |

| Recycling of food and agri residues | Mostly continental. Imported flows of food and agri residues from overseas are limited; commodities like used cooking oil (UCO) are imported from overseas. | In case of biofuels, the market is international. High value products may export overseas; currently, volumes exported overseas are limited. |

| Metals recycling | Continental, and mainly local. Metal waste is not traded or shipped over long distances. | Mainly international. Scrap (in various qualities) is often traded internationally, e.g., to India or Turkey where the metal scrap is either rerolled or melted for recycling. |

| General waste processing | Mostly local, even though the state-owned waste processing installation imports waste from the UK. | Mostly local. The processed waste is mainly sold to other companies in Amsterdam’s ecosystem. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

de Langen, P.W.; Sornn-Friese, H.; Hallworth, J. The Role of Port Development Companies in Transitioning the Port Business Ecosystem; The Case of Port of Amsterdam’s Circular Activities. Sustainability 2020, 12, 4397. https://doi.org/10.3390/su12114397

de Langen PW, Sornn-Friese H, Hallworth J. The Role of Port Development Companies in Transitioning the Port Business Ecosystem; The Case of Port of Amsterdam’s Circular Activities. Sustainability. 2020; 12(11):4397. https://doi.org/10.3390/su12114397

Chicago/Turabian Stylede Langen, Peter W., Henrik Sornn-Friese, and James Hallworth. 2020. "The Role of Port Development Companies in Transitioning the Port Business Ecosystem; The Case of Port of Amsterdam’s Circular Activities" Sustainability 12, no. 11: 4397. https://doi.org/10.3390/su12114397

APA Stylede Langen, P. W., Sornn-Friese, H., & Hallworth, J. (2020). The Role of Port Development Companies in Transitioning the Port Business Ecosystem; The Case of Port of Amsterdam’s Circular Activities. Sustainability, 12(11), 4397. https://doi.org/10.3390/su12114397