1. Introduction

Today, enterprises are increasingly contributing to the progressive degradation of existing ecosystems by emitting huge amounts of hazardous pollutants and excessive use of available natural resources, causing a serious threat to our planet’s biodiversity. Hence, there is a need to take varied measures to stop the degradation of the environment by human activity. Initiatives aimed at mere neutralization of produced pollutants are no longer sufficient. It is necessary to search for solutions to reduce the environmental burden of business activity at all phases of the production process, from the designing stage and production planning to every stage of the manufacturing process [

1].

The key event that influenced the recognition of the importance of corporate social responsibility (CSR) was a 2004 publication by the European Commission, a document entitled “Green Paper on CSR”. The document postulates that social responsibility has become an integral part of management in European enterprises and an everyday practice followed by owners and managers. Such approach, however, takes a profound change in the way enterprises are run, as well as new managerial skills, competences, and mental change among both managerial staff and employees. The analysis of the evolution of the theory of corporate social responsibility in the theory of management [

2] points to the changing characteristics of the relation between business and society over time. These differences determine the way entities interact and collaborate. The last 20 years was a period of growing importance and presence of CSR practices, which can be attributed to evident economic, social, and ecological benefits resulting therefrom. Corporate social responsibility, understood as respecting voluntarily social and ecological aspects of business operations and in relations with stakeholders, has become a commonplace concept in Poland.

Corporate Social Responsibility (CSR) towards the natural environment is a concept of conducting business activities—according to which the companies, in strict compliance with law, and while still making profits—voluntarily take into consideration the impacts of their operations on the environment in their business decisions. Such an approach contributes to improving the quality of life and implementing the concept of sustainable development.

Socially responsible entities assume responsibility for ecological ramifications of their activities, strive to eliminate pollutions and emissions of harmful substances, and attempt to increase the efficiency of using natural resources; thus, alleviating their ecological footprints [

3].

One should remember that fast economic growth connected with intense exploitation of natural resources is in overt contradiction with the need to preserve these resources for future generations. In fact, every nation can use available resources for the benefit of its people; however, nations are also responsible for their protection and preservation for the generations to come [

4].

A review of literature on corporate social responsibility shows that a large portion of studies carried out so far concerned whole organizations and their impacts on different groups of stakeholders. Social responsibility was considered in the context of profitability for the organizations undertaking socially responsible activities [

5,

6,

7]. A. Glavas notes that there are three main trends in the debate on corporate social responsibility [

8]. The first one concerns the role of enterprises in society. The main question, oftentimes put by default, is whether the companies play a role in societies beyond generating profit. The second trend in the debate is about whether corporate social responsibility is normative, which means that the companies have an obligation to get involved in socially responsible undertakings, or instrumental, i.e., it is in the company’s best interest to get involved in CSR actions. If CSR is normative, companies have a moral obligation toward society to care about its well-being [

9]. Other authors opt for combining normative nature of CSR with instrumental. The third trend of the debate is focused on the impacts of CSR on the company’s financial performance. Proving that the company’s involvement in CSR can generate additional profit makes other reasons (normative or instrumental) irrelevant as CSR is about doing good for both the company and society [

8].

According to the World Business Council for Sustainable Development, CSR is crucial to sustainable economic development and the well-being of societies [

10]. This is the reason why there is a need for in-depth studies on the profitability of socially responsible activities towards the silent stakeholder, the environment. Eco-management is aimed at reducing negative impacts the businesses exert on the environment. Increasing social awareness is forcing businesses to reduce their environmental burden.

In the short run, the relations between ecological and economic goals compete. However, as some authors argue, environmental protection can turn out to be a way to improve financial standing of the company by lowering the costs of energy, raw materials, etc. [

11].

The goal of this paper is to present the research findings of the study carried out in 2019 and to compare them with the study carried out 10 years earlier, in 2009, in order to establish the differences in approach to pro-environmental activities and evaluate the most frequent environmental initiatives undertaken by enterprises in the Lublin region.

2. Literature Review

One of the most frequently quoted definitions explaining the essence of corporate social responsibility, or CSR, is a definition proposed by Archie B. Carroll [

12]. A.B. Caroll asserts that CSR encompasses the economic, legal, ethical, and philanthropic expectations that society has of organizations at a given point in time [

12] (p. 500). Caroll refers to the concept of social responsibility in which the most important task of the company is to generate profit. Therefore, he claims that the company’s involvement in sponsoring charity programs or campaigns, when it actually is incurring financial losses and replacing economic goals, for which businesses are set up with social goals only, is irrational [

13] (pp. 315–316). However, it is important that the way the company generates revenues is honest, and a fast-growing profit is not a top priority that overshadows other goals.

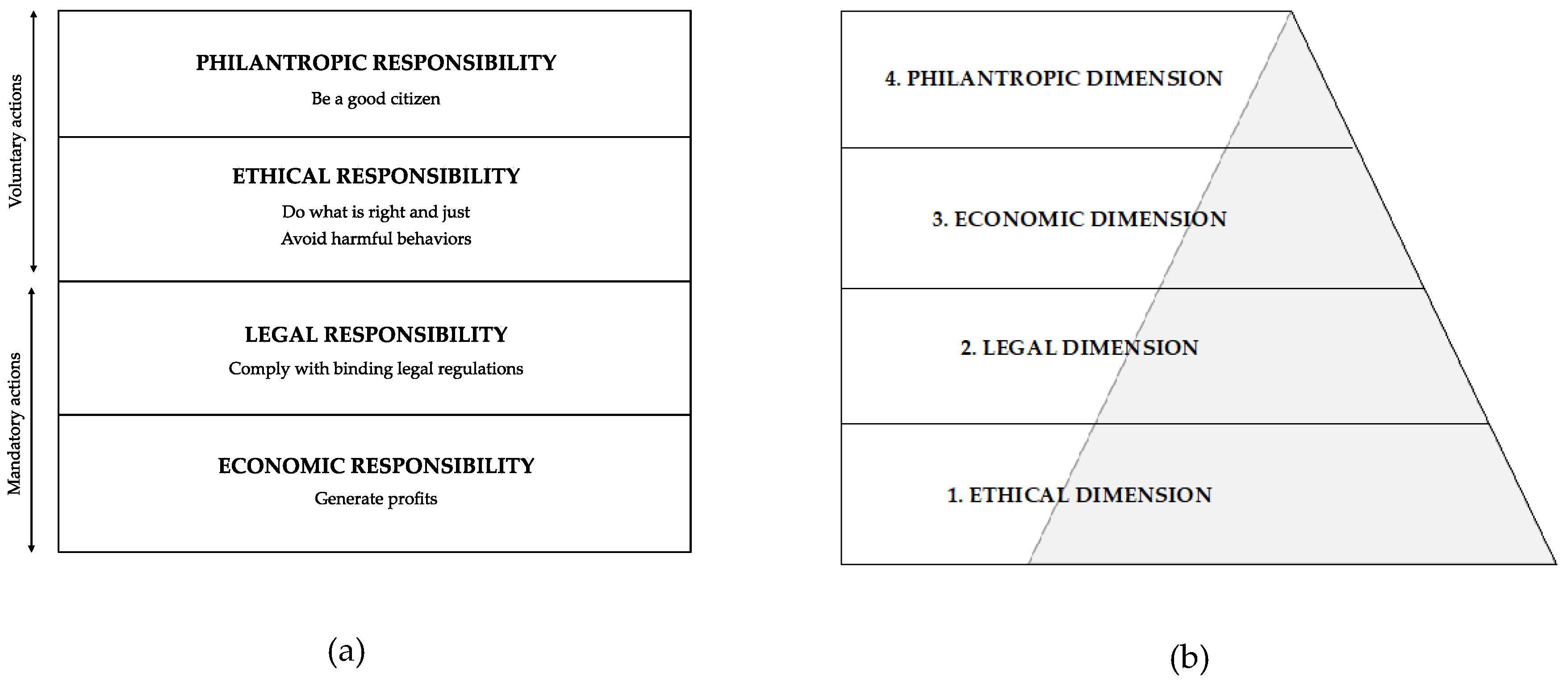

The base of Caroll’s model is economic responsibility (

Figure 1a). Caroll argues that enterprises should be profitable in the first place [

14] (p. 55). The legal component of his model includes the firm’s responsibility, such as the requirement to operate in a manner consistent with the law, and other binding applicable regulations, which determine the frameworks for the firm’s operations and reflect the concept of proper business practices. Businesses should obey existing environmental protection regulations, respect consumer rights, employee rights, and keep to all contractual obligations they agreed upon [

15] (p. 3). Although law is based on ethical premises, ethical dimension of social responsibility is about something more, it concerns social expectations, which may not be incorporated into law. Activities performed by enterprises should reflect the spirit of the law [

15] (p. 29); [

16] (p. 3). The philanthropic component of social responsibility includes the requirement to devote part of the firm’s resources (e.g., financial resources or labor time) to gratify the needs of society and communities.

Denise Baden [

17] presents a different view: placing the ethical and legal responsibilities before the economic ones, as she argues that the way enterprises pursue their business goals is very important. In Baden’s view, enterprises should accept their ethical responsibility, which means that they should refrain from any harmful activity, and in their operations, should take account of social expectations; that is the right foundation for generating profit and multiplying values (

Figure 1b).

In Polish and foreign literature alike, we can observe a growing interest in the concept of corporate social responsibility. This resulted in many research approaches. Some analyses seem to be incomplete which creates problems with interpretation of proposed CSR definitions. For example, A. Dahlsrud [

18] identified at least 37 definitions of CSR. Most approaches, however, put emphasis on the influence of CSR on economic, social, and ethical spheres of activity of enterprises [

19] (pp. 51–57). Until recently, the concept of social responsibility was studied through the prism of potential benefits for enterprises and related stakeholders [

20]. However, at the end of the 20th century, in the face of growing environmental challenges, many authors started to point to ecological aspects of corporate social responsibility as well.

Contemporary definitions of corporate social responsibility highlight the increased expectations of enterprises in ethical, ecological, social, and economic spheres (

Table 1).

Presently, the concept of corporate social responsibility associated with care of the environment, justice, and social order, and ethical conduct of enterprises, creates a real chance to implement principles of sustainable development at the lowest level—enterprises and entrepreneurs, employees and local residents [

26]. There are works to develop the conceptual framework for the description of the concept of sustainability tailored from the systemic perspective, the perspective of individual entities, and their role in creating the foundations of sustainable society [

27]. There are also studies concerning the perception of various CSR initiatives and programs by different groups of stakeholders, in particular employees, the addressees whose voices are important in the process of decision-making and implementing [

28]. It is also possible to evaluate the results of implementation of the “Green Human Resources Management” (GHRM), as well as an assessment based on an effective scale of measuring corporate social responsibility in the following three areas: economy, society, and the environment [

29].

It is assumed that socially responsible entities bear the consequences of ecological effects of their activities, strive to eliminate pollution, emission of harmful substances, and take steps to maximize the efficiency of using natural resources and minimize negative impact on the environment [

3]. This is the reason why, for some authors, the concept of corporate social responsibility is a synonym of the concept of sustainability, translated as sustainable development [

30] (p. 725); [

31] (p. 81); [

32] (p. 36), while other authors, in their definitions of social responsibility, refer directly to the concept of sustainable development [

21]. An attempt to tell the difference between sustainability and corporate social responsibility (CSR) is a difficult task, as I. Montiel pointed out in his extensive analysis [

33]. It is characteristic that the three key elements of sustainability at the corporate level have economic, social, and environmental dimensions [

34] (p. 132). However, many authors differentiate between the concept of sustainability and CSR, pointing to the differences in time activities and effects interact between the present and the future.

A.B. Carroll [

16] maintains that his model of the pyramid reflects responsibilities towards the present stakeholders, as well as the future generations of stakeholders.

Other authors distinct CSR from sustainability, explaining that the concept of sustainability time is crucial. P. Bansal [

35] argues that in order to ensure sustainable development at the organization’s level, it is essential to implement the following three principles: environmental integrity, which can be achieved by environmental management, social equity, which can be achieved by corporate social responsibility (CSR), and economic prosperity, which can be achieved by creating values. Krajnakova, E., Navickas, V., and Kontautiene, R. [

36] analyzed trends in the development of CSR in different periods of the economic cycle. Their research shows that strong socio-cultural ties, favorable cultural and legal climate, as well as scientific progress and technological innovations, exert a positive influence on the development of CSR. Climate changes and lasting ecological crises force enterprises to engage more actively in environmental issues. Rising inflation and growing unemployment rates, and decreasing consumer confidence result in a greater emphasis of businesses put on social and economic solutions. The authors of the study [

36] pointed out that, regardless of the fluctuations in the macro-economic environment of both economic and non-economic nature, both businesses and society, at large, are more actively contributing to the promotion of CSR ideas and practices.

The assumption that businesses should consider ethical aspects of their activities in the first place, however, does not exempt them from pursuing economic goals. The impact of business activity on cost accounting is significant, and environmental protection and cost accounting are becoming mutually supportive elements. As E. Seidel noted, environmental costing is a pivotal instrument of pro-ecological management in enterprises and an indispensable component on the way to sustainable management. Unfortunately, giving a general definition of environmental costs is a quite challenging task [

37] (p. 360) due to varied approaches and changing understanding of environmental costs over time.

Nowadays, it is commonly recognized that using and protecting the environment are essential parts of business processes that generate costs for enterprises. Environmental protection costs in enterprises can be divided into internal and external costs [

38] (p. 55). From the economic viewpoint of the enterprise, the most important are the total internal costs of environmental protection. Environmental protection costs are the sum of all investment outlays and current expenditures borne by the enterprise to reduce its environmental burden, by safe storing, preventing, neutralizing, reducing, or eliminating pollutions and/or environmental damage.

Environmental management can yield numerous benefits for enterprises, including costs and resources savings, increased satisfaction and loyalty of customers and morale of employees [

39].

In addition to research on the relationship between socially responsible activity and financial results, particularly important are studies that indicate the relationship between corporate responsibility and its impact on financial results that have been achieved through effective management of the company’s intangible resources, such as innovation, human capital, goodwill, and culture [

40], value for stakeholders, including consumers [

41], and measurement of consumer perception of the company’s socially responsible activity in different areas [

42].

From the 1990s, the European Community has supported active environmental policy instruments, including Environmental Management Systems (EMS) [

43]. By implementing such systems, enterprises can demonstrate their active approach to environmental protection issue [

44].

The European Commission developed the European Union (EU) Eco-Management and Audit Scheme (EMAS) to be used by companies and other organizations in order to reduce their environmental footprints. The EMAS registration procedures evolved over time; initially, they were time-consuming and were addressed only to industrial establishments. Then, the EMAS regulation was revised to make it easier for other organizations to comply with the regulation, including public administration [

45]. The Environmental Management Systems (EMS), such as ISO (International Organization for Standardization) or EMAS (Eco-Management and Audit Scheme), are designed to ensure a high level of environmental protection and competitive advantage of organizations resulting from introduced improvements. Moreover, they include instruments to inform the public and local communities about undertaken activities, such as environmental reports.

Economic and fiscal instruments have a strong impact on enterprises stimulating ecological, pro-environmental efforts. In economic theory on the environment, the basic economic and market regulations include taxes and fees on emissions of certain pollutants, public subsidies to businesses, and transferable polluting emission allowances [

46] (p. 293). The purpose of these economic mechanisms is to ensure [

47]: the rational use of the environment and its resources, ecological and economic efficiency of economic activity, enforcement of binding environmental protection regulations, as well as effective and efficient absorption of the EU aid addressed to ecological purposes.

3. Materials and Methods

Entrepreneurs face numerous challenges in terms of implementation of sustainable development principles. Hence, the need to evaluate their impacts on the environment and its components and assess activities they undertake in order to minimize their negative impact on the quality of water, air, and soil. It was interesting to discover the most effective drivers inducing decision-makers to take actions aimed at reducing the environmental footprints of businesses, as well as what kinds of investments are most frequent, and whether they are profitable. Therefore, in 2009, and a decade later in 2019, we carried out research to primarily identify the economic, environmental, and technological effects of completed pro-ecological investments, sources of financing ecological investments, and the levels of investment outlays by investment directions (incurred and planned). We also looked at the factors encouraging socially responsible actions towards the environment, and barriers and obstacles hampering such activity. A substantial part of the research findings from the study is presented in this paper. The authors put forward the following thesis: socially responsible activities towards the environment are an investment for businesses, not a cost.

The following research questions were considered:

What socially responsible ventures toward the natural environment are most often undertaken by the entities covered by the study?

What is the return on investment period?

What economic instruments are, in the respondents’ opinions, the most effective?

Is a socially responsible approach to the environment perceived as a cost or rather an investment for the future?

The 2009 study included enterprises in which activity had a significant impact on the environment in the Lublin region. These enterprises were tipped, based on the Regulation of the Minister of the Environment (26 July, 2002) on the types of installations that may significantly pollute the natural environment or its particular parts (Journal of Laws of 2002, No. 122, item 1055). The research sample, of 103 enterprises, was established in line with this regulation by the Voivodeship Office, the Regional Inspectorate of the Environmental Protection, and self-government units in Lublin Voivodeship. Of 103 enterprises included in the study, 52 entities returned completed questionnaires, 36 either failed to return the questionnaire or returned incomplete questionnaires, which prevented its analysis, 2 entities went into liquidation, and 13 refused to participate in the study.

In 2019, research on social responsibility towards the environment was repeated. This time the research sample, of 100 entities, was selected based on the new regulation of the Minister of the Environment of 27 August, 2014 (Journal of Laws of 2014, item 1169). A total of 48 entities returned properly completed questionnaires, 32 failed to return the questionnaire, and 20 enterprises refused to take part in the study.

The data were collected using direct measurement methods and dedicated tools. The research was carried out using a questionnaire on the identification of social responsibility of regional enterprises towards the environment. In the process of data reduction, raw data were subjected to the selection, coding, classification, and description. At this point, we obtained ordered data in tabular, graphic, and descriptive forms. At this stage, the acquired data were analyzed in terms of their completeness and legibility.

Collected data were analyzed based on the structure of received responses. Data from the questionnaires were processed using the spreadsheet software MS Excel, which enabled us to work out various cross-section collations used to develop a final report from the surveys.

4. Results and Discussion

Our research has shown that in the Lublin Voivodeship, social responsibility is identified with running a business that cares for the environment and its resources. This is a very promising sign that the principles of sustainable development and eco-management rules will be effectively put into practice by entrepreneurs.

The study shows that in 2019 most regional entrepreneurs (81%) undertook socially responsible pro-environmental activities aimed at reducing waste and harmful emissions to water and soil by implementing innovative technologies, and/or investment, in pro-environmental infrastructure. This means they responsibly consider the impacts of their activities on different resources and seek solutions that help minimize these impacts. Regional entrepreneurs also engage their employees and encourage them to save paper, energy, and water (almost 70% of respondents), while 67% of respondents declared that they run laboratory tests in order to monitor the impacts on the environment and, if necessary, undertake swift corrective action when any risk of excessive emission appears. Significantly less businesses pointed to the implementation of the ISO 14000 norms, Eco-Management and Audit Scheme (EMAS), or Clean Production Principles (38% of indications). Likewise, as little as 33% of respondents declared investments in renewable energy sources, which are, by far, a greater financial burden for businesses and require long-term capital commitments.

The analysis of the reasons that encourage entrepreneurs to make pro-ecological investments indicates that the main arguments for these actions changed slightly over the last decade. In the 2019 study, the respondents declared that among the most important reasons for pro-environmental investment were the need to limit their adverse impacts on the environment, high level of awareness of their chief managers, and the willingness to minimize a harmful impact of the company on its employees and local communities. In 2009, however, more entities financed such undertakings, being forced to do so by existing legal regulations, and/or required by the competent environmental protection bodies. Invariably in both studies, environmental awareness and managers’ beliefs were very important drivers in making pro-ecological decisions (

Table 2).

The analysis of the research findings shows that entrepreneurs regard environmental social responsibility as an investment for the future. In 2019, as much as 90% of respondents indicated that such activity was an investment, not cost (42% answered “definitely yes”, and 48% answered “rather yes”).

Due to the fact that pro-environmental investments can be profitable in the long run, the respondents were asked the question about the return on the investment period. Received responses show that—in opinions of surveyed entrepreneurs—a return on investment period changed over time. In 2009, in most companies included in the study, pro-ecological investments paid back within a period of 5 to 10 years (42% indications) [

1]. In 2019, however, 29% of questioned entrepreneurs indicated that pro-ecological investments repay within 5 to 10 years, while in the opinions of 17% of respondents, such investments repay within 3–5 years; in opinions of only 10%, a return on investment period is shorter than 1 year (

Table 3).

The study shows that, in 2019, the most effective instruments of ecological policies still proved to be economic instruments. These included fees for commercial use and making modifications in the environment, the option to allocate already imposed penalties for exceeding the permissive levels of emissions to finance undertakings, eliminating the cause of such emissions, tax reliefs, credit guarantees, preferential credit terms and conditions, and penalties for excessive emissions (

Table 4).

The study confirmed that environmental protection investments made by entrepreneurs covered by the study yielded numerous benefits for them, including tangible, measurable economic gains, such as a decrease in the amount of environmental fees calculated on the size of pollutions emitted to the environment (indicated by nearly 30% of respondents). One in four entrepreneurs pointed out that such investment brought about lower operational costs, depending on the size of production and efficiency of production equipment.

The shows that the entrepreneurs still tend to finance pro-ecological investments with their own resources (96% of respondents as compared to 87% in 2009), credits and loans (33% of respondents as compared to 27% in 2009), and EU funds (31% of responses, while in 2009 it was 23%). In contrast to 2009, in 2019, the entrepreneurs declared that they used less financial means from the National or Regional Environmental Protection Fund. In 2019, as little as 6% of respondents indicated that, in previous years, they had received subsidies from the National Environmental Protection Fund, while only 15% of questioned entrepreneurs from the Regional Environmental Protection Fund.

5. Conclusions

Although, every business is meant to generate positive financial results and multiply values in order to ensure profitability, in the long run, excessive or irresponsible use of natural resources cannot be morally justified. A perspective of short-term profits cannot compromise the well-being of future generations. Therefore, when considering the management of socially responsible activities of enterprises, or corporate social responsibility (CSR), one cannot disregard the relationship between the CSR concept and sustainable development. They both relate to the same spheres of enterprise impact, and enable achieving far-reaching social, ecological, and economical goals based on ethical standards. Today, humanity is trapped in a double race. On the one hand, we feel obliged to increase the pace of scientific advancement and economic growth; on the other hand, we must stay at least one-step ahead of the ecological disaster [

48]. We need new principles governing our lives on this crowded planet [

49]. In response to these needs, the concepts of sustainable development and corporate social responsibility, or CSR, were developed. The interest of entrepreneurs in corporate social responsibility toward many groups of stakeholders is growing. This is despite the fact that many argue that implementing CSR should not be focused on charity, marketing, and public relations, and the inclusion of CSR into management programs was only an ad hoc response to the needs of society following the global financial crisis of 2008, without any significant change in the management programs [

50]. An adequate response of businesses should manifest itself in the new era of business administrators, acting not only in accordance with the general rules of business ethics and CSR principles, but also devising, planning, and implementing CSR solutions in all spheres of business administration [

51]. Moreover, environmental accounting, which purpose is to include information on the environment into typical economic accounting, and can be realized either at the level of enterprises or national economies, offers a chance for many improvements. Environmental accounting can help societies understand how they use available resources and develop new policies to facilitate sustainable use of these resources [

52]. Although environmental management practices do not always have a positive impact on the level of satisfaction of organizational clients [

49], many studies confirm that taking a stand on social issues can lead to lasting competitive advantage [

53]. Our studies have shown that enterprises operating in the Lublin region take social responsibility very seriously, undertake efforts to reduce their negative impact on the environment, and the health of their employees, and managements demonstrate a high level of ecological awareness, and see social responsibility as an investment, which, in the long run, can lead to achieving a competitive advantage.

In the Lublin region, social responsibility is associated with running economic activity respecting environmental protection needs, which, for local businesses, is an opportunity to implement the principles of sustainable development and introduce the eco-management principles. Our study shows that businesses most often undertake environmental protection activities that are aimed at minimizing waste and emission to water and soil, in particular through innovative technologies and investments in pro-environmental infrastructure. This means that enterprises responsibly analyze their impacts on different resources and seek solutions that might minimalize environmental burdens of their business operations. To this end, they stimulate their employees to save paper, energy, and water, and monitor the levels of produced emissions in order to stick to applicable emission norms and, if necessary, undertake corresponding correction actions. In 2019, as much as 90% of respondents indicated that they regard socially responsible activities toward the environment as investment, not cost. This is a very optimistic declaration that bodes well for future ecological undertakings. This is especially important, keeping in mind that overwhelming majorities of pro-ecological investments are financed with the own funds of surveyed enterprises (96% of indications). Such investment decisions are driven mostly by the need to limit their adverse ecological footprints resulting from high ecological awareness of managements. In addition to these reasons, the need to reduce harmful effects on health of the other stakeholders (i.e., employees and local communities) are also decisive.

Our study contributes to the development of knowledge base, including environmental activities undertaken by enterprises, their motivations, constraints, and barriers. Since the study concerned—in addition to other issues—financial aspects of such activities, it was sometimes difficult for us to obtain these sensitive data, which enterprises for understandable reasons were reluctant to provide. The study, which covered enterprises carrying out in Lublin Voivodeship activities onerous to the environment, was carried out twice with an interval of 10 years. In our opinion, this approach constitutes a great value of the study and provides a long-term perspective. The fact that the way enterprises regard social responsibility has not changed essentially over this 10-year period has led us to believe that the concept of corporate social responsibility has already taken root in management, decision-making processes and entrepreneurs’ mindsets.

Although our research findings are limited only to the perspective of enterprises operating in one region, it should be stressed that this is one of the cleanest regions of Poland with relatively low levels of harmful emissions as compared with the other Polish regions. Therefore, we wanted to learn about the reasons and motivations of entrepreneurs that encourage them to take environmentally friendly actions in order to prevent the degradation of the environment as a whole or its components. This is very important from the viewpoint of implementing the CSR principles and, in a wider context, sustainable development. One of the major constraints of the study resulted from the fact that only about 50% of respondents returned the questionnaire. The response ratio may suggest that the questionnaires were filled out and returned as requested only by the firms whose owners or managements have some knowledge on the CSR issues and sustainable development problems.

The analysis presented in this paper is essentially only an initial, preliminary analysis of the main directions of pro-environmental initiatives undertaken by the enterprises included in the study, and its aim is to assess the differences in the most frequent pro-environmental activities of enterprises operating in the Lublin region. However, it should be stressed that the paper is the first one in a series of articles presenting the research findings from the studies carried out in 2019, and a decade earlier, in 2009. The following papers will present further studies of socially responsible activities towards the environment and local communities.

It seems worthwhile to analyze, in future studies, socially responsible activities towards the environment undertaken by businesses in other regions of the country and then compare them with the studies carried out in other countries. Despite the presented limitations, we believe that the research findings gave us a true picture of the situation in the analyzed area.

{kind=link}