Examining the Role of Local Products in Rural Development in the Light of Consumer Preferences—Results of a Consumer Survey from Hungary

Abstract

:1. Introduction

1.1. Conceptual Approach

- -

- “Direct on-farm sales: pick your own;

- -

- direct on-farm sales: sales to individual consumers;

- -

- direct off-farm sales: internet deliveries;

- -

- direct off-farm sales: delivery to consumers;

- -

- direct off-farm sales: farmers’ markets (fairs)

- -

- sales to small retail outlets (one intermediary)” ([9] p. 5.).

1.2. The Role of Short Supply Chains in Rural Development

1.3. Characteristics of Customers Who Prefer Short Supply Chains (and Local Products)

1.4. Consumer Perception of Short Supply Chains (and Local Products)

- Revealed preference: (1) Market data, (2) experiments (laboratory experiments, field experiments, auctions);

- Stated preference: (3) Direct surveys (expert judgement, customer survey), (4) indirect survey (conjoint analysis, discrete choice analysis).

2. Materials and Methods

2.1. Background of the Primary Research

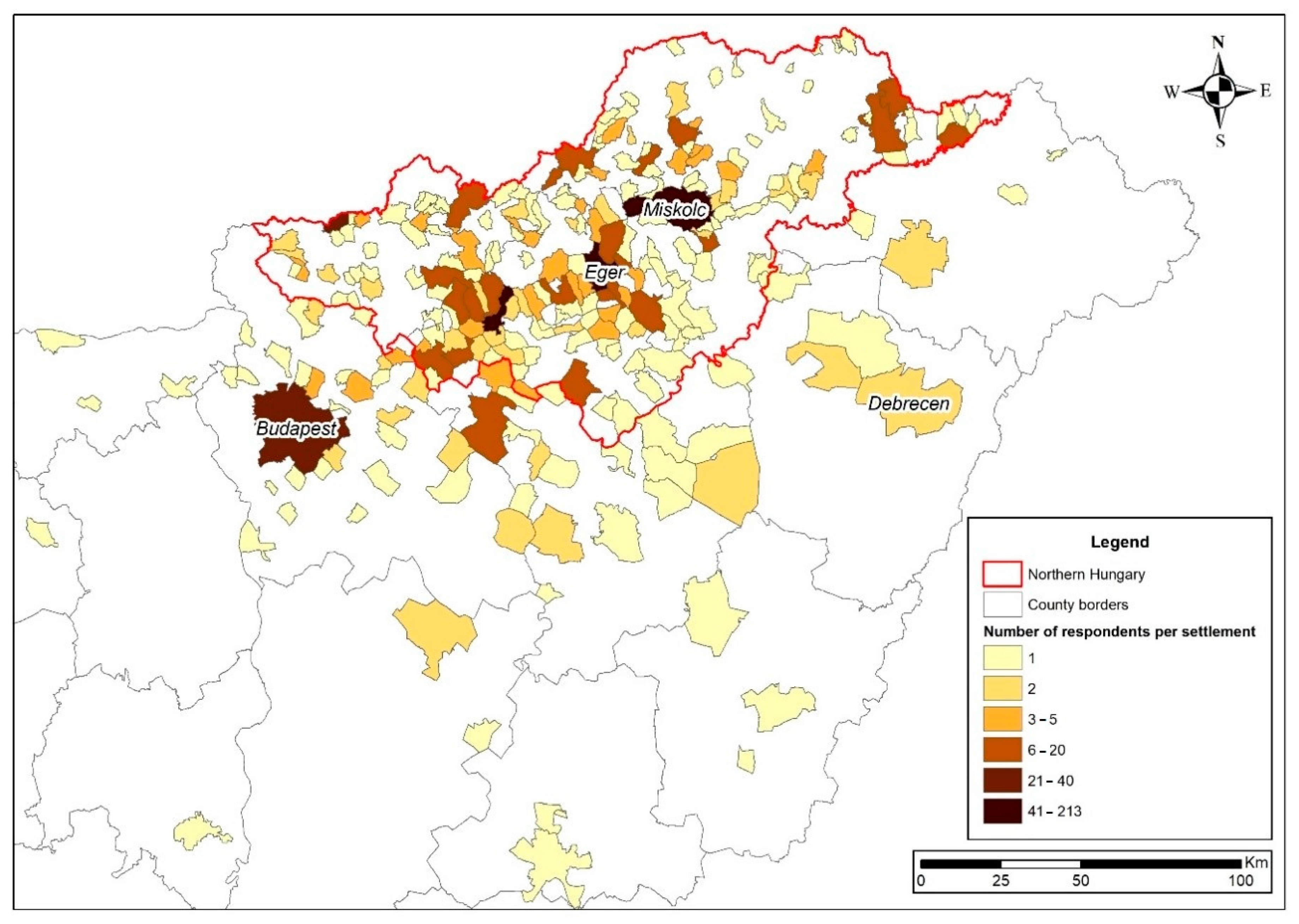

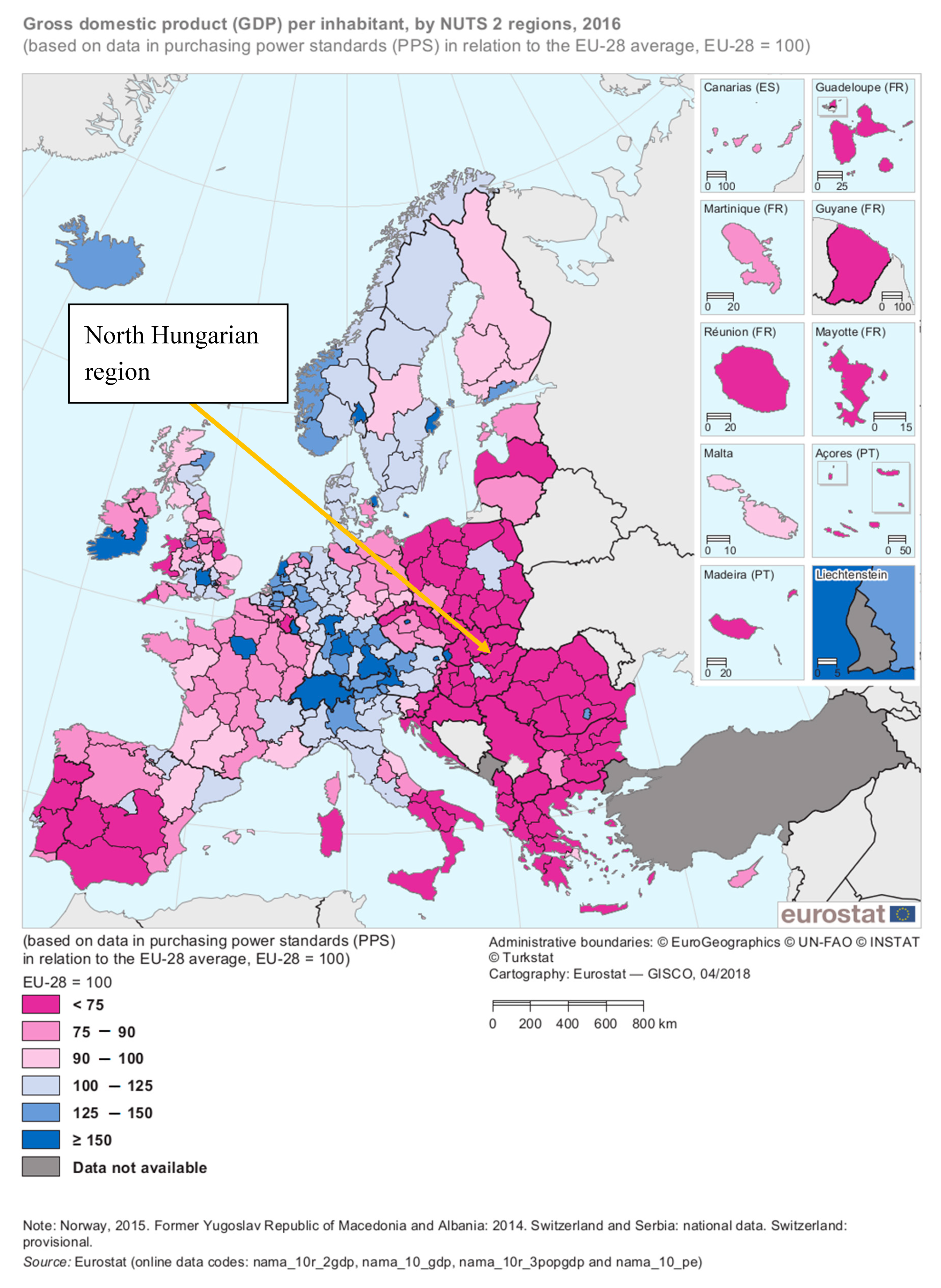

2.2. Sample Area of the Research

- Less developed regions (where GDP per inhabitant was less than 75% of the EU average);

- Transition regions (where GDP per inhabitant was between 75% and 90% of the EU average);

- More developed regions (where GDP per inhabitant was more than 90% of the EU average) [71]

3. Results

3.1. Demographic Characteristics of the Sample

- One person—8.5%

- Two people—26.7%;

- Three people—26.6%;

- Four people—25.1%;

- Five people—9.6%;

- (and some larger households and missing values) [76]

3.2. Consumer Preference for Local Products—Compared to the International Literature

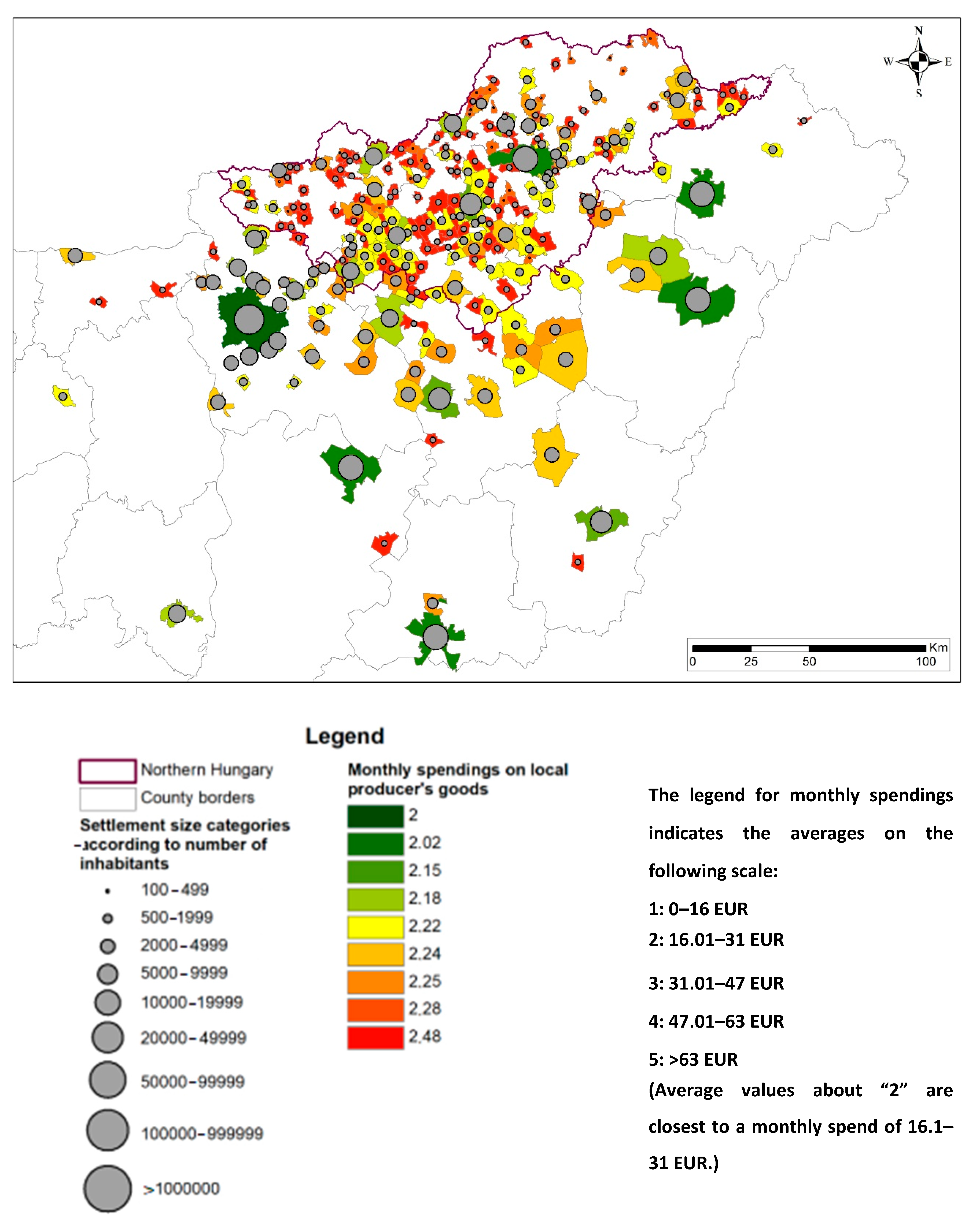

3.3. Territorial Correlations of Demand for Small Producer Goods

3.4. Further Contexts Suggesting the Importance of Local Products in Rural Settlements

- Based on our Chi-square tests, there was a statistically significant difference in people that lived in large cities and preferred the hypermarkets as food-shopping channels. The relationship is not strong (the value of the Cramer’s V coefficient showing that the strength of the relationship is 0.116).

- It showed a slightly stronger correlation (Cramer’s V: 0.128), that discount stores and supermarkets were preferred by urban respondents over those living in villages.

- In contrast, village respondents rated higher the importance of convenience stores (Cramer’s V: 0.130).

- Villagers had a slightly greater appreciation for the marketplaces as sales channels (on a five-rank scale with an average of a few hundredth-place values), but the difference is not statistically significant.

- Shopping in specialized grocery stores (such as bakeries) was less common in large cities (Cramer’s V: 0.115).

- There was a weak yet statistically significant difference in the greater importance of purchases from producers, on farms, and by home delivery in rural areas and smaller settlements. (Cramer’s V: 0.120).

- There was a strong correlation between the importance of own production and the place of residence of the respondents (Cramer’s V: 0.170). The importance of own production was highest in small villages (an average of 3.97 on the five-point Likert scale) and gradually decreased as the size of the settlement increased; in the case of large cities and metropolis, it decreased to an average of 2.45.

4. Discussion and Conclusions

- Hypermarkets, supermarkets, discount stores (to a certain extent) were preferred more by people living in larger cities.

- Small shops (as deconcentrated sales channels), as well as purchasing at the producers’ place or home delivery by producers, were more popular in the villages.

- Own growing or production as a food source was most popular in small villages, and its importance gradually decreased with the increase in the size of the settlements, which also covered a statistically stronger correlation.

- Consumers living in villages purchased more vegetables, fruits, meat and meat products from local producers than those living in cities.

- The demand for local producers’ honey was higher in villages and small towns than in large cities.

- The influence of family traditions on product choice decisions was also more characteristic in villages and small towns than in medium-sized towns.

- According to the sample, respondents from villages had a higher demand for organic products.

- In villages and small towns, consumers received more information from small producers (about their wares). This indicates a stronger nature of producer-consumer relations.

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A. Gross Domestic Product (GDP) Per Inhabitant, by NUTS 2 Regions (2016)

Appendix B. Addendum to Table 2

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Consumer Characteristics | Value of Chi-Square Test (χ2) | Decrees of Freedom (df) | Cramer’s V Coefficient |

|---|---|---|---|

| Gender | 6.09 | 4 | 0.08 |

| Age categories | 37.31 | 12 | 0.11 |

| Highest level of education | 36.83 | 12 | 0.11 |

| Marital status | 14.44 | 12 | 0.07 |

| Income level | 35.45 | 8 | 0.13 |

| Place of residence | 45.63 | 28 | 0.11 |

Appendix C. Addendum to Table 3

| Determinants of Product Choosing | Value of Chi-Square Test (χ2) | Decrees of Freedom (df) | Cramer’s V Coefficient |

|---|---|---|---|

| - price | 44.25 | 12 | 0.120 |

| - brand, manufacturer (generally) | 27.96 | 16 | 0.083 |

| - Hungarian (domestic) origin | 80.38 | 16 | 0.141 |

| - actual (price) discounts | 36.32 | 16 | 0.095 |

| - quality | 42.87 | 8 | 0.145 |

| - need for organic products | 97.46 | 16 | 0.155 |

| - uniqueness | 51.47 | 16 | 0.113 |

| - advertisements | 10.53 | 12 | - |

| - personal relationship, emotional attachment | 27.66 | 16 | 0.083 |

| - environmental awareness | 66.67 | 16 | 0.128 |

| - family traditions | 47,05 | 16 | 0,108 |

Appendix D. Addendum to Table 6

| Sales Channels | Value of Chi-Square Test (χ2) | Decrees of Freedom (df) | Cramer’s V Coefficient |

|---|---|---|---|

| - hypermarkets | 53.680 | 32 | 0.116 |

| - supermarkets | 66.505 | 32 | 0.128 |

| - convenience stores, small shops | 67.393 | 32 | 0.130 |

| - (conventional) marketplaces | 19.462 | 32 | 0.070 |

| - producers’ markets (marketplaces) | 31.460 | 32 | 0.089 |

| - specialized grocery stores (e.g., bakeries) | 52.575 | 32 | 0.115 |

| - purchasing at the producers’ place or home delivery by producers | 57.915 | 32 | 0.120 |

| - fairs, festivals | 38.014 | 32 | 0.097 |

| - online shopping | 32.133 | 32 | 0.090 |

| - own growing or production | 115.070 | 32 | 0.170 |

References

- Bazzani, C.; Caputo, V.; Nayga, R.M.; Canavari, M. Revisiting consumers’ valuation for local versus organic food using a non-hypothetical choice experiment: Does personality matter? Food Qual. Prefer. 2017, 62, 144–154. [Google Scholar] [CrossRef]

- Augère-Granier, M.-L. Short Food Supply Chains and Local Food Systems in the EU—Think Tank. Available online: http://www.europarl.europa.eu/thinktank/en/document.html?reference=EPRS_BRI(2016)586650 (accessed on 19 July 2019).

- Renting, H.; Marsden, T.K.; Banks, J. Understanding Alternative Food Networks: Exploring the Role of Short Food Supply Chains in Rural Development. Environ. Plan. A 2003, 35, 393–411. [Google Scholar] [CrossRef] [Green Version]

- Regulation (EU) No 807/2014: Commission Delegated Regulation (EU) No 807/2014 of 11 March 2014 supplementing Regulation (EU) No 1305/2013 of the European Parliament and of the Council on support for rural development by the European Agricultural Fund for Rural Development (EAFRD) and introducing transitional provision. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32014R0807&from=EN (accessed on 7 July 2020).

- Kneafsey, M.; Venn, L.; Schmutz, U.; Balázs, B.; Trenchard, L.; Eyden-Wood, T.; Bos, E.; Foster, G.; Blackett, M. Short Food Supply Chains and Local Food Systems in the EU. A State of Play of their Socio-Economic Characteristics; Publications Office of the European Union: Luxembourg, 2013; ISBN 978-9-27-929288-0. [Google Scholar]

- 52/2010 (IV.30.) MARD (The Hungarian Ministry of Agriculture and Regional Development) regulation on the conditions of the production, manufacture and sale of food by small producers (Unoffitial translation. In original Hungarian language: FVM rendelet a kistermelői élelmiszer-termelés, -előállítás és -értékesítés feltételeiről). Available online: https://net.jogtar.hu/jogszabaly?docid=a1000052.fvm (accessed on 29 May 2020).

- Government of Canada, Canadian Food Inspection Agency. Local Food Claims Interim Policy. Available online: https://www.inspection.gc.ca/food-label-requirements/labelling/industry/origin-claims-on-food-labels/local-food-claims/eng/1368135927256/1368136146333 (accessed on 22 May 2020).

- Martinez, S.; Hand, M.; Da Pra, M.; Pollack, S.; Ralston, K.; Smith, T.; Vogel, S.; Clarke, S.; Lohr, L.; Low, S.; et al. Local Food Systems: Concepts, Impacts, and Issues; United States Department of Agriculutre (USDA)—Economic Research Service: Washington, DC, USA, 2010; p. 80.

- Malak-Rawlikowska, A.; Majewski, E.; Wąs, A.; Borgen, S.O.; Csillag, P.; Donati, M.; Freeman, R.; Hoàng, V.; Lecoeur, J.-L.; Mancini, M.C.; et al. Measuring the Economic, Environmental, and Social Sustainability of Short Food Supply Chains. Sustainability 2019, 11, 4004. [Google Scholar] [CrossRef] [Green Version]

- Chiffoleau, Y.; Millet-Amrani, S.; Canard, A. From Short Food Supply Chains to Sustainable Agriculture in Urban Food Systems: Food Democracy as a Vector of Transition. Agriculture 2016, 6, 57. [Google Scholar] [CrossRef] [Green Version]

- Marsden, T.; Banks, J.; Bristow, G. Food Supply Chain Approaches: Exploring their Role in Rural Development. Sociol. Rural. 2000, 40, 424–438. [Google Scholar] [CrossRef]

- Coelho, F.C.; Coelho, E.M.; Egerer, M. Local food: Benefits and failings due to modern agriculture. Sci. Agric. 2018, 75, 84–94. [Google Scholar] [CrossRef] [Green Version]

- Deller, S.C.; Lamie, D.; Stickel, M. Local foods systems and community economic development. Community Dev. 2017, 48, 612–638. [Google Scholar] [CrossRef]

- Bowen, S.; Mutersbaugh, T. Local or localized? Exploring the contributions of Franco-Mediterranean agrifood theory to alternative food research. Agric. Hum. Values 2014, 31, 201–213. [Google Scholar] [CrossRef]

- Garnett, T. Food sustainability: Problems, perspectives and solutions. Proc Nutr Soc 2013, 72, 29–39. [Google Scholar] [CrossRef] [Green Version]

- Berti, G. Sustainable Agri-Food Economies: Re-Territorialising Farming Practices, Markets, Supply Chains, and Policies. Agriculture 2020, 10, 64. [Google Scholar] [CrossRef] [Green Version]

- Sonnino, R. The power of place: Embeddedness and local food systems in Italy and the UK. Anthropol. Food 2007. [Google Scholar] [CrossRef]

- Feldmann, C.; Hamm, U. Consumers’ perceptions and preferences for local food: A review. Food Qual. Prefer. 2015, 40, 152–164. [Google Scholar] [CrossRef]

- Blake, M.K.; Mellor, J.; Crane, L. Buying Local Food: Shopping Practices, Place, and Consumption Networks in Defining Food as “Local”. Ann. Assoc. Am. Geogr. 2010, 100, 409–426. [Google Scholar] [CrossRef]

- Alfnes, F.; Sharma, A. Locally produced food in restaurants: Are the customers willing to pay a premium and why? Int. J. Revenue Manag. 2010, 4, 238. [Google Scholar] [CrossRef]

- Martinez, S.W. Policies Supporting Local Food in the United States. Agriculture 2016, 6, 43. [Google Scholar] [CrossRef] [Green Version]

- Popp, J.; Oláh, J.; Kiss, A.; Temesi, Á.; Fogarassy, C.; Lakner, Z. The socio-economic force field of the creation of short food supply chains in Europe. J. Food Nutr. Res. 2019, 58, 31–41. [Google Scholar]

- Kiss, K.; Ruszkai, C.; Takács-György, K. Examination of Short Supply Chains Based on Circular Economy and Sustainability Aspects. Resources 2019, 8, 161. [Google Scholar] [CrossRef] [Green Version]

- Benedek, Z.; Balázs, B. Current status and future prospect of local food production in Hungary: A spatial analysis. Eur. Plan. Stud. 2016, 24, 607–624. [Google Scholar] [CrossRef] [Green Version]

- Mundler, P.; Laughrea, S. The contributions of short food supply chains to territorial development: A study of three Quebec territories. J. Rural Stud. 2016, 45, 218–229. [Google Scholar] [CrossRef]

- Schneider, M.L.; Francis, C.A. Marketing locally produced foods: Consumer and farmer opinions in Washington County, Nebraska. Renew. Agric. Food Syst. 2005, 20, 252–260. [Google Scholar] [CrossRef] [Green Version]

- Low, S.A.; Vogel, S.J. Direct and Intermediated Marketing of Local Foods in the United States; U.S. Department of Agriculture, Economic Research Service: Rochester, NY, USA, 2011; p. 32.

- Aggestam, V.; Fleiß, E.; Posch, A. Scaling-up short food supply chains? A survey study on the drivers behind the intention of food producers. J. Rural Stud. 2017, 51, 64–72. [Google Scholar] [CrossRef]

- European Comission. Statistical Factsheet—Sweden. 2019. Available online: https://ec.europa.eu/info/sites/info/files/food-farming-fisheries/farming/documents/agri-statistical-factsheet-se_en.pdf (accessed on 31 May 2020).

- Benedek, Z.; Fertő, I.; Szente, V. The Multiplier Effects of Food Relocalization: A Systematic Review. Sustainability 2020, 12, 3524. [Google Scholar] [CrossRef]

- Migliore, G.; Schifani, G.; Romeo, P.; Hashem, S.; Cembalo, L. Are Farmers in Alternative Food Networks Social Entrepreneurs? Evidence from a Behavioral Approach. J Agric Env. Ethics 2015, 28, 885–902. [Google Scholar] [CrossRef]

- Dunay, A.; Lehota, J.; Mácsai, É.; Illés, C.B. Short Supply Chain: Goals, Objectives and Attitudes of Producers. Acta Polytech. Hung. 2018, 15, 199–217. [Google Scholar]

- Garner, B. Communicating social support during crises at the farmers’ market: A social exchange approach to understanding customer-farmer communal relationships. Int. J. Consum. Stud. 2017, 41, 422–430. [Google Scholar] [CrossRef]

- Giampietri, E.; Verneau, F.; Del Giudice, T.; Carfora, V.; Finco, A. A Theory of Planned behaviour perspective for investigating the role of trust in consumer purchasing decision related to short food supply chains. Food Qual. Prefer. 2018, 64, 160–166. [Google Scholar] [CrossRef]

- Argent, N. Heading down to the local? Australian rural development and the evolving spatiality of the craft beer sector. J. Rural Stud. 2018, 61, 84–99. [Google Scholar] [CrossRef]

- Blasi, E.; Cicatiello, C.; Pancino, B.; Franco, S. Alternative food chains as a way to embed mountain agriculture in the urban market: The case of Trentino. Agric. Econ. 2015, 3, 3. [Google Scholar] [CrossRef] [Green Version]

- Schupp, J.L. Just where does local food live? Assessing farmers’ markets in the United States. Agric. Hum. Values 2016, 33, 827–841. [Google Scholar] [CrossRef]

- Kiss, K. The satisfaction of producers, selling in various marketplaces-results of a primary survey from Hungary. Ann. Pol. Assoc. Agric. Agribus. Econ. (Ann. PAAAE) 2019, XXI, 183–190. [Google Scholar] [CrossRef]

- Adalja, A.; Hanson, J.; Towe, C.; Tselepidakis, E. An Examination of Consumer Willingness to Pay for Local Products. Agric. Resour. Econ. Rev. 2015, 44, 253–274. [Google Scholar] [CrossRef] [Green Version]

- Rihn, A.L.; Yue, C. Visual Attention’s Influence on Consumers’ Willingness-to-Pay for Processed Food Products. Agribusiness 2016, 32, 314–328. [Google Scholar] [CrossRef]

- Demartini, E.; Gaviglio, A.; Pirani, A. Farmers’ motivation and perceived effects of participating in short food supply chains: Evidence from a North Italian survey. Agric. Econ. (Czech Repub.) 2017, 63, 204–216. [Google Scholar] [CrossRef] [Green Version]

- Berg, N.; Preston, K.L. Willingness to pay for local food?: Consumer preferences and shopping behavior at Otago Farmers Market. Transp. Res. Part A Policy Pract. 2017, 103, 343–361. [Google Scholar] [CrossRef]

- Campbell, J.; DiPietro, R.B.; Remar, D. Local foods in a university setting: Price consciousness, product involvement, price/quality inference and consumer’s willingness-to-pay. Int. J. Hosp. Manag. 2014, 42, 39–49. [Google Scholar] [CrossRef]

- Bakos, I.M. Local food systems supported by communities nationally and internationally. Deturope 2017, 9, 59–79. [Google Scholar]

- Carpio, C.E.; Isengildina-Massa, O. Consumer willingness to pay for locally grown products: The case of South Carolina. Agribusiness 2009, 25, 412–426. [Google Scholar] [CrossRef] [Green Version]

- Hempel, C.; Hamm, U. How important is local food to organic-minded consumers? Appetite 2016, 96, 309–318. [Google Scholar] [CrossRef]

- Brown, C. Consumers’ preferences for locally produced food: A study in southeast Missouri. Am. J. Altern. Agric. 2003, 18, 213–224. [Google Scholar] [CrossRef]

- Betz, M.E.; Farmer, J.R. Farmers’ market governance and its role on consumer motives and outcomes. Local Environ. 2016, 21, 1420–1434. [Google Scholar] [CrossRef]

- Szabó, D. Determining the target groups of Hungarian short food supply chains based on consumer attitude and socio-demographic factors. Stud. Agric. Econ. 2017, 119, 115–122. [Google Scholar] [CrossRef] [Green Version]

- Balázs, B.; Pataki, G.; Lazányi, O. Prospects for the future: Community supported agriculture in Hungary. Futures 2016, 83, 100–111. [Google Scholar] [CrossRef]

- Weatherell, C.; Tregear, A.; Allinson, J. In search of the concerned consumer: UK public perceptions of food, farming and buying local. J. Rural Stud. 2003, 19, 233–244. [Google Scholar] [CrossRef]

- Chambers, S.; Lobb, A.; Butler, L.; Harvey, K.; Bruce Traill, W. Local, national and imported foods: A qualitative study. Appetite 2007, 49, 208–213. [Google Scholar] [CrossRef] [PubMed]

- Kumpulainen, T.; Vainio, A.; Sandell, M.; Hopia, A. The effect of gender, age and product type on the origin induced food product experience among young consumers in Finland. Appetite 2018, 123, 101–107. [Google Scholar] [CrossRef] [PubMed]

- Galt, R.E.; Bradley, K.; Christensen, L.O.; Munden-Dixon, K. The (un)making of “CSA people”: Member retention and the customization paradox in Community Supported Agriculture (CSA) in California. J. Rural Stud. 2019, 65, 172–185. [Google Scholar] [CrossRef] [Green Version]

- Gaviglio, A.; Bertocchi, M.; Marescotti, M.E.; Demartini, E.; Pirani, A. The social pillar of sustainability: A quantitative approach at the farm level. Agric. Food Econ. 2016, 4, 15. [Google Scholar] [CrossRef] [Green Version]

- Grando, S.; Carey, J.M.; Hegger, E.; Jahrl, I.; Ortolani, L. Short Food Supply Chains in Urban Areas: Who Takes the Lead? Evidence from Three Cities across Europe. Urban Agric. Reg. Food Syst. 2017, 2, 1–11. [Google Scholar] [CrossRef] [Green Version]

- Schmidt, J.; Bijmolt, T.H.A. Accurately measuring willingness to pay for consumer goods: A meta-analysis of the hypothetical bias. J. Acad. Mark. Sci. 2020, 48, 499–518. [Google Scholar] [CrossRef] [Green Version]

- Breidert, C.; Hahsler, M.; Reutterer, T. A Review of Methods for Measuring Willingness-to-Pay. Innov. Mark. 2006, 2, 8–32. [Google Scholar]

- Aizuddin, A.N.; Sulong, S.; Aljunid, S.M. Methods and tools for measuring willingness to pay for healthcare: What is suitable for developing countries? BMC Public Health 2014, 14, O20. [Google Scholar] [CrossRef] [Green Version]

- Gracia, A. Consumers’ preferences for a local food product: A real choice experiment. Empir. Econ. 2014, 47, 111–128. [Google Scholar] [CrossRef]

- Onozaka, Y.; Mcfadden, D.T. Does Local Labeling Complement or Compete with Other Sustainable Labels? A Conjoint Analysis of Direct and Joint Values for Fresh Produce Claim. Am. J. Agric. Econ. 2011, 93, 693–706. [Google Scholar] [CrossRef]

- Willis, D.B.; Carpio, C.E.; Boys, K.A. Supporting local food system development through food price premium donations: A policy propsal. J. Agric. Appl. Econ. 2016, 48, 192–217. [Google Scholar] [CrossRef] [Green Version]

- Dogi, I.; Nagy, L.; Csipkés, M.; Balogh, P. Kézműves élelmiszerek vásárlásának fogyasztói magatartásvizsgálata a nők körében (Attitudes of Female Consumers to Purchasing Artisan Foods). Gazdálkodás Sci. J. Agric. Econ. 2014, 58, 1–13. [Google Scholar]

- Eastwood, D.B.; Brooker, J.R.; Orr, R.H. Consumer Preferences for Local Versus Out-Of-State Grown Selected Fresh Produce: The Case of Knoxville, Tennessee. J. Agric. Appl. Econ. 1987, 19, 183–194. [Google Scholar] [CrossRef] [Green Version]

- Cecchini, L.; Torquati, B.; Chiorri, M. Sustainable agri-food products: A review of consumer preference studies through experimental economics. Agric. Econ. 2018, 64, 554–565. [Google Scholar] [CrossRef]

- Lehota, Z.; Lencsés, E. Consumer willingness and price premium characteristics in the Hungarian food supply chain. In Proceedings of the 9th International Conference on Management: “People, Planet and Profit: Sustainable Business and Society, Gödöllő, Hungary, 13–14 June 2019; Dunay, A., Ed.; Szent István University Publishing House: Gödöllő, Hungary, 2019; Volume 2, pp. 199–203. [Google Scholar]

- Correlation Coefficient: Simple Definition, Formula, Easy Calculation Steps. Available online: https://www.statisticshowto.com/probability-and-statistics/correlation-coefficient-formula/ (accessed on 29 May 2020).

- Cramér’s V—Description. Available online: https://www.ibm.com/support/knowledgecenter/SSEP7J_11.1.0/com.ibm.swg.ba.cognos.ug_ca_dshb.doc/cramersv.html (accessed on 6 June 2020).

- Evans, J.R.; Mathur, A. The value of online surveys. Internet Res. 2005, 15, 195–219. [Google Scholar] [CrossRef]

- HCSO Hungarian Central Statistical Office: Interactive Charts and maps-Regional Breakdown: The NUTS Classification. Available online: https://www.ksh.hu/interactive_eumaps_nuts2 (accessed on 29 May 2020).

- European Commisson—Eurostat (Background). Available online: https://ec.europa.eu/eurostat/web/regions/background (accessed on 29 May 2020).

- European Comission—Regional Innovation Monitor Plus North Hungary. Available online: https://ec.europa.eu/growth/tools-databases/regional-innovation-monitor/base-profile/north-hungary-2 (accessed on 29 May 2020).

- United Nations: The Wye Group Handbook. Rural Households’ Livelihood and Well-Being. Statistics on Rural Development and. Agriculture Household Income; United Nations: New York, NY, USA; Genava, Switzerland, 2007; ISBN 978-9-21-116967-6.

- HCSO Hungarian Central Statistical Office: Annual statistical data—Settlements in Hungary. Available online: http://statinfo.ksh.hu/Statinfo/haDetails.jsp?query=kshquery&lang=en (accessed on 29 May 2020).

- HCSO Hungarian Central Statistical Office: TIMEA—Térképes Interaktív Megjelenítő Szolgáltatás (Map Interactive Display Service-Unofficial Translation). Available online: https://map.ksh.hu/timea/?locale=en (accessed on 29 May 2020).

- Kiss, K.; Koncz, G.; Nagy-Demeter, D.; Varró, B.; Németh, M.; Ruszkai, C. Survey of Consumers Responsiveness to Small-Scale Producers Marketing in the Northern Hungary Region. TMP 2019, 15, 25–34. [Google Scholar] [CrossRef]

- Eurostat—Statistics Explained File:Gross Domestic Product (GDP) per Inhabitant, by NUTS 2 Regions, 2016 (Based on Data in Purchasing Power Standards (PPS) in Relation to the EU-28 Average, EU-28 = 100)-RYB18.png—Statistics Explained. Available online: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=File:Gross_domestic_product_(GDP)_per_inhabitant,_by_NUTS_2_regions,_2016_(based_on_data_in_purchasing_power_standards_(PPS)_in_relation_to_the_EU-28_average,_EU-28_%3D_100)-RYB18.png (accessed on 29 May 2020).

| The Base of Comparison * | Willingness to Pay (Average Premium) | Source |

|---|---|---|

| - consumers’ preference for local lamb meats (location of the survey: Spain) | 9%, and 13% depending on the products | [60] |

| - consumers’ “positive preference for locally-grown products in comparison to domestically-grown products” (location of the survey: U.S.) | +9–15% | Onozaka and Mcfadden [61],—cited by Campbell et al. [43] p. 44. |

| - willingness to pay for a locally-grown product compared to non-local agricultural products (location of the survey: South Carolina) | +11% | [62] |

| - preference for handicraft products compared to conventional, non-local foods (location of the survey: Hungary) | 10–25%, for 2/3 part of the responders | [63] |

| - respondents’ willingness to pay for local products compared to products from the other Member States (location of the survey: South Carolina) | 23% and 27% depending on the products | [45] |

| Consumer Characteristics (and Corresponding Response Categories) | Average Monthly Expenditure on Local Producers’ Goods | Significant Relationship * Appendix B | |||||

|---|---|---|---|---|---|---|---|

| 0–16 EUR (n = 346) | 16.01–31 EUR (n = 331) | 31.01—47 EUR (n = 178) | 47.01—63 EUR (n = 97) | 63 EUR < (n = 68) | |||

| Gender ratio | Women | 72.5% | 70.0% | 62.9% | 64.6% | 67.6% | No |

| Men | 27.5% | 30.0% | 37.1% | 35.4% | 32.4% | ||

| Age distribution | under 20 years | 0.6% | 0.9% | 2.8% | 1.0% | 0.0% | Yes; medium/weak relationship |

| 20–35 years | 55.2% | 46.2% | 43.3% | 36.1% | 38.2% | ||

| 36–50 years | 24.0% | 32.9% | 37.6% | 43.3% | 45.6% | ||

| 51–65 years | 14.2% | 16.9% | 12.4% | 19.6% | 14.7% | ||

| above 65 years | 6.1% | 3.0% | 3.9% | 0.0% | 1.5% | ||

| Highest level of education (distribution) | elementary school | 0.3% | 0.9% | 0.6% | 0.0% | 1.5% | Yes; medium/weak relationship |

| skilled worker certificate | 5.2% | 4.5% | 2.2% | 2.1% | 11.9% | ||

| graduation/technical school | 33.8% | 27.3% | 24.7% | 18.6% | 16.4% | ||

| higher vocational training | 18.2% | 13.3% | 15.7% | 19.6% | 22.4% | ||

| college or university degree | 42.5% | 53.9% | 56.7% | 59.8% | 47.8% | ||

| Marital status (distribution) | unmarried | 31.5% | 25.4% | 28.1% | 20.8% | 19.1% | No |

| common law-partner | 24.3% | 22.9% | 24.7% | 20.8% | 23.5% | ||

| married | 35.3% | 43.4% | 38.8% | 52.1% | 48.5% | ||

| divorced | 7.5% | 7.0% | 7.3% | 4.2% | 8.8% | ||

| widow/widower | 1.4% | 1.2% | 1.1% | 2.1% | 0.0% | ||

| Income level (distribution) | significantly below average | 1% | 0% | 1% | 0% | 1% | Yes, medium relationship |

| below average | 12% | 5% | 7% | 8% | 4% | ||

| average | 73% | 77% | 65% | 63% | 66% | ||

| above average | 13% | 17% | 25% | 28% | 21% | ||

| significantly above average | 1% | 1% | 3% | 1% | 7% | ||

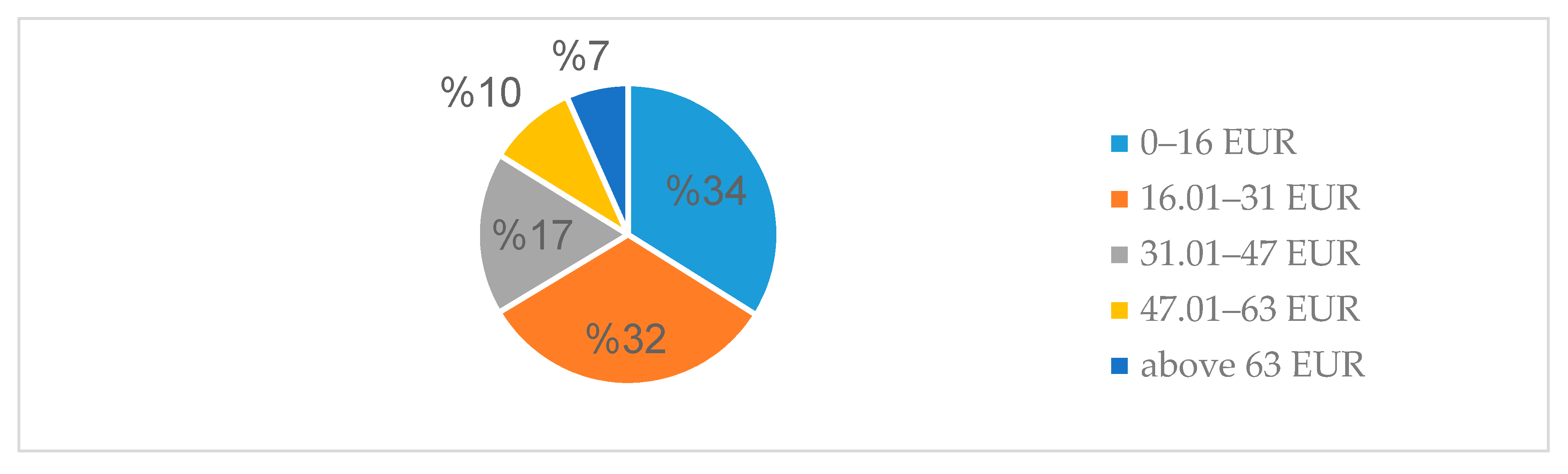

| Willingness to pay (how much premium the responders are willing to pay for local producers’ goods)—averages of answers | +15.7% | +20.7% | +24% | +25.3% | +31.1% | Yes | |

| Place of residence (distribution by settlement size) | small village | 3% | 3% | 3% | 3% | 5% | Yes; medium/weak relationship |

| medium-sized village | 11% | 17% | 14% | 18% | 26% | ||

| large village | 19% | 21% | 19% | 23% | 15% | ||

| village town | 7% | 4% | 5% | 7% | 8% | ||

| small town | 9% | 13% | 14% | 3% | 12% | ||

| small-medium sized town | 16% | 17% | 18% | 13% | 14% | ||

| medium-sized town | 23% | 20% | 22% | 27% | 11% | ||

| large city | 7% | 3% | 4% | 5% | 5% | ||

| metropolis | 5% | 2% | 2% | 1% | 6% | ||

| Determinants of Product Choosing | Consumer Groups on the Basis of Average Monthly Expenditure on Local Producers’ Goods | ||||

|---|---|---|---|---|---|

| 0–16 EUR (n = 336) | 16.01–31 EUR (n = 318) | 31.01–47 EUR (n = 173) | 47.01–63 EUR (n = 95) | 63 EUR< (n = 66) | |

| (Averages of Responses on a Five-Rank Likert-Scale) | |||||

| - price | 4.18 | 3.96 | 3.91 | 3.87 | 3.58 |

| - brand, manufacturer (generally) | 3.41 | 3.54 | 3.53 | 3.74 | 3.74 |

| - Hungarian (domestic) origin | 3.38 | 3.84 | 3.94 | 4.06 | 4.15 |

| - actual (price) discounts | 3.99 | 3.82 | 3.74 | 3.71 | 3.52 |

| - quality | 4.44 | 4.63 | 4.69 | 4.73 | 4.79 |

| - need for organic products | 2.50 | 3.03 | 3.06 | 3.27 | 3.48 |

| - uniqueness | 2.76 | 3.13 | 3.20 | 3.42 | 3.32 |

| - advertisements | 1.90 | 1.99 | 1.88 | 1.97 | 1.74 |

| - personal relationship, emotional attachment | 2.94 | 3.07 | 3.35 | 3.39 | 3.20 |

| - environmental awareness | 3.40 | 3.77 | 3.98 | 3.94 | 3.95 |

| - family traditions | 2.96 | 3.23 | 3.54 | 3.39 | 3.50 |

| Sales Channels | Average Ratings |

|---|---|

| - supermarkets and discount stores | 3.67 |

| - (conventional) marketplaces | 3.17 |

| - hypermarkets | 2.98 |

| - own growing or production | 2.90 |

| - convenience stores, small shops | 2.88 |

| - producers’ markets (marketplaces) | 2.85 |

| - specialized grocery stores (e.g., bakeries) | 2.63 |

| - online shopping | 2.28 |

| - fairs, festivals | 2.13 |

| - purchasing at the producers’ place or home delivery by producers | 2.12 |

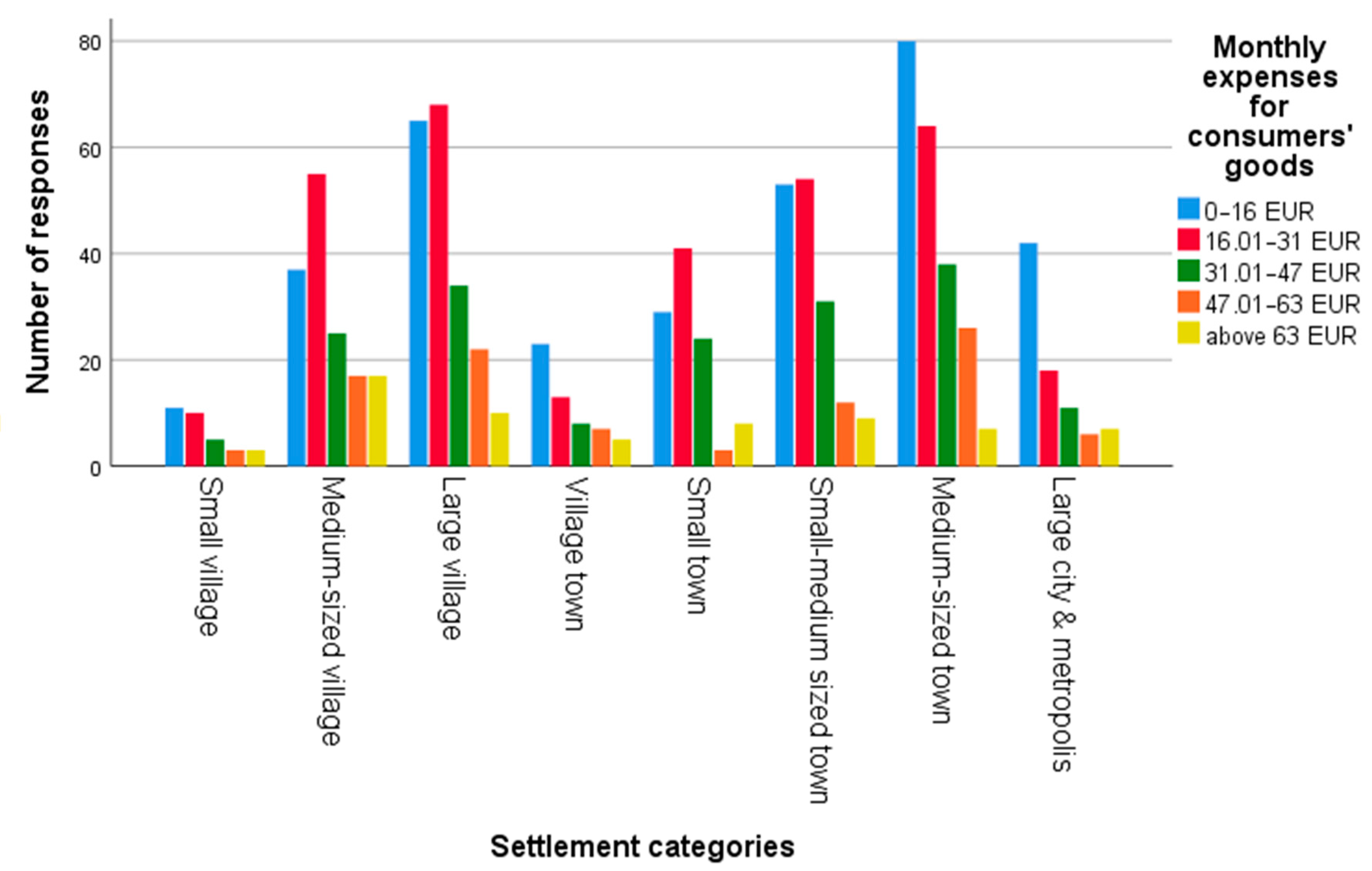

| Settlement Categories | Population Number of the Settlement Category (People) | Number of Respondents (n = 1001) * | Monthly Expenditure on Local Products (Averages of Answer-Categories)* (n = 1001) ** | Responders’ willingness to Pay—Average Theoretical Price Premium for Local Goods (%) (n = 959) ** |

|---|---|---|---|---|

| - small village | 100–499 | 32 | 2.28 | 21.12% |

| - medium-sized village | 500–1999 | 151 | 2.48 | 21.49% |

| - large village | 2000–4999 | 199 | 2.22 | 23.46% |

| - village town | 5000–9999 | 56 | 2.25 | 17.95% |

| - small town | 10,000–19,999 | 105 | 2.24 | 20.56% |

| - small-medium sized town | 20,000–49,999 | 159 | 2.18 | 18.78% |

| - medium-sized town | 50,000–99,999 | 215 | 2.15 | 18.08% |

| - large city | 100,000–999,999 | 50 | 2.02 | 25.64% |

| - metropolis | 1,000,000- | 34 | 2.22 | 19.12% |

| Sales Channels | Small Village | Medium-Sized Village | Large Village | Village Town | Small Town | Small-Medium Sized Town | Medium-Sized Town | Large City | Metropolis | Presence and Strength of Statistically Significant Relationship (Appendix D) |

|---|---|---|---|---|---|---|---|---|---|---|

| - hypermarkets | 2.91 | 3.11 | 2.93 | 3.00 | 2.68 | 2.84 | 3.02 | 3.58 | 3.15 | Yes, moderate/weak |

| - supermarkets | 3.45 | 3.50 | 3.44 | 3.61 | 3.82 | 3.81 | 3.81 | 3.58 | 3.15 | Yes, moderate |

| - convenience stores, small shops | 3.09 | 3.19 | 3.11 | 2.76 | 2.86 | 2.54 | 2.79 | 2.55 | 2.94 | Yes, moderate |

| - (conventional) marketplaces | 3.21 | 3.20 | 3.24 | 3.18 | 3.15 | 3.15 | 3.14 | 2.86 | 3.36 | No |

| - producers’ markets (marketplaces) | 3.15 | 2.98 | 2.99 | 2.84 | 2.85 | 2.67 | 2.84 | 2.37 | 2.85 | No |

| - specialized grocery stores (e.g., bakeries) | 2.61 | 2.66 | 2.80 | 2.56 | 2.80 | 2.53 | 2.63 | 2.28 | 2.18 | Yes, moderate/weak |

| - purchasing at the producers’ place or home delivery by producers | 2.27 | 2.29 | 2.35 | 2.38 | 2.16 | 1.9 | 2.00 | 1.76 | 1.61 | Yes, moderate/weak |

| - fairs, festivals | 2.48 | 2.11 | 2.20 | 2.16 | 2.06 | 2.05 | 2.20 | 2.02 | 1.91 | No |

| - online shopping | 2.18 | 2.97 | 2.52 | 2.49 | 2.08 | 2.13 | 2.16 | 2.16 | 2.24 | No |

| - own growing or production | 3.97 | 3.32 | 3.26 | 3.00 | 2.93 | 2.46 | 2.57 | 2.49 | 2.39 | Yes, strong |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kiss, K.; Ruszkai, C.; Szűcs, A.; Koncz, G. Examining the Role of Local Products in Rural Development in the Light of Consumer Preferences—Results of a Consumer Survey from Hungary. Sustainability 2020, 12, 5473. https://doi.org/10.3390/su12135473

Kiss K, Ruszkai C, Szűcs A, Koncz G. Examining the Role of Local Products in Rural Development in the Light of Consumer Preferences—Results of a Consumer Survey from Hungary. Sustainability. 2020; 12(13):5473. https://doi.org/10.3390/su12135473

Chicago/Turabian StyleKiss, Konrád, Csaba Ruszkai, Antónia Szűcs, and Gábor Koncz. 2020. "Examining the Role of Local Products in Rural Development in the Light of Consumer Preferences—Results of a Consumer Survey from Hungary" Sustainability 12, no. 13: 5473. https://doi.org/10.3390/su12135473

APA StyleKiss, K., Ruszkai, C., Szűcs, A., & Koncz, G. (2020). Examining the Role of Local Products in Rural Development in the Light of Consumer Preferences—Results of a Consumer Survey from Hungary. Sustainability, 12(13), 5473. https://doi.org/10.3390/su12135473