Plant-Based Sustainable Development—The Expansion and Anatomy of the Medicinal Plant Secondary Processing Sector in Nepal

,

,  , and

, and

Abstract

:1. Introduction

2. Materials and Methods

2.1. Terminology and Definitions

2.2. Study Area

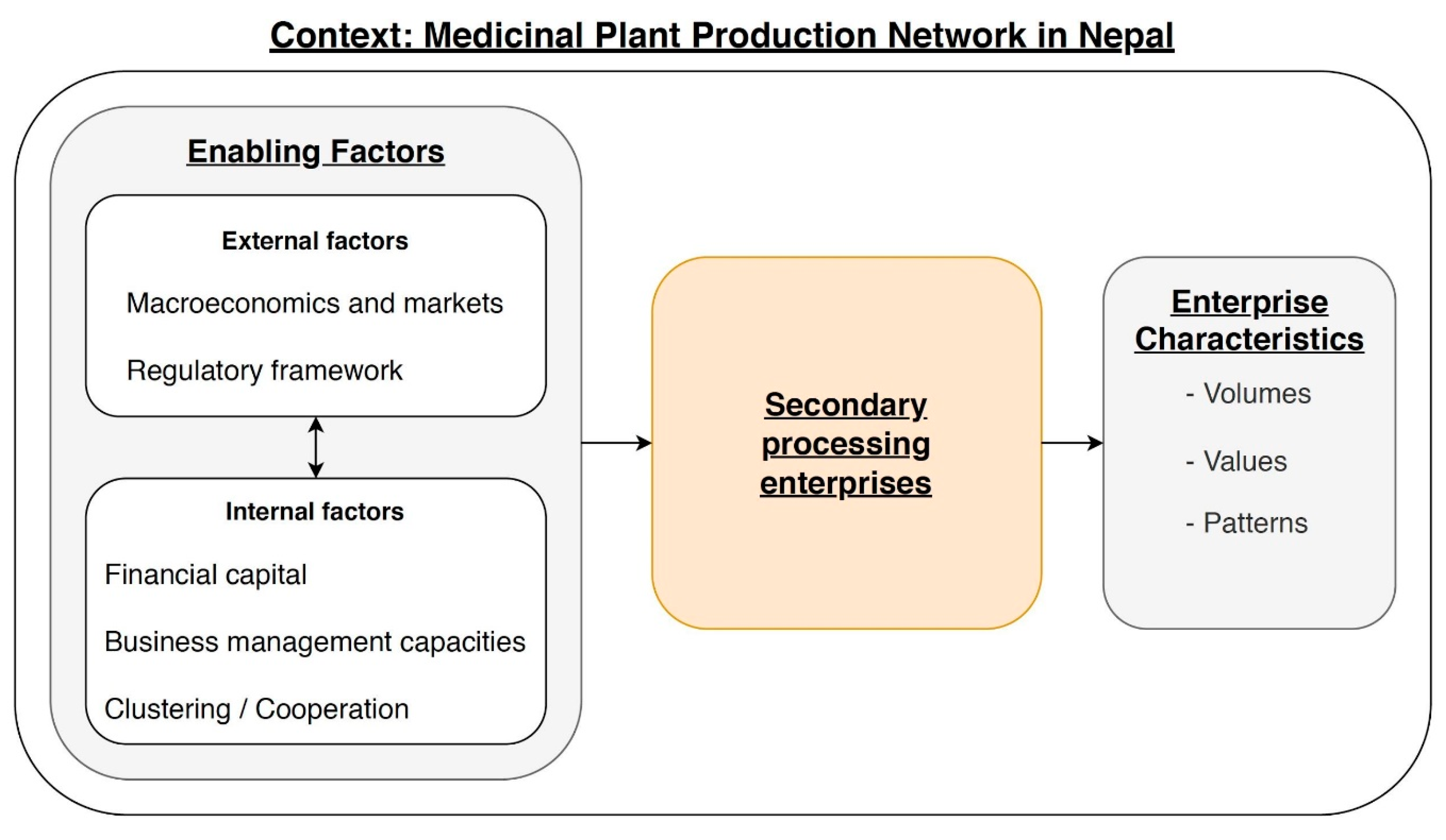

2.3. Analytical Framework

2.4. Data Collection and Analysis

3. Results

3.1. Factors Promoting and Hindering the Establishing and Operation of the Medicinal Plant Secondary Processing Sector

3.2. Basic Characteristics of Medicinal Plant Secondary Processing Enterprises

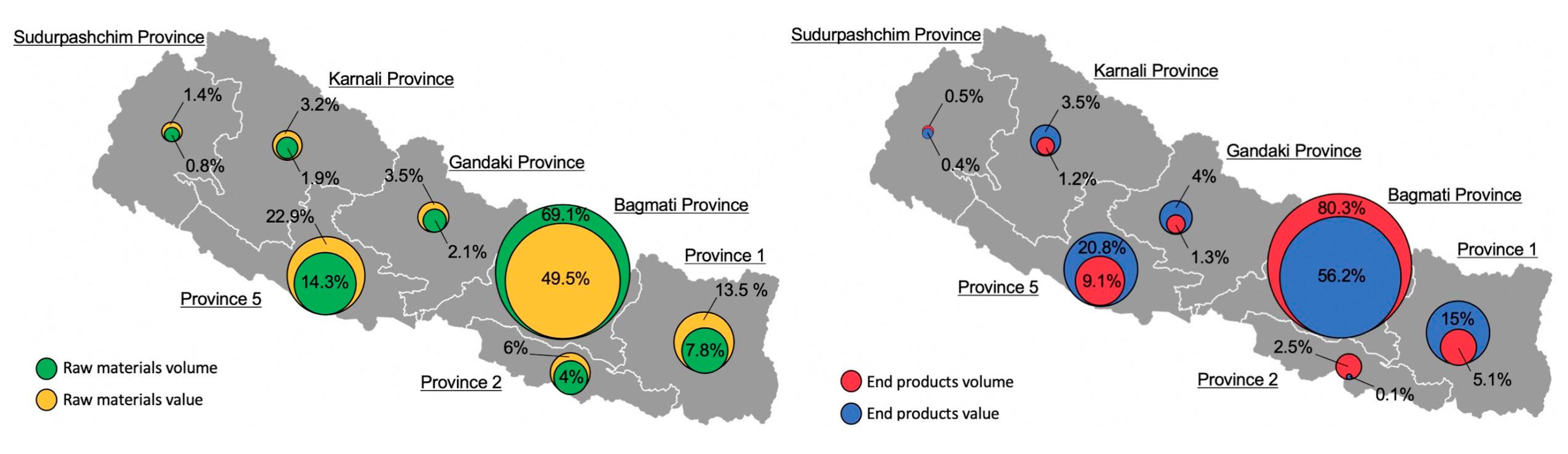

3.3. Quantifying the Volume and Value of the Annual Demand for Raw Materials

3.4. Quantifying the Volume and Value of the Annual Production of End Products

4. Discussion

4.1. The Emergence of the Nepalese Medicinal Plant Secondary Processing Sector

- Traditional medicine systems are increasingly commercialised, including mass production and marketing, and hence more widely available to consumers. While the change in Tibet took its point of departure from legislative requirements [20], the change in Nepal is purely demand-driven, indicating several pathways towards industrialisation and growth in traditional medicine systems.

4.2. The Economic Importance of the Nepalese Medicinal Plant Secondary Processing Sector

4.3. The Potential of the Nepalese Medicinal Plant Secondary Processing Sector to Contribute to the Bioeconomy

- How can Nepal transform from being a supplier of raw materials and producer of lower-value domestic consumer products to integrating into the global economy as an exporter of higher-value products? This transformation requires solutions to the obstacles identified above: export barriers, technology and service barriers, labour challenges, socio-economic and political instability, and the cumbersome and inefficient bureaucracy. Many of these obstacles are also faced by other natural product processing enterprises elsewhere, e.g., non-timber forest product-processing small enterprises in Africa struggle with developing upgrading and becoming part of traceability schemes [18]. While instability is a generic issue cutting across all sectors, as is the general difficulty of doing business (e.g., Nepal ranks as 135 out of 190 countries in terms of the ease of starting a business, [69]), the other challenges can, at least in theory, be addressed through initiatives aimed at the medicinal plant production network. Rather than trying to outguess the markets, the emphasis should be on establishing generic support functions and interventions that can then be accessed by a variety of enterprises. Paramount to accessing export markets is meeting established standards, such as international standards for phytosanitary measures and compliance with WHO-GMP standards in the case of traditional medicine products. This could be supported through funding to establish accredited laboratories and support for achieving certifications. This could have positive knock-on effects, e.g., such infrastructure could induce enterprise investment in improved technology that would increase competitiveness, and storage facilities that would allow more efficient trade throughout the year [18,19]. Labour shortage is common throughout Nepal, e.g., almost half of all households have at least one family member working abroad or a returnee [56] and important high-altitude medicinal plant production areas are being depopulated [70]. Attracting labour into medicinal plant secondary processing enterprises seems presently to be a matter of salaries; more competitive export-oriented enterprises would be better positioned to attract both skilled and unskilled labour. Cooperation between processing enterprises through associations and cooperatives could improve the sharing of skills and knowledge and increase bargaining power, e.g., with traders and the government [19,71]. The inefficient bureaucracy is not an issue that is easily addressed; recommendations to deal with the associated challenges have been made in a number of policies (that can be read as a long string of well-intentioned interventions), including the Herbs and Non-Timber Forest Product Development Policy from 2004. Rather than repeat past ineffective recommendations, there is a need to understand the political ecology of the medicinal plant production network in Nepal, to arrive at feasible solutions (at both national and provincial levels). Work has progressed on this in the wider forest sector [72,73] and forms a solid starting point for medicinal plant related progress. The importance of a supportive institutional framework is general to the development of competitive natural product enterprises regardless of location [16,19]. This would also serve to prevent repeats of the 2018 jatamansi trade ban and to increase the competitiveness of the sector, e.g., through less rent-seeking and clearer legislation on who can tax medicinal plant trade and processing. To provide a common agreement on goals and a consolidated effort to implement interventions, a theory of change should be developed.

- How can supplies be sustained in the face of increasing demands (whether to support ongoing raw material export or the development of the domestic industry)? Maintaining or developing an abundant resource base is essential for natural product processing industries [16,18]. Even if there is a lack of studies documenting unsustainable harvests [12]—such studies are resource consuming—there is widespread concern that a number of species may currently be overharvested (e.g., Paris polyphylla Sm., Nardostachys jatamansi (D. Don) DC., Neopicrorhiza scrophulariiflora (Pennell) D. Y. Hong, and Zanthoxylum armatum DC.) [4,44,58,74,75]. Given the currently available funding for medicinal plant-related research, there is no way to establish species-level sustainable harvest estimates for the 300 species in trade [26]. However, combining existing information on trade and vulnerability will allow the short-listing of species to focus on, e.g., in [27] it was shown that the medicinal plant trade focuses on few species, in both volume and value terms, while in [26] there is a recent conservation assessment. In addition to estimating species-level sustainable harvest estimates for highly traded and vulnerable species, it is important to improve our understanding of the political ecology of the bioeconomy of which the medicinal plant sector is a part. Studies from community forestry indicate that existing official harvest quotas, including those for medicinal plants from district level five-year plans, should be treated with scepticism [72,73] as they serve to satisfy bureaucracy rather than ensure sustainable harvests. Further understanding of the political ecology would reinforce sector understanding and thus underpin the formulation of feasible public policy interventions to address the identified obstacles to developing sustainable secondary medicinal plant processing in Nepal.

- Can commercial medicinal plants support a transition to the bioeconomy? Greenhouse gasses affect the earth’s climate [76] and actions are required to develop affordable and efficient transition pathways to low-carbon economies [65]. Ways to decarbonise include reducing the amount of CO2 returned to the atmosphere through the enhanced use of wood and other plant products in materials. This has led to a biotechnological dominance in the young research field of bioeconomy, with most published studies focused on the EU [45,77]. This dominant biotechnological approach is decoupled from sustainability concerns [45] and its emphasis on natural science, biotechnology, and patents makes it less relevant to low-income countries. There is a need to develop a bioeconomy of renewable resources in low-income countries. While this is beyond the scope of this paper, the presented case provides a rich starting point for providing input to such a school of thought—there is a huge and growing trade, ample opportunities for expanding processing (and reducing the export of raw materials), and a specific list of obstacles to be addressed from a bioeconomic starting point.

5. Conclusions

Supplementary Materials

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Stratum/Employees | Permanent Employees (no.) | Temporary Employees (no.) |

|---|---|---|

| Large enterprises | ||

| average ± SD | 24.9 ± 16.8 | 6.1 ± 7.7 |

| generalisation | 248.8 | 61.3 |

| Small enterprises—Kathmandu Valley | ||

| average ± SD | 5.1 ± 4.2 | 9.3 ± 10.1 |

| generalisation | 468.3 | 845.6 |

| Small enterprises—other districts | ||

| average ± SD | 3.1 ± 7.5 | 3.0 ± 7.0 |

| generalisation | 413.6 | 400.4 |

| Totals | 1130.7 | 1307.3 |

Appendix B

| Raw Materials Purchased from1 (%) | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Common Trade Name 2 | Species Scientific Name | Volume Purchased (kg) | Estimated Purchased Volume at National Level (kg) | % Purchased in Nepal | Average Price/kg (NPR) | Average Price Standard Deviation | Estimated Accumulated Value at National Level (USD) | Collec- Tors | Domesti-cators | Local Traders | Sub-local Permanent Traders | Local Specialist Traders | Local Generalist Traders | Central Whole-salers | Regional Whole- salers | Own Produc- tion |

| Jatamansi | Nardostachys jatamansi | 168,318 | 353,803 | 100.0 | 3844.0 | 11,403.3 | 2,151,574 | 21.2 | 0.0 | 0.0 | 0.0 | 5.8 | 6.2 | 66.9 | 0.0 | 0.0 |

| Timur | Zanthoxylum armatum | 143,297 | 301,209 | 100.0 | 220.7 | 82.7 | 267,544 | 6.0 | 13.1 | 0.0 | 0.0 | 0.0 | 9.5 | 61.9 | 0.0 | 9.5 |

| Sugandhawal (samayo) | Valeriana jatamansi | 64,478 | 135,532 | 100.0 | 220.9 | 87.9 | 240,933 | 23.5 | 0.0 | 0.0 | 0.0 | 5.9 | 15.3 | 55.3 | 0.0 | 0.0 |

| Silajeet | A rock exudate | 6797 | 14,287 | 100.0 | 1423.1 | 1508.8 | 194,941 | 0.0 | 0.0 | 12.5 | 0.0 | 0.0 | 0.0 | 87.5 | 0.0 | 0.0 |

| Sunpati | Rhododendron anthopogon | 161,410 | 339,282 | 100.0 | 32.5 | 40.3 | 120,775 | 58.3 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 41.7 | 0.0 | 0.0 |

| Sugandhakokila (sugandhkokila) | Cinnamomum glaucescens | 48,000 | 100,896 | 100.0 | 93.3 | 5.8 | 96,528 | 16.7 | 16.7 | 0.0 | 0.0 | 0.0 | 33.3 | 33.3 | 0.0 | 0.0 |

| Kutki (katuki) | Neopicrorhiza scrophulariiflora | 2613 | 5493 | 100.0 | 1389.1 | 227.8 | 80,370 | 7.7 | 0.0 | 0.0 | 0.0 | 0.0 | 7.7 | 84.6 | 0.0 | 0.0 |

| Amala | Phyllanthus emblica | 56,185 | 118,100 | 98.4 | 68.1 | 27.1 | 78,270 | 13.0 | 4.2 | 0.0 | 1.9 | 1.6 | 4.1 | 62.7 | 0.6 | 11.8 |

| Kurilo (satawari) | Asparagus spp. | 9957 | 20,930 | 100.0 | 254.3 | 65.9 | 58,587 | 8.2 | 0.9 | 0.0 | 4.5 | 0.0 | 0.0 | 72.7 | 0.0 | 13.6 |

| Dhupi (kalo) | Juniperus indica | 311,267 | 654,280 | 100.0 | 251.9 | 866.5 | 54,122 | 43.8 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 56.3 | 0.0 | 0.0 |

| Bojho (bhojo) | Acorus calamus | 47,420 | 99,676 | 100.0 | 84.0 | 30.8 | 52,485 | 10.0 | 10.0 | 0.0 | 0.0 | 5.0 | 0.0 | 65.0 | 0.0 | 10.0 |

| Pipla | Piper longum | 6044 | 12,704 | 100.0 | 520.8 | 427.0 | 50,227 | 5.0 | 0.0 | 0.0 | 5.0 | 0.0 | 15.0 | 75.0 | 0.0 | 0.0 |

| Other | - | 11,395 | 23,952 | 100.0 | 328.3 | 575.5 | 50,080 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 16.7 | 83.3 | 0.0 | 0.0 |

| Harro | Terminalia chebula | 36,409 | 76,531 | 94.8 | 58.8 | 21.2 | 49,164 | 19.9 | 2.7 | 0.0 | 0.0 | 2.3 | 7.4 | 57.8 | 0.6 | 9.3 |

| Dhasingre (machhino) | Gaultheria fragrantissima | 472,606 | 993,414 | 100.0 | 403.8 | 1198.6 | 48,340 | 72.7 | 0.0 | 9.1 | 0.0 | 0.0 | 0.0 | 18.2 | 0.0 | 0.0 |

| Chiraito (tite) | Swertia chirayita | 3456 | 7264 | 100.0 | 492.1 | 95.7 | 38,328 | 5.6 | 0.0 | 0.0 | 0.0 | 0.0 | 5.6 | 88.9 | 0.0 | 0.0 |

| Barro | Terminalia bellirica | 32,443 | 68,195 | 95.2 | 50.2 | 18.1 | 37,506 | 11.9 | 5.0 | 0.0 | 0.0 | 2.2 | 7.1 | 57.5 | 0.9 | 15.5 |

| Chiuri | Diploknema butyracea | 5670 | 11,918 | 100.0 | 281.5 | 50.1 | 34,901 | 0.0 | 7.7 | 7.7 | 0.0 | 0.0 | 0.0 | 84.6 | 0.0 | 0.0 |

| Satuwa (seto) | Paris polyphylla | 200 | 420 | 100.0 | 5900.0 | 1140.2 | 24,346 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 |

| Titepati | Artemisa spp. | 80,100 | 168,369 | 100.0 | 16.4 | 24.4 | 21,464 | 70.0 | 10.0 | 0.0 | 0.0 | 0.0 | 0.0 | 20.0 | 0.0 | 0.0 |

| Nirmasi (nirmansi) | Delphinium denudatum | 121 | 254 | 100.0 | 5675.0 | 236.3 | 14,386 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 |

| Dalchini | Cinnamomum tamala | 6395 | 13,442 | 100.0 | 100.0 | 38.6 | 13,237 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 8.3 | 87.5 | 0.0 | 4.2 |

| Tejpat | Cinnamomum tamala | 15,131 | 31,805 | 100.0 | 60.2 | 16.4 | 12,264 | 8.2 | 5.5 | 0.0 | 0.0 | 0.0 | 4.5 | 77.3 | 0.0 | 4.5 |

| Majitho | Rubia manjith | 3502 | 7361 | 100.0 | 121.0 | 52.6 | 10,450 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 |

| Kaulo | Machilus spp. | 5600 | 11,771 | 100.0 | 77.0 | 21.7 | 8387 | 5.0 | 5.0 | 0.0 | 0.0 | 0.0 | 10.0 | 80.0 | 0.0 | 0.0 |

| Rittha | Sapindus mukorossi | 14,339 | 30,140 | 100.0 | 28.3 | 7.5 | 7862 | 8.3 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 91.7 | 0.0 | 0.0 |

| Gurjo (guduchi) | Tinospora spp. | 8396 | 17,648 | 100.0 | 31.7 | 18.5 | 5760 | 16.7 | 0.0 | 0.0 | 0.0 | 8.3 | 0.0 | 33.3 | 0.0 | 41.7 |

| Kauso | Mucuna pruriens | 650 | 1366 | 33.0 | 400.0 | - | 5577 | 25.0 | 25.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 50.0 | 0.0 |

| Rudraksha (rudrakshya) | Elaeocarpus angustifolius | 141 | 296 | 100.0 | 1500.0 | - | 4536 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Sarpagandha | Rauvolfia serpentina | 965 | 2028 | 100.0 | 766.7 | 1068.1 | 3699 | 33.3 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 33.3 | 0.0 | 33.3 |

| Seto musli | Chlorophytum spp. | 75 | 158 | 100.0 | 1500.0 | - | 2414 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 |

| Sikakai | Senegalia rugata | 1170 | 2459 | 100.0 | 80.0 | 75.1 | 1790 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 |

| Chabo | Piper chaba | 284 | 597 | 100.0 | 246.7 | 219.4 | 1546 | 33.3 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 66.7 | 0.0 | 0.0 |

| Pakhanved | Bergenia spp. | 840 | 1766 | 92.0 | 58.5 | 23.3 | 1322 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 70.0 | 0.0 | 30.0 |

| Chutro | Berberis spp. | 1351 | 2840 | 100.0 | 32.0 | 13.6 | 1186 | 14.3 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 85.7 | 0.0 | 0.0 |

| Jiwanti | Dendrobium spp. | 35 | 74 | 100.0 | 1400.0 | - | 1050 | 100.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Bel | Aegle marmelos | 250 | 525 | 100.0 | 120.0 | - | 644 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 |

| Guchi chyau | Morchella spp. | 2 | 4 | 100.0 | 12,000.0 | - | 514 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 |

| Rato chyau | Laetiporus sulphureus | 20,000 | 42,040 | 100.0 | 1.0 | - | 428 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 |

| Nisodh | Operculina turpethum | 40 | 84 | 100.0 | 480.0 | - | 411 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 | 0.0 |

| Ghodtapre (brahmi) | Centella asiatica | 100 | 210 | 100.0 | 150.0 | - | 321 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 |

| Padamchal roots | Rheum spp. | 110 | 231 | 100.0 | 117.0 | 46.6 | 283 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 |

| Attis | Delphinium himalayae | 100 | 210 | 100.0 | 1200.0 | - | 257 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 |

| Arjun | Terminalia arjuna | 40 | 84 | 100.0 | 260.0 | - | 224 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 | 0.0 |

| Kukurdyane | Smilax spp. | 15 | 32 | 100.0 | 550.0 | - | 178 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 | 0.0 |

| Tulsi | Ocimum tenuiflorum | 150 | 315 | 100.0 | 40.5 | - | 174 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 50.0 | 0.0 | 50.0 |

| Aloe vera | Aloe vera | 700 | 1471 | 100.0 | 10.0 | - | 149 | 95.0 | 5.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Jamuno (jamun beej) | Syzygium cumini | 100 | 210 | 100.0 | 35.0 | - | 75 | 100.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Bhringiraj (bhringaraj) | Eclipta prostrata | 100 | 210 | 100.0 | 25.0 | - | 53 | 100.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Panchaaule | Dactylorhiza hatagirea | 33 | 69 | 36.0 | 36.0 | - | 26 | 100.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Vyakur | Dioscorea deltoidea | 25 | 53 | 100.0 | 35.0 | - | 18 | 100.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Asuro (ashuro) | Justicia adhatoda | 63 | 132 | 100.0 | 1.0 | - | 2 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Yarsagumba (yartsagunbu) | Ophiocordyceps sinensis | 8 | 17 | 100.0 | 5.7 | 8.1 | 0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 |

| Tope jhar | 3 | 6 | 100.0 | 0.0 | - | 0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | |

| Thulo begar | Astilbe rivularis | 20 | 42 | 100.0 | 0.0 | - | 0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 |

| Sikari lahara | Periploca calophylla | 20 | 42 | 100.0 | 0.0 | - | 0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 |

| Kukhurekath | 15 | 32 | 100.0 | 0.0 | - | 0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | |

| Chini lahara (chini jhar) | Scoparia dulcis | 3 | 6 | 100.0 | 0.0 | - | 0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 |

| Raw materials’ subtotals: | 1,748,957 | 3,676,292 | 3,849,707 | |||||||||||||

| Timur oil | Zanthoxylum armatum | 146 | 307 | 100.0 | 29,000.0 | - | 90,824 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Jatamansi oil | Nardostachys jatamansi | 30 | 63 | 100.0 | 46,500.0 | - | 30,246 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 |

| Dhasingre oil | Gaultheria fragrantissima | 400 | 841 | 100.0 | 2000.0 | - | 17,160 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Tejpat oil | Cinnamomum tamala | 90 | 189 | 100.0 | 5720.0 | - | 11,043 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Juniper oil | Juniperus indica | 70 | 147 | 100.0 | 4500.0 | - | 6757 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 |

| Sugandahkokila oil | Cinnamomum glaucescens | 100 | 210 | 100.0 | 3000.0 | - | 6434 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 |

| Sunpati oil | Rhododendron anthopogon | 100 | 210 | 100.0 | 2200.0 | - | 4718 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 |

| Dhupi oil | Juniperus spp. | 33 | 69 | 100.0 | 6500.0 | - | 4602 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| Jatamansi marc | Nardostachys jatamansi | 250 | 525 | 100.0 | 275.0 | - | 1395 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 100.0 | 0.0 | 0.0 |

| Intermediate products’ subtotals: | 1219 | 2562 | 173,179 | |||||||||||||

| Total volume purchased (kg) | Total estimated purchased volume at national level (kg) | Average % purchased in Nepal | Total estimated accumulated value at national level (USD) | Collec-tors | Domesti-cators | Local traders | Sub-local permanent traders | Local specialist traders | Local generalist traders | Central whole-salers | Regional whole-salers | Own produc-tion | ||||

| 1,750,176 | 3,678,854 | 97.8 | 4,022,886 | 16.9 | 1.7 | 0.4 | 0.2 | 9.4 | 6.7 | 50.0 | 0.8 | 13.9 | ||||

References

- World Bank. Strategic Segmentation Analysis: Nepal. Medicinal and Aromatic Plants; World Bank Group: Washington, DC, USA, 2018; Available online: http://documents.worldbank.org/curated/en/496421556737648658/Medicinal-and-Aromatic-Plants (accessed on 1 June 2020).

- Vasisht, K.; Sharma, N.; Maninder, K. Current perspective in the international trade of medicinal plants material: An update. Curr. Pharm. Des. 2016, 22, 4288–4366. [Google Scholar] [CrossRef] [PubMed]

- Smith-Hall, C.; Larsen, H.O.; Pouliot, M. People, plants and health: A conceptual framework for assessing changes in medicinal plant consumption. J. Ethnobiol. Ethnomed. 2012, 8, 43. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Cunningham, A.B.; Brinckmann, J.; Pei, S.-J.; Luo, P.; Schippmann, U. Paris in the spring: A review of trade, conservation and opportunities in the shift from wild harvest to cultivation of Paris polyphylla (Trilliaceae). J. Ethnopharmacol. 2018, 222, 208–216. [Google Scholar] [CrossRef] [PubMed]

- Homma, A.K.O. Modernisation and technological dualism in the extractive economy in Amazonia. In Current Issues in Non-Timber Forest Products Research; Ruiz Pérez, M., Arnold, J.E.M., Eds.; CIFOR: Bogor, Indonesia, 1996; pp. 59–81. Available online: http://www.cifor.org/ntfpcd/pdf/ntfp-current.pdf (accessed on 1 June 2020).

- Noorhosseini, S.A.; Fallahi, E.; Damalas, C.A. Promoting cultivation of medicinal and aromatic plants for natural resource management and livelihood enhancement in Iran. Environ. Dev. Sustain. 2019, 22, 4007–4024. [Google Scholar] [CrossRef]

- Pordié, L.; Hardon, A. Drugs’ stories and itineraries: On the making of Asian industrial medicines. Med. Anthropol. 2015, 22, 1–6. [Google Scholar] [CrossRef] [PubMed]

- Kessler, R.C.; Davis, R.B.; Foster, D.F.; Rompay, M.I.V.; Walters, E.E.; Wilkey, S.A.; Kaptchuk, T.J.; Eisenberg, D.M. Long-term trends in the use of complementary and alternative medical therapies in the United States. Ann. Intern. Med. 2001, 135, 262–268. [Google Scholar] [CrossRef] [PubMed]

- Ernst, E.; Fugh-Berman, A. Complementary and alternative medicine: What is it all about? Occup. Environ. Med. 2002, 59, 140–144. [Google Scholar] [CrossRef]

- Scheinman, D. Traditional Medicine in Tanga Today: The Ancient and Modern Worlds Meet, Indigenous Knowledge (IK); Notes No. 51; World Bank: Washington, DC, USA, 2002; Available online: http://documents.worldbank.org/curated/en/125771468760788645/Traditional-medicine-in-Tanga-today-the-ancient-and-modern-worlds-meet (accessed on 1 June 2020).

- Pauls, T.; Franz, M. Trading in the dark—The medicinal plants production network in Uttrakhand. Singap. J. Trop. Geogr. 2013, 34, 229–243. [Google Scholar] [CrossRef]

- Smith-Hall, C.; Chapagain, A.; Das, A.K.; Ghimire, S.K.; Pyakurel, D.; Treue, T.; Pouliot, M. Trade and Conservation of Medicinal and Aromatic Plants—An Annotated Bibliography for Nepal; Central Department of Botany, Tribhuvan University, Sopan Press: Kathmandu, Nepal, 2020. [Google Scholar]

- Kala, C.P. Medicinal and aromatic plants: Boon for enterprise development. J. Appl. Res. Med. Aromat. Plants 2015, 2, 134–139. [Google Scholar] [CrossRef]

- Chandra, P.; Sharma, V. Strategic marketing prospects for developing sustainable medicinal and aromatic plants businesses in the Indian Himalayan Region. Small-Scale For. 2018, 17, 423–441. [Google Scholar] [CrossRef]

- Kuniyal, C.P.; Bisht, V.K.; Negi, J.S.; Bhatt, V.P.; Bisht, D.S.; Butola, J.S.; Sundriyal, R.C.; Singh, S.K. Progress and prospect in the integrated development of medicinal and aromatic plants (MAPs) sector in Uttarakhand, Western Himalaya. Environ. Dev. Sustain. 2015, 17, 1141–1162. [Google Scholar] [CrossRef]

- Astutik, S.; Pretzsch, J.; Kimengsi, J.N. Asian medicinal plants’ production and utilization potentials: A review. Sustainability 2019, 11, 5483. [Google Scholar] [CrossRef] [Green Version]

- Badini, O.S.; Hajjar, R.; Kozak, R. Critical success factors for small and medium forest enterprises: A review. For. Policy Econ. 2018, 94, 35–45. [Google Scholar] [CrossRef]

- Cunningham, A.B. Non-timber products and markets: Lessons for export-oriented enterprise development from Africa. In Non-Timber Forest Products in the Global Context; Shackleton, S., Shackleton, C., Shanley, P., Eds.; Springer: Berlin, Germany, 2011; pp. 83–106. [Google Scholar] [CrossRef]

- Meinhold, K.; Darr, D. The processing of non-timber forest products through small and medium enterprises—A review of enabling and constraining factors. Forests 2019, 10, 1026. [Google Scholar] [CrossRef] [Green Version]

- Saxer, M. Herbs and traders in transit: Border regimes and the contemporary trans-Himalayan trade in Tibetan medicinal plants. Asian Med. 2009, 5, 317–339. [Google Scholar] [CrossRef] [Green Version]

- Kloos, S.; Madhavan, H.; Tidwell, T.; Blaikie, C.; Cuomu, M. The transnational Sowa Rigpa industry in Asia: New perspectives on an emerging economy. Soc. Sci. Med. 2020, 245, 112617. [Google Scholar] [CrossRef]

- Bode, M. Taking traditional knowledge to the market: The commoditization of Indian medicine. Med. Anthropol. 2006, 13, 225–236. [Google Scholar] [CrossRef]

- Biesen, C.M.Z. From coastal to global: The transnational flow of ayurveda and its relevance for Indo-African linkages. Glob. Public Health 2016, 13, 339–354. [Google Scholar] [CrossRef]

- Harilal, M.S. Commercialising traditional medicine: Ayurvedic manufacturing in Kerala. Econ. Polit. Wkly. 2009, 16, 44–51. Available online: https://www.jstor.org/stable/40279155 (accessed on 1 June 2020).

- Makunga, N.P.; Philander, L.E.; Smith, M. Current perspectives on an emerging formal natural products sector in South Africa. J. Ethnopharmacol. 2008, 119, 365–375. [Google Scholar] [CrossRef]

- Pyakurel, D.; Smith-Hall, C.; Bhattarai-Sharma, I.; Ghimire, S.K. Trade and conservation of Nepalese medicinal plants, fungi, and lichens. Econ. Bot. 2019, 73, 505–521. [Google Scholar] [CrossRef]

- Olsen, C.S. Valuation of commercial central Himalayan medicinal plants. Ambio 2005, 34, 607–610. [Google Scholar] [CrossRef] [PubMed]

- Pouliot, M.; Pyakurel, D.; Smith-Hall, C. High altitude organic gold: The production network for Ophiocordyceps sinensis from far-western Nepal. J. Ethnopharmacol. 2018, 218, 59–68. [Google Scholar] [CrossRef] [PubMed]

- Olsen, C.S.; Larsen, H.O. Alpine medicinal plant trade and Himalayan mountain livelihood strategies. Geogr. J. 2003, 169, 243–254. [Google Scholar] [CrossRef]

- Sharma, P.; Shrestha, N. Promoting Exports of Medicinal and Aromatic Plants (MAPs) and Essential Oils from Nepal; WTO/EIF Support Programme: Kathmandu, Nepal, 2011; Available online: http://sawtee.org/Research_Reports/R2011-04.pdf (accessed on 1 June 2020).

- Chapagain, A.; Kafle, G.; Das, A.K.; Caporale, F.; Mateo-Martín, J.; Usman, F.; Pouliot, M.; Smith-Hall, C. A Population List of Medicinal Plant Processing Enterprises in Nepal; IFRO Documentation 2019/3; Department of Food and Resource Economics, University of Copenhagen: Copenhagen, Denmark, 2019; Available online: https://static-curis.ku.dk/portal/files/230394492/IFRO_Documentation_2019_3.pdf (accessed on 1 June 2020).

- Paudel, N.S.; Adhikary, A.; Mbairamadji, J.; Nguyen, T.Q. Small-Scale Forest Enterprise Development in Nepal; Overview, Issues and Challenges; FAO: Rome, Italy, 2018; ISBN 978-92-5-131130-1. [Google Scholar]

- Subedi, B.P. Linking Plant-Based Enterprises and Local Communities to Biodiversity Conservation in Nepal Himalaya; Adroit Publishers: New Delhi, India, 2006; ISBN 81-87392-70-3. [Google Scholar]

- DFRS (State of Nepal’s Forests). Forest Resource Assessment (FRA) Nepal; Department of Forest Research and Survey: Kathmandu, Nepal, 2015. Available online: http://nkcs.org.np/dfrs/ecfl/pages/view.php?ref=567&k= (accessed on 1 June 2020).

- Olsen, C.S.; Helles, F. Market efficiency and benefit distribution in medicinal plant markets: Empirical evidence from South Asia. Int. J. Biodivers. Sci. Ecosyst. Serv. Manag. 2009, 5, 53–62. [Google Scholar] [CrossRef]

- Pyakurel, D.; Sharma, I.B.; Smith-Hall, C. Patterns of change: The dynamics of medicinal plant trade in far-western Nepal. J. Ethnopharmacol. 2018, 224, 323–334. [Google Scholar] [CrossRef]

- Larsen, H.O.; Olsen, C.S.; Boon, T.E. The non-timber forest policy process in Nepal: Actors, objectives and power. For. Policy Econ. 2000, 1, 267–281. [Google Scholar] [CrossRef]

- Larsen, H.O.; Smith, P.D.; Olsen, C.S. Nepal’s conservation policy options for commercial medicinal plant harvesting: Stakeholder views. Oryx 2005, 39, 435–441. [Google Scholar] [CrossRef] [Green Version]

- Pokharel, R.K.; Tiwari, K.R.; Thwaites, R. Community forestry in Nepal: Analysis of environmental outcomes. In Community Forestry in Nepal: Adapting to a Changing World; Thwaites, R., Fisher, R., Poudel, M., Eds.; Taylor & Francis: Oxon, UK, 2017; pp. 37–58. [Google Scholar] [CrossRef] [Green Version]

- Barakoti, T.P. Country status report on medicinal and aromatic plants in Nepal. In Proceedings of the Expert Consultation on Promotion of Medicinal and Aromatic Plants in the Asia-Pacific Region, Bangkok, Thailand, 2–3 December 2013; Paroda, R., Dasgupta, S., Mal, B., Ghosh, S.P., Pareek, S.K., Eds.; Asia-Pacific Association of Agricultural Research Institutions (APAARI): Bangkok, Thailand, 2014; pp. 124–138. Available online: http://www.apaari.org/wp-content/uploads/downloads/2014/10/Medicinal-and-Aromatic-Plants-Proceedings_21-10-2014-1.pdf (accessed on 1 June 2020).

- Olsen, C.S. The trade in medicinal and aromatic plants from central Nepal to northern India. Econ. Bot. 1998, 52, 279–292. [Google Scholar] [CrossRef]

- Macqueen, D.J. The role of small and medium forest enterprise associations in reducing poverty. In A Cut for the Poor, Proceedings of the International Conference on Managing Forests for Poverty Reduction: Capturing Opportunities in Forest Harvesting and Wood Processing for the Benefit of the Poor, Ho Chi Minh City, Vietnam, 3–6 October 2006; Oberndorf, R., Durst, P., Mahanty, S., Burslem, K., Suzuki, R., Eds.; FAO RAP Publication 2007/09 and RECOFTC Report 19; FAO: Bangkok, Thailand, 2007; pp. 192–203. Available online: http://www.fao.org/3/ag131e/ag131E00.htm (accessed on 1 June 2020).

- Larsen, H.O.; Olsen, C.S. Unsustainable collection and unfair trade? Uncovering and assessing assumptions regarding central Himalayan medicinal plant conservation. Biodivers. Conserv. 2007, 16, 1679–1697. [Google Scholar] [CrossRef]

- Kunwar, R.M.; Adhikari, Y.P.; Sharma, H.P.; Rimal, B.; Devkota, H.P.; Charmakar, S.; Acharya, R.P.; Baral, K.; Ansari, A.S.; Bhattarai, R.; et al. Distribution, use, trade and conservation of Paris polyphylla Sm. in Nepal. Glob. Ecol. Conserv. 2020, 23, e01081. [Google Scholar] [CrossRef]

- Bugge, M.M.; Hansen, T.; Klitkou, A. What is the bioeconomy? A review of the literature. Sustainability 2016, 8, 691. [Google Scholar] [CrossRef] [Green Version]

- Smith, T.; Beagley, L.; Bull, J.; Milner-Gulland, E.J.; Smith, M.; Vorhies, F.; Addison, P.F.E. Biodiversity means business: Reframing global biodiversity goals for the private sector. Conserv. Lett. 2020, 13, e12690. [Google Scholar] [CrossRef] [Green Version]

- Henderson, J.; Dicken, P.; Hess, M.; Coe, N.; Yeung, H.W.C. Global production networks and the analysis of economic development. Rev. Int. Polit. Econ. 2002, 9, 436–464. [Google Scholar] [CrossRef]

- Smith-Hall, C.; Pouliot, M.; Pyakurel, D.; Fold, N.; Chapagain, A.; Ghmire, S.; Meilby, H.; Kmoch, L.; Chapagain, D.J.; Das, A.; et al. Data Collection Instruments and Procedures for Investigating National-Level Trade in Medicinal and Aromatic Plants: The Case of Nepal; IFRO Documentation 2018/2; Department of Food and Resource Economics, University of Copenhagen: Copenhagen, Denmark, 2018; Available online: https://curis.ku.dk/portal/files/196408842/IFRO_Documentation_2018_2.pdf (accessed on 1 June 2020).

- Adam, Y.O.; Pettenella, D. The contribution of small-scale forestry-based enterprises to the rural economy in the developing world: The case of the informal carpentry sector, Sudan. Small Scale For. 2002, 12, 461–474. [Google Scholar] [CrossRef]

- Marshall, E. Health and Wealth from Medicinal Aromatic Plants; FAO Diversification Booklet 17; FAO: Rome, Italy, 2011; ISBN 978-92-5-107070-3. [Google Scholar]

- Fellows, P. Processing for Prosperity, 2nd ed.; FAO Diversification Booklet 5; FAO: Rome, Italy, 2011; Available online: http://www.fao.org/3/a-i2468e.pdf (accessed on 1 June 2020).

- Fellows, P. Value from Village Processing, 2nd ed.; FAO Diversification Booklet 4; FAO: Rome, Italy, 2011; Available online: http://www.fao.org/3/i2467e/i2467e00.pdf (accessed on 1 June 2020).

- Olsen, C.S.; Bhattarai, N. A typology of economic agents in the Himalayan plant trade. Mount. Res. Dev. 2005, 25, 37–44. [Google Scholar] [CrossRef] [Green Version]

- UNEP. Green Economy Sector Study. Biotrade: Harnessing the Potential for Transitioning to a Green Economy—The Case of Medicinal and Aromatic Plants in Nepal; United Nations Environment Programme: Geneva, Switzerland, 2012; Available online: https://wedocs.unep.org/bitstream/handle/20.500.11822/25917/biotrade_Nepal.pdf?sequence=1&isAllowed=y (accessed on 1 June 2020).

- Pant, P.R.; Dangol, D. Kathmandu Valley profile. In Proceedings of the Governance and Infrastructure Development Challenges in the Kathmandu Valley Workshop, Kathmandu, Nepal, 11–13 February 2009; Available online: https://www.eastwestcenter.org/fileadmin/resources/seminars/Urbanization_Seminar/Kathmandu_Valley_Brief_for_EWC___KMC_Workshop__Feb_2009_.pdf (accessed on 1 June 2020).

- Tiwari, S.; Bhattarai, K. Migration, Remittances and Forests: Disentangling the Impact of Population and Economic Growth on Forests; World Bank, Policy Research Working Paper 5907; World Bank: Washington, DC, USA, 2004. [Google Scholar] [CrossRef]

- Coe, N.M.; Yeung, H.W.-C. Global Production Networks: Theorizing Economic Development in an Interconnected World; Oxford University Press: Oxford, UK, 2015. [Google Scholar] [CrossRef]

- Kafle, G.; Bhattarai-Sharma, I.; Siwakoti, M.; Shrestha, A.K. Demand, end-uses, and conservation of alpine medicinal plant Neopicrorhiza scrophulariiflora (Pennell) D.Y. Hong in central Himalaya. Evid. Based Complement. Altern. Med. 2018, 2018. [Google Scholar] [CrossRef] [Green Version]

- Sharma, U.R. Medicinal and aromatic plants: A growing commercial sector of Nepal. Initiation 2007, 1, 4–8. [Google Scholar] [CrossRef] [Green Version]

- Goraya, G.S.; Ved, D.K. Medicinal Plants in India: An Assessment of their Demand and Supply; National Medicinal Plants Board, Ministry of AYUSH, Government of India; New Delhi and Indian Council of Forestry Research & Education: Dehradun, India, 2017; ISBN 978-81-211-0628-3.

- Cunningham, A.B.; Brinckmann, J.A.; Yang, X.; He, J. Introduction to the special issue: Saving plants, saving lifes: Trade, sustainable harvest and conservation of traditional medicinals in Asia. J. Ethnopharmacol. 2019, 229, 288–292. [Google Scholar] [CrossRef]

- Hinsley, A.; Milner-Gulland, E.J.; Cooney, R.; Timoshyna, A.; Ruan, X.; Lee, T.M. Building sustainability into the belt and road initiative’s traditional Chinese medicine trade. Nat. Sustain. 2020, 3, 96–100. [Google Scholar] [CrossRef]

- Meilby, H.; Smith-Hall, C.; Byg, A.; Larsen, H.O.; Nielsen, Ø.J.; Puri, L.; Rayamajhi, S. Are forest incomes sustainable? Firewood and timber extraction and forest productivity in community managed forests in Nepal. World Dev. 2014, 64, S113–S124. [Google Scholar] [CrossRef]

- National Planning Commission. Preliminary Results of National Economic Census 2018 of Nepal; National Planning Commission, Central Bureau of Statistics: Kathmandu, Nepal, 2019. Available online: https://cbs.gov.np/wp-content/upLoads/2018/12/NEC2018-Preliminary-Results-National-Report-No.1-complete-set-final-rev6-180916.pdf (accessed on 1 June 2020).

- Collier, P. The Plundered Planet; Penguin Books: London, UK, 2010; ISBN 978-0-1410-4214-5. [Google Scholar]

- National Planning Commission. Sustainable Development Goals, 2016–2030. National (Preliminary) Report; National Planning Commission, Central Bureau of Statistics: Kathmandu, Nepal, 2015. Available online: https://www.undp.org/content/dam/nepal/docs/reports/SDG%20final%20report-nepal.pdf (accessed on 1 June 2020).

- Cosic, D.; Dahal, S.; Kitzmuller, M. Climbing Higher: Toward a Middle-Income Nepal. Country Economic Memorandum; The World Bank: Washington, DC, USA, 2017. [Google Scholar] [CrossRef]

- MoC. Nepal Trade Integration Strategy (NTIS); Ministry of Commerce: Kathmandu, Nepal, 2016. Available online: https://www.oecd.org/aidfortrade/countryprofiles/dtis/Napal-DTIS-2016.pdf (accessed on 1 June 2020).

- World Bank. Doing Business 2020: Comparing Business Regulation in 190 Economies—Economy Profile of Nepal (English); World Bank Group: Washington, DC, USA, 2019. [Google Scholar]

- Childs, G.; Craig, S.; Beall, C.M.; Basnyat, B. Depopulating the Himalayan highlands: Education and outmigration from ethnically Tibetan communities of Nepal. Mt. Res. Dev. 2014, 34, 85–94. [Google Scholar] [CrossRef]

- Mala, W.A.; Tieguhong, J.C.; Ndoye, O.; Grouwels, S.; Betti, J.L. Collective action and promotion of forest based associations on non-wood forest products in Cameroon. Dev. Pract. 2012, 22, 1122–1134. [Google Scholar] [CrossRef]

- Baral, S.; Meilby, H.; Chettri, B.B.K.; Basnyat, B.; Rayamajhi, S.; Awale, S. Politics of getting the numbers right: Community forest inventory of Nepal. For. Policy Econ. 2018, 91, 19–26. [Google Scholar] [CrossRef]

- Basnyat, B.; Treue, T.; Pokharel, R.K. Bureaucratic recentralisation of Nepal’s community forestry sector. Int. For. Rev. 2019, 21, 401–415. [Google Scholar] [CrossRef]

- Kunwar, R.M.; Mahat, L.; Acharya, R.P.; Bussmann, R.W. Medicinal plants, traditional medicine, markets and management in far-west Nepal. J. Ethnobiol. Ethnomed. 2013, 9, 24. [Google Scholar] [CrossRef] [Green Version]

- Maneesha, S.; Deep, S. Zanthoxylum armatum DC: Past, present and future prospective. Biotech Today Int. J. Biol. Sci. 2017, 7, 21–24. [Google Scholar]

- IPCC. Climate Change and land: An IPCC Special Report on Climate Change, Desertification, Land Degradation, Sustainable Land Management, Food Security, and Greenhouse Gas Fluxes in Terrestrial Ecosystems. Summary for Policymakers; IPCC: Geneva, Switzerland, 2020; ISBN 978-92-9169-154-8. [Google Scholar]

- Staffas, L.; Gustavsson, M.; McCormick, K. Strategies and policies for the bioeconomy and bio-based economy: An analysis of official national approaches. Sustainability 2013, 5, 2751–2769. [Google Scholar] [CrossRef] [Green Version]

| Stratum | Subpopulation 1 | Sample | |

|---|---|---|---|

| Raw Materials | End Products 2 | ||

| Large enterprises | 10 | 8 | 5 |

| Small enterprises—Kathmandu Valley | 91 | 41 | 4 |

| Small enterprises—other districts | 132 | 30 | 11 |

| Totals | 233 | 79 | 20 3 |

| Enabling Factors | Mean ± SD 1 | Median | Mode | Min | Max |

|---|---|---|---|---|---|

| External: Macroeconomics and Markets | |||||

| Domestic demand | 4.23 ± 1.24 | 5 | 5 | 1 | 5 |

| Demand from China | 2.54 ± 1.56 | 2 | 1 | 1 | 5 |

| Demand from India | 2.23 ± 1.64 | 1 | 1 | 1 | 5 |

| Demand from the rest of the world | 3.15 ± 1.86 | 4 | 5 | 1 | 5 |

| Prices of raw materials | 4.15 ± 0.99 | 4 | 5 | 2 | 5 |

| Competitiveness with other companies | 3.31 ± 1.32 | 3 | 3 | 1 | 5 |

| Presence of monopolies/oligopolies | 2.69 ± 1.44 | 3 | 3 | 1 | 5 |

| Availability of new technologies | 4.62 ± 0.96 | 5 | 5 | 2 | 5 |

| Variations of interest rate | 3.62 ± 1.61 | 4 | 5 | 1 | 5 |

| China import regulations | 2.54 ± 1.81 | 1 | 1 | 1 | 5 |

| India import regulations | 2.69 ± 1.75 | 3 | 1 | 1 | 5 |

| Rest of the world import regulations | 3.15 ± 1.72 | 3 | 5 | 1 | 5 |

| Import regulations in Nepal | 3.77 ± 1.24 | 4 | 5 | 2 | 5 |

| Availability of skilled labour | 4.62 ± 0.77 | 5 | 5 | 3 | 5 |

| Cost of labour | 4.31 ± 0.75 | 4 | 5 | 3 | 5 |

| Improvement in infrastructure | 4.46 ± 0.88 | 5 | 5 | 3 | 5 |

| Socio-economic stability | 4.54 ± 0.66 | 5 | 5 | 3 | 5 |

| External: Regulatory Framework | |||||

| Regulations and requirements | 4.38 ± 1.33 | 5 | 5 | 1 | 5 |

| Standards and certifications | 4.23 ± 1.01 | 5 | 5 | 2 | 5 |

| Governmental taxes | 3.23 ± 1.59 | 3 | 5 | 1 | 5 |

| Governmental subsidies | 3.92 ± 1.50 | 5 | 5 | 1 | 5 |

| Rent-seeking behaviour (12) 2 | 3.83 ± 1.34 | 4 | 5 | 2 | 5 |

| Bureaucratic delays | 4.00 ± 1.22 | 4 | 5 | 1 | 5 |

| Restrictions on specific plants | 3.85 ± 1.41 | 4 | 4 | 1 | 5 |

| Internal: Financial Capital | |||||

| Access to capital and credit | 3.92 ± 1.44 | 5 | 5 | 1 | 5 |

| Access to insurance | 4.00 ± 1.29 | 4 | 5 | 1 | 5 |

| Internal: Business Management Capacities | |||||

| Marketing skills | 4.54 ± 0.66 | 5 | 5 | 3 | 5 |

| Decentralised management | 2.38 ± 1.76 | 1 | 1 | 1 | 5 |

| Role of auditing | 4.31 ± 1.49 | 5 | 5 | 1 | 5 |

| Internal: Clustering / Collaboration with other companies | |||||

| Importance of being a member of producers’ organisations (11) | 4.36 ± 1.03 | 5 | 5 | 2 | 5 |

| Importance of sharing knowledge and good practices (10) | 3.90 ± 1.37 | 4 | 4 | 1 | 5 |

| Importance of sharing production costs (2) | 4.67 ± 0.58 | 5 | 5 | 4 | 5 |

| A. Enterprise Characteristics | Estimate |

| Ownership | |

| Privately owned | 86.1% |

| State owned | 8.9% |

| Community forest user groups | 2.5% |

| Multi-purpose cooperative | 2.5% |

| Permanent employees (no., mean ± SD, min–max) | 6.4 ± 9.8 (0–50) |

| Temporary employees (no., mean ± SD, min–max) | 6.6 ± 9.2 (0–50) |

| Mode of operation | |

| Continuous | 44.3% |

| Seasonal | 55.7% |

| Profitability | |

| Profit | 70.9% |

| No answer | 16.5% |

| Loss | 8.9% |

| Breaking even | 3.8% |

| B. CEO Characteristics | Estimate |

| Gender (male, female) | 93.7%, 6.3% |

| Age (yrs, mean ± SD, min–max) | 46.4 ± 11.0 (27–78) |

| Age distribution (yrs) | |

| ≤30 | 3.8% |

| 31–40 | 29.1% |

| 41–50 | 34.2% |

| >50 | 32.9% |

| Experience (yrs, mean ± SD, min–max) | 11.8 ± 7.6 (1–36) |

| Experience distribution (yrs) | |

| ≤2 | 3.8% |

| 3–5 | 16.5% |

| 6–10 | 30.0% |

| >10 | 41.8% |

| Education | |

| Above high school | 72.2% |

| School Leaving Certificate and equivalent | 15.2% |

| Lower secondary or primary | 7.6% |

| Non-formal education, no answer | 5.1% |

| Castes | |

| Brahman, Chhetri, Newar (higher) | 77.2% |

| Sanyasi, Gurung, Muslim, Tharu, Limbu, Magar, Marwadi, Rai, Sherpa, Sonar, Sudhi, Thakuri (lower) | 22.8% |

| Purchased Medicinal Plants | End Products | |||||||

|---|---|---|---|---|---|---|---|---|

| Volume (kg) | Volume (%) | Value (USD) | Value (%) | Volume (kg) | Volume (%) | Value (USD) | Value (%) | |

| Large enterprises | 863,571 | 23.5 | 1,258,268 | 31.3 | 70,328 | 14.2 | 1,146,635 | 10.2 |

| Small enterprises | ||||||||

| Kathmandu Valley | 1,818,067 | 49.4 | 884,457 | 22.0 | 336,973 | 68.2 | 4,518,476 | 40.2 |

| Other districts | 997,216 | 27.1 | 1,880,161 | 46.7 | 86,868 | 17.6 | 5,581,175 | 49.6 |

| Total | 3,678,854 | 100.0 | 4,022,886 | 100.0 | 494,169 | 100.0 | 11,246,286 | 100.0 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Caporale, F.; Mateo-Martín, J.; Usman, M.F.; Smith-Hall, C. Plant-Based Sustainable Development—The Expansion and Anatomy of the Medicinal Plant Secondary Processing Sector in Nepal. Sustainability 2020, 12, 5575. https://doi.org/10.3390/su12145575

Caporale F, Mateo-Martín J, Usman MF, Smith-Hall C. Plant-Based Sustainable Development—The Expansion and Anatomy of the Medicinal Plant Secondary Processing Sector in Nepal. Sustainability. 2020; 12(14):5575. https://doi.org/10.3390/su12145575

Chicago/Turabian StyleCaporale, Filippo, Jimena Mateo-Martín, Muhammad Faizan Usman, and Carsten Smith-Hall. 2020. "Plant-Based Sustainable Development—The Expansion and Anatomy of the Medicinal Plant Secondary Processing Sector in Nepal" Sustainability 12, no. 14: 5575. https://doi.org/10.3390/su12145575

APA StyleCaporale, F., Mateo-Martín, J., Usman, M. F., & Smith-Hall, C. (2020). Plant-Based Sustainable Development—The Expansion and Anatomy of the Medicinal Plant Secondary Processing Sector in Nepal. Sustainability, 12(14), 5575. https://doi.org/10.3390/su12145575