Exploring CEO Messages in Sustainability Management Reports: Applying Sentiment Mining and Sustainability Balanced Scorecard Methods

Abstract

:1. Introduction

This sustainability report includes both financial and non-financial performance. Some major issues contain recent and past three years’ quantitative data to help readers’ understanding.(Lotte Engineering and Construction)

In order to effectively respond to environmental changes in financial and non-financial risks that may occur in the entire process of business activities, including project orders, contracts, construction, and delivery, we operate a risk management team. We identified tasks that reduce construction costs, thereby improving profit margins.(Samsung Heavy Industries)

2. Literature Review and Hypothesis Development

2.1. Implications of CEO Messages

2.2. Issuance of the Sustainability Management Report

2.3. Balanced Scorecard Approach

2.4. Hypothesis Development

In 2017, the financial value was approximately 42.19 trillion KRW, while the “True Value”, including social, economic, and environmental values, reached to 49.16 trillion KRW. This is about 16.5% higher than the financial value, which is 89.2% higher than the “True Value” in 2016.(Samsung Electronics 2017 Sustainability Management Report)

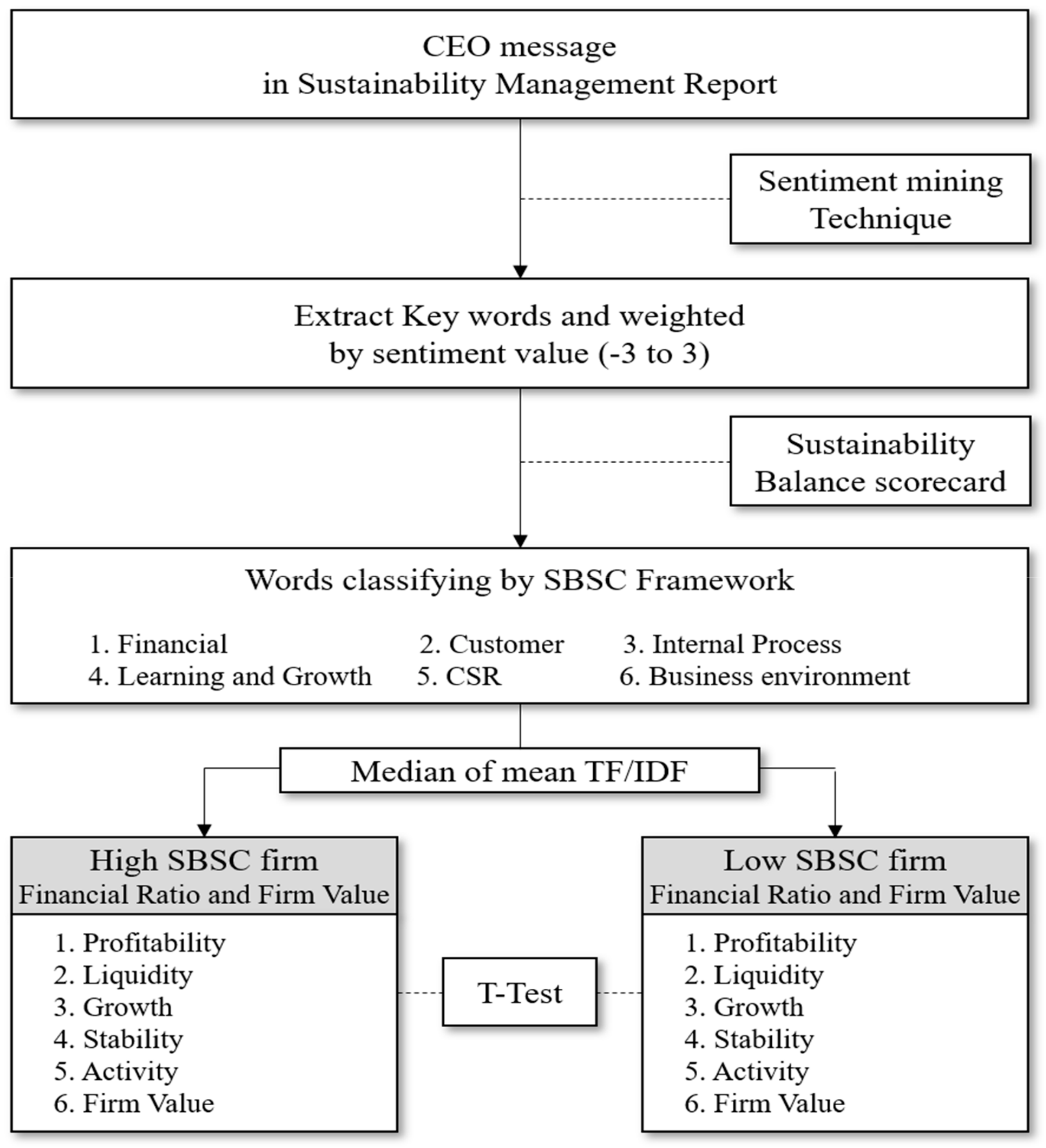

3. Research Design

3.1. Sample Selection

3.2. Sentiment Mining Technique for Analyzing Textual Data

3.3. Classifying Sustainability Management Perspectives by SBSC Framework

3.4. Financial Indicators

3.5. Research Methodology

4. Empirical Results

4.1. Descriptive Statistics

4.2. CEO Message in Sustainable Management Report and Financial Status

4.3. One-Year Change in Financial Status after Disclosing the CEO Message in the Sustainable Management Report

4.4. Multi-Regression Analysis

5. Summary of Results and Discussion

6. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Cormier, D.; Magnan, M. The economic relevance of environmental disclosure and its impact on corporate legitimacy: An empirical investigation. Bus. Strategy Environ. 2015, 24, 431–450. [Google Scholar] [CrossRef]

- Burke, J.J.; Clark, C.E. The business case for integrated reporting: Insights from leading practitioners, regulators, and academics. Bus. Horiz. 2016, 59, 273–283. [Google Scholar] [CrossRef]

- Butler, J.B.; Henderson, S.C.; Raiborn, C. Sustainability and the balanced scorecard: Integrating green measures into business reporting. Manag. Account. Q. 2011, 12, 1–10. [Google Scholar]

- Falle, S.; Rauter, R.; Engert, S.; Baumgartner, R. Sustainability management with the sustainability balanced scorecard in SMEs: Findings from an Austrian case study. Sustainability 2016, 8, 545. [Google Scholar] [CrossRef] [Green Version]

- Kang, J.S.; Chiang, C.F.; Huangthanapan, K.; Downing, S. Corporate social responsibility and sustainability balanced scorecard: The case study of family-owned hotels. Int. J. Hosp. Manag. 2015, 48, 124–134. [Google Scholar] [CrossRef]

- Rabbani, A.; Zamani, M.; Yazdani-Chamzini, A.; Zavadskas, E.K. Proposing a new integrated model based on sustainability balanced scorecard (SBSC) and MCDM approaches by using linguistic variables for the performance evaluation of oil producing companies. Expert Syst. Appl. 2014, 41, 7316–7327. [Google Scholar] [CrossRef]

- Lueg, R.; Pedersen, M.M.; Clemmensen, S.N. The role of corporate sustainability in a low-cost business model–A case study in the Scandinavian fashion industry. Bus. Strategy Environ. 2015, 24, 344–359. [Google Scholar] [CrossRef]

- Amernic, J.; Craig, R.; Tourish, D. Measuring and Assessing Tone at the Top Using Annual Report CEO Letters; The Institute of Chartered Accountants of Scotland: Edinburgh, UK, 2010. [Google Scholar]

- Andreia Costa, G.; Cristina Oliveira, L.; Lima Rodrigues, L.; Craig, R. Factors associated with the publication of a CEO letter. Corp. Commun. Int. J. 2013, 18, 432–450. [Google Scholar] [CrossRef]

- Aerts, W.; Cormier, D.; Magnan, M. Corporate environmental disclosure, financial markets and the media: An international perspective. Ecol. Econ. 2008, 64, 643–659. [Google Scholar] [CrossRef]

- Amernic, J.H.; Craig, R.J. Guidelines for CEO-speak: Editing the language of corporate leadership. Strategy Leadersh. 2007, 35, 25–31. [Google Scholar] [CrossRef]

- Amernic, J.; Russell, C. Improving CEO-speak. J. Account. 2007, 203, 65–66. [Google Scholar]

- Santema, S.; Van de Rijt, J. Strategy disclosure in Dutch annual reports. Eur. Manag. J. 2001, 19, 101–108. [Google Scholar] [CrossRef]

- Mäkelä, H.; Laine, M. A CEO with many messages: Comparing the ideological representations provided by different corporate reports. Account. Forum 2011, 35, 217–231. [Google Scholar] [CrossRef]

- Kohut, G.F.; Segars, A.H. The president’s letter to stockholders: An examination of corporate communication strategy. J. Bus. Commun. (1973) 1992, 29, 7–21. [Google Scholar] [CrossRef]

- Segars, A.H.; Kohut, G.F. Strategic communication through the World Wide Web: An empirical model of effectiveness in the CEO’s letter to shareholders. J. Manag. Stud. 2001, 38, 535–556. [Google Scholar] [CrossRef]

- Clatworthy, M.; Jones, M.J. The effect of thematic structure on the variability of annual report readability. Account. Audit. Account. J. 2001, 14, 311–326. [Google Scholar] [CrossRef]

- Clatworthy, M.A.; Jones, M.J. Differential patterns of textual characteristics and company performance in the chairman’s statement. Account. Audit. Account. J. 2006, 19, 493–511. [Google Scholar] [CrossRef]

- Diouf, D.; Boiral, O. The quality of sustainability reports and impression management: A stakeholder perspective. Account. Audit. Account. J. 2017, 30, 643–667. [Google Scholar] [CrossRef]

- King, A.; Bartels, W. The KPMG Survey of Corporate Responsibility Reporting 2015. KPMG. 2015. Available online: https://assets.kpmg.com/content/dam/kpmg/pdf/2016/05/KPMGSurvey_of_CRReporting_2015.pdf (accessed on 22 September 2019).

- UNGC Homepage. Available online: https://www.unglobalcompact.org (accessed on 22 September 2019).

- Henry, E. Are investors influenced by how earnings press releases are written? J. Bus. Commun. (1973) 2008, 45, 363–407. [Google Scholar] [CrossRef]

- Jameson, D.A. Telling the investment story: A narrative analysis of shareholder reports. J. Bus. Commun. (1973) 2000, 37, 7–38. [Google Scholar] [CrossRef]

- Cho, C.H.; Roberts, R.W.; Patten, D.M. The language of US corporate environmental disclosure. Account. Organ. Soc. 2010, 35, 431–443. [Google Scholar] [CrossRef]

- Guay, W.; Samuels, D.; Taylor, D. Guiding through the fog: Financial statement complexity and voluntary disclosure. J. Account. Econ. 2016, 62, 234–269. [Google Scholar] [CrossRef]

- Barkemeyer, R.; Holt, D.; Preuss, L.; Tsang, S. What happened to the ‘development’ in sustainable development? Business guidelines two decades after Brundtland. Sustain. Dev. 2014, 22, 15–32. [Google Scholar] [CrossRef] [Green Version]

- Hooghiemstra, R. Corporate communication and impression management–new perspectives why companies engage in corporate social reporting. J. Bus. Ethics 2000, 27, 55–68. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Norton, D.P. Linking the balanced scorecard to strategy. Calif. Manag. Rev. 1996, 39, 53–79. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Norton, D.P. Measuring the strategic readiness of intangible assets. Harv. Bus. Rev. 2004, 82, 52–63. [Google Scholar]

- Kaplan, R.S.; Norton, D.P. The balanced scorecard: Measures that drive performance. Harv. Bus. Rev. 1992, 70, 71–79. [Google Scholar]

- Hansen, E.G.; Schaltegger, S. The sustainability balanced scorecard: A systematic review of architectures. J. Bus. Ethics 2016, 133, 193–221. [Google Scholar] [CrossRef]

- Bonner, S.E.; Hastie, R.; Sprinkle, G.B.; Young, S.M. A review of the effects of financial incentives on performance in laboratory tasks: Implications for management accounting. J. Manag. Account. Res. 2000, 12, 19–64. [Google Scholar] [CrossRef]

- Kaplan, R.S. The balanced scorecard: Comments on balanced scorecard commentaries. J. Account. Organ. Chang. 2012, 8, 539–545. [Google Scholar] [CrossRef]

- Kaplan, R.S.; Norton, D.P. Transforming the balanced scorecard from performance measurement to strategic management: Part II. Account. Horiz. 2001, 15, 147–160. [Google Scholar] [CrossRef]

- Lipe, M.G.; Salterio, S.E. The balanced scorecard: Judgmental effects of common and unique performance measures. Account. Rev. 2000, 75, 283–298. [Google Scholar] [CrossRef]

- Cooper, D.J.; Ezzamel, M.; Qu, S.Q. Popularizing a management accounting idea: The case of the balanced scorecard. Contemp. Account. Res. 2017, 34, 991–1025. [Google Scholar] [CrossRef]

- Figge, F.; Hahn, T.; Schaltegger, S.; Wagner, M. The Sustainability Balanced Scorecard–Theory and Application of a Tool for Value-Based Sustainability Management. In Proceedings of the Greening of Industry Network Conference, Göteborg, Sweden, 23–26 June 2002; Volume 2. [Google Scholar]

- Gumbus, A.; Lussier, R.N. Entrepreneurs use a balanced scorecard to translate strategy into performance measures. J. Small Bus. Manag. 2006, 44, 407–425. [Google Scholar] [CrossRef]

- Johnson, M.P.; Schaltegger, S. Two decades of sustainability management tools for SMEs: How far have we come? J. Small Bus. Manag. 2016, 54, 481–505. [Google Scholar] [CrossRef]

- Malagueño, R.; Lopez-Valeiras, E.; Gomez-Conde, J. Balanced scorecard in SMEs: Effects on innovation and financial performance. Small Bus. Econ. 2018, 51, 221–244. [Google Scholar] [CrossRef]

- Lin, H.F. Linking knowledge management orientation to balanced scorecard outcomes. J. Knowl. Manag. 2015, 19, 1224–1249. [Google Scholar] [CrossRef]

- Aly, A.H.; Mansour, M.E. Evaluating the sustainable performance of corporate boards: The balanced scorecard approach. Manag. Audit. J. 2017, 32, 167–195. [Google Scholar] [CrossRef]

- Bournois, F.; Point, S. A letter from the president: Seduction, charm and obfuscation in French CEO letters. J. Bus. Strategy 2006, 27, 46–55. [Google Scholar] [CrossRef]

- Grueber, M.; Studt, T. 2011 Global R&D Funding Forecast: CEO Message. R D Mag. 2010, 52, 31–64. [Google Scholar]

- Sonnier, B.M. Intellectual capital disclosure: High-tech versus traditional sector companies. J. Intellect. Cap. 2008, 9, 705–722. [Google Scholar] [CrossRef]

- Cianci, A.M.; Kaplan, S.E. The effect of CEO reputation and explanations for poor performance on investors’ judgments about the company’s future performance and management. Account. Organ. Soc. 2010, 35, 478–495. [Google Scholar] [CrossRef]

- Manner, M.H. The impact of CEO characteristics on corporate social performance. J. Bus. Ethics 2010, 93, 53–72. [Google Scholar] [CrossRef]

- Barker III, V.L.; Mueller, G.C. CEO characteristics and firm R&D spending. Manag. Sci. 2002, 48, 782–801. [Google Scholar]

- Bird, R.; Hall, A.D.; Momentè, F.; Reggiani, F. What corporate social responsibility activities are valued by the market? J. Bus. Ethics 2007, 76, 189–206. [Google Scholar] [CrossRef]

- BISD Homepage. Available online: https://www.bisd.or.kr (accessed on 22 September 2019).

- KIS-VALUE. Available online: https://www.kisvalue.com (accessed on 22 September 2019).

- TS-2000. Available online: http://www.kocoinfo.com (accessed on 22 September 2019).

- Collobert, R.; Weston, J. A Unified Architecture for Natural Language Processing: Deep Neural Networks with Multitask Learning. In Proceedings of the 25th International Conference on Machine Learning, Helsinki, Finland, 5–9 July 2008; pp. 160–167. [Google Scholar]

- Manning, C.; Surdeanu, M.; Bauer, J.; Finkel, J.; Bethard, S.; McClosky, D. The Stanford CoreNLP Natural Language Processing Toolkit. In Proceedings of the 52nd Annual Meeting of the Association for Computational Linguistics: System Demonstrations, Baltimore, MD, USA, 22–27 June 2014; pp. 55–60. [Google Scholar]

- Joulin, A.; Grave, E.; Bojanowski, P.; Mikolov, T. Bag of tricks for efficient text classification. arXiv 2016, arXiv:1607.01759. [Google Scholar]

- Nahm, U.Y.; Mooney, R.J. Text Mining with Information Extraction. In Proceedings of the AAAI 2002 Spring Symposium on Mining Answers from Texts and Knowledge Bases, Palo Alto, CA, USA, 25–27 March 2002; pp. 60–67. [Google Scholar]

- Sriram, B.; Fuhry, D.; Demir, E.; Ferhatosmanoglu, H.; Demirbas, M. Short Text Classification in Twitter to Improve Information Filtering. In Proceedings of the 33rd International ACM SIGIR Conference on Research and Development in Information Retrieval, Geneva, Switzerland, 19–23 July 2010; pp. 841–842. [Google Scholar]

- Sun, H.; Sun, X.; Wang, H.; Li, Y.; Li, X. Automatic target detection in high-resolution remote sensing images using spatial sparse coding bag-of-words model. IEEE Geosci. Remote Sens. Lett. 2011, 9, 109–113. [Google Scholar] [CrossRef]

- Jing, L.P.; Huang, H.K.; Shi, H.B. Improved Feature Selection Approach TFIDF in Text Mining. In Proceedings of the International Conference on Machine Learning and Cybernetics, Beijing, China, 4–5 November 2002; Volume 2, pp. 944–946. [Google Scholar]

- Ramos, J. Using TF-IDF to Determine Word Relevance in Document Queries. In Proceedings of the First Instructional Conference on Machine Learning, Piscataway, NJ, USA, 3–8 December 2003; Volume 242, pp. 133–142. [Google Scholar]

- Zhang, W.; Yoshida, T.; Tang, X. A comparative study of TF* IDF, LSI and multi-words for text classification. Expert Syst. Appl. 2011, 38, 2758–2765. [Google Scholar] [CrossRef]

- Mohamad, N.E.A.B.; Saad, N.B.M. Working capital management: The effect of market valuation and profitability in Malaysia. Int. J. Bus. Manag. 2010, 5, 140. [Google Scholar]

- Anbar, A.; Alper, D. Bank specific and macroeconomic determinants of commercial bank profitability: Empirical evidence from Turkey. Bus. Econ. Res. J. 2011, 2, 139–152. [Google Scholar]

- Ball, R.; Gerakos, J.; Linnainmaa, J.T.; Nikolaev, V. Accruals, cash flows, and operating profitability in the cross section of stock returns. J. Financ. Econ. 2016, 121, 28–45. [Google Scholar] [CrossRef]

- Saleem, Q.; Rehman, R.U. Impacts of liquidity ratios on profitability. Interdiscip. J. Res. Bus. 2011, 1, 95–98. [Google Scholar]

- Al Nimer, M.; Warrad, L.; Al Omari, R. The impact of liquidity on Jordanian banks profitability through return on assets. Eur. J. Bus. Manag. 2015, 7, 229–232. [Google Scholar]

- Emery, G.W.; Cogger, K.O. The measurement of liquidity. J. Account. Res. 1982, 20, 290–303. [Google Scholar] [CrossRef]

- Cooper, M.J.; Gulen, H.; Schill, M.J. Asset growth and the cross-section of stock returns. J. Financ. 2008, 63, 1609–1651. [Google Scholar] [CrossRef]

- Covin, J.G.; Green, K.M.; Slevin, D.P. Strategic process effects on the entrepreneurial orientation–sales growth rate relationship. Entrep. Theory Pract. 2006, 30, 57–81. [Google Scholar] [CrossRef]

- Varaiya, N.; Kerin, R.A.; Weeks, D. The relationship between growth, profitability, and firm value. Strateg. Manag. J. 1987, 8, 487–497. [Google Scholar] [CrossRef]

- Shin, H.S. Securitisation and financial stability. Econ. J. 2009, 119, 309–332. [Google Scholar] [CrossRef]

- Deakin, E.B. Distributions of financial accounting ratios: Some empirical evidence. Account. Rev. 1976, 51, 90–96. [Google Scholar]

- Wilcox, J.A. Nominal interest rate effects on real consumer expenditure. Bus. Econ. 1990, 25, 31–37. [Google Scholar]

- Gupta, M.C. The effect of size, growth, and industry on the financial structure of manufacturing companies. J. Financ. 1969, 24, 517–529. [Google Scholar]

- Warrad, L. The impact of working capital turnover on Jordanian chemical industries’ profitability. Am. J. Econ. Bus. Adm. 2013, 5, 116–119. [Google Scholar]

- Büyüksalvarci, A.; Abdioglu, H. Corporate governance, financial ratios and stock returns: An empirical analysis of Istanbul Stock Exchange (ISE). Int. Res. J. Financ. Econ. 2010, 57, 70–81. [Google Scholar]

- Ou, J.A.; Penman, S.H. Accounting measurement, price-earnings ratio, and the information content of security prices. J. Account. Res. 1989, 27, 111–144. [Google Scholar] [CrossRef]

- Pae, J.; Thornton, D.B.; Welker, M. The link between earnings conservatism and the price-to-book ratio. Contemp. Account. Res. 2005, 22, 693–717. [Google Scholar] [CrossRef]

- Lang, L.H.; Stulz, R.M. Tobin’s q, corporate diversification, and firm performance. J. Polit. Econ. 1994, 102, 1248–1280. [Google Scholar]

{kind=link}

| Variables | Definition | |

|---|---|---|

| Profitable | ROA | Return on asset [62] |

| ROE | Return on equity [63] | |

| CFO | Cash flow from operating scaled by asset [64] | |

| Liquidity | CUR | Current ratio [65] |

| QUICK | Quick ratio [66] | |

| DEFINT | Defensive interval [67] | |

| Growth | ASSGRW | Asset growth [68] |

| REVGRW | Sales growth [69] | |

| TANGRW | Tangible asset growth [70] | |

| Stability | DEBT | Debt to equity ratio [71] |

| BORR | Liabilities to asset ratio [72] | |

| COD | The average after-tax interest from total borrowing [73] | |

| Activity | ASSTOV | Asset turnover [74] |

| WCTOV | Working capital turnover [75] | |

| TANTOV | Tangible asset turnover [76] | |

| Firm Value | PER | Price to earning ratio [77] |

| PBR | Price to book ratio [78] | |

| TQ | Tobin’s Q [79] | |

| Variables | Definition | |

|---|---|---|

| TF/IDF | FIN | The mean of word’s TF/IDF related to financial perspective |

| CUS | The mean of word’s TF/IDF related to customer perspective | |

| INP | The mean of word’s TF/IDF related to internal process perspective | |

| LNG | The mean of word’s TF/IDF related to learning and growth perspective | |

| CSR | The mean of word’s TF/IDF related to CSR perspective | |

| ENV | The mean of word’s TF/IDF related to business environment perspective | |

| Variables | N | Mean | Std | Min | Q1 | Median | Q3 | Max | |

|---|---|---|---|---|---|---|---|---|---|

| TF/IDF | FIN | 129 | 0.007 | 0.006 | 0.000 | 0.003 | 0.006 | 0.011 | 0.019 |

| CUS | 129 | 0.007 | 0.005 | 0.001 | 0.003 | 0.005 | 0.009 | 0.017 | |

| INP | 129 | 0.008 | 0.004 | 0.003 | 0.005 | 0.008 | 0.010 | 0.015 | |

| LNG | 129 | 0.007 | 0.003 | 0.003 | 0.005 | 0.007 | 0.010 | 0.013 | |

| CSR | 129 | 0.006 | 0.006 | 0.000 | 0.002 | 0.005 | 0.009 | 0.018 | |

| ENV | 129 | 0.006 | 0.003 | 0.001 | 0.003 | 0.005 | 0.007 | 0.012 | |

| Profitable | ROA | 129 | 0.043 | 0.047 | −0.021 | 0.011 | 0.033 | 0.067 | 0.148 |

| ROE | 128 | 0.075 | 0.110 | −0.053 | 0.023 | 0.062 | 0.110 | 0.261 | |

| CFO | 129 | 0.070 | 0.075 | −0.070 | 0.032 | 0.067 | 0.117 | 0.191 | |

| Liquidity | CUR | 129 | 2.326 | 5.360 | 0.488 | 0.897 | 1.254 | 1.747 | 4.350 |

| QUICK | 129 | 1.989 | 4.720 | 0.387 | 0.712 | 1.032 | 1.438 | 3.656 | |

| DEFINT | 129 | 2.904 | 1.551 | 0.543 | 1.869 | 2.506 | 3.975 | 5.862 | |

| Growth | ASSGRW | 127 | 0.035 | 0.093 | −0.107 | 0.001 | 0.031 | 0.078 | 0.165 |

| REVGRW | 127 | 0.068 | 0.311 | −0.230 | −0.044 | 0.037 | 0.112 | 0.270 | |

| TANGRW | 127 | 0.068 | 0.431 | −0.248 | −0.044 | 0.012 | 0.075 | 0.426 | |

| Stability | LIAB | 129 | 1.186 | 1.404 | 0.169 | 0.438 | 0.904 | 1.338 | 3.976 |

| DEBT | 128 | 0.492 | 0.837 | 0.013 | 0.119 | 0.306 | 0.553 | 1.152 | |

| COD | 129 | 0.036 | 0.028 | 0.007 | 0.026 | 0.032 | 0.042 | 0.066 | |

| Activity | ASSTOV | 129 | 0.819 | 0.538 | 0.110 | 0.470 | 0.700 | 1.130 | 1.870 |

| WCTOV | 129 | 5.250 | 34.698 | −26.070 | −2.550 | 3.660 | 8.400 | 66.370 | |

| TANTOV | 129 | 18.967 | 87.034 | 0.710 | 1.620 | 3.400 | 5.560 | 96.130 | |

| Firm Value | PER | 83 | 32.149 | 46.540 | 5.260 | 10.586 | 15.029 | 25.609 | 158.784 |

| PBR | 104 | 1.738 | 1.961 | 0.466 | 0.799 | 1.307 | 1.774 | 7.122 | |

| TQ | 104 | 1.423 | 1.159 | 0.757 | 0.908 | 1.106 | 1.328 | 3.914 | |

| Perspective | A. Financial | B. Customer | C. Internal Process | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Variable | Mean | Diff | t-Value | Mean | Diff | t-Value | Mean | Diff | t-Value | ||||

| High | Low | High | Low | High | Low | ||||||||

| Profitable | ROAt | 0.042 | 0.043 | −0.001 | −0.07 | 0.051 | 0.035 | 0.017 | 2.00 ** | 0.044 | 0.042 | 0.002 | 0.18 |

| ROEt | 0.072 | 0.078 | −0.006 | −0.31 | 0.095 | 0.056 | 0.039 | 2.02 ** | 0.075 | 0.075 | 0.000 | 0.00 | |

| CFOt | 0.067 | 0.073 | −0.006 | −0.48 | 0.081 | 0.059 | 0.022 | 1.70 * | 0.066 | 0.074 | −0.007 | −0.54 | |

| Liquidity | CURt | 1.427 | 3.210 | −1.783 | −1.92 * | 2.939 | 1.722 | 1.217 | 1.28 | 2.691 | 1.966 | 0.726 | 0.76 |

| QUICKt | 1.166 | 2.800 | −1.633 | −2.00 ** | 2.514 | 1.473 | 1.040 | 1.25 | 2.231 | 1.752 | 0.479 | 0.57 | |

| DEFINTt | 2.780 | 3.026 | −0.247 | −0.90 | 3.220 | 2.582 | 0.638 | 2.36 ** | 3.070 | 2.740 | 0.330 | 1.20 | |

| Growth | ASSGRWt | 0.038 | 0.032 | 0.006 | 0.38 | 0.037 | 0.033 | 0.004 | 0.25 | 0.025 | 0.044 | −0.019 | −1.14 |

| REVGRWt | 0.054 | 0.083 | −0.029 | −0.53 | 0.075 | 0.062 | 0.014 | 0.25 | 0.097 | 0.040 | 0.057 | 1.02 | |

| TANGRWt | 0.037 | 0.099 | −0.062 | −0.82 | 0.077 | 0.059 | 0.018 | 0.23 | −0.017 | 0.152 | −0.169 | −2.25 ** | |

| Stability | LEVt | 1.260 | 1.114 | 0.145 | 0.58 | 1.398 | 0.978 | 0.420 | 1.70 * | 1.302 | 1.073 | 0.229 | 0.92 |

| BORRt | 0.506 | 0.479 | 0.027 | 0.18 | 0.275 | 0.224 | 0.051 | 1.91 * | 0.520 | 0.465 | 0.055 | 0.37 | |

| CODt | 0.037 | 0.036 | 0.001 | 0.14 | 0.043 | 0.031 | 0.012 | 2.08 ** | 0.041 | 0.032 | 0.009 | 1.70 * | |

| Activity | ASSTOVt | 0.838 | 0.801 | 0.038 | 0.40 | 0.971 | 0.670 | 0.301 | 3.28 *** | 0.884 | 0.756 | 0.128 | 1.36 |

| WCTOVt | 9.602 | 0.964 | 8.638 | 1.42 | 10.212 | 0.364 | 9.849 | 1.62 | 6.275 | 4.240 | 2.035 | 0.33 | |

| TANTOVt | 10.525 | 27.278 | −16.754 | −1.10 | 31.118 | 7.002 | 24.117 | 1.57 | 22.275 | 15.709 | 6.565 | 0.42 | |

| Firm Value | PERt | 29.448 | 35.507 | −6.059 | −0.59 | 30.939 | 33.450 | −2.511 | −0.24 | 32.203 | 32.094 | 0.109 | 0.01 |

| PBRt | 1.483 | 2.035 | −0.552 | −1.40 | 2.254 | 1.222 | 1.032 | 2.77 *** | 1.811 | 1.668 | 0.143 | 0.37 | |

| TQt | 1.204 | 1.679 | −0.475 | −2.01 ** | 1.702 | 1.144 | 0.557 | 2.51 ** | 1.511 | 1.339 | 0.172 | 0.75 | |

| Perspective | D. Learning and Growth | E. CSR | F. Business Environment | ||||||||||

| Variable | Mean | Diff | t-Value | Mean | Diff | t-Value | Mean | Diff | t-Value | ||||

| High | Low | High | Low | High | Low | ||||||||

| Profitable | ROAt | 0.046 | 0.040 | 0.006 | 0.74 | 0.044 | 0.041 | 0.003 | 0.31 | 0.042 | 0.044 | −0.002 | −0.21 |

| ROEt | 0.075 | 0.075 | 0.001 | 0.03 | 0.078 | 0.072 | 0.006 | 0.29 | 0.075 | 0.075 | −0.001 | −0.04 | |

| CFOt | 0.076 | 0.065 | 0.011 | 0.84 | 0.070 | 0.070 | 0.000 | −0.02 | 0.066 | 0.074 | −0.007 | −0.55 | |

| Liquidity | CURt | 1.581 | 3.058 | −1.477 | −1.59 | 2.736 | 1.922 | 0.814 | 0.86 | 2.628 | 2.028 | 0.601 | 0.63 |

| QUICKt | 1.329 | 2.639 | −1.310 | −1.60 | 2.289 | 1.695 | 0.594 | 0.71 | 2.189 | 1.792 | 0.397 | 0.47 | |

| DEFINTt | 3.130 | 2.681 | 0.449 | 1.64 | 2.991 | 2.818 | 0.174 | 0.63 | 3.151 | 2.653 | 0.499 | 1.63 | |

| Growth | ASSGRWt | 0.044 | 0.026 | 0.018 | 1.10 | 0.034 | 0.035 | −0.001 | −0.05 | 0.038 | 0.031 | 0.007 | 0.42 |

| REVGRWt | 0.072 | 0.065 | 0.007 | 0.13 | 0.103 | 0.034 | 0.069 | 1.25 | 0.046 | 0.091 | −0.046 | −0.82 | |

| TANGRWt | 0.078 | 0.059 | 0.019 | 0.25 | 0.054 | 0.083 | −0.029 | −0.38 | 0.086 | 0.051 | 0.035 | 0.45 | |

| Stability | LEVt | 1.218 | 1.156 | 0.062 | 0.25 | 1.130 | 1.243 | −0.113 | −0.46 | 1.165 | 1.207 | −0.042 | −0.17 |

| BORRt | 0.507 | 0.478 | 0.029 | 0.20 | 0.490 | 0.494 | −0.004 | −0.02 | 0.541 | 0.444 | 0.097 | 0.66 | |

| CODt | 0.035 | 0.037 | −0.002 | −0.43 | 0.036 | 0.037 | −0.001 | −0.09 | 0.033 | 0.040 | −0.007 | −1.24 | |

| Activity | ASSTOVt | 0.896 | 0.744 | 0.152 | 1.61 | 0.827 | 0.812 | 0.015 | 0.16 | 0.796 | 0.843 | −0.047 | −0.49 |

| ICTOVt | 5.305 | 5.195 | 0.110 | 0.02 | 4.805 | 5.688 | −0.883 | −0.14 | 7.188 | 3.341 | 3.847 | 0.62 | |

| TANTOVt | 8.916 | 28.863 | −19.947 | −1.31 | 26.419 | 11.629 | 14.790 | 0.96 | 10.490 | 27.313 | −16.823 | −1.11 | |

| Firm Value | PERt | 24.898 | 38.894 | −13.997 | −1.40 | 31.335 | 32.943 | −1.608 | −0.16 | 42.561 | 21.985 | 20.577 | 2.04 ** |

| PBRt | 1.821 | 1.648 | 0.173 | 0.45 | 1.563 | 1.894 | −0.332 | −0.86 | 2.179 | 1.330 | 0.848 | 2.19 ** | |

| TQt | 1.341 | 1.511 | −0.170 | −0.73 | 1.448 | 1.401 | 0.047 | 0.21 | 1.718 | 1.149 | 0.569 | 2.49 ** | |

| Perspective | A. Financial | B. Customer | C. Internal Process | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Variable | Mean | Diff | t-Value | Mean | Diff | t-Value | Mean | Diff | t-Value | ||||

| High | Low | High | Low | High | Low | ||||||||

| Profitable | ΔROAt+1 | −0.004 | −0.004 | 0.000 | 0.05 | −0.006 | −0.002 | −0.003 | −0.52 | −0.009 | 0.001 | −0.010 | −1.52 |

| ΔROEt+1 | −0.002 | −0.021 | 0.019 | 0.82 | −0.018 | −0.005 | −0.014 | −0.60 | −0.018 | −0.005 | −0.013 | −0.58 | |

| ΔCFOt+1 | −0.007 | −0.009 | 0.002 | 0.10 | −0.010 | −0.005 | −0.004 | −0.21 | −0.013 | −0.002 | −0.012 | −0.56 | |

| Liquidity | ΔCURt+1 | 0.010 | −0.026 | 0.036 | 0.17 | −0.026 | 0.009 | −0.035 | −0.16 | 0.182 | −0.196 | 0.378 | 1.82 * |

| ΔQUICKt+1 | −0.008 | −0.050 | 0.041 | 0.20 | −0.052 | −0.007 | −0.045 | −0.21 | 0.159 | −0.214 | 0.374 | 1.80 * | |

| ΔDEFINTt+1 | −0.024 | −0.011 | −0.014 | −0.23 | −0.028 | −0.007 | −0.021 | −0.35 | 0.037 | −0.071 | 0.107 | 1.80 * | |

| Growth | ΔASSGRWt+1 | −0.007 | 0.005 | −0.012 | −0.51 | −0.014 | 0.013 | −0.027 | −1.13 | −0.011 | 0.009 | −0.021 | −0.86 |

| ΔREVGRWt+1 | 0.012 | −0.054 | 0.066 | 0.98 | −0.053 | 0.011 | −0.064 | −0.95 | −0.062 | 0.019 | −0.081 | −1.20 | |

| ΔTANGRWt+1 | 0.008 | −0.081 | 0.089 | 1.07 | −0.056 | −0.017 | −0.040 | −0.48 | 0.015 | −0.088 | 0.103 | 1.24 | |

| Stability | ΔLEVt+1 | −0.113 | −0.031 | −0.082 | −0.60 | −0.160 | 0.015 | −0.175 | −1.28 | −0.165 | 0.020 | −0.184 | −1.35 |

| ΔBORRt+1 | −0.048 | −0.006 | −0.042 | −0.59 | −0.058 | 0.004 | −0.062 | −0.87 | −0.061 | 0.007 | −0.069 | −0.96 | |

| ΔCODt+1 | 0.000 | 0.001 | −0.002 | −0.08 | −0.004 | 0.005 | −0.008 | −0.47 | 0.008 | −0.007 | 0.015 | 0.83 | |

| Activity | ΔASSTOVt+1 | 0.019 | 0.001 | 0.018 | 0.75 | −0.007 | 0.027 | −0.034 | −1.41 | 0.000 | 0.019 | −0.019 | −0.80 |

| ΔWCTOVt+1 | −7.935 | −14.609 | 6.674 | 0.72 | −13.439 | −9.189 | −4.251 | −0.46 | −8.366 | −14.184 | 5.818 | 0.63 | |

| ΔTANTOVt+1 | 0.639 | 10.069 | −9.430 | −0.70 | 10.278 | 0.578 | 9.700 | 0.71 | 11.793 | −0.914 | 12.707 | 0.94 | |

| Firm Value | ΔPERt+1 | 0.494 | −4.515 | 5.009 | 0.56 | 1.316 | −4.677 | 5.993 | 0.60 | −5.617 | 2.054 | −7.672 | −0.78 |

| ΔPBRt+1 | 0.053 | −0.178 | 0.230 | 1.50 | −0.128 | 0.021 | −0.149 | −0.97 | −0.091 | −0.018 | −0.073 | −0.47 | |

| ΔTQt+1 | 0.028 | −0.138 | 0.166 | 1.70 * | −0.104 | 0.006 | −0.109 | −1.14 | −0.020 | −0.077 | 0.057 | 0.58 | |

| Perspective | D. Learning and Growth | E. CSR | F. Business Environment | ||||||||||

| Variable | Mean | Diff | t-Value | Mean | Diff | t-Value | Mean | Diff | t-Value | ||||

| High | Low | High | Low | High | Low | ||||||||

| Profitable | ΔROAt+1 | −0.002 | −0.006 | 0.004 | 0.65 | −0.012 | 0.004 | −0.016 | −2.53 ** | −0.004 | −0.004 | −0.001 | −0.14 |

| ΔROEt+1 | 0.005 | −0.028 | 0.033 | 1.44 | −0.034 | 0.011 | −0.046 | −2.03 ** | −0.013 | −0.010 | −0.004 | −0.16 | |

| ΔCFOt+1 | −0.004 | −0.012 | 0.008 | 0.39 | −0.017 | 0.002 | −0.019 | −0.90 | −0.015 | 0.000 | −0.015 | −0.72 | |

| Liquidity | ΔCURt+1 | 0.024 | −0.040 | 0.065 | 0.31 | 0.171 | −0.184 | 0.355 | 1.70 * | 0.122 | −0.137 | 0.259 | 1.24 |

| ΔQUICKt+1 | 0.007 | −0.065 | 0.072 | 0.34 | 0.154 | −0.210 | 0.364 | 1.75 * | 0.099 | −0.155 | 0.253 | 1.21 | |

| ΔDEFINTt+1 | −0.002 | −0.033 | 0.031 | 0.52 | 0.031 | −0.065 | 0.096 | 1.61 | 0.019 | −0.053 | 0.073 | 1.21 | |

| Growth | ΔASSGRWt+1 | 0.015 | −0.016 | 0.031 | 1.29 | −0.001 | 0.000 | −0.001 | −0.04 | 0.008 | −0.010 | 0.018 | 0.76 |

| ΔREVGRWt+1 | −0.007 | −0.036 | 0.028 | 0.42 | −0.062 | 0.019 | −0.081 | −1.20 | 0.017 | −0.060 | 0.077 | 1.13 | |

| ΔTANGRWt+1 | −0.034 | −0.040 | 0.006 | 0.07 | −0.061 | −0.012 | −0.049 | −0.59 | −0.043 | −0.031 | −0.012 | −0.15 | |

| Stability | ΔLEVt+1 | −0.112 | −0.033 | −0.079 | −0.58 | −0.023 | −0.120 | 0.098 | 0.72 | 0.035 | −0.177 | 0.211 | 1.57 |

| ΔBORRt+1 | −0.056 | 0.002 | −0.058 | −0.81 | 0.009 | −0.061 | 0.069 | 0.99 | 0.015 | −0.067 | 0.081 | 1.17 | |

| ΔCODt+1 | −0.004 | 0.004 | −0.008 | −0.43 | 0.002 | −0.001 | 0.003 | 0.14 | 0.007 | −0.006 | 0.013 | 0.74 | |

| Activity | ΔASSTOVt+1 | −0.005 | 0.025 | −0.030 | −1.24 | −0.006 | 0.026 | −0.032 | −1.34 | 0.016 | 0.004 | 0.012 | 0.49 |

| ΔWCTOVt+1 | −11.687 | −10.914 | −0.774 | −0.08 | −12.545 | −10.069 | −2.475 | −0.27 | −14.859 | −7.791 | −7.068 | −0.76 | |

| ΔTANTOVt+1 | 0.424 | 10.281 | −9.857 | −0.74 | 12.050 | −1.167 | 13.218 | 0.97 | 0.364 | 10.339 | −9.975 | −0.75 | |

| Firm Value | ΔPERt+1 | 7.414 | −9.866 | 17.280 | 1.73 * | −2.372 | −1.025 | −1.347 | −0.14 | −0.053 | −3.397 | 3.344 | 0.34 |

| ΔPBRt+1 | 0.110 | −0.230 | 0.340 | 2.25 ** | −0.025 | −0.079 | 0.054 | 0.35 | −0.060 | −0.048 | −0.013 | −0.08 | |

| ΔTQt+1 | 0.065 | −0.172 | 0.237 | 2.50 ** | −0.090 | −0.012 | −0.078 | −0.80 | −0.066 | −0.034 | −0.032 | −0.33 | |

| Panel A. Regression Results Using Profit Indicators as Dependent Variables | ||||||

|---|---|---|---|---|---|---|

| Variable | Dep = ROA | Dep = ROE | Dep = CFO | |||

| β | t-Value | β | t-Value | β | t-Value | |

| Intercept | 0.017 | 0.119 | −0.125 | −0.363 | −0.325 | −1.379 |

| FIN | 0.303 | 0.490 | 0.248 | 0.170 | 0.229 | 0.229 |

| CUS | 2.158 | 2.699 *** | 3.698 | 1.958 * | 3.737 | 2.896 *** |

| INP | −0.443 | −0.393 | −1.785 | −0.670 | −2.973 | −1.634 |

| LNG | 0.146 | 0.129 | −0.999 | −0.373 | 1.643 | 0.897 |

| CSR | −0.288 | −0.383 | −0.677 | −0.381 | 0.575 | 0.474 |

| ENV | −0.558 | −0.464 | 0.531 | 0.187 | 0.005 | 0.003 |

| CUR | 0.000 | 0.458 | 0.001 | 0.337 | −0.001 | −0.844 |

| ASSGRW | 0.183 | 4.364 *** | 0.342 | 3.459 *** | 0.271 | 4.009 *** |

| LEV | −0.012 | −4.303 *** | −0.025 | −3.774 *** | −0.008 | −1.733 * |

| ASSTOV | 0.018 | 2.358 ** | 0.071 | 3.994 *** | 0.008 | 0.644 |

| SIZE | 0.001 | 0.142 | 0.008 | 0.611 | 0.010 | 1.170 |

| PPE | 0.035 | 1.500 | 0.069 | 1.260 | 0.112 | 3.000 *** |

| AGE | −0.006 | −0.980 | −0.022 | −1.581 | 0.018 | 1.890 * |

| Fixed Effect | Included | Included | Included | |||

| Fvalue | 5.231 *** | 4.671 *** | 4.518 *** | |||

| Adj_Rsq | 0.320 | 0.290 | 0.281 | |||

| N_obs | 127 | 127 | 127 | |||

| Panel B. Regression Results Using Liquidity Indicators as Dependent Variables | ||||||

| Variable | Dep = CUR | Dep = QUICK | Dep = DEFINT | |||

| β | t-Value | β | t-Value | β | t-Value | |

| Intercept | 39.079 | 2.300** | 39.215 | 2.651 *** | 4.796 | 1.090 |

| FIN | −28.966 | −0.393 | −32.743 | −0.510 | 1.627 | 0.085 |

| CUS | 147.602 | 1.516 | 138.553 | 1.634 | 58.880 | 2.335 ** |

| INP | 39.594 | 0.294 | 34.150 | 0.292 | 1.527 | 0.044 |

| LNG | −77.119 | −0.571 | −67.952 | −0.578 | −26.144 | −0.747 |

| CSR | 384.244 | 4.687 *** | 327.914 | 4.593 *** | 96.823 | 4.561 *** |

| ENV | −93.003 | −0.650 | −88.787 | −0.712 | −14.383 | −0.388 |

| ROA | 5.155 | 0.458 | 4.669 | 0.477 | 0.085 | 0.029 |

| ASSGRW | −3.473 | −0.644 | −3.045 | −0.648 | −0.137 | −0.098 |

| LEV | −0.382 | −1.072 | −0.304 | −0.981 | −0.104 | −1.127 |

| ASSTOV | −2.525 | −2.851 *** | −2.306 | −2.990 *** | −0.639 | −2.788 *** |

| SIZE | −1.393 | −2.237 ** | −1.394 | −2.572 ** | −0.173 | −1.071 |

| PPE | −4.017 | −1.463 | −3.978 | −1.664 * | −1.324 | −1.862 * |

| AGE | 0.862 | 1.211 | 0.758 | 1.222 | 0.192 | 1.043 |

| Fixed Effect | Included | Included | Included | |||

| Fvalue | 3.972 *** | 4.239 *** | 3.824 *** | |||

| Adj_Rsq | 0.248 | 0.265 | 0.239 | |||

| N_obs | 127 | 127 | 127 | |||

| Panel C. Regression Results Using Growth Indicators as Dependent Variables | ||||||

| Variable | Dep = ASSGRW | Dep = REVGRW | Dep = TANGRW | |||

| β | t-Value | β | t-Value | β | t-Value | |

| Intercept | 0.814 | 2.767 *** | −0.656 | −0.617 | 4.066 | 2.663 *** |

| FIN | −0.428 | −0.332 | −3.973 | −0.853 | −1.564 | −0.234 |

| CUS | −1.858 | −1.086 | −6.512 | −1.054 | 5.223 | 0.588 |

| INP | −1.582 | −0.674 | 9.367 | 1.105 | −6.782 | −0.556 |

| LNG | 1.624 | 0.688 | −7.731 | −0.907 | 10.484 | 0.856 |

| CSR | 0.950 | 0.607 | 4.760 | 0.842 | −8.432 | −1.038 |

| ENV | 0.208 | 0.083 | −8.264 | −0.912 | 7.254 | 0.557 |

| ROA | 0.795 | 4.364 *** | 1.465 | 2.228 ** | −0.499 | −0.528 |

| CUR | −0.001 | −0.644 | 0.002 | 0.407 | 0.005 | 0.550 |

| LEV | −0.003 | −0.511 | 0.034 | 1.503 | −0.033 | −1.023 |

| ASSTOV | 0.008 | 0.512 | 0.084 | 1.458 | −0.004 | −0.049 |

| SIZE | −0.032 | −3.025 *** | 0.039 | 1.002 | −0.155 | −2.797 *** |

| PPE | 0.082 | 1.715 * | −0.294 | −1.700 * | 0.123 | 0.494 |

| AGE | 0.022 | 1.763 * | −0.111 | −2.487 ** | 0.091 | 1.410 |

| Fixed Effect | Included | Included | Included | |||

| Fvalue | 3.568 *** | 1.975 ** | 1.251 | |||

| Adj_Rsq | 0.222 | 0.098 | 0.027 | |||

| N_obs | 127 | 127 | 127 | |||

| Panel D. Regression Results Using Stability Indicators as Dependent Variables | ||||||

| Variable | Dep = LIAB | Dep = DEBT | Dep = COD | |||

| β | t-Value | β | t-Value | β | t-Value | |

| Intercept | 0.374 | 0.081 | −1.141 | −0.405 | −0.012 | −0.121 |

| FIN | 49.440 | 2.612 ** | 22.895 | 1.971 * | −0.341 | −0.866 |

| CUS | 71.648 | 2.856 *** | 43.703 | 2.838 *** | −0.569 | −1.089 |

| INP | −34.797 | −0.983 | −26.028 | −1.198 | 1.056 | 1.434 |

| LNG | −30.486 | −0.856 | −13.070 | −0.598 | −0.755 | −1.018 |

| CSR | 0.967 | 0.041 | −3.038 | −0.209 | 0.048 | 0.098 |

| ENV | 6.493 | 0.171 | 22.281 | 0.958 | −1.048 | −1.328 |

| ROA | −11.861 | −4.303 *** | −6.118 | −3.617 *** | −0.023 | −0.400 |

| CUR | −0.027 | −1.072 | −0.014 | −0.918 | −0.001 | −1.332 |

| ASSGRW | −0.728 | −0.511 | 0.219 | 0.250 | −0.032 | −1.076 |

| ASSTOV | 0.582 | 2.465 ** | −0.062 | −0.428 | 0.009 | 1.858 * |

| SIZE | 0.027 | 0.163 | 0.046 | 0.448 | 0.002 | 0.511 |

| PPE | 1.180 | 1.631 | 1.199 | 2.699 *** | −0.002 | −0.101 |

| AGE | −0.120 | −0.635 | 0.055 | 0.475 | −0.002 | −0.385 |

| Fixed Effect | Included | Included | Included | |||

| Fvalue | 3.759 *** | 3.048 *** | 1.532 | |||

| Adj_Rsq | 0.235 | 0.185 | 0.056 | |||

| N_obs | 127 | 127 | 127 | |||

| Panel E. Regression Results Using Activity Indicators as Dependent Variables | ||||||

| Variable | Dep = ASSTOV | Dep = ICTOV | Dep = TANTOV | |||

| β | t-Value | β | t-Value | β | t-Value | |

| Intercept | 1.044 | 0.584 | −61.027 | −0.468 | 994.209 | 3.590 *** |

| FIN | −6.904 | −0.911 | 692.168 | 1.254 | −1374.822 | −1.172 |

| CUS | 11.995 | 1.191 | 504.671 | 0.688 | 2266.819 | 1.454 |

| INP | 26.356 | 1.933 * | −160.751 | −0.162 | 2690.233 | 1.274 |

| LNG | −5.807 | −0.417 | −1016.446 | −1.002 | −4632.724 | −2.148 ** |

| CSR | 8.366 | 0.909 | −181.882 | −0.271 | 1832.026 | 1.286 |

| ENV | −28.370 | −1.953 * | 1067.116 | 1.008 | −4547.355 | −2.021 ** |

| ROA | 2.671 | 2.358 ** | 24.482 | 0.297 | −230.221 | −1.313 |

| CUR | −0.027 | −2.851 *** | 0.227 | 0.331 | −1.205 | −0.828 |

| LEV | 0.285 | 0.512 | 56.636 | 1.398 | −211.924 | −2.461 ** |

| ASSGRW | 0.089 | 2.465 ** | 2.872 | 1.099 | 5.576 | 1.003 |

| SIZE | 0.003 | 0.049 | 3.512 | 0.735 | −27.922 | −2.751 *** |

| PPE | −0.344 | −1.213 | −25.565 | −1.237 | −55.280 | −1.258 |

| AGE | −0.137 | −1.878 * | −11.379 | −2.149 ** | −42.519 | −3.778 *** |

| Fixed Effect | Included | Included | Included | |||

| Fvalue | 3.037 *** | 0.848 | 4.415 *** | |||

| Adj_Rsq | 0.185 | -0.017 | 0.275 | |||

| N_obs | 127 | 127 | 127 | |||

| Panel F. Regression Results Using Value Indicators as Dependent Variables | ||||||

| Variable | Dep = PER | Dep = PBR | Dep = TQ | |||

| β | t-Value | β | t-Value | β | t-Value | |

| Intercept | 0.074 | 0.001 | −4.975 | −0.966 | 1.127 | 0.414 |

| FIN | −224.787 | −0.761 | 0.287 | 0.021 | 0.961 | 0.136 |

| CUS | −92.020 | −0.252 | 30.324 | 1.620 | 6.893 | 0.696 |

| INP | −286.696 | −0.582 | −40.111 | −1.628 * | −23.041 | −1.769 * |

| LNG | −380.267 | −0.747 | 30.620 | 1.220 | 3.360 | 0.253 |

| CSR | 194.037 | 0.582 | −20.595 | −1.189 | −2.302 | −0.251 |

| ENV | 1015.298 | 1.791 * | 77.497 | 2.732 *** | 44.332 | 2.955 *** |

| ROA | −168.145 | −3.831 *** | 6.318 | 2.931 *** | 6.504 | 5.706 *** |

| CUR | 0.419 | 1.335 | 0.078 | 4.648 *** | 0.039 | 4.425 *** |

| LEV | 32.459 | 1.436 | 1.394 | 1.337 | 0.050 | 0.090 |

| ASSGRW | −2.114 | −0.808 | 0.092 | 1.451 | 0.028 | 0.833 |

| ASSTOV | −1.926 | −0.529 | 0.182 | 0.979 | 0.010 | 0.098 |

| SIZE | 1.655 | 0.392 | 0.237 | 1.282 | 0.010 | 0.098 |

| PPE | −17.678 | −1.537 | −1.003 | −1.719 * | −0.487 | −1.577 |

| AGE | −3.625 | −1.304 | −0.326 | −2.267 ** | −0.160 | −2.107 ** |

| Fixed Effect | Included | Included | Included | |||

| Fvalue | 2.610 *** | 5.087 *** | 6.998 *** | |||

| Adj_Rsq | 0.230 | 0.375 | 0.469 | |||

| N_obs | 82 | 103 | 103 | |||

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Na, H.J.; Lee, K.C.; Choi, S.U.; Kim, S.T. Exploring CEO Messages in Sustainability Management Reports: Applying Sentiment Mining and Sustainability Balanced Scorecard Methods. Sustainability 2020, 12, 590. https://doi.org/10.3390/su12020590

Na HJ, Lee KC, Choi SU, Kim ST. Exploring CEO Messages in Sustainability Management Reports: Applying Sentiment Mining and Sustainability Balanced Scorecard Methods. Sustainability. 2020; 12(2):590. https://doi.org/10.3390/su12020590

Chicago/Turabian StyleNa, Hyung Jong, Kun Chang Lee, Seung Uk Choi, and Seong Tae Kim. 2020. "Exploring CEO Messages in Sustainability Management Reports: Applying Sentiment Mining and Sustainability Balanced Scorecard Methods" Sustainability 12, no. 2: 590. https://doi.org/10.3390/su12020590

APA StyleNa, H. J., Lee, K. C., Choi, S. U., & Kim, S. T. (2020). Exploring CEO Messages in Sustainability Management Reports: Applying Sentiment Mining and Sustainability Balanced Scorecard Methods. Sustainability, 12(2), 590. https://doi.org/10.3390/su12020590