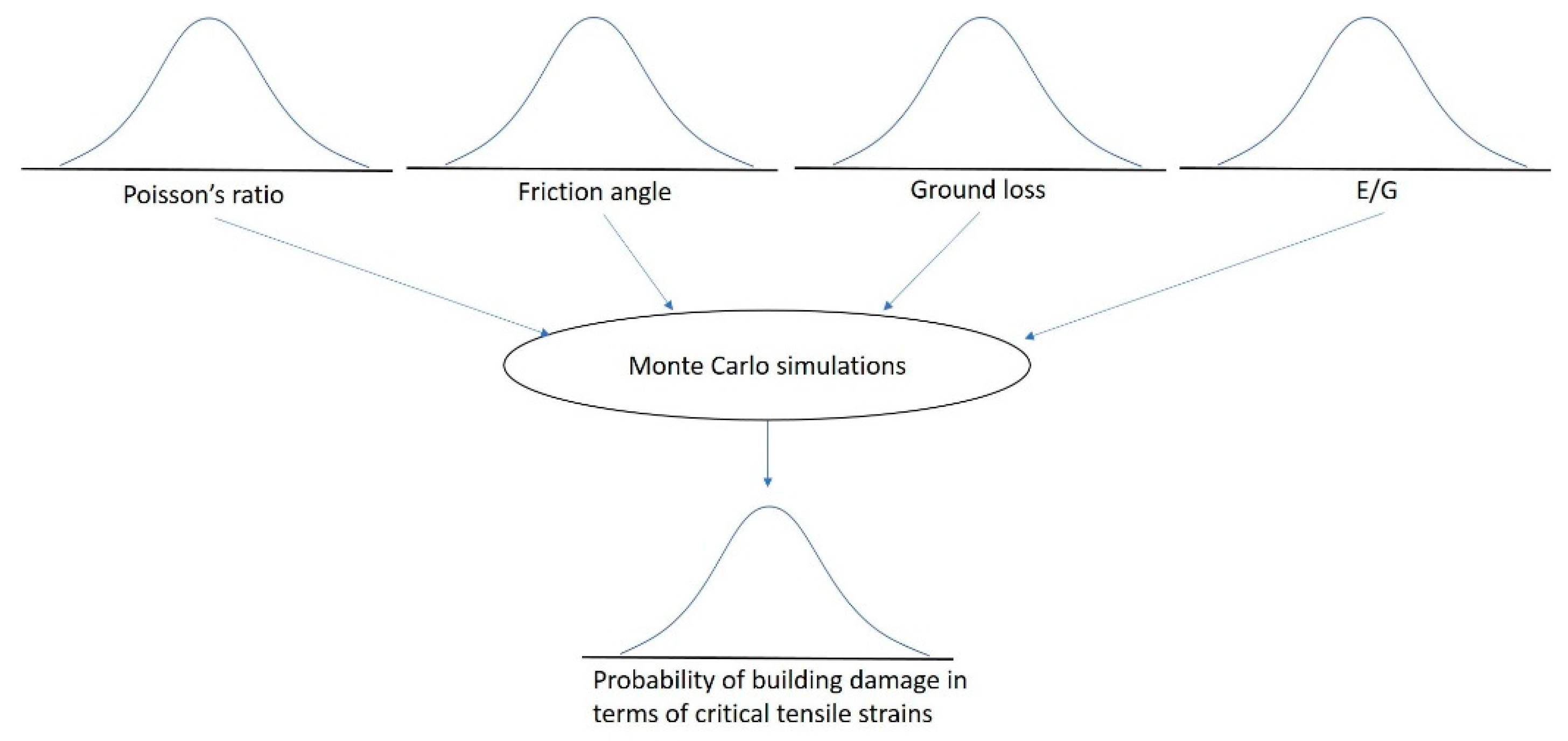

In the case of a model including several inputs with uncertainties, a stochastic analysis could be used to provide subsequent uncertainty evaluations, i.e., how the input uncertainty has an impact on the characteristics of the model [

26]. Monte Carlo simulation is a type of stochastic modeling where the output probability distribution is derived from a repeat of random-sampling tests of inputs [

23]. A large number of simulations ensures that a random variation of the inputs is reflected [

57]. In the present analysis, using the Monte Carlo simulations, uncertainties of the geotechnical factors used in Equation (2) or of the

E/

G factor in Equation (6) have an impact on each other. The concept of the Monte Carlo analysis used is presented in

Figure 5. The damage of the buildings in the proposed analysis is a function of the critical tensile strain

εcrit using

Table 3. The key points of the Monte Carlo simulations used in the proposed methodology are:

2.3.2. Building Damage Cost Analysis Using Probability Density Functions

As previously mentioned, in the settlement-induced building-damage scheme used in this case, the critical tensile strain (

εcrit) levels are related to this damage. Minor critical strains are associated with negligible damage and small repair-costs, whereas larger critical strains affect the function or the main structure of a building resulting in substantial damage and costs. The consequences of this damage are described by a continuous function providing the settlement economic risk (Rs) for each building, as presented in Equation (7) [

14].

where

Rs is the settlement economic risk due to tunneling given by a combination of the economic cost,

Cs, induced by the settlement and the probability density function (PDF) of damage occurring,

fs.

The settlement economic risk,

Rs, is initially calculated for each building. The sum of

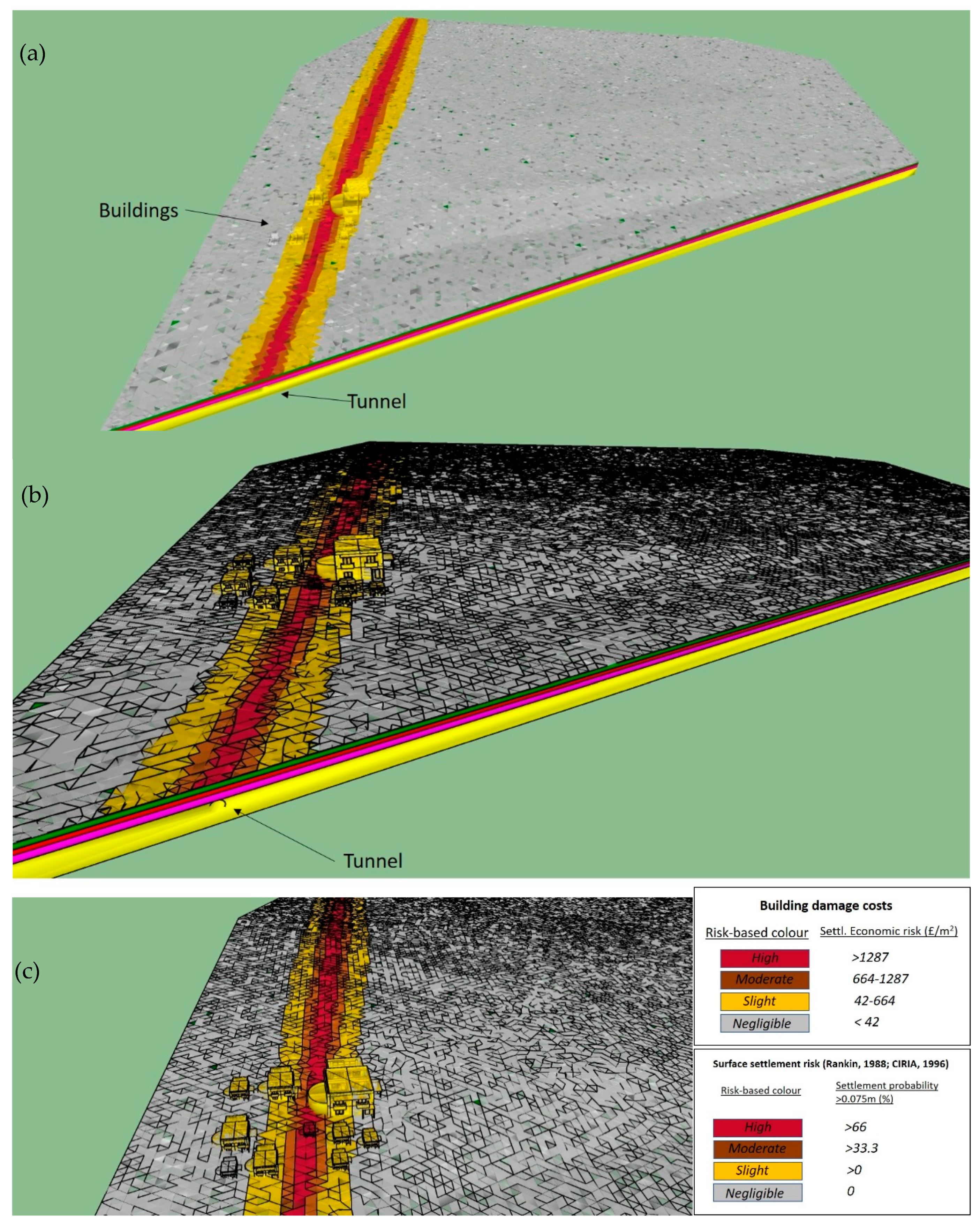

Rs for all buildings included in the investigated urban area gives the total economic risk for a specific settlement hazard for this urban area. The economic costs (

Cs) are made up of direct costs (i.e., costs of repairing of settlement damage) and indirect costs (e.g., related to project delay, a reduced market value of damaged buildings and tenant issues) [

14]. Only the direct costs are accounted for here to illustrate the approach. Due to the fact that no rigorous related damage database exists for the UK, the economic cost valuation in the proposed method was based on earlier research and not directly related to tunneling-induced settlement damage. Hence, the proposed methodology employed the “damage index” adopted by Blong [

16] that enables the damage evaluation due to any hazard and any type of building to be determined. This was used to estimate the settlement damage in terms of complete replacement costs for any investigated building or building at risk. This is expressed in units of average gross charge (cost) for a new property (house) in meter squared of floor area. The average gross charge for new construction in England and Wales in the year 2016 was 2400 £/m

2, while the highest reasonable gross charge reached 6600 £/m

2 in the wider London area [

15]. The average property area in England and Wales in the year 2016 was 90.1 m

2 [

15].

To estimate the damage costs from a particular hazard, the full scale of potential values from 0 to 1 corresponds to the complete range of the observed damage, i.e., from no damage to the total collapse of the building. Blong [

16], after reviewing studies of damage caused by natural hazards, identified five alternative damage categories: light, moderate, heavy, severe and collapse, with a qualitative description provided for the nature of this damage. A summary of the categories used in that study is presented in

Table 5, adapted from Blong [

16]. Each damage category has a corresponding range of damage-values, where for estimation purposes, Blong [

16] has taken the central value and called this the “central damage value” (CDV) (

Table 5).

In the current approach, the five damage categories after Blong [

16] are correlated with the building damage categories (No 1–5) based on the critical strains of

Table 3 [

12,

41], caused by the tunneling-induced settlements generated within the building footprints. Subsequently, the cost of the settlement damage for each of the five damage categories is estimated from Equation (8).

Considering Equation (8) and

Table 5, the average damage cost per m

2 (gross) floor area is estimated for each corresponding damage category as presented in

Table 6. Due to the fact that probability density functions (PDFs) are not directly defined by a number, the highest reasonable damage cost for a respective category is estimated in combination with the expertise of the authors in this field. The resulting highest value would then represent the 95% percentile in the respective category. The values of the 95% percentile cost per m

2 floor area for each damage category are also summarized in

Table 6. To obtain these values, the prices used were adapted using the study of Sundell et al. [

14] combined with the expertise of the authors, in addition to the highest gross charge (cost) in the wider London area taken from the Office for National Statistics [

15]. It is important to note that the intention here is to demonstrate how the method works rather than providing exact values for these costs, which will be dependent on the particular costs associated with a country/region or city.

Damage from various hazards often follows a skewed probability distribution [

58]. The log-normal distribution is commonly employed to analyze the positively skewed damage distributions of PDF [

58]. By definition, a PDF of damage is “lognormally” distributed when the log-transformed PDF of the damage is normally distributed. This can be described as a function: Y = ln(X) that is normally distributed with a mean,

μ, and a variance,

σ2. Then, X is lognormally distributed with parameters, mean (

μ), and variance (

σ2). It should be noted that

μ and

σ2 are not the mean and variance of the log-normal random variable, X, but are the mean and variance of the log-transformed random variable, Y and the log-normal distribution is commonly referred to as

LN(μ, σ2). The log-normal PDF was selected in the present methodology to provide positive (damage) costs,

Cs, and represent larger uncertainties in the correct part of the curve [

58]. If the average cost per m

2 is the expected value

m and the 95% percentile is the variable

q for each damage category, the Equations (9)–(12) can be employed to evaluate the parameters

μ, and variance, σ

2, of the log-normal PDF for damage cost,

Cs, for each damage category [

59]. The value from the log-normal distribution,

m, and the 95% percentile,

q, is given by Equations (9) and (10), respectively [

59]:

where

z0.95 is the 95% percentile of the standard normal distribution profile (approximately equal to 1.645). Then, taking the logarithms of

m and

q, are represented by Equations (11) and (12) [

59]:

From Equations (9)–(12), the Equations (13) and (14) [

59] are obtained:

The equation with the positive solution for σ and μ is selected (unless

q >

m).

Table 7 shows the resulting mean (

μ) and variance (σ

2) for the log-normal PDF,

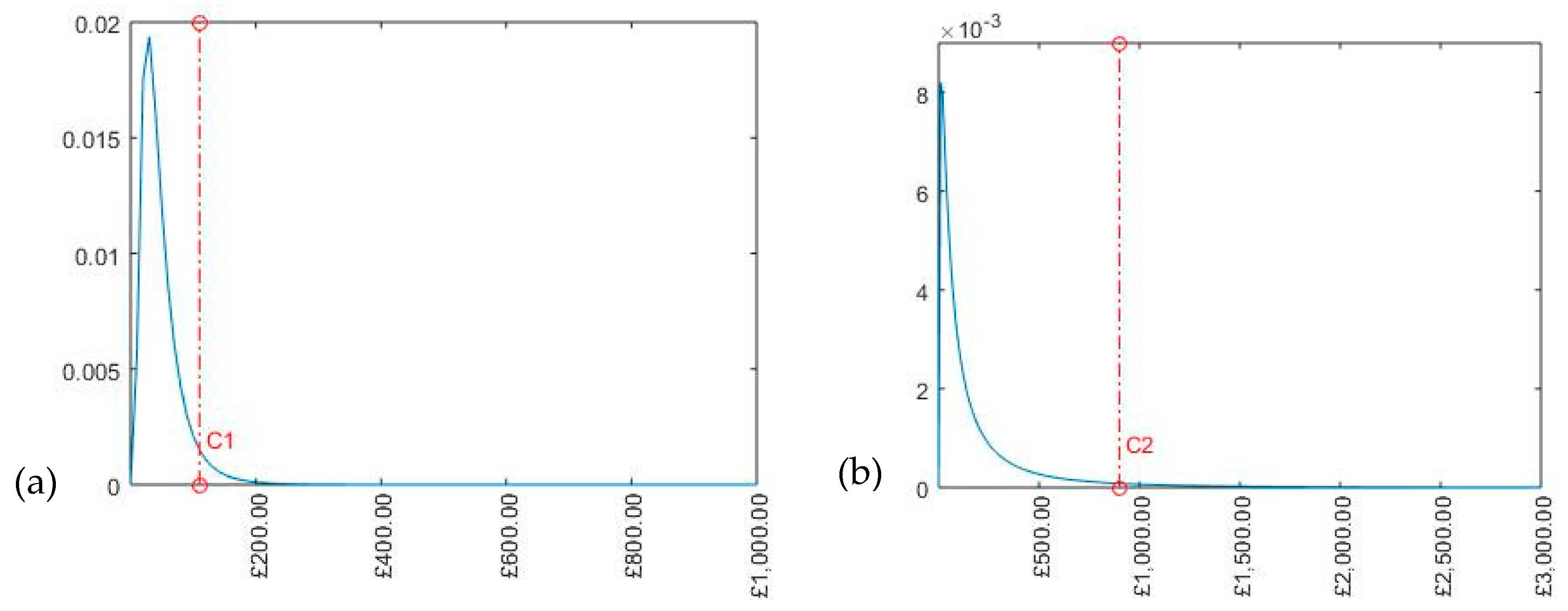

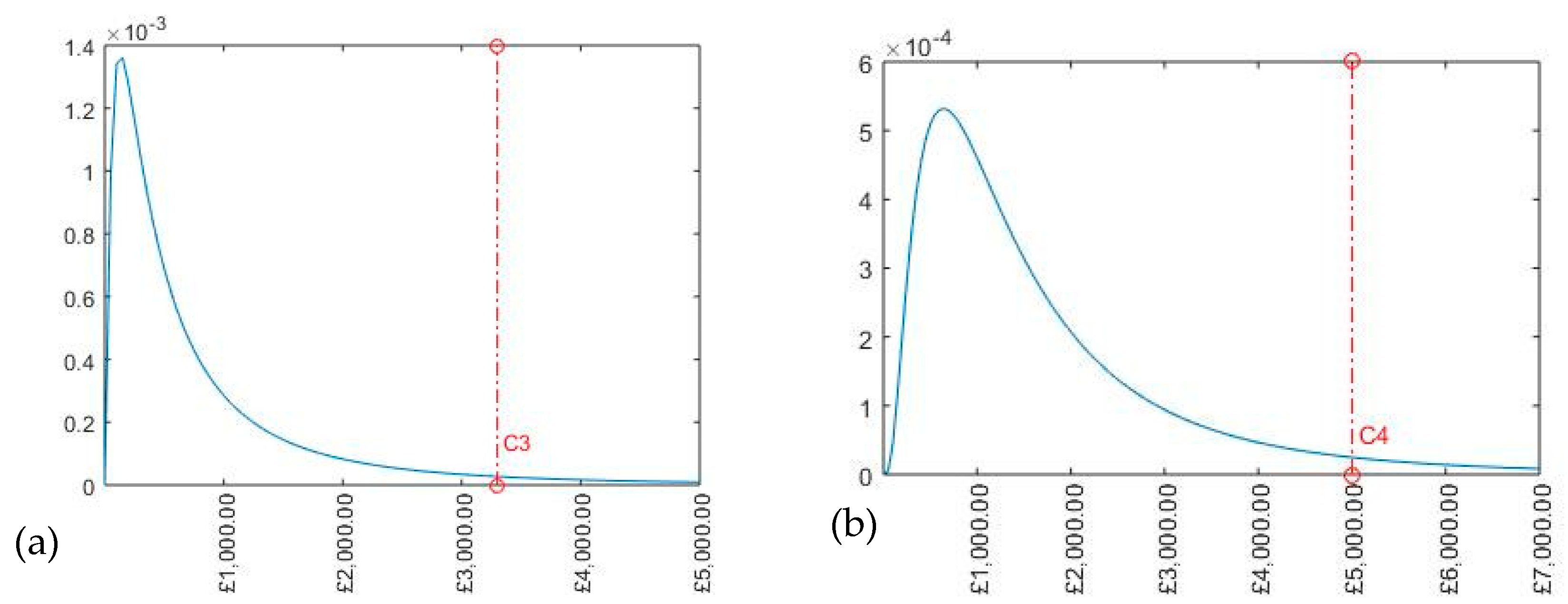

LN(μ, σ2), for the building damage costs for each damage category. Using these values, a log-normal PDF (

fs) describing the variation in the corresponding (repair) cost (

Cs) for each damage category is presented in

Figure 11,

Figure 12 and

Figure 13, using MATLAB.

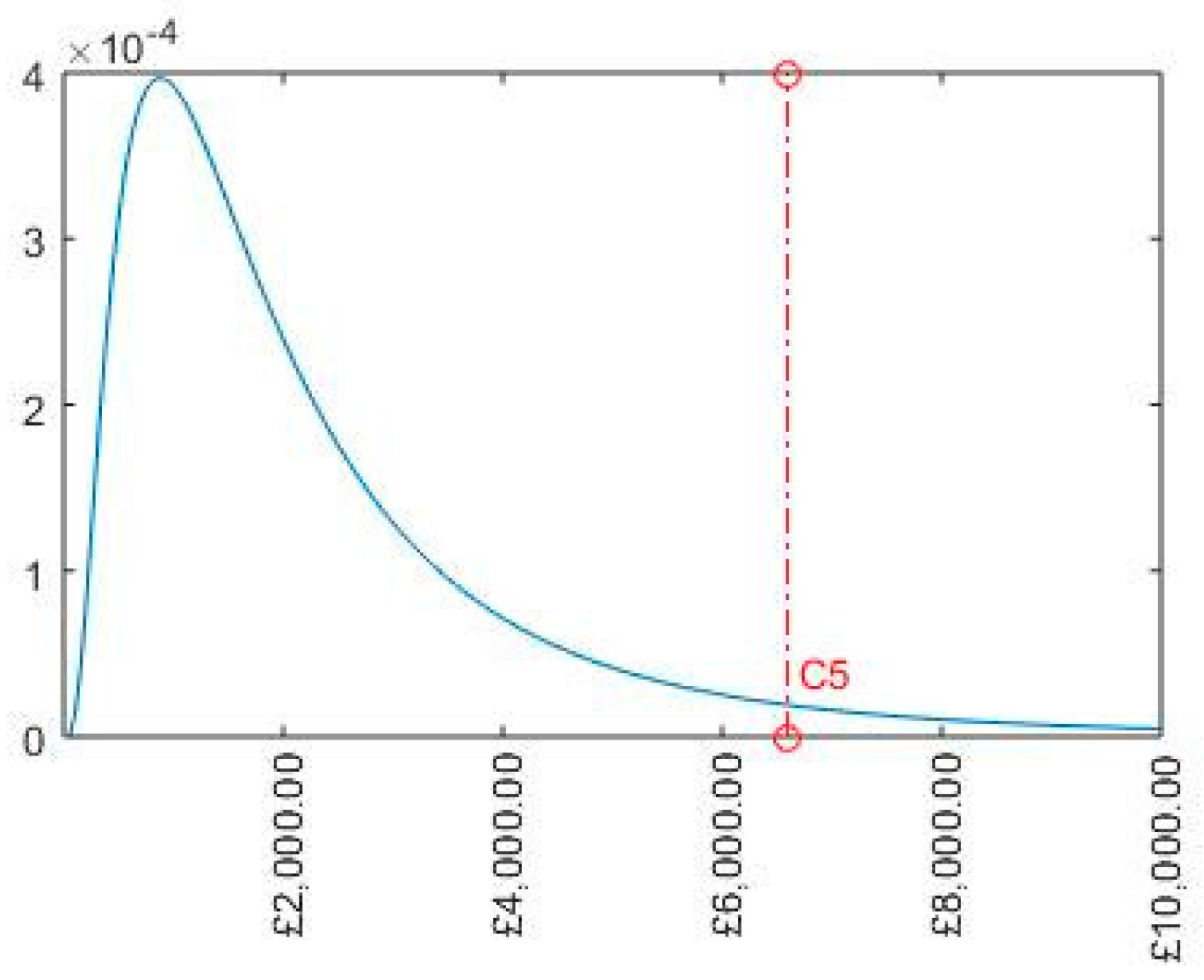

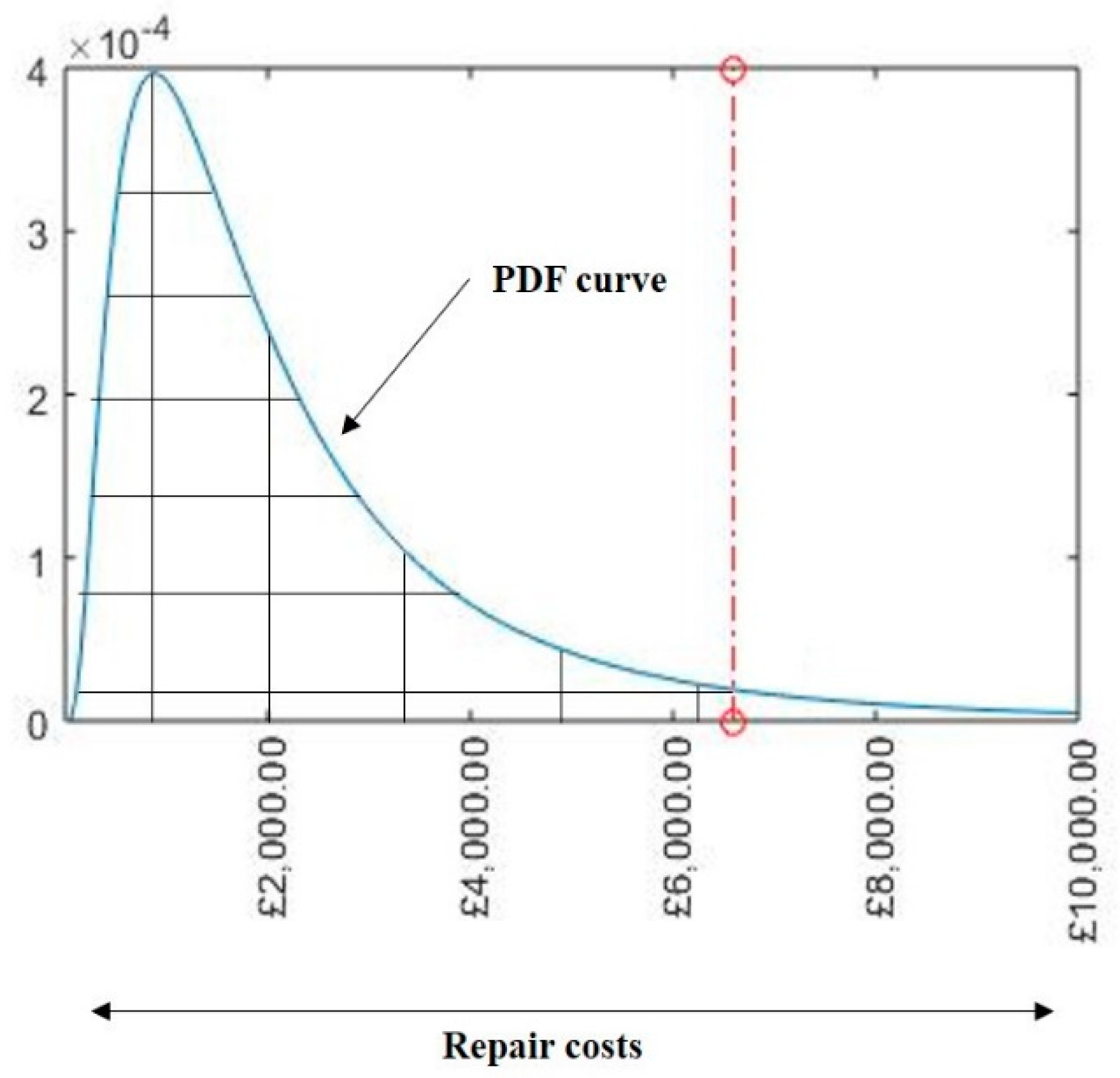

Finally, the settlement economic risk is provided for a building in relation to the probability of damage within one of the damage categories. This is estimated using Equation (7), using the integral indicated by the area bounded by the PDF curve for a damage category and by the repair costs up to the point of the cost corresponding to the probability of this damage category. By way of example, as shown in

Figure 14, the settlement economic risk for the damage category No. 5 (severe) is provided using the grid-area created by the PDF curve and the repair costs up to the cost corresponding in this case to the 95% percentile probability of damage (damage category No. 5). This is also applied for the other damage categories, and their sum provides the settlement economic risk of a building. These can then be presented visually, as discussed in the next section of the paper.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}