Responsible Innovation in SMEs: A Systematic Literature Review for a Conceptual Model

Abstract

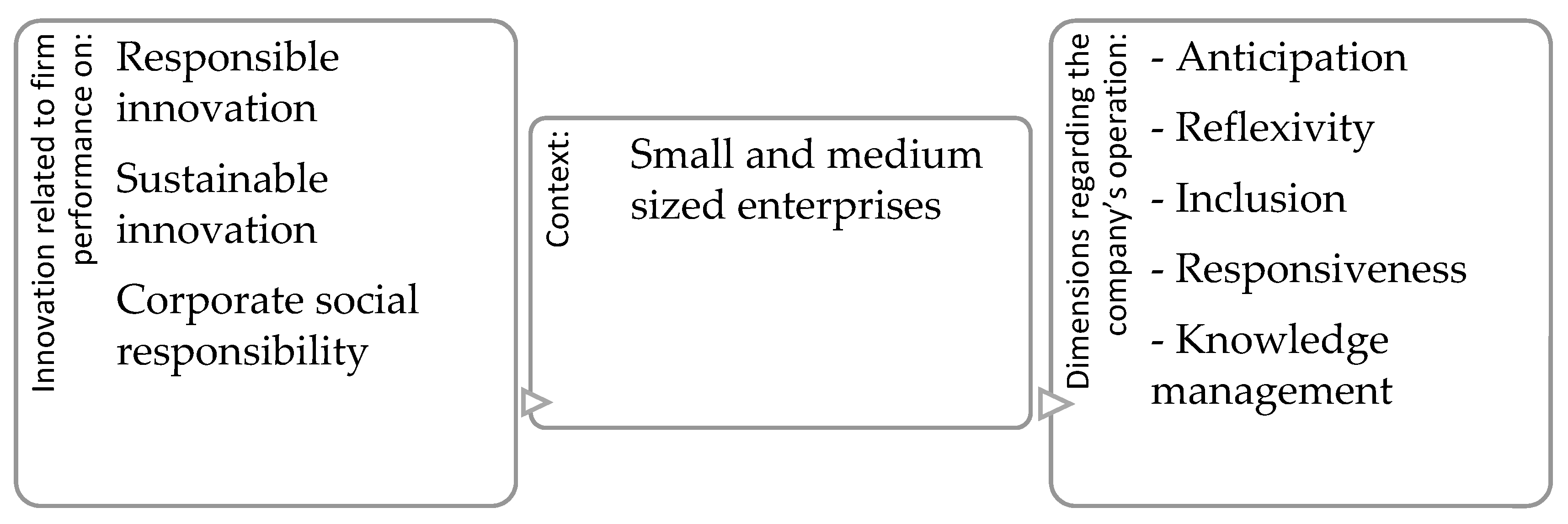

:1. Introduction

2. Background

- (a)

- “A transparent, interactive process by which societal actors and innovators become mutually responsive to each other with a view to the (ethical) acceptability, sustainability and societal desirability of the innovation process and its marketable products (in order to allow a proper embedding of scientific and technological advances in our society)” [26] (p. 9).

- (b)

- Responsible research and innovation refers to the comprehensive approach of proceeding in research and innovation in ways that allow all stakeholders that are involved in the processes of research and innovation at an early stage (A) to obtain relevant knowledge on the consequences of the outcomes of their actions and on the range of options open to them, and (B) to effectively evaluate both outcomes and options in terms of societal needs and moral values, and (C) to use these considerations (under A and B) as functional requirements for the design and development of new research, products, and services [27].

- (c)

- “Responsible innovation means taking care of the future through collective stewardship of science and innovation in the present” [14] (p. 1570).

- (d)

- Responsible innovation refers to a new or significantly improved product, service, or business model whose implementation at the market solves or alleviates an environmental or a social problem [28] (p. 548).

3. Methodology

3.1. Question Formulation

- What are the key dimensions that contribute to the implementation of responsible innovation in SMEs?

- How can activities contributing to the implementation of responsible innovation affect the performance of SMEs?

- What are the contingent variables that influence the relationship between responsible innovation and performance in SMEs?

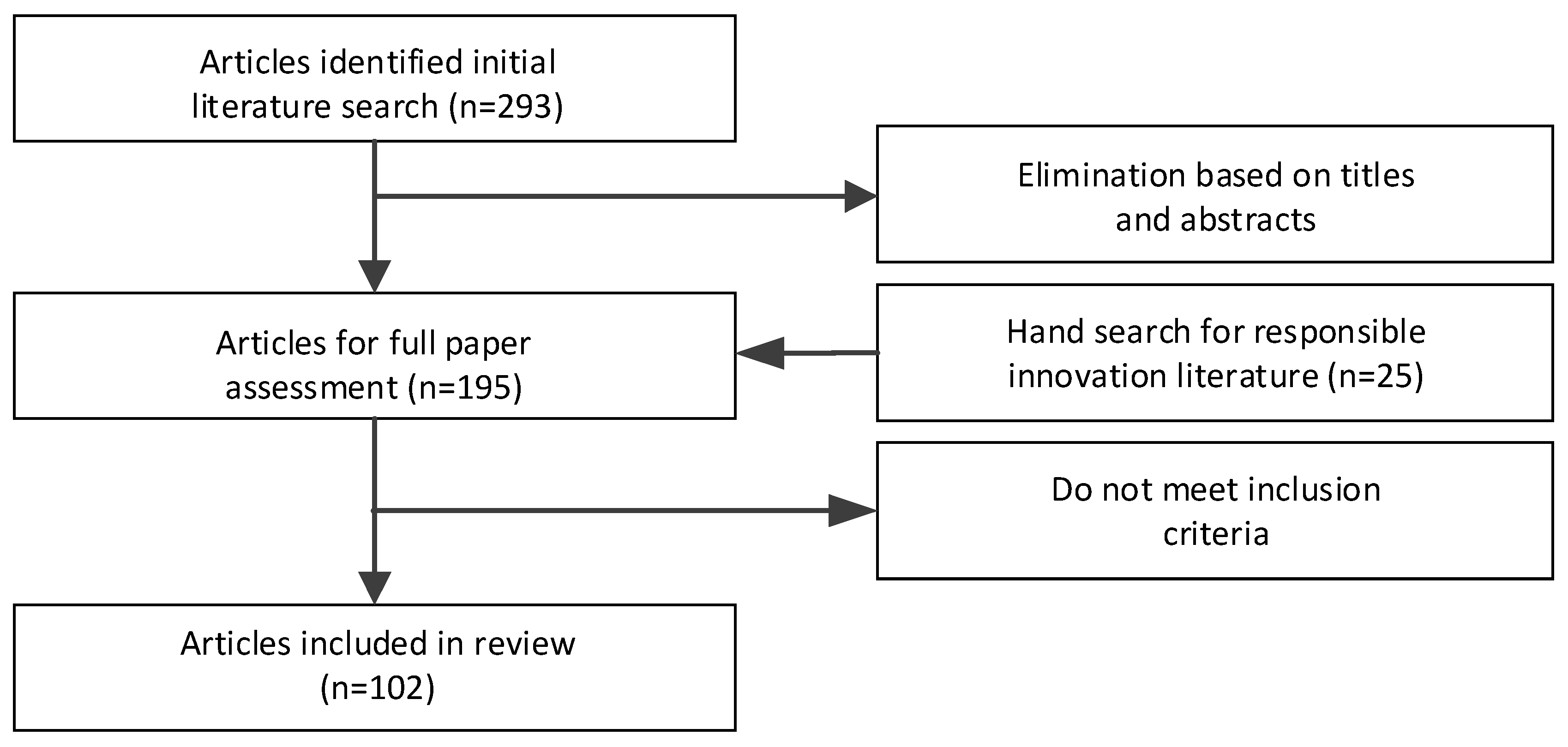

3.2. Locating and Selection Studies

- (1)

- Articles based on empirical and peer-reviewed research;

- (2)

- that included one of the key words in the title or the abstract;

- (3)

- articles that consider SMEs as research centres;

- (4)

- available in the above-mentioned database;

- (5)

- published between 2000 and 2020;

- (6)

- articles in English; and

- (7)

- articles in the areas of business research, economics, social sciences, environmental sciences, or technological science.

3.3. Data Analysis

4. Results

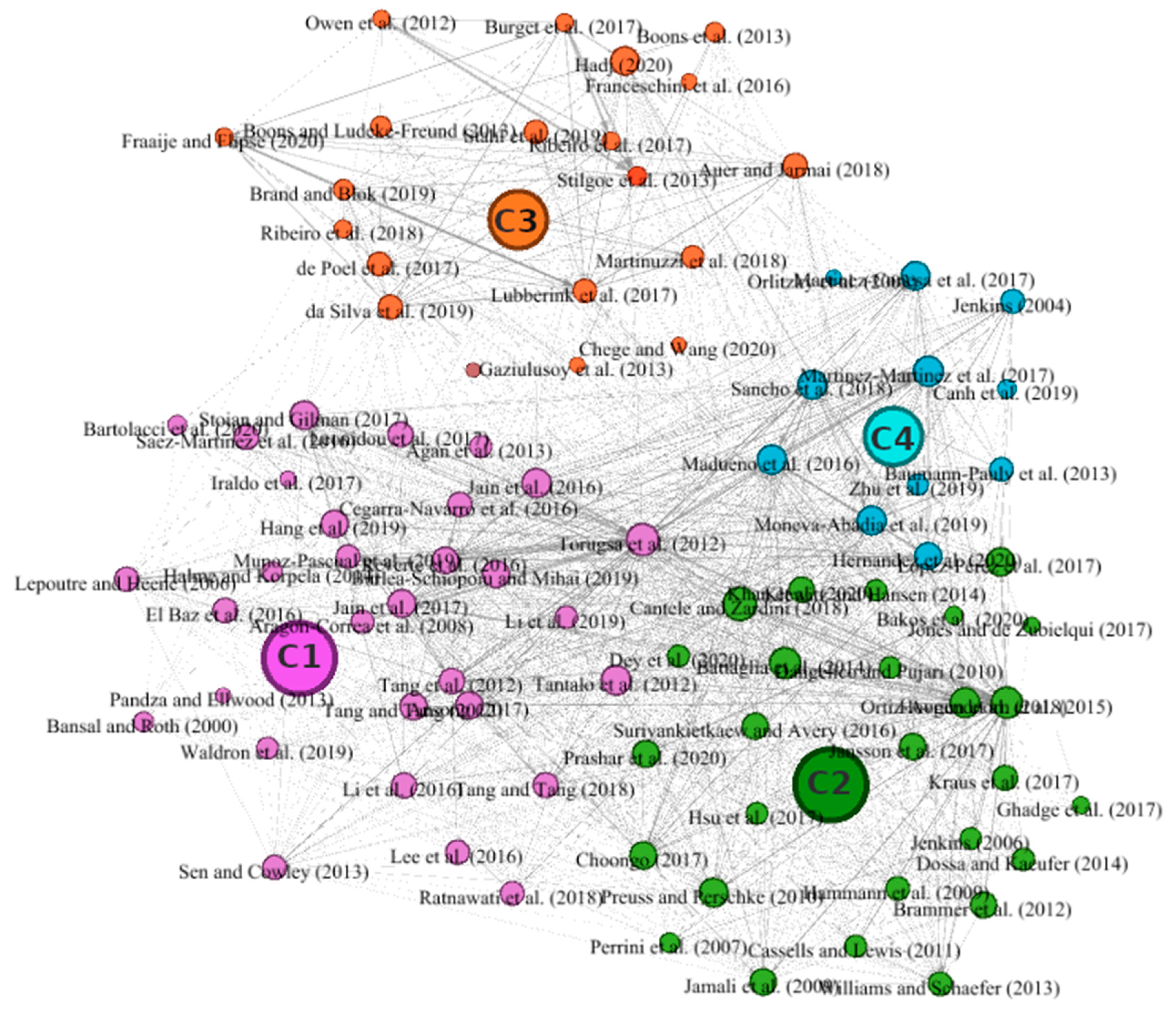

4.1. Bibliometric Analysis

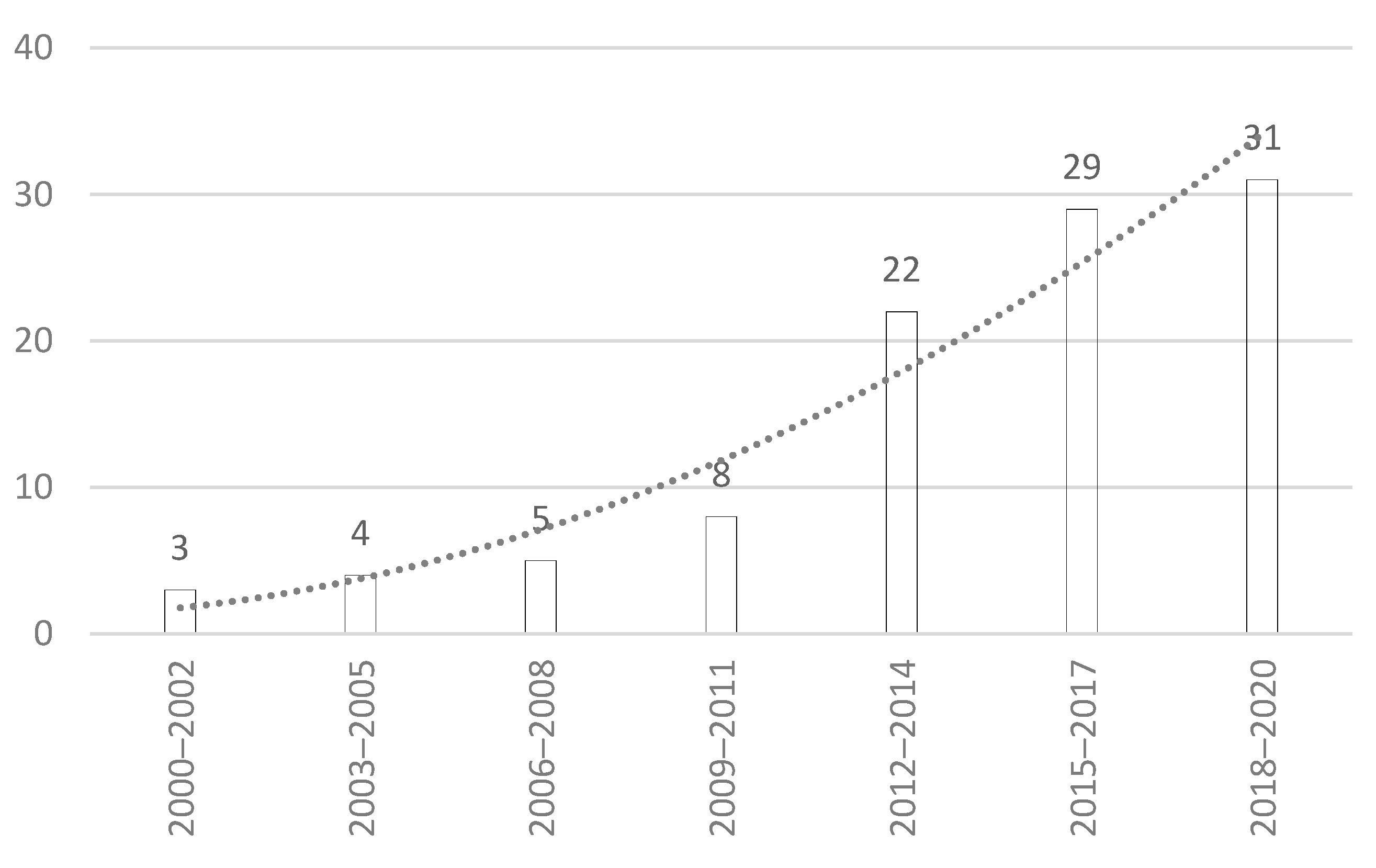

4.2. Research Trends over Time

4.3. Associated Communities

4.3.1. Cluster 1: Responsible Innovation Drivers in SMEs

4.3.2. Cluster 2: Genuine Silent Responsibility Practices

4.3.3. Cluster 3: Responsible Innovation Framework

4.3.4. Cluster 4: Social Responsibility Practices and Performance in SMEs

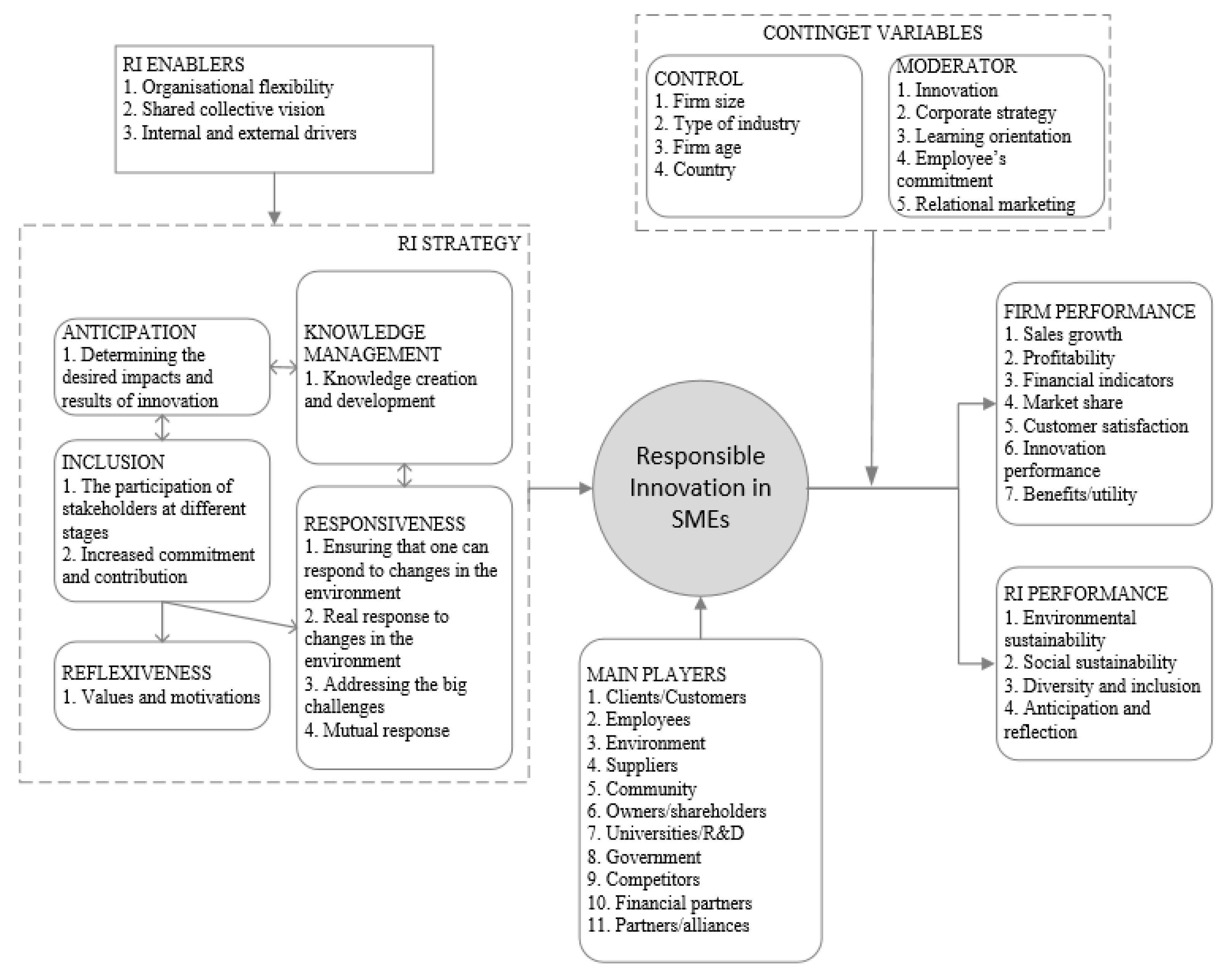

5. Theoretical Framework Based on the Literature

5.1. Dimensions of Responsible Innovation

5.1.1. Anticipation

5.1.2. Reflexiveness

5.1.3. Inclusion

5.1.4. Responsiveness

5.1.5. Knowledge Management

5.2. Relationship of Responsible Innovation with Performance

5.3. Contingent Variables

5.4. Responsible Innovation Antecedents and Enablers

6. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Main Code | Strategy | Qty | References |

|---|---|---|---|

| Inclusion | The participation of stakeholders at different stages | 18 | [13,15,18,28,43,52,53,57,58,61,70,76,77,84,92,94,95,107] |

| Increased commitment and contribution | 12 | [15,18,23,32,43,44,45,58,62,77,84,109] | |

| Responsiveness | Ensuring that one can respond to changes in the environment | 12 | [9,13,20,23,32,48,52,70,71,84,94,96] |

| Addressing the big challenges | 12 | [1,6,21,28,46,49,58,60,64,66,96,103] | |

| Real response to changes in the environment | 6 | [22,28,46,50,56,69] | |

| Mutual response | 3 | [31,50,96] | |

| Reflexiveness | Values and motivations | 18 | [6,13,17,22,31,32,43,44,46,48,53,60,61,66,70,75,77,92] |

| Knowledge management | Knowledge creation and development | 19 | [2,6,17,21,23,31,32,47,51,53,60,62,64,66,75,83,84,92,93] |

| Firm performance | Sales growth | 19 | [1,15,34,44,61,63,64,65,67,68,72,84,92,93,94,96,99,102,110] |

| Profitability | 21 | [1,15,34,38,51,52,55,59,60,61,63,65,72,82,84,87,92,99,110] | |

| Financial indicators | 15 | [20,52,54,55,59,63,65,67,72,82,85,93,96,99,110] | |

| Market share | 13 | [15,51,63,64,65,67,72,76,84,93,96,110] | |

| Customer satisfaction | 10 | [15,59,63,64,65,81,84,96,99,108] | |

| Innovation performance | 7 | [15,53,59,64,66,101,107] | |

| Benefits/utility | 6 | [20,32,49,63,64,84] | |

| Productivity | 4 | [1,39,68,109] | |

| RI performance | Environmental sustainability | 27 | [2,21,38,46,48,49,50,51,53,57,65,66,67,68,69,75,76,86,87,94,101,103,104,106,107,108,109,111,112] |

| Social sustainability | 24 | [2,11,13,15,21,31,32,34,39,51,53,57,60,68,76,82,86,89,100,102,104,109,111,112] | |

| Diversity and inclusion - Engagement | 13 | [15,18,32,41,59,63,76,81,84,90,99,104,110] | |

| Anticipation and reflection - Legislative landscape - Assessment - Public and ethical issues - Imagen | 11 | [21,32,51,63,76,81,87,93,99,104,110] | |

| Main players | Clients/Customers | 31 | [15,20,21,32,38,41,43,44,48,49,51,52,53,59,61,62,63,68,69,80,81,91,92,93,96,99,103,104,106,107,108] |

| Employees | 27 | [15,20,21,32,41,43,44,48,49,53,59,61,62,63,68,80,85,86,91,92,93,96,99,104,106,107,108] | |

| Environment | 15 | [15,20,21,32,38,43,53,59,61,63,86,92,104,107,108] | |

| Suppliers | 14 | [15,20,32,43,48,49,52,53,59,62,68,85,106,107] | |

| Community | 14 | [15,32,38,43,52,53,59,61,85,86,92,104,106,107] | |

| Owners/shareholders | 7 | [15,20,32,43,52,91,106] | |

| R&D | 7 | [1,21,46,55,58,94,100] | |

| Government | 5 | [48,52,69,86,106] | |

| Competitors | 4 | [20,52,69,108] | |

| Funding agencies/Investors | 4 | [52,58,62,69,106] | |

| Alliances | 4 | [41,46,60,94] | |

| Contingent variables | Size | 27 | [15,20,22,39,44,48,49,50,51,52,53,54,55,60,61,63,72,80,82,84,85,89,94,95,96,99,100,101] |

| Type of industry | 17 | [38,39,45,49,51,53,54,60,65,89,92,94,96,99,100,101,102] | |

| Firm age | 12 | [15,22,39,49,50,61,72,89,95,96,101,103] | |

| Innovation | 13 | [1,20,64,81,85,86,93,96,102,104] | |

| Country | 3 | [38,45,94] | |

| Corporate strategy | 2 | [89,96] | |

| Learning orientation | 2 | [47,67] | |

| Employee’s commitment | 2 | [72,84] | |

| Relational marketing | 2 | [80,84] |

References

- Jones, J.; De Zubielqui, G.C. Doing well by doing good: A study of university-industry interactions, innovationess and firm performance in sustainability-oriented Australian SMEs. Technol. Forecast. Soc. Chang. 2017, 123, 262–270. [Google Scholar] [CrossRef]

- Kraus, S.; Burtscher, J.; Niemand, T.; Roig-Tierno, N.; Syrjä, P.; Kraus, S.; Burtscher, J.; Niemand, T.; Roig-Tierno, N.; Syrjä, P. Configurational paths to social performance in SMEs: The interplay of innovation, sustainability, resources and achievement motivation. Sustainability 2017, 9, 1828. [Google Scholar] [CrossRef] [Green Version]

- Porter, M.E. Technology and competitive advantage. J. Bus. Strategy 1985, 5, 60–78. [Google Scholar] [CrossRef]

- Von Schomberg, R. A vision of responsible research and innovation. In Responsible Innovation: Managing the Responsible Emergence of Science and Innovation in Society; Wiley: Hoboken, NJ, USA, 2013; pp. 51–74. [Google Scholar]

- Ribeiro, B.; Bengtsson, L.; Benneworth, P.S.; Bührer, S.; Castro-Martínez, E.; Hansen, M.; Jarmai, K.; Lindner, R.; Olmos-Peñuela, J.; Ott, C.; et al. Introducing the dilemma of societal alignment for inclusive and responsible research and innovation. J. Responsible Innov. 2018, 5, 316–331. [Google Scholar] [CrossRef] [Green Version]

- Auer, A.; Jarmai, K. Implementing responsible research and innovation practices in SMEs: Insights into drivers and barriers from the Austrian medical device sector. Sustainability 2017, 10, 17. [Google Scholar] [CrossRef] [Green Version]

- Martinuzzi, A.; Blok, V.; Brem, A.; Stahl, B.C.; Schönherr, N. Responsible research and innovation in industry—Challenges, insights and perspectives. Sustainability 2018, 10, 702. [Google Scholar] [CrossRef] [Green Version]

- Visser, W. The age of responsibility: CSR 2.0 and the New DNA of Business. J. Bus. Syst. Gov. Ethics 2010, 5, 7. [Google Scholar] [CrossRef]

- Van De Poel, I.; Asveld, L.; Flipse, S.M.; Klaassen, P.; Scholten, V.E.; Yaghmaei, E. Company strategies for responsible research and innovation (rri): A conceptual model. Sustainability 2017, 9, 2045. [Google Scholar] [CrossRef] [Green Version]

- Ribeiro, B.E.; Smith, R.D.J.; Millar, K. A Mobilising Concept? Unpacking Academic Representations of Responsible Research and Innovation. Sci. Eng. Ethics 2017, 23, 81–103. [Google Scholar] [CrossRef] [Green Version]

- Pandza, K.; Ellwood, P. Strategic and ethical foundations for responsible innovation. Res. Policy 2013, 42, 1112–1125. [Google Scholar] [CrossRef]

- European Commission. Rome Declaration on Responsible Research and Innovation in Europe; European Commission: Brussels, Belgium, 2014. [Google Scholar]

- Burget, M.; Bardone, E.; Pedaste, M. Definitions and Conceptual Dimensions of Responsible Research and Innovation: A Literature Review. Sci. Eng. Ethics 2017, 23, 1–19. [Google Scholar] [CrossRef] [PubMed]

- Stilgoe, J.; Owen, R.; Macnaghten, P. Developing a framework for responsible innovation. Res. Policy 2013, 42, 1568–1580. [Google Scholar] [CrossRef] [Green Version]

- Khan, S.Z.; Yang, Q.; Khan, N.U.; Kherbachi, S.; Huemann, M. Sustainable social responsibility toward multiple stakeholders as a trump card for small and medium-sized enterprise performance (evidence from China). Corp. Soc. Responsib. Environ. Manag. 2020, 27, 95–108. [Google Scholar] [CrossRef]

- Miller, K.; Neubauer, A.; Varma, A.; Williams, E. First Assessment of the Environmental Compliance Assistance Programme for SMEs (ECAP); Report Prepared for the European Commission, DG Environment and Climate Action; European Commission: Brussels, Belgium, 2011. [Google Scholar]

- Lubberink, R.; Blok, V.; Van Ophem, J.; Omta, O. Lessons for responsible innovation in the business context: A systematic literature review of responsible, social and sustainable innovation practices. Sustainability 2017, 9, 721. [Google Scholar] [CrossRef] [Green Version]

- Hammann, E.-M.; Habisch, A.; Pechlaner, H. Values that create value: Socially responsible business practices in SMEs—Empirical evidence from German companies. Bus. Ethics Eur. Rev. 2009, 18, 37–51. [Google Scholar] [CrossRef]

- Klewitz, J.; Hansen, E.G. Sustainability-oriented innovation of SMEs: A systematic review. J. Clean. Prod. 2014, 65, 57–75. [Google Scholar] [CrossRef]

- Aragón-Correa, J.A.; Hurtado-Torres, N.; Sharma, S.; García-Morales, V.J. Environmental strategy and performance in small firms: A resource-based perspective. J. Environ. Manag. 2008, 86, 88–103. [Google Scholar] [CrossRef]

- Bos-Brouwers, H.E.J. Corporate sustainability and innovation in SMEs: Evidence of themes and activities in practice. Bus. Strat. Environ. 2010, 19, 417–435. [Google Scholar] [CrossRef]

- Cassells, S.; Lewis, K.V. SMEs and environmental responsibility: Do actions reflect attitudes? Corp. Soc. Responsib. Environ. Manag. 2011, 18, 186–199. [Google Scholar] [CrossRef]

- Avram, D.O.; Domnanovich, J.; Kronenberg, C.; Scholz, M. Exploring the integration of corporate social responsibility into the strategies of small- and medium-sized enterprises: A systematic literature review. J. Clean. Prod. 2018, 201, 254–271. [Google Scholar] [CrossRef]

- Valdivia, W.D.; Guston, D.H. Responsible Innovation: A Primer for Policymakers; The Brookings Institute: Washington, DC, USA, 2015. [Google Scholar]

- Organisation for Economic Cooperation and Development (OECD); Statistical Office of the European Communities. Oslo Manual: Guidelines for Collecting and Interpreting Innovation Data; OECD: Paris, France, 2005; Volume 46. [Google Scholar]

- Von Schomberg, R. Prospects for technology assessment in a framework of responsible research and innovation. In Technikfolgen Abschätzen Lehren; Springer: Berlin/Heidelberg, Germany, 2012; pp. 39–61. [Google Scholar]

- European Commission. A collection of good practice cases among small and medium-sized enterprises across Europe: 1–60. Visited 2003, 10, 2005. [Google Scholar]

- Halme, M.; Korpela, M. Responsible innovation toward sustainable development in small and medium-sized enterprises: A resource perspective. Bus. Strat. Environ. 2014, 23, 547–566. [Google Scholar] [CrossRef]

- Chatfield, K.; Iatridis, K.; Stahl, B.C.; Paspallis, N. Innovating responsibly in ICT for ageing: Drivers, obstacles and implementation. Sustainability 2017, 9, 971. [Google Scholar] [CrossRef] [Green Version]

- Owen, R.; Macnaghten, P.; Stilgoe, J. Responsible research and innovation: From science in society to science for society, with society. Sci. Public Policy 2012, 39, 751–760. [Google Scholar] [CrossRef] [Green Version]

- Lepoutre, J.; Heene, A. Investigating the impact of firm size on small business social responsibility: A critical review. J. Bus. Ethics 2006, 67, 257–273. [Google Scholar] [CrossRef]

- Jenkins, H. Small business champions for corporate social responsibility. J. Bus. Ethics 2006, 67, 241–256. [Google Scholar] [CrossRef]

- Fuller, T.; Tian, Y. Social and symbolic capital and responsible entrepreneurship: An empirical investigation of SME narratives. J. Bus. Ethics 2006, 67, 287–304. [Google Scholar] [CrossRef]

- Suriyankietkaew, S.; Avery, G.C. Sustainable leadership practices driving financial performance: Empirical evidence from Thai SMEs. Sustainability 2016, 8, 327. [Google Scholar] [CrossRef] [Green Version]

- Tranfield, D.; Denyer, D.; Smart, P. Towards a methodology for developing evidence-informed management knowledge by means of systematic review. Br. J. Manag. 2003, 14, 207–222. [Google Scholar] [CrossRef]

- Denyer, D.; Tranfield, D. Producing a systematic review. In The Sage Handbook of Organizational Research Methods; Sage Publications Ltd.: Thousand Oaks, CA, USA, 2009; pp. 671–689. [Google Scholar]

- Aboelmaged, M.G. Six Sigma quality: A structured review and implications for future research. Int. J. Qual. Reliab. Manag. 2010, 27, 268–317. [Google Scholar] [CrossRef]

- Bansal, P.; Roth, K. Why companies go green: A model of ecological responsiveness. Acad. Manag. J. 2000, 43, 717–736. [Google Scholar]

- Besser, T.L.; Miller, N. Is the good corporation dead? The community social responsibility of small business operators. J. Socio-Econ. 2001, 30, 221–241. [Google Scholar] [CrossRef]

- Jenkins, H. A critique of conventional CSR theory: An SME perspective. J. Gen. Manag. 2004, 29, 37–57. [Google Scholar] [CrossRef]

- Castka, P.; Balzarova, M.A.; Bamber, C.; Sharp, J.M. How can SMEs effectively implement the CSR agenda? A UK case study perspective. Corp. Soc. Responsib. Environ. Manag. 2004, 11, 140–149. [Google Scholar] [CrossRef]

- Salzmann, O.; Ionescu-Somers, A.; Steger, U. The business case for corporate sustainability: Literature review and research options. Eur. Manag. J. 2005, 23, 27–36. [Google Scholar] [CrossRef]

- Jamali, D.; Zanhour, M.; Keshishian, T. Peculiar strengths and relational attributes of SMEs in the context of CSR. J. Bus. Ethics 2009, 87, 355–377. [Google Scholar] [CrossRef]

- Preuss, L.; Perschke, J. Slipstreaming the larger boats: Social responsibility in medium-sized businesses. J. Bus. Ethics 2010, 92, 531–551. [Google Scholar] [CrossRef]

- Perrini, F.; Russo, A.; Tencati, A. CSR strategies of SMEs and large firms. Evidence from Italy. J. Bus. Ethics 2007, 74, 285–300. [Google Scholar] [CrossRef]

- Dangelico, R.M.; Pujari, D. Mainstreaming green product innovation: Why and how companies integrate environmental sustainability. J. Bus. Ethics 2010, 95, 471–486. [Google Scholar] [CrossRef]

- Rhee, J.; Park, T.; Lee, D.H. Drivers of innovativeness and performance for innovative SMEs in South Korea: Mediation of learning orientation. Technovation 2010, 30, 65–75. [Google Scholar] [CrossRef]

- Brammer, S.; Hoejmose, S.; Marchant, K. Environmental management in SME s in the UK: Practices, pressures and perceived benefits. Bus. Strategy Environ. 2012, 21, 423–434. [Google Scholar] [CrossRef]

- Hofmann, K.H.; Theyel, G.; Wood, C.H. Identifying firm capabilities as drivers of environmental management and sustainability practices—Evidence from small and medium-sized manufacturers. Bus. Strategy Environ. 2012, 21, 530–545. [Google Scholar] [CrossRef]

- Tang, Z.; Tang, J. Stakeholder–firm power difference, stakeholders’ CSR orientation, and SMEs’ environmental performance in China. J. Bus. Ventur. 2012, 27, 436–455. [Google Scholar] [CrossRef]

- Agan, Y.; Acar, M.F.; Borodin, A. Drivers of environmental processes and their impact on performance: A study of Turkish SMEs. J. Clean. Prod. 2013, 51, 23–33. [Google Scholar] [CrossRef]

- Torugsa, N.A.; O’Donohue, W.; Hecker, R. Capabilities, proactive CSR and financial performance in SMEs: Empirical evidence from an Australian manufacturing industry sector. J. Bus. Ethics 2012, 109, 483–500. [Google Scholar] [CrossRef] [Green Version]

- Tantalo, C.; Caroli, M.G.; Vanevenhoven, J. Corporate social responsibility and SME’s competitiveness. Int. J. Technol. Manag. 2012, 58, 129–151. [Google Scholar] [CrossRef]

- Tang, Z.; Hull, C.E.; Rothenberg, S. How corporate social responsibility engagement strategy moderates the CSR-financial performance relationship. J. Manag. Stud. 2012, 49, 1274–1303. [Google Scholar] [CrossRef]

- Torugsa, N.A.; O’Donohue, W.; Hecker, R. Proactive CSR: An empirical analysis of the role of its economic, social and environmental dimensions on the association between capabilities and performance. J. Bus. Ethics 2013, 115, 383–402. [Google Scholar] [CrossRef] [Green Version]

- Boons, F.; Lüdeke-Freund, F. Business models for sustainable innovation: State-of-the-art and steps towards a research agenda. J. Clean. Prod. 2013, 45, 9–19. [Google Scholar] [CrossRef]

- Gaziulusoy, A.I.; Boyle, C.; McDowall, R. System innovation for sustainability: A systemic double-flow scenario method for companies. J. Clean. Prod. 2013, 45, 104–116. [Google Scholar] [CrossRef]

- Da Silva, L.M.; Bitencourt, C.C.; Faccin, K.; Iakovleva, T. The Role of Stakeholders in the Context of Responsible Innovation: A Meta-Synthesis. Sustainability 2019, 11, 1766. [Google Scholar] [CrossRef] [Green Version]

- Martinez-Conesa, I.; Soto-Acosta, P.; Palacios-Manzano, M. Corporate social responsibility and its effect on innovation and firm performance: An empirical research in SMEs. J. Clean. Prod. 2017, 142, 2374–2383. [Google Scholar] [CrossRef]

- Burlea-Schiopoiu, A.; Mihai, L.S. An Integrated Framework on the Sustainability of SMEs. Sustainability 2019, 11, 6026. [Google Scholar] [CrossRef] [Green Version]

- Jain, P.; Vyas, V.; Chalasani, D.P.S. Corporate social responsibility and financial performance in SMEs: A structural equation modelling approach. Glob. Bus. Rev. 2016, 17, 630–653. [Google Scholar] [CrossRef]

- Sen, S.; Cowley, J. The relevance of stakeholder theory and social capital theory in the context of csr in SMEs: An australian perspective. J. Bus. Ethics 2013, 118, 413–427. [Google Scholar] [CrossRef]

- Madueno, J.H.; Jorge, M.L.; Conesa, I.M.; Martínez-Martínez, D. Relationship between corporate social responsibility and competitive performance in Spanish SMEs: Empirical evidence from a stakeholders’ perspective. BRQ Bus. Res. Q. 2016, 19, 55–72. [Google Scholar] [CrossRef] [Green Version]

- Ratnawati Soetjipto, B.E.; Murwani, F.D.; Wahyono, H. The Role of SMEs’ Innovation and Learning Orientation in Mediating the Effect of CSR Programme on SMEs’ Performance and Competitive Advantage. Glob. Bus. Rev. 2018, 19, S21–S38. [Google Scholar] [CrossRef]

- Leonidou, L.C.; Christodoulides, P.; Kyrgidou, L.P.; Palihawadana, D. Internal drivers and performance consequences of small firm green business strategy: The moderating role of external forces. J. Bus. Ethics 2017, 140, 585–606. [Google Scholar] [CrossRef] [Green Version]

- Li, L.; Li, G.; Tsai, F.-S.; Lee, H.-Y.; Lee, C.-H. The effects of corporate social responsibility on service innovation performance: The role of dynamic capability for sustainability. Sustainability 2019, 11, 2739. [Google Scholar] [CrossRef] [Green Version]

- Hang, M.; Geyer-Klingeberg, J.; Rathgeber, A. It is merely a matter of time: A meta-analysis of the causality between environmental performance and financial performance. Bus. Strategy Environ. 2019, 28, 257–273. [Google Scholar] [CrossRef]

- Dey, P.K.; Malesios, C.; De, D.; Chowdhury, S.; Ben Abdelaziz, F. The impact of lean management practices and sustainably-oriented innovation on sustainability performance of small and medium-sized enterprises: Empirical evidence from the UK. Br. J. Manag. 2019, 31, 141–161. [Google Scholar] [CrossRef]

- Ghadge, A.; Kaklamanou, M.; Choudhary, S.; Bourlakis, M. Implementing environmental practices within the Greek dairy supply chain. Ind. Manag. Data Syst. 2017, 117, 1995–2014. [Google Scholar] [CrossRef]

- Jansson, J.; Nilsson, J.; Modig, F.; Vall, G.H. Commitment to sustainability in small and medium-sized enterprises: The influence of strategic orientations and management values. Bus. Strategy Environ. 2017, 26, 69–83. [Google Scholar] [CrossRef]

- Hsu, C.-H.; Chang, A.-Y.; Luo, W. Identifying key performance factors for sustainability development of SMEs—Integrating QFD and fuzzy MADM methods. J. Clean. Prod. 2017, 161, 629–645. [Google Scholar] [CrossRef]

- Choongo, P. A longitudinal study of the impact of corporate social responsibility on firm performance in SMEs in Zambia. Sustainability 2017, 9, 1300. [Google Scholar] [CrossRef] [Green Version]

- Baumann-Pauly, D.; Wickert, C.; Spence, L.J.; Scherer, A.G. Organizing corporate social responsibility in small and large firms: Size matters. J. Bus. Ethics 2013, 115, 693–705. [Google Scholar] [CrossRef] [Green Version]

- Lee, K.-H.; Herold, D.M.; Yu, A.-L. Small and medium enterprises and corporate social responsibility practice: A Swedish perspective. Corp. Soc. Responsib. Environ. Manag. 2016, 23, 88–99. [Google Scholar] [CrossRef]

- Williams, S.; Schaefer, A. Small and medium-sized enterprises and sustainability: Managers’ values and engagement with environmental and climate change issues. Bus. Strategy Environ. 2013, 22, 173–186. [Google Scholar] [CrossRef] [Green Version]

- Stahl, B.C.; Chatfield, K.; Holter, C.T.; Brem, A. Ethics in corporate research and development: Can responsible research and innovation approaches aid sustainability? J. Clean. Prod. 2019, 239, 118044. [Google Scholar] [CrossRef]

- Dossa, Z.; Kaeufer, K. Understanding sustainability innovations through positive ethical networks. J. Bus. Ethics 2014, 119, 543–559. [Google Scholar] [CrossRef]

- Boons, F.; Montalvo, C.; Quist, J.; Wagner, M. Sustainable innovation, business models and economic performance: An overview. J. Clean. Prod. 2013, 45, 1–8. [Google Scholar] [CrossRef]

- Brand, T.; Blok, V. Responsible innovation in business: A critical reflection on deliberative engagement as a central governance mechanism. J. Responsible Innov. 2019, 6, 4–24. [Google Scholar] [CrossRef] [Green Version]

- Martínez-Martínez, D.; Madueño, J.H.; Jorge, M.L.; Sancho, M.P.L. The strategic nature of corporate social responsibility in SMEs: A multiple mediator analysis. Ind. Manag. Data Syst. 2017, 117, 2–31. [Google Scholar] [CrossRef]

- Moneva-Abadía, J.M.; Gallardo-Vázquez, D.; Sánchez-Hernández, M.I. Corporate social responsibility as a strategic opportunity for small firms during economic crises. J. Small Bus. Manag. 2019, 57, 172–199. [Google Scholar] [CrossRef] [Green Version]

- Hernández, J.P.S.-I.; Yañez-Araque, B.; Moreno-García, J. Moderating effect of firm size on the influence of corporate social responsibility in the economic performance of micro-, small- and medium-sized enterprises. Technol. Forecast. Soc. Chang. 2020, 151, 119774. [Google Scholar] [CrossRef]

- Orlitzky, M.; Schmidt, F.L.; Rynes, S.L. Corporate Social and Financial Performance: A Meta-Analysis. Organ. Stud. 2003, 24, 403–441. [Google Scholar] [CrossRef]

- Sancho, M.P.L.; Martínez-Martínez, D.; Jorge, M.L.; Madueño, J.H. Understanding the link between socially responsible human resource management and competitive performance in SMEs. Pers. Rev. 2018, 47, 1211–1243. [Google Scholar] [CrossRef]

- Canh, N.T.; Liem, N.T.; Thu, P.A.; Khuong, N.V. The Impact of Innovation on the Firm Performance and Corporate Social Responsibility of Vietnamese Manufacturing Firms. Sustainability 2019, 11, 3666. [Google Scholar] [CrossRef] [Green Version]

- Zhu, Q.; Zou, F.; Zhang, P. The role of innovation for performance improvement through corporate social responsibility practices among small and medium-sized suppliers in China. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 341–350. [Google Scholar] [CrossRef]

- Chege, S.M.; Wang, D. The influence of technology innovation on SME performance through environmental sustainability practices in Kenya. Technol. Soc. 2020, 60, 101210. [Google Scholar] [CrossRef]

- Fraaije, A.; Steven, F. Synthesizing an implementation framework for responsible research and innovation. J. Responsible Innov. 2020, 7, 113–137. [Google Scholar] [CrossRef] [Green Version]

- Stoian, C.; Gilman, M. Corporate social responsibility that ‘pays’: A strategic approach to CSR for SMEs. J. Small Bus. Manag. 2017, 55, 5–31. [Google Scholar] [CrossRef]

- El Baz, J.; Laguir, I.; Marais, M.; Staglianò, R. Influence of national institutions on the corporate social responsibility practices of small- and medium-sized enterprises in the food-processing industry: Differences between France and Morocco. J. Bus. Ethics 2016, 134, 117–133. [Google Scholar] [CrossRef]

- Li, N.; Toppinen, A.; Lantta, M. Managerial perceptions of smes in the wood industry supply chain on corporate responsibility and competitive advantage: Evidence from China and Finland. J. Small Bus. Manag. 2016, 54, 162–186. [Google Scholar] [CrossRef]

- Jain, P.; Vyas, V.; Roy, A. Exploring the mediating role of intellectual capital and competitive advantage on the relation between CSR and financial performance in SMEs. Soc. Responsib. J. 2017, 13, 1–23. [Google Scholar] [CrossRef]

- Cegarra-Navarro, J.-G.; Reverte, C.; Gómez-Melero, E.; Wensley, A.K. Linking social and economic responsibilities with financial performance: The role of innovation. Eur. Manag. J. 2016, 34, 530–539. [Google Scholar] [CrossRef]

- Sáez-Martínez, F.J.; Díaz-García, C.; González-Moreno, Á. Factors Promoting Environmental Responsibility in European SMEs: The Effect on Performance. Sustainability 2016, 8, 898. [Google Scholar] [CrossRef] [Green Version]

- Tang, Z. Stakeholder corporate social responsibility orientation congruence, entrepreneurial orientation and environmental performance of Chinese small and medium-sized enterprises. Br. J. Manag. 2018, 29, 634–651. [Google Scholar] [CrossRef]

- Reverte, C.; Gómez-Melero, E.; Cegarra-Navarro, J.-G. The influence of corporate social responsibility practices on organizational performance: Evidence from Eco-Responsible Spanish firms. J. Clean. Prod. 2016, 112, 2870–2884. [Google Scholar] [CrossRef]

- European Commission. Implementing the Partnership for Growth and Jobs: Making Europe a Pole of Excellence on Corporate Social Responsibility; European Commission: Brussels, Belgium, 2006. [Google Scholar]

- Bartolacci, F.; Caputo, A.; Soverchia, M. Sustainability and financial performance of small and medium sized enterprises: A bibliometric and systematic literature review. Bus. Strategy Environ. 2019, 29, 1297–1309. [Google Scholar] [CrossRef]

- Cantele, S.; Zardini, A. Is sustainability a competitive advantage for small businesses? An empirical analysis of possible mediators in the sustainability–financial performance relationship. J. Clean. Prod. 2018, 182, 166–176. [Google Scholar] [CrossRef]

- McWilliams, A.; Siegel, D. Corporate social responsibility and financial performance: Correlation or misspecification? Strategy Manag. J. 2000, 21, 603–609. [Google Scholar] [CrossRef]

- Muñoz-Pascual, L.; Curado, C.; Galende, J. The triple bottom line on sustainable product innovation performance in SMEs: A mixed methods approach. Sustainability 2019, 11, 1689. [Google Scholar] [CrossRef] [Green Version]

- Hull, C.E.; Rothenberg, S. Firm performance: The interactions of corporate social performance with innovation and industry differentiation. Strateg. Manag. J. 2008, 29, 781–789. [Google Scholar] [CrossRef]

- Hoogendoorn, B.; Guerra, D.; Van Der Zwan, P. What drives environmental practices of SMEs? Small Bus. Econ. 2015, 44, 759–781. [Google Scholar] [CrossRef]

- Hadj, T.B. Effects of corporate social responsibility towards stakeholders and environmental management on responsible innovation and competitiveness. J. Clean. Prod. 2020, 250, 119490. [Google Scholar] [CrossRef]

- Bakos, J.; Siu, M.; Orengo, A.; Kasiri, N. An analysis of environmental sustainability in small & medium-sized enterprises: Patterns and trends. Bus. Strategy Environ. 2020, 29, 1285–1296. [Google Scholar]

- Lee, J.W.; Kim, Y.M. Antecedents of adopting corporate environmental responsibility and green practices. J. Bus. Ethics 2018, 148, 397–409. [Google Scholar] [CrossRef]

- Battaglia, M.; Testa, F.; Bianchi, L.; Iraldo, F.; Frey, M. Corporate social responsibility and competitiveness within SMEs of the fashion industry: Evidence from Italy and France. Sustainability 2014, 6, 872–893. [Google Scholar] [CrossRef] [Green Version]

- Iraldo, F.; Testa, F.; Lanzini, P.; Battaglia, M. Greening competitiveness for hotels and restaurants. J. Small Bus. Enterp. Dev. 2017, 24, 607–628. [Google Scholar] [CrossRef]

- Hsu, C.-L.; Lu, H.-P.; Hsu, H.-H. Adoption of the mobile Internet: An empirical study of multimedia message service (MMS). Omega 2007, 35, 715–726. [Google Scholar] [CrossRef]

- Ikram, M.; Sroufe, R.; Mohsin, M.; Solangi, Y.A.; Shah, S.Z.A.; Shahza, F. Does CSR influence firm performance? A longitudinal study of SME sectors of Pakistan. J. Glob. Responsib. 2019, 11, 27–53. [Google Scholar] [CrossRef]

- Prashar, A. A bibliometric and content analysis of sustainable development in small and medium-sized enterprises. J. Clean. Prod. 2020, 245, 118665. [Google Scholar] [CrossRef]

- Waldron, T.L.; Navis, C.; Karam, E.P.; Markman, G.D. Toward a theory of activist-driven responsible innovation: How activists pressure firms to adopt more responsible practices. J. Manag. Stud. 2019. [Google Scholar] [CrossRef]

| Coding | |

|---|---|

| 1: Dimensions Anticipation Reflexiveness Inclusion Responsiveness Know ledge Management 2: Firm performance Sales growth Profitability Financial indicators Market share Customer satisfaction Innovation performance RI performance Environmental sustainability Social sustainability Diversity and inclusion Anticipation and reflection | 3: Contingent variables Firm size Type of industry Firm age Country Corporate strategy Learning orientation Employee’s commitment Relational marketing 4: Main Players Clients/Customers Employees Environment Suppliers Community Owners/shareholders R&D Government Competitors Funding agencies/Investors Alliances |

| Journal | Publications | Citations |

|---|---|---|

| Journal of Cleaner Production | 14 | 1608 |

| Journal of Business Ethics | 14 | 2095 |

| Sustainability | 14 | 187 |

| Business Strategy and The Environment | 9 | 719 |

| Corporate Social Responsibility and Environmental Management | 6 | 503 |

| Journal of Responsible Innovation | 4 | 25 |

| Journal of Small Business Management | 3 | 38 |

| Strategic Management Journal | 2 | 1764 |

| Research Policy | 2 | 1612 |

| European Management Journal | 2 | 1076 |

| Journal of Management Studies | 2 | 159 |

| Science and Engineering Ethics | 2 | 152 |

| Industrial Management & Data Systems | 2 | 26 |

| Global Business Review | 2 | 15 |

| Technological Forecasting and Social Change | 2 | 15 |

| British Journal of Management | 2 | 7 |

| Firm Performance |

| Sales growth |

| Profitability |

| Financial indicators |

| Market share |

| Customer satisfaction |

| Innovation performance |

| Benefits/utility |

| RI Performance |

| Environmental sustainability |

| Social sustainability |

| Diversity and inclusion |

| Anticipation and reflection |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gonzales-Gemio, C.; Cruz-Cázares, C.; Parmentier, M.J. Responsible Innovation in SMEs: A Systematic Literature Review for a Conceptual Model. Sustainability 2020, 12, 10232. https://doi.org/10.3390/su122410232

Gonzales-Gemio C, Cruz-Cázares C, Parmentier MJ. Responsible Innovation in SMEs: A Systematic Literature Review for a Conceptual Model. Sustainability. 2020; 12(24):10232. https://doi.org/10.3390/su122410232

Chicago/Turabian StyleGonzales-Gemio, Carla, Claudio Cruz-Cázares, and Mary Jane Parmentier. 2020. "Responsible Innovation in SMEs: A Systematic Literature Review for a Conceptual Model" Sustainability 12, no. 24: 10232. https://doi.org/10.3390/su122410232

APA StyleGonzales-Gemio, C., Cruz-Cázares, C., & Parmentier, M. J. (2020). Responsible Innovation in SMEs: A Systematic Literature Review for a Conceptual Model. Sustainability, 12(24), 10232. https://doi.org/10.3390/su122410232