Asymmetric Dependence between Oil Prices and Maritime Freight Rates: A Time-Varying Copula Approach

Abstract

:1. Introduction

2. Literature Review

3. Methodology

4. Empirical Analysis and Results

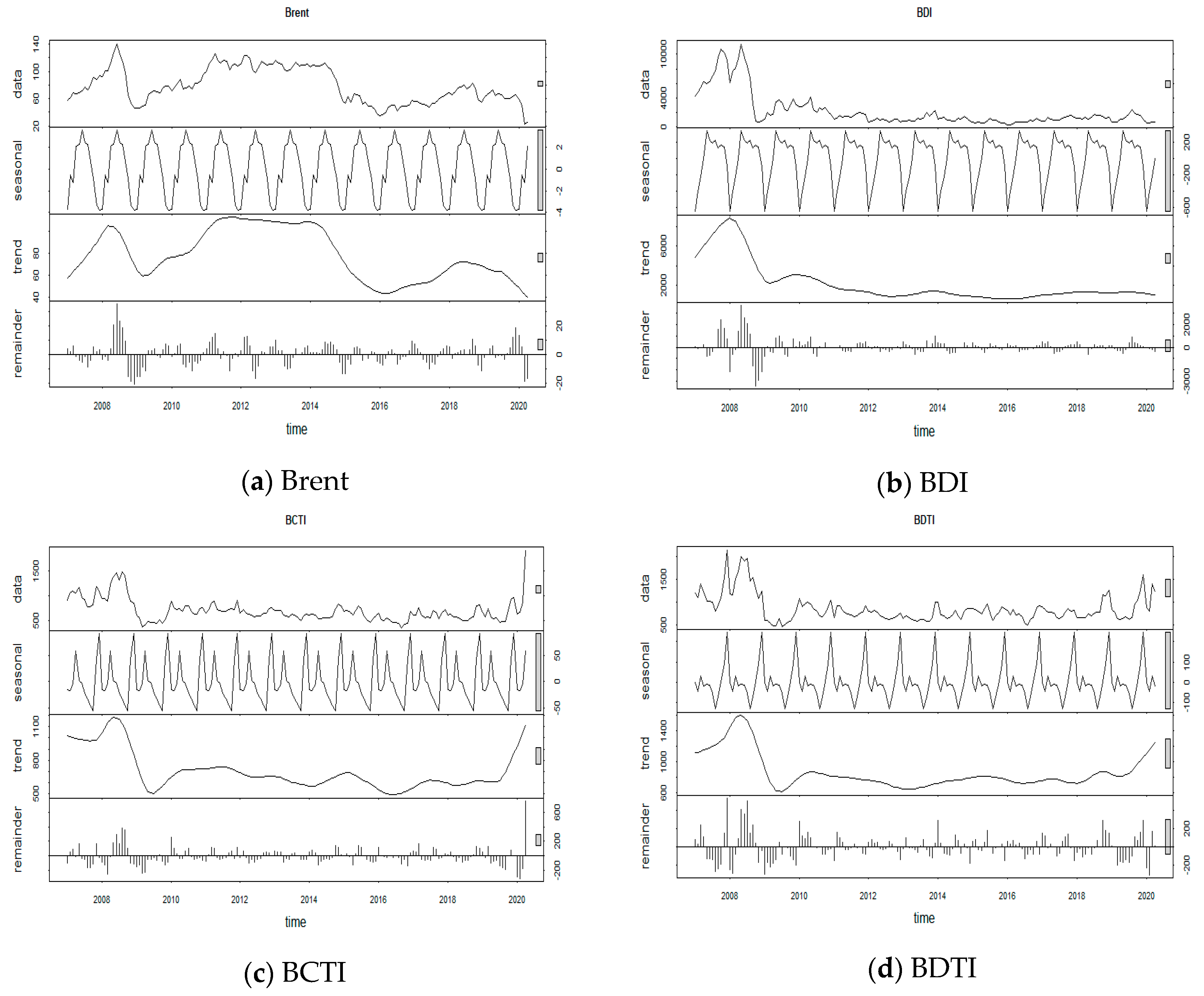

4.1. Sample Data

4.2. Decomposition

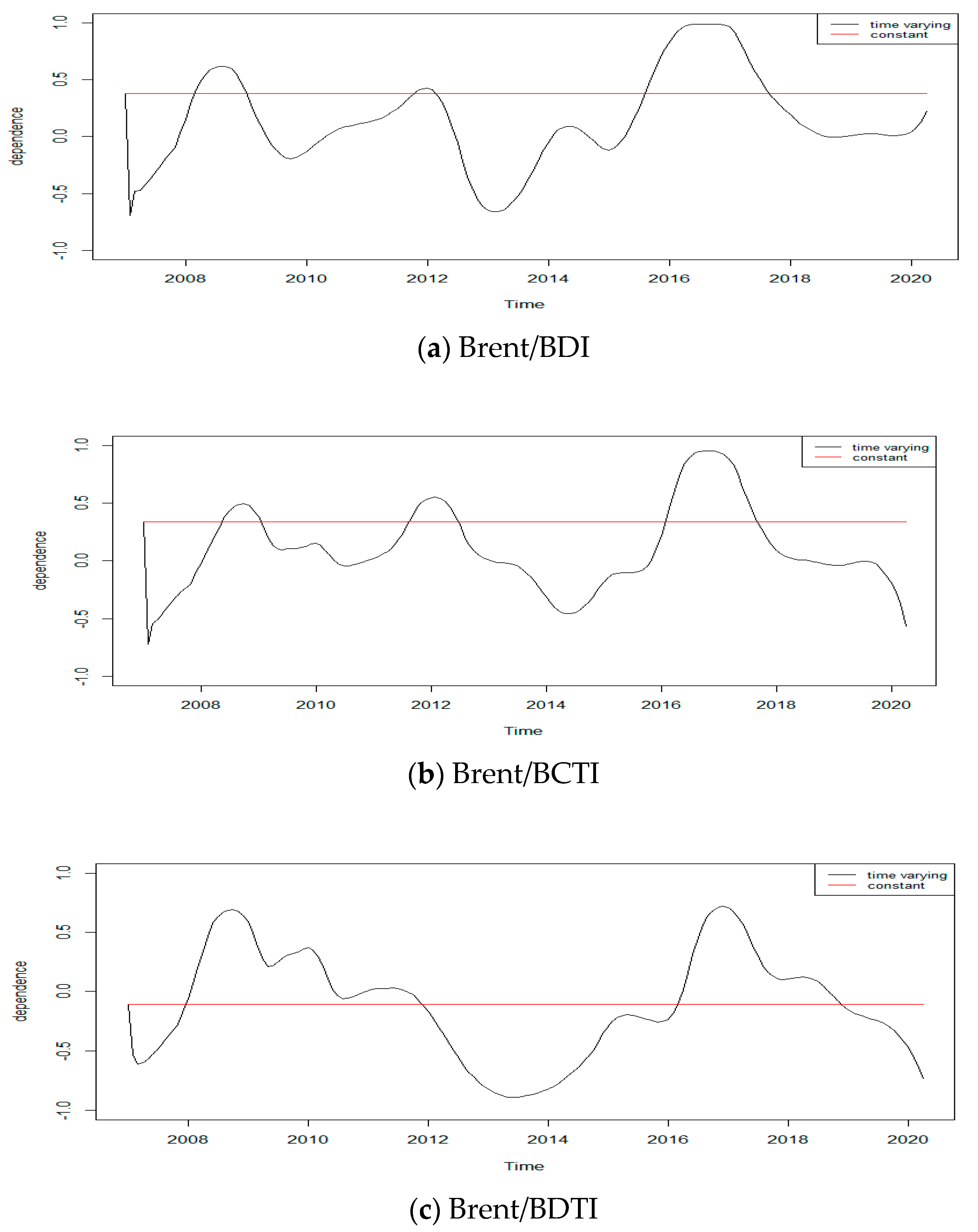

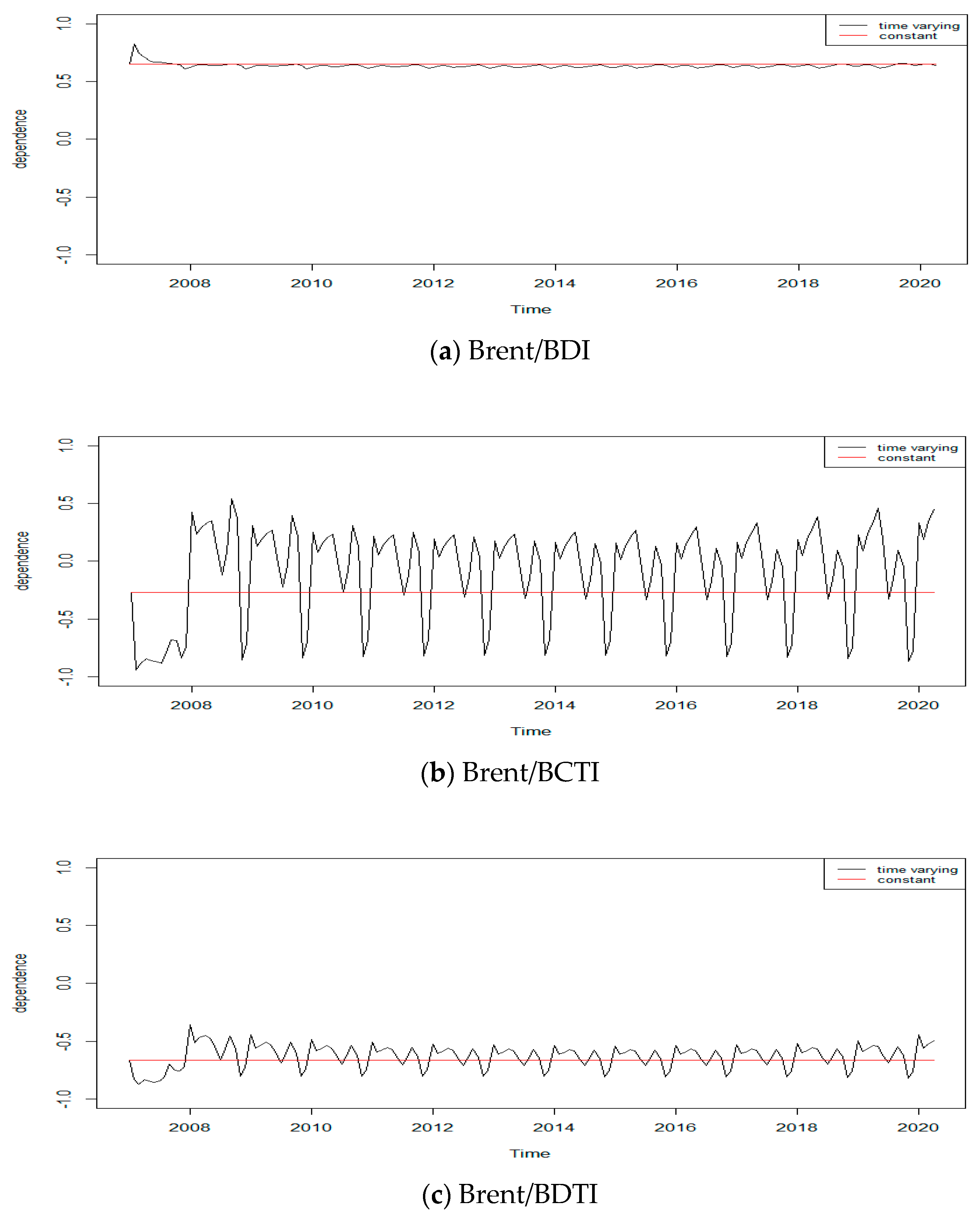

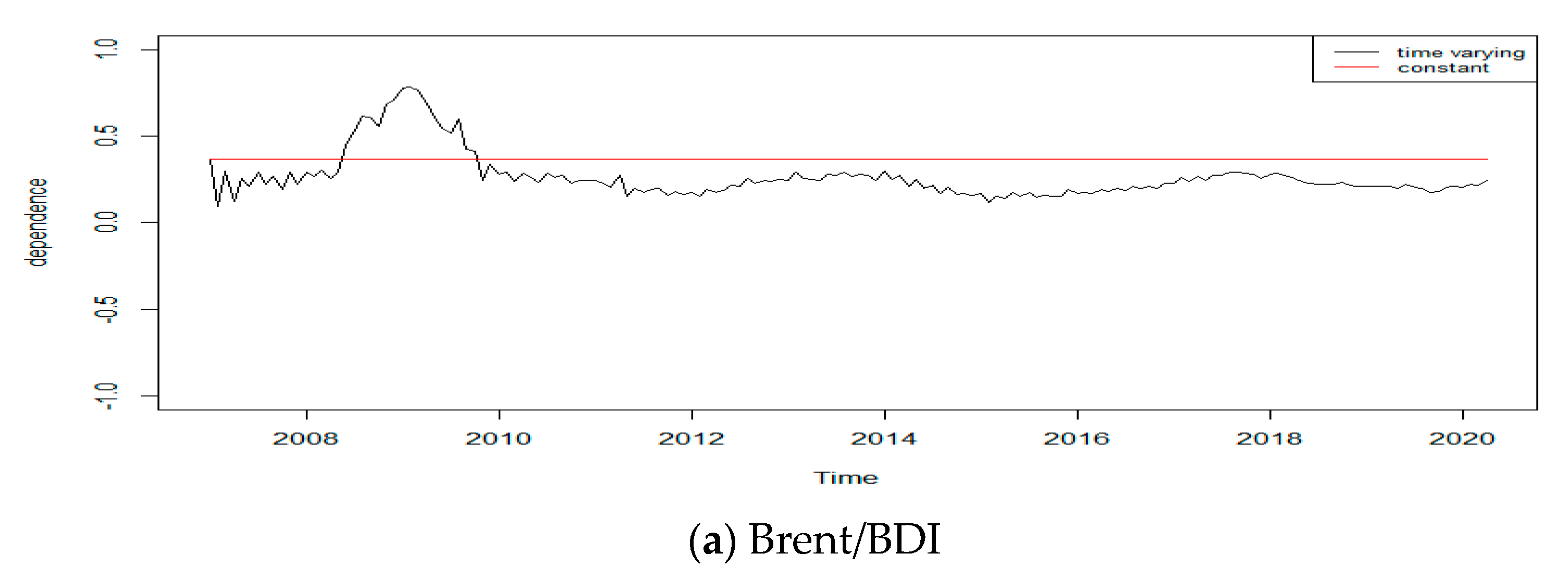

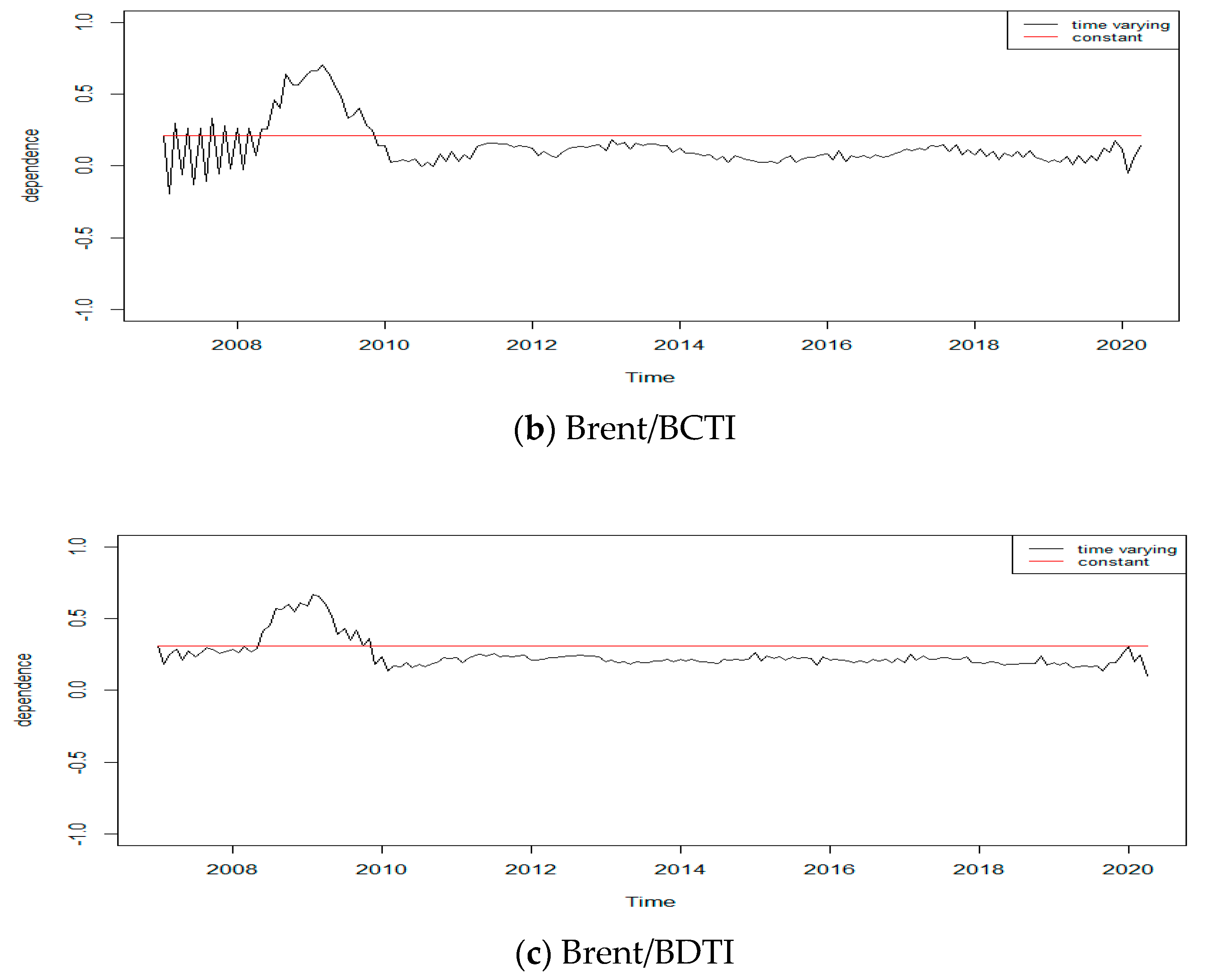

4.3. Time-Varying Dependence Results

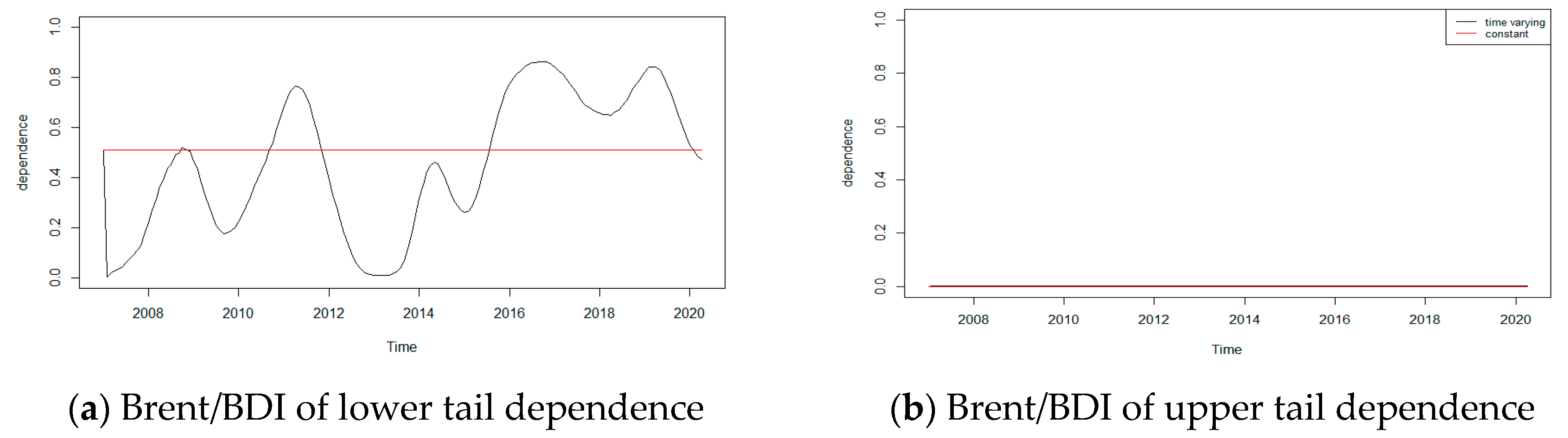

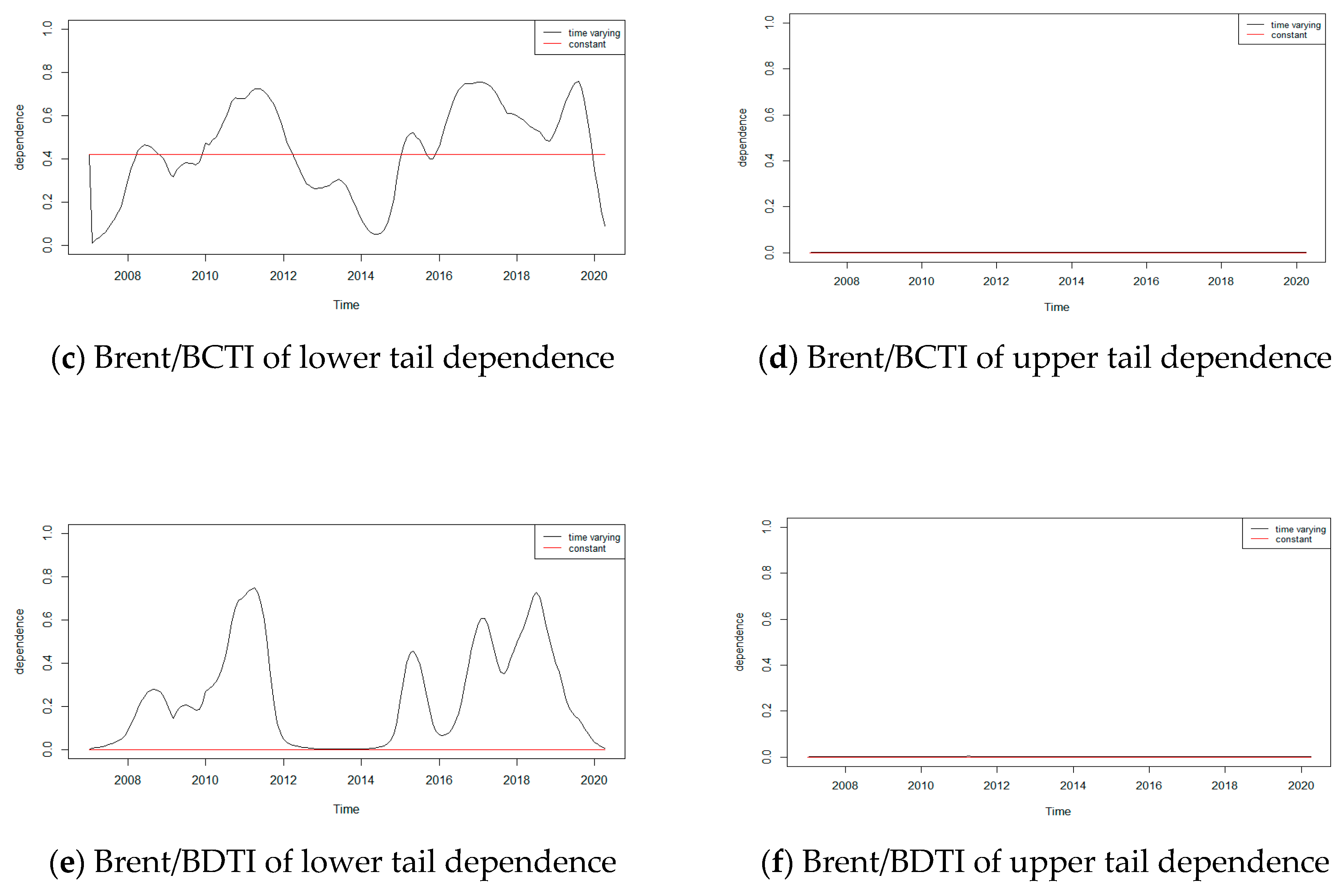

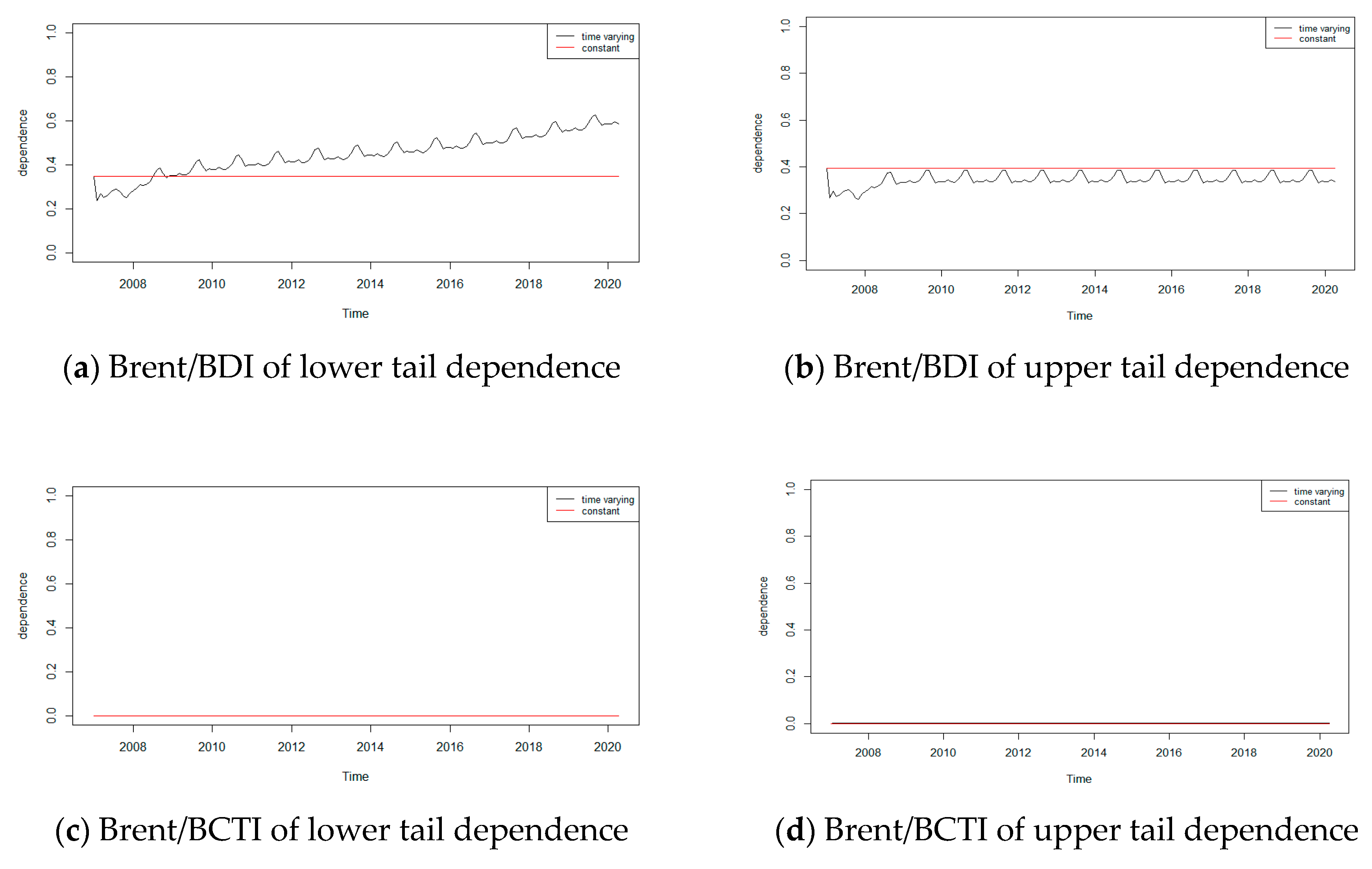

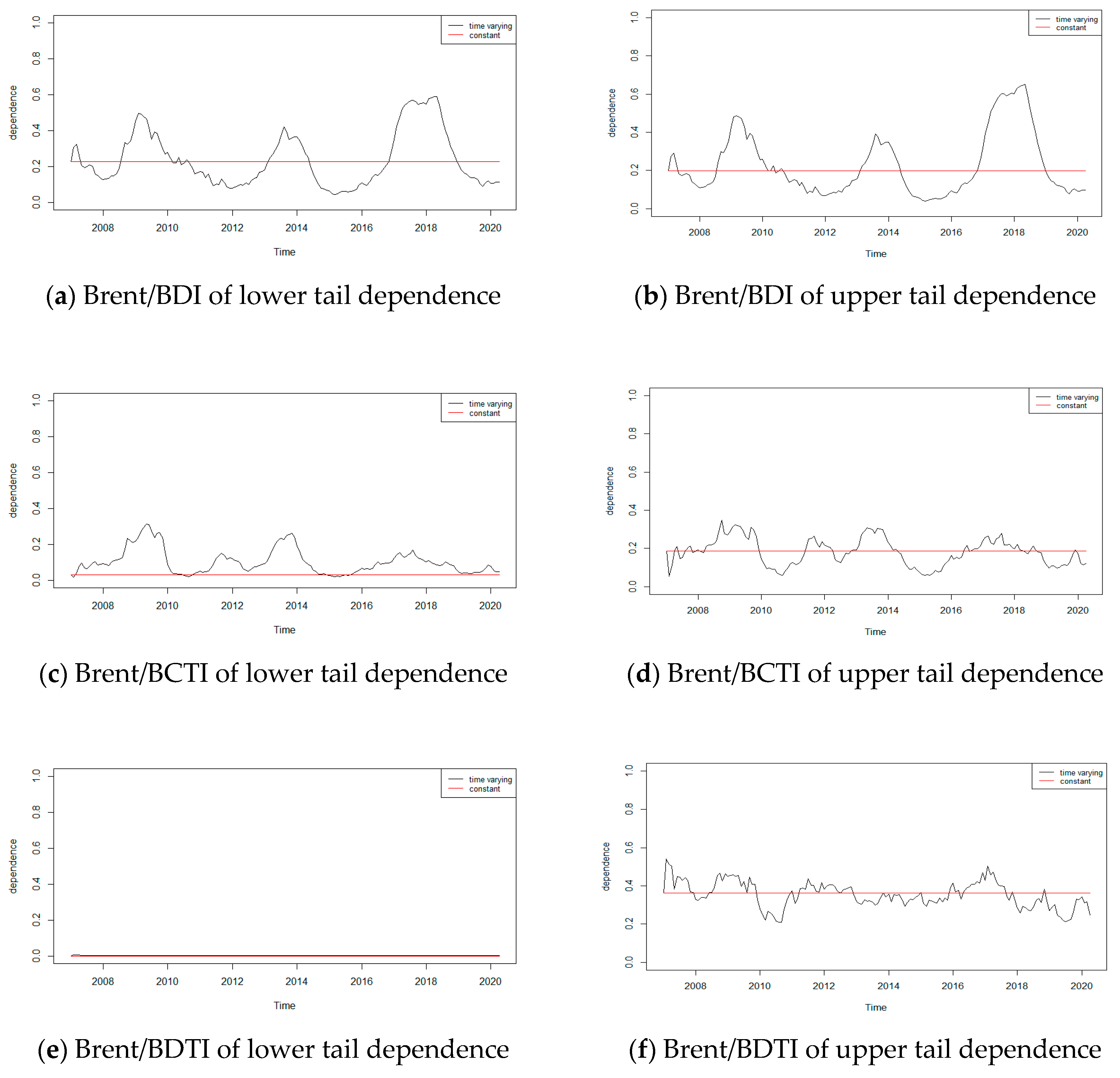

4.4. Time-Varying Tail Dependence Results

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- UNCTAD. Review of Maritime Transport 2017; United Nations: New York, NY, USA, 2017. [Google Scholar]

- Kutin, N.; Moussa, Z.; Vallée, T. Factors Behind the Freight Rates in the Liner Shipping Industry. Working Papers Halshs-01828633, HAL. 2018. Available online: https://halshs.archives-ouvertes.fr/halshs-01828633 (accessed on 8 August 2020).

- UNCTAD. Maritime Transport; Data Center, UNCTADstat: Geneva, Switzerland, 2019. [Google Scholar]

- Lyridis, D.V.; Zacharioudakis, P.G. Liquid bulk shipping. The Black. Com. to Mari. Econ. 2012, 205–229. [Google Scholar]

- Stopford, M. Maritime Economics, 3rd ed.; Routledge: Oxford, UK, 2009. [Google Scholar]

- Kavussanos, M.G. Price risk modelling of different size vessels in the tanker industry using autoregressive conditional heterskedastic (ARCH) models. Logist. Transp. Rev. 1996, 32, 161. [Google Scholar]

- Glen, D.R.; Martin, B.T. A survey of the modelling of dry bulk and tanker markets. Res. Transp. Econ. 2005, 12, 19–64. [Google Scholar] [CrossRef]

- Notteboom, T.E.; Vernimmen, B. The effect of high fuel costs on liner service configuration in container shipping. J. Transp. Geogr. 2009, 17, 325–337. [Google Scholar] [CrossRef]

- Poulakidas, A.; Joutz, F. Exploring the link between oil prices and tanker rates. Marit. Policy Manag. 2009, 36, 215–233. [Google Scholar] [CrossRef]

- El-Masry, A.A.; Olugbode, M.; Pointon, J. The exposure of shipping firms’ stock returns to financial risks and oil prices: A global perspective. Marit. Policy Manag. 2010, 37, 453–473. [Google Scholar] [CrossRef] [Green Version]

- UNCTAD. Oil Prices and Maritime Freight Rates: An Empirical Investigation; UNCTAD/DTL/TLB/2009/2; UNCTAD: Geneva, Switzerland, 2010. [Google Scholar]

- Shi, W.; Yang, Z.; Li, K.X. The impact of crude oil price on the tanker market. Marit. Policy Manag. 2013, 40, 309–322. [Google Scholar] [CrossRef]

- Yang, Y.; Liu, C.; Sun, X.; Yang, J.L. Spillover effect of international crude oil market on tanker market. Int. J. Glob. Energy Issues 2015, 38, 257–277. [Google Scholar] [CrossRef]

- Gavriilidis, K.; Kambouroudis, D.S.; Tsakou, K.; Tsouknidis, D.A. Volatility forecasting across tanker freight rates: The role of oil price shocks. Transp. Res. Part E Logist. Transp. Rev. 2018, 118, 376–391. [Google Scholar] [CrossRef] [Green Version]

- Maitra, D.; Chandra, S.; Dash, S.R. Liner shipping industry and oil price volatility: Dynamic connectedness and portfolio diversification. Transp. Res. Part E Logist. Transp. Rev. 2020, 138, 101962. [Google Scholar] [CrossRef]

- Siddiqui, A.W.; Basu, R. An empirical analysis of relationships between cyclical components of oil price and tanker freight rates. Energy 2020, 200, 117494. [Google Scholar] [CrossRef]

- Michail, N.A.; Melas, K.D. Shipping markets in turmoil: An analysis of the Covid-19 outbreak and its implications. Transp. Res. Interdiscip. Perspect. 2020, 7, 100178. [Google Scholar] [CrossRef]

- Angelopoulos, J.; Sahoo, S.; Visvikis, I.D. Commodity and transportation economic market interactions revisited: New evidence from a dynamic factor model. Transp. Res. Part E Logist. Transp. Rev. 2020, 133, 101836. [Google Scholar] [CrossRef]

- Alizadeh, A.H.; Nomikos, N.K. Cost of carry, causality and arbitrage between oil futures and tanker freight markets. Transp. Res. Part E Logist. Transp. Rev. 2004, 40, 297–316. [Google Scholar] [CrossRef]

- Zhang, Y. Investigating dependencies among oil price and tanker market variables by copula-based multivariate models. Energy 2018, 161, 435–446. [Google Scholar] [CrossRef]

- Li, K.X.; Xiao, Y.; Chen, S.L.; Zhang, W.; Du, Y.; Shi, W. Dynamics and interdependencies among different shipping freight markets. Marit. Policy Manag. 2018, 45, 837–849. [Google Scholar] [CrossRef]

- Bai, X.; Lam, J.S.L. A copula-GARCH approach for analyzing dynamic conditional dependency structure between liquefied petroleum gas freight rate, product price arbitrage and crude oil price. Energy Econ. 2019, 78, 412–427. [Google Scholar] [CrossRef]

- Sun, X.; Liu, C.; Wang, J.; Li, J. Assessing the extreme risk spillovers of international commodities on maritime markets: A GARCH-Copula-CoVaR approach. Int. Rev. Financ. Anal. 2020, 68, 101453. [Google Scholar] [CrossRef]

- Reboredo, J.C.; Ugolini, A. Downside/upside price spillovers between precious metals: A vine copula approach. N. Am. J. Econ. Financ. 2015, 34, 84–102. [Google Scholar] [CrossRef]

- Jondeau, E. Asymmetry in tail dependence in equity portfolios. Comput. Stat. Data Anal. 2016, 100, 351–368. [Google Scholar] [CrossRef]

- Patton, A.J. Modelling asymmetric exchange rate dependence. Int. Econ. Rev. 2006, 47, 527–556. [Google Scholar] [CrossRef]

- Clarksons Research, Shipping Intelligence Weekly, No. 1224. 2016. Available online: https://www.crsl.com/acatalog/shipping-intelligence-weekly.html (accessed on 15 August 2020).

- Cleveland, R.B.; Cleveland, W.S.; McRae, J.E.; Terpenning, I. STL: A seasonal-trend decomposition. J. Off. Stat. 1990, 6, 3–73. [Google Scholar]

- An, J.; Mikaylov, A. Russian energy projects in South Africa. J. Energy S. Afr. 2020, 31, 58–64. [Google Scholar] [CrossRef]

- Yumashev, A.; Ślusarczyk, B.; Kondrashev, S.; Mikhaylov, A. Global indicators of sustainable development: Evaluation of the influence of the human development index on consumption and quality of energy. Energies 2020, 13, 2768. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Panel A. Trend | |||||

|---|---|---|---|---|---|

| AIC | |||||

| Brent/BDI | 0.0079 (0.2939) | 1.5817 *** (0.3354) | −0.4983 (0.9188) | 14.9997 ** (7.4949) | −94.1023 |

| Brent/BCTI | −1.1610 *** (0.3191) | 1.2494 *** (0.4060) | −0.3961 (1.1687) | 14.9999 * (7.9541) | −67.4002 |

| Brent/BDTI | −0.1695 (0.1547) | 1.1797 ** (0.4890) | 0.6775 (0.8829) | 14.9997 ** (5.9410) | −63.5371 |

| Panel B. Seasonal | |||||

| Brent/BDI | 0.1912 (1.9665) | 0.1532 *** (0.0231) | 0.0997 (3.3384) | 5.0000 *** (0.8740) | −74.0731 |

| Brent/BCTI | −2.0283 *** (0.3049) | −4.4851 *** (0.9144) | 0.2443 (0.3730) | 5.0000 *** (1.0342) | −57.2134 |

| Brent/BDTI | −3.6848 *** (1.1416) | −1.7579 ** (0.7629) | −0.9887 (1.1614) | 5.0000 *** (1.2499) | −98.3152 |

| Panel C. Remainder | |||||

| Brent/BDI | 0.7825 * (0.4664) | 0.4083 ** (0.1985) | −1.6808 ** (0.6709) | 5.0121 * (2.6340) | −40.5075 |

| Brent/BCTI | 0.3331 (0.4205) | 0.4560 * (0.2549) | −1.9655 *** (0.2342) | 3.6300 *** (1.4069) | −33.6880 |

| Brent/BDTI | 0.7411 * (0.4145) | 0.2796 (0.2135) | −1.6777 ** (0.8316) | 3.2386 *** (1.2523) | −35.0155 |

| Panel A. Trend | |||||

|---|---|---|---|---|---|

| Mean | Median | Maximum | Minimum | Std. Dev. | |

| Brent/BDI | 0.1415 | 0.0760 | 0.9911 | −0.6916 | 0.4017 |

| Brent/BCTI | 0.1050 | 0.0231 | 0.9560 | −0.7204 | 0.3564 |

| Brent/BDTI | −0.1114 | −0.1090 | 0.7205 | −0.8921 | 0.4449 |

| Panel B. Seasonal | |||||

| Brent/BDI | 0.6388 | 0.6370 | 0.8253 | 0.6125 | 0.0214 |

| Brent/BCTI | −0.0992 | 0.0342 | 0.5424 | −0.9430 | 0.4055 |

| Brent/BDTI | −0.6326 | −0.6128 | −0.3550 | −0.8711 | 0.1015 |

| Panel C. Remainder | |||||

| Brent/BDI | 0.2665 | 0.2328 | 0.7847 | 0.0943 | 0.1312 |

| Brent/BCTI | 0.1346 | 0.0950 | 0.7042 | −0.1955 | 0.1540 |

| Brent/BDTI | 0.2482 | 0.2178 | 0.6711 | 0.1026 | 0.1036 |

| Panel A. Trend | |||

|---|---|---|---|

| Brent/BDI | Brent/BCTI | Brent/BDTI | |

| AIC | −50.3479 | −29.5475 | −41.2468 |

| −10.4073 (2.4523) *** | −9.9001 (2.8714) *** | −4.9053 (1.8031) *** | |

| −0.5923 (2.1069) | −9.4402 (5.3444) * | −9.9836 (2.1519) *** | |

| 0.0045 (1.0001) | 0.1998 (0.9679) | −1.4274 (0.0571) *** | |

| 5.3496 (0.0829) *** | 3.2528 (0.7102) *** | 1.2914 (0.0393) *** | |

| −14.3559 (3.6421) *** | −9.9999 (5.3147) * | −9.9999 (0.0754) *** | |

| −3.8566 (0.4930) *** | −2.3200 (0.7949) *** | 1.1606 (0.0453) *** | |

| AIC | −114.9619 | −76.7813 | −17.8445 |

| Panel B. Seasonal | |||

| −2.8822 (6.0745) | −15.4850 (228.2767) | −15.9229 (44.1790) | |

| 4.9929 (30.2431) | −1.9252 (67.1816) | −0.0126 (1.1915) | |

| 3.7201 (1.8230) ** | 0.0063 (1.1358) | 0.0350 (2.0439) | |

| −2.9914 (5.2964) | −14.3271 (60.4751) | −15.2534 (65.6691) | |

| 4.9950 (27.8251) | −1.0149 (20.7762) | −0.7769 (39.5632) | |

| 4.0796 (0.2375) *** | 0.0093 (1.0463) | 0.0305 (1.8479) | |

| AIC | −76.8316 | −5.5420 | 2.3875 |

| Panel C. Remainder | |||

| −0.8485 (1.1235) | −0.3306 (5.3986) | 1.2178 (1.4987) | |

| −4.9999 (4.1836) | −4.9997 (8.7713) | −4.9985 (6.0124) | |

| 3.2467 (1.3242) ** | 0.7359 (16.8868) | −1.6328 (2.8994) | |

| −0.6895 (0.7630) | −1.4432 (3.6187) | −4.9984 (4.7115) | |

| −5.0000 (3.0861) | −4.9997 (12.5020) | −4.9975 (7.4477) | |

| 2.8619 (0.8451) *** | 4.6257 (5.6482) | −0.1557 (1.0587) | |

| Panel A. Lower Tail Dependence | |||||

|---|---|---|---|---|---|

| Mean | Median | Maximum | Minimum | Std. Dev. | |

| Brent/BDI | 0.4602 | 0.4637 | 0.8630 | 0.0033 | 0.2699 |

| Brent/BCTI | 0.4467 | 0.4624 | 0.7594 | 0.0091 | 0.2087 |

| Brent/BDTI | 0.2432 | 0.1908 | 0.7476 | 0.0000 | 0.2281 |

| Panel B. Upper Tail Dependence | |||||

| Brent/BDI | 0.0010 | 0.0010 | 0.0010 | 0.0000 | 0.0000 |

| Brent/BCTI | 0.0010 | 0.0010 | 0.0010 | 0.0000 | 0.0000 |

| Brent/BDTI | 0.0015 | 0.0013 | 0.0035 | 0.0000 | 0.0000 |

| Panel A. Lower Tail Dependence | |||||

|---|---|---|---|---|---|

| Mean | Median | Maximum | Minimum | Std. Dev. | |

| Brent/BDI | 0.4469 | 0.4489 | 0.6258 | 0.2372 | 0.0882 |

| Brent/BCTI | 0.0009 | 0.0010 | 0.0010 | 0.0000 | 0.0000 |

| Brent/BDTI | 0.0009 | 0.0010 | 0.0010 | 0.0000 | 0.0000 |

| Panel B. Upper Tail Dependence | |||||

| Brent/BDI | 0.3437 | 0.3388 | 0.3940 | 0.2626 | 0.0256 |

| Brent/BCTI | 0.0009 | 0.0010 | 0.0010 | 0.0000 | 0.0000 |

| Brent/BDTI | 0.0000 | 0.0010 | 0.0010 | 0.0000 | 0.0000 |

| Panel A. Lower Tail Dependence | |||||

|---|---|---|---|---|---|

| Mean | Median | Maximum | Minimum | Std. Dev. | |

| Brent/BDI | 0.2390 | 0.1937 | 0.5897 | 0.0448 | 0.1511 |

| Brent/BCTI | 0.1033 | 0.0882 | 0.3122 | 0.0182 | 0.0701 |

| Brent/BDTI | 0.0030 | 0.0028 | 0.0060 | 0.0000 | 0.0008 |

| Panel B. Upper Tail Dependence | |||||

| Brent/BDI | 0.2283 | 0.1708 | 0.6501 | 0.0385 | 0.1643 |

| Brent/BCTI | 0.1827 | 0.1878 | 0.3487 | 0.0533 | 0.0710 |

| Brent/BDTI | 0.3540 | 0.3523 | 0.5402 | 0.2106 | 0.0677 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Choi, K.-H.; Yoon, S.-M. Asymmetric Dependence between Oil Prices and Maritime Freight Rates: A Time-Varying Copula Approach. Sustainability 2020, 12, 10687. https://doi.org/10.3390/su122410687

Choi K-H, Yoon S-M. Asymmetric Dependence between Oil Prices and Maritime Freight Rates: A Time-Varying Copula Approach. Sustainability. 2020; 12(24):10687. https://doi.org/10.3390/su122410687

Chicago/Turabian StyleChoi, Ki-Hong, and Seong-Min Yoon. 2020. "Asymmetric Dependence between Oil Prices and Maritime Freight Rates: A Time-Varying Copula Approach" Sustainability 12, no. 24: 10687. https://doi.org/10.3390/su122410687

APA StyleChoi, K. -H., & Yoon, S. -M. (2020). Asymmetric Dependence between Oil Prices and Maritime Freight Rates: A Time-Varying Copula Approach. Sustainability, 12(24), 10687. https://doi.org/10.3390/su122410687