The Influence of Internet Finance on the Sustainable Development of the Financial Ecosystem in China

Abstract

:1. Introduction

2. Literature Review

3. Data and Methodology

3.1. Descriptive Statistics

3.2. Stationarity Test

3.3. Univariate GARCH Modeling

3.4. The DCC-GARCH-BEKK Models

- H1: , indicating that there is no volatility spillover from the variable i to the variable j.

- H2: , indicating that there is no volatility spillover from the variable j to the variable i.

- H3: and , indicating the absence of the mutual volatility spillover effect between the variables i and j.

4. Empirical Analysis

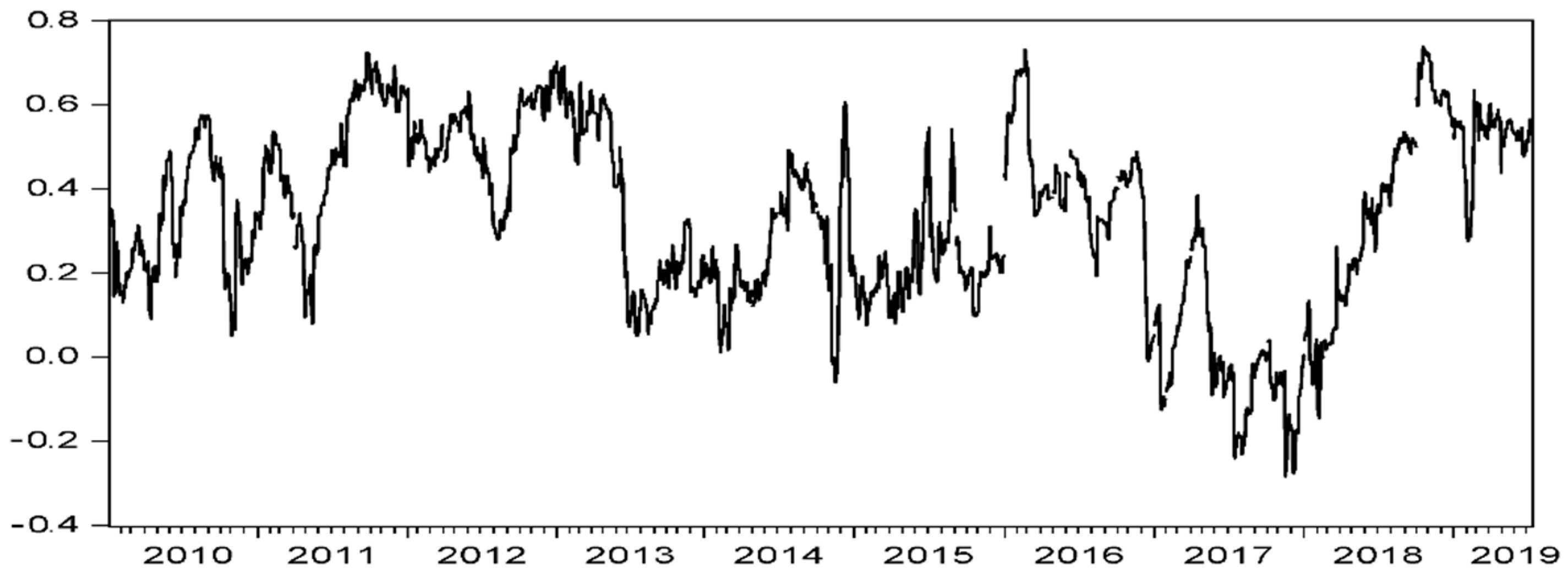

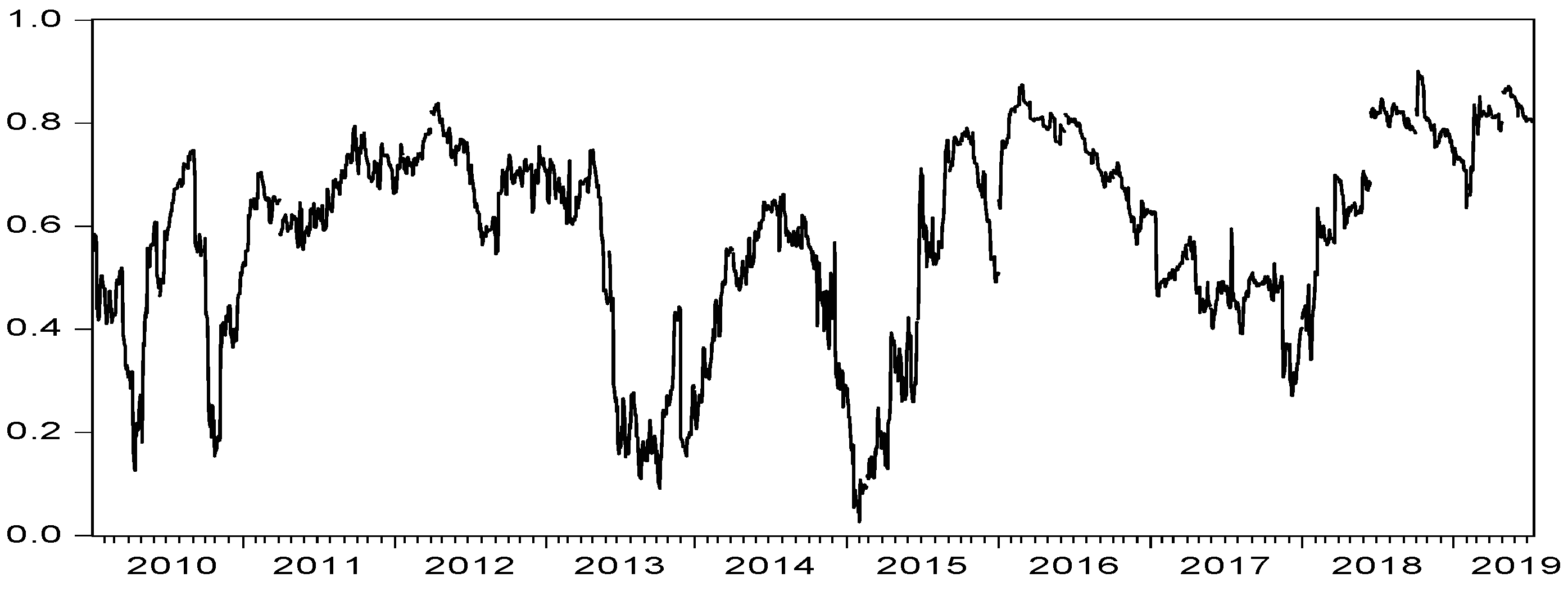

4.1. Dynamic Correlation Coefficient Test between Internet Finance and the Traditional Financial Industries

4.2. Risk Transmission (Volatility Spillover) Effect Influence of Internet Finance on the Traditional Financial Ecosystem

4.2.1. Risk Transmission (Volatility Spillover) Effect between the Ecological Subjects of the Traditional Financial Industries

4.2.2. The Model’s Robustness Check

4.2.3. Risk Transmission (Volatility Spillover) Effect between All Four Financial Markets Based on the Relevance Perspective

4.2.4. The Model’s Robustness Check

4.2.5. The Change in the Risk Transmission (Volatility Spillover) Effect between the Traditional Financial Industries after the Introduction of Internet Finance

5. Discussion

6. Conclusions

6.1. Theoretical Implication

6.2. Practical Implications

6.3. Limitations

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Monnet, E.; Pagliari, S.; Vallee, S. Beyond “financial repression” and “capture of regulation” recomposition of European financial ecosystems after the crisis. Actes De La Rech. En Sci. Soc. 2019, 229, 14–33. [Google Scholar]

- Hendrikse, R.; van Meeteren, M.; Bassens, D. Strategic coupling between finance, technology and the state: Cultivating a Fintech ecosystem for incumbent finance. Environ. Planing A Econ. Space 2019, 11, 0308518X19887967. [Google Scholar] [CrossRef]

- De Luca, V.V.; Margherita, A.; Passiante, G. Crowd-funding: A systemic framework of benefits. Int. J. Entrep. Behav. Res. 2019, 25, 1321–1339. [Google Scholar] [CrossRef]

- Lee, K.H.; Kim, D.H. A peer-to-peer (P2P) platform business model: The case of Airbnb. Serv. Bus. 2019, 13, 647–669. [Google Scholar] [CrossRef]

- Burtch, G.; Ghose, A.; Wattal, S. The hidden cost of accommodating crowdfunder privacy preferences: A randomized field experiment. Manag. Sci. 2015, 61, 949–962. [Google Scholar] [CrossRef] [Green Version]

- Dorfleitner, G.; Priberny, C.; Schuster, S.; Stoiber, J.; Weber, M.; Castro, I.; Kammler, J. Description-text related soft information in peer-to-peer lending–evidence from two leading European platforms. J. Bank. Financ. 2016, 64, 169–187. [Google Scholar] [CrossRef]

- Paravisini, D.; Rappoport, V.; Ravina, E. Risk aversion and wealth: Evidence from person-to-person lending Portfolios. Manag. Sci. 2016, 63, 279–297. [Google Scholar] [CrossRef] [Green Version]

- Liu, X.; Chen, J.; Wang, Y. The construction of Internet finance ecosystem--from the perspective of business ecosystem. Mod. Econ. Res. 2017, 4, 53–57. [Google Scholar]

- Chen, L.; Tan, Y. The development trend of the Internet financial ecosystem and its regulatory countermeasures. Financ. Econ. 2016, 3, 68. [Google Scholar]

- Huang, J.; Zhang, W.; Ruan, W. Spatial spillover and impact factors of the Internet finance development in China. Phys. A 2019, 527, 1–12. [Google Scholar] [CrossRef]

- Peter, G.; Robert, J.; Kauffman, C.P.; Bruce, W.W. Financial information systems and the fintech revolution. J. Manag. Inf. Syst. 2018, 35, 12–18. [Google Scholar]

- Sanjiv, R.D. The future of fintech. Financ. Manag. 2019, 48, 981–1007. [Google Scholar]

- Zhao, Q.; Pei-Hsuan, T.; Wang, J. Improving financial service innovation strategies for enhancing China’s banking industry competitive advantage during the fintech revolution: A hybrid MCDM model. Sustainability 2019, 11, 1419. [Google Scholar] [CrossRef] [Green Version]

- Sangmin, L. Evaluation of mobile application in User’s perspective: Case of P2P lending apps in fintech industry. KSII Trans. Internet Inf. Syst. 2017, 11, 1105–1117. [Google Scholar]

- Raza, S.A.; Hanif, N. Factors affecting Internet banking adoption among internal and external customers: A case of Pakistan. Int. J. Electron. Financ. 2013, 7, 82–96. [Google Scholar] [CrossRef] [Green Version]

- Berg, K.A.; Vu, N.T. International spillovers of US financial volatility. J. Int. Money Financ. 2019, 97, 19–34. [Google Scholar] [CrossRef]

- Gulzar, S.; Kayani, G.M.; Xiaofeng, H.; Ayub, U.; Rafique, A. Financial cointegration and spillover effect of global financial crisis: A study of emerging Asian financial markets. Ekon. Istraživanja Econ. Res. 2019, 32, 187–218. [Google Scholar] [CrossRef] [Green Version]

- Yoon, S.M.; Al Mamun, M.; Uddin, G.S.; Kang, S.H. Network connectedness and net spillover between financial and commodity markets. N. Am. J. Econ. Financ. 2019, 48, 801–818. [Google Scholar] [CrossRef]

- Gamba-Santamaria, S.; Gomez-Gonzalez, J.; Hurtado-Guarin, J.L.; Melo-Velandia, L.F. Volatility spillovers among global stock markets: Measuring total and directional effects. Empir. Econ. 2019, 56, 1581–1599. [Google Scholar] [CrossRef] [Green Version]

- Chen, R.; Chen, H.; Jin, C.; Wei, B.; Yu, L. Linkages and Spillover between Internet Finance and Traditional Finance: Evidence from China. Emerg. Mark. Financ. Trade 2019, 1–15. [Google Scholar] [CrossRef]

- Satish, K.; Ashis, K.P.; Aviral, K.T.; Sang, H.K. Correlations and volatility spillovers between oil, natural gas, and stock prices in India. Resour. Policy 2019, 62, 282–291. [Google Scholar]

- Aaron, D.S. Analyzing exchange rate uncertainty and bilateral export growth in China: A multivariate GARCH-based approach. Econ. Model. 2019, 82, 332–344. [Google Scholar]

- Vo, X.V.; Ellis, C. International financial integration: Stock return linkages and volatility transmission between Vietnam and advanced countries. Emerg. Mark. Rev. 2018, 36, 19–27. [Google Scholar] [CrossRef]

- de Oliveira, F.A.; Maia, S.F.; de Jesus, D.P.; Besarria, C.D.N. Which information matters to market risk spreading in Brazil? Volatility transmission modelling using MGARCH-BEKK, DCC, t-Copulas. N. Am. J. Econ. Financ. 2018, 45, 83–100. [Google Scholar] [CrossRef]

- Mumtaz, M.Z.; Smith, Z.A. Estimation of the spillover effect between patents and innovation using the GARCH-BEKK model. Pac. Econ. Rev. 2017, 22, 772–791. [Google Scholar] [CrossRef]

- Gomez-Gonzalez, J.E.; Rojas-Espinosa, W. Detecting contagion in Asian exchange rate markets using asymmetric DCC-GARCH and R-vine copulas. Econ. Syst. 2019, 43, 100717. [Google Scholar] [CrossRef] [Green Version]

- Cardona, L.; Gutiérrez, M.; Agudelo, D.A. Volatility transmission between US and Latin American stock markets: Testing the decoupling hypothesis. Res. Int. Bus. Financ. 2017, 39, 115–127. [Google Scholar] [CrossRef] [Green Version]

- Helmut, L. New Introduction to Multiple Time Series Analysis; Springer: Berlin/Heidelberg, Germany, 2005; Volume 83, pp. 109–110. [Google Scholar]

- Alfreedi, A.A. Shocks and volatility spillover between stock markets of developed countries and GCC stock markets. J. Taibah Univ. Sci. 2019, 13, 112–120. [Google Scholar] [CrossRef]

- Arouri, M.E.H.; Lahiani, A.; Nguyen, D.K. Return and volatility transmission between world oil prices and stock markets of the GCC countries. Econ. Model. 2011, 28, 1815–1825. [Google Scholar] [CrossRef] [Green Version]

- Awartani, B.; Maghyereh, A.I. Dynamic spillovers between oil and stock markets in the Gulf Cooperation Council countries. Energy Econ. 2013, 36, 28–42. [Google Scholar] [CrossRef]

- Caporale, G.M.; Menla, A.F.; Spagnolo, N. Exchange rate uncertainty and international portfolio flows: A multivariate GARCH-in-mean approach. J. Int. Money Financ. 2015, 54, 70–92. [Google Scholar] [CrossRef] [Green Version]

- Hu, Y.; Zhou, J. A time-varying study on systemic risk and intra-system risk transmission in China’s financial system from the perspective of interconnectedness. Nankai Econ. Stud. 2018, 3, 117–135. [Google Scholar]

- Ziolo, M.; Filipiak, B.Z.; Bąk, I.; Cheba, K. How to design more sustainable financial systems: The roles of environmental, social, and governance factors in the decision-making process. Sustainability 2019, 11, 5604. [Google Scholar] [CrossRef] [Green Version]

- Deng, X.; Huang, Z.; Cheng, X. FinTech and sustainable development: Evidence from China based on P2P data. Sustainability 2019, 11, 6434. [Google Scholar] [CrossRef] [Green Version]

- Wang, K.; Tsai, S.; Du, X.; Bi, D. Internet finance, green finance, and sustainability. Sustainability 2019, 11, 3856. [Google Scholar] [CrossRef] [Green Version]

- Engle, R.F.; Kroner, K.F. Multivariate simultaneous generalized ARCH. Econom. Theory 1995, 11, 122–150. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Internet Finance | Banking Industry | Securities Industry | Insurance Industry | |

|---|---|---|---|---|

| Mean | 0.0232 | 0.0054 | −0.0047 | 0.0149 |

| Median | 0.0433 | −0.0180 | −0.0374 | −0.0091 |

| Maximum | 4.6657 | 3.4087 | 4.1392 | 3.9993 |

| Minimum | −4.1539 | −4.5625 | −4.5760 | −4.3099 |

| Std. Dev. | 0.9899 | 0.6588 | 1.0250 | 0.8585 |

| Skewness | −0.4169 | 0.0429 | 0.0409 | 0.0964 |

| Kurtosis | 5.0021 | 9.3269 | 6.8036 | 6.0315 |

| Jarque–Bera | 454.5364 | 3868.6210 | 1398.6170 | 891.5911 |

| Probability | 0.0000 | 0.0000 | 0.0000 | 0.0000 |

| Observations | 2319 | 2319 | 2319 | 2319 |

| Variable | 1% | 5% | 10% | T-Statistics | P-Statistics | Conclusion | Q (10) | Q2 (10) |

|---|---|---|---|---|---|---|---|---|

| Internet finance | −3.4398 | −2.8626 | −2.5673 | −42.9206 *** | 0.0000 | stationary | 59.2880 *** | 942.4800 *** |

| Banking industry | −3.4398 | −2.8626 | −2.5673 | −48.9334 *** | 0.0001 | stationary | 33.0720 *** | 508.4200 *** |

| Securities industry | −3.4398 | −2.8626 | −2.5673 | −46.2962 *** | 0.0000 | stationary | 18.8200 ** | 492.8300 *** |

| Insurance industry | −3.4398 | −2.8626 | −2.5673 | −42.9206 *** | 0.0000 | stationary | 23.2740 *** | 323.1300 *** |

| List | Variable | Coefficient | Standard Deviation | Z-Value | p-Value |

|---|---|---|---|---|---|

| Internet finance | C | 3.02E-06 | 5.51E-07 | 5.4780 | 0.0000 |

| RESID(-1)^2 | 0.0478 | 0.0050 | 9.4141 | 0.0000 | |

| GARCH(-1) | 0.9462 | 0.0050 | 187.4317 | 0.0000 | |

| Banking industry | C | 2.37E-06 | 3.77E-07 | 6.2861 | 0.0000 |

| RESID(-1)^2 | 0.0738 | 0.0056 | 13.1777 | 0.0000 | |

| GARCH(-1) | 0.9184 | 0.0050 | 183.2538 | 0.0000 | |

| Securities industry | C | 2.71E-06 | 5.31E-07 | 5.1011 | 0.0000 |

| RESID(-1)^2 | 0.0476 | 0.0038 | 12.4377 | 0.0000 | |

| GARCH(-1) | 0.9490 | 0.0035 | 264.2489 | 0.0000 | |

| Insurance industry | C | 3.03E-06 | 6.17E-07 | 4.9081 | 0.0000 |

| RESID(-1)^2 | 0.0624 | 0.0058 | 10.7078 | 0.0000 | |

| GARCH(-1) | 0.9319 | 0.0060 | 154.4614 | 0.0000 |

| Internet Finance-Banking Industry | Internet Finance-Securities Industry | Internet Finance-Insurance Industry | |

|---|---|---|---|

| α | 0.0331 | 0.0350 | 0.0207 |

| β | 0.9642 | 0.9616 | 0.9772 |

| α + β | 0.9973 | 0.9966 | 0.9979 |

| Mean value | 0.3363 | 0.5822 | 0.3894 |

| Standard deviation | 0.2131 | 0.1916 | 0.1906 |

| Minimum value | −0.2701 | 0.0261 | −0.1286 |

| Maximum value | 0.7395 | 0.9013 | 0.7194 |

| T-statistic | 75.8060 | 146.1074 | 98.2918 |

| Log-likelihood ratio | 12663.7055 | 12002.5642 | 11975.8792 |

| α | β | α + β | |

|---|---|---|---|

| Internet finance-banking industry | 0.0331 *** (0.0002) | 0.9642 *** (0.0000) | 0.9973 |

| Internet finance-securities industry | 0.0350 *** (0.0000) | 0.9616 *** (0.0000) | 0.9966 |

| Internet finance-insurance industry | 0.0207 *** (0.0000) | 0.9772 *** (0.0000) | 0.9979 |

| Sequence | Hypothesis 1: There Is no Volatility Spillover Effect from Market A to Market B H0: a12= b12=0 | Hypothesis 2: There Is no Volatility Spillover Effect from Market B to Market A H0: a21 = b21=0 | Hypothesis 3: There Is no Mutual Volatility Spillover Effect between the Two Markets H0: a12 = b12=0, a21 = b21=0 |

|---|---|---|---|

| Banking industry–securities industry | Wald=0.7282 (0.6948) | Wald=4.1162 (0.1276) | Wald=4.7060 (0.3188) |

| Banking industry–insurance industry | Wald=0.6067 (0.7383) | Wald=9.5671 *** (0.0083) | Wald=11.6617 ** (0.0200) |

| Securities industry–insurance industry | Wald=5.2695 * (0.0717) | Wald=8.3037 ** (0.0157) | Wald=13.1103 ** (0.0107) |

| Banking Industry | Securities Industry | Insurance Industry | |

|---|---|---|---|

| Q2(10) | 9.0050 | 7.6760 | 9.7260 |

| p-value | 0.1732 | 0.2628 | 0.1366 |

| Sequence | Hypothesis 1: There Is no Volatility Spillover Effect from Market A to Market B H0: a12= b12=0 | Hypothesis 2: There Is no Volatility Spillover Effect from Market B to Market A H0: a21 = b21=0 | Hypothesis 3: There Is no Mutual Volatility Spillover Effect between the Two Markets H0: a12 = b12=0, a21 = b21=0 |

|---|---|---|---|

| Internet finance–banking industry | Wald=1.0171 (0.6013) | Wald=15.5383 *** (0.0004) | Wald=21.1596 *** (0.0003) |

| Internet finance–securities industry | Wald= 0.5306 (0.7669) | Wald=1.2960 (0.5230) | Wald=4.6391 (0.3263) |

| Internet finance–insurance industry | Wald=0.2738 (0.8720) | Wald=0.1848 (0.9117) | Wald=0.3247 (0.9881) |

| Banking industry–securities industry | Wald=2.5843 (0.2746) | Wald=7.3055 ** (0.0259) | Wald=8.3965 * (0.0780) |

| Banking industry– insurance industry | Wald=3.4924 (0.1744) | Wald=9.7250 *** (0.0077) | Wald=10.1864 ** (0.0374) |

| Securities industry–insurance industry | Wald=4.0312 0.1332 | Wald=7.7568 ** 0.0206 | Wald=12.6431 ** 0.0131 |

| Internet Finance | Banking Industry | Securities Industry | Insurance Industry | |

|---|---|---|---|---|

| Q2(10) | 5.612 | 8.902 | 8.845 | 10.644 |

| p-Value | 0.6678 | 0.4128 | 0.8371 | 0.9099 |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, S.; Liu, X.; Wang, C. The Influence of Internet Finance on the Sustainable Development of the Financial Ecosystem in China. Sustainability 2020, 12, 2365. https://doi.org/10.3390/su12062365

Li S, Liu X, Wang C. The Influence of Internet Finance on the Sustainable Development of the Financial Ecosystem in China. Sustainability. 2020; 12(6):2365. https://doi.org/10.3390/su12062365

Chicago/Turabian StyleLi, Shuping, Xinghua Liu, and Chongren Wang. 2020. "The Influence of Internet Finance on the Sustainable Development of the Financial Ecosystem in China" Sustainability 12, no. 6: 2365. https://doi.org/10.3390/su12062365

APA StyleLi, S., Liu, X., & Wang, C. (2020). The Influence of Internet Finance on the Sustainable Development of the Financial Ecosystem in China. Sustainability, 12(6), 2365. https://doi.org/10.3390/su12062365