Intellectual Capital: ISVA, the Alternative Way of Calculating Creating Value in Agricultural Entities—Case of Poland

Abstract

:1. Introduction

- Are both methods of calculation (VAIC™ and ISVA) consistent with fundamental economic principles?

- How much are VAIC™ results consistent with the actual contribution of physical and intellectual capital to adding value in an agricultural holding?

- How much are ISVA results consistent with the actual productivity of tangible and intangible (intellectual) inputs in adding value in an agricultural holding?

- What are the efficiency of physical and intellectual capital and the productivity of tangible and intangible inputs of agricultural holdings, established based on calculation results delivered by the two methods?

- Does the proposed alternative measure, ISVA, allow better evaluation of productivity of tangible and intangible expenditures to be involved in creation of value added?

2. Background

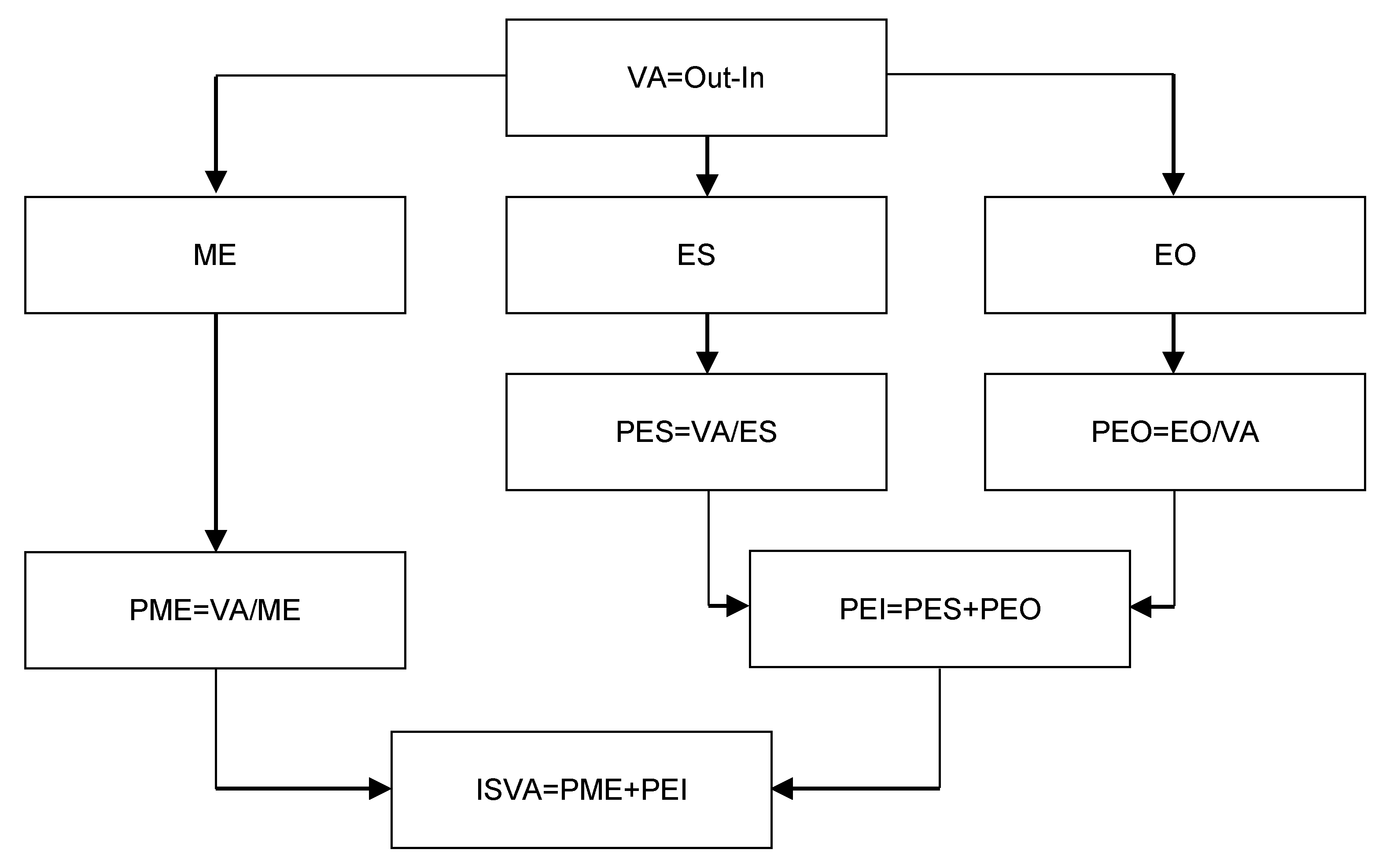

3. Materials and Methods

- Value added is the total of: Depreciation, remuneration, social insurance and other employee benefits, agricultural tax and fees, interest, income tax, and net profit.

- Material expenditure reflects the consumption of fixed and current assets (total of depreciation and material, energy, and external service consumption).

- Intellectual expenditure reflects the labor inputs (total of remuneration, social insurance, and other employee benefits) and other organizational and operational inputs (total of taxes and fees, other prime costs, and other operating costs).

- The sum of tangible and intangible inputs (expenditure) expresses the total value of expenditure incurred in the reporting period.

4. Results

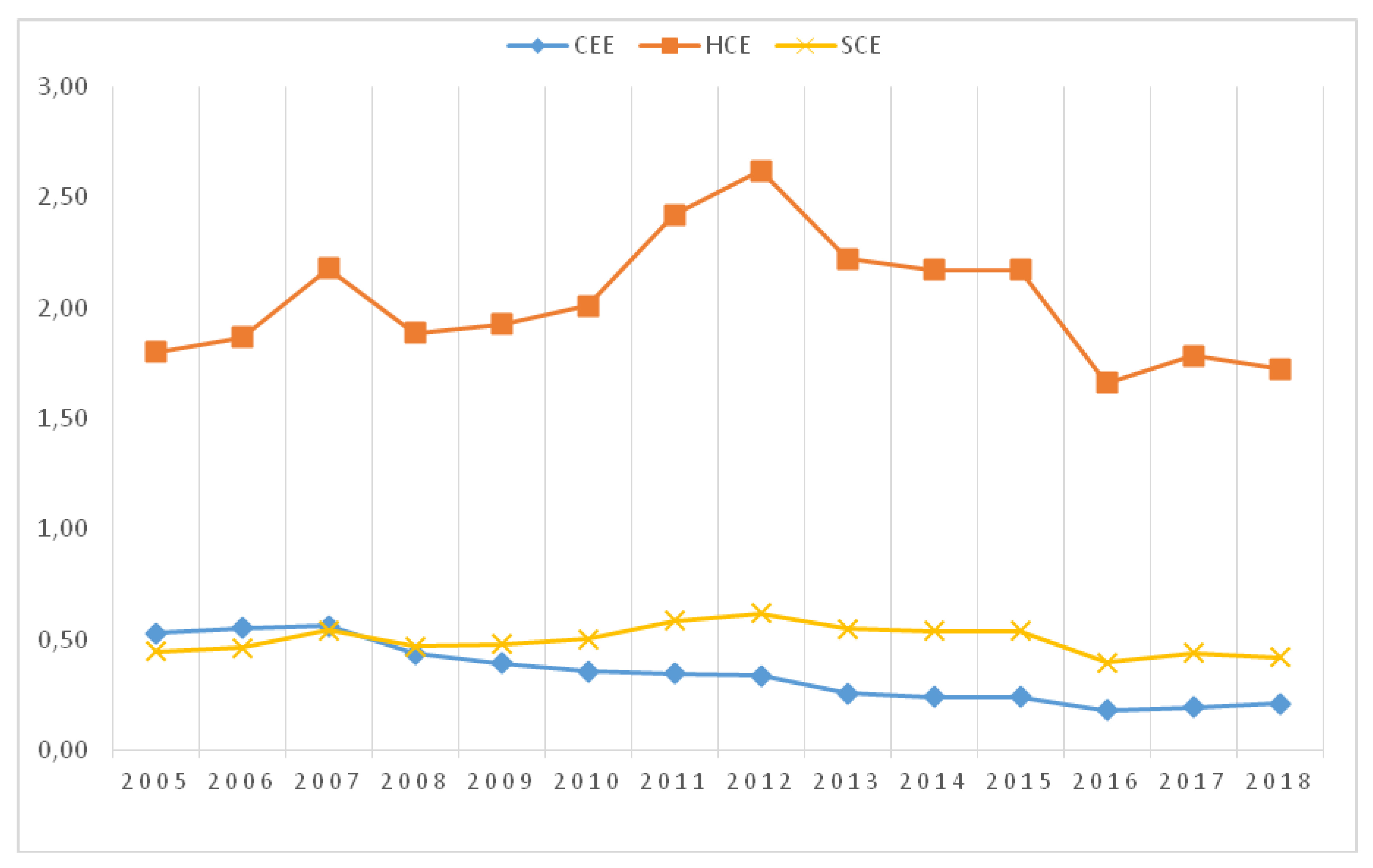

4.1. VAIC™

- Human capital was the most efficient in the value-adding process;

- in the enterprises surveyed, the share of intellectual capital efficiency (ICE = HCE + SCE) in the overall efficiency indicator was above 80%.

4.2. ISVA

5. Discussion

- The importance of intangible assets in creation of value added was proven by both methods.

- The same fluctuation of productivity of human expenditures (HCE and PES) is the result of the similar way of calculation.

- There is a significant difference as concerns the productivity of tangible expenditures (CEE and PME). While CEE constantly declines, PME fluctuates similarly to human expenditures (PES). This behavior seems to be more realistic and coherent with changes in the functioning of enterprises enforced by internal and external conditions;

- Differences concerning fluctuation of productivity of structural capital (SCE and PEO) need further analysis, especially because there is not a precise definition of this factor in either method.

6. Conclusions

- ISVA is based on calculations that rely solely on flows (streams), which is consistent with fundamental economic principles, in opposition to VAICTM, the index of use efficiency of intellectual capital initially found to be suitable for research purposes. This demonstrates certain methodological flaws, as indicated by other authors, including the simultaneous use of resource- and flow-based values, which is inconsistent with fundamental economic principles and is unacceptable to the author of this paper.

- For VAICTM, the index results of empirical tests pointed out results of the calculation of tangible assets that were not coherent with reality.

- For ISVA, the index results of empirical tests pointed out results of the calculation of tangible and intangible assets that were more coherent with reality.

- The empirical tests of the VAICTM and ISVA methods enabled identification of the importance of intangible inputs and confirmed their important contribution to value added in the surveyed agricultural holdings.

- ISVA is better alternative method for determining the factors that contribute to creation of value added of agricultural enterprises, and complements the new tool proposed for comprehensive business evaluation in accordance with the assumptions of the economics of complexity [54].

- Extending the scope of research to entities from other agribusiness links.

- Establishing benchmarks for the efficiency of using intellectual capital in other agribusiness enterprises. These values could be the benchmark for assessing the use of intangible assets.

- Extending research by making comparisons with companies in other sectors and countries.

Funding

Conflicts of Interest

References

- Hunt, S.D.; Lambe, C.J. Marketing’s Contribution to Business Strategy: Market Orientation, Relationship Marketing and Resource-Advantage Theory. Int. J. Manag. Rev. 2000, 2, 17–43. [Google Scholar] [CrossRef]

- Van Hoek, R.I.; Chatham, R.; Wilding, R. Managers in supply chain management, the critical dimension. Supply Chain Manag. 2002, 7, 119–125. [Google Scholar] [CrossRef]

- Leśniewski, M.A. Kapitał intelektualny w kształtowaniu zrównoważonego rozwoju przedsiębiorstw. Ekon. I Organ. Przedsiębiorstwa 2015, 3, 14–25. [Google Scholar]

- Dal Mas, F. The Relationship between Intellectual Capital and Sustainability: An Analysis of Practitioner’s Thought. In Intellectual Capital Management as a Driver of Sustainability; Matos, F., Vairinhos, V., Selig, P., Edvinsson, L., Eds.; Springer: Berlin/Heidelberg, Germany, 2019. [Google Scholar]

- Januškaitė, V.; Užienė, L. Intellectual Capital as a Factor of Sustainable Regional Competitiveness. Sustainability 2018, 10, 4848. [Google Scholar] [CrossRef] [Green Version]

- Kozera-Kowalska, M. Kapitał Intelektualny w Tworzeniu Wartości Dodanej Przedsiębiorstw Rolnych; Poznan University of Life Sciences Publisher: Poznań, Poland, 2017. [Google Scholar]

- Edvisson, L.; Malone, M.S. Intellectual Capital: The Proven Way to Establish Your Company’s Real Value by Measuring Its Hidden Brainpower; Piatkus: London, UK, 1997. [Google Scholar]

- Stewart, T.A. Intellectual Capital. The New Wealth of Organizations; Nicholas Brealey Publishing: London, UK, 2003. [Google Scholar]

- Gu, F.; Lev, B. Intangible Assets: Measurements, Drivers, Usefulness, 2002. Available online: https://pdfs.semanticscholar.org/4d25/211f5ce58a92e9be781eebfd591ecae38985.pdf (accessed on 25 August 2018).

- Roos, G.; Roos, J. Measuring your company’s intellectual performance. Long Range Plan. 1997, 30, 413–426. [Google Scholar] [CrossRef]

- Urbanek, G. Pomiar Kapitału Intelektualnego i Aktywów Niematerialnych Przedsiębiorstwa; Wyd. Uniwersytetu Łódzkiego: Łódź, Poland, 2007. [Google Scholar]

- Dobija, M.; Indulska, M. Accountants and Accounting for Human Resources Accountability and Intellectual Entrepreneurship; Kwiatkowski, S., Edvinsson, L., Eds.; Knowledge Café for Intellectual Entrepreneurship: Warsaw, Poland, 1999. [Google Scholar]

- Pherson, P.K.M.; Pike, S. Accounting, empirical measurement and intellectual capital. J. Intellect. Cap. 2011, 2, 246–260. [Google Scholar] [CrossRef] [Green Version]

- White, F.C. Valuation of intangible capital in agriculture. J. Agric. Appl. Econ. 1995, 27, 437–445. [Google Scholar] [CrossRef] [Green Version]

- Alston, J.M. An analysis of Growth of US Farmland Prices 1963–1982. Am. J. Agric. Econ. 1986, 68, 1–9. [Google Scholar] [CrossRef]

- Allaire-Arrive, V. Protecting and Capitalizing on Intangible Agricultural Assets 2007. Available online: http://www.momagri.org/UK/points-of-view/Protecting-and-Capitalizing-on-Intangible-Agricultural-Assets_216.html (accessed on 12 March 2019).

- Moor, L.; Craig, L. Intellectual Capital in Enterprise Success: Strategy Revisited; John Wiley and Sons Inc.: Hoboken, NJ, USA, 2008; pp. 5–8. [Google Scholar]

- Goldsmith, P.; Gow, H. Strategic positioning under agricultural structural change: A critique of long jump co-operative ventures. Int. Food Agribus. Manag. 2005, 8, 1–21. [Google Scholar]

- Fulton, M.; Giannakas, K. Agricultural biotechnology and industry structure. J. Agrobiotechnology Ind. Struct. 2002, 4, 137–151. [Google Scholar]

- Sporleder, T.L.; Moss, L.E. Knowledge Capital, Intangible Assets, and Leverage, Evidence from US Agricultural Biotechnology Firms. Int. Food Agribus. Manag. Rev. 2004, 7, 26–36. [Google Scholar]

- Bontis, N. Assessing knowledge assets: A review of the models used to measure intellectual capital. Int. J. Manag. Rev. 2001, 3, 41–60. [Google Scholar] [CrossRef]

- Sveiby, K.-E. Methods for Measuring Intangibles Assets, 2001 (updated 27 April 2010). Available online: http://www.sveiby.com/articles/IntangibleMethods.htm (accessed on 29 July 2015).

- Pulic, A. Measuring the performance of intellectual potential in knowledge economy. In Proceedings of the 2nd World Congress on Measuring and Managing Intellectual Capital, McMaster University, Hamilton, ON, Canada, 21–24 January 1998; McMaster University: Hamilton, ON, Canada, 1998. [Google Scholar]

- Pulic, A. VAIC- An Accounting Tool for IC Management, 2000. Available online: http://www.measuring-ip.at/papers/ham99txt.htm (accessed on 20 December 2013).

- Rocznik Statystyczny Rzeczypospolitej Polskiej 2018. Available online: https://stat.gov.pl/download/gfx/portalinformacyjny/pl/defaultaktualnosci/5515/2/18/1/rocznik_statystyczny_rzeczypospolitej_polskiej_2018_.pdf (accessed on 21 September 2019).

- Ryś-Jurek, R. Porównanie sytuacji ekonomicznej polskich indywidualnych gospodarstw rolnych z gospodarstwami innych krajów UE w latach 2000–2005. Probl. World Agric. 2007, 2, 114–123. [Google Scholar]

- Józwiak, W. Polskie Rolnictwo i Gospodarstwa Rolne w Pierwszej i Drugiej Dekadzie XXI Wieku; Institute of Agricultural and Food Economics National Research Institute: Warszawa, Poland, 2013. [Google Scholar]

- Czubak, W.; Sadowski, A. Wpływ modernizacji wspieranych funduszami UE na zmiany sytuacji majątkowej w gospodarstwach rolnych w Polsce. J. Agribus. Rural Dev. 2014, 2, 45–57. [Google Scholar]

- Komnenic, B.; Tomic, D.V.; Tomic, G.R. Measuring efficiency of intellectual capital in agriculture sector of Vojvodina. Appl. Stud. Agribus. Commer. 2010, 4, 25–31. [Google Scholar] [CrossRef] [PubMed]

- Ghatak, S.; Ingersent, K. Agriculture and Economic Development; Harvester Press: Brighton, UK, 1984. [Google Scholar]

- Lee, K.; Yoo, J.; Choi, M.; Zo, H.; Ciganek, A.P. Does External Knowledge Sourcing Enhance Market Performance? Evidence from the Korean Manufacturing Industry. PLoS ONE 2016, 11, e0168676. [Google Scholar] [CrossRef] [PubMed]

- Vega-Jurado, J.; Gutiérrez-Gracia, A.; Fernández-de-Lucio, I. Does external knowledge sourcing matter for innovation? Evidence from the Spanish manufacturing industry. Ind. Corp. Chang. 2009, 18, 637–670. [Google Scholar] [CrossRef]

- Scafarto, V.; Ricci, F.; Scafarto, F. Intellectual capital and firm performance in the global agribusiness industry: The moderating role of human capital. J. Intellect. Cap. 2016, 17, 530–552. [Google Scholar] [CrossRef]

- Boljanovic, J.D.; Dobrijevic, G.; Cerovic, S.; Alcakovic, S.; Djokovic, F. Knowledge-based bioeconomy: The use of intellectual capital in food industry of Serbia. Amfiteatru Econ. 2018, 20, 717–731. [Google Scholar] [CrossRef]

- Yasnolob, I.; Chayka, T.; Gorb, O.; Shvedenko, P.; Protas, N.; Tereshchenko, I. Intellectual Rent in the Context of the Ecological, Social, and Economic Development of the Agrarian Sector of Economics. J. Environ. Manag. Tour. 2017, 7, 1442–1450. [Google Scholar]

- Cavicchi, C.; Vagnoni, E. Intellectual Capital in Support of Farm Businesses’ Strategic Management: A Case Study. J. Intellect. Cap. 2018, 19, 692–711. [Google Scholar] [CrossRef]

- Barrett, C.B.; Carter, M.R.; Timmer, C.P. A century-long perspective on agricultural development. Am. J. Agric. Econ. 2010, 92, 447–468. [Google Scholar] [CrossRef]

- Boehlje, M.; Roucan-Kane, M.; Bröring, S. Future agribusiness challenges: Strategic uncertainty, innovation and structural change. Int. Food Agribus. Manag. Rev. 2011, 14, 53–82. [Google Scholar]

- Cavicchi, C.; Vagnoni, E. Does intellectual capital promote the shift of healthcare organizations towards sustainable development? Evidence from Italy. J. Clean. Prod. 2017, 153, 275–286. [Google Scholar] [CrossRef]

- Parker, W. Agriculture and the environment: A codependent future requiring new technology, systems and expertise. In Proceedings of the 18th International Farm Managment Congress Methven, Christchurch, New Zealand, 20–25 March 2011; Congress Proceedings. ISBN 978-92-990056-7-5. Available online: http://ifmaonline.org/wp-content/uploads/2014/08/11_PL_Parker_P363-366.pdf (accessed on 27 August 2019).

- Hill, B.; Ray, D. Economics for Agriculture: Food, Farming and the Rural Economy; Macmillan Education: Basingstoke, UK; London, UK, 1987. [Google Scholar]

- Chavas, J.-P.; Aliber, M. An analysis of economic efficiency in agriculture: A nonparametric approach. J. Agric. Resour. Econ. 1993, 18, 1–16. [Google Scholar]

- Klepacki, B. Economic condition of peasant farms in the transformation period. Probl. Agric. Econ. 1997, 2–3, 37–46. [Google Scholar]

- Gębska, M.; Filipiak, T. Basics of Economics and Organization of Farms; Warsaw University of Life Sciences: Warszawa, Poland, 2006. [Google Scholar]

- Kasiewicz, S.; Rogowski, W.; Kicińska, M. Intellectual Capital as Seen by Stakeholders; Oficyna Ekonomiczna Publishing House: Krakow, Poland, 2006; pp. 93–94. [Google Scholar]

- Kunasz, M. Using VAIC™ to analyze the efficiency of the value adding process based on tangible and intangible assets: Research findings. Problemy Jakości 2006, 3, 15–21. [Google Scholar]

- Jóźwiak, W.; Kagan, A. Commercial farms vs. large-scale agricultural holdings. Agric. Sci. Yearb. 2008, 95, 22–30. [Google Scholar]

- Kozioł, D.; Parlińska, A. Factors affecting the value of agricultural property. Sci. Yearb. Assoc. Agric. Agribus. Econ. 2009, 11, 120–125. [Google Scholar]

- Kondraszczuk, T. Specific elements of financial analyses and assessments in the agriculture sector. Sci. J. Univ. Szczec. Financ. Financ. Mark. Insur. 2009, 20, 243–257. [Google Scholar]

- Domański, H. A Happy Slave Goes to Work: Attitudes towards Economic Activity of Women in 23 Countries; Publishing House IFiS PAN: Warsaw, Poland, 1999. [Google Scholar]

- Polak, T. Challenges and threats faced by the labor market in the context of today’s socio-economic transformation. Sel. Probl. Contemp. Econ. 2010, 4, 23–38. [Google Scholar]

- Kozera-Kowalska, M.; Baum, R. Measurement of intellectual capital in agricultural enterprises: A case study in Poland. In Proceedings of the Economics and Finance Conferences, International Institute of Social and Economic Sciences, Rome, Italy, 10–13 September 2018; pp. 209–220. [Google Scholar]

- Kulawik, J. Monitoring system for the efficiency and productivity of agricultural enterprises. Zagadnienia Ekonomiki Rolnej 2009, 3, 33–49. [Google Scholar]

- Niezgoda, M. Effectiveness of substituting human labor with capital in large-scale agricultural holdings. Ann. Pol. Assoc. Agric. Agribus. Econ. 2009, 11, 314–319. [Google Scholar]

- Czyżewski, B. Resource productivity in Polish agriculture in the context of sustainable development. Econ. Stud. 2012, 2, 165–189. [Google Scholar]

- Wójcik, E.; Nowak, A. Analysis of the substitution of human labor with capital in commercial farms in the first years after Poland joined the EU. Sci. J. Wars. Univ. Life Sci. Financ. Mark. 2012, 8, 505–517. [Google Scholar]

- Tamura, R. Human capital and the switch from agriculture to industry. J. Econ. Dyn. Control 2002, 27, 207–242. [Google Scholar] [CrossRef]

- Huffman, W.E.; Orazem, P.F. Agriculture and human capital in economic growth: Farmers, schooling and nutrition. In Handbook of Agricultural Economics; Evenson, R., Pingali, P., Eds.; Elsevier: Amsterdam, The Netherlands, 2007; Volume 3, pp. 2281–2341. [Google Scholar]

- Bogoviz, A.V.; Alekseev, A.N.; Lobova, S.V.; Telegina, Z.A.; Barcho, M.K. The human component of the process of improving productivity in the agrarian sector. Qual. Access Success 2018, 19, 166–170. [Google Scholar]

- Bukraba-Rylska, I. O potrzebie i korzyściach z badania wsi i rolnictwa w Polsce. Wieś i Rolnictwo 2018, 179, 13–30. [Google Scholar]

- Zegar, J. Rolnictwo w rozwoju obszarów wiejskich. Wieś i Rolnictwo 2018, 179, 31–48. [Google Scholar]

- Kalinowski, J. Technologie informatyczne a konkurencyjność w rolnictwie: Wybrane aspekty. Roczniki Naukowe Stowarzyszenia Ekonomistów Rolnictwa i Agrobiznesu 2008, 4, 161–166. [Google Scholar]

- Kocira, S.; Lorencowicz, E. Wykorzystanie technik komputerowych w gospodarstwach rodzinnych. Inżynieria Rolnicza 2011, 15, 77–83. [Google Scholar]

- Kozera, M. Kapitał Intelektualny w Rolnictwie–Zrozumieć, Zmierzyć, Zastosować. Prace Naukowe Uniwersytetu Ekonomicznego we Wrocławiu 2012, 262, 177–187. [Google Scholar]

- Kozera, M.; Kaliowski, S. Intellectual capital—Non-material element of farm businesses economic succes. In Proceedings of the International Conference on Management of Human Resources, Management—Leadership—Strategy—Competitiveness, Godollo, Hungary, 14–15 June 2012; Szent Istvan University: Godollo, Hungary, 2012; pp. 405–413. [Google Scholar]

- Kozera, M. Efektywność wykorzystania kapitału intelektualnego w przedsiębiorstwach rolniczych Wielkopolski. Przedsiębiorczość I Zarządzanie 2014, 15, 165–179. [Google Scholar]

- Kozera, M. Efektywność wykorzystania kapitału intelektualnego przedsiębiorstw rolniczych w Polsce. Roczniki Naukowe Ekonomii Rolnictwa i Rozwoju Obszarów Wiejskich 2015, 102, 37–46. [Google Scholar]

- Łobos, K.; Szewczyk, M. Pomiar kapitału intelektualnego i jego wpływ na efektywność przedsiębiorstw produkujących podłoże pod uprawę pieczarek. J. Agribus. Rural Dev. 2013, 1, 143–152. [Google Scholar]

- Wilkin, J. Can economics be beautiful? Discussing the subject matter and methods of economics. Economist 2009, 3, 295–313. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Specification | Years | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | Ave. | ||

| Expenditure (thousand PLN) | ||||||||||||||||

| Value of Net Assets (CE) | 3273 | 3358 | 4415 | 5316 | 6002 | 6978 | 8869 | 10358 | 11479 | 12455 | 12455 | 13003 | 13219 | 12051 | 8802 | |

| Intangible | Human Capital (HC) | 963 | 996 | 1137 | 1225 | 1222 | 1240 | 1263 | 1337 | 1323 | 1374 | 1374 | 1404 | 1435 | 1461 | 1268 |

| Structural Capital Value (SC) | 771 | 863 | 1341 | 1088 | 1131 | 1250 | 1796 | 2166 | 1617 | 1610 | 1610 | 927 | 1126 | 1058 | 1311 | |

| Value Added (VA) | 1733 | 1860 | 2478 | 2312 | 2353 | 2490 | 3059 | 3502 | 2940 | 2984 | 2984 | 2331 | 2562 | 2518 | 2579 | |

| Productivity of Expenditure (%) | ||||||||||||||||

| Capital Employed Efficiency (CEE) | 0.53 | 0.55 | 0.56 | 0.43 | 0.39 | 0.36 | 0.34 | 0.34 | 0.26 | 0.24 | 0.24 | 0.18 | 0.19 | 0.21 | 0.34 | |

| Intangible | Human Capital Efficiency (HCE) | 1.80 | 1.87 | 2.18 | 1.89 | 1.93 | 2.01 | 2.42 | 2.62 | 2.22 | 2.17 | 2.17 | 1.66 | 1.78 | 1.72 | 2,03 |

| Efficiency of Structural Capital (SCE) | 0.44 | 0.46 | 0.54 | 0.47 | 0.48 | 0.50 | 0.59 | 0.62 | 0.55 | 0.54 | 0.54 | 0.40 | 0.44 | 0.42 | 0.50 | |

| Value Added Intellectual Coefficient (VAICTM) | 2.77 | 2.88 | 3.28 | 2.79 | 2.80 | 2.87 | 3.35 | 3.58 | 3.03 | 2.95 | 2.95 | 2.24 | 2.42 | 2.35 | 2.88 | |

| Specification | Years | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | Ave. | ||

| Expenditure (%) | ||||||||||||||||

| Value of Net Assets (CE) | 65.38 | 64.36 | 64.05 | 69.69 | 71.83 | 73.70 | 74.35 | 74.73 | 79.61 | 80.67 | 80.67 | 84.80 | 83.77 | 82.71 | 75.02 | |

| Intangible | Expenditure on Staff (ES) | 19.23 | 19.09 | 16.50 | 16.05 | 14.62 | 13.10 | 10.59 | 9.65 | 9.18 | 8.90 | 8.90 | 9.16 | 9.10 | 10.02 | 12.43 |

| Expenditure on Organization (EO) | 15.39 | 16.55 | 19.45 | 14.26 | 13.54 | 13.20 | 15.06 | 15.62 | 11.21 | 10.43 | 10.43 | 6.04 | 7.14 | 7.26 | 12.54 | |

| Value Added (VA) | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | |

| Productivity of Expenditure (%) | ||||||||||||||||

| Capital Employed Efficiency (CEE) | 19.09 | 19.20 | 17.10 | 15.57 | 14.01 | 12.45 | 10.29 | 9.45 | 8.46 | 8.12 | 8.12 | 8.01 | 8.01 | 8.88 | 11.91 | |

| Intangible | Human Capital Efficiency (HCE) | 64.89 | 64.71 | 66.41 | 67.59 | 68.81 | 70.04 | 72.21 | 73.26 | 73.38 | 73.60 | 73.60 | 74.21 | 73.80 | 73.27 | 70.70 |

| Efficiency of Structural Capital (SCE) | 16.02 | 16.09 | 16.49 | 16.84 | 17.18 | 17.51 | 17.50 | 17.29 | 18.16 | 18.28 | 18.28 | 17.77 | 18.18 | 17.85 | 17.39 | |

| Value Added Intellectual Coefficient (VAIC) | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | |

| Specification | Years | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | Ave. | ||

| Expenditure (thousand PLN) | ||||||||||||||||

| Material Expenditure (ME) | 2902 | 3166 | 3642 | 3996 | 3794 | 3816 | 4189 | 4714 | 4533 | 4781 | 4781 | 4545 | 4451 | 4377 | 4120 | |

| Intangible | Expenditure on Staff (ES) | 963 | 966 | 1137 | 1225 | 1222 | 1240 | 1263 | 1337 | 1323 | 1374 | 1374 | 1374 | 1435 | 1461 | 1268 |

| Expenditure on Organization (EO) | 130 | 127 | 137 | 160 | 152 | 163 | 182 | 212 | 223 | 187 | 187 | 177 | 206 | 217 | 175 | |

| Value Added (VA) | 1733 | 1860 | 2478 | 2312 | 2353 | 2490 | 3059 | 3502 | 2940 | 2984 | 2984 | 2331 | 2562 | 2518 | 2579 | |

| Productivity of Expenditure (%) | ||||||||||||||||

| Productivity of Material Expenditure (PME) | 0.60 | 0.59 | 0.68 | 0.58 | 0.62 | 0.65 | 0.73 | 0.74 | 0.65 | 0.62 | 0.62 | 0.51 | 0.58 | 0.58 | 0.63 | |

| Intangible | Productivity of Expenditure on Staff (PES) | 1.80 | 1.87 | 2.18 | 1.89 | 1.93 | 2.01 | 2.42 | 2.62 | 2.22 | 2.17 | 2.17 | 1.66 | 1.78 | 1.72 | 2.03 |

| Productivity of Expenditure on Organization (PEO) | 0.07 | 0.07 | 0.06 | 0.07 | 0.06 | 0.07 | 0.06 | 0.06 | 0.08 | 0.06 | 0.06 | 0.08 | 0.08 | 0.09 | 0.07 | |

| Intellectual Sources of Value Added (ISVA) | 2.47 | 2.52 | 2.91 | 2.54 | 2.61 | 2.73 | 3.21 | 3.42 | 2.95 | 2.86 | 2.86 | 2.25 | 2.44 | 2.39 | 2.73 | |

| Specification | Years | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | Ave. | ||

| Expenditure (%) | ||||||||||||||||

| Material Expenditure (ME) | 72.65 | 73.82 | 74.09 | 74.26 | 73.42 | 73.12 | 74.35 | 75.27 | 74.56 | 75.39 | 75.39 | 74.19 | 73.05 | 72.29 | 73.99 | |

| Intangible | Expenditure on Staff (ES) | 24.10 | 23.22 | 23.13 | 22.76 | 23.64 | 23.76 | 22.42 | 21.35 | 21.77 | 21.66 | 21.66 | 22.92 | 23.56 | 24.12 | 22.86 |

| Expenditure on Organization (EO) | 3.25 | 2.96 | 2.78 | 2.98 | 2.94 | 3.12 | 3.23 | 3.38 | 3.67 | 2.95 | 2.95 | 2.88 | 3.39 | 3.58 | 3.15 | |

| Value Added (VA) | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | |

| Productivity of Expenditure (%) | ||||||||||||||||

| Productivity of Material Expenditure (PME) | 24.16 | 23.28 | 23.35 | 22.82 | 23.76 | 23.94 | 22.74 | 21.70 | 22.02 | 21.83 | 21.83 | 22.81 | 23.58 | 24.12 | 23.00 | |

| Intangible | Productivity of Expenditure on Staff (PES) | 72.82 | 74.01 | 74.76 | 74.45 | 73.77 | 73.66 | 75.41 | 76.53 | 75.41 | 75.97 | 75.97 | 73.82 | 73.12 | 72.27 | 74.43 |

| Productivity of Expenditure on Organization (PEO) | 3.03 | 2.70 | 1.89 | 2.73 | 2.47 | 2.40 | 1.85 | 1.77 | 2.57 | 2.19 | 2.19 | 3.37 | 3.30 | 3.61 | 2.58 | |

| Intellectual Sources of Value Added (ISVA) | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | 100 | |

© 2020 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kozera-Kowalska, M. Intellectual Capital: ISVA, the Alternative Way of Calculating Creating Value in Agricultural Entities—Case of Poland. Sustainability 2020, 12, 2645. https://doi.org/10.3390/su12072645

Kozera-Kowalska M. Intellectual Capital: ISVA, the Alternative Way of Calculating Creating Value in Agricultural Entities—Case of Poland. Sustainability. 2020; 12(7):2645. https://doi.org/10.3390/su12072645

Chicago/Turabian StyleKozera-Kowalska, Magdalena. 2020. "Intellectual Capital: ISVA, the Alternative Way of Calculating Creating Value in Agricultural Entities—Case of Poland" Sustainability 12, no. 7: 2645. https://doi.org/10.3390/su12072645

APA StyleKozera-Kowalska, M. (2020). Intellectual Capital: ISVA, the Alternative Way of Calculating Creating Value in Agricultural Entities—Case of Poland. Sustainability, 12(7), 2645. https://doi.org/10.3390/su12072645