The Role of Venture Capital Investment in Startups’ Sustainable Growth and Performance: Focusing on Absorptive Capacity and Venture Capitalists’ Reputation

Abstract

:1. Introduction

2. Background: The Five Stages of Startup Growth

3. Theory and Hypotheses Development

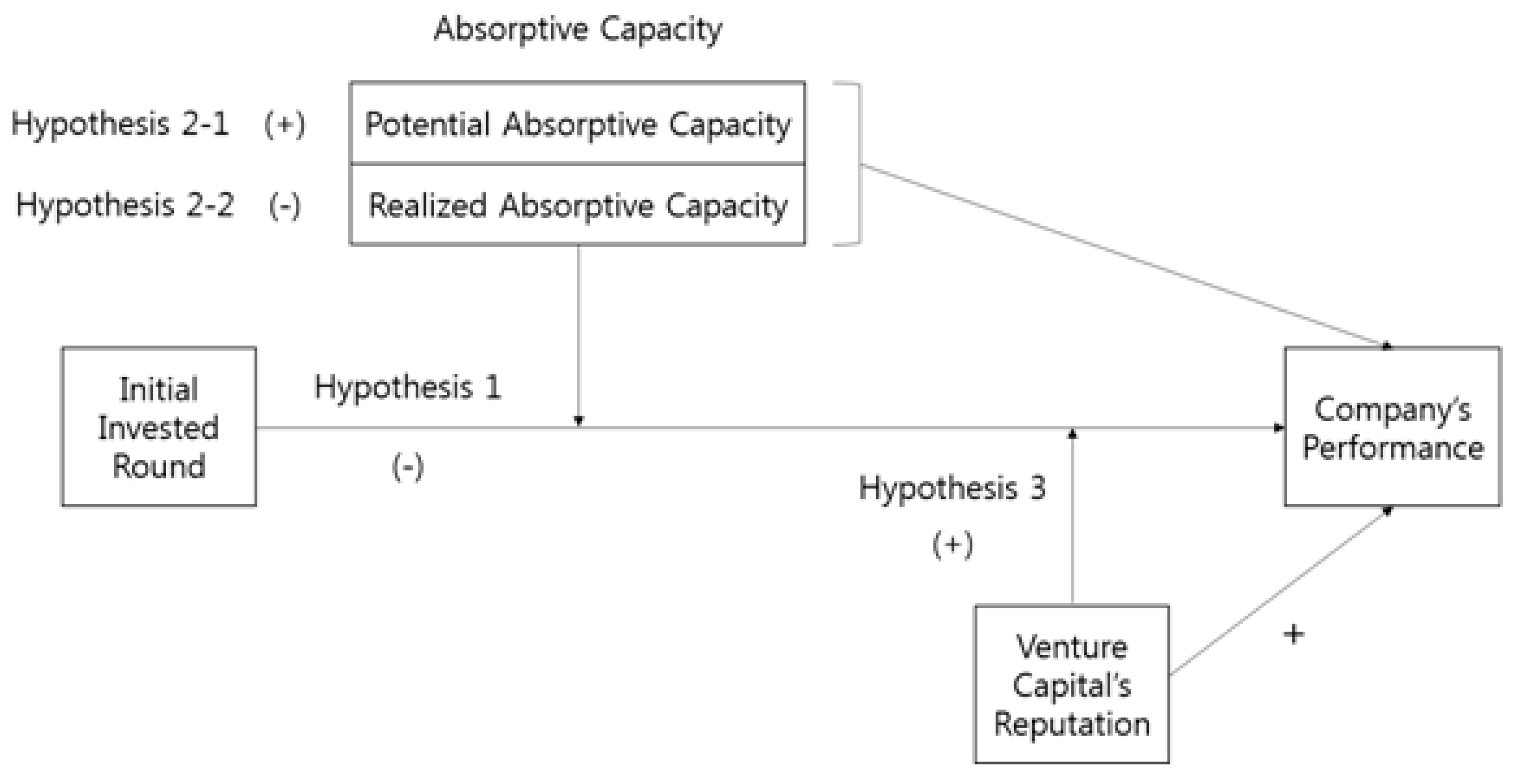

3.1. Signaling Effects of Venture Capital Investment on Startups

3.2. Moderating Effects of Startups’ Learning Capability: Absorptive Capacity

3.3. Moderating Effects of the Reputation of VC Companies

4. Method

4.1. Data

4.2. Variables

5. Results

6. Discussion

Author Contributions

Funding

Conflicts of Interest

References

- Barry, C.B.; Muscarella, C.J.; Peavy Iii, J.W.; Vetsuypens, M.R. The role of venture capital in the creation of public companies: Evidence from the going-public process. J. Financ. Econ. 1990, 27, 447–471. [Google Scholar] [CrossRef]

- Kaplan, S.N.; Strömberg, P. Financial contracting theory meets the real world: An empirical analysis of venture capital contracts. Rev. Econ. Stud. 2003, 70, 281–315. [Google Scholar] [CrossRef]

- Kortum, S.; Lerner, J. Assessing the contribution of venture capital to innovation. RAND J. Econ. 2000, 31, 674–692. [Google Scholar] [CrossRef] [Green Version]

- Hellmann, T.; Puri, M. Venture capital and the professionalization of start-up firms: Empirical evidence. J. Financ. 2002, 57, 169–197. [Google Scholar] [CrossRef]

- Wang, S.; Zhou, H. Staged financing in venture capital: Moral hazard and risks. J. Corp. Financ. 2004, 10, 131–155. [Google Scholar] [CrossRef]

- Gompers, P.; Lerner, J. The venture capital revolution. J. Econ. Perspect. 2001, 15, 145–168. [Google Scholar] [CrossRef] [Green Version]

- Byers, B. Relationship between venture capitalist and entrepreneur. In Pratt’s Guide to Venture Capital Sources; Venture Economics: Wellesly Hills, MA, USA, 1997. [Google Scholar]

- Bygrave, W.D.; Timmons, J.A. Venture Capital at the Crossroads; Harvard Business School Press: Cambridge, MA, USA, 1992. [Google Scholar]

- Gompers, P.A. Optimal investment, monitoring, and the staging of venture capital. J. Financ. 1995, 50, 1461–1489. [Google Scholar] [CrossRef]

- Maula, M.; Murray, G. Complementary value-adding roles of corporate venture capital and independent venture capital investors. J. Biolaw Bus. 2001, 5. [Google Scholar]

- Teece, D.J. Profiting from technological innovation: Implications for integration, collaboration, licensing and public policy. Res. Policy 1986, 15, 285–305. [Google Scholar] [CrossRef]

- Antarciuc, E.; Zhu, Q.; Almarri, J.; Zhao, S.; Feng, Y.; Agyemang, M. Sustainable venture capital investments: An enabler investigation. Sustainability 2018, 10, 1204. [Google Scholar] [CrossRef] [Green Version]

- Wang, G.; Li, L.; Jiang, X. Entrepreneurial business ties and new venture growth: The mediating role of resource acquiring, bundling and leveraging. Sustainability 2019, 11, 244. [Google Scholar] [CrossRef] [Green Version]

- Repullo, R.; Suarez, J. Venture capital finance: A security design approach. Rev. Financ. 2004, 8, 75–108. [Google Scholar] [CrossRef]

- Wright, M.; Lockett, A. The structure and management of alliances: Syndication in the venture capital industry. J. Manag. Stud. 2003, 40, 2073–2102. [Google Scholar] [CrossRef]

- Gompers, P.; Lerner, J. An analysis of compensation in the US venture capital partnership. J. Financ. Econ. 1999, 51, 3–44. [Google Scholar] [CrossRef]

- Jain, B.A.; Kini, O. Venture capitalist participation and the post-issue operating performance of IPO firms. Manag. Decis. Econ. 1995, 16, 593–606. [Google Scholar] [CrossRef]

- Sapienza, H.J. When do venture capitalists add value? J. Bus. Ventur. 1992, 7, 9–27. [Google Scholar] [CrossRef]

- Burgel, O.; Fier, A.; Licht, G.; Murray, G.C. Internationalisation of high-tech start-ups and fast growth-evidence for UK and Germany. Zew-Discuss. Pap. 2000, 00–35. [Google Scholar] [CrossRef] [Green Version]

- Manigart, S.; Van Hyfte, W. Post-investment evolution of Belgian venture capital backed companies: An empirical study. In Frontiers of Entrepreneurship Research 1999. Nineteenth Annual Entrepreneurship Research Conference; Babson Center for Entrepreneurial Studies: Babson Park, MA, USA, 1999. [Google Scholar]

- Anton, J.J.; Yao, D.A. Expropriation and inventions: Appropriable rents in the absence of property rights. Am. Econ. Rev. 1994, 84, 190–209. [Google Scholar]

- Bhattacharya, S.; Ritter, J.R. Innovation and communication: Signalling with partial disclosure. Rev. Econ. Stud. 1983, 50, 331–346. [Google Scholar] [CrossRef]

- Ueda, M. Banks versus venture capital: Project evaluation, screening, and expropriation. J. Financ. 2004, 59, 601–621. [Google Scholar] [CrossRef]

- Yosha, O. Information disclosure costs and the choice of financing source. J. Financ. Intermediation 1995, 4, 3–20. [Google Scholar] [CrossRef]

- Ruhnka, J.C.; Young, J.E. A venture capital model of the development process for new ventures. J. Bus. Ventur. 1987, 2, 167–184. [Google Scholar] [CrossRef]

- Valentim, L.; Lisboa, J.V.; Franco, M. Knowledge management practices and absorptive capacity in small and medium-sized enterprises: Is there really a linkage? RD Manag. 2016, 46, 711–725. [Google Scholar] [CrossRef]

- Ruhnka, J.C.; Young, J.E. Some hypotheses about risk in venture capital investing. J. Bus. Ventur. 1991, 6, 115–133. [Google Scholar] [CrossRef]

- Baum, J.A.; Oliver, C. Institutional linkages and organizational mortality. Adm. Sci. Q. 1991, 187–218. [Google Scholar] [CrossRef]

- Cox Pahnke, E.; McDonald, R.; Wang, D.; Hallen, B. Exposed: Venture capital, competitor ties, and entrepreneurial innovation. Acad. Manag. J. 2015, 58, 1334–1360. [Google Scholar] [CrossRef]

- Ueda, M. Bank versus venture capital. Upf Econ. Bus. Work. Pap. 2000, 522. [Google Scholar] [CrossRef] [Green Version]

- Lukkarinen, A.; Teich, J.E.; Wallenius, H.; Wallenius, J. Success drivers of online equity crowdfunding campaigns. Decis. Support Syst. 2016, 87, 26–38. [Google Scholar] [CrossRef]

- Wang, L.; Wang, S. Economic freedom and cross-border venture capital performance. J. Empir. Financ. 2012, 19, 26–50. [Google Scholar] [CrossRef]

- Zhang, H.; Sun, X.; Lyu, C. Exploratory orientation, business model innovation and new venture growth. Sustainability 2017, 10, 1–15. [Google Scholar] [CrossRef] [Green Version]

- Ang, S.H. Country-of-origin effect of VC investment in biotechnology companies. J. Commer. Biotechnol. 2006, 13, 12–19. [Google Scholar] [CrossRef]

- Bacon-Gerasymenko, V.; Eggers, J.P. The dynamics of advice giving by venture capital firms: Antecedents of managerial cognitive effort. J. Manag. 2019, 45, 1660–1688. [Google Scholar] [CrossRef]

- Lounsbury, M.; Glynn, M.A. Cultural entrepreneurship: Stories, legitimacy, and the acquisition of resources. Strateg. Manag. J. 2001, 22, 545–564. [Google Scholar] [CrossRef]

- Aldrich, H.; Auster, E.R. Even dwarfs started small: Liabilities of age and size and their strategic implications. Res. Organ. Behav. 1986, 8, 165–198. [Google Scholar]

- Rickne, A. Connectivity and performance of science-based firms. Small Bus. Econ. 2006, 26, 393–407. [Google Scholar] [CrossRef]

- Pisano, G.P. Knowledge, integration, and the locus of learning: An empirical analysis of process development. Strateg. Manag. J. 1994, 15, 85–100. [Google Scholar] [CrossRef]

- Teece, D.J. Competition, cooperation, and innovation: Organizational arrangements for regimes of rapid technological progress. J. Econ. Behav. Organ. 1992, 18, 1–25. [Google Scholar] [CrossRef]

- Carter, R.; Manaster, S. Initial public offerings and underwriter reputation. J. Financ. 1990, 45, 1045–1067. [Google Scholar] [CrossRef]

- Shan, W.; Walker, G.; Kogut, B. Interfirm cooperation and startup innovation in the biotechnology industry. Strateg. Manag. J. 1994, 15, 387–394. [Google Scholar] [CrossRef]

- Stuart, T.E.; Hoang, H.; Hybels, R.C. Interorganizational endorsements and the performance of entrepreneurial ventures. Adm. Sci. Q. 1999, 44, 315–349. [Google Scholar] [CrossRef] [Green Version]

- Stuart, T.E. Interorganizational alliances and the performance of firms: A study of growth and innovation rates in a high-technology industry. Strateg. Manag. J. 2000, 21, 791–811. [Google Scholar] [CrossRef]

- Barney, J. Firm resources and sustained competitive advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Gulati, R.; Higgins, M.C. Which ties matter when? The contingent effects of interorganizational partnerships on IPO success. Strateg. Manag. J. 2003, 24, 127–144. [Google Scholar] [CrossRef]

- Heeley, M.B.; Matusik, S.F.; Jain, N. Innovation, appropriability, and the underpricing of initial public offerings. Acad. Manag. J. 2007, 50, 209–225. [Google Scholar] [CrossRef]

- Hsu, D.H.; Ziedonis, R.H. Resources as dual sources of advantage: Implications for valuing entrepreneurial-firm patents. Strateg. Manag. J. 2013, 34, 761–781. [Google Scholar] [CrossRef]

- Bhatt, G.D. Organizing knowledge in the knowledge development cycle. J. Knowl. Manag. 2000. [Google Scholar] [CrossRef]

- Grant, R.M. Toward a knowledge-based theory of the firm. Strateg. Manag. J. 1996, 17, 109–122. [Google Scholar] [CrossRef]

- Prahaland, C.; Hamel, G. The core competence of the corporation. Harv. Bus. Rev. 1990, 82–84. [Google Scholar]

- Cohen, W.M.; Levinthal, D.A. Absorptive capacity: A new perspective on learning and innovation. Adm. Sci. Q. 1990, 35, 128–152. [Google Scholar] [CrossRef]

- Ben-Oz, C.; Greve, H.R. 2015. Short- and Long-Term Performance Feedback and Absorptive Capacity. J. Manag. 2015, 41, 1827–1853. [Google Scholar]

- Zahra, S.A.; George, G. Absorptive capacity: A review, reconceptualization, and extension. Acad. Manag. Rev. 2002, 27, 185–203. [Google Scholar] [CrossRef] [Green Version]

- Engelen, A.; Kube, H.; Schmidt, S.; Flatten, T.C. Entrepreneurial orientation in turbulent environments: The moderating role of absorptive capacity. Res. Policy 2014, 43, 1353–1369. [Google Scholar] [CrossRef]

- Volberda, H.W.; Foss, N.J.; Lyles, M.A. Perspective—Absorbing the concept of absorptive capacity: How to realize its potential in the organization field. Organ. Sci. 2010, 21, 931–951. [Google Scholar] [CrossRef] [Green Version]

- Bergh, D.D.; Lim, E.N.K. Learning how to restructure: Absorptive capacity and improvisational views of restructuring actions and performance. Strateg. Manag. J. 2008, 29, 593–616. [Google Scholar] [CrossRef]

- Lane, P.J.; Koka, B.R.; Pathak, S. The reification of absorptive capacity: A critical review and rejuvenation of the construct. Acad. Manag. Rev. 2006, 31, 833–863. [Google Scholar] [CrossRef]

- Flatten, T.C.; Greve, G.I.; Brettel, M. Absorptive capacity and firm performance in SMEs: The mediating influence of strategic alliances. Eur. Manag. Rev. 2011, 8, 137–152. [Google Scholar] [CrossRef]

- Covin, J.G.; Lumpkin, G.T. Entrepreneurial orientation theory and research: Reflections on a needed construct. Entrep. Theory Pract. 2011, 35, 855–872. [Google Scholar] [CrossRef]

- Zott, C. Dynamic capabilities and the emergence of intraindustry differential firm performance: Insights from a simulation study. Strateg. Manag. J. 2003, 24, 97–125. [Google Scholar] [CrossRef]

- Dierkens, N. Information asymmetry and equity issues. J. Financ. Quant. Anal. 1991, 26, 181–199. [Google Scholar] [CrossRef]

- Rosenstein, J.; Bruno, A.V.; Bygrave, W.D.; Taylor, N.T. The CEO, venture capitalists, and the board. J. Bus. Ventur. 1993, 8, 99–113. [Google Scholar] [CrossRef]

- Chahine, S.; Filatotchev, I.; Bruton, G.D.; Wright, M. “Success by Association”: The Impact of Venture Capital Firm Reputation Trend on Initial Public Offering Valuations. J. Manag. 2019, 0149206319847265. [Google Scholar] [CrossRef]

- Croce, A.; Ughetto, E. The role of venture quality and investor reputation in the switching phenomenon to different types of venture capitalists. J. Ind. Bus. Econ. 2019, 46, 191–227. [Google Scholar] [CrossRef]

- Chung, K.H.; Pruitt, S.W. A simple approximation of Tobin’s q. Financ. Manag. 1994, 70–74. [Google Scholar] [CrossRef]

- Geroski, P.A. Understanding the implications of empirical work on corporate growth rates. Manag. Decis. Econ. 2005, 26, 129–138. [Google Scholar] [CrossRef]

- Mowery, D.C.; Oxley, J.E.; Silverman, B.S. Strategic alliances and interfirm knowledge transfer. Strateg. Manag. J. 1996, 17, 77–91. [Google Scholar] [CrossRef] [Green Version]

- Tsai, W. Knowledge transfer in intraorganizational networks: Effects of network position and absorptive capacity on business unit innovation and performance. Acad. Manag. J. 2001, 44, 996–1004. [Google Scholar]

- Keller, W. Absorptive capacity: On the creation and acquisition of technology in development. J. Dev. Econ. 1996, 49, 199–227. [Google Scholar] [CrossRef]

- Veugelers, R. Internal R & D expenditures and external technology sourcing. Res. Policy 1997, 26, 303–315. [Google Scholar]

- Lee, P.M.; Pollock, T.G.; Jin, K. The contingent value of venture capitalist reputation. Strat. Organ. 2011, 9, 33–69. [Google Scholar] [CrossRef] [Green Version]

- Chen, J.; Chen, Y.; Vanhaverbeke, W. The influence of scope, depth, and orientation of external technology sources on the innovative performance of Chinese firms. Technovation 2011, 31, 362–373. [Google Scholar] [CrossRef] [Green Version]

- Agarwal, R.; Sarkar, M.; Echambadi, R. The conditioning effect of time on firm survival: An industry life cycle approach. Acad. Manag. J. 2002, 45, 971–994. [Google Scholar]

- Cooper, A.C.; Gimeno-Gascon, F.J.; Woo, C.Y. Initial human and financial capital as predictors of new venture performance. J. Bus. Ventur. 1994, 9, 371–395. [Google Scholar] [CrossRef]

- Cooper, A.C.; Gascon, F.J.G. Entrepreneurs, processes of founding, and new-firm performance. The State of the Art of Entrepreneurship; Sexton, D.L., Kasarda, J.D., Eds.; PWS-Kent: Boston, MA, USA, 1992; pp. 301–340. [Google Scholar]

- Bontis, N.; Wu, S.; Chen, M.C.; Cheng, S.J.; Hwang, Y. An empirical investigation of the relationship between intellectual capital and firms’ market value and financial performance. J. Intellect. Cap. 2005. [Google Scholar]

- Beard, D.W.; Dess, G.G. Corporate-level strategy, business-level strategy, and firm performance. Acad. Manag. J. 1981, 24, 663–688. [Google Scholar]

- Erhardt, N.L.; Werbel, J.D.; Shrader, C.B. Board of director diversity and firm financial performance. Corp. Gov. 2003, 11, 102–111. [Google Scholar] [CrossRef] [Green Version]

- Shrader, R.C.; Simon, M. Corporate versus independent new ventures: Resource, strategy, and performance differences. J. Bus. Ventur. 1997, 12, 47–66. [Google Scholar] [CrossRef]

- Beatty, R.P.; Ritter, J.R. Investment banking, reputation, and the underpricing of initial public offerings. J. Financ. Econ. 1986, 15, 213–232. [Google Scholar] [CrossRef] [Green Version]

- Brainard, W.C.; Tobin, J. Pitfalls in financial model building. Am. Econ. Rev. 1968, 58, 99–122. [Google Scholar]

- Bertoni, F.; Colombo, M.G.; Quas, A. The role of governmental venture capital in the venture capital ecosystem: An organizational ecology perspective. Entrep. Theory Pract. 2019, 43, 611–628. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Variables | β | p | β | p | β | p | β | p | β | p |

| (Constant) | 5.672 | 0.000 | 6.067 | 0.000 | 6.091 | 0.000 | 5.88 | 0.000 | 6.073 | 0.000 |

| Total invested capital | −0.25 *** | 0.000 | −0.22 *** | 0.000 | −0.20 *** | 0.000 | −0.20 *** | 0.000 | −0.202 *** | 0.000 |

| Intangible assets | −0.099 * | 0.018 | −0.088 * | 0.038 | −0.086 * | 0.043 | −0.084 * | 0.049 | −0.088 * | 0.039 |

| Leverage ratio | −0.02 | 0.565 | −0.022 | 0.523 | −0.022 | 0.526 | −0.021 | 0.535 | −0.022 | 0.524 |

| Firm age | −0.066 † | 0.096 | −0.05 | 0.215 | −0.045 | 0.272 | −0.049 | 0.225 | −0.05 | 0.215 |

| Number of employees | 0.019 | 0.662 | 0.021 | 0.622 | 0.025 | 0.567 | 0.021 | 0.623 | 0.021 | 0.624 |

| ROA | −0.056 | 0.172 | −0.053 | 0.201 | −0.045 | 0.279 | −0.052 | 0.203 | −0.053 | 0.203 |

| Agriculture and mining industry | −0.047 | 0.193 | −0.064 † | 0.091 | −0.071 † | 0.006 | −0.06 | 0.119 | −0.064 † | 0.095 |

| Construction industry | −0.018 | 0.601 | −0.019 | 0.587 | −0.022 | 0.525 | −0.019 | 0.590 | −0.019 | 0.586 |

| Manufacturing industry | 0.008 | 0.849 | −0.049 | 0.366 | −0.065 | 0.235 | −0.029 | 0.635 | −0.05 | 0.381 |

| Transportation industry | −0.062 † | 0.096 | −0.088 * | 0.032 | −0.095 * | 0.021 | −0.08 † | 0.057 | −0.088 * | 0.036 |

| Wholesale and retail industry | −0.029 | 0.440 | −0.05 | 0.214 | −0.062 | 0.122 | −0.045 | 0.269 | −0.05 | 0.216 |

| Finance and insurance industry | −0.16 *** | 0.000 | −0.19 *** | 0.000 | −0.20 *** | 0.000 | −0.18 *** | 0.000 | −0.19 *** | 0.000 |

| Services industry | 0.157 *** | 0.000 | 0.11 * | 0.023 | 0.095 † | 0.05 | 0.125 * | 0.017 | 0.11 * | 0.029 |

| Public administration industry | −0.027 | 0.432 | −0.035 | 0.313 | −0.048 | 0.174 | −0.033 | 0.350 | −0.035 | 0.313 |

| Number of patents | −0.002 | 0.950 | 0.000 | 0.995 | 0.01 | 0.772 | 0.03 | 0.579 | 0.000 | 0.998 |

| Reputation | 0.027 | 0.463 | 0.019† | 0.600 | 0.014 | 0.715 | 0.021 | 0.566 | 0.023 | 0.765 |

| R&D expense | 0.225 *** | 0.000 | 0.221 *** | 0.000 | 0.363 *** | 0.000 | 0.225 *** | 0.000 | 0.221 *** | 0.000 |

| Initial invested round | −0.089 † | 0.086 | −0.117 * | 0.049 | −0.061 | 0.370 | −0.09 | 0.158 | ||

| R&D expense × Round | −0.162 * | 0.033 | ||||||||

| Patent × Round | −0.046 | 0.454 | ||||||||

| Reputation × Round | −0.004 | 0.961 | ||||||||

| F-value | 13.699 *** | 13.096 *** | 12.718 *** | 12.427 *** | 12.387 *** | |||||

| R-square | 0.272 | 0.275 | 0.28 | 0.275 | 0.275 | |||||

| Adjusted R-square | 0.252 | 0.254 | 0.258 | 0.253 | 0.252 | |||||

| Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | ||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Variables | β | p | β | p | β | p | β | p | β | p |

| (Constant) | 5.672 | 0.000 | 6.067 | 0.000 | 6.091 | 0.000 | 5.88 | 0.000 | 6.073 | 0.000 |

| Total invested capital | −0.25 *** | 0.000 | −0.22 *** | 0.000 | −0.20 *** | 0.000 | −0.20 *** | 0.000 | −0.202 *** | 0.000 |

| Intangible assets | −0.099 * | 0.018 | −0.088 * | 0.038 | −0.086 * | 0.043 | −0.084 * | 0.049 | −0.088 * | 0.039 |

| Leverage ratio | −0.02 | 0.565 | −0.022 | 0.523 | −0.022 | 0.526 | −0.021 | 0.535 | −0.022 | 0.524 |

| Firm age | −0.066 † | 0.096 | −0.05 | 0.215 | −0.045 | 0.272 | −0.049 | 0.225 | −0.05 | 0.215 |

| Number of employees | 0.019 | 0.662 | 0.021 | 0.622 | 0.025 | 0.567 | 0.021 | 0.623 | 0.021 | 0.624 |

| ROA | −0.056 | 0.172 | −0.053 | 0.201 | −0.045 | 0.279 | −0.052 | 0.203 | −0.053 | 0.203 |

| Agriculture and mining industry | −0.047 | 0.193 | −0.064 † | 0.091 | −0.071 † | 0.006 | −0.06 | 0.119 | −0.064 † | 0.095 |

| Construction industry | −0.018 | 0.601 | −0.019 | 0.587 | −0.022 | 0.525 | −0.019 | 0.590 | −0.019 | 0.586 |

| Manufacturing industry | 0.008 | 0.849 | −0.049 | 0.366 | −0.065 | 0.235 | −0.029 | 0.635 | −0.05 | 0.381 |

| Transportation industry | −0.062 † | 0.096 | −0.088 * | 0.032 | −0.095 * | 0.021 | −0.08 † | 0.057 | −0.088 * | 0.036 |

| Wholesale and retail industry | −0.029 | 0.440 | −0.05 | 0.214 | −0.062 | 0.122 | −0.045 | 0.269 | −0.05 | 0.216 |

| Finance and insurance industry | −0.16 *** | 0.000 | −0.19 *** | 0.000 | −0.20 *** | 0.000 | −0.18 *** | 0.000 | −0.19 *** | 0.000 |

| Services industry | 0.157 *** | 0.000 | 0.11 * | 0.023 | 0.095 † | 0.05 | 0.125 * | 0.017 | 0.11 * | 0.029 |

| Public administration industry | −0.027 | 0.432 | −0.035 | 0.313 | −0.048 | 0.174 | −0.033 | 0.350 | −0.035 | 0.313 |

| Number of patents | −0.002 | 0.950 | 0.000 | 0.995 | 0.01 | 0.772 | 0.03 | 0.579 | 0.000 | 0.998 |

| Reputation | 0.027 | 0.463 | 0.019 † | 0.600 | 0.014 | 0.715 | 0.021 | 0.566 | 0.023 | 0.765 |

| R&D expense | 0.225 *** | 0.000 | 0.221 *** | 0.000 | 0.363 *** | 0.000 | 0.225 *** | 0.000 | 0.221 *** | 0.000 |

| Initial invested round | −0.089 † | 0.086 | −0.117 * | 0.049 | −0.061 | 0.370 | −0.09 | 0.158 | ||

| R&D expense × Round | −0.162 * | 0.033 | ||||||||

| Patent × Round | −0.046 | 0.454 | ||||||||

| Reputation × Round | −0.004 | 0.961 | ||||||||

| F-value | 13.699 *** | 13.096 *** | 12.718 *** | 12.427 *** | 12.387 *** | |||||

| R-square | 0.272 | 0.275 | 0.28 | 0.275 | 0.275 | |||||

| Adjusted R-square | 0.252 | 0.254 | 0.258 | 0.253 | 0.252 | |||||

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Jeong, J.; Kim, J.; Son, H.; Nam, D.-i. The Role of Venture Capital Investment in Startups’ Sustainable Growth and Performance: Focusing on Absorptive Capacity and Venture Capitalists’ Reputation. Sustainability 2020, 12, 3447. https://doi.org/10.3390/su12083447

Jeong J, Kim J, Son H, Nam D-i. The Role of Venture Capital Investment in Startups’ Sustainable Growth and Performance: Focusing on Absorptive Capacity and Venture Capitalists’ Reputation. Sustainability. 2020; 12(8):3447. https://doi.org/10.3390/su12083447

Chicago/Turabian StyleJeong, Jihye, Juhee Kim, Hanei Son, and Dae-il Nam. 2020. "The Role of Venture Capital Investment in Startups’ Sustainable Growth and Performance: Focusing on Absorptive Capacity and Venture Capitalists’ Reputation" Sustainability 12, no. 8: 3447. https://doi.org/10.3390/su12083447

APA StyleJeong, J., Kim, J., Son, H., & Nam, D. -i. (2020). The Role of Venture Capital Investment in Startups’ Sustainable Growth and Performance: Focusing on Absorptive Capacity and Venture Capitalists’ Reputation. Sustainability, 12(8), 3447. https://doi.org/10.3390/su12083447