1. Introduction

Environmental problems such as ecological imbalance, resource exhaustion, and environmental pollution have become global economic and political problems because they are closely related to social development and human survival [

1,

2]. The efficient green economy (GE), which boasts low energy consumption, low pollution, and low emissions, has become a necessary choice and direction for China’s economic advancement and a channel to help developing countries achieve sustainable development [

3]. The development of the GE is inseparable from the support of green finance (GF). On the basis of traditional finance, GF regards social responsibility and environmental protection interests as the core of development, and has become a new growth point and a new engine for promoting the development of the GE [

4,

5,

6]. In August 2016, seven ministries and commissions of China issued Guidelines for Establishing the Green Financial System which explicitly proposed to promote green economic transformation through constructing a GF system. In practice, all kinds of GF investment are also increasing. According to public data, the balance of the green credit of 21 major domestic banks reached ¥8.22 trillion by the end of June 2017.

GF is an emerging concept. Early research focused on the theoretical analysis of the concept and system structure [

7,

8,

9]. Soppe (2009) [

10] introduced the concept of sustainability into financial practice and financial academic literature. Some researchers have studied profitability in the GF development of financial institutions. Chami et al. (2002) [

11] and Scholtens and Dam (2007) [

12] revealed that financial institutions who implemented GF and the Equator Principles could gain social recognition and renown, enabling them to successfully carry out financial business and improve financial performance. For GF instruments, Climent and Soriano (2011) [

13] investigated and compared the performance between US green mutual funds and other socially responsible investing mutual funds by using a CAPM-based methodology, concluding that green mutual funds had poorer performance than other conventional funds. Based on daily closing prices of the S&P Green Bond index, Pham (2016) [

14] identified the fluctuations of the green bond market over the period 2010–2015. Antimiani et al. (2017) [

15] developed a computable general equilibrium model of dynamic climate and economy to research how the Green Climate Fund potentially compensated for adaptation and mitigation behaviors under the global climate framework. Cui and Huang (2018) [

16] discussed several schemes for raising the public finance of the Green Climate Fund among developed countries, namely, the historical emission responsibility (HR), ability to pay (AP), United Nations (UN) membership dues, Official Development Assistance (ODA), and Global Environment Facility (GEF) approaches. Among these schemes, HR and AP have been widely examined, whereas the remaining three schemes draw lessons from ongoing international financing mechanisms. Environmental pollution liability insurance could be a useful tool to mitigate the problems of environmental risk [

17,

18].

Recently, scholars have become increasingly interested in the relationship between GF and the GE. Liu et al. (2019) [

19] discussed the influence of GF on GE by establishing a super-efficient slack-based model and an index system for 30 Chinese provinces. After discussing the need for greening the financial system and the role of financial governance, Volz (2018) [

20] believed that the financial sector would have to play a primary role in this green transformation. However, there has been little discussion about them so far.

Research on the relationship between economic growth and financial development dates back to the eighteenth century, when Smith (1776) [

21] studied economic growth and capital accumulation. At the beginning of the twentieth century, Schumpeter (1911) [

22] explored the mechanism for banks to promote economic growth. It has been recognized that financial development can facilitate economic growth, and a causality relationship lies between them [

23,

24]. Other scholars focused on the relationship between financialization and the real economy. After the financial crisis (i.e. 2008–2009), most studies argued that financialization weakened the investment that supported real economic growth [

25]. Nevertheless, Shen and Lee (2006) [

26] examined the panel data on 46 countries over 1976–2001 and found that financial development and economic growth shared an inverted-U-shaped relationship. Law and Singh (2014) [

27] further determined this threshold effect with the aid of a dynamic panel threshold model.

GF evaluation is the foundation and essential scientific basis for the management of GF development. However, due to the lack of clear quantitative standards and statistical data, the research on GF evaluation still faces many difficulties. Scholars mostly carried out case studies on the concept and the economic and environmental benefits of GF, but they have barely quantitatively measured the development level of GF [

28]. In addition, the relationship between GF and the GE is rarely discussed. With the aim of more accurately revealing the status and level of GF development in China, this study constructs a quantitative evaluation system from multiple dimensions under the existing conditions and integrated actual development of GF in developing countries. It also discusses the coordination relationship between GF and the GE. This study can provide valuable reference for promoting the development of GF.

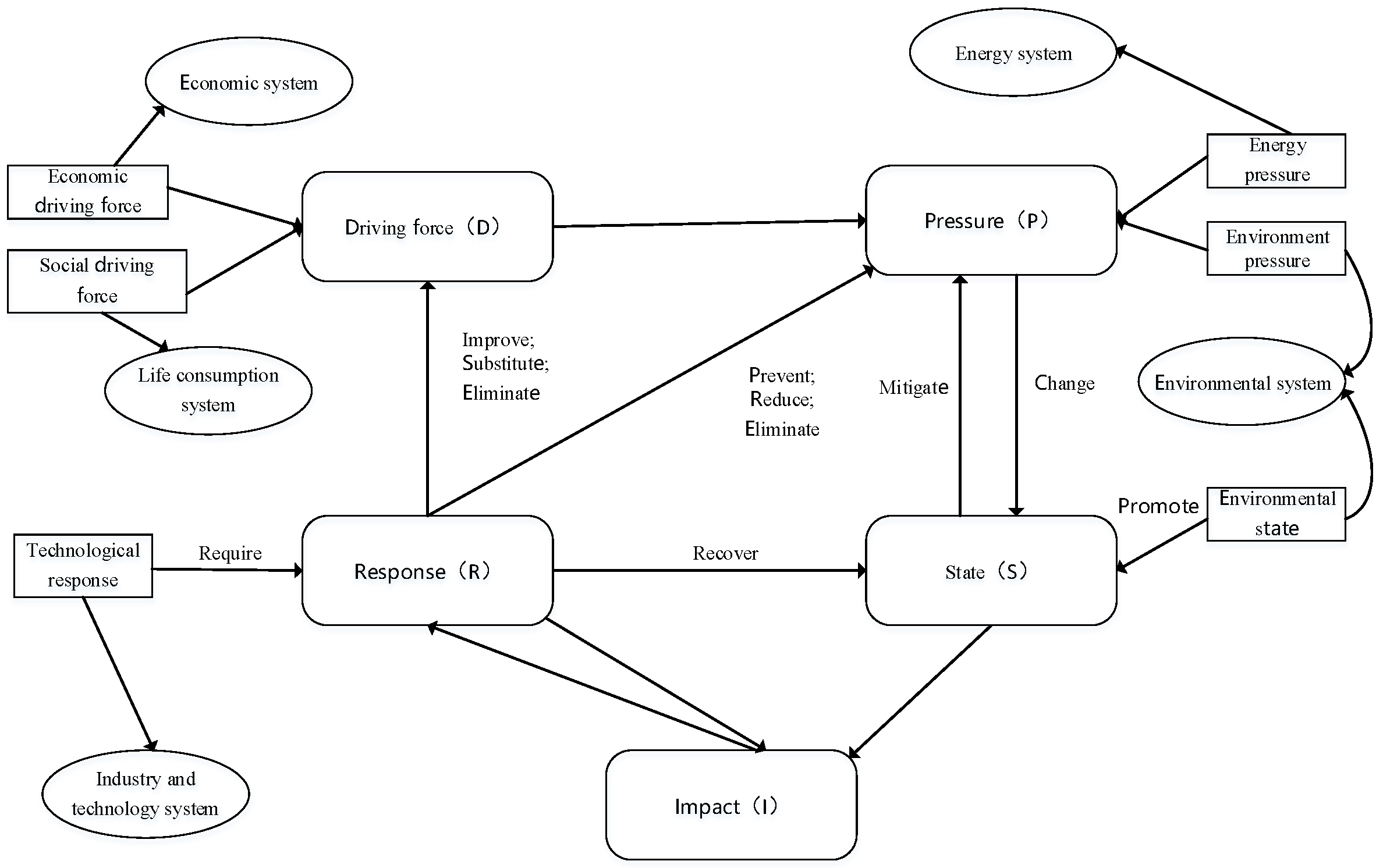

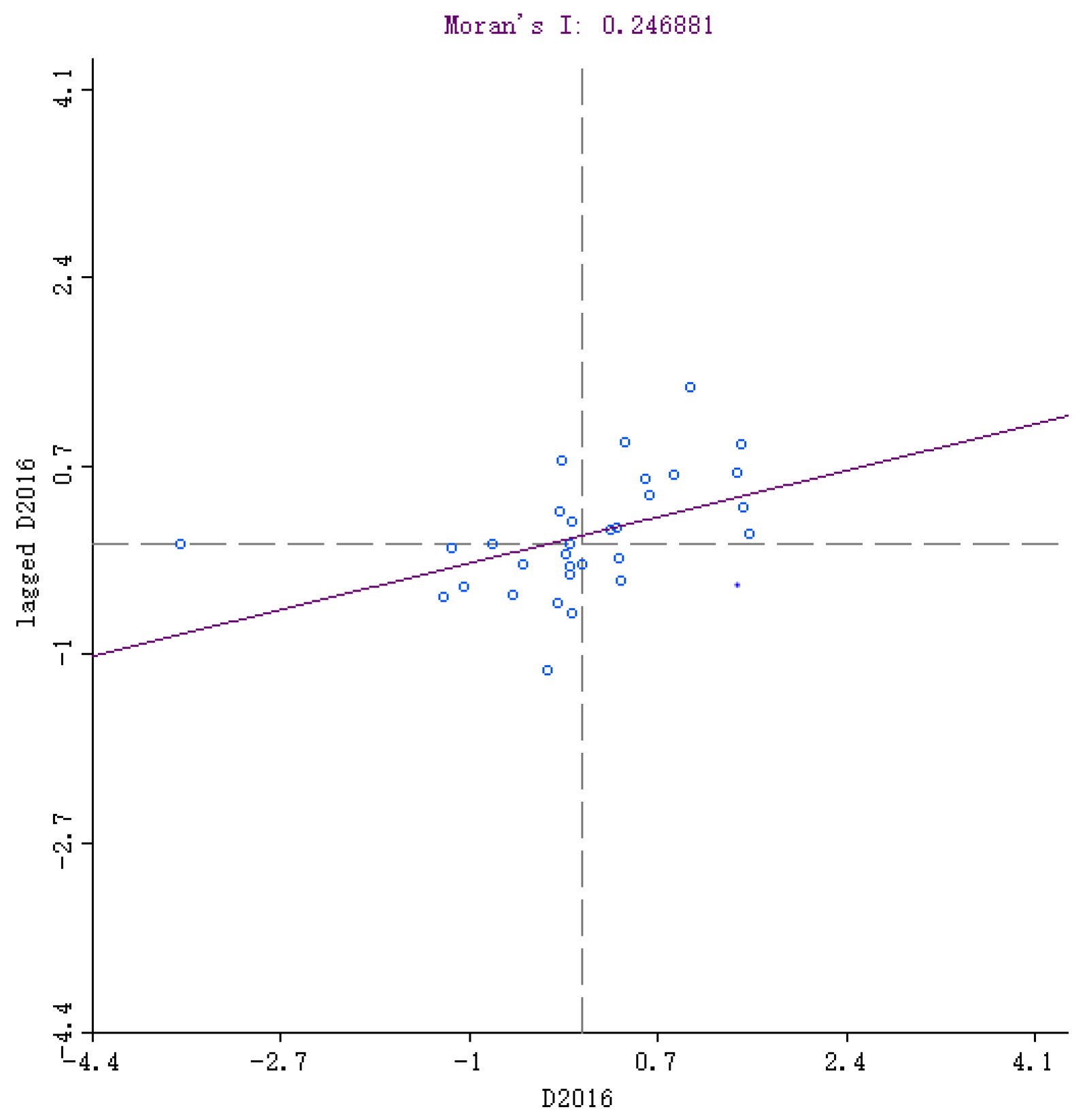

While describing and analyzing coordinated development between the past and the present, most existing research has regarded each region as independent, ignoring the fact that regions interacted with each other spatially. Few researchers forecasted the future coordination state, not to mention investigated the spatial distribution and dynamic evolution of coordination degree considering the spatial spillover effect. It is essential to study the coupling relationship between GF and the GE from a broader viewpoint, instead of a local one. Moreover, it is also necessary to especially study the temporal and spatial variations in the coupling degree and clustering patterns. Aiming to temporally and spatially reveal the coupling coordination between GF and the GE in China, this study evaluated their relationship over the period 2007–2016 by putting forward a coupling coordination degree model on the basis of a physics coupling model. In order to explore the clusters, spatial association, and spatial dynamics for the coupling coordination, the spatial distribution was described and visualized by means of an exploratory spatial data analysis (ESDA) proposed by the authors of [

29]. Moreover, the trend of coordination value was forecasted by using a space Markov chain and a local indicators of spatial association (LISA) Markov chain. The study provides a scientific basis for the practice of GF and sustainable economic development in developing countries.

This study includes five sections. In

Section 2, index systems for green finance and the green economy are established. This section gives theoretical foundation regarding the mechanism of coordination between GF and the GE. In

Section 3, the materials and methods are introduced, specifically, the entropy method, the space Markov chain, the LISA Markov chain and the ESDA are described in detail. In

Section 4, the results of coupling coordination, spatial analysis, and spatial dynamics are presented on the basis of the model put forward in

Section 3. Finally, conclusions are given in

Section 5.

5. Discussion and Conclusions

This paper aimed at investigating the coupling coordination between the Chinese GF and GE systems. Since GF and the GE are coupled systematically and complexly, it was crucial to employ the coupling coordination degree model in order to grasp the cooperative interaction and feedback among different determinants. Besides, for overcoming subjectivity or computational complexity, the study determined the weights of indicators in the GE system by means of an entropy weighting method. This study is of practical significance for investigation and research on the coordinated development of GF and the GE.

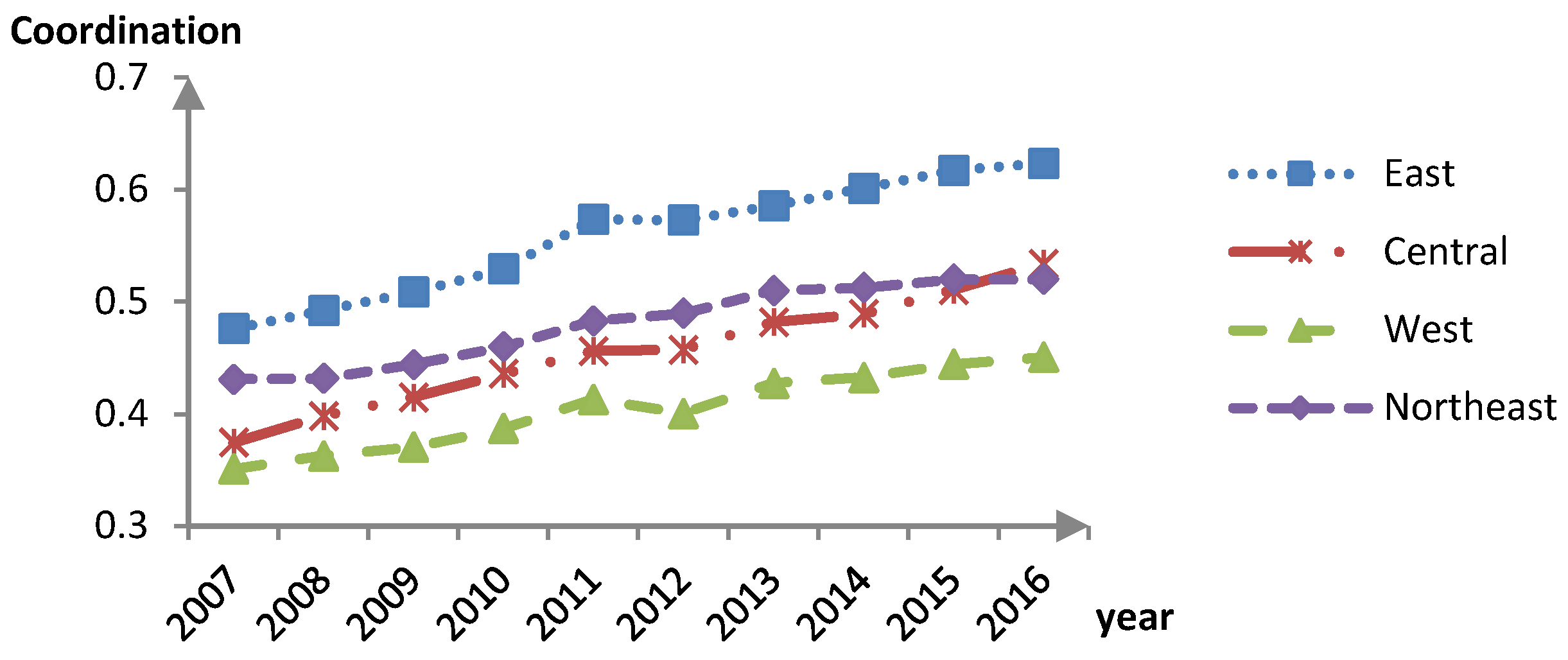

The Chinese GF and GE share a complex relationship, and their coupling coordination degree exhibits an upward trend. However, the Eastern, Central, Western and Northeastern regions still differ in terms of coordination states. To be specific, the Eastern region boasts the highest level of coordinated development of GF and the GE, reaching 0.6 in 2014 and realizing the transformation from barely balanced development to favorably balanced development. At present, the coordination values of GF and the GE in the Central and Northeastern regions lie between 0.5 and 0.6, and they are still in the phase of barely balanced development. The coordinated development of GF and GE in the western region is relatively backward and remains in the phase of slightly unbalanced development.

Compared with previous studies, it is innovative and enlightening to analyze the spatial correlation of coupling coordination between various regions. Researchers have probed into the evolving distribution of high-pollution industries [

50,

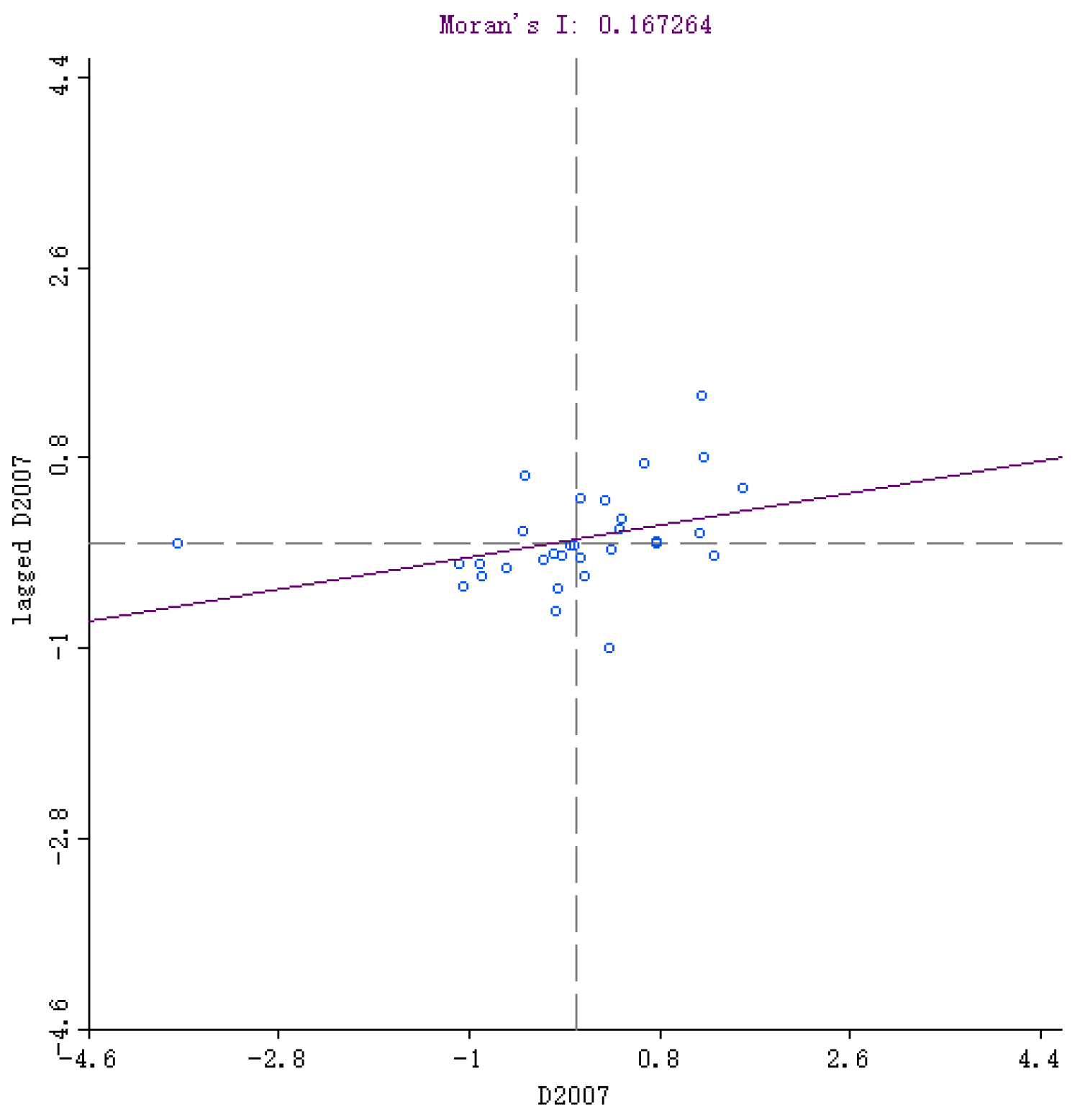

51]. In fact, for the sake of local green development, the local governments of China’s developed areas would rather transfer high-pollution industries to developing areas than reduce pollution. This phenomenon can explain the evolving distribution. In terms of global correlation, the differences of coordination between GF and the GE among the provinces in China are not randomly distributed in space, but positively correlated, showing a strong spatial dependence on the whole. From the perspective of local correlation, most provinces are in HH and LL clustering patterns, and the spatial clustering patterns of most provinces and their adjacent provinces experience no transfer and remain spatially stable.

The spatial clustering pattern evolution of the coordination values of GF and the GE were analyzed on the basis of the LISA Markov chain. The results reveal that the clustering pattern of the coordination values of the GF and GE of 30 Chinese provinces remain stable, especially the HH clustering pattern which reached 0.9643.

Some developed countries are more mature in green finance and green economy development and may provide some experience to China. For example, the United States, as a developed economy, had an early start in green finance. Since the 1970s, the U.S. Congress has passed more than 20 laws on environmental protection related to water environment, air pollution, waste management, and the cleanup of polluted sites, etc. In 1980, the U.S. federal government introduced the Comprehensive Environmental Response, Compensation and Liability Act, which makes banks responsible for environmental pollution caused by their customers. In addition, the European Union (EU) attaches great importance to the development of green finance, with a mature legal system and active product innovation. The EU incentivizes green projects through tax incentives and government guarantees. For example: the German government gives certain subsidies and interest rates for loans for green projects; the European Union provides tax incentives for green credits and securitized products; and the British government uses a “loan guarantee scheme” to support small and medium-sized enterprises (SMEs), especially environmental SMEs.

In recent years, green finance has developed rapidly in countries with an emerging economy. The Central Bank of Brazil introduced a new regulatory approach in April 2014 that required commercial banks to develop strategic actions and governance frameworks for environmental and social risk management and to implement them as core elements of overall risk management. Currently about 10% of bank loans in Brazil are classified as green loans. In particular, the central bank of Bangladesh has made increasing financial inclusion an explicit objective of monetary policy and has provided credit guidelines for commercial banks that include new energy, pollution control, and energy efficiency, etc. The share of green credit now stands at 5%.

Compared to these countries discussed above, there are a number of problems and challenges in green finance development for China, such as: (a) the overall proportion of investment and loans for green projects by financial institutions is still low; (b) the lack of a green financial indicator system and incentive mechanisms; (c) the government’s policy of supporting green industries is inadequate; (d) the failure to establish a virtuous circular market mechanism for building ecological civilization. Therefore, it is necessary for China to learn from the experience of some developed countries and further improve the construction of green finance laws and regulations, insist on market-based operation, and encourage market innovation as a long-term mechanism for optimizing the allocation of green finance funds, enhancing the efficiency of the use of green finance funds and building China’s green finance development.

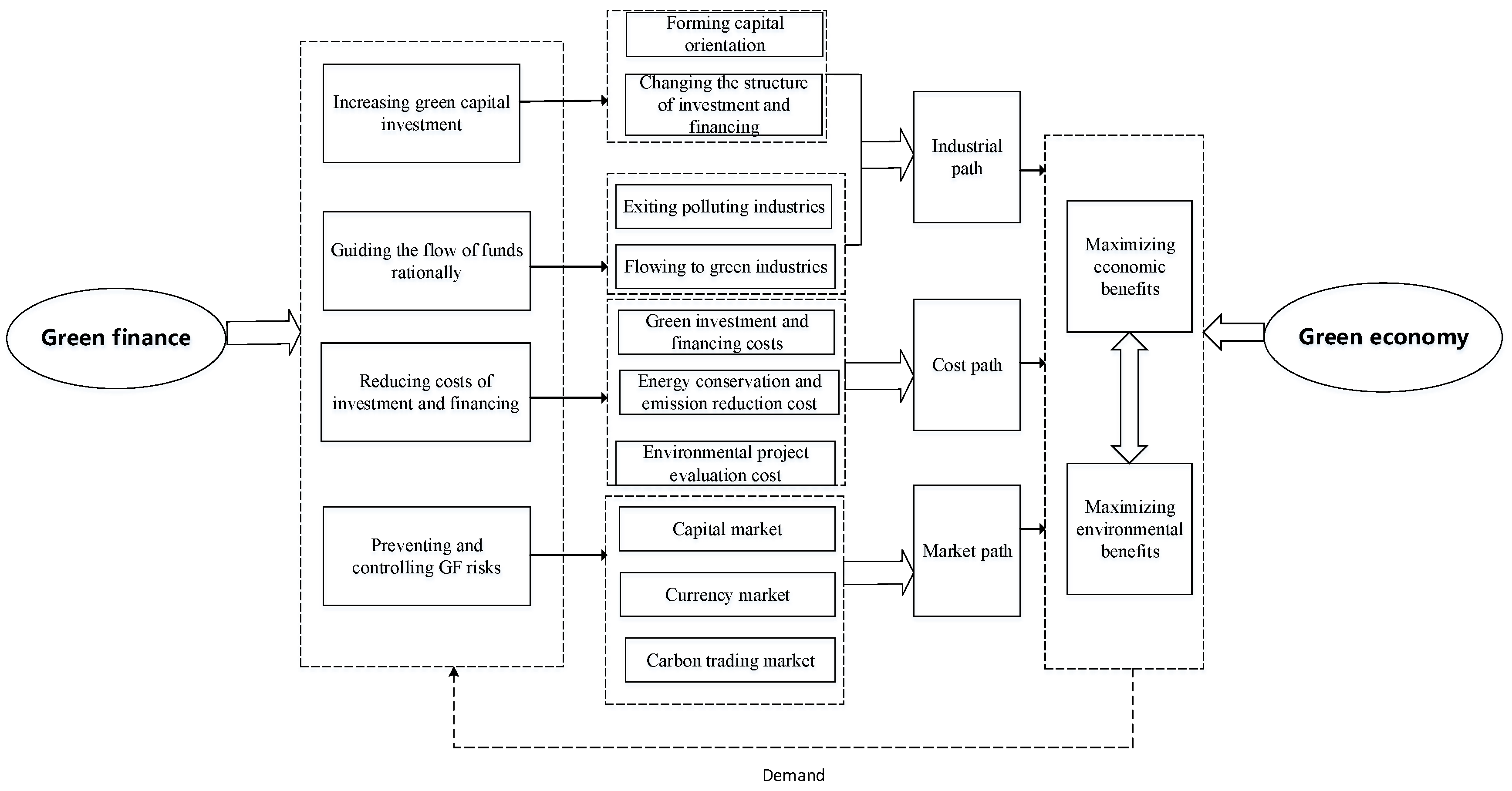

This paper may contribute to the realization of social and economic sustainable development through exploring the coronation between green finance and the green economy. Our results prove that there is a certain gap in the coordinated development of green finance and the green economy for 30 provinces in China. Therefore, in order to further narrow this gap, it is necessary to strengthen the construction of a diversified green financial system in the central and western regions, for example, by vigorously develop green bonds, energy conservation and environmental protection risk investment funds, and introducing clean development trading projects, as well as avoiding the transfer of polluting industries to the central and western regions, especially in areas with weak environmental and ecological carrying capacity, so as to achieve comprehensive coordination between regions, promote green finance and the green economy, and achieve the country’s overall social sustainable development.

In addition, this paper also provides some suggestions for the government about how to effectively execute financial policies. Specifically, policy-makers need to recognize the coupling and coordination between green finance and the green economy. It is important not to focus only on changes in the scale of one, but to make it a policy objective to promote coordinated development between the two. The first suggestion is to improve the investment channels of the green financial system and raise the level of investment; the second is to improve the relevant policies and provide policy support for the development of green industries in order to promote the balanced development of the two systems. Also, the regulator should establish a monitoring and feedback system between the two systems and enhance the operational efficiency of the coupled system through a positive feedback effect. It is important to establish and improve a system for monitoring the use of funds by enterprises, earmarking funds for green enterprises and improving the efficiency of their use. A feedback mechanism should also be improved to fully receive feedback on the effectiveness of the use of green finance policies. Policies already enacted should be revised based on market feedback to better promote green industries. At the same time, green financial institutions should be guided to establish information service platforms, to strengthen exchanges with green enterprises, and to better understand the financing needs of energy-saving and environmental protection enterprises, and to provide them with matching financing solutions.

Our application of the spatial Markov approach to the field of environmental finance, in particular to the coordinated development of GF and the GE, provides new ideas and insights for enriching the research literature on green finance and the green economy and coordinated development. Therefore, in order to better achieve the coordinated development of green finance and the green economy, we will further explore the path of green finance for the green economy and the dynamic coordination between the two.

However, this study has certain limitations. First, in terms of the construction of green finance indicators, generally, the green financial system can be divided into five areas, namely, green credit, green securities, green insurance, green investment, and carbon finance. But this paper does not include carbon finance in the indicator system due to a serious lack of data, even if only a small percentage of the development of green finance is in carbon finance. Second, this paper evaluates the spatial distribution difference and dynamic evolution trend of the coordination by introducing global/local spatial autocorrelation, a space Markov chain, and a local indicators of spatial association Markov chain. However, considering the accuracy of results, we only predict coordination in the short term, but not in the long term (e.g., over the next 10–20 years). In the future, we hope to take a more appropriate approach to predicting the long-term degree of coordination. Third, this paper predicts the degree of coordination between GF and the GE, but there is no further research on the early warning model of coordination. Therefore, in the future we will explore the early warning model of coordinated development of GF and the GE to provide better policy recommendations for sustainable development.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}