Investor Sentiment and Price Discrepancies between Common and Preferred Stocks in Korea

Abstract

:1. Introduction

2. Preferred Stocks in Korea and Price Discrepancies

3. Data and Methods

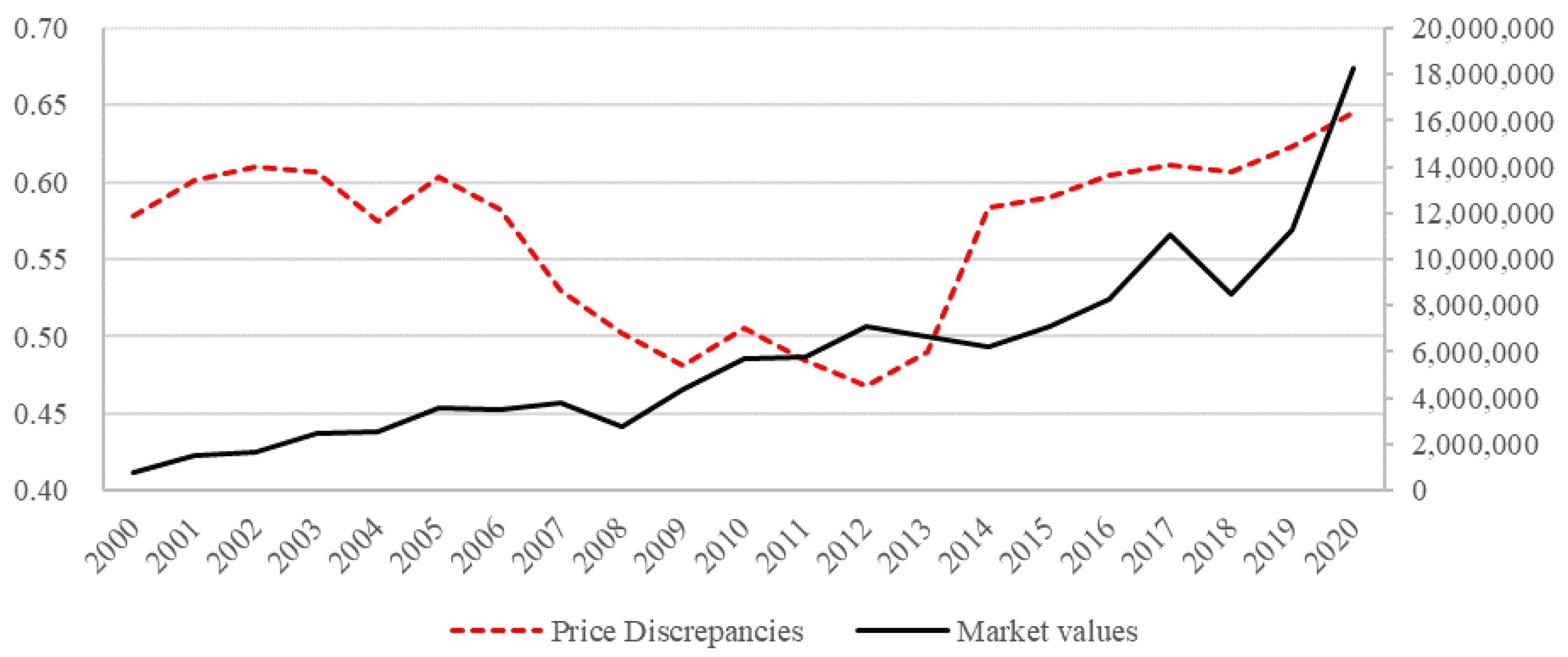

4. Empirical Results

5. Conclusions and Suggestions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Nenova, T. The value of corporate voting rights and control: A cross-country analysis. J. Financ. Econ. 2003, 68, 325–351. [Google Scholar] [CrossRef]

- Doidge, C.U.S. Cross-listings and the private benefits of control: Evidence from dual-class firms. J. Financ. Econ. 2004, 72, 519–553. [Google Scholar] [CrossRef]

- Masulis, W.R.; Wang, C.; Xie, F. Agency problems at dual-class companies. J. Financ. 2009, 64, 1697–1727. [Google Scholar] [CrossRef]

- Gompers, P.A.; Ishii, J.; Metrick, A. Extreme governance: An analysis of dual-class firms in the United States. Rev. Financ. Stud. 2010, 23, 1051–1088. [Google Scholar] [CrossRef]

- Zingales, L. What determines the value of corporate votes? Q. J. Econ. 1995, 110, 1047–1073. [Google Scholar] [CrossRef]

- Schultz, P.; Shive, S. Mispricing of dual-class shares: Profit opportunities, arbitrage, and trading. J. Financ. Econ. 2010, 98, 524–549. [Google Scholar] [CrossRef]

- Baker, M.; Wurgler, J. Investor sentiment and the cross-section of stock returns. J. Financ. 2006, 61, 1645–1680. [Google Scholar] [CrossRef] [Green Version]

- Kumar, A.; Lee, C.M.C. Retail investor sentiment and return comovements. J. Financ. 2006, 61, 2451–2486. [Google Scholar] [CrossRef]

- Baker, M.P.; Wurgler, J.A. Investor sentiment in the stock market. J. Econ. Perspect. 2007, 21, 129–152. [Google Scholar] [CrossRef] [Green Version]

- Baker, M.; Wurgler, J.; Yuan, Y. Global, local, and contagious investor sentiment. J. Financ. Econ. 2012, 104, 272–287. [Google Scholar] [CrossRef] [Green Version]

- Stambaugh, R.F.; Yu, J.; Yuan, Y. The short of it: Investor sentiment and anomalies. J. Financ. Econ. 2012, 104, 288–302. [Google Scholar] [CrossRef] [Green Version]

- Zingales, L. The value of the voting right: A study of the milan stock exchange experience. Rev. Financ. Stud. 1994, 7, 125–148. [Google Scholar] [CrossRef] [Green Version]

- Neumann, R. Price differentials between dual-class stocks: Voting premium or liquidity discount? Eur. Financ. Manag. 2003, 9, 315–332. [Google Scholar] [CrossRef]

- Ryu, D.; Ryu, D.; Yang, H. Investor sentiment, market competition, and financial crisis: Evidence from the Korean stock market. Emerg. Mark. Financ. Trade 2020, 56, 1804–1816. [Google Scholar] [CrossRef]

- Chong, T.T.-L.; Ng, W.-K. Technical analysis and the London stock exchange: Testing the MACD and RSI rules using the FT30. Appl. Econ. Lett. 2008, 15, 1111–1114. [Google Scholar] [CrossRef]

- Chen, H.; Chong, T.T.-L.; Duan, X. A principal-component approach to measuring investor sentiment. Quant. Financ. 2010, 10, 339–347. [Google Scholar] [CrossRef]

- Yang, C.; Gao, B. The term structure of sentiment effect in stock index futures market. N. Am. J. Econ. Financ. 2014, 30, 171–182. [Google Scholar] [CrossRef]

- Baker, M.; Stein, J. Market liquidity as a sentiment indicator. J. Financ. Mark. 2004, 7, 271–299. [Google Scholar] [CrossRef] [Green Version]

- Liao, T.-L.; Huang, C.-J.; Wu, C.-Y. Do fund managers herd to counter investor sentiment? J. Bus. Res. 2011, 64, 207–212. [Google Scholar] [CrossRef]

- Yang, C.; Zhang, R. Does mixed-frequency investor sentiment impact stock returns? Based on the empirical study of MIDAS regression model. Appl. Econ. 2014, 46, 966–972. [Google Scholar] [CrossRef]

- Kim, K.; Ryu, D.; Yang, H. Investor sentiment, stock returns, and analyst recommendation changes: The KOSPI stock market. Invest. Anal. J. 2019, 48, 89–101. [Google Scholar] [CrossRef]

- Ryu, D.; Kim, H.; Yang, H. Investor sentiment, trading behavior and stock returns. Appl. Econ. Lett. 2017, 24, 826–830. [Google Scholar] [CrossRef]

- Yang, H.; Ryu, D.; Ryu, D. Investor sentiment, asset returns and firm characteristics: Evidence from the Korean stock market. Invest. Anal. J. 2017, 46, 132–147. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Type | Cash Flow Rights | Dividend Ratio | Voting Rights | Residual Claims |

|---|---|---|---|---|

| Preferred stock | Almost same | High (relatively) | None | Senior |

| Common stock | Almost same | Low (relatively) | Yes | Junior |

| Factors | Definitions |

|---|---|

| Relative Strength Index (RSI) | |

| Psychological line index (PLI) | |

| Logarithm of trading volume (LTV) | |

| Adjusted turnover rate (ATR) | |

| Buy-sell imbalance of individual investors (IBSI) |

| Variable | Definitions |

|---|---|

| Price discrepancies (Dependent variable) | 1. (Ratio) Preferred stock price divided by common stock price. |

| 2. (Difference) Common stock price minus preferred stock price. | |

| Sentiment (Main variable) | Consider the five sentiment proxies: relative strength index (RSI), psychological line index (PLI), adjusted turnover rate (ATR), the logarithm of trading volume (LTV), and the buy-sell imbalance of individual investors (IBSI), simultaneously, through the principal component analysis. Then, set the regression model with the market risk factor and adopt the residual as sentiment measure for individual stock. |

| Volume | Total number of shares of a security that were traded during the day. |

| Outstanding | Number of the firms’ outstanding common (preferred) stock. |

| Size | Natural log of total assets. |

| Lev | Total debt divided by total assets. |

| ΔSentiment | Difference between common and preferred stock characteristics for each variable. |

| ΔVolume | |

| ΔOutstanding |

| Panel A. Preferred Stock (N = 325,198) | |||||||

| Variable | Mean | Min. | P25 | Median | P75 | Max. | Std. |

| Sentiment | −0.0176 | −7.8674 | −0.9019 | −0.0851 | 0.7983 | 13.6855 | 1.3019 |

| Price | 37,009 | 97 | 3359 | 10,400 | 33,225 | 1,419,971 | 90,807 |

| Volume | 30,943 | 1 | 640 | 3590 | 15,619 | 11,126,669 | 154,459 |

| Outstanding | 5,958,453 | 9074 | 589,875 | 2,067,500 | 4,021,927 | 903,629,000 | 38,030,064 |

| Panel B. Common Stock (N = 325,198) | |||||||

| Variable | Mean | Min. | P25 | Median | P75 | Max. | Std. |

| Sentiment | 0.0195 | −14.0459 | −0.9511 | −0.0255 | 0.9422 | 12.0080 | 1.3835 |

| Price | 74,719 | 108 | 6169 | 20,000 | 66,007 | 3,687,967 | 180,659 |

| Volume | 489,462 | 1 | 25,910 | 123,357 | 414,488 | 205,995,279 | 1,880,330 |

| Outstanding | 68,541,398 | 624,615 | 11,152,546 | 27,543,086 | 74,958,735 | 6,419,324,700 | 279,701,268 |

| Panel C. Dependent and Control Variables (N = 325,198) | |||||||

| Variable | Mean | Min. | P25 | Median | P75 | Max. | Std. |

| ΔSentiment | 0.0371 | −15.3646 | −0.7588 | 0.0416 | 0.8449 | 15.1008 | 1.2757 |

| Price discrepancies ratio | 0.5609 | 0.1191 | 0.4287 | 0.5415 | 0.6752 | 1.0000 | 0.1800 |

| Price discrepancies | 37.7099 | 0.0000 | 2.1070 | 8.3000 | 31.4510 | 2307.4400 | 96.2360 |

| ΔVolume | 0.4585 | −6.9137 | 0.0214 | 0.1113 | 0.3868 | 202.9676 | 1.8104 |

| ΔOutstanding | 0.0626 | 0.0004 | 0.0095 | 0.0240 | 0.0718 | 5.5157 | 0.2429 |

| Firm Size | 21.7619 | 17.2473 | 20.4452 | 21.7584 | 23.0776 | 26.6588 | 1.7694 |

| Leverage | 0.5847 | 0.1300 | 0.4282 | 0.6058 | 0.7418 | 1.5006 | 0.2136 |

| Dependent Variable: Price Discrepancies Ratio (Preferred Stock Price Divided by Common Stock Price) | ||||

|---|---|---|---|---|

| Variable | (1) | (2) | (3) | (4) |

| ΔSentiment | −0.009 *** (−38.42) | −0.009 *** (−38.24) | −0.009 *** (−37.66) | −0.01 *** (−41.58) |

| ΔVolume | −0.003 *** (−13.77) | −0.003 *** (−17.25) | ||

| ΔOutstanding | 0.051 *** (39.38) | 0.059 *** (41.56) | 0.11 *** (77.08) | |

| Size | −0.026 *** (−135.9) | |||

| Lev | 0.089 *** (57.36) | |||

| Intercept | 0.561 *** (1781.3) | 0.558 *** (1719.18) | 0.559 *** (1701.42) | 1.071 *** (272.56) |

| Adj. R2 | 0.005 | 0.009 | 0.01 | 0.063 |

| F-Value | 1476.39 (Pr. < 0.0001) | 1516.98 (Pr. < 0.0001) | 1075.08 (Pr. < 0.0001) | 4393.69 (Pr. < 0.0001) |

| N | 325,198 | 325,198 | 325,198 | 324,536 |

| Dependent Variable: Price Discrepancies Ratio (Preferred Stock Price Divided by Common Stock Price) | ||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Variable/Year | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | |||||||||

| ΔSentiment | −0.017 *** (−16.04) | −0.015 *** (−13.28) | −0.013 *** (−10.42) | −0.017 *** (−14.18) | 0.004 *** (3.46) | −0.005 *** (−6.6) | −0.003 *** (−3.31) | −0.009 *** (−10.94) | −0.011 *** (−10.63) | −0.002 ** (−2.56) | −0.007 *** (−6.89) | |||||||||

| ΔVolume | 0.003 *** (5.5) | 0.001 ** (2.27) | −0.008 *** (−4.09) | −0.033 *** (−19.12) | −0.017 *** (−8.86) | −0.024 *** (−26.52) | −0.03 *** (−9.34) | −0.002 *** (−2.93) | −0.02 *** (−21.35) | −0.008 *** (−15.09) | −0.012 *** (−8.32) | |||||||||

| ΔOutstanding | 0.242 *** (8.23) | 0.313 *** (10.03) | 0.59 *** (13.63) | 0.644 *** (17.15) | 0.547 *** (17.54) | 1.033 *** (35.36) | 0.444 *** (16.28) | 1.051 *** (42.55) | 1.379 *** (52.62) | 0.724 *** (28.54) | 0.183 *** (9.32) | |||||||||

| Size | −0.036 *** (−37.7) | −0.059 *** (−48.77) | −0.055 *** (−43.86) | −0.043 *** (−36.21) | −0.04 *** (−38.34) | −0.02 *** (−23.46) | −0.008 *** (−8.75) | −0.025 *** (−32.71) | −0.05 *** (−55.81) | −0.046 *** (−51.87) | −0.043 *** (−48.96) | |||||||||

| Lev | 0.053 *** (8.54) | 0.089 *** (9.62) | −0.009 (−1.22) | −0.089 *** (−10.97) | −0.048 *** (−6.43) | −0.076 *** (−11.93) | 0.135 *** (22.36) | −0.047 *** (−8.4) | −0.027 *** (−3.81) | 0.051 *** (7.98) | 0.102 *** (15.7) | |||||||||

| Intercept | 1.285 *** (67.89) | 1.772 *** (79.09) | 1.752 *** (74.08) | 1.55 *** (69.05) | 1.427 *** (71.18) | 1.047 *** (63.48) | 0.693 *** (36.42) | 1.056 *** (69.38) | 1.56 *** (87.32) | 1.424 *** (79.85) | 1.386 *** (74.53) | |||||||||

| Adj. R2 | 0.116 | 0.191 | 0.2 | 0.206 | 0.151 | 0.107 | 0.051 | 0.129 | 0.224 | 0.135 | 0.128 | |||||||||

| F-Value | 374.67 (Pr. < 0.0001) | 648.48 (Pr. < 0.0001) | 663.36 (Pr. < 0.0001) | 708.64 (Pr. < 0.0001) | 498.66 (Pr. < 0.0001) | 380.93 (Pr. < 0.0001) | 167.2 (Pr. < 0.0001) | 503.58 (Pr. < 0.0001) | 955.11 (Pr. < 0.0001) | 572.16 (Pr. < 0.0001) | 522.32 (Pr. < 0.0001) | |||||||||

| N | 14,311 | 13,676 | 13,214 | 13,632 | 14,048 | 15,911 | 15,440 | 17,020 | 16,518 | 18,311 | 17,702 | |||||||||

| Variable/Year | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | ||||||||||

| ΔSentiment | −0.022 *** (−18.69) | −0.001 (−0.68) | −0.004 *** (−4.39) | 0.005 *** (6.02) | −0.005 *** (−4.94) | −0.003 *** (−3.31) | −0.006 *** (−5.79) | −0.004 *** (−3.89) | −0.01 *** (−10.1) | −0.007 *** (−6.31) | ||||||||||

| ΔVolume | −0.005 *** (−11.2) | −0.007 *** (−6.7) | −0.001 (−0.66) | 0.001 (0.81) | −0.007 *** (−5.27) | −0.03 *** (−9.34) | −0.025 *** (−10.93) | −0.013 *** (−7.53) | −0.014 *** (−6.86) | 0.002 ** (2.28) | ||||||||||

| ΔOutstanding | 0.316 *** (15.22) | 0.436 *** (20.82) | 0.67 *** (27.75) | 0.475 *** (19.1) | 0.42 *** (17.42) | 0.444 *** (16.28) | 0.254 *** (12.54) | 0.093 *** (22.47) | 0.114 *** (26.21) | 0.08 *** (18.5) | ||||||||||

| Size | −0.059 *** (−61.05) | −0.06 *** (−62.81) | −0.048 *** (−51.33) | −0.02 *** (−23.82) | −0.015 *** (−17.66) | −0.008 *** (−8.75) | −0.017 *** (−18.81) | −0.025 *** (−27.2) | −0.036 *** (−40.68) | −0.029 *** (−26.9) | ||||||||||

| Lev | 0.141 *** (20.11) | 0.26 *** (36.19) | 0.194 *** (30.03) | 0.169 *** (30.31) | 0.146 *** (26.25) | 0.135 *** (22.36) | 0.183 *** (28.17) | 0.238 *** (35.18) | 0.331 *** (49.72) | 0.349 *** (44.53) | ||||||||||

| Intercept | 1.674 *** (82.36) | 1.607 *** (79.7) | 1.394 *** (71.04) | 0.905 *** (51.17) | 0.818 *** (46.47) | 0.693 *** (36.42) | 0.891 *** (46.24) | 1.021 *** (54.69) | 1.25 *** (67.8) | 1.09 *** (48.35) | ||||||||||

| Adj. R * | 0.205 | 0.213 | 0.159 | 0.089 | 0.06 | 0.051 | 0.065 | 0.105 | 0.201 | 0.19 | ||||||||||

| F-Value | 884.44 (Pr. < 0.0001) | 928.41 (Pr. < 0.0001) | 656.66 (Pr. < 0.0001) | 337.87 (Pr. < 0.0001) | 213.85 (Pr. < 0.0001) | 167.2 (Pr. < 0.0001) | 205.13 (Pr. < 0.0001) | 334.67 (Pr. < 0.0001) | 673.35 (Pr. < 0.0001) | 532.9 (Pr. < 0.0001) | ||||||||||

| N | 17,092 | 17,132 | 17,389 | 17,219 | 16,547 | 15,440 | 14,703 | 14,289 | 13,342 | 11,378 | ||||||||||

| Dependent Variable: Price Discrepancies (Common Stock Price Subtract Preferred Stock Price) | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Variable/Year | 2000 | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 |

| ΔSentiment | 0.751 *** (3.76) | 0.737 *** (5.87) | 0.739 *** (3.03) | −0.363 (−1.6) | −1.014 * (−1.87) | −1.88 *** (−3.46) | 2.632 *** (5.2) | 1.807 (1.57) | −0.034 (−0.04) | −1.368 ** (−2.42) | 2.707 *** (4.24) |

| ΔVolume | 0.76 *** (7.31) | 0.485 *** (7.54) | −2.473 *** (−6.36) | −0.475 (−1.44) | −2.902 *** (−2.92) | 0.875 (1.44) | −1.404 (−1.56) | 4.715 *** (6.18) | 5.553 *** (7.39) | 2.14 *** (7.1) | −1.241 (−1.39) |

| ΔOutstanding | −10.8 * (−1.94) | −28.677 *** (−8.34) | −79.946 *** (−9.12) | −124.348 *** (−17.11) | −269.878 *** (−16.21) | −378.678 *** (−19.7) | −342.682 *** (−20.98) | −831.246 *** (−23.46) | −565.096 *** (−26.26) | −330.449 *** (−22.42) | −119.614 *** (−9.71) |

| Size | 4.269 *** (23.47) | 3.741 *** (28.12) | 5.334 *** (21.07) | 6.518 *** (28.56) | 11.968 *** (21.72) | 12.503 *** (22.19) | 11.838 *** (24.89) | 25.319 *** (22.85) | 19.301 *** (25.99) | 12.97 *** (24.97) | 15.322 *** (27.41) |

| Lev | −0.282 (−0.24) | −9.804 *** (−9.6) | −1.351 (−0.87) | −21.036 *** (−13.38) | −13.276 *** (−3.3) | −4.634 (−1.11) | −6.038 * (−1.68) | 12.383 (1.53) | −14.201** (−2.44) | −1.664 (−0.45) | −46.035 *** (−11.24) |

| Intercept | −76.43 *** (−21.3) | −62.595 *** (−25.38) | −92.425 *** (−19.31) | −107.701 *** (−24.81) | −211.78 *** (−19.79) | −222.76 *** (−20.53) | −206.072 *** (−22.32) | −459.723 *** (−21.07) | −334.972 *** (−22.83) | −224.486 *** (−21.66) | −253.378 *** (−21.66) |

| Adj. R2 | 0.058 | 0.065 | 0.045 | 0.057 | 0.036 | 0.04 | 0.049 | 0.042 | 0.056 | 0.045 | 0.045 |

| F-Value | 178.28 (Pr. < 0.0001) | 190.06 (Pr. < 0.0001) | 126.66 (Pr. < 0.0001) | 166.55 (Pr. < 0.0001) | 105.6 (Pr. < 0.0001) | 132.6 (Pr. < 0.0001) | 163.67 (Pr. < 0.0001) | 150.38 (Pr. < 0.0001) | 196.69 (Pr. < 0.0001) | 173.29 (Pr. < 0.0001) | 169.44 (Pr. < 0.0001) |

| N | 14,311 | 13,676 | 13,214 | 13,632 | 14,048 | 15,911 | 15,662 | 17,020 | 16,518 | 18,311 | 17,702 |

| Variable/Year | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | Full Sample |

| ΔSentiment | −2.695 *** (−4.55) | 2.597 *** (5.09) | 0.29 (0.64) | −0.885 ** (−2.55) | 2.483 *** (5.14) | 2.574 *** (4.68) | −0.002 ** (−2.41) | −1.407 ** (−2.45) | −0.006 (−0.01) | 3.52 *** (4.53) | 1.074 ***(7.75) |

| ΔVolume | 1.384 *** (6.07) | 1.13 ** (2.55) | 0.373 (0.36) | 3.997 *** (6.28) | 4.874 *** (6.6) | 5.796 *** (3.35) | −0.023 *** (−15.69) | −1.745 * (−1.85) | −1.719 (−1.49) | −1.352 ** (−2.04) | −0.292 *** (−2.9) |

| ΔOutstanding | −141.469 *** (−13.33) | −167.756 *** (−18) | −274.092 *** (−23.43) | −309.801 *** (−29.99) | −417.397 *** (−33.27) | −457.407 *** (−31.29) | 0.729 *** (27.02) | −29.857 *** (−13.31) | −32.409 *** (−13.39) | −39.575 *** (−13.68) | −35.224 *** (−45.72) |

| Size | 17.898 *** (36.46) | 17.182 *** (40.41) | 16.703 *** (36.88) | 12.548 *** (35.67) | 15.295 *** (34.69) | 16.437 *** (33.07) | −0.015 *** (−19.06) | 16.216 *** (33.2) | 18.525 *** (37.09) | 26.155 *** (35.98) | 11.763 *** (113.5) |

| Lev | −92.056 *** (−25.69) | −112.523 *** (−35.2) | −106.019 *** (−33.93) | −90.234 *** (−38.94) | −112.052 *** (−38.73) | −127.662 *** (−39.43) | −0.027 *** (−4.56) | −186.776 *** (−50.92) | −186.429 *** (−50.22) | −235.973 *** (−44.89) | −81.833 *** (−98.07) |

| Intercept | −276.218 *** (−26.59) | −252.382 *** (−28.09) | −244.644 *** (−25.73) | −174.504 *** (−23.75) | −210.006 *** (−22.94) | −226.456 *** (−22.19) | 0.897 *** (58.86) | −208.243 *** (−20.61) | −265.574 *** (−25.85) | −407.835 *** (−27.02) | −168.056 *** (−79.18) |

| Adj. R * | 0.098 | 0.139 | 0.124 | 0.144 | 0.151 | 0.154 | 0.056 | 0.165 | 0.172 | 0.169 | 0.051 |

| F-Value | 372.49 (Pr. < 0.0001) | 551.98 (Pr. < 0.0001) | 493.84 (Pr. < 0.0001) | 580.77 (Pr. < 0.0001) | 588.33 (Pr. < 0.0001) | 563.18 (Pr. < 0.0001) | 185.89 (Pr. < 0.0001) | 564.47 (Pr. < 0.0001) | 554.51 (Pr. < 0.0001) | 462.27 (Pr. < 0.0001) | 3458.45 (Pr. < 0.0001) |

| N | 17,092 | 17,132 | 17,389 | 17,219 | 16,547 | 15,440 | 15,662 | 14,289 | 13,342 | 11,378 | 324,536 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yang, H.; Ryu, D. Investor Sentiment and Price Discrepancies between Common and Preferred Stocks in Korea. Sustainability 2021, 13, 5539. https://doi.org/10.3390/su13105539

Yang H, Ryu D. Investor Sentiment and Price Discrepancies between Common and Preferred Stocks in Korea. Sustainability. 2021; 13(10):5539. https://doi.org/10.3390/su13105539

Chicago/Turabian StyleYang, Heejin, and Doowon Ryu. 2021. "Investor Sentiment and Price Discrepancies between Common and Preferred Stocks in Korea" Sustainability 13, no. 10: 5539. https://doi.org/10.3390/su13105539

APA StyleYang, H., & Ryu, D. (2021). Investor Sentiment and Price Discrepancies between Common and Preferred Stocks in Korea. Sustainability, 13(10), 5539. https://doi.org/10.3390/su13105539