Factors Influencing Corporate Social Responsibility Disclosure and Its Impact on Financial Performance: The Case of Vietnam

Abstract

:1. Introduction

2. Theoretical Background

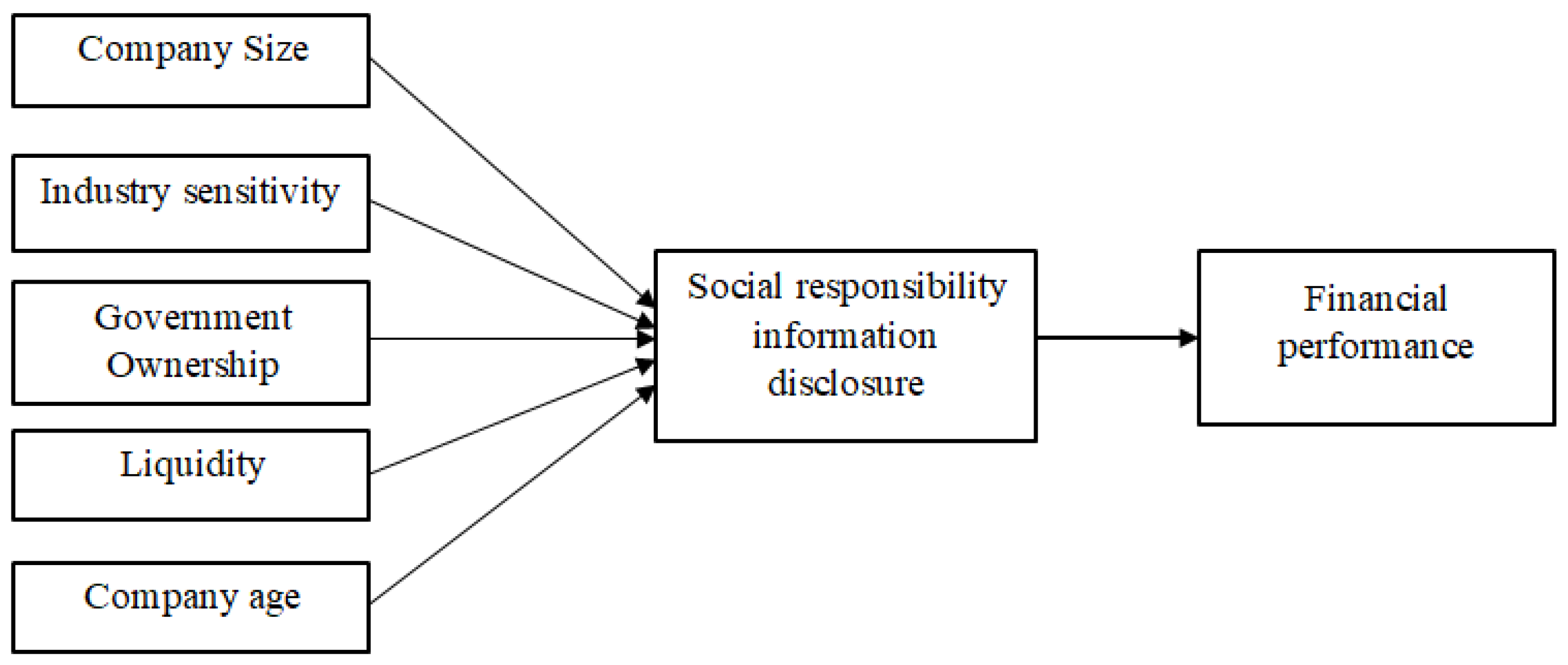

3. Development of Research Hypotheses

3.1. Company Size

3.2. Industry Sensitivity

3.3. Government Ownership

3.4. Liquidity

3.5. Company Age

3.6. Financial Performance

4. Data and Methodology

4.1. Sample

4.2. Measurement

4.2.1. Company Size

4.2.2. Industry Sensitivity

4.2.3. Government Ownership

4.2.4. Liquidity

4.2.5. Company Age

4.2.6. Financial Performance

4.2.7. Corporate Social Responsibilities Disclosure

- CSRDIi: CSR disclosure index of company i;

- CSRi: total disclosure score of company i;

- M: maximum score of items (15).

4.3. Empirical Models

- CSRD: level of corporate social responsibilities disclosure;

- SIZE: company size;

- INDS: industry sensitivity;

- GOV: government ownership;

- LIQ: liquidity;

- AGE: company age;

- ROA: average return on assets;

- ROE: average return on equity.

5. Results and Discussion

5.1. Descriptive Analysis

5.2. Analysis of the Main Results

6. Conclusions and Recommendations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Hackston, D.; Milne, M.J. Some determinants of social and environmental disclosures in New Zealand companies. Account. Audit. Account. J. 1996, 9, 77–108. [Google Scholar] [CrossRef]

- Godfrey, P.C.; Hatch, N.W. Researching Corporate Social Responsibility: An Agenda for the 21st Century. J. Bus. Ethics 2007, 70, 87–98. [Google Scholar] [CrossRef]

- Reverte, C. Determinants of Corporate Social Responsibility Disclosure Ratings by Spanish Listed Firms. J. Bus. Ethics 2009, 88, 351–366. [Google Scholar] [CrossRef]

- Branco, M.C.; Rodrigues, L.L. Factors Influencing Social Responsibility Disclosure by Portuguese Companies. J. Bus. Ethics 2008, 83, 685–701. [Google Scholar] [CrossRef]

- Gray, R.R.; Lavers, K. Corporate Social and Environmental Reporting: A Review of the Literature and a Longitudinal Study of UK Disclosure. Account. Audit. Account. J. 1995, 8, 47–77. [Google Scholar] [CrossRef]

- Belal, A.R.; Owen, D.L. The views of corporate managers on the current state of, and future prospects for, social reporting in Bangladesh. Account. Audit. Account. J. 2007, 20, 472–494. [Google Scholar] [CrossRef] [Green Version]

- Islam, M.A.; Deegan, C. Motivations for an organisation within a developing country to report social responsibility in-formation. Account. Audit. Account. J. 2008, 21, 850–874. [Google Scholar] [CrossRef] [Green Version]

- Guthrie, J.; Parker, L.D. Corporate Social Reporting: A Rebuttal of Legitimacy Theory. Account. Bus. Res. 1989, 19, 343–352. [Google Scholar] [CrossRef]

- Adams, C. Internal organisational factors influencing corporate social and ethical reporting. Account. Audit. Account. J. 2002, 15, 223–250. [Google Scholar] [CrossRef]

- Cowen, L.B.; Scott, S. The impact of corporate characteristics on social responsibility disclosure: A typology and frequency-based analysis. Account. Organ. Soc. 1987, 12, 111–122. [Google Scholar] [CrossRef]

- Barnett, M.L. Stakeholder influence capacity and the variability of financial returns to corporate social responsibility. Acad. Manag. Rev. 2007, 32, 794–816. [Google Scholar] [CrossRef]

- Roberts, R.W. Determinants of corporate social responsibility disclosure: An application of stakeholder theory. Account. Organ. Soc. 1992, 17, 595–612. [Google Scholar] [CrossRef] [Green Version]

- Tilt, C. The influence of external pressure groups on corporate social disclosure: Some empirical evidence. Account. Audit. Account. J. 1994, 7, 47–72. [Google Scholar] [CrossRef]

- Moneva, J.M.; Llena, F. Environmental disclosures in the annual reports of large companies in Spain. Eur. Account. Rev. 2000, 9, 7–29. [Google Scholar] [CrossRef]

- Deegan, C.; Blomquist, C. Stakeholder influence on corporate reporting: An exploration of the interaction between WWF-Australia and the Australian minerals industry. Account. Organ. Soc. 2006, 31, 343–372. [Google Scholar] [CrossRef]

- Patten, D.M. Intra-industry environmental disclosures in response to the Alaskan oil spill: A note on legitimacy theory. Account. Organ. Soc. 1992, 17, 471–475. [Google Scholar] [CrossRef]

- Brown, N.; Deegan, C. The public disclosure of environmental performance information—A dual test of media agenda setting theory and legitimacy theory. Account. Bus. Res. 1998, 29, 21–41. [Google Scholar] [CrossRef]

- Wilmshurst, T.D.; Frost, G.R. Corporate environmental reporting. Account. Audit. Account. J. 2000, 13, 10–26. [Google Scholar] [CrossRef]

- Deegan, C. The legitimising effect of social and environmental disclosures. A theoretical foundation. Account. Audit. Account. J. 2002, 15, 282–311. [Google Scholar] [CrossRef]

- O’Donovan, G. Environmental disclosures in the annual report. Extending the applicability and predictive power of legitimacy theory. Account. Audit. Account. J. 2002, 15, 344–371. [Google Scholar] [CrossRef]

- Mobus, J.L. Mandatory environmental disclosures in a legitimacy theory context. Account. Audit. Account. J. 2005, 18, 492–517. [Google Scholar] [CrossRef]

- Aerts, W.; Cormier, D. Media legitimacy and corporate environmental communication. Account. Organ. Soc. 2009, 34, 1–27. [Google Scholar] [CrossRef]

- Monteiro, M.S.; Aibar-Guzmán, B. Determinants of Environmental Disclosure in the Annual Reports of Large Companies Operating in Portugal. Corp. Soc. Responsib. Environ. Manag. 2010, 17, 185–204. [Google Scholar] [CrossRef]

- Moore, G. Corporate Social and Financial Performance: An Investigation in the U.K. Supermarket Industry. J. Bus. Ethics 2001, 34, 299–315. [Google Scholar] [CrossRef]

- Delaney, J.T.; Huselid, M.A. The impact of human resource management practices on perceptions of organizational performance. Acad. Manag. J. 1996, 39, 949–969. [Google Scholar]

- Cho, C.H.; Patten, D.M. The role of environmental disclosures as tools of legitimacy: A research note. Account. Organ. Soc. 2007, 32, 639–647. [Google Scholar] [CrossRef]

- de Villiers, C.; van Staden, C. Can less environmental disclosure have a legitimising effect? Evidence from Africa. Account. Organ. Soc. 2006, 31, 763–781. [Google Scholar] [CrossRef]

- Preston, L.E.; O’Bannon, D.P. The corporate social financial performance relationship: A typology and analysis. Bus. Soc. 1997, 36, 419–429. [Google Scholar] [CrossRef]

- Moore, G.; Robson, A. The UK supermarket industry: An analysis of corporate social and financial performance. Bus. Ethics A Eur. Rev. 2002, 11, 25–39. [Google Scholar] [CrossRef]

- Simpson, W.G.; Kohers, T. The Link Between Corporate Social and Financial Performance: Evidence from the Banking Industry. J. Bus. Ethics 2002, 35, 97–109. [Google Scholar] [CrossRef]

- Malik, M.S.; Kanwal, L. Impact of Corporate Social Responsibility Disclosure on Financial Performance: Case Study of Listed Pharmaceutical Firms of Pakistan. J. Bus. Ethics 2016, 150, 69–78. [Google Scholar] [CrossRef]

- Patten, D.M. Exposure, Legitimacy, and Social Disclosure. J. Account. Public Policy 1991, 10, 297–308. [Google Scholar] [CrossRef]

- Andrikopoulos, A.; Kriklani, N. Environmental Disclosure and Financial Characteristics of the Firm: The Case of Denmark. Corp. Soc. Responsib. Environ. Manag. 2012, 20, 55–64. [Google Scholar] [CrossRef]

- Adams, C.A.; Hill, W.-Y.; Roberts, C.B. Corporate social reporting practices in western europe: Legitimating corporate behaviour? Br. Account. Rev. 1998, 30, 1–21. [Google Scholar] [CrossRef]

- Kansal, M.; Joshi, M.; Batra, G.S. Determinants of corporate social responsibility disclosures: Evidence from India. Adv. Account. 2014, 30, 217–229. [Google Scholar] [CrossRef]

- Neu, D.; Warsame, H.; Pedwell, K. Managing Public Impressions: Environmental Disclosures in Annual Reports. Account. Organ. Soc. 1998, 23, 265–282. [Google Scholar] [CrossRef]

- Suwaidan, M.S.; Al-Omari, A.; Haddad, R.H. Social responsibility disclosure and corporate characteristics: The case of Jordanian industrial companies. Int. J. Account. Audit. Perform. Eval. 2004, 1, 432. [Google Scholar] [CrossRef]

- Tagesson, T.; Blank, V.; Broberg, P.; Collin, S.O. What explains the extent and content of social and environmental disclosures on corporate websites: A study of social and environmental reporting in Swedish listed corporations. Corp. Soc. Responsib. Environ. Manag. 2009, 16, 352–364. [Google Scholar] [CrossRef]

- Brammer, S.; Pavelin, S. Building a Good Reputation. Eur. Manag. J. 2004, 22, 704–713. [Google Scholar] [CrossRef]

- Brammer, S.; Pavelin, S. Factors influencing the quality of corporate environmental disclosure. Bus. Strat. Environ. 2008, 17, 120–136. [Google Scholar] [CrossRef]

- Clarke, J.; Gibson, S.M. The Use of Corporate Social Disclosures in the Management of Reputation and Legitimacy: A Cross Sectoral Analysis of UK Top 100 Companies. Bus. Ethics 1999, 8, 5–13. [Google Scholar] [CrossRef]

- Line, M.; Hawley, H.; Krut, R. Development in Global Environmental and Social Reporting. Corp. Environ. Strategy 2002, 9, 69–78. [Google Scholar] [CrossRef]

- Newson, M.; Deegan, C. Global expectations and their association with corporate social disclosure practices in Australia, Singapore, and South Korea. Int. J. Account. 2002, 37, 183–213. [Google Scholar] [CrossRef]

- Wanderley, L.S.O.; Lucian, R.; Farache, F.; Filho, J.M.D.S. CSR Information Disclosure on the Web: A Context-Based Approach Analysing the Influence of Country of Origin and Industry Sector. J. Bus. Ethics 2008, 82, 369–378. [Google Scholar] [CrossRef]

- Amran, A.; Devi, S.S. The impact of government and foreign affiliate influence on corporate social reporting: The case of Malaysia. Manag. Audit. J. 2008, 23, 386–404. [Google Scholar] [CrossRef]

- Cormier, D.; Gordon, I.M. An examination of social and environmental reporting strategies. Account. Audit. Account. J. 2001, 14, 587–617. [Google Scholar] [CrossRef]

- Secchi, D. The Italian experience in social reporting: An empirical analysis. Corp. Soc. Responsib. Environ. Manag. 2006, 13, 135–149. [Google Scholar] [CrossRef]

- Abd-El Salam, H.O.; Weetman, P. Introducing international accounting standards to an emerging capital market: Relative familiarity and language effect in Egypt. J. Int. Account. Audit. 2003, 12, 63–84. [Google Scholar] [CrossRef]

- Ezat, A.; Em-Masry, A. The impact of corporate governance on the timeliness of corporate internet reporting by Egyptian listed companies. Manag. Finance 2008, 34, 848–867. [Google Scholar] [CrossRef] [Green Version]

- Samaha, K.; Dahawy, K. Factors influencing voluntary corporate disclosure by the actively traded Egyptian firms. Res. Account. Emerg. Econ. 2010, 10, 87–119. [Google Scholar]

- Waddock, S.A.; Graves, S.B. The corporate social performance-financial performance link. Strateg. Manag. J. 1997, 18, 303–319. [Google Scholar] [CrossRef]

- Hamid, F.Z.A. Corporate social disclosure by banks and finance companies: Malaysian evidence. Corp. Ownersh. Control. 2004, 1, 118–130. [Google Scholar] [CrossRef]

- Akhtaruddin, M. Corporate mandatory disclosure practices in Bangladesh. Int. J. Account. 2005, 40, 399–422. [Google Scholar] [CrossRef]

- Liu, X.; Anbumozhi, V. Determinant factors of corporate environmental information disclosure: An empirical study of Chinese listed companies. J. Clean. Prod. 2009, 17, 593–600. [Google Scholar] [CrossRef]

- Rettab, B.; Ben Brik, A.; Mellahi, K. A Study of Management Perceptions of the Impact of Corporate Social Responsibility on Organisational Performance in Emerging Economies: The Case of Dubai. J. Bus. Ethics 2008, 89, 371–390. [Google Scholar] [CrossRef]

- Uwuigbe, U.; Egbide, B.C. Corporate social responsibility disclosures in Nigeria: A study of listed financial and nonfinancial firms. J. Manag. Sustain. 2012, 2, 160–169. [Google Scholar] [CrossRef] [Green Version]

- Ratmono, D.; Nugrahini, D.E.; Cahyonowati, N. The Effect of Corporate Governance on Corporate Social Responsibility Disclosure and Performance. J. Asia. Financ. Bus. 2021, 8, 933–941. [Google Scholar]

- Saleh, M.; Zulkifli, N.; Muhamad, R. An Empirical Examination of the Relationship between Corporate Social Responsibility Disclosure and Financial Performance in an Emerging Market. Asia Pac. J. Bus. Adm. 2008, 3, 1–22. [Google Scholar]

- Andrian, T. Linking Corporate Carbon Emission, Social Responsibility Disclosures and Firm Financial Performance. Test. Eng. Manag. 2020, 83, 22356–22366. [Google Scholar]

- Hussainey, K.; Elsayed, M.; Razik, M.A. Factors affecting corporate social responsibility disclosure in Egypt. Corp. Ownersh. Control. 2011, 8, 432–443. [Google Scholar] [CrossRef]

- National Assembly of Vietnam. Law on Enterprises in Vietnam, No. 59/2020/QH14; Government Office: Hanoi, Vietnam, 2020.

- The Ministry of Finance. Guidelines for Information Disclosure on Securities Market, Circular 155/2015/TT-BTC; Government Office: Hanoi, Vietnam, 2015.

- Chakroun, R.; Matoussi, H.; Mbirki, S. Determinants of CSR disclosure of Tunisian listed banks: A multi-support analysis. Soc. Responsib. J. 2017, 13, 552–584. [Google Scholar] [CrossRef]

- Vu, Q.N. Technical Efficiency of Industrial State-Owned Enterprises in Vietnam. Asian Econ. J. 2003, 17, 87–101. [Google Scholar] [CrossRef]

- Rahman, S. Evaluation of definitions: Ten dimensions of corporate social responsibility. World. Rev. Bus. Res. 2011, 1, 166–176. [Google Scholar]

- McWilliams, A.; Siegel, D. Corporate social responsibility and financial performance: Correlation or misspecification? Strateg. Manag. J. 2000, 21, 603–609. [Google Scholar] [CrossRef]

- Makni, R.; Francoeur, C.; Bellavance, F. Causality Between Corporate Social Performance and Financial Performance: Evidence from Canadian Firms. J. Bus. Ethics 2008, 89, 409–422. [Google Scholar] [CrossRef]

- Saleh, M.; Zulkifli, N.; Muhamad, R. Looking for evidence of the relationship between corporate social responsibility and corporate financial performance in an emerging market. Asia-Pac. J. Bus. Adm. 2011, 3, 165–190. [Google Scholar] [CrossRef] [Green Version]

- Rehman, Z.U.; Zahid, M.; Rehman, H.U.; Asif, M.; Alharthi, M.; Irfan, M.; Glowacz, A. Do Corporate Social Responsibility Disclosures Improve Financial Performance? A Perspective of the Islamic Banking Industry in Pakistan. Sustainability 2020, 12, 3302. [Google Scholar] [CrossRef] [Green Version]

- Buallay, A.; Kukreja, G.; Aldhaen, E.; Al Mubarak, M.; Hamdan, A.M. Corporate social responsibility disclosure and firms’ performance in Mediterranean countries: A stakeholders’ perspective. EuroMed J. Bus. 2020, 15, 361–375. [Google Scholar] [CrossRef]

{kind=link}

| No | Sector | Number of Companies | Percentage |

|---|---|---|---|

| 1 | Information Technology | 2 | 2.0 |

| 2 | Industrials | 22 | 22.0 |

| 3 | Materials | 9 | 9.0 |

| 4 | Financial | 17 | 17.0 |

| 5 | Utilities | 7 | 7.0 |

| 6 | Energy | 2 | 2.0 |

| 7 | Communication Services | 1 | 1.0 |

| 8 | Consumer Discretionary | 8 | 8.0 |

| 9 | Health Care | 3 | 3.0 |

| 10 | Food, Beverage and Tobacco | 11 | 11 |

| 11 | Real Estate | 18 | 18 |

| Total | 100 | 100 |

| Aspects | Item Examples |

|---|---|

| Environment: Management of raw materials | EN1: The total amount of materials used in the production and packaging of the company’s main products and services during the year |

| EN2: The percentage of materials recycled to manufacture products and services of the company | |

| Environment: Energy consumption | EN3: Energy consumption—directly and indirectly |

| EN4: Energy saved through innovative energy efficiency | |

| EN5: Energy efficiency Initiative Reports and report on the results of these initiatives | |

| Environment: Water consumption | EN6: Water supply and amount of water used |

| EN7: Percentage and total volume of recycled and reused water | |

| Environment: Compliance with the law on environmental protection | EN8: Number of times fined for not complying with laws and regulations on the environment |

| EN9: The total amount fined for not complying with laws and regulations on the environment | |

| Employees: Policies related to employees | EM1: Number of workers |

| EM2: Average wages of employees | |

| EM3: Labor policies to ensure health, safety and welfare of employees | |

| EM4: The average number of training hours per year | |

| EM5: The skills development program and continuous learning to support workers to ensure employment and career development | |

| Society: Responsibility for local community | SO1: Community investment and other community development activities, including financial support to serve the community |

| Item | Percentage (%) | Average Percentage (%) |

|---|---|---|

| EN1 | 28 | Environment: 31.7 |

| EN2 | 22 | |

| EN3 | 36 | |

| EN4 | 32 | |

| EN5 | 24 | |

| EN6 | 35 | |

| EN7 | 21 | |

| EN8 | 45 | |

| EN9 | 42 | |

| EM1 | 82 | Employees: 65 |

| EM2 | 55 | |

| EM3 | 74 | |

| EM4 | 49 | |

| EM5 | 65 | |

| SO1 | 87 | Society: 87 |

| SIZE | INDS | GOV | LIQ | AGE | |

|---|---|---|---|---|---|

| SIZE | 1 | 0.258 ** | 0.401 ** | 0.377 ** | 0.272 ** |

| INDS | 1 | 0.266 ** | 0.117 ** | 0.067 ** | |

| GOV | 1 | 0.273 ** | 0.308 ** | ||

| LIQ | 1 | 0.214 ** | |||

| AGE | 1 |

| Variable | Coefficient | Std. Error | t-Statistic | Prob. | VIF |

|---|---|---|---|---|---|

| C | −0.598515 | 0.216236 | −2.767880 | 0.0068 | |

| SIZE | 0.822513 | 0.217217 | 3.786590 | 0.0003 | 1.119416 |

| INDS | 0.549640 | 0.116457 | 4.719666 | 0.0000 | 1.112852 |

| GOV | 0.347067 | 0.117240 | 2.960313 | 0.0039 | 1.053056 |

| LIQ | 0.093069 | 0.041803 | 2.226393 | 0.0284 | 1.010602 |

| AGE | 0.064111 | 0.045107 | 1.421295 | 0.1585 | 1.028219 |

| R-squared | 0.449939 | ||||

| Adjusted R-squared | 0.420680 | ||||

| CSRD | ROA | ROE |

|---|---|---|

| Significance/p-value | 0.000 | 0.000 |

| Adjusted R-squared | 72.9% | 64.8% |

| Observation | 100 | 100 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nguyen, T.H.; Vu, Q.T.; Nguyen, D.M.; Le, H.L. Factors Influencing Corporate Social Responsibility Disclosure and Its Impact on Financial Performance: The Case of Vietnam. Sustainability 2021, 13, 8197. https://doi.org/10.3390/su13158197

Nguyen TH, Vu QT, Nguyen DM, Le HL. Factors Influencing Corporate Social Responsibility Disclosure and Its Impact on Financial Performance: The Case of Vietnam. Sustainability. 2021; 13(15):8197. https://doi.org/10.3390/su13158197

Chicago/Turabian StyleNguyen, Thanh Hung, Quang Trong Vu, Duc Minh Nguyen, and Hoang Long Le. 2021. "Factors Influencing Corporate Social Responsibility Disclosure and Its Impact on Financial Performance: The Case of Vietnam" Sustainability 13, no. 15: 8197. https://doi.org/10.3390/su13158197

APA StyleNguyen, T. H., Vu, Q. T., Nguyen, D. M., & Le, H. L. (2021). Factors Influencing Corporate Social Responsibility Disclosure and Its Impact on Financial Performance: The Case of Vietnam. Sustainability, 13(15), 8197. https://doi.org/10.3390/su13158197