3.2. ESG Performance and Probability of Default

We perform ordinary least squares (OLS) regressions of the following specification to assess the effect of ESG rating scores on the probability of default (

):

where

i denotes the firm,

t denotes the year,

and

representing industry-fixed and year-fixed effects, respectively, and

stands for the error term. The additional

k independent or control variables are denoted by the

regressor vector

X with the

coefficient matrix

. By using the

(in %) instead of ordinally scaled credit ratings, we account for the non-equidistant scaling of credit ratings. We are specifically interested in the lagged independent variable

and the respective pillar scores

E,

S and

G. We then extend our analysis by controlling for the market-driven variables abnormal return, denoted as

and

, which is the firm’s annual idiosyncratic volatility defined as the standard deviation of daily abnormal returns. The daily abnormal returns are defined as the difference between observed daily log returns and expected returns, which in turn are estimated by using a simple market model. We use daily log returns of the S & P 500 index in the market model and retrieve annual abnormal returns from daily by summation.

Additionally, we implement various firm controls proposed by Shumway [

40] who developed a hazard model to forecast bankruptcy, as well as industry and time-fixed effects in our regression. For the sector classification, we use the Global Industry Classification Standard’s (GICS), which defines 11 sectors in total. We report cluster-adjusted standard errors at firm-level.

In

Table 2, we present the results of our baseline regressions. Our dependent variable is

and we employ the one-year lagged ESG score and its lagged single constituents as independent variables in univariate regressions (models (1) to (4)). We then add the contemporary market-driven controls

and

for each specification (models (5) to (8)). We find that in the univariate models, all independent variables are highly significant and all coefficients are negative. As we include market controls, the coefficients for

and its respective pillar scores remain highly significant, even when maintaining controls for industry and time-fixed effects and clustering of standard errors on the firm-level. The coefficients for

and the constituents are negative and have nearly half the magnitude compared to the univariate models. As for

and abnormal returns

, the coefficients are positive and are also highly significant across all specifications. For the aggregate ESG score in the multivariate case, we conclude that an increase in

by one unit decreases the probability of default by

on average and while holding everything else constant. This first set of results indicates that environmental, social and governance performance as well as the aggregate ESG score significantly affects the probability of corporate credit default.

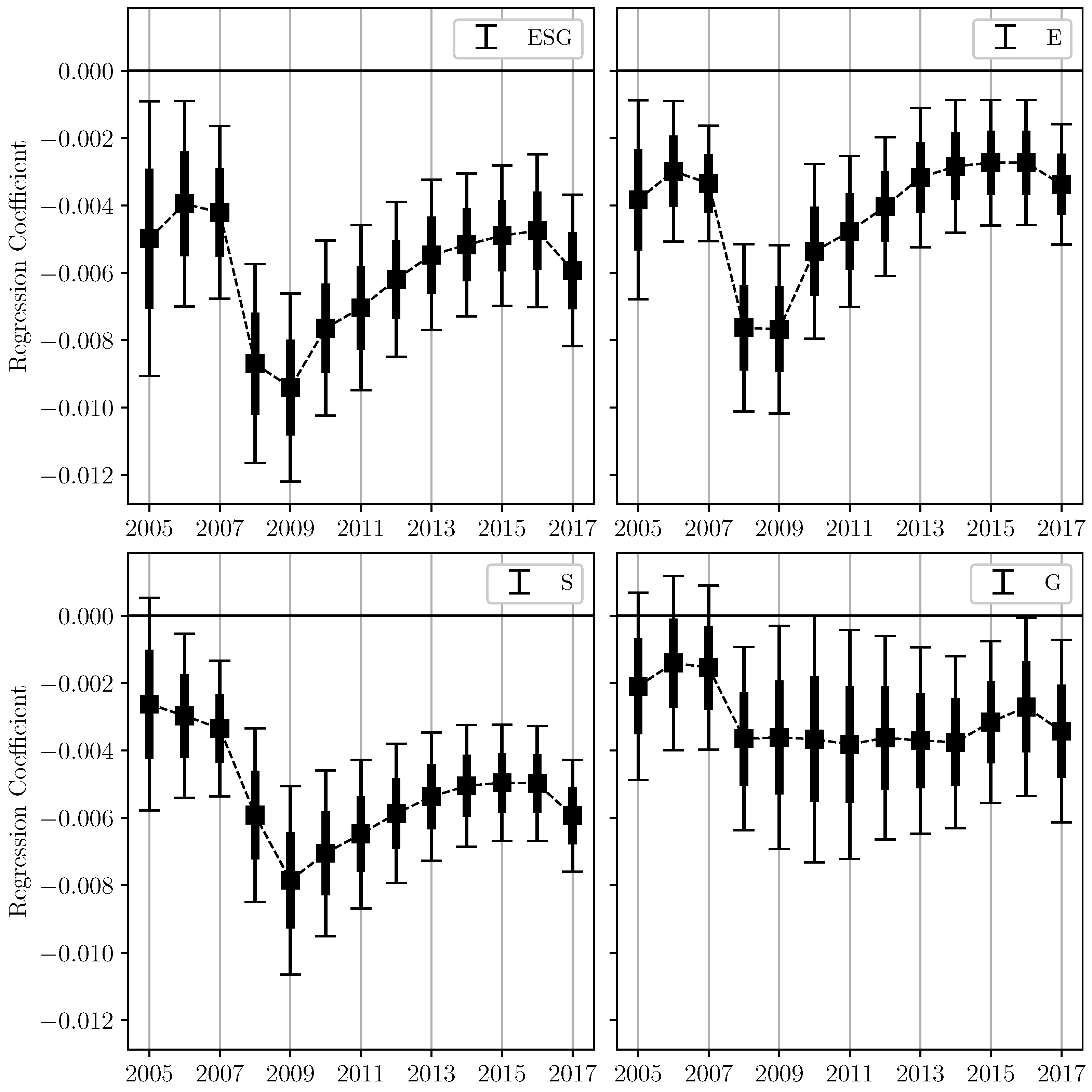

In order to further understand the effect of

on

over time, we plot the estimated coefficients for

and its constituents in the specification from

Table 2 (models (5) to (8)) from 2005 to 2017 in

Figure 1. By using an expanding time window starting in 2002 for the estimation, we observe that the ESG score and each respective pillar score negatively affect the probability of corporate credit default in every subsample that is created by adding observations from the subsequent year.

We observe a sharp decline of the coefficients’ magnitude from 2007 to 2008, which indicates an increased effect of

on

. By taking into account the subprime mortgage crisis during the respective period, a stronger impact of ESG performance on the probability of default during this financial shock can be observed. The relevance of ESG criteria is perceived by credit rating agencies, for example, the rating agency Fitch’s addresses the importance and integration of the so-called ESG relevance scores, which are embedded in the credit rating process [

41]. From this, it may be deduced that the rating agency readjusted its credit risk model with regard to ESG performance.

The magnitude of the

coefficient increases post-crisis to a slightly lower value than pre-crisis, indicating that the rating agencies may have decreased the importance of

in their evaluation of credit default risk. We observe that the coefficients for

are decreasing since 2016, which might indicate that ESG performance is regaining importance for the risk evaluation of credit rating agencies. The increased emphasis on ESG from 2016 onward is consistent with the literature, which links this trend to the Paris Climate Change Agreement and the UN Principles for Responsible Investment (PRI) initiative of 2016 on ESG in Credit Ratings (see, e.g., [

42,

43]). Companies that operate in high-emission industries or generally have poor environmental performance tend to a higher average bond yield spread post Paris Climate Change Agreement [

16].

Compared with the other pillars, the time evolution of the governance pillar score is very different; in particular, no minimum can be observed around the year 2009 and overall the influence is much smaller and shows little variation. A similar observation was made by Bebchuk et al. [

44], who could not document any correlation between governance indices and abnormal returns during the period of 2000–2008. In the original work on the governance index (or G-Index), which uses various guidelines to define a proxy for the level of shareholder rights, a strong correlation between shareholder rights and firm value was observed in the 1990s [

45]. The authors explain the subsequent disappearance of the effect with a learning effect on the part of the market participants, which allows them to distinguish between companies that score well and those that score poorly on the governance indices. Moreover, the structural break between the governance-return correlation corresponds to a simultaneous increase in media attention to corporate governance.

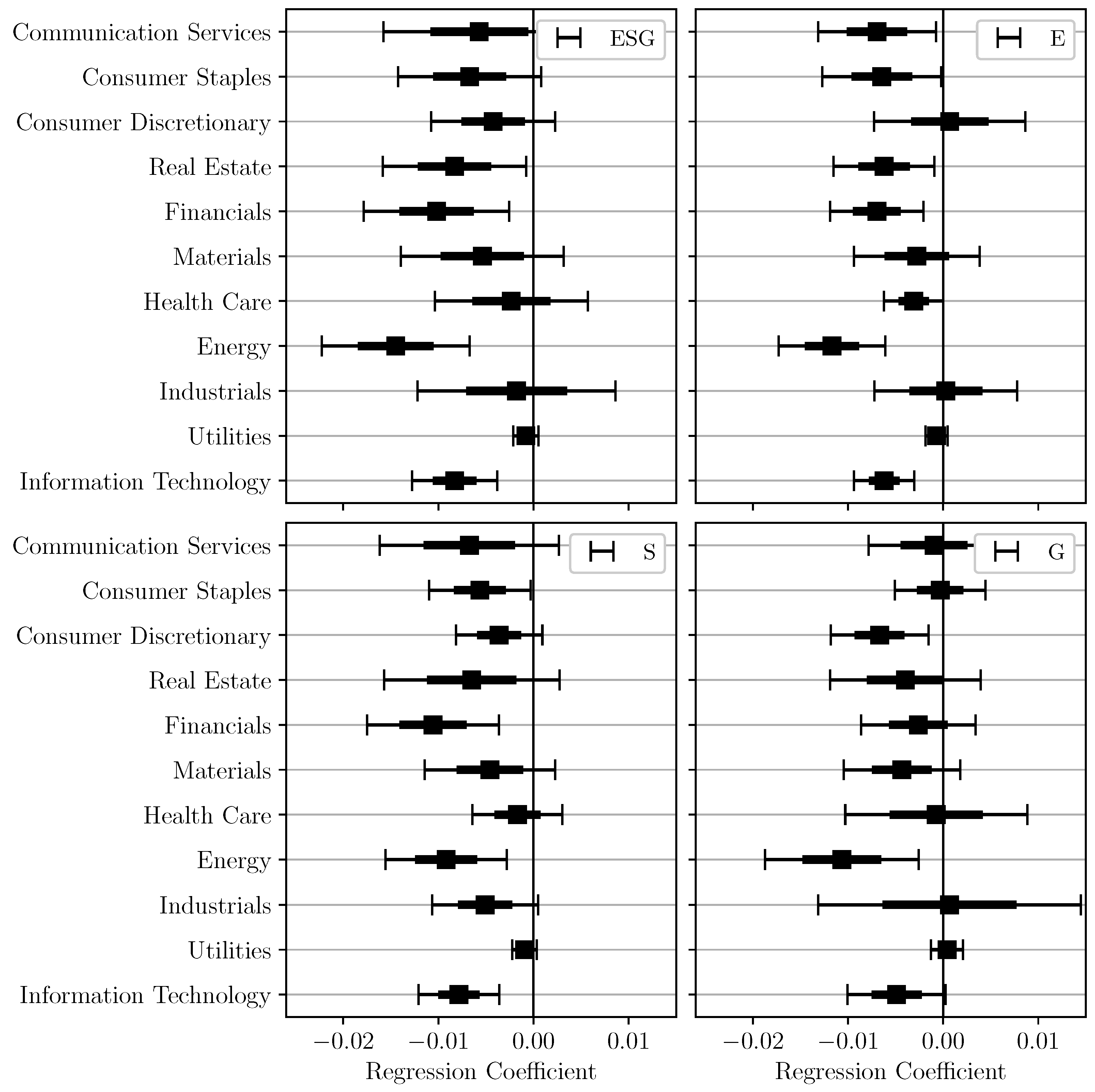

In

Figure 2, we partition our panel to observe the magnitude of the estimated coefficient from

Table 2 and specification (5) to (7) for different GICS sectors. Considering the aggregated

, all industries show a negative influence of

on

. The industries

Energy,

Financials and

Real Estate are most heavily influenced by

in their

. By further breaking down

into its constituents, we can state that the environmental performance has the highest influence on

in the

Energy,

Financials and

Communication Services sectors. This is in line with the ongoing debate on the need for an ecological disruption, which affects the

Energy sector in particular [

46]. In contrast, we observe that

Industrials and

Consumer Discretionary have a positive coefficient for the effect of the environmental pillar score on

, indicating that an increment in

E increases the probability of credit default.

We interpret the positive coefficient that investment in environmental performance may be costly in these sectors and, therefore, negatively affects the . For the social pillar score S, we observe the highest impact of on for Financials, Energy and Information Technology. The effect of governance performance on reducing is most influential in Energy, Consumer Discretionary and Information Technology. The Industrials and Utilities sectors show a positive coefficient, which indicates that increasing governance performance in these sectors is costly and increases the .

Overall, the results from our tests indicate that environmental, social and governance performance significantly affects the probability of credit default. Although the average magnitude of the effect is not very large, we observe that the size of the coefficients varies strongly over time. This finding indicates, that rating agencies may adjust the weighting of performance in their credit risk modeling. We thereby conclude that may contribute to reducing the cost of capital through the credit risk channel.

3.3. Robustness

We perform several robustness checks to ensure the validity of our results. First, we examine the linear dependence in our regression specification by using a scatterplot of standardized residuals against the independent variables, yielding an indication of linear dependence. We further observe a serial correlation in our dependent variable by testing, as proposed by Wooldridge [

47] (see, e.g.,

Table A4), but clustering the standard errors on a firm-level ensures robustness regarding inference [

48]. We confirm stationarity for our dependent variable by performing the Dickey–Fuller test in our panel as proposed by Choi [

49] (see, e.g.,

Table A5). Furthermore, a quantile–quantile plot of regression residuals on the inverse normal distribution shows that we have deviations from the normal distribution in the tails. In addition to the linear model estimated in this paper, we estimate a logistic regression with the probability of default as the dependent variable, which is similar to Orlando and Pelosi [

50]. Additionally, we estimate an ordered logit with the respective credit rating as the dependent variable in order to better account for possible nonlinearities and the boundedness of our dependent variable. In both models, we estimate univariate models with the ESG Score as our main independent variable. Moreover, we estimate multivariate models by adding idiosyncratic volatility and abnormal returns as market driven control variables. We observe significant parameters and qualitatively equal signs, which are consistent with the results of the linear model. For reasons of brevity, we do not report the respective tables here.

After introducing market control variables in

Table 2, we follow [

40] and add a set of firm controls which consist of Altman’s [

51] variables proposed in his Z-Score model. These include ratios of working capital to total assets (

), retained earnings to total assets (

), earnings before interest and taxes to total assets (

), market equity to total assets (

) and sales to total assets (

). According to the Z-score model, these five selected ratios are particularly well suited for describing or predicting corporate default. From the model estimates, the ratio of retained earnings to total assets (

) as a measure of cumulative profitability over the company life is shown to be particularly meaningful for describing the probability of default. Furthermore, the ratio describes the degree of leverage of the firm, since firms that finance their assets by retaining profits may require less debt capital. The ratio of EBIT to TA has a significant influence as a measure of the companies’ profitability [

52]. Due to the substantially higher leverage compared to other sectors as well as increased sensitivity to financial risks, we neglect financial service firms in the following models [

53]. The models were additionally calculated by including the companies from the financial sector and consistent results with significant effects were obtained. In addition, we add ratios of net income to total assets (

) (return on assets), total liabilities to total assets (

) to account for firm’s financial leverage and current assets to current liabilities (

) to control for liquidity as proposed by Zmijewski [

54].

Since we leave out interpreting the respective coefficients for the additional control variables, their use in

Table 3 and

Table 4 is labeled

Additional Controls for purposes of clarity. The results presented in

Table 3 are similar to those from our baseline and market model, which indicates the aggregate ESG score as well as environmental and social pillar scores to be significantly associated with the lower probability of credit default.

There exists a strong correlation between ESG scores (

) and firm size (

), which can be explained by better organizational legitimacy and resources available to a firm [

55,

56]. These dissimilarities are also discussed in the context of stakeholder theory and social capital by Russo et al. [

57], who argues that a distinction must be made between SMEs and large companies since different idiosyncrasies between large companies and SMEs must be taken into account. Therefore, we further determine whether firm size affects our model and, therefore, estimate models with an interaction term between ESG score and the respective pillar scores with the natural logarithm of total assets as a proxy for firm size. Since the further added firm controls are already calculated as ratios divided by either total assets or current liabilities, we do not adjust it further.

Table 4 displays our results for the regression with

as the dependent variable and interacted one-year lagged

scores. Despite the coefficients for

,

and

are significant and they are smaller in magnitude compared to the results from

Table 3. Although not reported for reasons of brevity, we additionally subdivide our data based upon the investment-grade boundary. Companies with a credit rating better than BB are defined as investment grade. Observations with a credit rating of BB or worse correspond to high yield or speculative grade. We calculate the extended regression specifications from

Table 4 with size interaction terms and find more significant results for firms that are marked as investment-grade (

). For the subsample corresponding to the speculative grade, no significant influence (

) of

on

can be observed (

). In addition, we use ESG scores with greater lags and obtain similar results, although the magnitude decreases proportionally with increasing lag (see

Table A2). Overall, our various robustness checks provide further support for the negative relationship between

and the probability of corporate credit default

.

{kind=link}

{kind=link}