COVID-19 Pandemic: Is the Crypto Market a Safe Haven? The Impact of the First Wave

, , , and

, , , and

Abstract

:1. Introduction

2. Theoretical Background

3. Data and Methodology

3.1. Data

3.2. Methodology

3.2.1. COVID-19 Global Index Construction

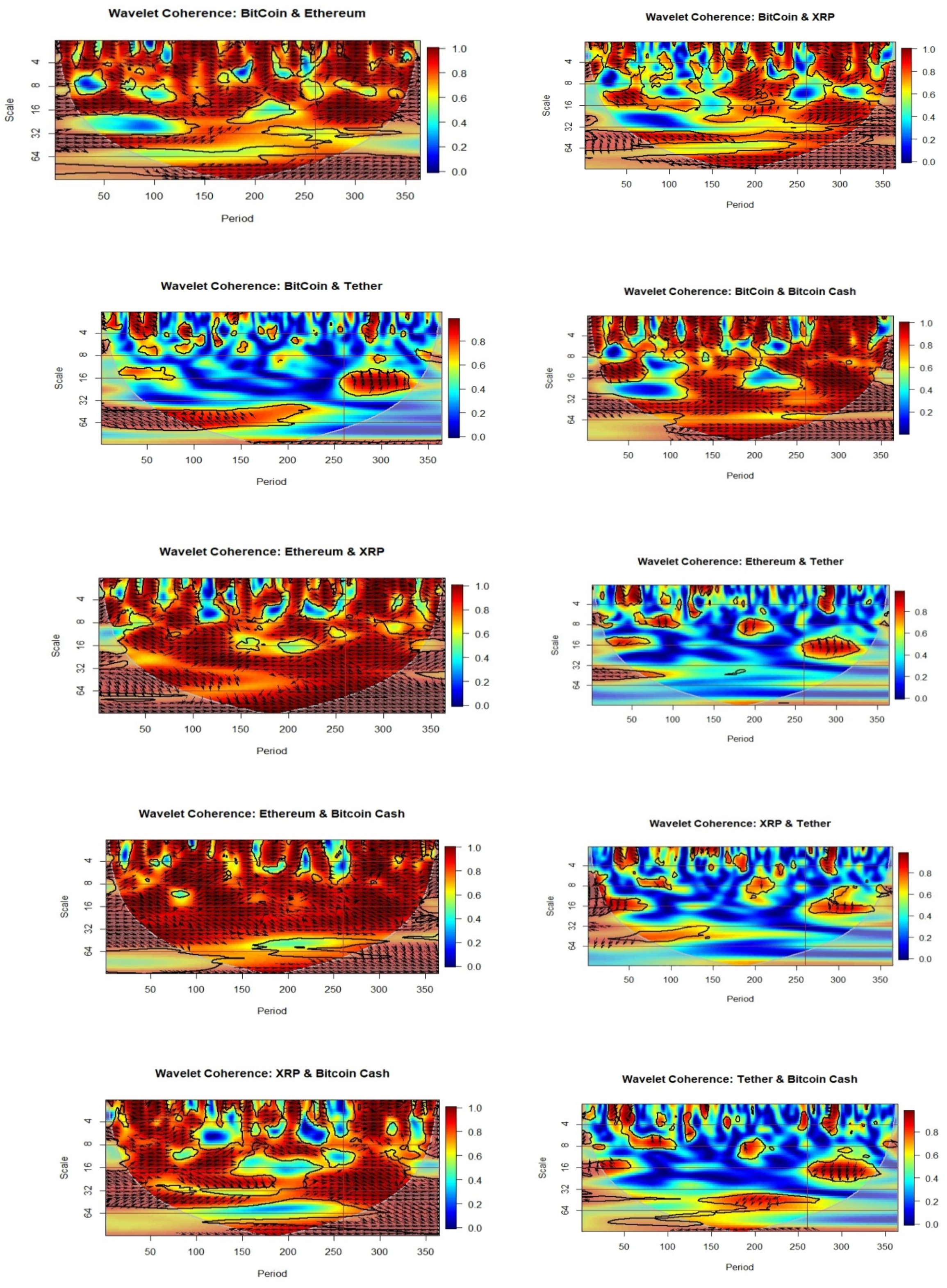

3.2.2. Wavelet Coherence

3.2.3. Regressions

OLS Regression

Quantile Regression

4. Results and Discussion

4.1. Preliminary Analysis

4.2. Wavelet Coherence

4.3. OLS Estimates

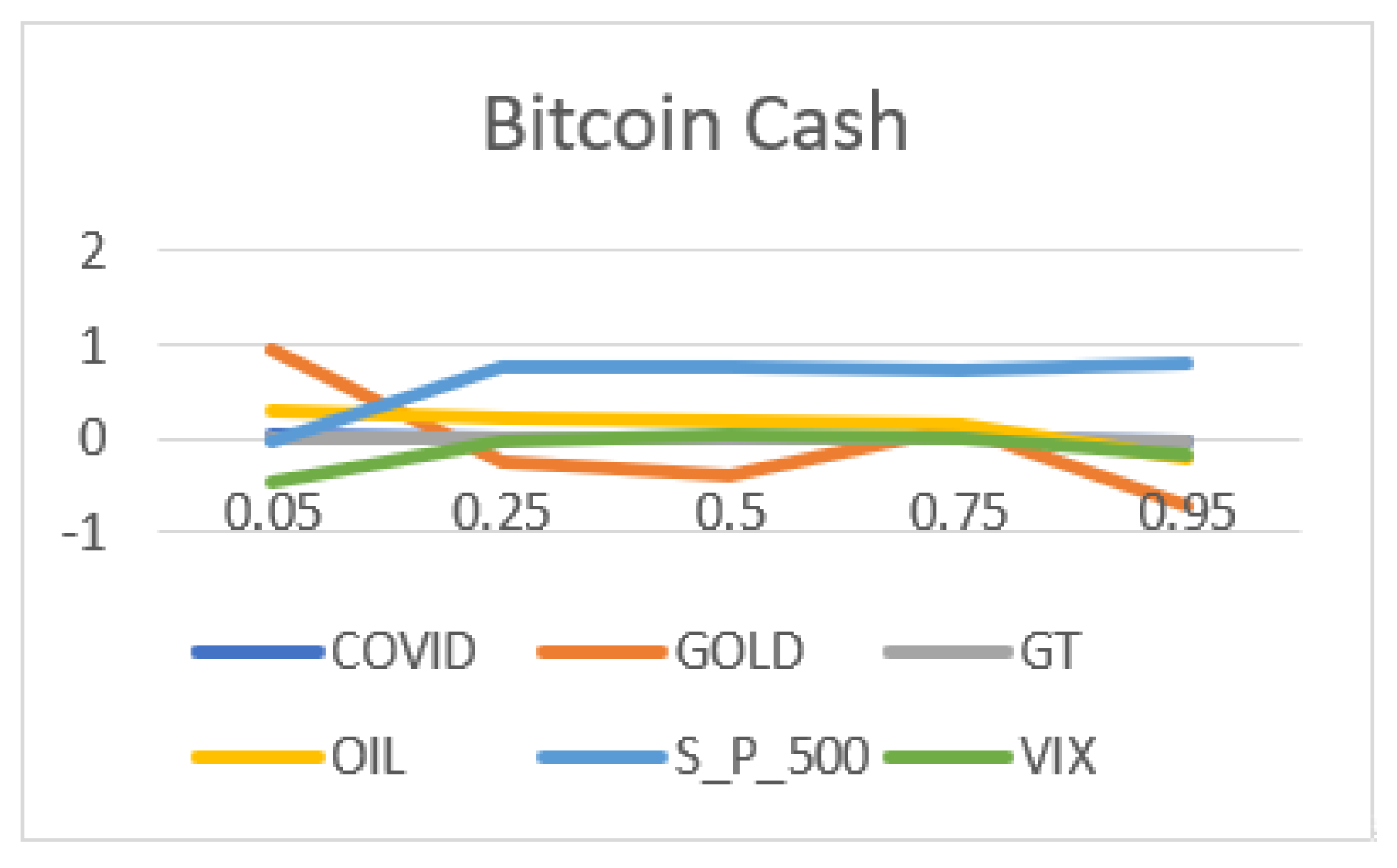

4.4. Quantile Regression Estimates

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Grobys, K. When Bitcoin has the flu: On Bitcoin’s performance to hedge equity risk in the early wake of the COVID-19 outbreak. Appl. Econ. Lett. 2021, 28, 860–865. [Google Scholar] [CrossRef]

- Taleb, N. The Black Swan: The Impact of the Highly Improbable; Random House Inc.: New York, NY, USA, 2007. [Google Scholar]

- Mnif, E.; Salhi, B.; Jarboui, A. Herding behaviour and Islamic market efficiency assessment: Case of Dow Jones and Sukuk market. Int. J. Islam. Middle East. Financ. Manag. 2019, 13, 24–41. [Google Scholar] [CrossRef]

- Vukovic, D.; Lapshina, K.A.; Maiti, M. European Monetary Union bond market dynamics: Pre & post crisis. Res. Int. Bus. Financ. 2019, 50, 369–380. [Google Scholar] [CrossRef]

- Vukovic, D.; Vyklyuk, Y.; Matsiuk, N.; Maiti, M.; Chernova, N. Neural network forecasting in prediction Sharpe ratio: Evidence from EU debt market. Phys. A Stat. Mech. Its Appl. 2020, 542, 123331. [Google Scholar] [CrossRef]

- Mnif, E.; Jarboui, A.; Mouakhar, K. How the cryptocurrency market has performed during COVID 19? A multifractal analysis. Financ. Res. Lett. 2020, 36, 101647. [Google Scholar] [CrossRef]

- Corbet, S.; Hou, G.; Yang, H.; Lucey, B.M.; Les, O. Aye Corona! The Contagion Effects of Being Named Corona during the COVID-19 Pandemic. 2020. Available online: https://ssrn.com/abstract=3561866 (accessed on 26 March 2020).

- Jana, R.K.; Das, D. Did Bitcoin act as an antidote to the Chinese equity market and booster to Altcoins during the Novel Coronavirus outbreak? SSRN 2020. [Google Scholar] [CrossRef]

- Shahzad, S.J.H.; Bouri, E.; Roubaud, D.; Kristoufek, L.; Lucey, B. Is Bitcoin a better safe-haven investment than gold and commodities? Int. Rev. Financ. Anal. 2019, 63, 322–330. [Google Scholar] [CrossRef]

- Klein, T.; Thu, H.P.; Walther, T. Bitcoin is not the New Gold–A comparison of volatility, correlation, and portfolio performance. Int. Rev. Financ. Anal. 2018, 59, 105–116. [Google Scholar] [CrossRef]

- Das, D.; Le Roux, C.; Jana, R.; Dutta, A. Does Bitcoin hedge crude oil implied volatility and structural shocks? A comparison with gold, commodity and the US Dollar. Financ. Res. Lett. 2020, 36, 101335. [Google Scholar] [CrossRef]

- Corbet, S.; Lucey, B.; Urquhart, A.; Yarovaya, L. Cryptocurrencies as a financial asset: A systematic analysis. Int. Rev. Financ. Anal. 2019, 62, 182–199. [Google Scholar] [CrossRef] [Green Version]

- Özer, M.; Kamenković, S.; Grubišić, Z. Frequency domain causality analysis of intra- and inter-regional return and volatility spillovers of South-East European (SEE) stock markets. Econ. Res. Ekon. Istraživanja 2019, 33, 1–25. [Google Scholar] [CrossRef]

- Yarovaya, L.; Matkovskyy, R.; Jalan, A. The COVID-19 Black Swan Crisis: Reaction and recovery of various financial markets. SSRN 2020. [Google Scholar] [CrossRef]

- Aalborg, H.A.; Molnar, P.; de Vries, J.E. What can explain the price, volatility and trading volume of Bitcoin? Financ. Res. Lett. 2020, 29, 255–265. [Google Scholar] [CrossRef]

- Goodell, J.W. COVID-19 and finance: Agendas for future research. Financ. Res. Lett. 2020, 35, 101512. [Google Scholar] [CrossRef] [PubMed]

- Goodell, J.W.; Goutte, S. Co-Movement of COVID-19 and Bitcoin: Evidence from Wavelet Coherence Analysis. 2020. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3597144 (accessed on 1 June 2020).

- Cheach, F. Speculative bubbles in Bitcoin markets? An empirical investigation into the fundamental value of Bitcoin. Econ. Lett. 2015, 130, 32–36. [Google Scholar] [CrossRef] [Green Version]

- Hafner, C.M. Testing for bubbles in cryptocurrencies with time-varying volatility. J. Financ. Econ. 2018. [Google Scholar] [CrossRef]

- Maiti, M.; Grubisic, Z.; Vukovic, D.B. Dissecting tether’s nonlinear dynamics during Covid-19. J. Open Innov. Technol. Mark. Complex. 2020, 6, 161. [Google Scholar] [CrossRef]

- Ardia, D.; Bluteau, K.; Rüede, M. Regime changes in Bitcoin GARCH volatility dynamics. Financ. Res. Lett. 2019, 29, 266–271. [Google Scholar] [CrossRef]

- Griffin, J.M.; Shams, A. Is bitcoin really un-tethered. SSRN 2019. [Google Scholar] [CrossRef]

- Liu, Y.; Tsyvinski, A. Risks and returns of cryptocurrency. Rev. Financ. Stud. 2021, 34, 2689–2727. [Google Scholar] [CrossRef]

- Brunnermeier, M.K.; Nagel, S. Hedge funds and the technology bubble. J. Financ. 2004, 59, 2013–2040. [Google Scholar] [CrossRef] [Green Version]

- Shi, S.; Arora, V. An application of models of speculative behaviour to oil prices. Econ. Lett. 2012, 115, 469–472. [Google Scholar] [CrossRef] [Green Version]

- Tsvetanov, D.; Coakley, J.; Kellard, N. Bubbling over! The behaviour of oil futures along the yield curve. J. Empir. Financ. 2016, 38, 516–533. [Google Scholar] [CrossRef] [Green Version]

- Kruse, R.; Wegener, C. Time-varying persistence in real oil prices and its determinant. Energy Econ. 2020, 85, 104328. [Google Scholar] [CrossRef]

- Liu, J.; Serletis, A. Volatility in the cryptocurrency market. Open Econ. Rev. 2019, 30, 779–811. [Google Scholar] [CrossRef] [Green Version]

- Fakhfekh, M.; Jeribi, A. Volatility dynamics of crypto-currencies’ returns: Evidence from asymmetric and long memory GARCH models. Res. Int. Bus. Financ. 2020, 51, 101075. [Google Scholar] [CrossRef]

- Bouri, E.; Vo, X.V.; Saeed, T. Return equicorrelation in the cryptocurrency market: Analysis and determinants. Financ. Res. Lett. 2021, 38, 101497. [Google Scholar] [CrossRef]

- Bouri, E.; Shahzad, S.J.H.; Roubaud, D. Co-explosivity in the cryptocurrency market. Financ. Res. Lett. 2019, 29, 178–183. [Google Scholar] [CrossRef]

- Baek, C.; Elbeck, M.A. Bitcoins as an investment or speculative vehicle? A first look. Appl. Econ. Lett. 2015, 22, 30–34. [Google Scholar] [CrossRef]

- Dyhrberg, A.H. Bitcoin, gold and the dollar—A GARCH volatility analysis. Financ. Res. Lett. 2016, 16, 85–92. [Google Scholar] [CrossRef] [Green Version]

- Bouri, E.; Das, M.; Gupta, R.; Roubaud, D. Spillovers between Bitcoin and other assets during bear and bull markets. Appl. Econ. 2018, 50, 5935–5949. [Google Scholar] [CrossRef] [Green Version]

- Dyhrberg, A.H. Hedging capabilities of bitcoin. Is it a virtual gold. Financ. Res. Lett. 2016, 16, 139–144. [Google Scholar] [CrossRef] [Green Version]

- Baur, D.G.; Dimpfl, T.; Kuck, K. Bitcoin, gold and the US dollar—A replication and extension. Financ. Res. Lett. 2018, 25, 103–110. [Google Scholar] [CrossRef]

- Jeevan, R.; Shubhashree, P.K.A. Arbitrary behavior of bitcoin towards gold and crudeoil. Int. J. Res. Anal. Rev. 2019, 6, 481–486. [Google Scholar]

- Baur, D.G.; Glover, K.J. The destruction of a safe haven asset? Appl. Financ. Lett. 2012, 1, 8. [Google Scholar] [CrossRef] [Green Version]

- Shrydeh, N.; Shahateet, M.; Mohammad, S.; Sumadi, M. The hedging effectiveness of gold against US stocks in a post-financial crisis era. Cogent Econ. Financ. 2019, 7. [Google Scholar] [CrossRef]

- Chen, K.; Wang, M. Is gold a hedge and safe haven for stock market? Appl. Econ. Lett. 2018, 26, 1080–1086. [Google Scholar] [CrossRef]

- Dar, A.B.; Mitra, D. Is gold a weak or strong hedge and safe haven against stocks? Robust evidences from three major gold-consuming countries. Appl. Econ. 2017, 49, 5491–5503. [Google Scholar] [CrossRef]

- Beckmann, J.; Berger, T.; Czudaj, R. Gold price dynamics and the role of uncertainty. Quant. Financ. 2018, 19, 663–681. [Google Scholar] [CrossRef] [Green Version]

- Maiti, M.; Vyklyuk, Y.; Vuković, D. Cryptocurrencies chaotic co-movement forecasting with neural networks. Internet Technol. Lett. 2020, 3, e157. [Google Scholar] [CrossRef]

- Qiuhua, X.; Yixuan, Z.; Ziyang, Z. Tail-risk spillovers in cryptocurrency markets. Financ. Res. Lett. 2021, 38, 101453. [Google Scholar]

- Ji, Q.; Bouri, E.; Lau, C.K.M.; Roubaud, D. Dynamic connectedness and integration in cryptocurrency markets. Int. Rev. Financ. Anal. 2019, 63, 257–272. [Google Scholar] [CrossRef]

- Zięba, D.; Kokoszczynski, R.; Śledziewska, K. Shock transmission in the cryptocurrency market. Is Bitcoin the most influential? Int. Rev. Financ. Anal. 2019, 64, 102–125. [Google Scholar] [CrossRef]

- Härdle, W.K.; Wang, W.; Yu, L. TENET: Tail-Event driven NETwork risk. J. Econ. 2016, 192, 499–513. [Google Scholar] [CrossRef]

- Fan, Y.; Härdle, W.K.; Wang, W.; Zhu, L. Single-index-based CoVaR with very high-dimensional covariates. J. Bus. Econ. Stat. 2017, 36, 212–226. [Google Scholar] [CrossRef] [Green Version]

- Ike, G.N.; Usman, O.; Sarkodie, S.A. Testing the role of oil production in the environmental Kuznets curve of oil producing countries: New insights from Method of Moments Quantile Regression. Sci. Total Environ. 2020, 711, 135208. [Google Scholar] [CrossRef]

- Koenker, R.W.; Bassett, G., Jr. Regression quantiles. Econometrica 1978, 46, 33–50. [Google Scholar] [CrossRef]

- Koenker, R.W.; Hallock, G. Quantile regression. J. Econ. Perspect. 2001, 15, 143–156. [Google Scholar] [CrossRef]

- Allen, D.E.; Powell, S.R. Asset pricing, the Fama—French Factor Model and the implications of quantile-regression analysis. In Financial Econometrics Modeling: Market Microstructure, Factor Models and Financial Risk Measures; Gregoriou, G.N., Pascalau, G.N., Eds.; Palgrave Macmillan: London, UK, 2011. [Google Scholar]

- Barnes, M.L.; Hughes, A.W. A Quantile regression analysis of the cross section of stock market returns. SSRN 2004. [Google Scholar] [CrossRef] [Green Version]

- Onyedikachi, J. Quantile regression analysis as a robust alternative to ordinary least squares. Sci. Afr. 2009, 8, 61–65. [Google Scholar]

- Karlsson, A. Estimation and inference for quantile regression of longitudinal data, with applications in biostatistic. Diss. Acta Univ. Ups. 2006, 18, 36. [Google Scholar]

- Buchinsky, M. Recent advances in quantile regression models: A practical guideline for empirical research. J. Hum. Resour. 1998, 33, 88. [Google Scholar] [CrossRef]

- Jareño, F.; de la O González, M.; Tolentino, M.; Sierra, K. Bitcoin and gold price returns: A quantile regression and NARDL analysis. Resour. Policy 2020, 67, 101666. [Google Scholar] [CrossRef]

- Nardo, M.; Saisana, M.; Saltelli, A.; Tarantola, S. Tools for Composite Indicators Building; Working paper No. EUR 21682 EN.; European Commission: Ispra, Italy, 2005. [Google Scholar]

- Nardo, M.; Saisana, M.; Saltelli, A.; Tarantola, S.; Hoffman, A.; Giovannini, E. Handbook on Constructing Composite Indicators: Methodology and User Guide; OECD: Ispra, Italy, 2008. [Google Scholar]

- Maiti, M.; Jadhav, P. Impact of pollution level, death rate and illness on economic growth: Evidences from global economy. SN Bus. Econ. 2021. [Google Scholar] [CrossRef]

- Vukovic, D.B.; Lapshina, K.A.; Maiti, M. Wavelet coherence analysis of returns, volatility and interdependence of the US and the EU money markets: Pre & post crisis. N. Am. J. Econ. Financ. 2021, 58, 101457. [Google Scholar] [CrossRef]

- Maiti, M.; Vukovic, D.; Krakovich, V.; Pandey, M.K. How integrated are cryptocurrencies. Int. J. Big Data Manag. 2020, 1, 64–80. [Google Scholar] [CrossRef]

- Maiti, M. OLS versus quantile regression in extreme distributions. Contaduría Adm. 2019, 64, 12. [Google Scholar] [CrossRef]

- Maiti, M. Quantile regression, asset pricing and investment decision. IIMB Manag. Rev. 2021, 33, 28–37. [Google Scholar] [CrossRef]

- Maiti, M.; Maiti, J. A study on India’s first offshore LIDAR-based wind profiling at Gulf of Khambhat. J. Public Aff. 2020, 20, e2044. [Google Scholar] [CrossRef]

- Maiti, M. A critical review on evolution of risk factors and factor models. J. Econ. Surv. 2020, 34, 175–184. [Google Scholar] [CrossRef]

- Maiti, M. A Six Factor Asset Pricing Model. Ph.D. Thesis, Pondicherry University, Puducherry, India, 2018. Available online: http://dspace.pondiuni.edu.in/jspui/bitstream/123456789/3180/1/T6617.pdf (accessed on 1 May 2021).

- Maiti, M. Is ESG the succeeding risk factor? J. Sustain. Financ. Invest. 2021, 11, 199–213. [Google Scholar] [CrossRef]

- Maiti, M.; Balakrishnan, A. Can leverage effect coexist with value effect? IIMB Manag. Rev. 2020, 32, 7–23. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| COVID-19 | GOLD | GT * | OIL | S&P 500 | VIX | |

|---|---|---|---|---|---|---|

| Mean | 0.279 | 0.002 | 38.531 | −0.002 | −0.003 | 0.025 |

| Std. Dev. | 1.105 | 0.019 | 11.943 | 0.093 | 0.038 | 0.141 |

| Skewness | 2.911 | 0.451 | 2.526 | 0.242 | 0.328 | 1.098 |

| Kurtosis | 11.559 | 6.118 | 11.271 | 5.510 | 4.708 | 4.640 |

| COVID-19 | GOLD | GT * | OIL | S&P 500 | VIX | |

|---|---|---|---|---|---|---|

| COVID-19 | 1.000 | |||||

| GOLD | −0.011 | 1.000 | ||||

| GT | 0.029 | −0.233 | 1.000 | |||

| OIL | −0.057 | 0.107 | 0.083 | 1.000 | ||

| S&P 500 | 0.096 | −0.095 | 0.110 | −0.191 | 1.000 | |

| VIX | 0.058 | 0.091 | −0.147 | 0.009 | −0.692 | 1.000 |

| C | COVID-19 | GOLD | GT | OIL | S&P 500 | VIX | R2 | |

|---|---|---|---|---|---|---|---|---|

| Bitcoin | 0.029 | 0.005 | 0.017 | −0.001 | 0.116 ** | 0.570 * | −0.068 | 0.260 |

| Ethereum | 0.005 | 0.006 | 0.174 | 0.000 | 0.190 * | 0.822 * | −0.057 | 0.274 |

| XRP | −0.009 | 0.008 | −0.033 | 0.000 | 0.112 ** | 0.673 * | −0.034 | 0.274 |

| Tether | −0.004 | −0.002 * | 0.036 | 0.000 | −0.027 * | −0.076 * | 0.005 | 0.218 |

| Bitcoin Cash | 0.004 | 0.003 | −0.178 | 0.000 | 0.156 ** | 0.790 * | −0.044 | 0.210 |

| Coefficient Values | ||||||||

|---|---|---|---|---|---|---|---|---|

| C | COVID-19 | GOLD | GT | OIL | S&P 500 | VIX | ||

| 0.05 | 0.145 | −0.001 | −0.581 | −0.006 | 0.295 | 1.696 | 0.166 | Bitcoin |

| 0.25 | 0.015 | 0.001 | −0.151 | −0.001 | 0.180 | 0.652 | 0.008 | |

| 0.5 | 0.016 | −0.002 | 0.008 | 0.000 | 0.123 | 0.620 | 0.022 | |

| 0.75 | −0.019 | 0.001 | 0.067 | 0.001 | 0.085 | 0.517 | 0.019 | |

| 0.95 | −0.076 | −0.008 | 0.358 | 0.004 | −0.145 | 0.487 | −0.003 | |

| 0.05 | −0.092 | 0.024 | 1.630 | −0.001 | 0.224 | −0.221 | −0.533 | Ethereum |

| 0.25 | 0.007 | 0.000 | −0.024 | −0.001 | 0.194 | 0.718 | 0.021 | |

| 0.5 | 0.001 | −0.001 | −0.188 | 0.000 | 0.184 | 0.862 | 0.052 | |

| 0.75 | 0.013 | −0.007 | 0.321 | 0.001 | 0.114 | 1.207 | 0.062 | |

| 0.95 | 0.045 | 0.002 | 0.680 | 0.001 | −0.072 | 0.444 | −0.158 | |

| 0.05 | −0.022 | 0.016 | 1.325 | −0.002 | 0.162 | 0.192 | −0.214 | XRP |

| 0.25 | 0.002 | 0.004 | −0.350 | −0.001 | 0.204 | 0.826 | 0.062 | |

| 0.5 | −0.028 | 0.003 | −0.170 | 0.001 | 0.130 | 0.572 | −0.008 | |

| 0.75 | 0.004 | 0.003 | −0.361 | 0.001 | 0.090 | 0.760 | 0.064 | |

| 0.95 | 0.032 | 0.006 | 0.118 | 0.001 | −0.012 | 0.432 | −0.041 | |

| 0.05 | 0.015 | 0.000 | 0.183 | 0.000 | −0.035 | −0.143 | −0.007 | Tether |

| 0.25 | 0.002 | 0.000 | 0.036 | 0.000 | −0.010 | 0.007 | 0.002 | |

| 0.5 | 0.000 | 0.000 | 0.011 | 0.000 | −0.003 | 0.005 | 0.000 | |

| 0.75 | −0.002 | 0.000 | 0.012 | 0.000 | −0.009 | −0.018 | 0.000 | |

| 0.95 | −0.002 | −0.003 | −0.193 | 0.000 | −0.019 | 0.009 | 0.058 | |

| 0.05 | −0.164 | 0.022 | 0.934 | 0.001 | 0.306 | −0.040 | −0.460 | Bitcoin Cash |

| 0.25 | −0.011 | 0.004 | −0.235 | 0.000 | 0.238 | 0.750 | −0.050 | |

| 0.5 | 0.012 | −0.001 | −0.405 | 0.000 | 0.177 | 0.755 | 0.028 | |

| 0.75 | 0.034 | −0.006 | 0.118 | 0.000 | 0.135 | 0.734 | 0.012 | |

| 0.95 | 0.153 | −0.019 | −0.722 | −0.001 | −0.210 | 0.810 | −0.166 | |

| p values | ||||||||

| C | COVID-19 | GOLD | GT | OIL | S&P 500 | VIX | ||

| 0.05 | 0.000 | 0.802 | 0.247 | 0.000 | 0.026 | 0.000 | 0.044 | Bitcoin |

| 0.25 | 0.745 | 0.763 | 0.641 | 0.568 | 0.034 | 0.000 | 0.851 | |

| 0.5 | 0.495 | 0.392 | 0.963 | 0.536 | 0.002 | 0.000 | 0.507 | |

| 0.75 | 0.354 | 0.854 | 0.840 | 0.091 | 0.354 | 0.075 | 0.730 | |

| 0.95 | 0.316 | 0.065 | 0.595 | 0.076 | 0.293 | 0.375 | 0.966 | |

| 0.05 | 0.013 | 0.007 | 0.016 | 0.300 | 0.057 | 0.679 | 0.061 | Ethereum |

| 0.25 | 0.655 | 0.970 | 0.932 | 0.120 | 0.021 | 0.003 | 0.749 | |

| 0.5 | 0.947 | 0.775 | 0.726 | 0.818 | 0.054 | 0.051 | 0.439 | |

| 0.75 | 0.502 | 0.101 | 0.707 | 0.125 | 0.254 | 0.003 | 0.298 | |

| 0.95 | 0.088 | 0.842 | 0.340 | 0.077 | 0.622 | 0.489 | 0.085 | |

| 0.05 | 0.761 | 0.111 | 0.026 | 0.319 | 0.058 | 0.626 | 0.254 | XRP |

| 0.25 | 0.972 | 0.499 | 0.207 | 0.733 | 0.038 | 0.004 | 0.461 | |

| 0.5 | 0.071 | 0.502 | 0.509 | 0.047 | 0.044 | 0.006 | 0.893 | |

| 0.75 | 0.828 | 0.651 | 0.568 | 0.198 | 0.106 | 0.001 | 0.202 | |

| 0.95 | 0.323 | 0.703 | 0.866 | 0.339 | 0.903 | 0.128 | 0.458 | |

| 0.05 | 0.008 | 0.763 | 0.005 | 0.000 | 0.014 | 0.016 | 0.540 | Tether |

| 0.25 | 0.635 | 0.826 | 0.466 | 0.517 | 0.463 | 0.844 | 0.647 | |

| 0.5 | 0.979 | 0.881 | 0.718 | 0.965 | 0.544 | 0.846 | 0.922 | |

| 0.75 | 0.563 | 0.226 | 0.763 | 0.411 | 0.428 | 0.658 | 0.990 | |

| 0.95 | 0.888 | 0.001 | 0.113 | 0.157 | 0.362 | 0.934 | 0.154 | |

| 0.05 | 0.000 | 0.003 | 0.283 | 0.052 | 0.019 | 0.944 | 0.114 | Bitcoin Cash |

| 0.25 | 0.523 | 0.399 | 0.494 | 0.562 | 0.003 | 0.009 | 0.490 | |

| 0.5 | 0.347 | 0.818 | 0.295 | 0.531 | 0.019 | 0.003 | 0.748 | |

| 0.75 | 0.003 | 0.153 | 0.841 | 0.430 | 0.149 | 0.006 | 0.864 | |

| 0.95 | 0.000 | 0.002 | 0.385 | 0.074 | 0.116 | 0.068 | 0.043 | |

| C | COVID-19 | GOLD | GT | OIL | S&P 500 | VIX | R2 | |

|---|---|---|---|---|---|---|---|---|

| Bitcoin | 0.059 | −0.002 | −0.055 | −0.016 | 0.142 * | 0.656 * | 0.045 | 0.229 |

| Ethereum | 0.016 | −0.001 | 0.160 | −0.003 | 0.231 * | 0.869 * | 0.049 | 0.138 |

| XRP | −0.117 | 0.002 | −0.175 | 0.033 | 0.148 * | 0.730 * | 0.027 | 0.225 |

| Tether | 0.000 | 0.000 | 0.007 | 0.000 | 0.001 | 0.018 * | 0.002 | 0.031 |

| Bitcoin Cash | −0.091 | −0.001 | −0.521 | 0.024 | 0.216 * | 1.097 * | 0.060 | 0.194 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Vukovic, D.; Maiti, M.; Grubisic, Z.; Grigorieva, E.M.; Frömmel, M. COVID-19 Pandemic: Is the Crypto Market a Safe Haven? The Impact of the First Wave. Sustainability 2021, 13, 8578. https://doi.org/10.3390/su13158578

Vukovic D, Maiti M, Grubisic Z, Grigorieva EM, Frömmel M. COVID-19 Pandemic: Is the Crypto Market a Safe Haven? The Impact of the First Wave. Sustainability. 2021; 13(15):8578. https://doi.org/10.3390/su13158578

Chicago/Turabian StyleVukovic, Darko, Moinak Maiti, Zoran Grubisic, Elena M. Grigorieva, and Michael Frömmel. 2021. "COVID-19 Pandemic: Is the Crypto Market a Safe Haven? The Impact of the First Wave" Sustainability 13, no. 15: 8578. https://doi.org/10.3390/su13158578

APA StyleVukovic, D., Maiti, M., Grubisic, Z., Grigorieva, E. M., & Frömmel, M. (2021). COVID-19 Pandemic: Is the Crypto Market a Safe Haven? The Impact of the First Wave. Sustainability, 13(15), 8578. https://doi.org/10.3390/su13158578