1. Introduction

Recent literature on economic policy uncertainty (EPU) and sustainable economic growth has mostly addressed issues related to financial stability without due regards being given to debt financing instruments. For example, Phan et al. [

1], Ashraf and Shen [

2], Xu et al. [

3], and Guedhami et al. [

4] are among those who considered various EPU models and financial stability. However, the issue of EPU on sustainable economic growth under debt financing practices vis-à-vis a socioeconomic structure based on cultural values is ignored. This paper fills this gap in the literature and unveils interesting dynamic characteristics of national culture, which play a defining role in debt financing under EPU. Phan et al. [

1] investigated the impact of EPU on financial stability, demonstrating a significantly negative impact. This motivated the idea to redefine EPU as an assortment of economic risk, which converts an evolution into an ambiguous position, e.g., monetary, and fiscal policy uncertainty, tax regime uncertainty, and other regulatory institution uncertainty. Furthermore, it is defined as the discrepancies confronted by economic mediators in forecasting the future course of fiscal policies, regulatory, monetary, and trade policy [

5]. Many academic scholars and other policy makers have admitted the dreadful outcomes of economic policy uncertainty on sustainable economic growth. Baker et al. (2016) highlight that the industrial production of the USA during 2005 to 2012 decreased by 1.1 percent due to an increment in economic policy uncertainty. According to Business media, there was a wave of 1 percent in gross domestic product (GDP), and 1 million employees were sacked during the year 2011 to 2012 after a huge positive economic policy uncertainty shock in the USA [

6]. The economies where economic policy uncertainty exists change their behaviors and decisions dynamically.

Hofstede [

7] defined the term “culture” as the collectively programming of the human mind that separates the masses of one country, group, or region from the other countries, regions, or groups. He also debates that anyone can demonstrate the culture of a state by following six cultural dimensions. However, this study has taken uncertainty avoidance as a proxy of national culture, which means that having a high uncertainty avoidance culture leads to managers’ risk-averse and non-flexible behaviors. The managers eradicate obscurities before making any decisions and prefer those decisions which have minimum risk. Moreover, in an ardent, contemporary, and vigorous business environment, the purpose of gaining economic efficiency in the firm is not only attached to technical novelty, but it is also associated with national-level factors, i.e., country-level culture. The research has acknowledged the significant impact of EPU on firm financing policy [

8,

9]. These studies recognized that there exist negative links between EPU and firm financing decisions, but this study encompasses national culture affect for bending risk-averse behavior into risk-friendly behavior. Does culture play a moderating role in enhancing debt financing with high EPU economies? The culture plays a vital contribution in the vigorous planning of business. The numerous tools and techniques of management at the firm level apply according to cultural values which can modify the firm manager’s decision. The valuation of human behavior (which becomes cultural values) differs across borders (countries).

The most familiar debate in finance literature is firm financing decisions despite vast research on the topic. Although there are various finance theories for advocating efficient capital structure, there is no theory which generalizes this trend. The companies have two sources which are used to fulfill their funding needs, i.e., interior, and exterior sources of funding. The interior basis financing comprises of retained earnings or capital reserves. As per the pecking order theory, the firms prefer to use their inside funding first, and if they do not have enough internal funds, then they seek external funding sources. The external funds are further separated into equity and debt sources of financing. The theories of capital structure, i.e., pecking order theory, trade-off theory, and agency cost theory, argue about equity and debt financing. Generally, firms follow financing opportunities according to the pecking order theory, i.e., capital reserve, debt sources of financing, and equity sources of financing. According to Modigliani and Miller’s [

10] trade-off theory, the firms prefer more economical fund sources, i.e., high EPU leads to spreading information asymmetry, which creates biases and hence firms prefer debt financing over economical financing. Most of the firms prefer debt financing because it curbs the important information to spread. Moreover, Jensen and Meckling [

11] highlighted that agency cost theory is applicable during high EPU, convincing the management towards debt financing as it increases firms’ wealth by mitigating the conflict between managers and shareholders. The managers try to eliminate the agency conflict by adopting debt financing. Thus, Myers and Majluf [

12] used pecking order theory, which proclaims that the firms do not focus to use their internal source of financing due to high EPU and which indicates firms to consider debt as source of financing.

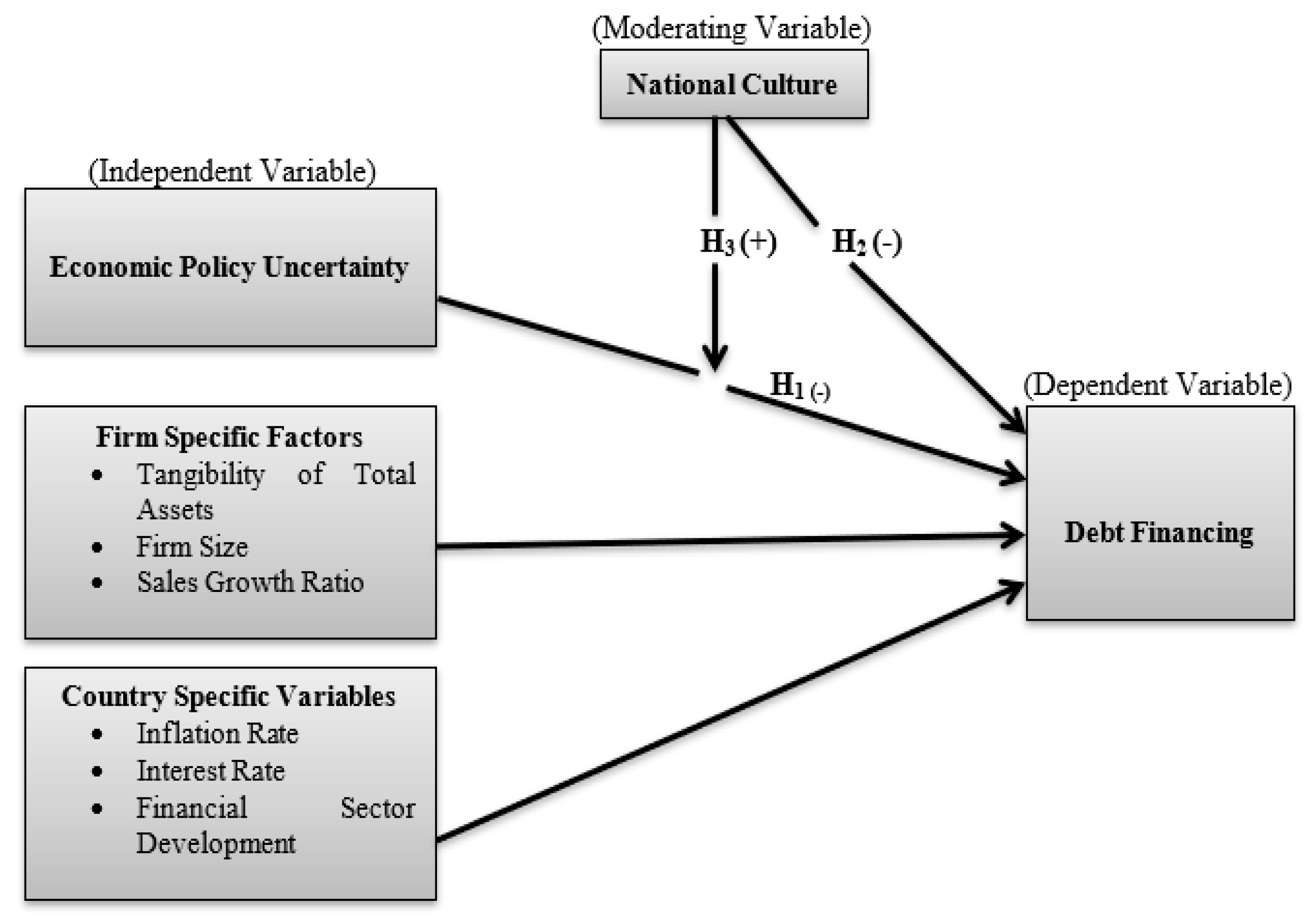

This research attempts to reveal the contribution of EPU in firm financing decisions through the channel of national culture. It inspires to record how EPU influences firm financing decisions with the existence of national culture. The earlier studies have confirmed the effect of EPU on firm financing options and have verified from the literature that the change in national culture has an influence on firm financing decisions. In addition, the national culture has direct influence on firm financing decisions due to the attitude of managers. Furthermore, this research pursues to investigate the moderating effect of national culture with EPU and leverage financing by applying 10 years of data (2007–2016). The System Generalized Method of Moments (GMM) was employed with appropriate instruments due to the problem of endogeneity. The outcomes of this research indicate the vigorous influence of EPU on leverage financing through the moderating effect of national culture. The findings further state that the executives should consider the sensitivity of national culture while making financing decisions with high EPU.

More precisely, this research ascribes to enrich empirical literature on both EPU and financing decisions by accumulating the national level culture. A recent study demonstrated how culture played a moderating role with tax evasion, religiosity, and social norms [

13]. Another recent study considered financing decisions as a moderating variable with national culture and firm financial performance [

3,

4,

14]. However, no research has been conducted to explore this relationship. There is plenty of literature available on the most used determinants of firm financing decisions. Nevertheless, no research has been found which depicts such arrangement of variables, particularly in those economies where the EPU is high. It highlights new understandings of how EPU affects firm financing decisions via channels of national culture. It covers the prevailing literature on EPU and firm debt financing options to national culture and strengthens the results of prior studies which forecasted the influence of EPU on firm debt financing decisions. Moreover, the research holds empirical and practical implications. The empirical outcomes of the research demonstrate how EPU and UND empirically affect debt financing. This study verifies empirically the appearance of national culture to determine debt financing with high EPU economies. Practically, this study advocates for managers to consider the sensitivity of culture while making debt financing decisions with high EPU economies. This aspect (national culture) is non-financial and non-firm specific.

The rest of the paper is organized as follows. In

Section 2, we encompass the theoretical and empirical aspects of the literature and briefly describe the hypotheses development.

Section 3 discusses the data, materials, and methodology used and the research framework and econometrics model implemented in our study.

Section 4 presents some important results obtain from this study. The

Section 5 contains some concluding remarks in outlining the policy implications.

4. Results and Findings

This section demonstrates the findings of the current study on how economic policy uncertainty determines the choice of debt source financing in the presence of national culture. This is performed by computing descriptive statistics for all the variable, which are shown in

Table 4 below.

Table 4 represents the overall reactions of respondent firms in the shape of mean, median, and standard deviation. The leverage ratio has 0.283 as its mean value, which articulates that firms have 28.3 percent debt financing in their capital structure. The digit 0.271 states the median value of the leverage ratio, which is closer to the mean value and reveals the debt financing behavior of firms. Moreover, the standard deviation of LR is 0.174, which shows the level of scattering from its mean value. The skewness and kurtosis have values of 0.381 and 2.508, respectively, which verify the normality of data. Furthermore, the economic policy uncertainty has 129.0 as its mean value and 127.9 as its median value. The EPU has 0.047 as its standard deviation value, which shows the dispersion of data from its mean value. Furthermore, the skewness has a value of 0.378 and kurtosis has a value of 12.22, and these show that the data are stationary at normal. The mean, median, and standard deviation values of the firm-specific variables exhibit the responses of firms in their firm-specific form. The 2.487 percent is the average interest rate of the mentioned countries. Similarly, an average inflation rate is 2.745 percent, which is normal. The financial sector development has 0.696 as its mean value, which shows that the mentioned countries are advanced because, according to the IMF, economies having more than 0.60 FSD statistics are considered as developed. The next section is about the correlation analysis.

The results of the correlation analysis among the variables are given in

Table 5. The statics’ values corroborate the degree of association among variables. The EPU has positively correlated with the leverage ratio, but UND has a negative correlation with the LR. Similarly, the tangibility and sales growth ratios are positively correlated with the leverage ratio because when the asset tangibility and sales growth ratio enhance, the firms increase the debt ratio. Moreover, the firm size has negatively correlated with leverage ratio because when managers expand their businesses, they obtain financial stability and have enough funds to use. The interest rate and inflation rate are positive correlated with leverage ratio which means that they both are moving in same direction with debt financing. However, financial sector development is negatively correlated with the LR, which also reveals an inverse relation with the LR. The values of the VIF imply that there is no multicollinearity in the data as the values are less than 10 (benchmark is 10).

Table 6 signifies the outcomes of the regression model, which replies to the research query of how EPU effects debt financing. The economic policy uncertainty has −0.009 as its coefficient value, which describes that EPU has a negative and significant link with leverage financing, which also means that the businesses will not prefer debt financing with high uncertainty. Additionally, firms minimize their business activities which will mitigate funds need. Therefore, the probabilities of default debts increase, which forces financial institutions and banks to upsurge their rate of interest. Moreover, tangibility has 0.357 as its coefficient value, which shows a positive relation with debt financing, which also defines that more tangible assets can be used as loan collateral to obtain the debt easily. Similarly, firm size also has a positive coefficient value (0.083), which shows that larger firms are more stable firms, and they may acquire debt for their financing needs. The sales growth ratio has negative coefficient value (−0.013), which means that the debt increases volatility and risk of the firm which will stop risk averse firms from debt financing, and they feel hesitation in growth [

14,

36]. The country-specific variables, i.e., interest rate, has a negative and significant coefficient value (−0.001), which means that there is an inverse relationship between EPU and debt financing because, in high uncertainty economies, the banks and other financial institutions increase their interest rate and the rational managers do not prefer to take debt for financing. Similarly, inflation rate also has an inverse relationship with debt financing, which means that an increment in inflation rate leads to an increase in interest rate, which will expel finance managers in complexities regarding their debt financing. Moreover, the financial sector development has a positive and significant link with debt financing because the businesses in developed economies may obtain the debt on the minimum rate, and they prefer debt for financing.

The adjusted R-square value is 0.559, which represents the degree of cohesiveness with economic policy uncertainty. It also means that the independent variables explain 55.9 percent dependent variable. The value of the standard error is 0.115, which shows responses of contributed firms are just 11.5 from the actual line of regression. The probability value of the J-statistic is 0.165, which is insignificant and shows the valid instruments of GMM.

Table 7 represents the outcomes of the regression analysis, which reply to the research question of how uncertainty avoidance influences debt financing. The coefficient value of the uncertainty avoidance is −0.007, which is less than 0.05 and shows that the uncertainty avoidance has a significant but negative impact on debt. It means that there is an inverse relationship between the uncertainty avoidance and debt financing, which expresses that high uncertainty leads to the pessimistic behavior of corporate managers about debt financing. Furthermore, when firm managers find substitutes and safe ways to finance their businesses, they show an offensive attitude for leverage financing. The rest of the variables, including firm-specific and country-specific variables, are the same relationship as the

Table 6 results. Moreover, the adjusted R-square is 12.9, which is low because the uncertainty avoidance is a non-financial nature of variable.

Table 8 portrays the results of the regression analysis. The EPU has a positive and significant impact on debt financing due to an interaction term in the form of uncertainty avoidance. In addition, the rigid behavior of corporate managers’ expelling them to consider culture importance, which leads to an optimistic behavior towards debt financing. It transforms their risk-adverse behavior into risk-friendly behavior. The norms and values insist that they think optimistically about debt despite high economic policy uncertainty. The other variables, i.e., firm-specific and country-specific variables, have a similar relationship as the

Table 6 and

Table 7 results. Furthermore, the value of the adjusted R-square is 0.726, whereas the value of the standard error is 0.052. The

p value of the

J-stat is 0.173 (see

Table 9). Briefly, the study summarizes that there is a significant effect of EPU and UND on debt financing, and it also authenticates the presence of uncertainty avoidance to determine leverage financing in high EPU economies.

We have checked the robustness by using the system GMM model with another proxy of national-level culture (Indulgence) and obtained sustainable outcomes as mentioned in the previous

Table 8. All our outcomes are reliable to a series of robustness checks and offer useful information.

5. Concluding Remarks

This study examines the influence of economic policy uncertainty on debt financing in the presence of national-level culture by using data of non-financial firms from six Asian economies (Pakistan, India, Singapore, China, South Korea, and Japan) from the period of 2007 to 2016. Considering the potential endogeneity problem, we used the generalized method of moments. The overall findings validated the first hypothesis that the economic policy uncertainty negatively drives the corporate debt financing in our sample because uncertainty creates an anonymous situation for the industries to equip capital structure with debt. Similarly, the uncertainty avoidance has an inverse relationship with debt financing due to the pessimistic and risk-averse approach of corporate managers regarding debt financing. Interestingly, we find that national culture positively moderates the negative impact of economic policy uncertainty on debt financing because managers demonstrate rigidity to preserve the culture while opting for debt as a financing source. It implies that the national culture converts risk-averse behavior into risk-tolerant behavior. Moreover, the findings of this study signify that economic policy uncertainty has a significant impact on debt financing via the channel of uncertainty avoidance (national culture).

5.1. Implications

This study offers some empirical and practical implications, which are as follows:

The empirical findings show that economic policy uncertainty and uncertainty avoidance affect debt financing. It authenticates the importance of national culture in diffusing the negative impact of high economic policy uncertainty in financing decisions may not be overlooked in selected Asian economies. It also participates in the literature.

This research practically guides corporate managers by considering the sensitivity of uncertainty avoidance while deliberating about leverage financing with high economic policy uncertainty economies. This aspect (national culture) is non-financial and non-firm specific.

5.2. Limitations and Future Research

The current study has not reflected all Asian economies due to data constraints.

It is time-consuming to consider all the variables that determine debt financing.

This study can be extended by considering primary and secondary sources of financing with six dimensions of culture as determinants of financing.

{kind=link}