Corporate Social Responsibility Development and Climate Change: Regional Evidence of China

Abstract

:1. Introduction and Literature Review

2. Data and Methods

2.1. Firm-Level Data

2.2. Provincial-Level Data

2.3. Methods

3. Analysis and Results

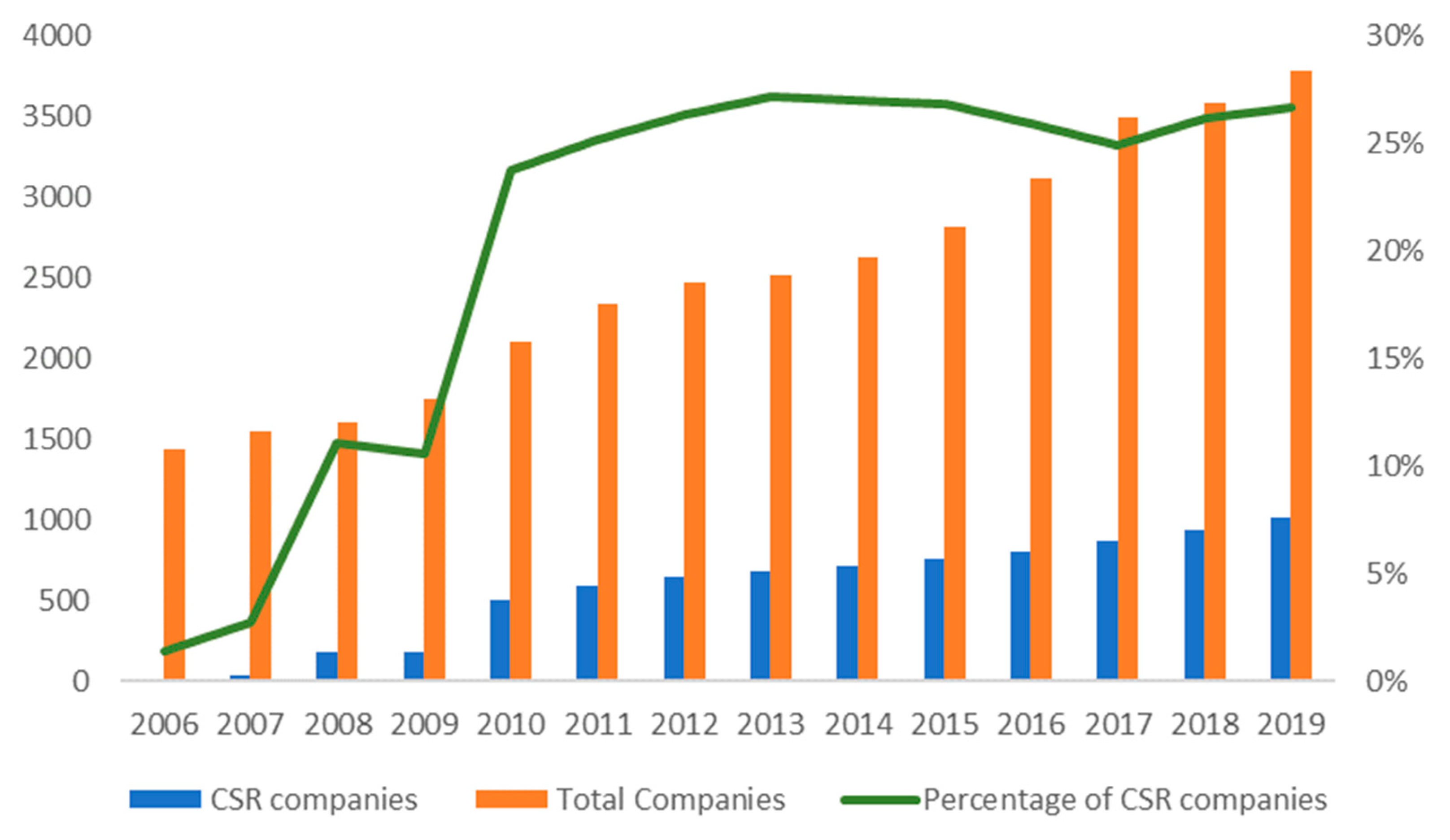

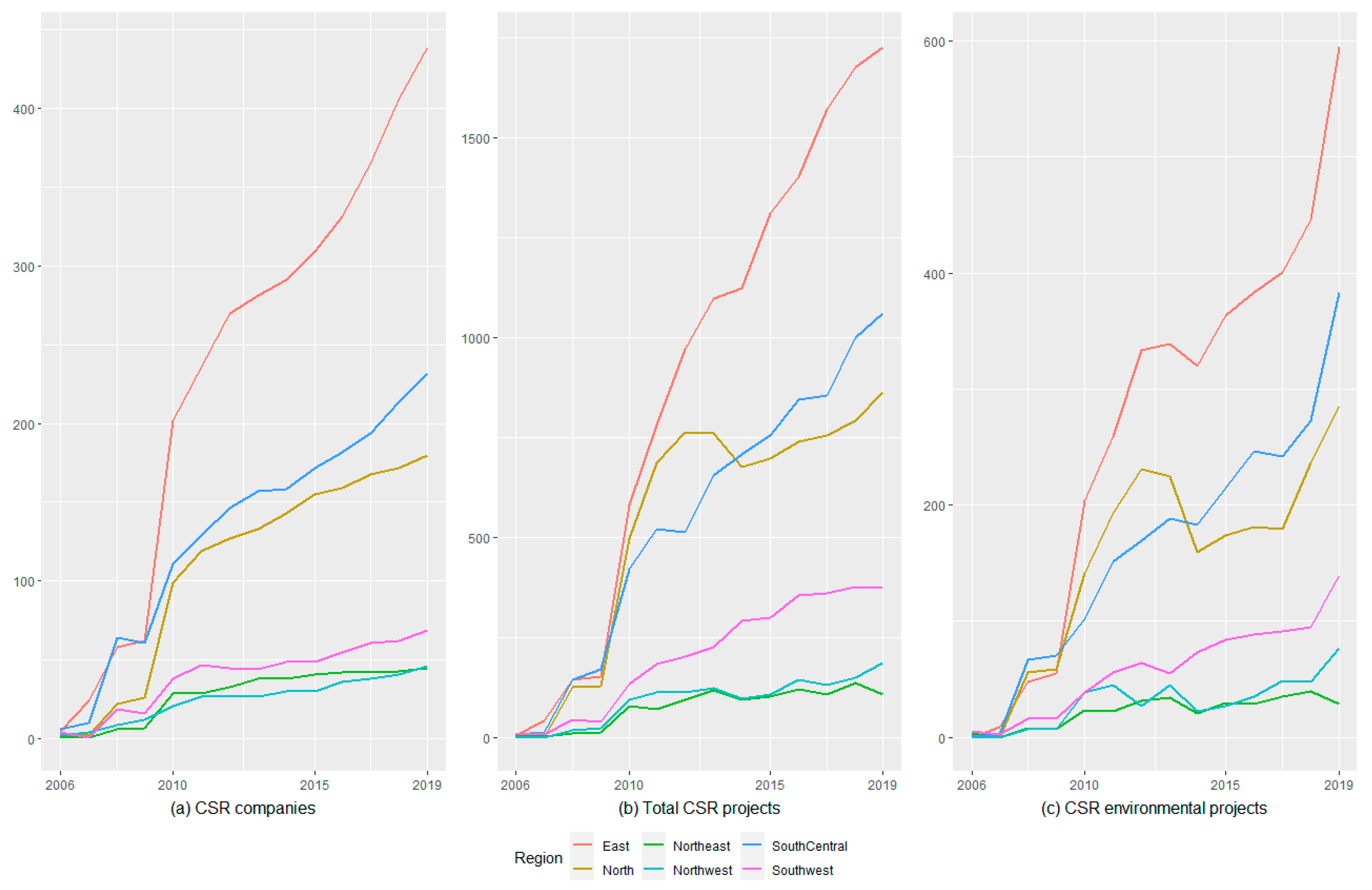

3.1. CSR Development in China

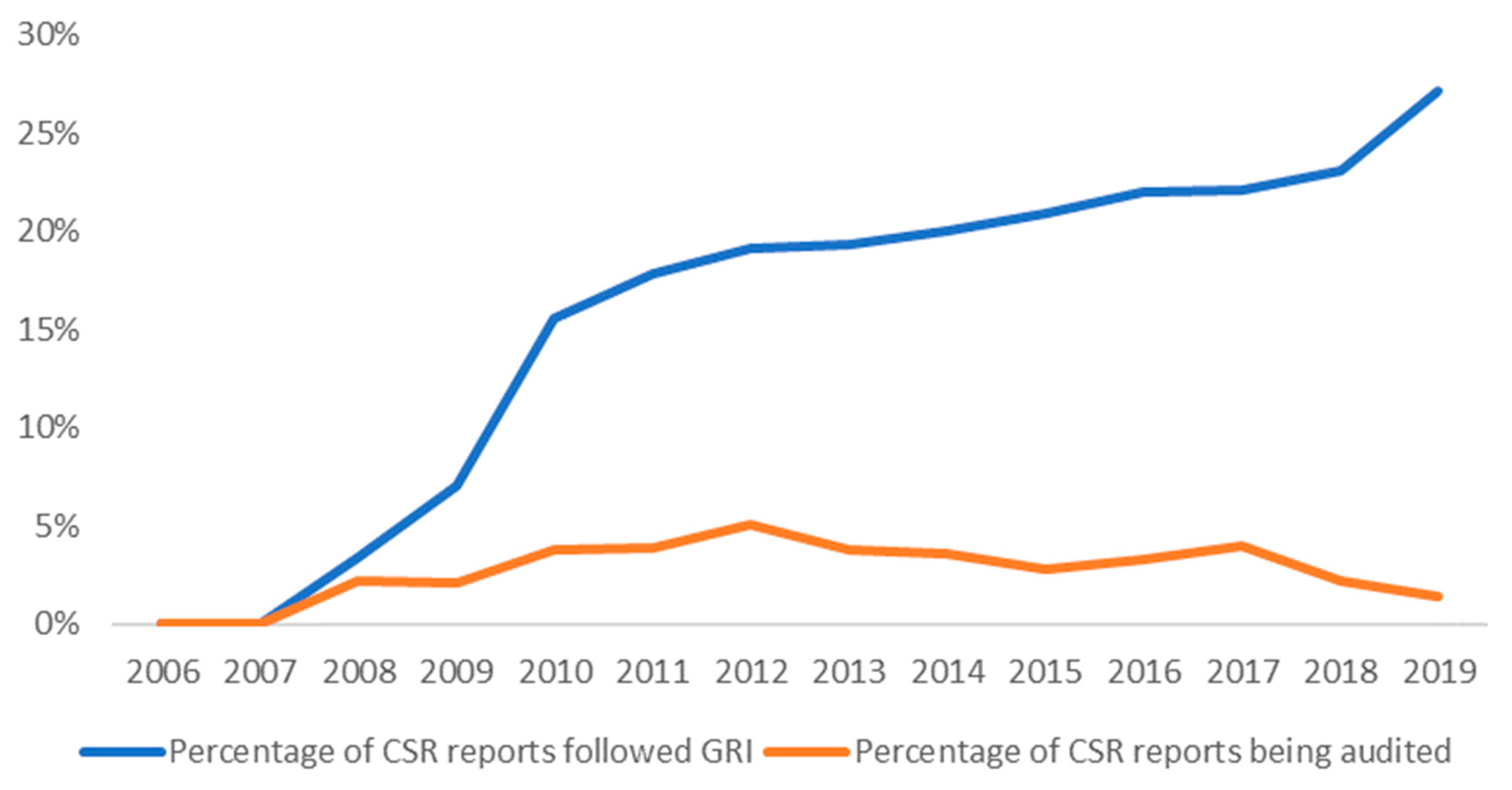

3.2. CSR Disclosure Behavior

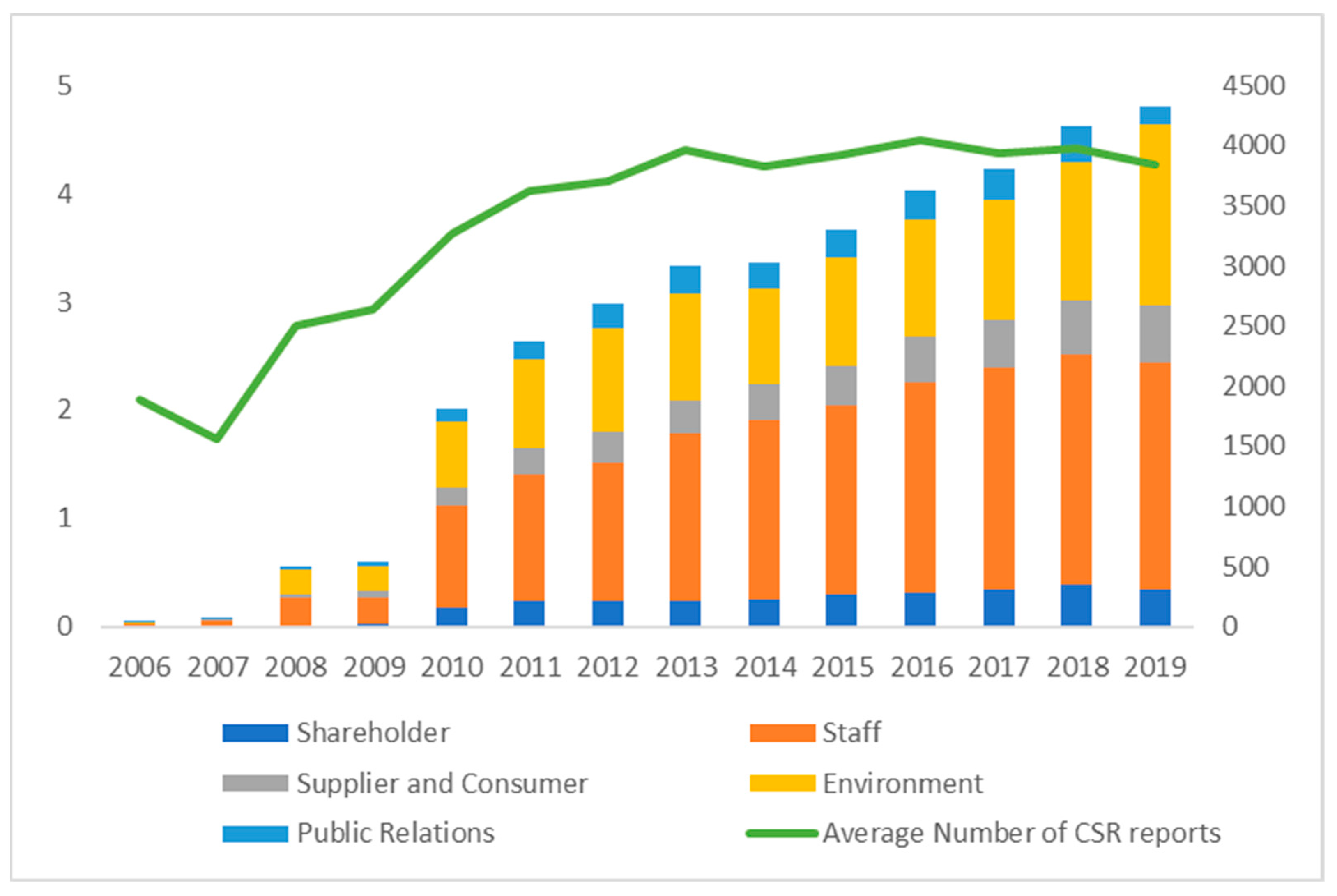

3.3. Firms’ CSR Activities’ Impact on Sustainable Economic Development

4. Conclusions and Discussion

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Region | Province | GDP per Capita (2019, RMB) | CSR Companies (2019) | CSR Projects (2019) |

|---|---|---|---|---|

| North | Beijing * | 164,555 | 129 | 626 |

| Tianjin * | 89,984 | 20 | 111 | |

| Hebei | 46,073 | 15 | 40 | |

| Shanxi | 45,486 | 10 | 53 | |

| Inner Mongolia | 67,766 | 6 | 33 | |

| Northeast | Liaoning | 57,112 | 27 | 81 |

| Jilin | 43,578 | 11 | 20 | |

| Heilongjiang | 36,109 | 7 | 7 | |

| East | Shanghai * | 156,456 | 110 | 601 |

| Jiangsu | 122,251 | 71 | 244 | |

| Zhejiang | 106,773 | 93 | 310 | |

| Anhui | 57,879 | 33 | 131 | |

| Fujian | 106,536 | 69 | 185 | |

| Jiangxi | 52,866 | 17 | 68 | |

| Shandong | 70,050 | 46 | 189 | |

| South-Central | Henan | 55,724 | 35 | 149 |

| Hubei | 76,648 | 28 | 95 | |

| Hunan | 57,667 | 19 | 52 | |

| Guangdong | 93,730 | 133 | 671 | |

| Guangxi | 42,817 | 9 | 70 | |

| Hainan | 56,411 | 8 | 24 | |

| Southwest | Chongqing * | 75,563 | 15 | 75 |

| Sichuan | 55,360 | 28 | 149 | |

| Guizhou | 46,286 | 9 | 41 | |

| Yunnan | 47,805 | 17 | 110 | |

| Northwest | Shaanxi | 66,546 | 15 | 71 |

| Gansu | 32,937 | 7 | 21 | |

| Qinghai | 48,373 | 5 | 11 | |

| Ningxia | 53,935 | 5 | 37 | |

| Xinjiang | 53,893 | 14 | 47 |

References

- Okereke, C.; Wittneben, B.; Bowen, F. Climate Change: Challenging Business, Transforming Politics. Bus. Soc. 2011, 51, 7–30. [Google Scholar] [CrossRef]

- Stanghellini, P.L.; Marchello, M.P.; Michetti, M. Climate Change, Sustainability and Corporate Social Responsibility: The Role of Financial Institutions. In Proceedings of the Sixth International Conference on Ethics and Environmental Policies, Padova, Italy, 23–25 October 2008. [Google Scholar]

- SShu, T.; Liu, Q.; Chen, S.; Wang, S.; Lai, K.K. Pricing Decisions of CSR Closed-Loop Supply Chains with Carbon Emission Constraints. Sustainability 2018, 10, 4430. [Google Scholar] [CrossRef] [Green Version]

- Allen, M.W.; Craig, C.A. Rethinking Corporate Social Responsibility in the Age of Climate Change: A Communication Perspective. Int. J. Corp. Soc. Responsib. 2016, 1, 1–11. [Google Scholar] [CrossRef] [Green Version]

- Elkington, J. Partnerships from Cannibals with Forks: The Triple Bottom Line of 21st-Century Business. Environ. Qual. Manag. 1998, 8, 37–51. [Google Scholar] [CrossRef]

- Hopkins, M. Corporate Social Responsibility and International Development: Is Business the Solution? Routledge: Abingdon-on-Thames, Oxfordshire, UK, 2012. [Google Scholar]

- Berger-Walliser, G.; Scott, I. Redefining Corporate Social Responsibility in an Era of Globalization and Regulatory Hardening. Am. Bus. Law J. 2018, 55, 167–218. [Google Scholar] [CrossRef]

- Patten, D.M. Intra-Industry Environmental Disclosures in Response to the Alaskan Oil Spill: A Note on Legitimacy Theory. Account. Organ. Soc. 1992, 17, 471–475. [Google Scholar] [CrossRef]

- Breton, G. A Postmodern Accounting Theory: An Institutional Approach; Emerald Group Publishing: Bingley, UK, 2018; ISBN 978-1-78769-795-9. [Google Scholar]

- Deegan, C.M. Legitimacy Theory: Despite Its Enduring Popularity and Contribution, Time Is Right for a Necessary Makeover. AAAJ 2019, 32. [Google Scholar] [CrossRef]

- Deegan, C. Introduction: The Legitimising Effect of Social and Environmental Disclosures—A Theoretical Foundation. Acc. Audit. Account. J. 2002, 15, 282–311. [Google Scholar] [CrossRef]

- Adams, C.A. Internal Organisational Factors Influencing Corporate Social and Ethical Reporting: Beyond Current Theorising. Acc. Audit. Account. J. 2002, 15, 223–250. [Google Scholar] [CrossRef]

- Renukappa, S.; Akintoye, A.; Egbu, C.; Goulding, J. Carbon Emission Reduction Strategies in the UK Industrial Sectors: An Empirical Study. Int. J. Clim. Chang. Strat. Manag. 2013, 5, 304–323. [Google Scholar] [CrossRef]

- Cormier, D.; Magnan, M. Corporate Environmental Disclosure Strategies: Determinants, Costs and Benefits. J. Account. Audit. Financ. 1999, 14, 429–451. [Google Scholar] [CrossRef]

- Cormier, D.; Magnan, M. Environmental Reporting Management: A Continental European Perspective. J. Account. Public Policy 2003, 22, 43–62. [Google Scholar] [CrossRef]

- Larrinaga, C.; Carrasco, F.; Correa, C.; Llena, F.; Moneva, J. Accountability and Accounting Regulation: The Case of the Spanish Environmental Disclosure Standard. Eur. Account. Rev. 2002, 11, 723–740. [Google Scholar] [CrossRef]

- O’Dwyer, B.; Unerman, J.; Hession, E. User Needs in Sustainability Reporting: Perspectives of Stakeholders in Ireland. Eur. Account. Rev. 2005, 14, 759–787. [Google Scholar] [CrossRef]

- Sharfman, M.P.; Fernando, C.S. Environmental Risk Management and the Cost of Capital. Strat. Manag. J. 2008, 29, 569–592. [Google Scholar] [CrossRef]

- Jo, H.; Na, H. Does CSR Reduce Firm Risk? Evidence from Controversial Industry Sectors. J. Bus. Ethics 2012, 110, 441–456. [Google Scholar] [CrossRef]

- Cordeiro, J.J.; Tewari, M. Firm Characteristics, Industry Context, and Investor Reactions to Environmental CSR: A Stakeholder Theory Approach. J. Bus. Ethics 2015, 130, 833–849. [Google Scholar] [CrossRef]

- Othman, S.; Darus, F.; Arshad, R. The Influence of Coercive Isomorphism on Corporate Social Responsibility Reporting and Reputation. Soc. Responsib. J. 2011, 7, 119–135. [Google Scholar] [CrossRef]

- Sadou, A.; Alom, F.; Laluddin, H. Corporate Social Responsibility Disclosures in Malaysia: Evidence from Large Companies. SRJ 2017, 13, 177–202. [Google Scholar] [CrossRef]

- Sana, S.S. Price Competition between Green and Non Green Products under Corporate Social Responsible Firm. J. Retail. Consum. Serv. 2020, 55, 102118. [Google Scholar] [CrossRef]

- Ye, M.; Lu, W.; Flanagan, R.; Chau, K.W. Corporate Social Responsibility “Glocalisation”: Evidence from the International Construction Business. Corp. Soc. Responsib. Environ. Manag. 2020, 27, 655–669. [Google Scholar] [CrossRef]

- Chen, Y.-C.; Hung, M.; Wang, Y. The Effect of Mandatory CSR Disclosure on Firm Profitability and Social Externalities: Evidence from China. J. Account. Econ. 2018, 65, 169–190. [Google Scholar] [CrossRef]

- Kolk, A. Environmental Reporting by Multinationals from the Triad: Convergence or Divergence? MIR Manag. Int. Rev. 2005, 45, 145–166. [Google Scholar]

- Haque, S.; Deegan, C. Corporate Climate Change-Related Governance Practices and Related Disclosures: Evidence from Australia: Corporate Climate Change-Related Governance Practices and Related Disclosures. Aust. Account. Rev. 2010, 20, 317–333. [Google Scholar] [CrossRef] [Green Version]

- Freedman, M.; Jaggi, B. Global Warming Disclosures: Impact of Kyoto Protocol Across Countries: Global Warming Disclosures. J. Int. Financ. Manag. Account. 2011, 22, 46–90. [Google Scholar] [CrossRef]

- Jaggi, B.; Allini, A.; Macchioni, R.; Zagaria, C. The Factors Motivating Voluntary Disclosure of Carbon Information: Evidence Based on Italian Listed Companies. Organ. Environ. 2018, 31, 178–202. [Google Scholar] [CrossRef]

- Yu, J.; Lee, S. The Impact of Greenhouse Gas Emissions on Corporate Social Responsibility in Korea. Sustainability 2017, 9, 1135. [Google Scholar] [CrossRef] [Green Version]

- Huang, Y. Policy Experimentation and the Emergence of Domestic Voluntary Carbon Trading in China. East Asia 2013, 30, 67–89. [Google Scholar] [CrossRef]

- Zeng, H.; Zhou, Z.; Xiao, Y.; Ziqi, D.; Liu, L.; Chen, X. Determinants of Corporate Carbon Efficiency: Evidence from CDP 2011–2014 Questionnaire for Standard & Poor’s 500 Index Companies. Environ. Eng. Manag. J. 2017, 16, 1595–1608. [Google Scholar]

- Doda, B.; Gennaioli, C.; Gouldson, A.; Grover, D.; Sullivan, R. Are Corporate Carbon Management Practices Reducing Corporate Carbon Emissions? Corp. Soc. Responsib. Environ. Manag. 2016, 23, 257–270. [Google Scholar] [CrossRef] [Green Version]

- Sullivan, R. The Management of Greenhouse Gas Emissions in Large European Companies. Corp. Soc. Responsib. Environ. Manag. 2009, 16, 301–309. [Google Scholar] [CrossRef]

- Prado-Lorenzo, J.-M.; Garcia-Sanchez, I.-M. The Role of the Board of Directors in Disseminating Relevant Information on Greenhouse Gases. J. Bus. Ethics 2010, 97, 391–424. [Google Scholar] [CrossRef]

- Luo, L.; Lan, Y.-C.; Tang, Q. Corporate Incentives to Disclose Carbon Information: Evidence from the CDP Global 500 Report. J. Int. Financ. Manag. Account. 2012, 23, 93–120. [Google Scholar] [CrossRef]

- Bae Choi, B.; Lee, D.; Psaros, J. An Analysis of Australian Company Carbon Emission Disclosures. Pac. Account. Rev. 2013, 25, 58–79. [Google Scholar] [CrossRef]

- Depoers, F.; Jeanjean, T.; Jérôme, T. Voluntary Disclosure of Greenhouse Gas Emissions: Contrasting the Carbon Disclosure Project and Corporate Reports. J. Bus. Ethics 2016, 134, 445–461. [Google Scholar] [CrossRef]

- Wegener, M.; Labelle, R.; Jerman, L. Unpacking Carbon Accounting Numbers: A Study of the Commensurability and Comparability of Corporate Greenhouse Gas Emission Disclosures. J. Clean. Prod. 2019, 211, 652–664. [Google Scholar] [CrossRef]

- Olhoff, A.; Christensen, J.M.; Kuramochi, T.; Elzen, M.G.J.D.; Peters, G.; Höhne, N.; Fransen, T.; Hans, F.; Rogelj, J.; Kejun, J.; et al. Emissions Gap Report; United Nations Environment Programme: Nairobi, Kenya, 2019. [Google Scholar] [CrossRef]

- Liu, J.; Diamond, J. China’s Environment in a Globalizing World. Nature 2005, 435, 1179–1186. [Google Scholar] [CrossRef]

- Bagnai, A. The Role of China in Global External Imbalances: Some Further Evidence. China Econ. Rev. 2009, 20, 508–526. [Google Scholar] [CrossRef]

- Zhou, W. Will CSR Work in China? Leading Perspectives, CSR in the People’s Republic of China. Bus. Soc. Responsib. 2006. Available online: https://www.eldis.org/document/A22623 (accessed on 11 September 2019).

- Hou, S.; Fu, W.; Li, X. Achieving Sustainability with A Stakeholder-Based CSR Assessment Model For Fines In China. J. Int. Bus. Ethics 2010, 3, 41. [Google Scholar]

- Hanson, K.O.; Rothlin, S. Taking your codes to China. In Dimensions of Teaching Business Ethics in Asia; Springer: Berlin/Heidelberg, Germany, 2013; pp. 77–89. [Google Scholar]

- Wang, H.; Bernell, D. Environmental Disclosure in China: An Examination of the Green Securities Policy. J. Environ. Dev. 2013, 22, 339–369. [Google Scholar] [CrossRef] [Green Version]

- Mol, A.P.J.; He, G.; Zhang, L. Information Disclosure in Environmental Risk Management: Developments in China. J. Curr. Chin. Aff. 2011, 40, 163–192. [Google Scholar] [CrossRef] [Green Version]

- Tian, Y.; Zhu, Q.; Geng, Y. An Analysis of Energy-Related Greenhouse Gas Emissions in the Chinese Iron and Steel Industry. Energy Policy 2013, 56, 352–361. [Google Scholar] [CrossRef]

- Li, K.; Khalili, N.R.; Cheng, W. Corporate Social Responsibility Practices in China: Trends, Context, and Impact on Company Performance. Sustainability 2019, 11, 354. [Google Scholar] [CrossRef] [Green Version]

- Li, W.; Zhang, R. Corporate Social Responsibility, Ownership Structure, and Political Interference: Evidence from China. J. Bus. Ethics 2010, 96, 631–645. [Google Scholar] [CrossRef]

- Wang, F.; Sun, J.; Liu, Y.S. Institutional Pressure, Ultimate Ownership, and Corporate Carbon Reduction Engagement: Evidence from China. J. Bus. Res. 2019, 104, 14–26. [Google Scholar] [CrossRef]

- Zhou, Z.; Nie, L.; Ji, H.; Zeng, H.; Chen, X. Does a Firm’s Low-Carbon Awareness Promote Low-Carbon Behaviors? Empirical Evidence from China. J. Clean. Prod. 2020, 244, 118903. [Google Scholar] [CrossRef]

- Li, Q.; Luo, W.; Wang, Y.; Wu, L. Firm Performance, Corporate Ownership, and Corporate Social Responsibility Disclosure in China. Bus. Ethics Eur. Rev. 2013, 22, 159–173. [Google Scholar] [CrossRef]

- Lu, Y.; Abeysekera, I. Stakeholders’ Power, Corporate Characteristics, and Social and Environmental Disclosure: Evidence from China. J. Clean. Prod. 2014, 64, 426–436. [Google Scholar] [CrossRef] [Green Version]

- Li, W.; Hu, M. An Overview of the Environmental Finance Policies in China: Retrofitting an Integrated Mechanism for Environmental Management. Front. Environ. Sci. Eng. 2014, 8, 316–328. [Google Scholar] [CrossRef]

- Peng, J.; Sun, J.; Luo, R. Corporate Voluntary Carbon Information Disclosure: Evidence from China’s Listed Companies. World Econ. 2015, 38, 91–109. [Google Scholar] [CrossRef]

- Guan, X.; Zhang, J.; Wu, X.; Cheng, L. The Shadow Prices of Carbon Emissions in China’s Planting Industry. Sustainability 2018, 10, 753. [Google Scholar] [CrossRef] [Green Version]

- He, C.; Wang, J. Energy Intensity in Light of China’s Economic Transition. Eurasian Geogr. Econ. 2007, 48, 439–468. [Google Scholar] [CrossRef]

- Clarke-Sather, A.; Qu, J.; Wang, Q.; Zeng, J.; Li, Y. Carbon Inequality at the Sub-National Scale: A Case Study of Provincial-Level Inequality in CO2 Emissions in China 1997–2007. Energy Policy 2011, 39, 5420–5428. [Google Scholar] [CrossRef]

- Cadez, S.; Czerny, A. Climate Change Mitigation Strategies in Carbon-Intensive Firms. J. Clean. Prod. 2016, 112, 4132–4143. [Google Scholar] [CrossRef]

- Cadez, S.; Czerny, A.; Letmathe, P. Stakeholder Pressures and Corporate Climate Change Mitigation Strategies. Bus. Strategy Environ. 2019, 28, 1–14. [Google Scholar] [CrossRef]

- Galant, A.; Cadez, S. Corporate Social Responsibility and Financial Performance Relationship: A Review of Measurement Approaches. Econ. Res. Ekon. Istraz. 2017, 30, 676–693. [Google Scholar] [CrossRef]

- Cadez, S.; Guilding, C. Examining Distinct Carbon Cost Structures and Climate Change Abatement Strategies in CO2 Polluting Firms. Account. Audit. Account. J. 2017, 30, 1041–1064. [Google Scholar] [CrossRef]

- Du, L. Impact Factors of China’s Carbon Dioxide Emissions: Provincial Panel Data Analysis. South. Econ. 2010, 11, 20–33. [Google Scholar]

- Wang, J.; Song, L.; Yao, S. The Determinants of Corporate Social Responsibility Disclosure: Evidence from China. J. Appl. Bus. Res. JABR 2013, 29, 1833. [Google Scholar] [CrossRef]

- Yu, H.-C.; Kuo, L.; Ma, B. The Drivers of Carbon Disclosure: Evidence from China’s Sustainability Plans. Carbon Manag. 2020, 11, 399–414. [Google Scholar] [CrossRef]

| Variable | Symbol | Measurement |

|---|---|---|

| Dependent variables | ||

| Total CSR disclosure | CSR Total | Total number of CSR projects disclosed by a firm |

| Types of CSR projects disclosed | Shareholder | Number of CSR shareholder protection projects |

| Staff | Number of CSR staff protection projects | |

| Consumer | Number of CSR consumer and supplier protection projects | |

| Environment | Number of CSR environment protection projects | |

| Public | Number of CSR public relations projects | |

| Independent variables | ||

| Global Reporting Initiative | GRI | GRI = 1 if the CSR report followed GRI standard, GRI = 0 otherwise |

| CSR certification | Audit | Audit = 1 if the CSR report was audited, Audit = 0 otherwise |

| CSR mandatory disclosure | Mandate | Mandate = 1 if the firm was required to disclose CSR reports, Mandate = 0 otherwise |

| Firm age | Age | Years since the firm established |

| Firm experience in list | List Exp | Years since the firm became publicly listed |

| Firm experience in CSR disclosure | CSR Exp | Years since the firm started disclosing CSR |

| Firm high education | High Edu | Percentage of firm employees holding graduate level degrees (master’s and PhD’s) |

| Firm mid and high education | Mid Edu | Percentage of firm employees holding undergraduate level degrees and above (bachelor’s, master’s and PhD’s) |

| State ownership | SOE | Percentage of firm’s state-owned shares, divided by total shares |

| Control variables | ||

| Firm size | Size | The natural logarithm of firm’s total asset |

| Firm revenue | Revenue | The firm’s total revenue to total asset ratio |

| Tax paid to the government | Tax | The firm’s total tax paid to total asset ratio |

| Cash paid to employees | Cash | The firm’s total cash paid to employees to total asset ratio |

| Firm net profit margin | Profit | The firm’s total net profit to total revenue ratio |

| Variable | N of Firms | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| CSR Total | 6295 | 5.2353 | 4.9489 | 1 | 39 |

| Shareholder | 6295 | 0.41 | 0.645 | 0 | 7 |

| Staff | 6295 | 2.4221 | 2.933 | 0 | 26 |

| Consumer | 6295 | 0.5252 | 1.2262 | 0 | 16 |

| Environment | 6295 | 1.533 | 2.1629 | 0 | 23 |

| Public | 6295 | 0.345 | 0.7093 | 0 | 9 |

| Age | 6295 | 17.2386 | 5.8892 | 0 | 40 |

| List Exp | 6295 | 12.1617 | 6.7801 | 0 | 29 |

| CSR Exp | 6295 | 3.783 | 3.0468 | 0 | 13 |

| High Edu | 4518 | 0.0603 | 0.1037 | 0.0003 | 4.5194 |

| Mid Edu | 4518 | 0.3906 | 0.282 | 0.0034 | 5.5374 |

| SOE | 6294 | 0.0692 | 0.1611 | 0 | 0.9 |

| GRI | 6295 | 0.2372 | 0.4254 | 0 | 1 |

| Audit | 6295 | 0.0373 | 0.1896 | 0 | 1 |

| Mandate | 6295 | 0.5508 | 0.4975 | 0 | 1 |

| Size | 6295 | 23.426 | 1.8193 | 18.7602 | 31.0359 |

| Revenue | 6295 | 0.6205 | 0.5336 | 0.0044 | 8.601 |

| Tax | 6295 | 0.0384 | 0.0364 | −0.0184 | 0.6196 |

| Cash | 6295 | 0.0591 | 0.0529 | 0 | 1.4208 |

| Profit | 6295 | 0.1065 | 0.2803 | −2.9663 | 12.0805 |

| Variable | Symbol | Measurement |

|---|---|---|

| Dependent variable | ||

| Carbon Emission | CO2 | Natural logarithm of carbon emission in metric ton per 1,000,000 RMB GDP |

| Independent variables | ||

| CSR adoption rate | CSR Adoption | Percentage of CSR companies over all listed firms |

| CSR total effort | CSR Project | Average number of CSR projects disclosed per CSR company |

| CSR environment effort | CSR Environment | Percentage of CSR environment protection over all CSR projects |

| CSR firm size | CSR Size | CSR companies’ total asset to provincial GDP ratio |

| Control variables | ||

| GDP per capita | GDP per capita | The natural logarithm of GDP per capita of provinces |

| Population | Population | The natural logarithm of population of provinces |

| Trade activities | Trade | The total import and export to GDP ratio of provinces |

| Province | Statistics | CO2 | CSR Adoption | CSR Project | CSR Environment | CSR Size | GDP per Capita | Population | Trade |

|---|---|---|---|---|---|---|---|---|---|

| Anhui | Mean | 5.18 | 0.19 | 3.50 | 0.36 | 15.80 | 10.14 | 8.71 | 0.13 |

| N | 12 | 12 | 12 | 12 | 12 | 12 | 12 | 12 | |

| Beijing | Mean | 3.91 | 0.33 | 4.44 | 0.29 | 21.47 | 11.42 | 7.60 | 1.15 |

| N | 11 | 11 | 11 | 11 | 11 | 11 | 11 | 11 | |

| Chongqing | Mean | 4.83 | 0.17 | 3.49 | 0.21 | 16.53 | 10.57 | 7.99 | 0.23 |

| N | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | |

| Fujian | Mean | 4.61 | 0.49 | 2.35 | 0.26 | 17.57 | 10.75 | 8.23 | 0.46 |

| N | 12 | 12 | 12 | 12 | 12 | 12 | 12 | 12 | |

| Gansu | Mean | 5.44 | 0.17 | 2.60 | 0.26 | 15.97 | 10.06 | 7.86 | 0.08 |

| N | 6 | 6 | 6 | 6 | 6 | 6 | 6 | 6 | |

| Guangdong | Mean | 4.31 | 0.19 | 3.83 | 0.25 | 18.39 | 10.87 | 9.26 | 1.04 |

| N | 11 | 11 | 11 | 11 | 11 | 11 | 11 | 11 | |

| Guangxi | Mean | 4.97 | 0.17 | 5.38 | 0.39 | 15.17 | 9.99 | 8.47 | 0.16 |

| N | 11 | 11 | 11 | 11 | 11 | 11 | 11 | 11 | |

| Guizhou | Mean | 5.69 | 0.28 | 3.70 | 0.13 | 16.44 | 10.06 | 8.16 | 0.06 |

| N | 8 | 8 | 8 | 8 | 8 | 8 | 8 | 8 | |

| Hainan | Mean | 4.79 | 0.17 | 3.36 | 0.28 | 16.35 | 10.25 | 6.79 | 0.25 |

| N | 11 | 11 | 11 | 11 | 11 | 11 | 11 | 11 | |

| Hebei | Mean | 5.85 | 0.18 | 4.61 | 0.36 | 16.38 | 10.25 | 8.89 | 0.14 |

| N | 11 | 11 | 11 | 11 | 11 | 11 | 11 | 11 | |

| Heilongjiang | Mean | 5.49 | 0.19 | 1.43 | 0.33 | 15.65 | 10.27 | 8.25 | 0.18 |

| N | 8 | 8 | 8 | 8 | 8 | 8 | 8 | 8 | |

| Henan | Mean | 5.19 | 0.39 | 3.22 | 0.37 | 15.80 | 10.33 | 9.15 | 0.10 |

| N | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | |

| Hubei | Mean | 4.93 | 0.16 | 3.95 | 0.32 | 15.89 | 10.48 | 8.66 | 0.10 |

| N | 11 | 11 | 11 | 11 | 11 | 11 | 11 | 11 | |

| Hunan | Mean | 4.86 | 0.14 | 2.81 | 0.27 | 15.91 | 10.29 | 8.80 | 0.07 |

| N | 11 | 11 | 11 | 11 | 11 | 11 | 11 | 11 | |

| Inner Mongolia | Mean | 6.38 | 0.16 | 3.58 | 0.49 | 15.57 | 10.68 | 7.82 | 0.07 |

| N | 9 | 9 | 9 | 9 | 9 | 9 | 9 | 9 | |

| Jiangsu | Mean | 4.69 | 0.14 | 3.33 | 0.27 | 16.35 | 11.13 | 8.98 | 0.61 |

| N | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | |

| Jiangxi | Mean | 4.76 | 0.25 | 3.51 | 0.24 | 16.24 | 10.37 | 8.42 | 0.16 |

| N | 8 | 8 | 8 | 8 | 8 | 8 | 8 | 8 | |

| Jilin | Mean | 5.59 | 0.20 | 3.12 | 0.37 | 16.57 | 10.18 | 7.92 | 0.16 |

| N | 11 | 11 | 11 | 11 | 11 | 11 | 11 | 11 | |

| Liaoning | Mean | 5.56 | 0.21 | 2.94 | 0.31 | 17.02 | 10.58 | 8.38 | 0.35 |

| N | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | |

| Ningxia | Mean | 6.56 | 0.25 | 4.29 | 0.30 | 15.38 | 10.28 | 6.47 | 0.09 |

| N | 11 | 11 | 11 | 11 | 11 | 11 | 11 | 11 | |

| Qinghai | Mean | 5.64 | 0.36 | 3.88 | 0.38 | 17.57 | 10.24 | 6.36 | 0.05 |

| N | 9 | 9 | 9 | 9 | 9 | 9 | 9 | 9 | |

| Shaanxi | Mean | 5.48 | 0.15 | 3.58 | 0.20 | 15.12 | 10.33 | 8.23 | 0.09 |

| N | 12 | 12 | 12 | 12 | 12 | 12 | 12 | 12 | |

| Shandong | Mean | 5.31 | 0.20 | 3.82 | 0.44 | 16.45 | 10.70 | 9.18 | 0.34 |

| N | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | |

| Shanghai | Mean | 4.40 | 0.28 | 5.47 | 0.24 | 20.05 | 11.49 | 7.77 | 1.18 |

| N | 9 | 9 | 9 | 9 | 9 | 9 | 9 | 9 | |

| Shanxi | Mean | 6.44 | 0.32 | 9.00 | 0.35 | 17.05 | 10.29 | 8.19 | 0.09 |

| N | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | |

| Sichuan | Mean | 4.94 | 0.16 | 4.14 | 0.32 | 16.17 | 10.17 | 9.01 | 0.13 |

| N | 11 | 11 | 11 | 11 | 11 | 11 | 11 | 11 | |

| Tianjin | Mean | 5.01 | 0.34 | 4.25 | 0.21 | 17.06 | 11.03 | 7.25 | 0.77 |

| N | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | |

| Xinjiang | Mean | 5.92 | 0.23 | 3.76 | 0.31 | 17.10 | 10.36 | 7.73 | 0.20 |

| N | 10 | 10 | 10 | 10 | 10 | 10 | 10 | 10 | |

| Yunnan | Mean | 5.35 | 0.35 | 6.30 | 0.34 | 16.35 | 9.93 | 8.44 | 0.11 |

| N | 12 | 12 | 12 | 12 | 12 | 12 | 12 | 12 | |

| Zhejiang | Mean | 4.56 | 0.17 | 2.67 | 0.37 | 16.54 | 11.00 | 8.60 | 0.57 |

| N | 11 | 11 | 11 | 11 | 11 | 11 | 11 | 11 | |

| National | Mean | 5.21 | 0.23 | 3.91 | 0.31 | 16.67 | 10.49 | 8.20 | 0.31 |

| N | 306 | 306 | 306 | 306 | 306 | 306 | 306 | 306 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Dependent Variable | CSR Total | Shareholder | Employee | Consumer | Environment | Public |

| F1 | −22.171 * | −0.431 | −16.237 ** | −1.675 | −2.673 | −1.155 |

| (−1.723) | (−0.263) | (−2.332) | (−0.659) | (−0.485) | (−0.577) | |

| F2 | 0.753 * | 0.023 | 0.363 | 0.061 | 0.233 | 0.072 |

| (1.911) | (0.400) | (1.617) | (0.471) | (1.606) | (0.791) | |

| F3 | −4.264 | 0.065 | −3.245 * | −0.628 | −0.314 | −0.142 |

| (−1.303) | (0.143) | (−1.726) | (−0.941) | (−0.201) | (−0.349) | |

| F4 | −7.579 | −0.677 | −4.755 | 0.388 | −1.919 | −0.617 |

| (−1.166) | (−0.734) | (−1.158) | (0.219) | (−0.695) | (−0.410) | |

| Size | 0.192 | 0.000 | −0.033 | −0.042 | 0.269 ** | −0.003 |

| (0.773) | (0.007) | (−0.214) | (−0.675) | (2.182) | (−0.079) | |

| Revenue | −0.544 | −0.038 | −0.317 | −0.004 | −0.138 | −0.048 |

| (−1.417) | (−0.567) | (−1.160) | (−0.057) | (−0.896) | (−0.953) | |

| Tax | 22.277 *** | 0.463 | 9.655 *** | 1.333 | 9.629 *** | 1.198 |

| (4.424) | (0.750) | (2.866) | (1.284) | (4.243) | (1.422) | |

| Cash | 0.512 | −0.012 | −1.057 | −0.156 | 1.125 | 0.613 |

| (0.160) | (−0.025) | (−0.404) | (−0.162) | (1.081) | (0.955) | |

| Profit | −0.100 | −0.003 | −0.026 | −0.021 | −0.030 | −0.020 |

| (−0.986) | (−0.214) | (−0.395) | (−0.665) | (−0.808) | (−0.769) | |

| Constant | −86.544 * | −2.518 | −57.126 ** | −3.823 | −18.248 | −4.830 |

| (−1.838) | (−0.425) | (−2.231) | (−0.397) | (−0.934) | (−0.592) | |

| Firm fixed effect | yes | yes | yes | yes | yes | yes |

| Year fixed effect | yes | yes | yes | yes | yes | yes |

| N | 4517 | 4517 | 4517 | 4517 | 4517 | 4517 |

| Within Model R2 | 0.035 | 0.015 | 0.026 | 0.014 | 0.031 | 0.027 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Dependent Variable | CSR Total | Shareholder | Employee | Consumer | Environment | Public |

| GRI | 1.888 *** | 0.121 *** | 0.930 *** | 0.132 | 0.576 *** | 0.130 *** |

| (5.663) | (3.050) | (4.272) | (1.554) | (4.630) | (3.239) | |

| Audit | 1.301 * | 0.085 | 0.797 ** | 0.070 | 0.423 | −0.075 |

| (1.669) | (1.022) | (2.094) | (0.280) | (1.600) | (−0.542) | |

| Mandate | 0.295 | −0.011 | 0.162 | 0.049 | 0.095 | 0.000 |

| (1.279) | (−0.300) | (1.098) | (0.994) | (0.876) | (0.008) | |

| Size | 0.292 | 0.012 | −0.011 | −0.022 | 0.273 ** | 0.041 |

| (1.226) | (0.357) | (−0.079) | (−0.454) | (2.436) | (1.432) | |

| Revenue | −0.379 | −0.015 | −0.195 | 0.050 | −0.223 | 0.003 |

| (−1.151) | (−0.307) | (−0.977) | (0.899) | (−1.380) | (0.092) | |

| Tax | 16.724 *** | −0.022 | 6.268 ** | 1.518 * | 8.063 *** | 0.897 |

| (3.869) | (−0.044) | (2.123) | (1.669) | (4.579) | (1.416) | |

| Cash | 1.540 | 0.094 | 0.232 | −0.761 | 1.019 | 0.956 |

| (0.600) | (0.243) | (0.127) | (−0.905) | (0.926) | (1.223) | |

| Profit | 0.012 | −0.010 | 0.022 | 0.007 | 0.001 | −0.007 |

| (0.118) | (−0.501) | (0.274) | (0.242) | (0.015) | (−0.326) | |

| Constant | −4.502 | −0.131 | 1.921 | 0.735 | −6.171 ** | −0.856 |

| (−0.841) | (−0.185) | (0.627) | (0.666) | (−2.412) | (−1.295) | |

| Firm fixed effect | yes | yes | yes | yes | yes | yes |

| Year fixed effect | yes | yes | yes | yes | yes | yes |

| N | 6295 | 6295 | 6295 | 6295 | 6295 | 6295 |

| Within Model R2 | 0.056 | 0.021 | 0.036 | 0.010 | 0.037 | 0.026 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | |

|---|---|---|---|---|---|---|---|

| Region | All | North | Northeast | East | South-Central | Southwest | Northwest |

| CSR Adoption | −0.526 *** | −0.245 | 0.421 | 0.152 | −0.047 | −0.927 ** | −0.704 ** |

| (−4.308) | (−0.696) | (1.021) | (1.198) | (−0.228) | (−2.397) | (−2.066) | |

| CSR Project | −0.002 | 0.005 | −0.006 | −0.006 | 0.021 *** | −0.010 | 0.005 |

| (−0.494) | (0.383) | (−0.473) | (−0.696) | (3.035) | (−0.615) | (0.473) | |

| CSR Environment | 0.067 | 0.006 | −0.037 | 0.019 | −0.001 | −0.122 | 0.006 |

| (1.417) | (0.035) | (−0.442) | (0.237) | (−0.007) | (−0.804) | (0.051) | |

| CSR Size | 0.007 | 0.009 | −0.009 | 0.001 | 0.018 | 0.045 | 0.036 |

| (0.647) | (0.308) | (−0.403) | (0.067) | (0.608) | (0.974) | (1.158) | |

| GDP per capita | −0.674 *** | −0.965 * | −1.268 ** | −0.780 *** | −0.468 * | −0.057 | −0.095 |

| (−6.860) | (−1.949) | (−3.220) | (−4.097) | (−1.960) | (−0.177) | (−0.191) | |

| Population | −0.465 | −1.524 ** | −4.501 | −3.079 *** | 0.655 | 2.823 | 3.503 ** |

| (−1.528) | (−2.617) | (−0.713) | (−3.694) | (0.895) | (1.242) | (2.477) | |

| Trade | 0.137 | 0.185 | −1.102 | 0.285 ** | 0.096 | −0.567 | −0.547 |

| (1.552) | (1.267) | (−1.274) | (2.378) | (0.622) | (−1.449) | (−0.946) | |

| Constant | 15.862 *** | 27.474 *** | 55.317 | 39.159 *** | 3.774 | −17.805 | −18.889 |

| (5.287) | (3.180) | (1.012) | (4.573) | (0.521) | (−0.934) | (−1.416) | |

| Province fixed effect | yes | yes | yes | yes | yes | yes | yes |

| Year fixed effect | yes | yes | yes | yes | yes | yes | yes |

| N | 306 | 51 | 29 | 72 | 65 | 41 | 48 |

| Within Model R2 | 0.868 | 0.944 | 0.995 | 0.978 | 0.966 | 0.990 | 0.832 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Li, S.; Cheng, W.; Li, J.; Shen, H. Corporate Social Responsibility Development and Climate Change: Regional Evidence of China. Sustainability 2021, 13, 11859. https://doi.org/10.3390/su132111859

Li S, Cheng W, Li J, Shen H. Corporate Social Responsibility Development and Climate Change: Regional Evidence of China. Sustainability. 2021; 13(21):11859. https://doi.org/10.3390/su132111859

Chicago/Turabian StyleLi, Shouhao, Weiquan Cheng, Jingjing Li, and Hao Shen. 2021. "Corporate Social Responsibility Development and Climate Change: Regional Evidence of China" Sustainability 13, no. 21: 11859. https://doi.org/10.3390/su132111859

APA StyleLi, S., Cheng, W., Li, J., & Shen, H. (2021). Corporate Social Responsibility Development and Climate Change: Regional Evidence of China. Sustainability, 13(21), 11859. https://doi.org/10.3390/su132111859