Can Green Finance Development Reduce Carbon Emissions? Empirical Evidence from 30 Chinese Provinces

Abstract

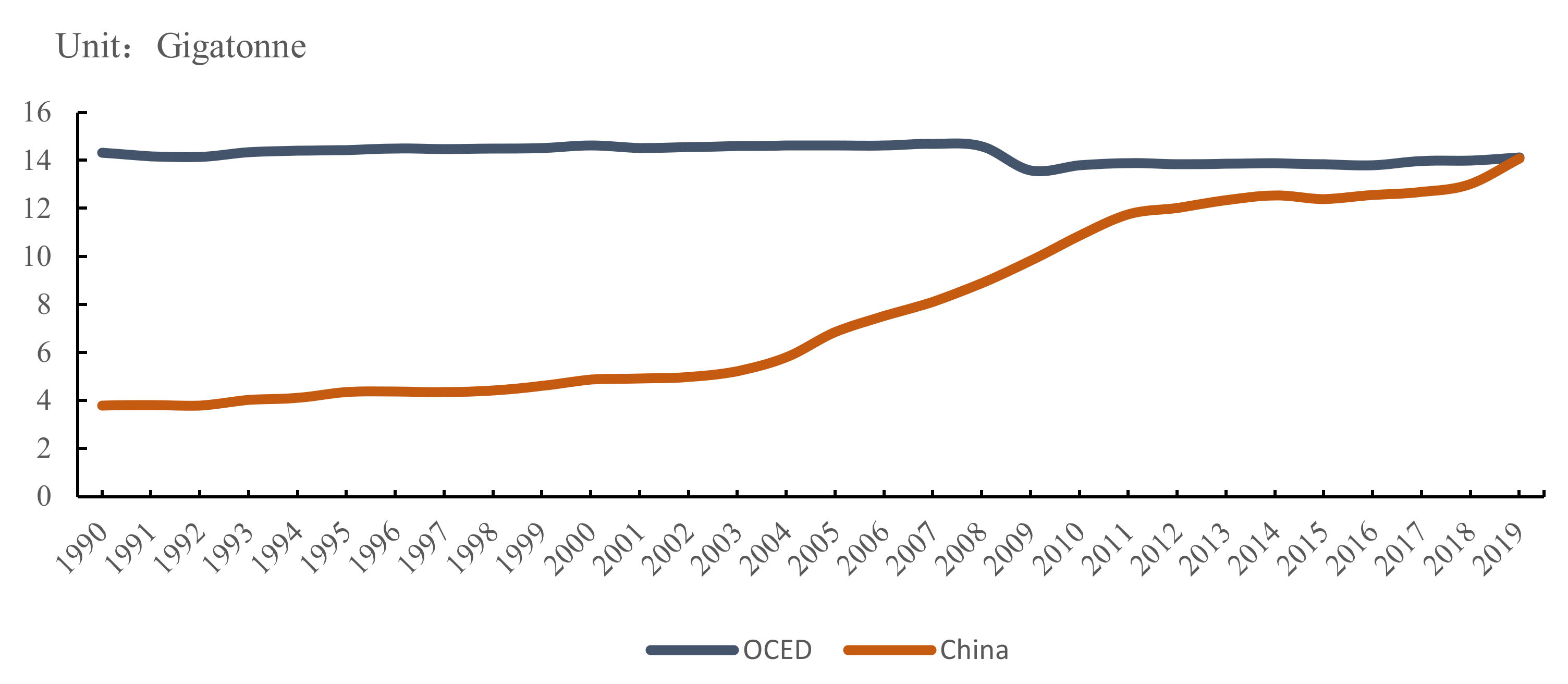

:1. Introduction

2. Literature Review

2.1. Financial Development and Carbon Emission

2.2. Green Financial Development and Carbon Emission

2.3. Summary

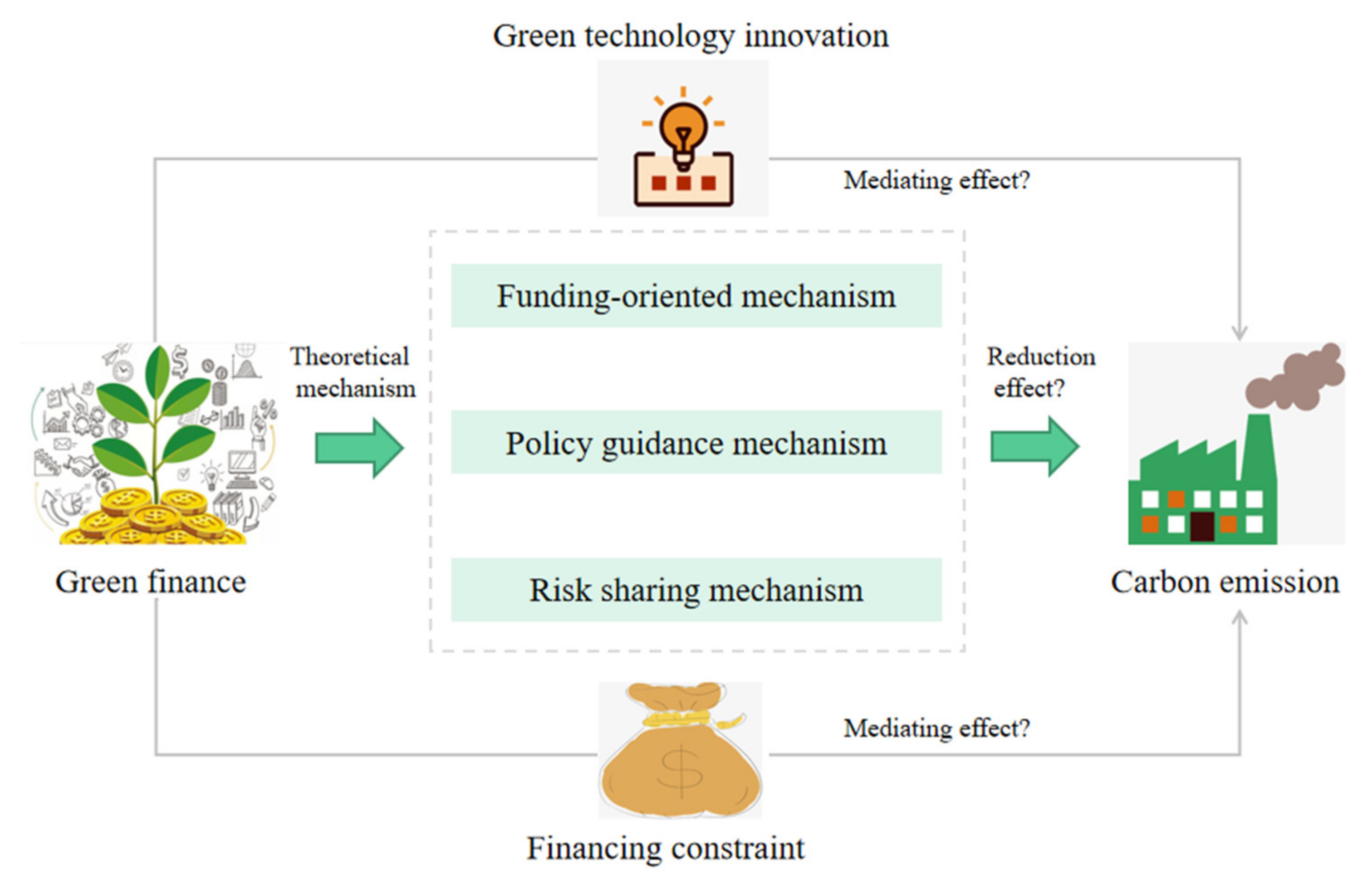

3. Theoretical Hypotheses

4. Empirical Model and Data Explanation

4.1. Spatial Econometric Model

4.2. Description of Variables

4.2.1. Explained Variable: Carbon Emission (C)

4.2.2. Core Explanatory Variable: Green Finance Development (GFin)

4.2.3. Control Variables

4.2.4. Mediating Variable

4.3. Data Source

5. Empirical Regression

5.1. Impact of Green Finance Development on Carbon Emission

5.1.1. Selection of Spatial Econometric Model

5.1.2. Benchmark Regression Test

5.1.3. Robustness Test

5.1.4. Spatial Spillover Effect

5.2. Analysis on the Intermediary Effect of Green Finance on Carbon Emission

6. Conclusions, Suggestions, and Discussion

6.1. Conclusions

6.2. Suggestions

6.3. Discussion

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Daniel, G.A.; Herman, D.J. Optimism or pessimism? A composite view on English living standards during the Industrial Revolution. Eur. Rev. Econ. Hist. 2021, 25, 1–19. [Google Scholar]

- Gennaioli, N.; Shleifer, A.; Vishny, R. Neglected risks, financial innovation, and financial fragility. J. Financ. Econ. 2012, 104, 452–468. [Google Scholar] [CrossRef] [Green Version]

- Dikau, S.; Volz, U. Central bank mandates, sustainability objectives and the promotion of green finance. Ecol. Econ. 2021, 184, 10–70. [Google Scholar] [CrossRef]

- Andrew, M.; Mary, A.S.; Emily, T.; Williams, A.P. Barriers and opportunities facing the UK Peatland Code: A case-study of blended green finance. Land Use Policy 2021, 108, 105594. [Google Scholar]

- Freebairn, J. Policy Forum: Designing a Carbon Price Policy: Reducing Greenhouse Gas Emissions at the Lowest Cost. Aust. Econ. Rev. 2012, 45, 96–104. [Google Scholar] [CrossRef]

- Gu, B.; Chen, F.; Zhang, K. The policy effect of green finance in promoting industrial transformation and upgrading efficiency in China: Analysis from the perspective of government regulation and public environmental demands. Environ. Sci. Pollut. Res. 2021, 28, 1–18. [Google Scholar] [CrossRef] [PubMed]

- Peng, H.; Jiang, R.; Zhou, C. Literature Review of the Study of Carbon Emission Rights. Low Carbon Econ. 2017, 8, 133–138. [Google Scholar] [CrossRef] [Green Version]

- Liu, L.C.; Gang, W. Relating five bounded environmental problems to China’s household consumption in 2011–2015. Energy 2013, 57, 427–433. [Google Scholar] [CrossRef]

- Chen, T.; Gozgor, G.; Koo, C.K. Does international cooperation affect CO2 emissions? Evidence from OECD countries. Environ. Sci. Pollut. Res. 2020, 27, 8548–8556. [Google Scholar] [CrossRef]

- Jung, H.; Song, S.; Song, C.K. Carbon Emission Regulation, Green Boards, and Corporate Environmental Responsibility. Sustainability 2021, 13, 4463. [Google Scholar] [CrossRef]

- Sbia, R.; Shahbaz, M.; Hamdi, H. A contribution of foreign direct investment, clean energy, trade openness, carbon emissions and economic growth to energy demand in UAE. Econ. Model. 2014, 36, 191–197. [Google Scholar] [CrossRef] [Green Version]

- Yu, X.; Wu, Z.; Wang, Q. Exploring the investment strategy of power enterprises under the nationwide carbon emissions trading mechanism: A scenario-based system dynamics approach. Energy Policy 2020, 140, 111409. [Google Scholar] [CrossRef]

- Schmidt, T.S. Low-carbon investment risks and de-risking. Nat. Clim. Chang. 2014, 4, 237–239. [Google Scholar] [CrossRef]

- Li, W.; Zhang, P. Relationship and integrated development of low-carbon economy, food safety, and agricultural mechanization. Environ. Sci. Pollut. Res. 2021, 17, 1–11. [Google Scholar]

- Wang, A.; Tong, Z.; Du, W. Comprehensive Evaluation of Green Development in Dongliao River Basin from the Integration System of “Multi-Dimensions”. Sustainability 2021, 13, 4785. [Google Scholar] [CrossRef]

- Ke, H.; Dai, S.; Yu, H. Spatial effect of innovation efficiency on ecological footprint: City-level empirical evidence from China. Environ. Technol. Innov. 2021, 22, 101536. [Google Scholar] [CrossRef]

- Sadorsky, P. The Impact of Financial Development on Energy Consumption in Economies. Energy Policy 2010, 38, 2528–2535. [Google Scholar] [CrossRef]

- Shahbaz, M.; Solarin, S.A.; Mahmood, H. Does Financial Development Reduce CO2 Emissions in Malaysian Economy? A Time Series Analysis. Econ. Model. 2013, 35, 145–152. [Google Scholar] [CrossRef] [Green Version]

- Tamazian, A.; Chousa, J.P.; Vadlamannati, K.C. Does higher economic and financial development lead to environment degradation? evidence from BRIC countries. Energy Policy 2009, 37, 246–253. [Google Scholar] [CrossRef]

- Jalil, A.; Feridun, M. The impact of growth, energy and financial development on the environment in China: A cointegrationanalysis. Energy Econ. 2011, 33, 284–291. [Google Scholar] [CrossRef]

- Gu, H.M.; He, B. Research on China’s provincial financial development and carbon emissions. China Popul. Resour. Environ. 2012, 22, 22–27. [Google Scholar]

- Li, W.; Hu, M. An overview of the environmental finance policies in China: Retrofitting an integrated mechanism for environmental management. Front. Environ. Sci. Eng. 2014, 8, 316–328. [Google Scholar] [CrossRef]

- Aizawa, M.; Yang, C. Green credit, green stimulus, green revolution? China’s mobilization of banks for environmental cleanup. J. Environ. Dev. 2010, 19, 119–144. [Google Scholar] [CrossRef]

- Xiu, J.; Liu, H.Y.; Zang, X.Q. The industrial growth and prediction under the background of green credit and energy savingand emission reduction. Model Econ. Sci. 2015, 37, 55–62. [Google Scholar]

- Liu, J.-Y.; Xia, Y.; Fan, Y.; Lin, S.M.; Wu, J. Assessment of a green credit policy aimed at energy-intensive industries in China based on a financial CGE model. J. Clean. Prod. 2017, 163, 293–302. [Google Scholar] [CrossRef]

- Taghizadeh-Hesary, F.; Yoshino, N.; Han, P. Analyzing the Characteristics of Green Bond Markets to Facilitate Green Finance in the Post-COVID-19 World. Sustainability 2021, 13, 5719. [Google Scholar] [CrossRef]

- Huang, H.; Zhang, J. Research on the Environmental Effect of Green Finance Policy Based on the Analysis of Pilot Zones for Green Finance Reform and Innovations. Sustainability 2021, 13, 3754. [Google Scholar] [CrossRef]

- Iqbal, S.; Taghizadeh-Hesary, F.; Mohsin, M. Assessing the Role of the Green Finance Index in Environmental Pollution Reduction. Stud. Appl. Econ. 2021, 39. [Google Scholar] [CrossRef]

- Eyraud, L.; Clements, B.; Wane, A. Green investment: Trends and determinants. Energy Policy 2013, 60, 852–865. [Google Scholar] [CrossRef]

- Liu, Z.; Zhang, X.; Yang, L. Access to Digital Financial Services and Green Technology Advances: Regional Evidence from China. Sustainability 2021, 13, 4927. [Google Scholar] [CrossRef]

- Zhou, P.; Ang, B.W.; Han, J.Y. Total factor carbon emission performance: A Malmquist index analysis. Energy Econ. 2010, 32, 194–201. [Google Scholar] [CrossRef]

- Liu, N.; Liu, C.; Xia, Y.; Ren, Y.; Liang, J. Examining the Coordination Between Green Finance and Green Economy Aiming for Sustainable Development: A Case Study of China. Sustainability 2020, 12, 3717. [Google Scholar] [CrossRef]

- Eichholtz, P.; Quigley, J.M. Green building finance and investments: Practice, policy and research. Eur. Econ. Rev. 2012, 56, 903–904. [Google Scholar] [CrossRef]

- Wang, Y.; Zhi, Q. The Role of Green Finance in Environmental Protection: Two Aspects of Market Mechanism and Policies. Energy Procedia 2016, 104, 311–316. [Google Scholar] [CrossRef]

- Liang, G.; Yu, D.; Ke, L. An Empirical Study on Dynamic Evolution of Industrial Structure and Green Economic Growth—Based on Data from China’s Underdeveloped Areas. Sustainability 2021, 13, 8154. [Google Scholar] [CrossRef]

- Xra, B.; Qspd, B.; Rza, B. Nexus between green finance, non-fossil energy use, and carbon intensity: Empirical evidence from China based on a vector error correction model. J. Clean. Prod. 2020, 277, 122844. [Google Scholar]

- Hu, Y.; Jiang, H.; Zhong, Z. Impact of green credit on industrial structure in China: Theoretical mechanism and empirical analysis. Environ. Sci. Pollut. Res. 2020, 27, 1–14. [Google Scholar] [CrossRef]

- Tu, C.A.; Sarker, T.; Rasoulinezhad, E. Factors Influencing the Green Bond Market Expansion: Evidence from a Multi-Dimensional Analysis. J. Risk Financ. Manag. 2020, 13, 1–14. [Google Scholar]

- Chakraborty, D.; Mukherjee, S. How do trade and investment flows affect environmental sustainability? Evidence from panel data. Environ. Dev. 2013, 6, 34–47. [Google Scholar] [CrossRef]

- Mao, W.; Wang, W.; Sun, H. Driving patterns of industrial green transformation: A multiple regions case learning from China. Sci. Total Environ. 2019, 697, 1341–1367. [Google Scholar] [CrossRef]

- Qin, J.; Zhao, Y.; Xia, L. Carbon Emission Reduction with Capital Constraint under Greening Financing and Cost Sharing Contract. Int. J. Environ. Res. Public Health 2018, 15, 750. [Google Scholar] [CrossRef] [Green Version]

- Anselin, L. Some robust approaches to testing and estimation in spatial econometrics. Reg. Sci. Urban Econ. 1990, 20, 141–163. [Google Scholar] [CrossRef]

- LeSage, J.; James, P. What Regional Scientists Need to Know about Spatial Econometrics. Rev. Reg. Stud. 2014, 26, 56–87. [Google Scholar] [CrossRef]

- Elhorst, J.P. Software for spatial panels. Int. Reg. Sci. Rev. 2014, 37, 389–405. [Google Scholar] [CrossRef] [Green Version]

- Shao, S.; Yang, L.L.; Yu, M.B.; Yu, M.L. Estimation, Characteristics and Determinants of Energy-related Industrial CO2 Emissions in Shanghai (China) 1994–2009. Energy Policy 2011, 39, 6476–6494. [Google Scholar] [CrossRef]

- The Intergovernmental Panel on Climate Change (IPCC). 2006 IPCC Guidelines for National Greenhouse Gas Inventories; Institute for Global Environmental Strategies (IGES): Hayama, Kanagawa, Japan, 2006. [Google Scholar]

- Tu, C.A.; Rasoulinezhad, E.; Sarker, T. Investigating Solutions for the Development of a Green Bond Market: Evidence from Analytic Hierarchy Process. Financ. Res. Lett. 2020, 34, 101457. [Google Scholar] [CrossRef]

- Mashud, A.H.M.; Roy, D.; Daryanto, Y.; Chakraborty, R.; Tseng, M.L. A controllable carbon emission and deterioration inventory model with advance payments scheme. J. Clean. Prod. 2021, 296, 126608. [Google Scholar] [CrossRef]

- Mishra, U.; Mashud, A.; Tseng, M.L.; Wu, J.Z. Optimizing a Sustainable Supply Chain Inventory Model for Controllable Deterioration and Emission Rates in a Greenhouse Farm. Mathematics 2021, 9, 495. [Google Scholar] [CrossRef]

- Li, L.; Wu, W.; Zhang, M. Linkage Analysis Between Finance and Environmental Protection Sectors in China: An Approach to Evaluating Green Finance. Int. J. Environ. Res. Public Health 2021, 18, 2634. [Google Scholar] [CrossRef]

- Mashud, A.H.M.; Pervin, M.; Mishra, U.; Daryanto, Y.; Tseng, M.L.; Lim, M.K. A sustainable inventory model with controllable carbon emissions for green-warehouse farms. J. Clean. Prod. 2021, 298, 126777. [Google Scholar] [CrossRef]

- Rodriguez, M.C.; Dupont-Courtade, L.; Oueslat, W. Air Pollution and Urban Structure Linkage Evidence from European Cities. Renew. Sustain. Energy Rev. 2016, 53, 1–9. [Google Scholar] [CrossRef]

- Shen, N.; Wang, Q.W.; Zhao, Z.Y. Trade linkages, spatial agglomeration and carbon emissions. Manag. World 2014, 1, 22–34. [Google Scholar]

- Ding, W.; Gilli, M.; Mazzanti, M.; Nicolli, F. Green inventions and greenhouse gas emission dynamics: A close examination of provincial Italian data. Environ. Econ. Policy Stud. 2016, 18, 1–17. [Google Scholar]

- Beck, T.; Levine, R.; Loayza, N. Finance and the sources of growth. J. Financ. Econ. 2004, 58, 261–300. [Google Scholar] [CrossRef] [Green Version]

- Ke, H.; Dai, S.; Yu, H. Effect of green innovation efficiency on ecological footprint in 283 Chinese Cities from 2008 to 2018. Environ. Dev. Sustain. 2021, 1–20. [Google Scholar] [CrossRef]

- Chen, X.; Chen, Z. Can China’s Environmental Regulations Effectively Reduce Pollution Emissions? Int. J. Environ. Res. Public Health 2021, 18, 4658. [Google Scholar] [CrossRef]

- LeSage, J.; Pace, R.K. Introduction to Spatial Econometrics; CRC Press: New York, NY, USA, 2009. [Google Scholar]

- Baron, R.M.; Kenny, D.A. The Moderator-mediator Variable Distinction in Social Psychological Research: Conceptual, Strategic, and Statistical Considerations. J. Personal. Soc. Psychol. 1986, 51, 1173–1182. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Index | Index Description | |

|---|---|---|

| Green credit | Proportion of interest expense of high-energy consumption industry | Interest expense of six high-energy consuming industries/total industrial interest expense |

| Green securities | Proportion of market value of environmental protection enterprises | Market value of environmental protection enterprises/total market value of listed companies |

| Green investment | Proportion of investment in environmental pollution control in GDP | Investment in environmental pollution control/GDP |

| Green insurance | Proportion of agricultural insurance scale | Agricultural insurance expenditure/total insurance expenditure |

| Agricultural insurance loss ratio | Agricultural insurance expenditure/agricultural insurance income |

| Variable | Index Selection | Sign | Description | Data Source |

|---|---|---|---|---|

| Dependent variable | Carbon emission | C | Calculated based on Formula (1) | China Energy Statistics Yearbook (2006–2019) China Financial Statistics Yearbook (2006–2019) |

| Core independent variable | Green finance | Gfin | The index system is constructed from the four dimensions of green credit, green insurance, green investment and green securities, and the weight is given by the entropy method | China Statistical Yearbook (2006–2019) China Insurance Statistical Yearbook (2006–2019) Wind database CSMAR database Flush Ifind database |

| Control variable | Economic development | Pgdp | Per-capita GDP | China Energy Statistics Yearbook (2006–2019) China Statistical Yearbook (2006–2019) |

| Energy resource structure | Estru | Proportion of coal consumption in energy consumption | ||

| Openness | Open | Total import and export/GDP | ||

| Industrial structure | Instu | Industrial added value/GDP | ||

| Urbanization | City | Urban population/total population | ||

| Mediating variable | Financing constraints | Fcon | Calculated by cash flow sensitivity model | Wind database |

| Green technology innovation | Gtech | Number of green patent applications | Wind database |

| Model | Static Spatial Model | Dynamic Spatial Model | ||

|---|---|---|---|---|

| W | W1 | W2 | W1 | W2 |

| LR-lag | 132.78 *** | 135.40 *** | 110.59 *** | 112.49 *** |

| LR-error | 101.35 *** | 98.56 *** | 82.23 *** | 78.90 *** |

| LM-lag | 167.87 *** | 168.45 *** | 231.25 *** | 227.82 *** |

| LM-error | 186.12 *** | 194.62 *** | 276.77 *** | 287.90 *** |

| Variable | OLS | GMM | Static SDM | Dynamic SDM |

|---|---|---|---|---|

| M1 | M2 | M3 | M4 | |

| L.C | 0.7456 *** (12.59) | 0.5591 *** (13.60) | ||

| Gfin | −1.3757 * (−1.70) | −1.0190 ** (2.02) | −1.7991 ** (−1.98) | −0.9857 *** (−3.05) |

| Pgdp | 0.4232 (1.10) | 0.0421 ** (2.13) | 1.1007 *** (2.83) | 0.2503 *** (5.66) |

| sPgdp | −0.0512 *** (−2.62) | −0.0142 * (−1.93) | −0.06975 *** (−3.43) | −0.0160 *** (−3.82) |

| Estru | 0.1539 ** (2.68) | 0.3405 * (1.65) | 0.1001 ** (2.23) | 0.0490 *** (6.30) |

| Indu | 0.0527 (0.85) | 0.0663 ** (2.21) | 0.0337 (0.43) | 0.0369 ** (2.02) |

| Open | −0.0617 ** (−2.23) | −0.0563 * (−1.82) | −0.0094 (−0.39) | −0.0404 ** (−2.25) |

| City | 0.0784 (1.28) | 0.0238 (1.48) | 0.1384 * (1.84) | 0.0813 *** (4.63) |

| Log | 389.8303 | 834.7580 | ||

| Rho | 0.8819 *** (3.88) | 0.7625 *** (3.49) | ||

| R2 | 0.8527 | 0.8902 | 0.6103 | 0.9407 |

| AR(2) [P] | 2.0232 (0.3341) | |||

| Sargan [P] | 156.38 (0.9331) | |||

| Obs | 420 | 390 | 420 | 420 |

| Variable | Replace Weight | Replace Index | Replace Model |

|---|---|---|---|

| L.C | 0.5449 *** (13.31) | 0.8403 *** (14.58) | 1.0434 *** (6.38) |

| Gfin | −0.4912 * (−1.83) | −0.2776 *** (−2.95) | −1.0453 *** (−5.61) |

| Pgdp | 0.7351 ** (2.09) | 0.3342 * (1.69) | 0.5430 *** (4.07) |

| sPgdp | −0.0292 ** (−1.69) | −0.0850 *** (−7.98) | −0.0057 ** (−2.26) |

| Estru | 0.0475 *** (2.91) | 0.2245 *** (5.84) | 0.0308 * (1.80) |

| Indu | 0.0617 ** (1.99) | 0.0127 *** (4.07) | 0.0023 * (1.72) |

| Open | −0.0938 *** (−4.35) | 0.0077 *** (3.70) | 0.0053 ** (2.36) |

| City | 0.1267 *** (2.06) | 0.0075 * (1.83) | 0.0036 *** (6.09) |

| Log | 177.7073 | 889.9060 | 1867.2806 |

| Global Moran’s I [P] | 0.1034 *** (0.000) | ||

| Rho | 0.1890 *** (2.61) | 0.7002 *** (6.90) | |

| R2 | 0.9462 | 0.9506 | 0.8052 |

| Obs | 420 | 420 | 420 |

| Variable | Direct Effect | Indirect Effect | Total Effect | |||

|---|---|---|---|---|---|---|

| W1 | W2 | W1 | W2 | W1 | W2 | |

| Gfin | −0.9857 *** (−3.05) | −0.4912 * (−1.83) | −0.0436 * (−1.89) | −0.0042 ** (−1.97) | −1.0293 ** (−2.01) | −0.4954 ** (−2.12) |

| Pgdp | 0.2503 *** (5.66) | 0.7351 ** (2.09) | 0.0158 ** (2.02) | 0.0075 ** (2.32) | 0.2261 * (1.79) | −07426 *** (−4.70) |

| sPgdp | −0.0160 *** (−3.82) | −0.0292 ** (−1.69) | 0.0139 * (1.89) | 0.0280 * (1.69) | −0.0021 * (−1.68) | −0.0012 (1.57) |

| Estru | 0.0490 *** (6.30) | 0.0475 *** (2.91) | 0.0139 (0.73) | 0.0528 (1.01) | 0.1880 (0.76) | 0.1003 *** (4.48) |

| Indu | 0.0369 ** (2.02) | 0.0617 ** (1.99) | 0.0560 * (1.69) | 0.1827 (1.01) | 0.0929 * (1.71) | 0.2444 *** (8.04) |

| Open | −0.0404 ** (−2.25) | −0.0938 *** (−4.35) | 0.1693 * (1.71) | 0.1561 *** (3.25) | 0.1289 *** (4.40) | 0.0623 *** (3.56) |

| City | 0.0813 *** (4.63) | 0.1267 *** (2.06) | 0.3385 (1.22) | 0.1240 (0.98) | 0.5011 * (1.80) | 0.2507 (0.57) |

| Log | 834.7580 | 177.7073 | 834.7580 | 177.7073 | 834.7580 | 177.7073 |

| Rho | 0.7625 *** (3.49) | 0.1890 *** (2.61) | 0.7625 *** (3.49) | 0.1890 *** (2.61) | 0.7625 *** (3.49) | 0.1890 *** (2.61) |

| R2 | 0.9407 | 0.9462 | 0.9407 | 0.9462 | 0.9407 | 0.9462 |

| Obs | 420 | 420 | 420 | 420 | 420 | 420 |

| Variable | M = Fcon | Variable | M = Gteh | ||||

|---|---|---|---|---|---|---|---|

| (4) | (6) | (7) | (4) | (6) | (7) | ||

| L.Fcon | 0.0423 ** (5.38) | L.Gteh | 0.6054 *** (5.78) | ||||

| L.C | 0.5591 *** (13.60) | 0.4514 *** (13.80) | L.C | 0.5591 *** (13.60) | 0.6374 *** (12.50) | ||

| Fcon | 0.0890 *** (3.09) | Gteh | 0.3643 *** (5.74) | ||||

| Gfin | −0.9857 *** (−3.05) | −0.0347 ** (2.10) | −0.6709 ** (−2.20) | Gfin | −0.9857 *** (−3.05) | 0.0147 *** (2.80) | −0.0466 ** (2.03) |

| Control | Yes | Yes | Yes | Control | Yes | Yes | Yes |

| Log | 834.7580 | 653.0568 | 853.6860 | Log | 834.7580 | 645.5168 | 850.156 |

| Rho | 0.7625 *** (3.49) | 0.2891 * (1.69) | 2.1709 *** (17.70) | Rho | 0.7625 *** (3.49) | 0.3451 *** (2.67) | 1.4570 *** (17.08) |

| R2 | 0.9407 | 0.6670 | 0.9691 | R2 | 0.9407 | 0.7593 | 0.9451 |

| Obs | 420 | 420 | 420 | Obs | 420 | 420 | 420 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, X.; Chen, Z. Can Green Finance Development Reduce Carbon Emissions? Empirical Evidence from 30 Chinese Provinces. Sustainability 2021, 13, 12137. https://doi.org/10.3390/su132112137

Chen X, Chen Z. Can Green Finance Development Reduce Carbon Emissions? Empirical Evidence from 30 Chinese Provinces. Sustainability. 2021; 13(21):12137. https://doi.org/10.3390/su132112137

Chicago/Turabian StyleChen, Xi, and Zhigang Chen. 2021. "Can Green Finance Development Reduce Carbon Emissions? Empirical Evidence from 30 Chinese Provinces" Sustainability 13, no. 21: 12137. https://doi.org/10.3390/su132112137

APA StyleChen, X., & Chen, Z. (2021). Can Green Finance Development Reduce Carbon Emissions? Empirical Evidence from 30 Chinese Provinces. Sustainability, 13(21), 12137. https://doi.org/10.3390/su132112137