Sustainable Development Goals in Strategy and Practice: Businesses in Colombia and Egypt

Abstract

:1. Introduction

2. Theoretical Perspective and Hypotheses

2.1. Coupling between Strategy and Practice

2.2. Embeddedness of Strategy and Practice in Society

2.3. Embeddedness of Coupling in Society

3. Research Design

3.1. Sampling

3.2. Measurements

3.2.1. Strategies Supporting SDGs

- -

- When making decisions about the future of your business, you always consider social implications such as access to education, health, safety, inclusive work, housing, transportation, quality of life at work.

- -

- When making decisions about the future of your business, you always consider environmental implications such as preservation of green areas, reduction of the emission of pollutants and toxic gases, selective garbage collection, conscious consumption of water, electricity, and fuels.

- -

- You prioritize the social and/or environmental impact of your business above profitability or growth.

3.2.2. Practices Supporting SDGs

- -

- Have you taken any steps to minimize the environmental impact of your business over the past year? This could include energy saving measures, measures to reduce carbon emissions or introducing more efficient machinery, take care of the solid waste generated, use of recyclable material, use of alternative means of transportation, such as cycling, walking, collective rides, public transportation, etc.

- -

- Have you taken any steps to maximize the social impact of your business over the past year? This could include creating posts for young unemployed and other groups with limited access to the labor market; including social enterprises into your supply chain; ensuring a diverse workforce; prioritize companies and/or suppliers that take actions that respect human rights and the environment, when buying a product or service; fight against any form of child or slave labor; invest or support projects or social organizations that develop the community and include less favored groups.

3.2.3. Society

3.2.4. Control Variables

- -

- Importance of the motive of desiring to improve the World, measured by agreement with the statement, “Please tell me the extent to which the following statements reflect the reasons you are involved in this business. To make a difference in the world.…” The respondent rated agreement on a Likert scale from strongly disagree to strongly agree, coded 1 to 5.

- -

- Importance of the motive of becoming wealthy, likewise coded 1 to 5.

- -

- Salience of the motive of continuing a family tradition, coded 1 to 5.

- -

- Prominence of the motive of earning a living because jobs are scarce, coded 1 to 5.

- -

- Age of the business, measured in years, and logged to reduce skewness.

- -

- Owners, measured as a count from 1 upwards, and logged to reduce skewness.

- -

- Employees, measured as a count from 0 upward, and logged to reduce skewness.

- -

- Gender of the owner-manager, coded 0 for women and 1 for men.

- -

- Age of the owner-manager, coded as years of age, between 18 and 64 years.

- -

- Education of the owner-manager, coded as years of schooling to highest degree.

3.3. Techniques for Analysis

4. Results

4.1. Background of the Businesses

4.2. Strategy

4.3. Practice

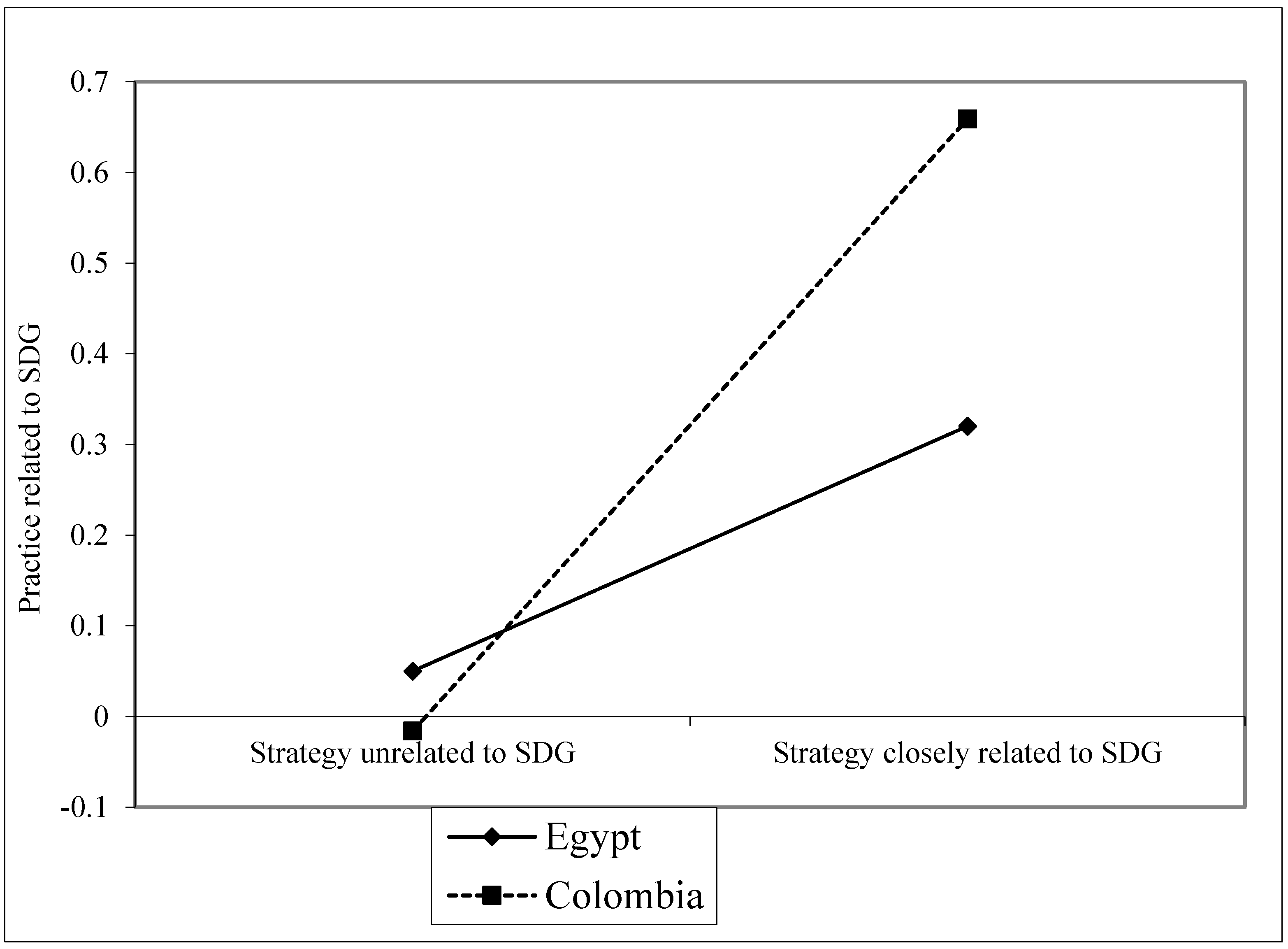

4.4. Effects of Strategy on Practice, Embedded in Society

5. Discussion

5.1. Findings

5.2. Contributions

5.3. Limitations

5.4. Further Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Colombia | Egypt | ||

|---|---|---|---|

| Samples | Number of businesses | 399 | 413 |

| Motive: Improve World | Mean on scale 1 to 5 | 3.54 | 3.44 |

| Motive: Enhance wealth | Mean on scale 1 to 5 | 3.49 | 3.65 |

| Motive: Family tradition | Mean on scale 1 to 5 | 2.88 | 2.96 |

| Motive: Need to earn a living | Mean on scale 1 to 5 | 4.07 | 4.31 |

| Age of business | Median number of years | 1 year | 2 years |

| Owners | Median number of owners | 2 owners | 2 owners |

| Employees | Median number of employees | 0 employee | 1 employee |

| Age of owner-manager | Mean number of years | 36.6 years | 33.5 years |

| Education of owner-manager | Mean number of years | 12.9 years | 12.5 years |

| Gender of owner-manager | Percent males | 54% | 77% |

| Col | Max | Min | Priorit | C.Env | C.Soc | World | Wealth | Family | Need | b.Age | Own | Empl | Agse | Educ | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Society: Colombia | |||||||||||||||

| Maximize social benefit | 0.14 *** | ||||||||||||||

| Minimize environmental | 0.32 *** | 0.58 *** | |||||||||||||

| Prioritize soc-env impact | −0.09 | 0.12 *** | 0.14 *** | ||||||||||||

| Consider environm harm | −0.01 | 0.13 *** | 0.17 *** | 0.39 *** | |||||||||||

| Consider social benefit | 0.00 | 0.10 ** | 0.13 *** | 0.30 *** | 0.38 *** | ||||||||||

| Motive: Improve World | 0.03 | 0.16 *** | 0.18 *** | 0.10 ** | 0.11 ** | 0.14 ** | |||||||||

| Motive: Enhance wealth | −0.06 | 0.02 | 0.05 | 0.06 † | 0.09 * | 0.06 † | 0.32 *** | ||||||||

| Motive: Family tradition | −0.02 | 0.03 | 0.06 | 0.07 * | 0.03 | 0.03 | 0.17 ** | 0.18 *** | |||||||

| Motive: Need to earn living | −0.10 ** | −0.02 | −0.02 | 0.07 * | 0.07 † | 0.08 | 0.00 | 0.06 | 0.12 *** | ||||||

| Age of business | −0.22 ** | −0.01 | −0.05 | −0.02 | −0.03 | −0.06 | −0.04 | 0.01 | 0.07 † | 0.02 | |||||

| Owners | 0.02 | 0.03 | 0.01 | −0.03 | −0.04 | 0.00 | −0.03 | −0.07 † | 0.11 ** | 0.03 | −0.05 | ||||

| Employees | −0.21 ** | 0.08 * | 0.03 | −0.03 | −0.05 | 0.01 | 0.06 † | 0.06 † | 0.12 *** | 0.00 | 0.47 *** | 0.13 *** | |||

| Age of owner-manager | 0.0.13 *** | −0.03 | 0.04 | −0.02 | 0.05 | 0.04 | −0.09 * | −0.19 ** | −0.03 | 0.01 | 0.16 *** | −0.01 | 0.04 | ||

| Education | 0.03 | 0.03 | 0.06 | 0.04 | 0.03 | 0.07 * | −0.05 | 0.03 | −0.20 ** | −0.12 ** | 0.00 | 0.01 | 0.04 | −0.08 * | |

| Gender: Male | −0.24 ** | 0.03 | −0.06 | 0.05 | −0.01 | −0.02 | 0.02 | 0.06 | 0.09* | 0.00 | 0.17 *** | 0.02 | 0.12 *** | −0.05 | −0.02 |

References

- United Nations. Sustainable Development Goals. 17 Goals to Transform Our World. 2018. Available online: https://www.un.org/sustainabledevelopment/sustainable-consumption-production/ (accessed on 12 July 2020).

- UN Secretary-General & World Commission on Environment and Development (WCED). Report of the World Commission on Environment and Development: Our common future. In Report of the World Commission on Environment and Development: Note/by the Secretary-General No. A/42/427; UN Secretary General: New York, NY, USA, 1987; Available online: https://digitallibrary.un.org/record/139811?ln=en (accessed on 1 November 2021).

- Rosati, F.; Faria, L.G. Business contribution to the Sustainable Development Agenda: Organizational factors related to early adoption of SDG reporting. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 588–597. [Google Scholar] [CrossRef]

- Global Reporting Initiative (GRI) & United Nations Global Compact (UN Global Compact). Business Reporting on the SDGs: An Analysis of the Goals and Targets. 2017. Available online: https://www.globalreporting.org/media/v5milwee/gri_ungc_business-reporting-on-sdgs_analysis-of-goals-and-targets.pdf (accessed on 1 November 2021).

- Luomi, M.; Fuller, G.; Dahan, L.; Lisboa Båsund, K.; de la Mothe Karoubi, E.; Lafortune, G. Arab Region SDG Index and Dashboards Report 2019; SDG Centre of Excellence for the Arab Region/Emirates Diplomatic Academy and Sustainable Development Solutions Network: Abu Dhabi, United Arab Emirates; New York, NY, USA, 2019. [Google Scholar]

- Shehata, N.F. Corporate governance: Are we on the right track? An overview of corporate governance development in Egypt. AUC Bus. Rev. 2015, 5, 46–49. [Google Scholar]

- UNCTAD. Guidance on Core Indicators for Entity Reporting on Contribution towards Implementation of the Sustainable Development Goals. 2019. Available online: https://unctad.org/webflyer/guidance-core-indicators-entity-reporting-contribution-towards-implementation-sustainable (accessed on 1 November 2021).

- Sachs, J.; Schmidt-Traub, G.; Kroll, C.; Lafortune, G.; Fuller, G. Sustainable Development Report 2021; Cambridge University Press: Cambridge, UK, 2021. [Google Scholar]

- Bansal, S.; Garg, I.; Sharma, G. Social entrepreneurship as a path for social change and driver of sustainable development: A systematic review and research agenda. Sustainability 2019, 11, 1091. [Google Scholar] [CrossRef] [Green Version]

- Kraus, S.; Burtscher, J.; Niemand, T.; Roig-Tierno, N.; Syrjä, P. Sustainable entrepreneurship in SMEs: Configurational paths to social performance. Sustainability 2017, 9, 1828. [Google Scholar] [CrossRef] [Green Version]

- Pérez, A. (Ed.) Future Advancements for CSR and the Sustainable Development Goals in a Post-COVID-19 World; IGI Global: Hershey, PA, USA, 2021. [Google Scholar] [CrossRef]

- Czerwińska, T.; Kaźmierkiewicz, P. ESG rating in investment risk analysis of companies listed on the public market in Poland. Econ. Notes Rev. Bank. Financ. Monet. Econ. 2015, 44, 211–248. [Google Scholar] [CrossRef]

- Sarango-Lalangui, P.; Santos, J.L.S.; Hormiga, E. The development of sustainable entrepreneurship research field. Sustainability 2018, 10, 2005. [Google Scholar] [CrossRef] [Green Version]

- Rendtorff, J.D. Management of the Political Enterprise in the Service of the Sustainable Development Goals (SDGs) in Cosmopolitan Society: Integrating Ethical Values-Driven Management in the Politicization of the Corporation. In Future Advancements for CSR and the Sustainable Development Goals in a Post-COVID-19 World; Pérez, A., Ed.; IGI Global: Hershey, PA, USA, 2021; pp. 50–66. [Google Scholar]

- Agarwal, N.; Gneiting, U.; Mhlanga, R. Raising the Bar: Rethinking the Role of Business in the Sustainable Development Goals (Oxfam Discussion Papers). 2017. Available online: https://www-cdn.oxfam.org/s3fs-public/dp-raising-the-bar-business-sdgs-130217-en_0.pdf (accessed on 1 November 2021).

- Larcker, D.; Tayan, B. Corporate Governance Matters; Pearson Education: Upper Saddle River, NJ, USA, 2016. [Google Scholar]

- Mattingly, J.E.; Berman, S.L. Measurement of corporate social action. Bus. Soc. 2006, 45, 20–46. [Google Scholar] [CrossRef]

- Rosati, F.; Faria, L.G. Addressing the SDGs in sustainability reports: The relationship with institutional factors. J. Clean. Prod. 2019, 215, 1312–1326. [Google Scholar] [CrossRef]

- Diez-Busto, E.; Fernandez-Laviada, A.; Sanchez-Ruiz, L. B Corp Certification Effects: Design and Validation of a Questionnaire Applying Delphi Method. In Future Advancements for CSR and the Sustainable Development Goals in a Post-COVID-19 World; Pérez, A., Ed.; IGI Global: Hershey, PA, USA, 2021; pp. 198–215. [Google Scholar]

- Figge, F.; Hahn, T. Is green and profitable sustainable? Assessing the trade-of between economic and environmental aspects. Int. J. Prod. Econ. 2012, 140, 92–102. [Google Scholar] [CrossRef]

- Schramade, W. Investing in the UN Sustainable Development Goals: Opportunities for companies and investors. J. Appl. Corp. Financ. 2017, 29, 87–99. [Google Scholar] [CrossRef]

- Schönherr, N.; Findler, F.; Martinuzzi, A. Exploring the interface of CSR and the sustainable development goals. Transnatl. Corp. 2017, 24, 33–47. [Google Scholar] [CrossRef] [Green Version]

- Hoogendoorn, B.; van der Zwan, P.; Thurik, R. Sustainable entrepreneurship: The role of perceived barriers and risk. J. Bus. Ethics 2019, 157, 1133–1154. [Google Scholar] [CrossRef] [Green Version]

- Garcia-Sanchez, I.M.; Cuadrado-Ballesteros, B.; Sepulveda, C. Does media pressure moderate CSR disclosures by external directors? Manag. Decis. 2014, 52, 1014–1045. [Google Scholar] [CrossRef]

- Srinidhi, B.; Gul, F.A.; Tsui, J. Female directors and earnings quality. Contemp. Account. Res. 2011, 28, 1610–1644. [Google Scholar] [CrossRef]

- Hockerts, K. A cognitive perspective on the business case for corporate sustainability. Bus. Strategy Environ. 2015, 24, 102–122. [Google Scholar] [CrossRef]

- Jizi, M. The influence of board composition on sustainable development disclosure. Bus. Strategy Environ. 2017, 26, 640–655. [Google Scholar] [CrossRef]

- Ahmad, N.H.; Seet, P.S. Gender variations in ethical and socially responsible considerations among SME entrepreneurs in Malaysia. Int. J. Bus. Soc. 2010, 11, 77–88. [Google Scholar]

- Hechavarría, D.M.; Terjesen, S.A.; Ingram, A.E.; Renko, M.; Justo, R.; Elam, A. Taking care of business: The impact of culture and gender on entrepreneurs’ blended value creation goals. Small Bus. Econ. 2016, 48, 225–257. [Google Scholar] [CrossRef]

- Tiba, S.; van Rijnsoever, F.J.; Hekkert, M.P. Firms with benefits: A systematic review of responsible entrepreneurship and corporate social responsibility literature. Corp. Soc. Responsib. Environ. Manag. 2018, 26, 265–284. [Google Scholar] [CrossRef] [Green Version]

- Calvin, C.G.; Street, D.L. An analysis of Dow 30 global core indicator disclosures and environmental, social, and governance-related ratings. J. Int. Financ. Manag. Account. 2020, 31, 323–349. [Google Scholar] [CrossRef]

- Hörisch, J.; Freeman, R.E.; Schaltegger, S. Applying stakeholder theory in sustainability management. Organ. Environ. 2014, 27, 328–346. [Google Scholar] [CrossRef]

- DANE. 2020. Available online: https://www.dane.gov.co/files/investigaciones/condiciones_vida/pobreza/2020/Comunicado-pobreza-monetaria_2020.pdf (accessed on 7 September 2021).

- Weick, K.E. Educational Organizations as Loosely Coupled Systems. Adm. Sci. Q. 1976, 21, 1–19. [Google Scholar] [CrossRef]

- Orton, J.D.; Weick, K.E. Loosely coupled systems: A reconceptualization. Acad. Manag. Rev. 1990, 15, 203–223. [Google Scholar] [CrossRef]

- York, J.G.; O’Neil, I.; Sarasvathy, S.D. Exploring environmental entrepreneurship: Identity coupling, venture goals, and stakeholder incentives. J. Manag. Stud. 2016, 53, 695–737. [Google Scholar] [CrossRef]

- Meyer, J.W.; Rowan, B. Institutionalized organizations: Formal structure as myth and ceremony. Am. J. Sociol. 1977, 83, 340–363. [Google Scholar] [CrossRef] [Green Version]

- Brinks, D.M.; Levitsky, S.; Murillo, M.V. Understanding Institutional Weakness; Cambridge University Press: Cambridge, UK, 2019. [Google Scholar]

- Moses, O.; Mohaimen, F.J.; Emmanuel, M. A meta-review of SEAJ: The past and projections for 2020 and beyond. Soc. Environ. Account. J. 2020, 40, 24–41. [Google Scholar] [CrossRef]

- Alvarez-Risco, A.; Del-Aguila-Arcentales, S.; Rosen, M.A.; García-Ibarra, V.; Maycotte-Felkel, S.; Martínez-Toro, G.M. Expectations and interests of university students in COVID-19 times about Sustainable Development Goals: Evidence from Colombia, Ecuador, Mexico, and Peru. Sustainability 2021, 13, 3306. [Google Scholar] [CrossRef]

- Owusu-Ansah, S. The impact of corporate attributes on the extent of mandatory disclosure and reporting by listed companies in Zimbabwe. Int. J. Account. 1998, 33, 605–631. [Google Scholar] [CrossRef]

- Shehata, N.F.; Dahawy, K. Review of Sustainable Development Goals Disclosures in Egypt. In International Accounting and Reporting Issues-2019 Review; United Nations: New York, NY, USA, 2020; pp. 13–22. Available online: https://unctad.org/system/files/official-document/diaeed2019d1_en.pdf (accessed on 1 November 2021).

- Ministry of Planning and Economic Development of Egypt (n.d.). Egypt’s Vision 2030. Available online: https://mped.gov.eg/EgyptVision?lang=en (accessed on 1 November 2021).

- Pineda-Escobar, M.A. Moving the 2030 agenda forward: SDG implementation in Colombia. Corp. Gov. Int. J. Bus. Soc. 2019, 19, 176–188. [Google Scholar] [CrossRef]

- Inglehart, R.; Welzel, C. Modernization, Cultural Change, and Democracy; Cambridge University Press: Cambridge, UK, 2005. [Google Scholar]

- Wang, D.; Schøtt, T. Coupling between financing and innovation in a startup: Embedded in networks with investors and researchers. Int. Entrep. Manag. J. 2020, 1–12. Available online: https://link.springer.com/article/10.1007%2Fs11365-020-00681-y (accessed on 1 November 2021). [CrossRef]

- Schøtt, T.; Wickstrøm, K.W. The coupling between entrepreneurship and public policy: Tight in developed countries but loose in developing countries. Estud. Econ. 2008, 35, 195–214. [Google Scholar] [CrossRef]

- Bosma, N. The Global Entrepreneurship Monitor (GEM) and its impact on entrepreneurship research. Found. Trends Entrep. 2013, 9, 2. [Google Scholar] [CrossRef] [Green Version]

| Colombia | Egypt | ||||||

|---|---|---|---|---|---|---|---|

| Considering Social Impact | Considering Environmental Impact | Prioritizing Social and Environmental Impact | Considering Social Impact | Considering Environmental Impact | Prioritizing Social and Environmental Impact | ||

| Strongly agree | 5 | 52% | 59% | 35% | 55% | 68% | 46% |

| Somewhat agree | 4 | 35% | 29% | 37% | 31% | 20% | 35% |

| Neither agree nor disagree | 3 | 5% | 5% | 9% | 4% | 3% | 4% |

| Somewhat disagree | 2 | 6% | 5% | 10% | 5% | 3% | 6% |

| Strongly disagree | 1 | 2% | 2% | 8% | 5% | 6% | 9% |

| Sum | 100% | 100% | 100% | 100% | 100% | 100% | |

| Mean | 4.29 | 4.38 | 3.82 | 4.28 | 4.40 | 4.004 | |

| N businesses | 390 | 393 | 387 | 411 | 412 | 408 | |

| Metric Coefficients | Standardized Coefficients | |

|---|---|---|

| Society: Colombia | −0.082 | −0.05 |

| Motive: Improve World | 0.080 ** | 0.14 ** |

| Motive: Enhance wealth | 0.027 | 0.05 |

| Motive: Family tradition | 0.027 | 0.06 |

| Motive: Earn a living | 0.046 | 0.06 |

| Age of business | −0.035 | −0.04 |

| Owners | −0.041 | −0.03 |

| Employees | −0.032 | −0.04 |

| Age of owner-manager | 0.005 | 0.07 |

| Education | 0.012 * | 0.08 * |

| Gender: Male | 0.053 | 0.03 |

| Intercept | 3.334 *** |

| Colombia | Egypt | ||||

|---|---|---|---|---|---|

| Maximize Social Benefit | Minimize Environmental Harm | Maximize Social Benefit | Minimize Environmental Harm | ||

| Practicing this | Percent of businesses | 71% | 61% | 39% | 46% |

| Not practicing this | Percent of businesses | 29% | 39% | 61% | 54% |

| Sum | 100% | 100% | 100% | 100% | |

| N businesses | 384 | 387 | 405 | 406 | |

| Threshold | Practice = 0 | 1.220 ** |

| Practice = 0.5 | 2.221 *** | |

| Location | Colombia | 1.213 *** |

| Motive: Improve the World | 0.252 *** | |

| Motive: Great wealth | −0.040 | |

| Motive: Family tradition | 0.057 | |

| Motive: Earn a living | −0.010 | |

| Age of business | −0.051 | |

| Owners | 0.052 | |

| Employees | 0.230 ** | |

| Age of owner-manager | −0.002 | |

| Education | 0.014 | |

| Gender: Male | 0.265 † |

| Threshold | Practice = 0 | 2.640 *** | 1.941 ** |

| Practice = 0.5 | 3.657 *** | 2.962 *** | |

| Location | Strategy | 0.427 *** | 0.256 * |

| Society: Colombia | 1.289 *** | −0.330 | |

| Strategy * Society Colombia | 0.384 * | ||

| Motive: Improve the World | 0.219 *** | 0.222 *** | |

| Motive: Great wealth | −0.050 | −0.043 | |

| Motive: Family tradition | 0.040 | 0.035 | |

| Motive: Earn a living | −0.027 | −0.024 | |

| Age of business | −0.033 | −0.025 | |

| Owners | 0.064 | 0.063 | |

| Employees | 0.251 ** | 0.245 ** | |

| Age of owner-manager | −0.005 | −0.005 | |

| Education | 0.009 | 0.011 | |

| Gender: Male | 0.263 † | 0.271 † |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, Y.; Samsami, M.; Meshreki, H.; Pereira, F.; Schøtt, T. Sustainable Development Goals in Strategy and Practice: Businesses in Colombia and Egypt. Sustainability 2021, 13, 12453. https://doi.org/10.3390/su132212453

Liu Y, Samsami M, Meshreki H, Pereira F, Schøtt T. Sustainable Development Goals in Strategy and Practice: Businesses in Colombia and Egypt. Sustainability. 2021; 13(22):12453. https://doi.org/10.3390/su132212453

Chicago/Turabian StyleLiu, Ye, Mahsa Samsami, Hakim Meshreki, Fernando Pereira, and Thomas Schøtt. 2021. "Sustainable Development Goals in Strategy and Practice: Businesses in Colombia and Egypt" Sustainability 13, no. 22: 12453. https://doi.org/10.3390/su132212453

APA StyleLiu, Y., Samsami, M., Meshreki, H., Pereira, F., & Schøtt, T. (2021). Sustainable Development Goals in Strategy and Practice: Businesses in Colombia and Egypt. Sustainability, 13(22), 12453. https://doi.org/10.3390/su132212453