1. Introduction

In reference to the “Intergovernmental Panel on Climate Change”, air pollution and global warming were considered to be the most significant issues in the last few decades [

1], and the cited carbon dioxide (CO

2) emissions were found to be the determinant of these challenges, and also a challenge to sustainability [

2]. For instance, Turkey was ranked 51st of 61 countries globally in terms of climate-change protection, according to the climate-change performance index in 2015, and the country was criticized for its absence of national policies to prevent climate change [

3]. The “International Energy Agency” (IEA) posits that “energy-related CO

2 emissions” in Turkey began to increase rapidly during the 1990s, and between 1990 and 2012, there was an increase of 138.3% change in CO

2 emissions in the country [

4]. According to the World Bank [

5], Turkey is a non-industrial nation with US

$754.412 billion “gross domestic product (GDP)” and “per capita GDP” of US

$14,998.98 in 2019. The percentages of exports and imports of goods and services were 31.61% and 29.78%, individually, for 2019. Bilgen et al. [

6] saw that Turkey is described by fast financial development, as well as its expanding pace of urbanization, unbending energy utilization, and expanding CO

2 emissions with hefty dependence on imported energy assets, which Kalmaz and Kirikkaleli [

7] noticed are liable for the principle wellspring of present record deficiencies for quite a long while. It was estimated by World Bank [

5] that 75% out of the total energy consumption in Turkey was imported from overseas in 2015. This indicates the level of Turley reliance on foreign energy resources, whereas, according to Türkiye İstatistik Kurumu (TÜİK) [

8], GHG is mostly generated by energy consumption, with over 80% of CO

2 emissions out of the total GHG in Turkey. In the case of Turkey, for instance, Akca, Ozturk, and Gunes [

9] considered air pollution to be among the causes of lung cancer and respiratory disease. In contrast, a nation is said to be sustainable “when it does not deplete or disrupt ecosystems to the prejudice of the livelihoods and well-being of others now or in the future” [

10]. Akca et al. [

9], in addition, stated that the challenges of environmental pollution in Turkey are not limited to urban areas and the rural areas, which indicates that the achievement of “sustainable development” in the country is under threat.

The significance of CO

2 emissions as a great contributor to “greenhouse gas (GHG) emissions” was emphasized by the Intergovernmental Panel on Climate Change (IPCC), which reported that about 76.6% of “GHG emissions”, which consist of CO

2 emissions, emanate from emerging economies countries with the view of ensuring acceleration of their “growth rate” and “national production” to achieve better economic conditions [

3,

11,

12]. According to Kirikkaleli and Kalmaz [

7], improved economic growth enhances living standards, but it also leads to urbanization increase and energy consumption, which are contributors to high levels of CO

2 emissions, which could be the result of “overuse” or “misallocation” of energy resources that is often predominant in less-developed countries [

13]. Three strands were notably identified in the studies that concentrate on this debate. Firstly, the validity of Environmental Kuznets Curve (EKC) theory was investigated by examining the economic growth effect on carbon emissions [

14,

15,

16]. In reference to Lorente and Alvarez-Herranz [

17], it was in the EKC theory that the nexus between CO

2 and economic growth displayed an inverted U-shape, which indicates that, at the initial stage of economic growth, pollution increases but starts declining when it arrives a threshold as a result of improved technology, regulations on the environment both at “intergovernmental” and “global level”, and educating the public about the increase, which contributes to the amelioration of environmental degradation. The second strand in the literature on EKC investigates the effect of economic growth on energy consumption, using causality and cointegration tests, in line with the study of Kraft and Kraft [

18], which is in line with another study that revealed “energy consumption” to be among the “environmental degradation” determinant factors [

19]. In the third strand, the two dimensions in the literature on EKC were combined with the inclusion of “energy consumption” and other economic variables for further analysis “EKC hypothesis”, to address the omission of “variable bias” in the literature [

20,

21,

22,

23,

24,

25,

26]. Meanwhile, there has not been a consensus on the “EKC hypothesis”, owing to the different outcomes from different studies from a different region. Therefore, it becomes imperative to consider “country-specific” indicators for investigation.

Despite how a couple of assessments have attempted to investigate the impact of different economic-related indicators on EKC [

7,

27,

28,

29,

30,

31], to the best of our understanding, the possible moderating effect of financial development has not been investigated. This formed the main focuses, similarly to the uniqueness, of the current assessment. The study of Aye and Edoja [

32] highlighted four theoretical perspectives due to related economic progression on CO

2 emissions, including the “eco-friendly technology”, the Foreign Direct Investment (FDI), improvement in the manufacturing industry, and the perspective consumers’ credit improvement. The suggestion that “financial development” decreases CO

2 when the money-related business areas makes a course of action for financial assistance to the close by firms so they can get eco-friendly and clean technology for industrial purposes. This speculative perspective was affirmed by the examination of Yuxiang and Chen [

33], who said that the financial market in China gives financing and concentrated assistance that engages the associations to grasp new and improved technology that improves their production and at the same time reduce the CO

2 radiations. The examination of Frankel and Rose [

34], in like manner, accepted that the financial market could effectively allocate money-related resources for domestic firms to enable them to purchase pleasant atmosphere technology. A couple of examinations saw that there would be an increase in CO

2, on the one hand, if financial progression leads to demands for energy-using advancements [

35,

36,

37]. In contrast, “credit facilities” and “investment channels”, given by the related money system and overall trade, may give space for an engaging atmosphere for inventive work of low-carbon energy sources if money-related improvement is intertwined into eco-friendly policies and rules [

38,

39]. This implies that financial improvement could reduce environmental defilement by decreasing carbon emissions in the economy [

40].

At that point, near assessments have a lot of the composing that focused in on a couple of pointers of CO

2 releases in Turkey [

3,

7,

41,

42]; regardless, the fundamental question of how financial progression impacts characteristic degradation in Turkey really requires further assessment. Our examination hopes to address this huge request by considering the coordinating position of “financial development” for various determinants of environmental degradation, since financial development makes a correspondence through influencing environmental degradation, just as addition economic growth, advance gross fixed capital plan, raise energy usage, and augmentation urbanization, as proposed in the literature [

3,

7,

35,

36,

37,

38,

39,

40,

43]. Notwithstanding the way that most of these examinations used a proper model for the assessment, at this point, they fail to consider the moderating position of financial development. This assessment aims to fill the opening inside Turkey’s setting, since Turkey is an intriguing examination setting both in the methodology field and the educational, as being the third most raised CO

2 emissions creating a country with the least energy use among the EU part countries [

7]. These real factors show the imperativeness of reshaping the public environmental policies in Turkey to control the CO

2 releases and reduce the defilement to a particular commendable level for the improvement of environmental quality. Thus, unprecedented for the composition, the impact of gross capital formation (GCF), GDP, energy use, urbanization, and financial development on CO

2 emissions inside the setting of Turkey is fused by this assessment, through using novel econometric strategies and considering the moderation effect of financial development to address the opening in the literature and to have the choice to give strong observational disclosures to policymakers. The contribution of this paper lies in the application of novel econometric techniques, the inclusion of new variables to the EKC hypothesis, and the conducting of the study within the setting of Turkey, which has not been exhaustively investigated. The findings will be valuable to the policymakers in formulating an environmental and financial-related policy that will ensure the improvement of the financial market and reduce carbon emission, with the view of ensuring a clean environment. Thus, the purpose of the paper is to examine the significance of different economic factors on environmental degradation and the possible moderating effect of financial development, which, to the best of the authors’ knowledge, has not been investigated especially in the context of Turkey. This was the main purpose of this study, as well as the novelty of our research. The significance of financial development on environmental degradation should not be underestimated, owing to its possible relationship with energy consumption and economic growth, which have been identified as being among the factors that trigger environmental degradation.

The remainder of the paper is composed as follows. A review of experimental assessments from the literature is discussed in

Section 2. Data description, sources, and strategy are given in

Section 3. The specific disclosures are presented in

Section 4, and

Section 5 contains the discussion and conclusion.

2. Review of Related Studies

In recent times, the issue of environmental pollution is becoming promising, and the attention received in the discussion among various stakeholders has increased, since environmental pollution is believed to be the genesis cause of both climate change and global warming [

13,

43]. Climate change and global warming are believed to impose a catastrophic adverse impact on people’s livelihoods and on the pace of economic growth, especially in industrialized countries. Meanwhile, Kirikkaleli and Kalmaz [

7] observed that developing countries aim to improve their “economic growth” for a good standard of living, which would be achieved by enhancing the production output. The increased output in these countries results in to increase in energy consumption and level of urbanization, which in turn contributes to the high levels of CO

2 emissions via the misapplication or misallocation of energy resources [

7]. Several studies abound in the literature that concentrate on this debate. Several of these studies have employed econometrics methods and procedures to empirically examine the nexus between economic growth, energy consumption, and carbon emissions. Some of these studies are country-specific (time series analysis) or panel studies, and three strands could be identified in the literature.

The first strand in the literature was under the “Environmental Kuznets Curve” (EKC), which posits that CO

2 increases, until it gets to a threshold level of income, which is reached when there is an increase in income. After that level, as there increase in income, the CO

2 emissions start decreasing. Several studies have investigated the EKC hypothesis [

14,

16,

44,

45,

46]. The second school of thought belongs to those that follow Kraft and Kraft [

18], who investigated the nexus between “energy consumption” and “carbon emissions”. Some of these studies utilized causality and cointegration tests [

19,

20,

41,

47,

48,

49,

50,

51,

52]. The third strand is those studies that combine the first two dimensions and introduced energy consumption into the nexus between income and carbon emission to address the challenges of “omitted variable bias” of the EKC hypotheses [

7,

21,

22,

23,

24,

53,

54]. About Turkey, several studies have investigated the EKC hypothesis extensively. The study of Haliciolglu [

54] employed Autoregressive Distributed Lag (ARDL) testing techniques for determining the nexus between energy consumption and carbon emissions in the long run. The study found the existence of EKC in Turkey. A similar study was conducted by Ozturk and Acaravci [

55], to investigate the EKC in Turkey, using data from 1968 to 2005. Different from the finding of Halicioglu [

54], Ozturk and Acaravci [

55] demonstrated that EKC is not valid for the period examined. However, in their study in 2013, the EKC was confirmed when financial development and trade were included with energy consumption, economic development, and CO

2 [

56]. Similarly, the EKC hypothesis was confirmed in the case of study in the study of Shahbaz et al. [

39], which investigated the relationship between CO

2, economic growth, energy intensity, and globalization, using data that spanned between 1970 and 2010. The study employed a “unit root test” and “cointegration technique” under the existence of structural breaks. A recent study by Kirikkaleli and Kalmaz [

7] confirmed the validity of the EKC hypothesis for Turkey and also demonstrated that energy consumption, trade, and urbanization are significant determinants of CO

2 emissions in Turkey. This finding corroborates the findings of Kalmaz and Kirikkaleli [

7], who demonstrated that CO

2 emission is triggered by energy consumption, economic growth, and urbanization.

As a result of the inconclusive findings on the relationship between energy use, economic development, and carbon emissions, some studies have attempted to include some indicators in their studies, among which is “gross fixed capital formation” (GFCF) [

51,

57,

58,

59]. These studies see GCF as a proxy for capital on the ground that changes in capital stock impact changes in investment, which is predicated on the standard assumption of a constant depreciation rate using the perpetual inventory techniques [

60,

61,

62]. The study of Solarin and Shabaz [

63] investigated the nexus between natural gas consumption and economic growth, including FDI, capital formation, and trade openness in Malaysia, using data that covers the period from 1971 to 2012. The study employed a structural break unit root test and cointegration techniques. ARDL was employed for the study robustness, and the study established a cointegration among the variables and also demonstrated the significant effect of FDI, natural gas consumption, capital formation, and trade openness on the economic growth in Malaysia. Several studies have also examined the effect of capital formation in a different context and found its significant relationship with economic growth [

57,

64,

65,

66,

67] and the consequent impact on environmental pollution through carbon emissions.

Economic growth in some countries, especially developing countries, increases the rate of urbanization [

68]. Urbanization has been found, in some studies, to have a significant relationship with energy consumption and environmental pollution [

69,

70]. These studies posit that about 75% of the energy consumption and 60% of carbon emission globally have been accounted for by urban spaces. Moreover, a few examinations contended that urbanization is a critical determinant of carbon emissions [

7,

71,

72,

73]. The writing in such a manner uncovers the presence of three hypotheses that inspect the nexus among urbanization and the natural environment. The hypotheses are natural modernization [

74], metropolitan ecological change [

75], and “compact city theories” [

76]. These hypotheses imply that the impact of urbanization on the climate can be positive or negative contingent upon the net effect, and, what is more, that financial exercises sway the metropolitan and mechanical spaces; in this manner, urbanization impacts fossil fuel byproducts [

77,

78,

79,

80,

81,

82,

83,

84].

From the observational perspective, studies flourish on the connection between financial development and CO

2 discharges. For example, Shahbaz et al. [

38] examined the nexus among economic development, trade openness, energy utilization, financial development, and CO

2 emissions in Indonesia, utilizing ARDL, Vector Error Correction Model (VECM), and the novel accounting way to deal with Granger causality. The discoveries from the examination demonstrate that, while in the oil-plentiful economy, energy utilization, and monetary development drive CO

2 emissions, the development of financial markets and trade openness adds to the decrease of CO

2 emanations. The investigation of Sy et al. [

85] researched the interrelationship between development in the financial market, CO

2 outflows, and economic development in 40 European nations, utilizing OLS procedures. The investigation found, among others, the presence of impartiality theory between financial development and CO

2 emanations. Furthermore, the connection between financial development and CO

2 emissions was inspected by Charfeddine and Khediri [

86], dependent on the EKC theory for United Arab Emirates (UAE). The examination uncovered a modified U-formed connection between financial development and environmental degradation, which shows that environmental degradation increases as the monetary area develops and then reduce when the monetary areas get to the maturity level and produce effectiveness in the designation of assets. A comparable report was led in Bangladesh by Alom et al. [

87], and the examination found a positive effect of monetary advancement on CO

2 discharges. Kong and Wei [

88] examined the nexus between financial development and CO

2 outflow, utilizing panel data that included China’s 30 areas. The investigation hypothesized that low monetary improvement adds to the decrease of CO

2, while more elevated levels of monetary advancement bring about an expansion in CO

2 emanations. The impact of monetary improvement on carbon emissions in 129 nations was investigated by Al-Mulali et al. [

89]. The outcome uncovered that monetary advancement in the short- and long-run improves the quality of the environment inferable from its negative effect on CO

2 emissions. The investigation of Nasreen et al. [

90] was inclined towards the assurance of the impact of monetary dependability on the CO

2 outflows. The outcome affirmed the commitment of monetary strength to the decrease of ecological corruption. A new report by Xu et al. [

36] inspected the nexus between financial development and environmental degradation in Saudi Arabia by utilizing the ARDL and VECM. The examination uncovered a huge and positive relationship and bidirectional causality between financial development and environmental degradation.

Evidence from the literature indicates that the existing studies have not exhaustively investigated the determinants of carbon emissions, hence the need for further studies. Thus, this study aimed to highlight the possible moderating effect of financial development on Turkey’s “environmental quality”, using the “Zivot–Andrew unit root test”, “Lee–Strazicich unit root test”, Bayer and Hack [

91] “cointegration test”, and “fully modified ordinary least square (FMOLS)” in reference to the suggestion of Shabaz et al. [

43] that it would be helpful for policymakers to articulate a sound environmental-related policy for “sustainable development” of the individual country if the researcher can employ new econometrics approach for different panels and time-series data.

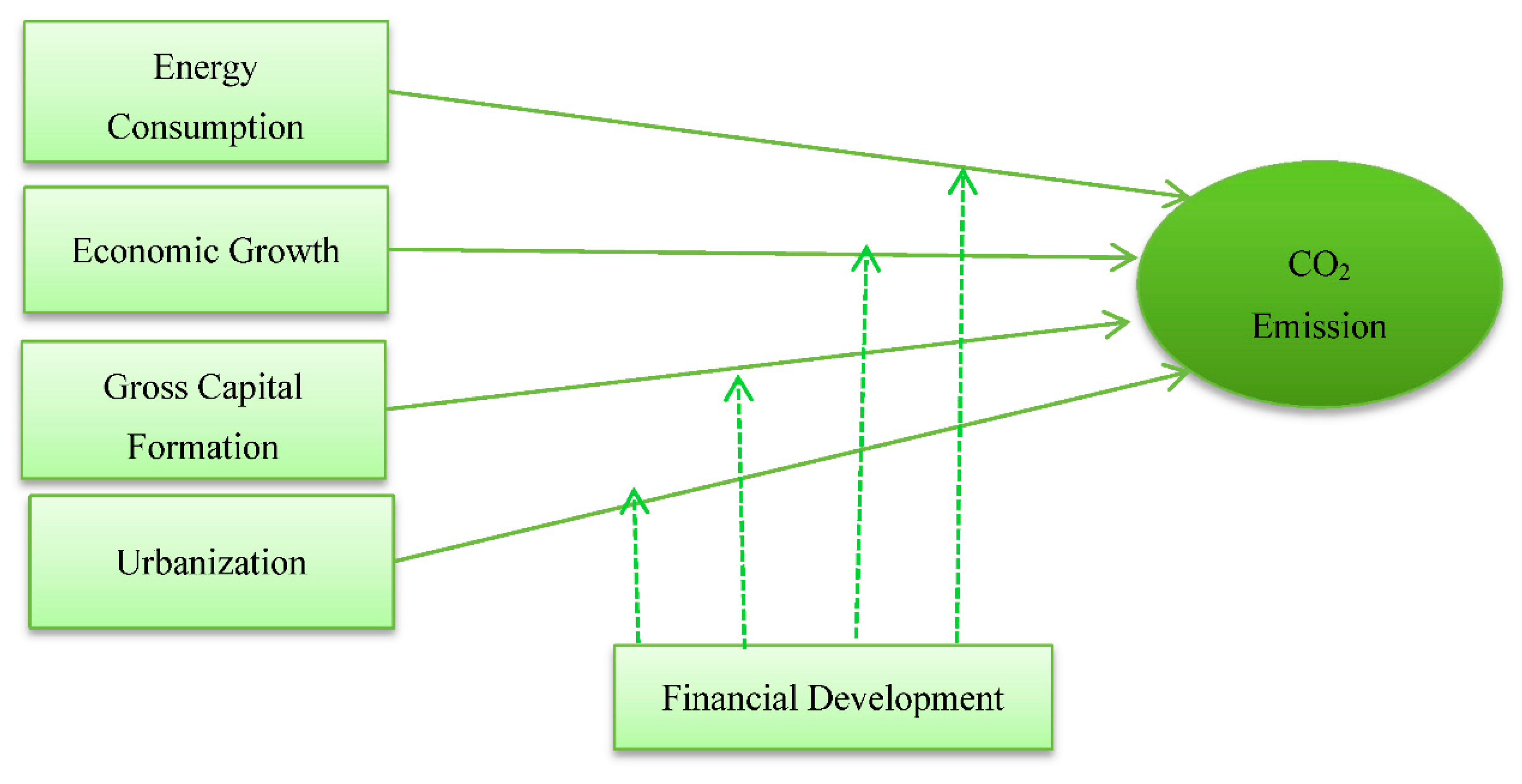

Moreover, in reference to the extant literature reviewed, this study hypothesized, in Equation (1), the significance of variables (economic growth, energy consumption, gross capital formation, urbanization, and financial development) employed in this study individually on environmental degradation. In addition, it was hypothesized in Equation (2) that financial development will moderate the possible relationship of energy consumption, economic growth, gross capita formation, and urbanization with environmental degradation.

4. Empirical Findings

We first exhibit in

Table 2 the descriptive statistics of all the variables studied in this paper. From the table, we confirm that all the variables are normally distributed, except for financial development, gross capital, and urbanization, as confirmed by using kurtosis and skewness values and the Jaqua–Bera test.

We first employed the Zivot and Andrew (ZA) and the Lee and Strazicich (LS) unit root tests, to capture the order of integrations and structural breaks and exhibit the results in

Table 3 and

Table 4, respectively. The outcomes of the ZA unit root test depicted in

Table 3 reveal that all the series are not stationary at level. However, after the first difference is taken, all the series are stationary with a structural break in 2006, 2001, 1995, 2005, 2004, and 1990 for CO

2, EN, GDP, GCF, FD, and URB, respectively. The outcomes of the LS unit root test portrayed in

Table 4 show that all the series are stationary with different mixed levels, except for GCF, which becomes stationary after differencing.

We then utilized the ARDL bounds test technique to explore the long-run interconnection among energy consumption, GDP growth, urbanization, financial development, and gross capital formation, in the case of Turkey, by using yearly data stretching between 1960 and 2017. The first phase in evaluating the ARDL bounds test was the selection of the optimal lag order for the indicators in the framework. As a result, the Schwartz Bayesian Criterion (SBC) was utilized.

Table 5 illustrates the cointegration outcomes for the two models. The outcome revealed evidence of cointegration in the two models, since the F-statistics (5.48) and (5.25) are greater than the lower- and upper-bound critical values.

In order to verify the outcomes of the ARDL bounds test, the current study utilized Bayer–Hanck combined cointegration test as a robustness check.

Table 6 illustrates the result of the Bayer–Hanck [

91] combined the cointegration test. The findings reveal that, at a 5% level of significance, there is evidence of long-run cointegration amongst the variables used in the two models.

The study also employs the fully modified OLS (FMOLS), dynamic OLS (DOLS) and Canonical Cointegration Regression (CCR) to capture the impact of financial development, urbanization, economic growth, energy consumption and gross capital formation on environmental degradation in Turkey between 1960 and 2016. Furthermore, the present study explored the moderating role of financial development on the long-run impact of financial development, urbanization, economic growth, energy consumption, and gross capital formation on Turkey’s environmental degradation.

The empirical results of the FMOLS, DOLS, and CCR (without financial development as moderator) are depicted in

Table 6. In the first model, the findings from the three long-run estimators revealed (i) a positive connection between CO

2 emissions and economic growth and (ii) a positive connection between financial development and CO

2 emissions. This implies that, keeping other indicators constant, a 1% increase in FD will deteriorate the quality of the environment by 0.0603%, 0.0549%, and 0.2749%, as revealed by the FMOLS, DOLS and CCR, respectively. (iii) Urbanization exerts a positive impact on CO

2 emissions. This implies that a 1% increase in URB will increase CO

2 emissions by 1.1479%, 1.0999%, and 0.8789%, as illustrated by FMOLS, DOLS, and CCR, respectively, keeping other indicators constant. (iv) A positive connection between gross capital formation and CO

2 emissions. This implies that, keeping other indicators constant, a 1% increase in GCF will harm environmental quality by 0.3968%, 0.4051%, and 1.4607%, as revealed by the FMOLS, DOLS and CCR, respectively. (v) Energy consumption exerts a positive impact on CO

2 emissions. This implies that a 1% increase in EN will increase CO

2 emissions by 0.9307%, 0.9196%, and 1.9037%, as illustrated by FMOLS, DOLS, and CCR, respectively, keeping other indicators constant. This study’s findings confirm the significance of all the variables employed as determinants of carbon emission in Turkey between 1960 and 2016. This indicates that the vulnerability of energy consumption, gross fixed capital formation, urbanization, economic growth, and financial development are significant for predicting Turkey’s environmental degradation.

Finally, we tested the moderating effect of financial development, and the results presented in

Table 7 show the result of the long-run estimations with moderating effect (Financial Development). The empirical findings revealed the following: (i) financial development positively moderates the relationship between economic growth and CO

2 emissions; (ii) there is no evidence of the moderating effect of financial development on the relationship between economic growth and CO

2 emissions; (iii) financial development negatively moderates the relationship between gross capital formation and CO

2 emissions; and (iv) financial development negatively moderates the relationship between urbanization and CO

2 emissions. It is worth noting these findings when comparing the coefficients of the variables without financial development as a moderator (

Table 7). Furthermore, when it is added as moderator (

Table 8), GDP, GCF, and URB still maintain their level of significance, but there is a change of sign in the coefficient of GCF and URB, which is an indication that financial development plays a vital role the impact of URB and GCF on CO

2. Thus, the moderating effect of financial development aid URB and GCF in mitigating environmental degradation. Therefore, it should be considered when initiating plans associated with environmental degradation.

In the two models, the R2 values are 0.99 and 0.99 for FMOLS, DOLS, and CCR, showing that 99% of the discrepancy in CO2 emissions can be explained by energy consumption, urbanization, economic growth, gross capital formation, and economic growth.

{kind=link}