Establishing Merger Feasibility Simulation Model Based on Multiple-Criteria Decision-Making Method: Case Study of Taiwan’s Property Management Industry

Abstract

:1. Introduction

1.1. Background Information

1.2. Current Problem Situation

1.3. Objective of This Study and Research Method

2. Literature Review

2.1. Modified Delphi Method

2.2. AHP (Analytical Hierarchy Process)

2.3. Utility Theory and Valuation

2.4. Best Worst Method (BWM)

2.5. Level Based Weight Assessment (LBWA)

2.6. The Full Consistency Method (FUCOM)

3. Materials and Methods

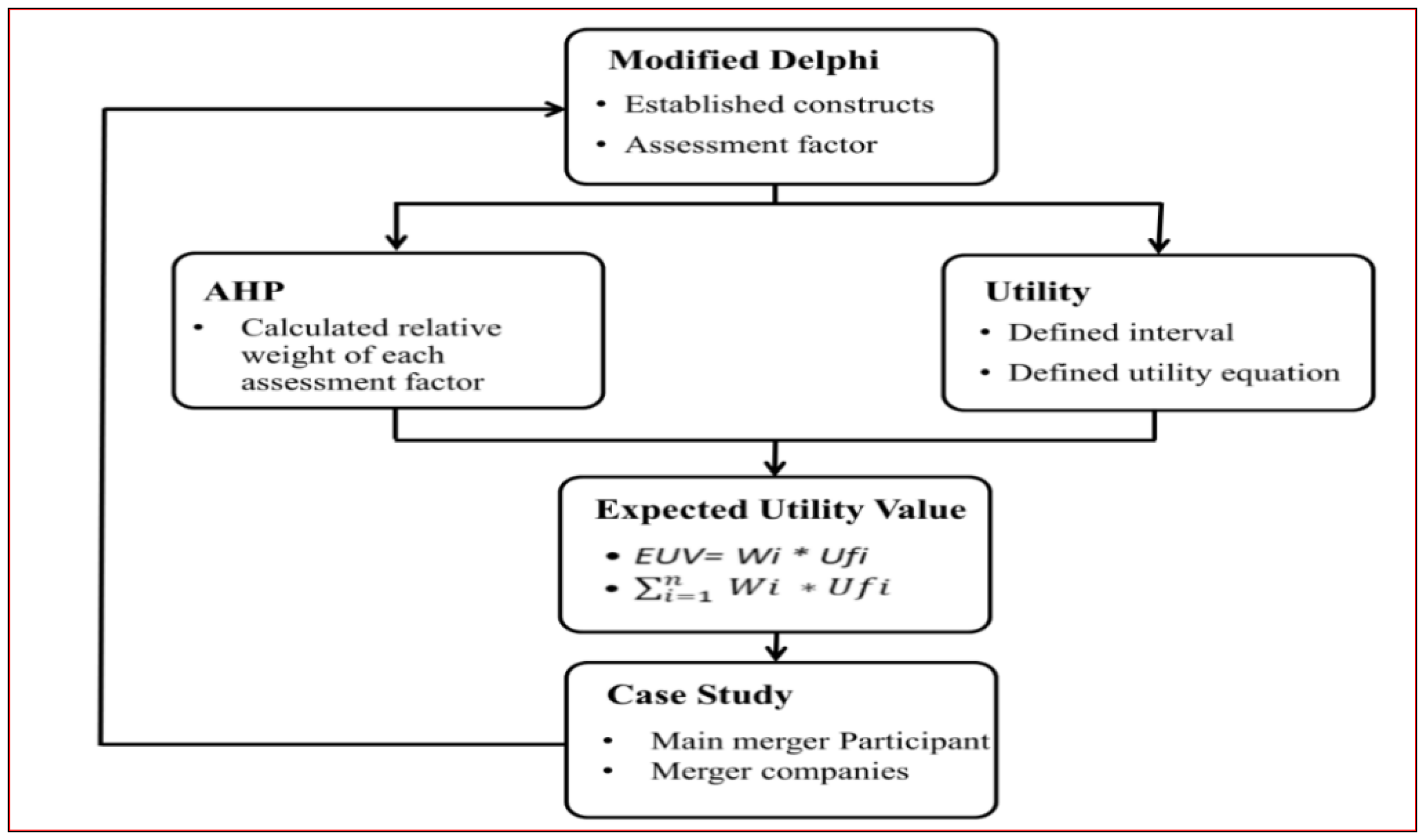

3.1. Construction of the Utility-Based Assessment Model of Merger Feasibilities

3.2. Construction Evaluation Model

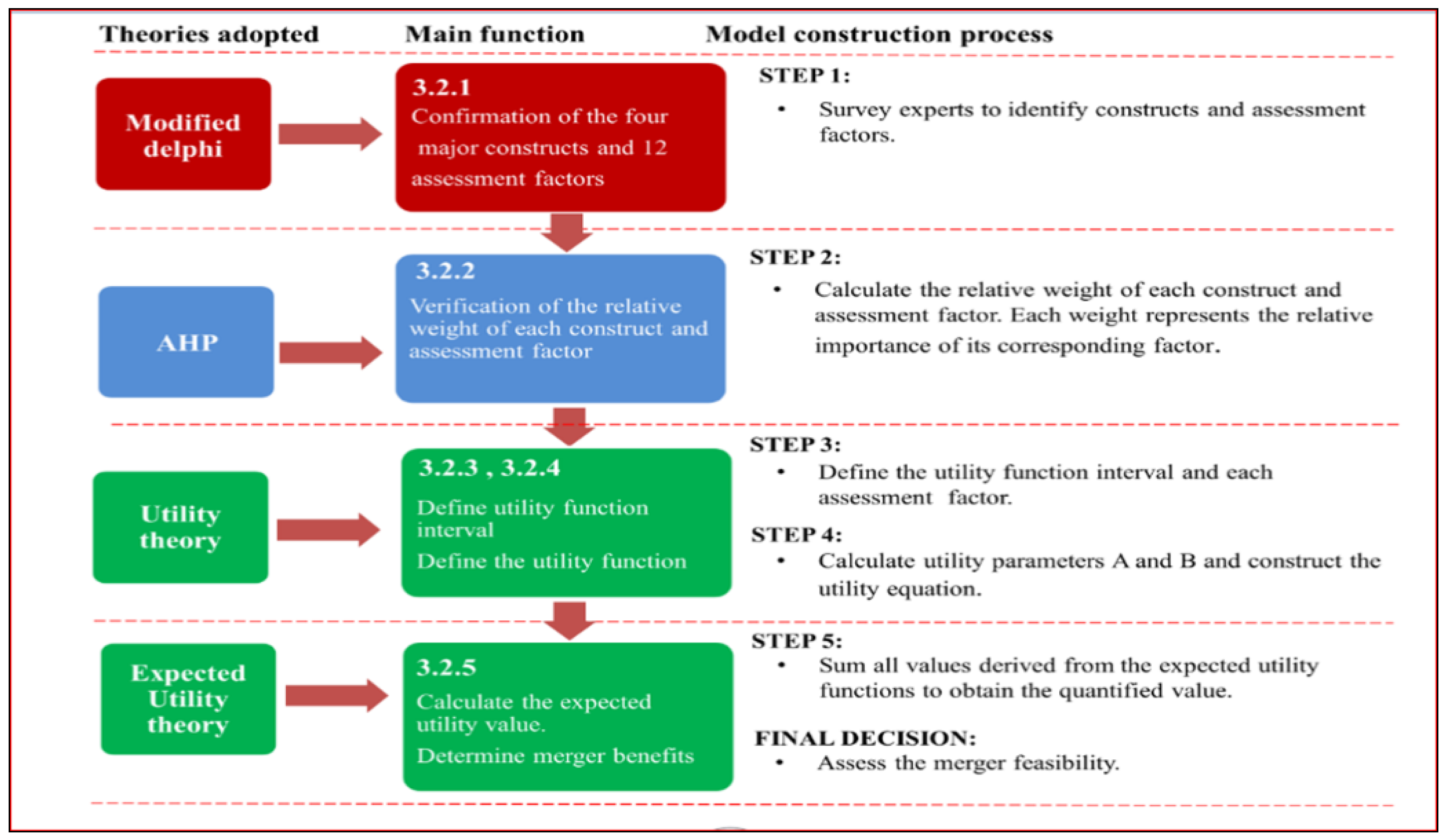

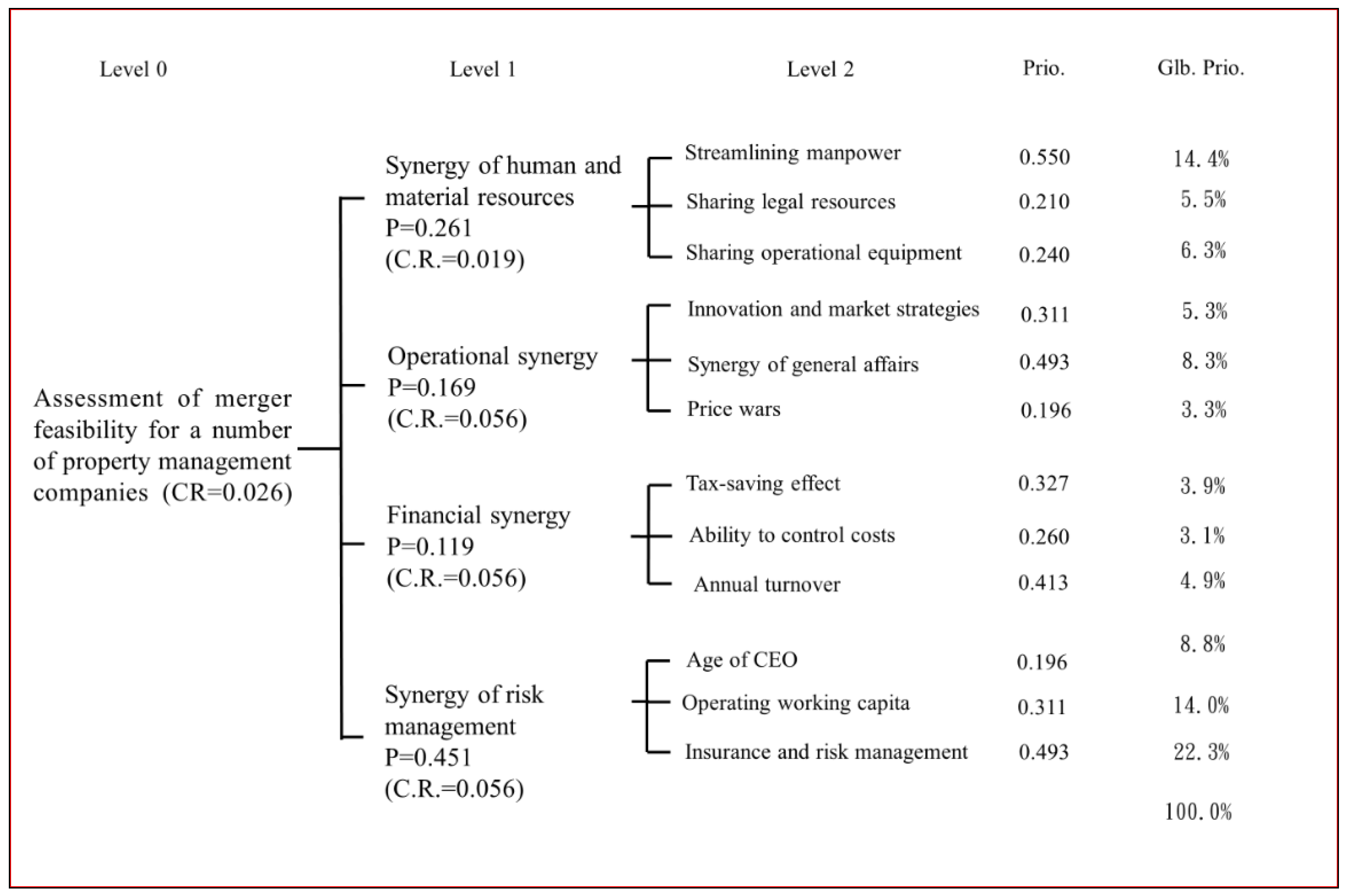

3.2.1. Confirmation of the Four Dimensions and 12 Assessment Criteria

3.2.2. Verification of Relative Weight for Each Dimension and Assessment Criteria

3.2.3. Definition of the Utility Function Interval and Each Assessment Criterion

- The linear utility equation was U(yi) = Ayi + B (items 1 to 12 in Table 2, except for item 10).

- The parabolic utility equation was U(yi) = Ax2 + Bx + C (item 10 in Table 2).

3.2.4. Calculation of Utility Parameters A and B and Construction of the Utility Equation

- The threshold point (yT) and optimal (yM) of each assessment factor were defined.

- 2.

- Parameters A and B of the utility function of merging property management companies were derived, and the utility function equations were constructed.

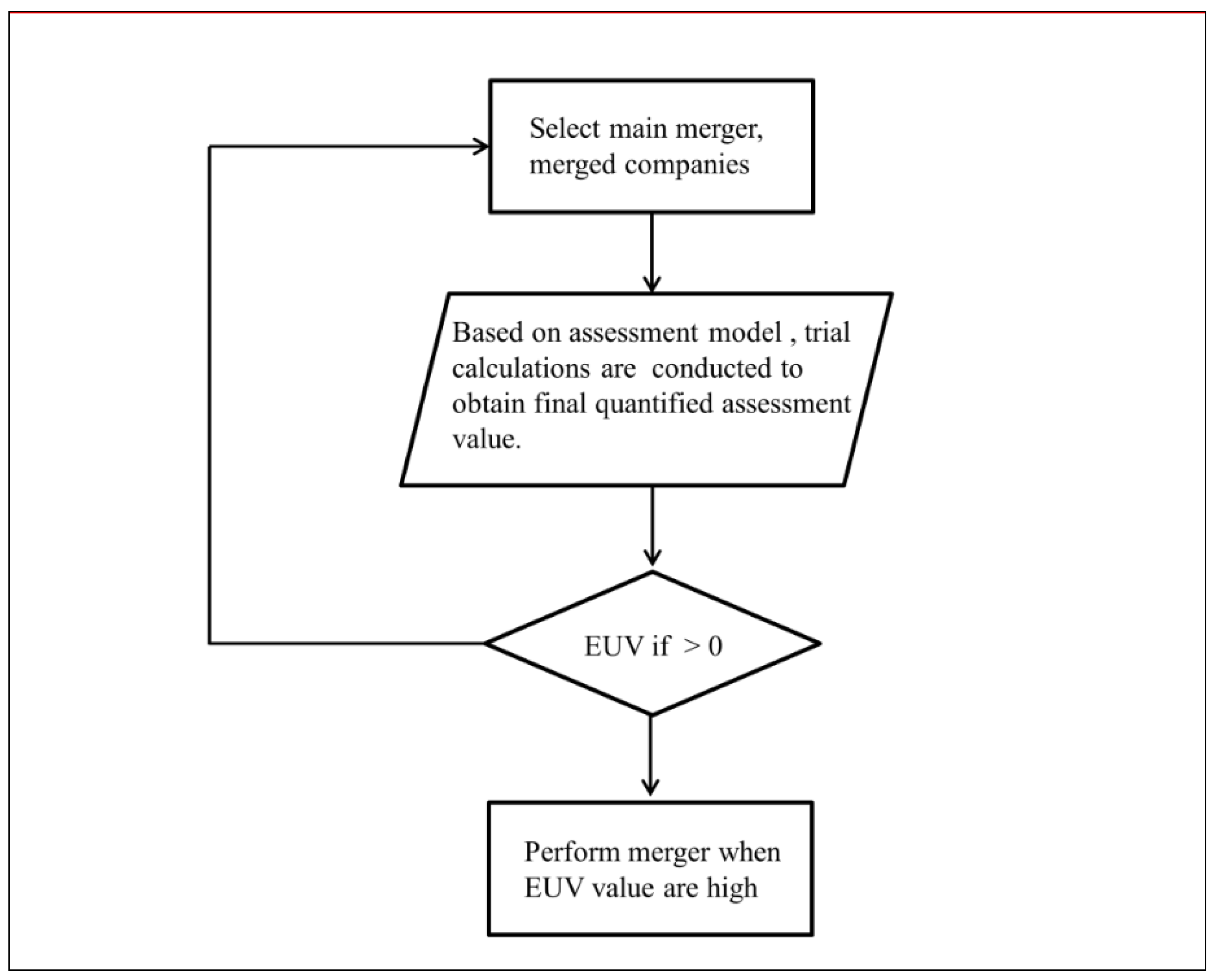

3.2.5. Description of the Final Model and Calculation Method

4. Discussion and Suggestion

4.1. Utility-Based Assessment of Merger Feasibility for Property Management Companies

4.2. Overview of Main Merger and Merged Property Management Companies

4.3. Description of Assessment Results of Merger Feasibility for All Companies

4.4. Suggestions

- In this study, we strongly recommend that the Property Management Association establishes minimum fees to prevent strong competition from reducing profits in the property management industry.

- This study discusses the use of Singapore AHP computing software to obtain the top four relative weights: (1) insurance and risk management (relative weight = 24.1%), (2) operating working capital (relative weight = 15.2%) (3) synergy of human resources (relative weight = 13.8%), and (4) age of CEO (relative weight = 9.6%). The first three relative weighting factors can be controlled and managed internally by the company, whereas the CEO’s age represents a risk of sudden death that cannot be determined or controlled. Accidental deaths of CEOs aged more than 65 years often lead to crises. Therefore, if a CEO is in poor health, the board should attend to the handing over of the company to the succeeding CEO as soon as possible.

- For many companies, adopting a merger operation for competitive survival is arduous. The improper implementation of the initial merger assessment work could ultimately cause the destruction of the company. This research paper is based on years of practical experience and comprehensive academic theory. The paper contributes to the revelation of key factors and an evaluation model for M&A decisions to provide a reference for M&A evaluation.

- The reasons for this paper’s use of a company to implement a company merger instead of a direct merger (capital purchase) are as follows: (i) Given the Taiwanese “like to be the boss” personality, the merger mode allows the boss to stay the same (retaining shares). (ii) Currently, a property management company requires legal capital of USD 1.643 million (NTD 50 million), but the actual capital investment is less than half, so competition with international enterprises is difficult. The source of direct M&A funds poses major problems for these companies. (iii) Tax reduction and tax avoidance effects—Many positive synergies and tax cuts result from the merger. For older business owners, in the case of sudden accidental death, tens of millions of dollars’ worth of estate tax expenses can be avoided.

5. Conclusions

Research Limitations and Future Study

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Porter, M.E. From Competitive Advantage to Corporate Strategy. Read. Strateg. Manag. 1989, 65, 234–255. [Google Scholar] [CrossRef]

- Dimopoulos, T.; Sacchetto, S. Merger activity in industry equilibrium. J. Financ. Econ. 2017, 126, 200–226. [Google Scholar] [CrossRef]

- Jap, S.; Gould, A.N.; Liu, A.H. Managing mergers: Why people first can improve brand and IT consolidations. Bus. Horiz. 2017, 60, 123–134. [Google Scholar] [CrossRef]

- Van De Velde, E.; Vermeir, W.; Corten, F. Corporate social responsibility and financial performance. Corp. Gov. Int. J. Bus. Soc. 2005, 5, 129–138. [Google Scholar] [CrossRef] [Green Version]

- Willebrands, D. A successful businessman is not a gambler. Risk attitude and business performance among small enter-prises in Nigeria. J. Econ. Psychol. 2012, 33, 342–354. [Google Scholar] [CrossRef]

- Ali, M.F. Gains from mergers and acquisitions in Japan. Glob. Financ. J. 2017, 32, 166–178. [Google Scholar]

- Fee, C.E.; Thomas, S. Sources of gains in horizontal mergers: Evidence from the customer, supplier, and rival firms. J. Financ. Econ. 2004, 74, 423–460. [Google Scholar] [CrossRef]

- Chang, Y.B.; Cho, W. The Risk Implications of Mergers and Acquisitions with Information Technology Firms. J. Manag. Inf. Syst. 2017, 34, 232–267. [Google Scholar] [CrossRef]

- Antoniou, A.P.; Zhao, H. Measuring the economic gains of mergers and acquisitions: Is it time for a change? Capco Inst. J. Financ. Transform. 2011, 32, 159–168. [Google Scholar] [CrossRef] [Green Version]

- Lahovnik, M. Strategic fit between business strategies in the post-acquisition period and acquisition performance. J. East Eur. Manag. Stud. 2011, 16, 358–370. [Google Scholar] [CrossRef]

- Ziara, M.M.; Ayyub, B.M. Decision analysis for housing-project development. J. Urban Plan. Dev. 1999, 125, 68–85. [Google Scholar] [CrossRef]

- Douglas, D.; Davis, A.; Wilson, B.J. Strategic buyers, horizontal mergers and synergies: An experimental investigation. Int. J. Ind. Organ. 2008, 26, 643–661. [Google Scholar]

- Comanor, W.S.; Scherer, F.M. The effects of the domestic merger on exports: A case study of the 1998 Korean automobile industry. J. Health Econ. 2013, 32, 106–113. [Google Scholar] [CrossRef]

- Kiker, G.A.; Bridges, T.S.; Varghese, A.; Seager, P.T.P.; Linkov, I. Application of Multicriteria Decision Analysis in Environmental Decision Making. Integr. Environ. Assess. Manag. 2005, 1, 95–108. [Google Scholar] [CrossRef]

- Guo, J.; Zhou, B.; Zhang, H.; Hu, C.; Song, M. Does strategic planning help firms translate slack resources into better performance? J. Manag. Organ. 2018, 26, 395–407. [Google Scholar] [CrossRef]

- Hsueh, S.-L.; Lee, J.-R.; Chen, Y.-L. Dfahp multicriteria risk assessment model for redeveloping derelict public buildings. Int. J. Strat. Prop. Manag. 2013, 17, 333–346. [Google Scholar] [CrossRef] [Green Version]

- Zhu, L. Research and application of AHP-fuzzy comprehensive evaluation model. Evol. Intell. 2020, 1–7. [Google Scholar] [CrossRef]

- Faems, D. Moving forward quantitative research on innovation management: A call for an inductive turn on using and presenting quantitative research. R D Manag. 2020, 50, 352–363. [Google Scholar] [CrossRef]

- Popović, M.; Kuzmanović, M.; Savić, G. A comparative empirical study of Analytic Hierarchy Process and Conjoint analysis: Literature review. Decis. Mak. Appl. Manag. Eng. 2018, 1, 153–163. [Google Scholar] [CrossRef]

- Lund, B.D. Review of the Delphi method in library and information science research. J. Doc. 2020, 76, 929–960. [Google Scholar] [CrossRef]

- Hsueh, S.-L. A Fuzzy Utility-Based Multi-Criteria Model for Evaluating Households’ Energy Conservation Performance: A Taiwanese Case Study. Energies 2012, 5, 2818–2834. [Google Scholar] [CrossRef]

- Watson, K.E.; Singleton, J.A.; Tippett, V.; Nissen, L.M. Defining pharmacists’ roles in disasters: A Delphi study. PLoS ONE 2019, 14, e0227132. [Google Scholar] [CrossRef] [Green Version]

- Fiore, P.; Donnarumma, G.; Falce, C.; D’Andria, E.; Sicignano, C. An AHP-Based Methodology for Decision Support in Integrated Interventions in School Buildings. Sustainability 2020, 12, 10181. [Google Scholar] [CrossRef]

- Dos Santos, P.H.; Neves, S.M.; Sant’Anna, D.O.; de Oliveira, C.H.; Carvalho, H.D. The analytic hierarchy process supporting decision making for sustainable development: An overview of applications. J. Clean. Prod. 2019, 212, 119–138. [Google Scholar] [CrossRef]

- Intharathirat, R.; Salam, P.A. Analytical Hierarchy Process-Based Decision Making for Sustainable MSW Management Systems in Small and Medium Cities. In Sustainable Waste Management: Policies and Case Studies; Springer International Publishing: Singapore, 2019; pp. 609–624. [Google Scholar]

- Janković, A.; Popović, M. Methods for assigning weights to decision makers in group AHP decision-making. Decis. Mak. Appl. Manag. Eng. 2019, 2, 147–165. [Google Scholar] [CrossRef]

- Małecka, M. The normative decision theory in economics: A philosophy of science perspective. The case of the expected utility theory. J. Econ. Methodol. 2020, 27, 36–50. [Google Scholar] [CrossRef] [Green Version]

- Kamaruzzaman, S.N.; Lou, E.C.W.; Wong, P.F.; Wood, R.; Che-Ani, A.I. Developing weighting system for refurbishment building assessment scheme in Malaysia through analytic hierarchy process (AHP) approach. Energy Policy 2018, 112, 280–290. [Google Scholar] [CrossRef]

- Aboutorab, H.; Saberi, M.; Asadabadi, M.R.; Hussain, O.; Chang, E. ZBWM: The Z-number extension of Best Worst Method and its application for supplier development. Expert Syst. Appl. 2018, 107, 115–125. [Google Scholar] [CrossRef]

- Mi, X.; Tang, M.; Liao, H.; Shen, W.; Lev, B. The state-of-the-art survey on integrations and applications of the best worst method in decision making: Why, what, what for and what’s next? Omega 2019, 87, 205–225. [Google Scholar] [CrossRef]

- Žižović, M.; Pamučar, D. New model for determining criteria weights: Level Based Weight Assessment (LBWA) model. Decis. Making Appl. Manag. Eng. 2019, 2. [Google Scholar] [CrossRef]

- Bozanic, D.; Tešić, D.; Milić, A. Multicriteria Decision Making Model with Z-Numbers Based on FUCOM and MABAC model. Decis. Mak. Appl. Manag. Eng. 2020, 3, 19–36. [Google Scholar] [CrossRef]

- Chen, Y.L.; Perng, Y.H.; Lien, H.C. Utility-based multicriteria model for evaluating real estate development projects. J. Environ. Prot. Ecol. 2014, 15, 1328–1336. [Google Scholar]

- Michail, P.; Alexandros, A.; Manthos, V.; George, D. Measuring the Effect of Mergers in Greece with the Use of Financial Ratios: A Bootstrapped Approach. Theor. Econ. Lett. 2018, 8, 3. [Google Scholar]

- Jin, Z.; Xia, B.; Li, V.; Li, H.; Skitmore, M. Measuring the effects of mergers and acquisitions on the economic performance of real estate developers. Int. J. Strat. Prop. Manag. 2015, 19, 358–367. [Google Scholar] [CrossRef] [Green Version]

- Afolayan, A.H.; Ojokoh, B.A.; Adetunmbi, A.O. Performance analysis of fuzzy analytic hierarchy process multi-criteria decision support models for contractor selection. Sci. Afr. 2020, 9, e00471. [Google Scholar] [CrossRef]

- Ishizaka, A.; Labib, A. Analytic hierarchy process and expert choice: Benefits and limitations. ORInsight 2009, 22, 201–220. [Google Scholar] [CrossRef] [Green Version]

- Wu, D.; Yang, Z.; Wang, N.; Li, C.; Yang, Y. An Integrated Multi-Criteria Decision Making Model and AHP Weighting Uncertainty Analysis for Sustainability Assessment of Coal-Fired Power Units. Sustainability 2018, 10, 1700. [Google Scholar] [CrossRef] [Green Version]

- Beiragh, R.G.; Alizadeh, R.; Kaleibari, S.S.; Cavallaro, F.; Zolfani, S.H.; Bausys, R.; Mardani, A. An integrated Multi-Criteria Decision Making Model for Sustainability Performance Assessment for Insurance Companies. Sustainability 2020, 12, 789. [Google Scholar] [CrossRef] [Green Version]

- Lüdeke-Freund, F. Sustainable entrepreneurship, innovation, and business models: Integrative framework and propositions for future research. Bus. Strat. Environ. 2020, 29, 665–681. [Google Scholar] [CrossRef]

- Dalalah, D.; Al-Rawabdeh, W. Benchmarking the utility theory: A data envelopment approach. Benchmark. Int. J. 2017, 24, 318–340. [Google Scholar] [CrossRef]

- Yan, M.-R.; Pong, C.-S.; Lo, W. Utility-Based Multicriteria Model for Evaluating Bot Projects Sep Projektų Vertinimo Modelis Pagrįstas Daugiakriterine Naudingumo Teorija/Sep Projektų Vertinimo Modelis Pagrįstas Daugiakriterine Naudingumo Teorija. Technol. Econ. Dev. Econ. 2011, 17, 207–218. [Google Scholar] [CrossRef] [Green Version]

- Gong, Z.; Zhang, N.; Chiclana, F. The optimization ordering model for intuitionistic fuzzy preference relations with utility functions. Knowl. Based Syst. 2018, 162, 174–184. [Google Scholar] [CrossRef] [Green Version]

- Gregory, J.; Hartman, F.T.; Krahn, J. The Delphi method for graduate research. J. Inf. Technol. Educ. 2007, 6, 1–21. [Google Scholar]

- Dubra, J.; Maccheroni, F.; Ok, E.A. Expected utility theory without the completeness axiom. J. Econ. Theory 2004, 115, 118–133. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Dimension (LEVEL-1) | Influencing Criteria (LEVEL-2) | Description |

|---|---|---|

| The synergy of human and material resources | Streamlining manpower | Labor cost synergy achieved by reducing accounting, human resources, sales, and senior management personnel |

| Sharing legal resources | Cost reduction achieved by sharing legal experience and legal consultants | |

| Sharing operational equipment and material resources | Cost reduction achieved by not investing in redundant furniture, fixtures, and equipment | |

| Operational synergy | Innovation and market strategy | Receptiveness to new management methods and tools, as well as the planning and implementation of business strategies, to achieve market expansion and effectiveness |

| The synergy of general affairs | Streamlining of general affairs personnel and improvement of managerial synergy | |

| Reducing the likelihood of price wars | Prevention of excessive competition and vicious price wars within the industry | |

| Financial synergy | Tax-saving effect | Tax-saving effect resulting from the merger, including accounting fees, business taxes, gift taxes, and property taxes |

| Concept of cost | Whether the directors (e.g., CEOs) of a property management company conduct actuarial calculations of costs every month for effective control | |

| Annual turnover | The annual turnover of each property management company | |

| The synergy of risk management | Aging CEO | The optimal age for the CEO of a property management company is 40 to 55 years. If a CEO is aged over 65 years, succession and decentralization of power to professional managers should be implemented. |

| Sufficient working capital | A company’s operating working capital should be at least USD 0.975 million and ideally USD 3.25 million. The margin of safety is twice the monthly sales total. | |

| Insurance and risk management | Hedging to reduce risks, including investment in corporate hedging programs, labor insurance, national health insurance, and group accident insurance |

| Item | wi × 100% | Assessment Criteria | Worst | Threshold ( U = 0) | Optimal (U = 1) |

|---|---|---|---|---|---|

| 1 | 13.8 | Streamlining manpower | −2.80 | 0.00 | 14.40 |

| 2 | 5.3 | Synergy of legal resources | −1.27 | 0.00 | 5.50 |

| 3 | 6.0 | Sharing of operational equipment | −3.89 | 0.00 | 6.30 |

| 4 | 4.1 | Innovation and market strategy | −1.55 | 0.00 | 5.30 |

| 5 | 8.6 | Synergy of general affairs | −7.35 | 0.00 | 8.30 |

| 6 | 3.0 | Price wars | −3.54 | 0.00 | 3.30 |

| 7 | 3.2 | Tax-saving effect | −0.44 | 0.00 | 3.90 |

| 8 | 2.0 | Ability to control costs | −4.65 | 0.00 | 3.10 |

| 9 | 5.1 | Annual turnover | −3.68 | 0.00 | 4.90 |

| 10 | 9.6 | Age of CEO | 0.00 | 0.00 | 8.80 |

| 11 | 15.2 | Operating working capital | −5.60 | 0.00 | 14.00 |

| 12 | 24.1 | Insurance and risk management | −12.39 | 0.00 | 22.30 |

| 100.0 | EUV | −47.16 | 0.00 | 100.0 |

| Item | Assessment Criteria | Description | Quantitative Unit of Measurement | Quantified Interval | Remarks | |

|---|---|---|---|---|---|---|

| Lower Limit | Higher Limit | |||||

| 1 | Streamlining manpower | Reduction of labor costs through the merger | Percentage | 28.4% | 68.9% | Substantial savings in labor costs achieved by reducing accounting, human resources, sales, and senior management personnel |

| 2 | Sharing legal resources | Reduction of costs through the merger | Percentage | 31.9% | 75.0% | Financial savings achieved by sharing experiences of legal consultants from multiple companies |

| 3 | Sharing operational equipment | Cost synergy of merging material resource and equipment costs | Percentage | 35.5% | 60.4% | Financial savings from not needing to invest in redundant furniture, fixtures, and equipment |

| 4 | Innovation and market strategy | Expanded market share and market power achieved through the merger | Percentage | 36.2% | 75.0% | Receptiveness to new management methods and tools, and planning and implementation of business strategies |

| 5 | The synergy of general affairs | Assessment of synergy of merging general affairs departments | Percentage | 34.9% | 56.4% | Overall synergistic improvement in a property management company’s general affairs department achieved by assessing manpower synergy |

| 6 | Price wars | Reduction of competitive pressure resulting from fewer competitors because of the merger | Percentage | 12.5% | 56.3% | Reduction in price wars because of merger and the resultant reduction in the number of companies operating within the same industry |

| 7 | Tax-saving effect | The tax-saving effect generated by the merger | Percentage | 35.5% | 80.0% | Tax-saving effect resulting from the merger, including accounting fees, business taxes, gift taxes, and property taxes |

| 8 | The concept of cost control | Whether the CEO has the ability to precisely calculate costs | Percentage | 15% | 90% | Whether the CEO of a property management company precisely calculates and effectively controls costs every month: CEOs that perform precise monthly calculations were allotted 100%. CEOs that look at financial reports but do not control costs were allotted 50%. CEOs that do not look at or understand financial reports were allotted 0%. |

| 9 | Annual turnover | Assessment of annual turnover | Annual turnover | USD 0.975 million | USD 3.25 million | The annual turnover of property management companies, where the range was USD 0.975 to USD 3.25 million (1 USD = 30.76 TWD) |

| 10 | Age of CEO | Risk assessment of CEO’s age (25 > 55 > 65) | Age | 25 | 65 | The optimal age for the CEO of a property management company is 40 to 55 years. If a CEO is aged over 65, succession and decentralization of power to professional managers should be implemented. |

| 11 | Operating working capital | Fund flows from business operations | Funds/month | USD 0.0975 million | USD 0.325 million | The operating working capital of a property management company should be at least USD 97,500, preferably at least USD 162,500, and ideally USD 325,000. The margin of safety is twice the total monthly sales. |

| 12 | Insurance and risk management | Corporate hedging program | Percentage | 25% | 95% | Hedging to reduce risks, including whether the company truly invests in a corporate hedging program, labor insurance, national health insurance, or group accident insurance (i.e., whether employees are insured or have no insurance coverage): All employees are insured (100%). Not all employees are insured (0%). Others (50%) such as possession of agricultural insurance or veterans insurance, or employees who are labor union members. |

| Item | wi × 100% | Assessment Criteria | yL | yU | yT | yM | A | B | Utility Function |

|---|---|---|---|---|---|---|---|---|---|

| 1 | 14.4 | Streamlining manpower | 28.4% | 68.9% | 35% | 68.9% | 2.950 | −1.032 | U(y1) = 2.950y1 − 1.032 |

| 2 | 5.5 | Sharing legal resources | 31.9% | 75.0% | 40% | 75.0% | 2.8571 | −1.1429 | U(y2) = 2.8571y2 − 1.1429 |

| 3 | 6.3 | Sharing of operational equipment | 35.5% | 60.4% | 45% | 60.4% | 6.494 | −2.922 | U(y3) = 6.494y3 − 2.922 |

| 4 | 5.3 | Innovation and market strategy | 36.2% | 75.0% | 45% | 75.0% | 3.333 | −1.500 | U(y4) = 3.333y4 − 1.50 |

| 5 | 8.3 | Synergy of general affairs | 34.9% | 56.4% | 45% | 56.4% | 8.772 | −3.947 | U(y5) = 8.772y5 − 3.947 |

| 6 | 3.3 | Price wars | 12.5% | 56.3% | 35% | 56.3% | 4.762 | −1.667 | U(y6) = 4.762y6 − 1.667 |

| 7 | 3.9 | Tax-saving effect | 35.5% | 80.0% | 40% | 80.0% | 2.500 | −1.000 | U(y7) = 2.500y7 − 1.0 |

| 8 | 3.1 | Ability to control costs | 15% | 90% | 60% | 90.0% | 3.333 | −2.000 | U(y8) = 3.333y8 − 2.0 |

| 9 | 4.9 | Annual turnover | 3000 | 10,000 | 6000 | 10,000 | 0.00025 | −1.500 | U(y9) = 0.00025y9 − 1.50 |

| 10 | 8.8 | Age of CEO | 25 | 65 | 25 | 45 | −0.0025 | 0.225 | * U(y10) = −0.0025y102 + 0.225y10 − 4.0625 |

| 11 | 14 | Operating working capital | 300 | 1000 | 500 | 1000 | 0.002 | −1.000 | U(y11) = 0.002y11 − 1.0 |

| 12 | 22.3 | Insurance and risk management | 25% | 95.0% | 50% | 95.0% | 2.222 | −1.111 | U(y12) = 2.222y12 − 1.111 |

| Company | Type | Nature of Business | Manpower | Yearly Turnover | Years of Experience | Age and Educational Level of CEO | Background of CEO |

|---|---|---|---|---|---|---|---|

| Main merger company | Main merger | Security, property management, and cleaning | 150 | USD 1.935 million | 10 | 58, bachelor’s degree | Engineering and business management |

| Case 1 K company | Merged | Security, property management, and cleaning | 110 | USD 1.548 million | 10 | 68, bachelor’s degree | Engineering and business |

| Case 2 T company | Merged | Security and cleaning | 80 | USD 0.967 million | 15 | 58, high school graduate | General business |

| Case 3 G company | Merged | Security, property management, and legal affairs | 280 | USD 3.87 million | 20 | 56, bachelor’s degree | Law and management |

| Item | wi × 100% | Assessment Criteria | CASE1 K Company | CASE2 T Company | CASE3 G Company | |||

|---|---|---|---|---|---|---|---|---|

| Yi | EUV | Yi | EUV | Yi | EUV | |||

| 1 | 14.4 | Streamlining manpower | 43.78% | 3.73 | 43.24% | 3.50 | 46.62% | 4.94 |

| 2 | 5.5 | Sharing legal resources | 40.10% | 0.02 | 40.10% | 0.02 | 53.86% | 2.18 |

| 3 | 6.3 | Sharing operational equipment | 42.46% | −1.04 | 45.30% | 0.12 | 44.86% | −0.06 |

| 4 | 5.3 | Innovation and market strategy | 47.10% | 0.37 | 50.00% | 0.88 | 47.10% | 0.37 |

| 5 | 8.3 | Synergy of general affairs | 40.00% | −3.64 | 46.98% | 1.44 | 43.49% | −1.10 |

| 6 | 3.3 | Price wars | 31.25% | −0.59 | 31.25% | −0.59 | 31.25% | −0.59 |

| 7 | 3.9 | Tax-saving effect | 50.00% | 0.98 | 54.67% | 1.43 | 59.35% | 1.89 |

| 8 | 3.1 | Ability to control costs | 70.00% | 1.03 | 45.00% | −1.55 | 91.00% | 3.20 |

| 9 | 4.9 | Annual turnover | USD 1.548 million | 2.45 | USD 0.967 million | −3.68 | USD 3.87 million | 4.90 |

| 10 | 8.8 | Age of CEO | 57.00 | 5.63 | 68.00 | −2.84 | 57.00 | 5.63 |

| 11 | 14.0 | Operating working capital | 650 | 4.20 | 200 | −8.40 | 1000 | 14.00 |

| 12 | 22.3 | Insurance and risk management | 80.0% | 14.87 | 55.0% | 2.48 | 90.0% | 19.82 |

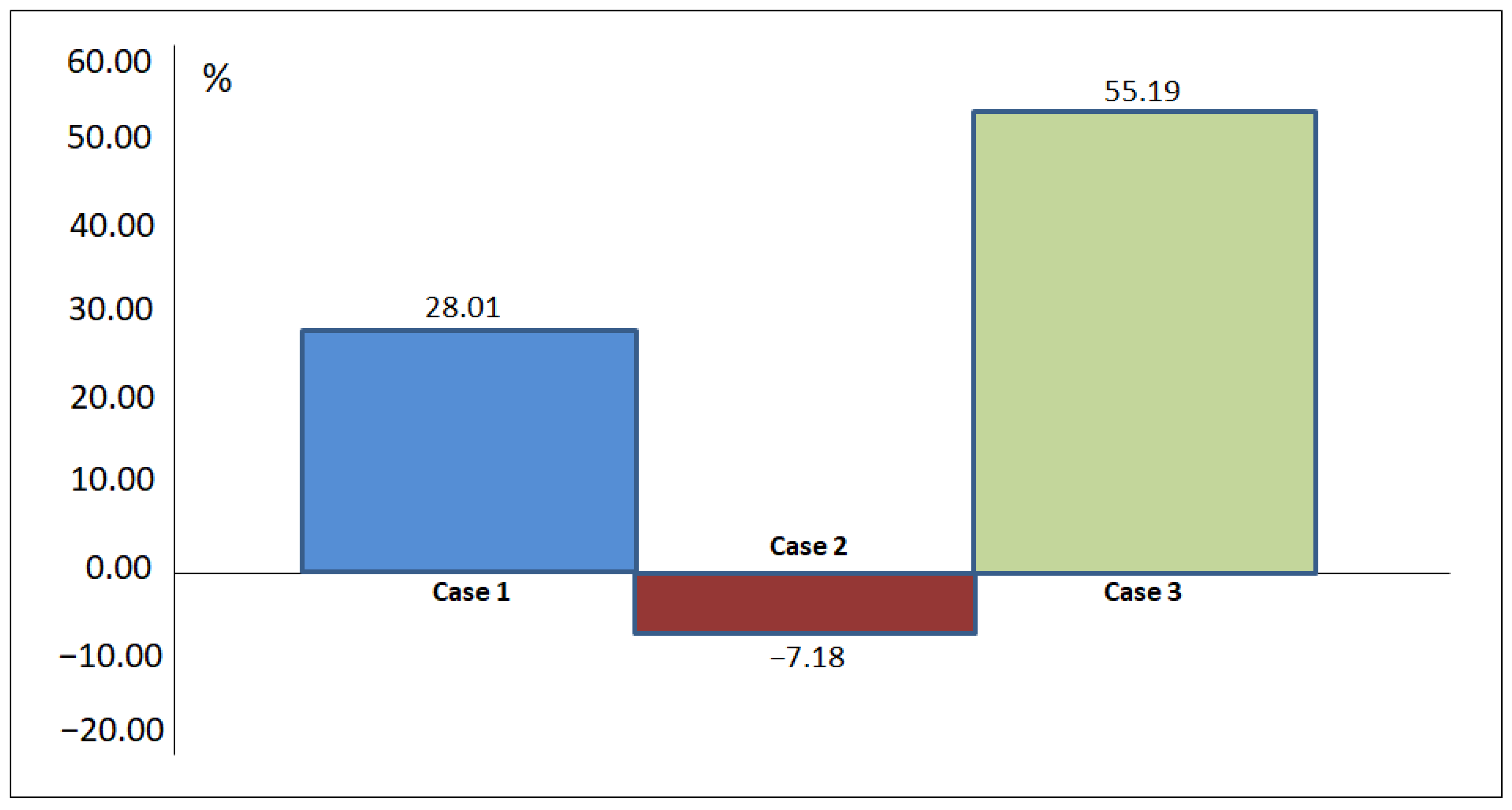

| % | 100.0 | 28.01 | −7.18 | 55.19 | ||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chien, L.-M.; Tu, K.-J. Establishing Merger Feasibility Simulation Model Based on Multiple-Criteria Decision-Making Method: Case Study of Taiwan’s Property Management Industry. Sustainability 2021, 13, 2448. https://doi.org/10.3390/su13052448

Chien L-M, Tu K-J. Establishing Merger Feasibility Simulation Model Based on Multiple-Criteria Decision-Making Method: Case Study of Taiwan’s Property Management Industry. Sustainability. 2021; 13(5):2448. https://doi.org/10.3390/su13052448

Chicago/Turabian StyleChien, Li-Ming, and Kung-Jen Tu. 2021. "Establishing Merger Feasibility Simulation Model Based on Multiple-Criteria Decision-Making Method: Case Study of Taiwan’s Property Management Industry" Sustainability 13, no. 5: 2448. https://doi.org/10.3390/su13052448

APA StyleChien, L. -M., & Tu, K. -J. (2021). Establishing Merger Feasibility Simulation Model Based on Multiple-Criteria Decision-Making Method: Case Study of Taiwan’s Property Management Industry. Sustainability, 13(5), 2448. https://doi.org/10.3390/su13052448