1. Introduction

The financial system dates from 2000 years BCE, although the real boom began as the mercantilist system gained importance in society during the 15th–17th centuries, due to the need to safely store gold and precious metals. The financial system has been defined as the set of regulations, standards, institutions and instruments that operate in and constitute the capital market, with activities mainly concerning savings and consumption, through money supply and demand. This market provides a channel of communication between savers and users, enabling them to allocate capital productively [

1].

Over time, the financial system has undergone increasing competition, provoking the appearance of new strategic applications seeking greater efficiency. In consequence, many financial decisions are now based on locating and retaining elements offering high added value, while those not providing the profitability required by the market are “excluded” from consideration [

2].

Various definitions of financial inclusion have been proposed. According to the World Bank (2014), it refers to the proportion of households and companies that use financial services [

3]. For Amidžić et al. (2014), on the other hand, financial inclusion is the economic state in which no one is denied access to basic financial services for reasons of efficiency [

4]. Demirgüç-Kunt et al. (2013) define it as the use by different groups of formal financial services that benefit people’s well-being [

5]. Sahay et al. (2015) described financial inclusion as the access to and use of financial services at a price that is affordable for the most vulnerable segments of society [

6]. Finally, Sarma (2012) offered a comprehensive vision of the concept, based on the dimensions of accessibility, availability and use of the formal financial system, by all agents within the economy [

7].

Greater access to the financial system increases savings [

8,

9], reduces income inequality and poverty [

10,

11,

12], improves employment levels [

13,

14], favours educational development [

15], helps households make better decisions about the family economy [

16] and facilitates business start-up [

17,

18,

19] (Banerjee et al., 2015; Guiso et al., 2004; Klapper et al., 2006).

A relevant element to promote financial inclusion is governance, which aims to build a global and competitive financial market that reduces transaction costs through innovation and competition, thus promoting true financial inclusion [

20]. Previous literature has identified the need for the participation of two important actors in the financial regulation process: activists and the financial system [

21]. Activists have created or adapted regulatory forms of best practice for developing countries but have failed because they have not taken into account social, cultural, and political institutions [

22,

23]. Similarly, independent action by the financial system has also generated a significant part of the good governance agenda because it has not been linked to local political and institutional realities [

24,

25]. Therefore, both actors must work together in the future to promote the design of a regulatory framework that promotes true inclusion and takes into account the specific needs of the excluded.

Despite the clarity of the concept of financial inclusion, and of its benefits, to our knowledge there exists no commonly accepted method with which to measure financial inclusion, across all economies. Individual proposals that have been made include Honohan (2008), who constructed an indicator based on data from bank accounts and microfinance institutions [

26]; Amidžić et al. (2014), who developed an index including the dimensions of the outreach and the use of the finance considered [

4]; Cámara and Tuesta (2014), whose index was composed of the dimensions of use, access and barriers [

27]; and Sarma (2012), who proposed a multidimensional index of financial inclusion that combined the dimensions of accessibility, availability and use [

7].

One of the first instruments used to promote financial inclusion was that of microfinance or microcredit. Microcredits are small loans made to persons in situations of economic exclusion. Morduch (1999) stated that microfinance was no longer a promise but a reality [

28], enabling the financial inclusion of over 100 million people each year [

29]. However, even today the real impact of microcredit continues to be questioned [

30], and the sector presents problems, such as mission drift [

31], high interest rates [

32], speculation [

33] and even reimbursement pressures, which can lead to suicide [

34].

One of the criticisms that have traditionally been made to the microfinance sector is that the credit assessment considers qualitative and informal explanatory variables in comparison to the traditional bank, generating higher costs [

35,

36] and barriers to financial inclusion. This led previous works in the literature to consider the evaluation of variables such as financial liquidity management or working capital as explanatory variables for models of borrower default probability. Thus, the greater the ability to recover liquidity, the lower the probability of default. In the case of the allocation (destination) of microcredit, working capital reduces the probability of default, while fixed assets increase due to subsequent depreciation [

37,

38].

A more recent instrument proposed to enhance financial inclusion is that of financial education. According to the OECD, financial education is “the process by which financial consumers/investors improve their understanding of financial products, concepts and risks and, through information, instruction and/or objective advice, develop the skills and confidence to become more aware of financial risks and opportunities, to make informed choices, to know where to go for help, and to take other effective actions to improve their financial well-being” [

39].

At the international level, financial education is widely recognised as a valuable tool to reduce social exclusion and develop the financial system [

40]. Financial understanding enables people to manage their investments and their savings in a rational way [

41]. In contrast, a lack of financial education can provide an opening for abuses by financial institutions, such as unreasonable commissions, excessive risk in financial operations and, in extreme cases, even fraud [

42].

An adequate awareness of financial education is essential, not only for the established clients of the financial system, but also for persons currently experiencing financial exclusion and for young people. Hogarth et al. (2002) showed that young people, in general, managed their financial resources poorly, due to the rapid evolution of financial products [

43], deficiencies in their own abilities and the increasing use of technologies in this field [

44,

45].

Financial education is sometimes confused with consumer protection. The former enables consumers to make informed decisions, through training and advice, while the second involves the application of laws and regulations to establish minimum standards of compliance for the financial sector [

39,

46]. The complementarity between these two concepts makes clients aware of the dangers posed by over-borrowing and lack of long-term foresight, whilst ensuring they receive accurate and reliable information [

36].

In general, studies of financial education in different countries, some with developed economies and others still developing, have found that a significant proportion of the population lack financial knowledge regarding concepts in common use such as budgets, savings or inflation [

47,

48,

49]. The implications of this are important, since financial knowledge plays a major role in decision-making.

Finally, new research trends in financial inclusion are focusing on fintech (or digital finance), i.e., the financial services provided via mobile phones, cards or the internet [

50,

51]. In the definition proposed by the Consultative Group to Assist the Poor, digital financial inclusion is the “digital access to and use of formal financial services by excluded and underserved populations” [

52]. Moreover, according to Gmober et al. (2017), it includes a wide range of financial products and businesses, software and innovative ways of interacting with clients [

53].

The main objective of digital financial services is to contribute to poverty reduction and to fostering financial inclusion in developing countries [

54]. The use of digital financial services is dependent on three key components: a digital transaction platform, retail agents and a mobile phone. The combination of these elements creates a highly effective tool for the rapid promotion of financial inclusion, on a global scale.

Among the many benefits offered by digital finance are: (a) the significant contribution it makes to financial inclusion, extending financial services to non-financial sectors and making basic services available to a wider public, since 50% of the population in developing countries own a mobile phone [

55]; (b) increased GDP, thanks to the credit facilities extended to retailers, SMEs and large companies [

56]; (c) enhanced performance of the banking system [

57].

Despite these advantages, the acceptance and use of the mobile phone for financial purposes remains limited compared to cash systems [

58]. Mobile money has inherent risks that could lead to the loss of financial assets [

59], making some people wary of using the virtual dimension of digital transactions [

60].

Most of the literature on fintech has focused on the potential benefits of innovation [

61,

62,

63], while few studies have analysed the actual use of this technology. One such, however, is Narteh et al. (2017), who examined behavioural intentions regarding the use of mobile money services in Ghana [

63]. However, these authors did not analyse perceptions of actual use. Since the intention of use is not reflected in users’ behaviour [

64], further work is needed in this line of research to determine the real impact of digital technology on financial inclusion and on the socioeconomic development [

65].

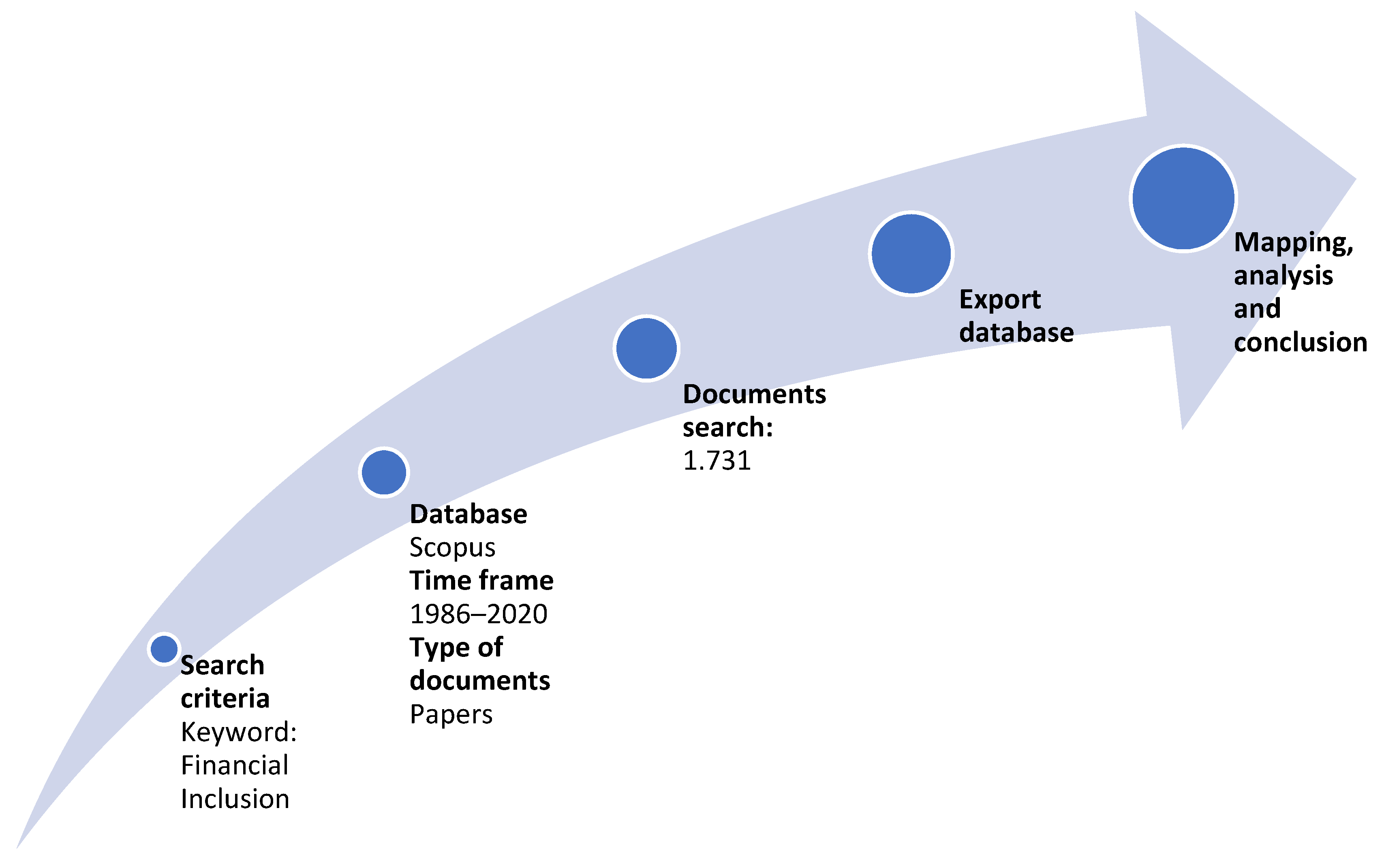

Having clarified the concept of financial inclusion and described some of the instruments that have been applied in this respect, the main study goal of this paper is to analyse the scientific knowledge generated in this field, to highlight the main research advances that have been achieved to date and to identify knowledge gaps, trends and future lines of research.

3. Results

3.1. Evolution of Scientific Output

This section presents the scientific output in the field of financial inclusion during the study period, including the number of articles published and of authors, countries, citations and scientific journals in question. These data are summarised in

Table 1, where the time horizon is divided into five-year sub-periods to facilitate analysis.

The data show that scientific production increased dramatically during the study period. In the first five years (1986–1990), only four articles in this area were published, but this figure rose exponentially to 1270 in the final five years. This growth was such that the number of articles published in the last five years represents 73.37% of those published during the entire period, thus producing an exponential growth in the number of articles published (see

Figure 2).

From 2006, the growth slope rises sharply. One factor that might account for this change is the 2009 Pittsburgh Summit, at which the G-20 resolved to improve levels of financial inclusion [

74], via joint strategies between central banks and large multilateral agencies such as the International Monetary Fund, the Alliance for Financial Inclusion, the Consultative Group to Assist the Poor and the World Bank, to be implemented through the Universal Financial Access 2020 initiative and related measures. This multinational, multilateral programme would have provoked significant interest among the international scientific community in expanding this area of knowledge.

To our knowledge, prior to 1986, only Muller et al. (1975) and Perry and Challoner (1979) had studied the concept of financial inclusion [

75,

76], and these papers were basically oriented towards access to health services.

During the study period, a total of 3831 authors published research articles on the subject of financial inclusion, in a growth pattern that mirrored that of the articles. Thus, the number of authors with articles published in the last five years considered (2016–2020) represents 69.56% of the total. The average number of authors per study also increased during the study period, from 1.3 in 1986–1990 to 2.1 in 2016–2020.

A similar pattern was observed in the number of countries that have contributed to the development of this research line, which rose from just one country in the first five years to 133 during the last sub-period. Significantly, since 2006–2010 this number has doubled in each subsequent period, which highlights the growing interest among the international research community in the subject of financial inclusion.

The number of citations to related work also increased considerably, from none at all in the first five years to 7434 in the last, among a total of 11,022 during the entire period analysed. In parallel, there has been a corresponding increase in the average number of citations per article. Throughout the period 1996–2010 this value remained above 12. Although it fell to 5.85 during the last five years, this is probably because the papers appearing most recently will, for this very reason, receive fewer citations.

Finally, and as with all the other indicators, the number of journals increased significantly. During the period 1986–1990, articles on financial inclusion were published in only four journals, while in the final five years considered (2016–2020), 588 journals were active in this respect. In total, 940 journals published one or more articles on this subject during the entire period analysed.

3.2. Analysis of Scientific Production by Areas: Journals, Authors and Countries

3.2.1. Distribution of Publications by Subject Area and Journal

This section analyses the main thematic areas addressed concerning published research into financial inclusion, illustrating growth trends and identifying the most productive journals in this field.

For the period 1986 to 2020, the bibliometric search identified 24 thematic areas of knowledge addressed in the 1731 research articles extracted from the Scopus database (although some articles could be classified in more than one subject area) [

77].

Figure 3 illustrates the evolution of research interest in each of the five main subject areas identified.

The subject area that was most often studied during the whole period was Social Science, which was addressed in 774 articles (26.60% of the total), followed by Economics, Econometrics and Finance (n = 766; 26.32%), Business, Management and Accounting (n = 469; 16.12%), Medicine (n = 212; 7.29%) and Computer Science (n = 109; 3.75%).

Medicine was the only subject area in which articles were published in each of the sub-periods analysed, while Computer Science, despite being among the five most studied subject areas, was first addressed in the period 2011–2015. For all subject areas, a change in the growth trend was apparent from the same date, and in some cases, the change in the slope was highly pronounced.

Table 2 shows the classification of the 20 most productive journals on financial inclusion in the period 1986–2020. Of these, 25% belonged to the first quartile (Q1) of the SJR index in 2019, 40% to Q2, 15% to Q3 and 20% to Q4. However, these 20 journals published only 310 articles (17.91% of the total), which shows that publications in this area of knowledge are widely distributed.

The journals Enterprise Development and Microfinance and Sustainability Switzerland were the most productive (each one publishing 25 articles). Of these publications, Sustainability Switzerland had the higher H-index in this research area (11 vs. 9), higher H-index overall (68 vs. 15), higher SJR index (0.581 Q2 vs. 0.402 Q2) and higher number of articles published during the last five years.

World Development is the journal with the highest number of total citations in research articles published in Financial Inclusion (395), followed by the Journal of African Business (293), which is why they have the highest number of average citations (23, 24, and 17.92, respectively). The journal with the worst results is Technological Research, although it has 19 articles published in the Financial Inclusion area but has only 4 citations, giving an average of 0.21 citations per article.

Sustainability Switzerland is the journal with the highest H-index among articles on Financial Inclusion (11), followed by the International Journal Of Social Economics (10), while World Development (164) and Journal Of Development Economics (133) are the only ones with the best results in the journal H-index, with these two journals also having the highest SJR index among the most productive (3.585 (Q1) Journal Of Development Economics and 2.223 (Q1) World Development), while Indian journals International Journal of Scientific and Technology Research and Indian Journal Of Finance have the lowest SJR index (0.12 (Q4) and 0.2 (Q4), respectively).

None of the journals published articles on financial inclusion throughout the study period. The Review of International Political Economy was the latest to arrive, publishing its first article on this subject in 2004. The most recent article, on the other hand, was published by the International Journal of Scientific and Technology Research in 2019. This journal has published 19 articles on financial inclusion in just two years, and is now a major point of reference in this field.

Regarding the geographic origin of the journals considered, 55% are published in Europe, 25% in the USA and 20% in Asia.

3.2.2. Productivity of the Authors

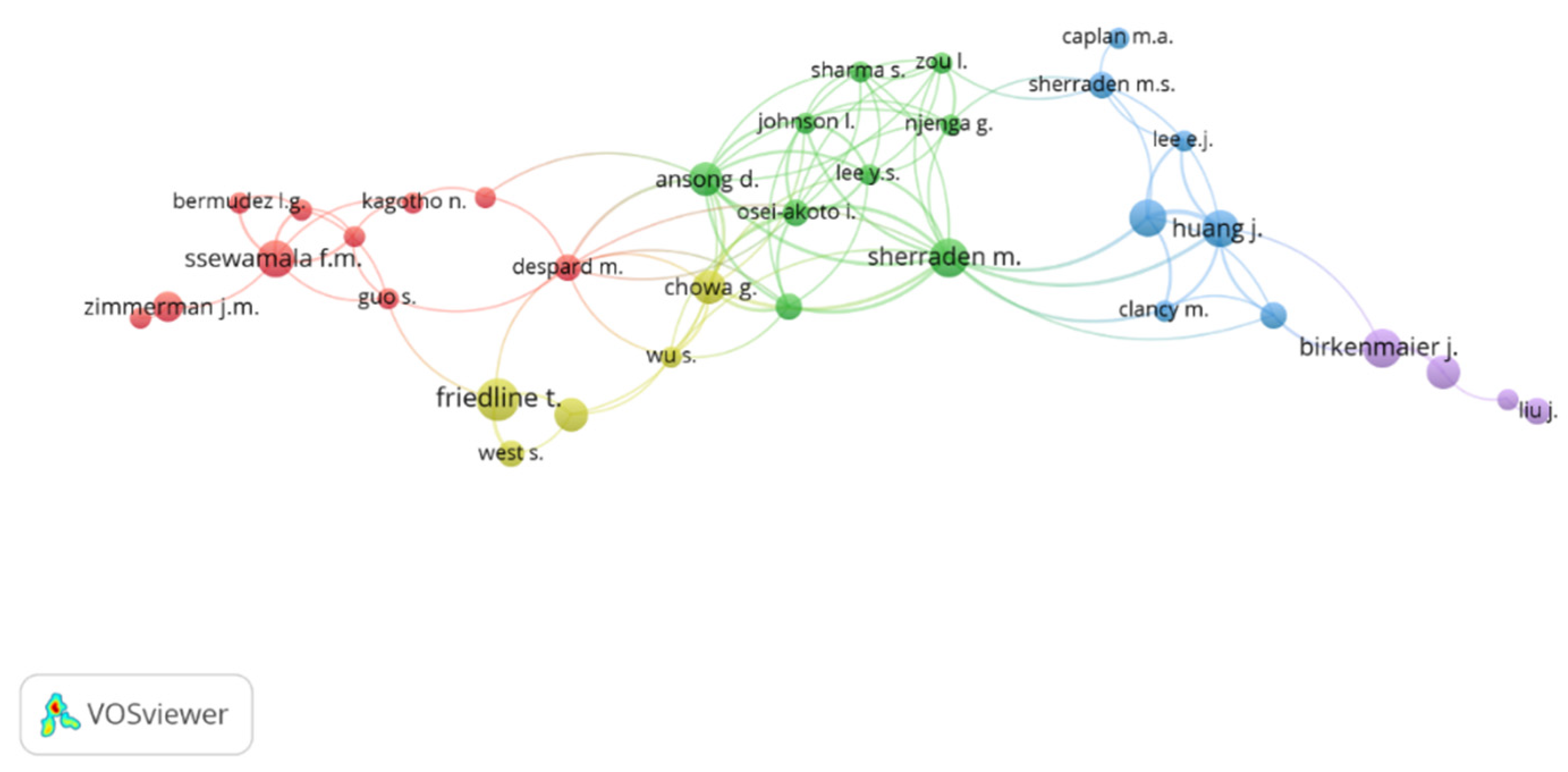

In this section, we focus on the authors’ output, highlighting those who are most productive, showing the main characteristics of their scientific production together with the international cooperation networks that have been created in the field of financial inclusion since 1986. Thus,

Table 3 shows the ten most productive researchers. Interestingly, 60% work in African countries, 20% in Asia and 20% in the USA.

Thus, the most productive researcher in the field of financial inclusion, and the author with the highest number of citations (175), is SA Asongu, from the University of South Africa, with a total of 18 published research articles, followed by JC Munene, from Makerere University in Uganda, with 17 articles. The latter author also collaborates frequently with researchers from the same institution, such as JM Ntayi, CB Okello and CA Malinga.

The earliest appearance in this ranking is that of T Friedline, whose first publication was in 2012. This author also has the highest average number of citations per article (11.38). In contrast, the most recent author is CA Malinga, whose first publication was in 2017. Nevertheless, this researcher has since become one of the most productive among those considered, with eight research articles published. Due to this recent appearance and the large number of articles published, this author has the lowest H index among those calculated for this area of knowledge (1).

Notably, among the ten most productive authors, nine have only been working in the field of financial inclusion for the last five years, which indicates that this question is currently attracting a great deal of attention among the research community.

Figure 4 maps the networks of international cooperation created among the leading researchers in financial inclusion, according to their co-authorship of at least two research papers. The colours represent the working groups established, and the size of the bubbles represent the number of articles published.

The network is widely dispersed, which suggests there is scant international cooperation in this area of knowledge. Five international cooperation clusters were obtained, although of the ten most productive authors presented in

Table 3, only the US researchers J Birkenmaier and T Friedline participated in international cooperation networks. From this we conclude that, in general, researchers in the field of financial inclusion have not created stable networks of international cooperation.

The red cluster is the most numerous and productive, with a total of 10 authors who have published a total of 27 research articles on Financial Inclusion, with Ssewamala, F. being the most prolific author with 6 publications. The green cluster consists of 9 authors who have published a total of 24 research articles with Ansong, D. being the author with the highest number of publications (5). The seven authors who make up the blue cluster also have 24 publications, with Nam, Y. as the most prolific author (6 articles). Five authors integrate the yellow cluster, which has published 23 research articles on Financial Inclusion and is led by Friedline, T. Finally, the purple cluster, led by Birkenmaier, J., has published 17 papers.

3.2.3. Productivity of Institutions and Countries

This section analyses the results obtained for institutions and countries, through indicators such as their productivity, rates of cooperation, collaborative networks based on co-authorship, and international collaborations.

Table 4 lists the ten most productive institutions. As in the case of individual researchers, there is a predominance of institutions located in Africa (50%), followed by 30% in the USA and 10% each in Europe and Asia.

The most productive institution is Makerere University (Uganda) with 27 research articles published on financial inclusion in the period 1986–2020, followed by the University of Ghana (Ghana) and the World Bank (USA), each of which recorded 26 publications.

The institutions with the highest H index (9) are Makerere University (Uganda) and the University of South Africa (South Africa). Although Covenant University and Symbiosis International (Deemed University) have published the same number of research articles as the University of Oxford, Washington University in St. Louis and George Warren Brown School of Social Work, these are the ones with the lower H index (3).

World Bank (USA) has the highest average number of citations per article (22.81), followed by University of South Africa and University of Ghana (7.83 and 7.7, respectively), while Washington University in St. Louis (USA) is the one with the lowest average number of citations per article (3.29) as it has received only 56 citations for the 17 published research articles.

The University of Cape Town presents the highest rate of international cooperation (78.6% of the articles published in this field were developed with international cooperation), followed by the University of Oxford (United Kingdom) (61.5%), and the World Bank (USA) (53.8%). The latter, moreover, has the highest average number of citations per article published with international cooperation (27.21). For the remaining institutions analysed, among those which are most productive, international cooperation rates are below 50%. Notably, the Symbiosis International (Deemed University) (India) has not published any article featuring international cooperation in this field.

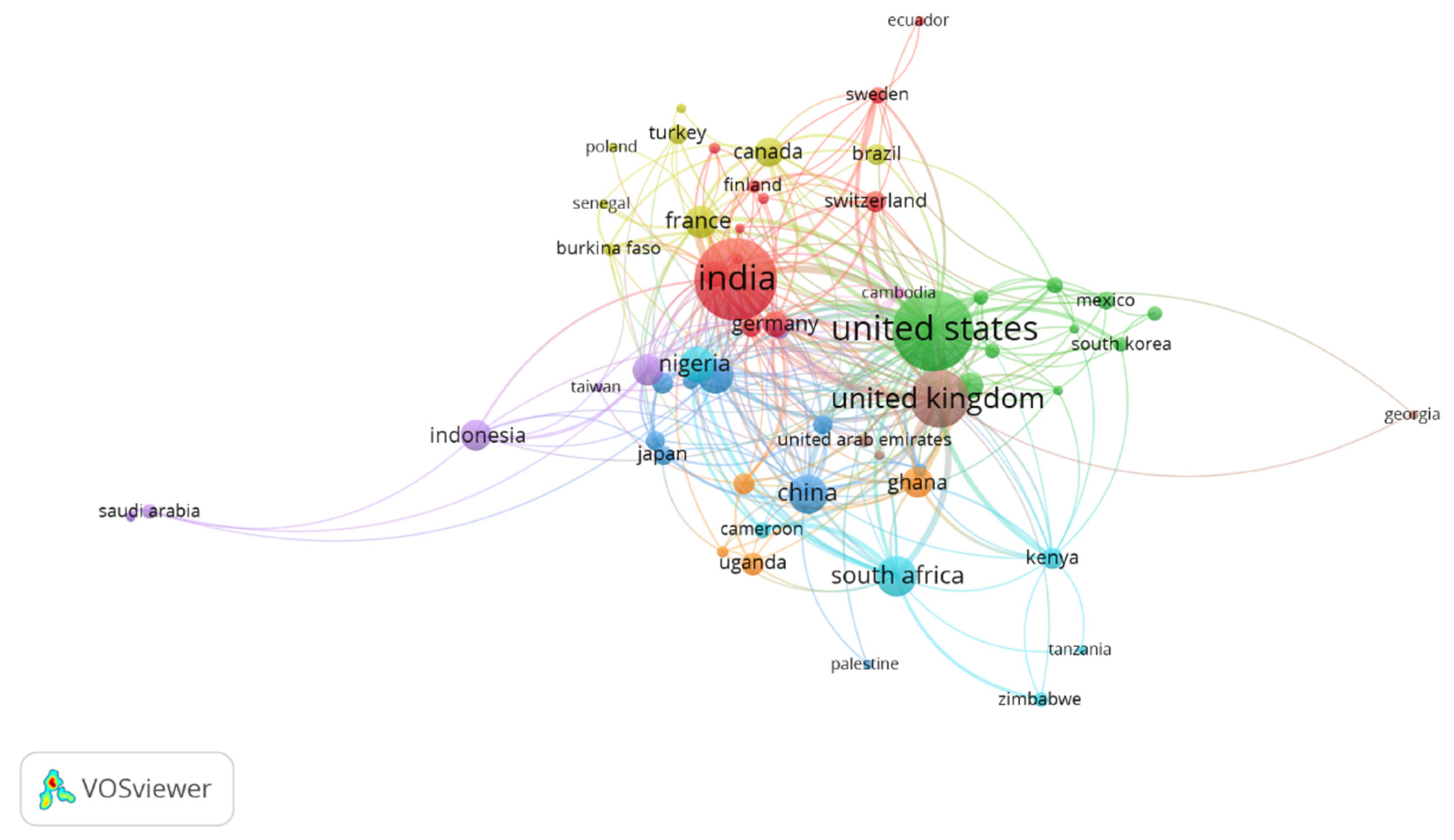

Table 5 shows the results obtained for the ten most productive countries. In this case, the geographic distribution is much more dispersed, although the African countries continue to predominate (40%). Of the rest, 20% of the articles are of Asian origin, 20% are from Europe and 10% each are from the USA and Oceania.

India is the most productive country, with a total of 356 publications on financial inclusion during the period 1986–2020, followed by the USA (347) and the UK (183). The USA, the only country to publish throughout the period, received the highest number of citations (5570), followed by the UK (2462). Only the high number of articles published during the last five years by India (265) displaced the USA from the first position overall, since at every stage of the previous 30 years this was the most productive country.

The USA and the UK have the highest average number of citations per article (16.05 and 13.45, respectively). In consequence, they also have the highest H index scores for publications on financial inclusion (92 and 58, respectively). India ranks between the two countries with an H-index of 77, while, Indonesia, despite being a country with a high number of articles on Financial Inclusion published (52), only has an H-index of 6.

The results for cooperation networks are shown in

Table 6. The largest numbers of international collaborators are based in the USA and the UK (53 and 50, respectively), highlighting the case of Indonesia, which only has 10 collaborators, all of them in addition to the Asian continent (except Australia). However, France has the highest rate of cooperation (63.8%), followed by Ghana (51%), South Africa and Australia, each with 50%. Finally, the UK has the highest average number of citations per article in international cooperation networks (14.14), followed by United States, Australia and China (10.63; 10.41; 10.13). Only the USA, France and Ghana present higher average numbers of citations in domestic publications than in those obtained through international cooperation.

Finally,

Figure 5 shows the collaboration map between the main countries, based on co-authorship, for at least five works published jointly. The colours show the international networks, while the size of the bubbles reflects the number of articles published. In total, eight international cooperation networks are identified.

The red cluster, with thirteen countries, is the most numerous. Led by India, this collaboration network generated 178 research articles (10.28% of the total). The green cluster, led by the USA, is made up of ten countries and is also the most productive, having published 474 articles (27.38% of the total). In third place is the dark blue cluster, led by China and Australia among nine countries in all, with 267 articles published (15.42% of the total). This is followed by the yellow cluster, led by France and made up of eight countries, which generated 174 articles (10% of the total). The purple cluster, led by Indonesia, contains seven countries, which generated 153 articles (8.83% of the total). The light blue cluster, led by South Africa and Nigeria, has six countries and published 209 articles (12.07% of the total). Finally, the orange and brown clusters each contain four countries. The first is led by Ghana and generated 110 articles (6.35%), while the second is led by the UK and has published 202 articles (11.67%).

3.3. Analysis of Keywords

The 1731 research articles on financial inclusion published during the period 1986–2020 contain 2523 keywords.

Table 7 lists the 20 keywords most frequently used, highlighting the topics in this research area considered of greatest significance by the authors.

In this analysis, five subject areas are differentiated. The first broad area “Financial inclusion” reflects the evolution of the main dimensions of this area of study. Although the sub-item Financial inclusion did not appear significantly before 2006, it is included in 760 articles overall, ahead of the related terms Microfinance (in 145 articles), Banking (in 104) and Financial education (in 21), a term that first appears in the period 2011–2015. Accordingly, it is much more recent than the others and is rapidly gaining significance.

Within the area of “Financial System”, the most common expression used is Financial services, which is found in 128 research articles, followed by Financial system (104), as a very generic concept, Credit provision (58) and Financial provision (27).

The “Social Inclusion” dimension refers to financial inclusion as an instrument of social empowerment and access to opportunities. This area of knowledge is related to those of Poverty (included in the keywords of 94 articles), Education (in 36) and Inequality (in 26).

“Technologies” is a line of research that is currently attracting considerable interest among the research community, as shown by the fact that all the keywords in this respect first appear during the last decade analysed (2011–2020). Among these, Mobile money (58) and Fintech (28) have generated the most interest.

In the area of “Development”, the topics most commonly cited are Financial development (45 articles), Sustainability development (34), Developing countries (33) and Vulnerability (15) (although in the latter respect, all of the articles in question were published in 2016 or later).

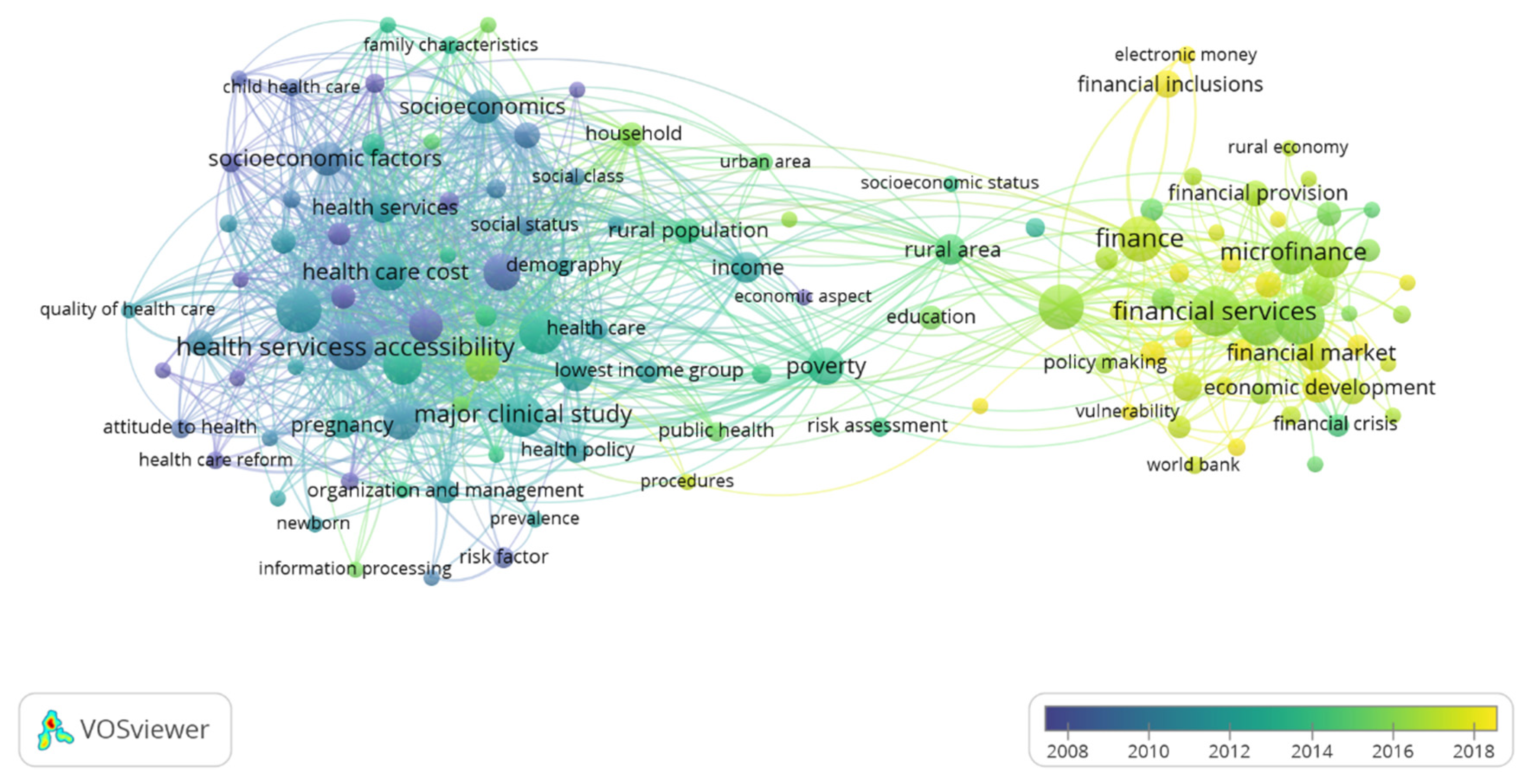

Figure 6 illustrates the relationships observed among the keywords, which are grouped according to co-occurrence. The colour of the clusters shows the keyword networks, while the size of the bubbles varies according to the number of times these expressions are highlighted in the articles. Thus, for the total of 1731 articles, those with at least ten interactions are shown, with 189 keywords.

In the above figure, three main clusters can be distinguished. The largest one, the red cluster, has 56 keywords and refers to research focused on the Financial System. Here, the most frequently used keywords are Financial services, in 128 articles, Financial system (in 104), Developing countries (in 90) and Finance (in 82).

The green cluster is composed of 38 items and relates to the Socioeconomic factors line of research. In this case, the most frequently used keywords are Socioeconomic factors (which appear in 45 papers), followed by Socioeconomics (in 44) and Income (in 37). A strong interrelated line of research with the blue cluster (with 33 keywords) is directly related to the Health factors area of research. In this cluster, the items appearing most frequently are Health services accessibility (observed in 87 articles), Health care delivery (in 83), Health care cost (in 55) and Health care policy (in 53).

Finally,

Figure 7 shows the main research trends according to the evolution of keywords, illustrating the most dynamic areas of research, both current and future.

Clearly, the entire Financial System area of research is attracting a great deal of attention, compared to the other two areas that are identified. Of special importance in this respect are the keywords associated with the use of digital technologies as an instrument to promote financial inclusion, together with those concerning social and sustainable development. This latter association is probably due to the attention drawn to this issue by the UN programme of Sustainable Development Goals.

Finally, in the Socioeconomic Factors line of research, although there are very few topics, significant research activity can be observed regarding the development of the family nucleus (Household and Family Size), while the research line linked to Health Factors seems to be the driver of the concept of Financial Inclusion as an instrument facilitating access to the health system. Nevertheless, at present, to our knowledge, no research papers refer to this sub-line of research in investigations of financial inclusion.

4. Conclusions and Discussion

The aim of this research is to analyse the evolution of the concept of financial inclusion during the period 1986–2020, through a bibliometric analysis of 1731 research articles recorded in the Scopus database, this being the first available bibliometric analysis on Financial Inclusion.

This analysis, focusing on the number of articles published, the authors and co-authors, number of citations, average number of citations per article, and countries and journals of publication shows there has been a generalised increase in research interest in the concept of financial inclusion, especially since 2006–2010, possibly spurred by the 2009 Pittsburgh Summit [

67] and subsequent international initiatives.

SA Asongu was the most productive author, with 18 research articles published. Of the ten most productive researchers, only one had produced a paper on financial inclusion prior to 2016, which highlights the currently rapid expansion of this line of research.

By subject areas, Social Science was most commonly studied during the 1986–2020 period (in 26.60% of the articles published), followed by Economics, Econometrics and Finance (26.32%), Business, Management and Accounting (16.12%), Medicine (7.29%) and Computer Science (3.75%), during the entire period analysed (1896–2020).

Among the journals, Enterprise Development and Microfinance and Sustainability Switzerland published the most articles during this period (25). However, the International Journal of Scientific and Technology Research only began to publish articles in this area of research in 2019, and in just two years it published 19 such articles. The highest average number of citations per article (23.24) was recorded for World Development, which also had the highest H index (164), while Journal of Development Economics had the highest SJR index (3.585-Q1).

Makerere University (Uganda) was the most productive institution in terms of its publication of research articles on financial inclusion (27), while the World Bank had the highest average number of citations per article (22.81). The University of Cape Town (South Africa) presented the highest rate of international cooperation (this was the case in 78.6% of the articles published), while Symbiosis International (Deemed University) (India), despite being among the most productive, only published articles in this field that were authored by domestic researchers.

The country-by-country analysis showed that research institutions in India generated the largest number of research papers on financial inclusion (356), while only those in the United States published throughout the 35-year study period. The highest rate of international cooperation (63.8%) was observed among papers originating in France.

Within the field of financial inclusion, the main lines of research identified were Financial System, Socioeconomic Factors and Health Factors. The first of these is currently generating the greatest interest among the scientific community, while the development of new digital technologies (fintech) as a means of promoting financial inclusion appears likely to attract most research attention in the near future.

Regarding the implications of this proposal, as previously stated, the continuous growth of articles, authors, countries, citations and scientific journals, motivated by the Pittsburg Summit in 2009, has been shown in the last few decades. The Sustainable Development Goals (SDGs) and the 2030 Agenda can motivate practitioners and researchers to broaden their perspectives to address the implications of financial inclusion. In addition, the relevance of the 17 SDGs should be highlighted, which suggests the importance of strengthening the global partnership for sustainable development. Precisely, to understand and measure the suitability of the variety of multiple actors that mobilize and share knowledge and experience, a bibliometric analysis provides clues and establishes links between clusters and relevant lines in the future.

It has been shown that financial inclusion is not a subject of study only in developing countries or exclusively aimed at poor people. Although there is a high presence of authors, institutions, and countries that are considered developing countries, there is also very high participation of actors and institutions from richer countries. Thus, the research article covers the gap of assuming that financial inclusion is only focused on the economic development of emerging countries or people with limited resources but also covers other groups of people present in rich countries, such as the elderly (see, e.g., [

78,

79]), youth (see, e.g., [

80,

81]) or people with disabilities (see, e.g., [

82,

83]). This research article is unique in the literature that shows the main characteristics of research in the Financial Inclusion, identifying the authors, journals, institutions, countries, international cooperation networks and research lines, thus helping the researchers to focus their investigations on current trends in the research field.

This analysis presents certain limitations that should be acknowledged. Firstly, it is a quantitative analysis and does not consider qualitative aspects of the question. Moreover, the use of other software instruments to generate network maps could provide slightly different results. Finally, the use of other keywords, a different study period, research materials other than the articles considered or performance of the search in other databases could all influence the results obtained.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}