Big Data-Based Assessment of Political Risk along the Belt and Road

Abstract

:1. Introduction

2. Literature Review

3. Data and Methods

3.1. Data

3.2. Methods

3.2.1. Choosing the Proper Type of Events—“Material Conflict”

3.2.2. Choosing the Proper Variable—Goldstein Scale

3.2.3. Designing the Proper Measure for Assessing Political Risk

4. Results

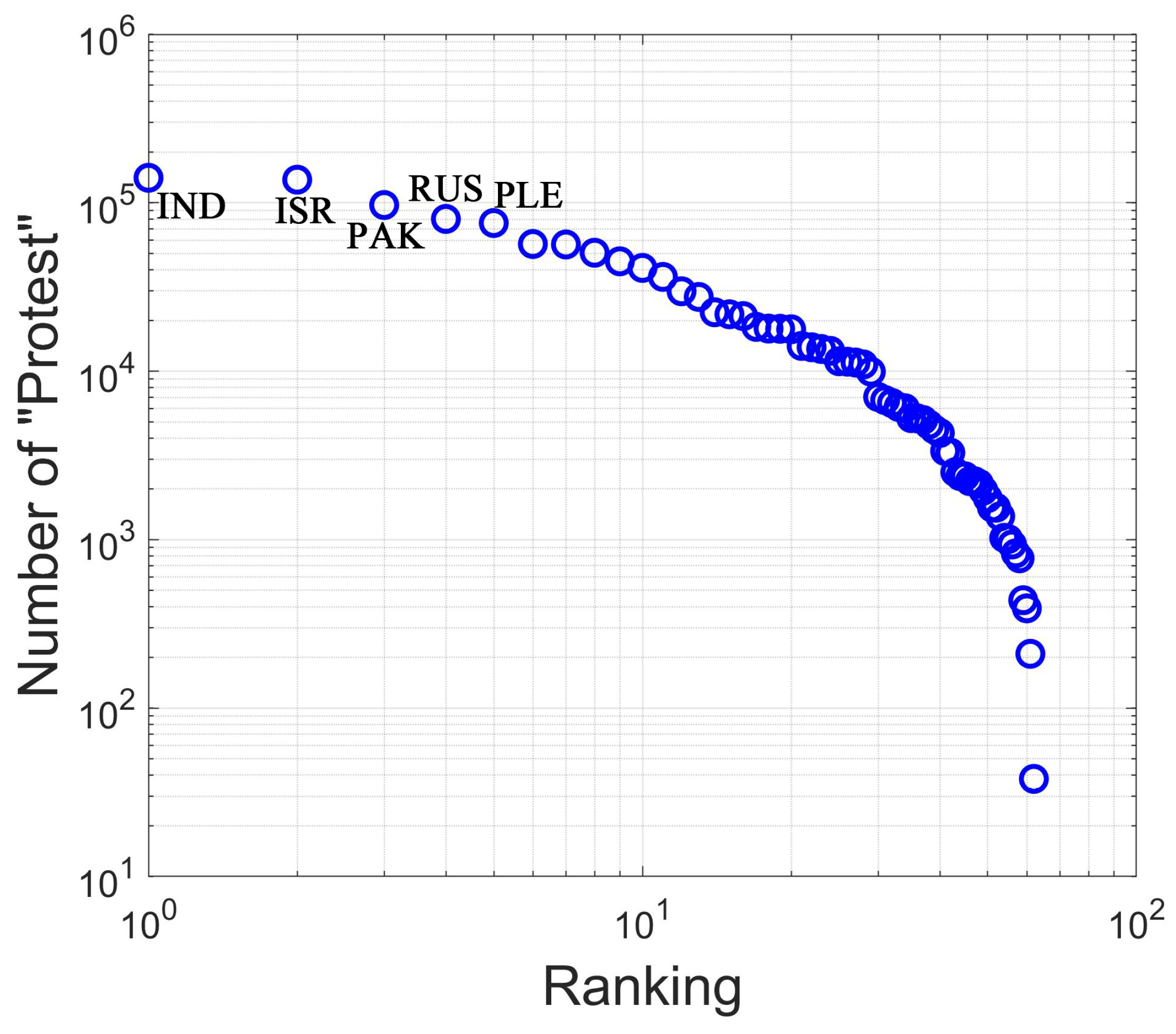

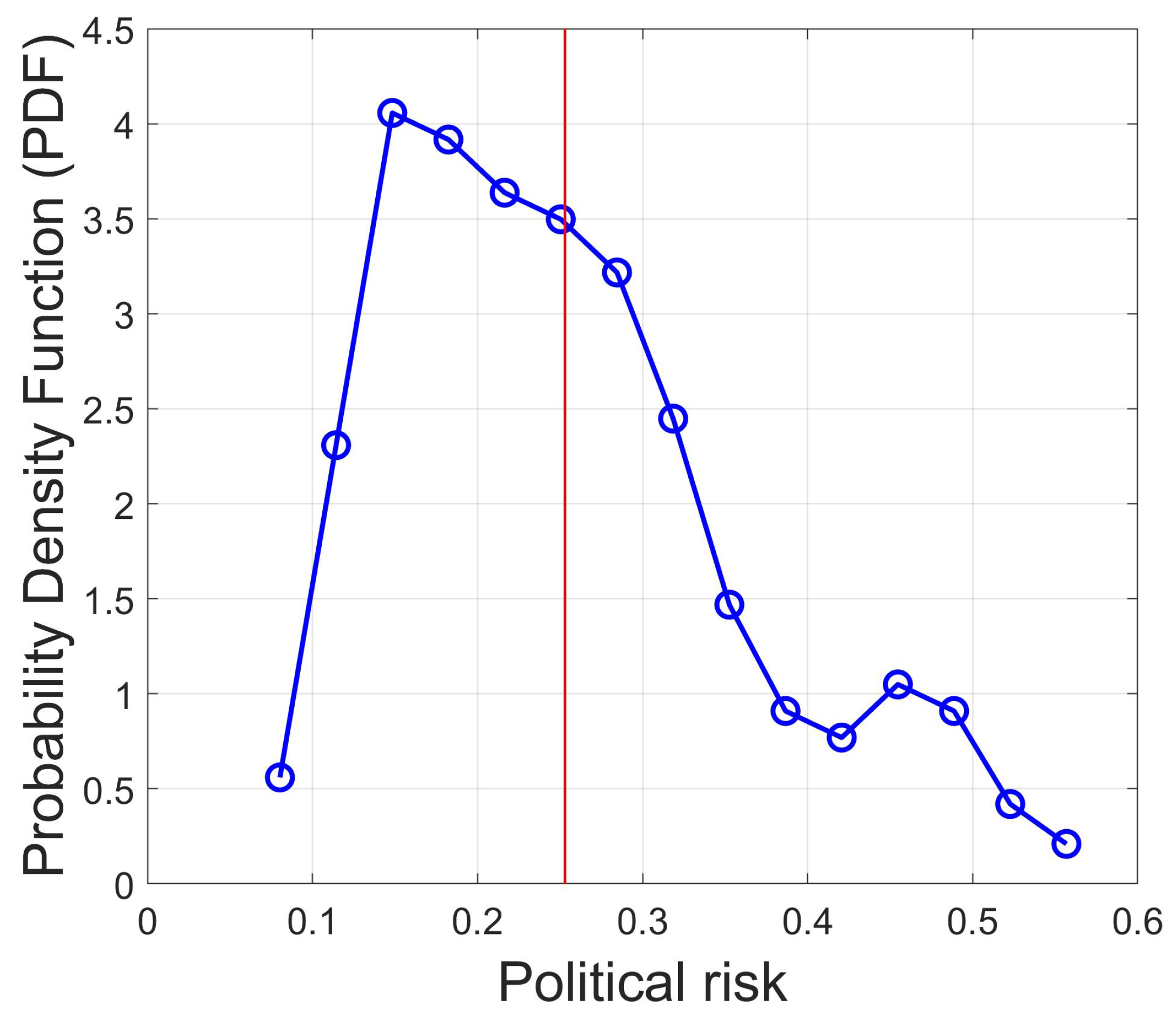

4.1. The Type of Events “Protest” Is Inappropriate to Be Included for Assessing Political Risk

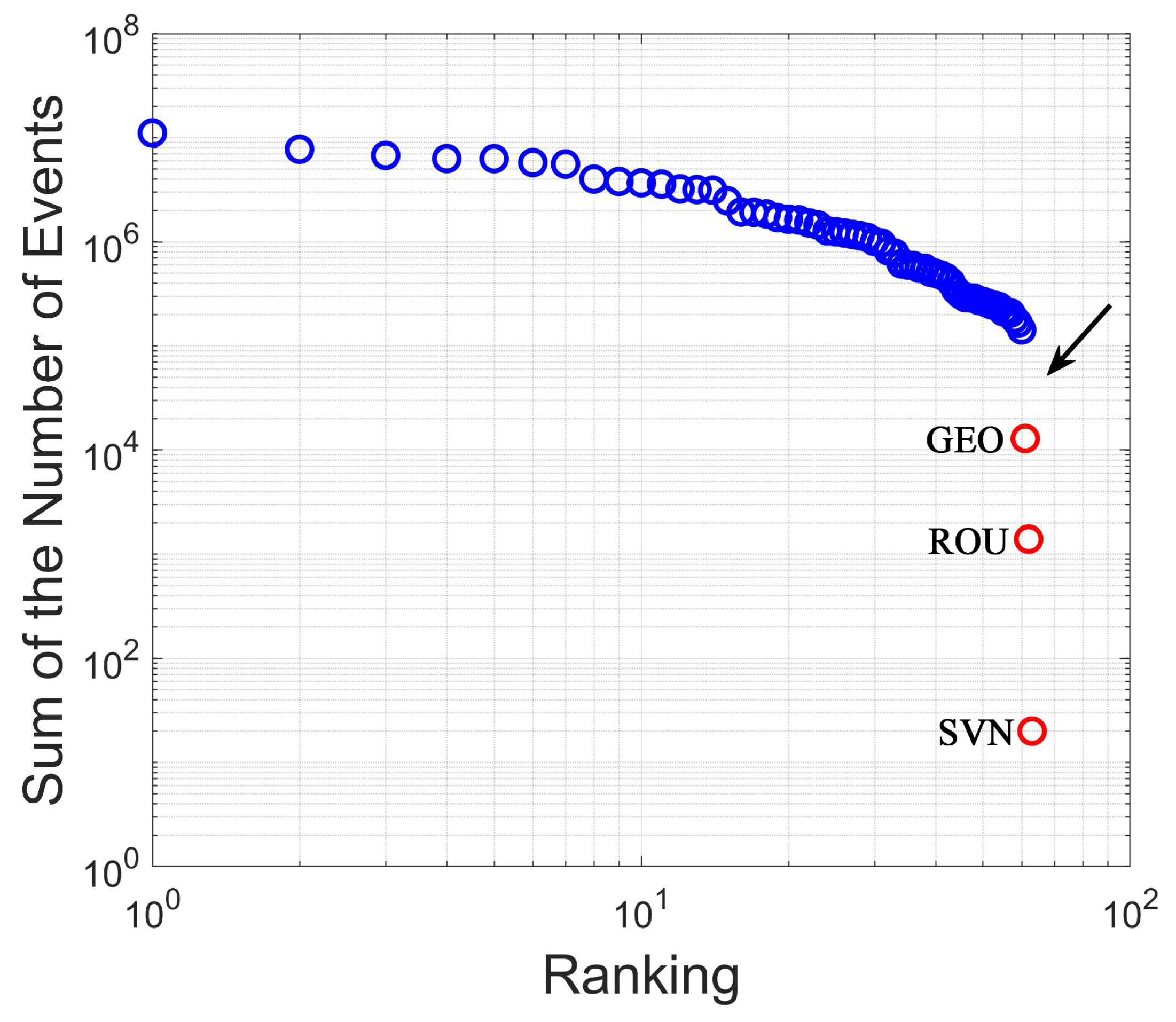

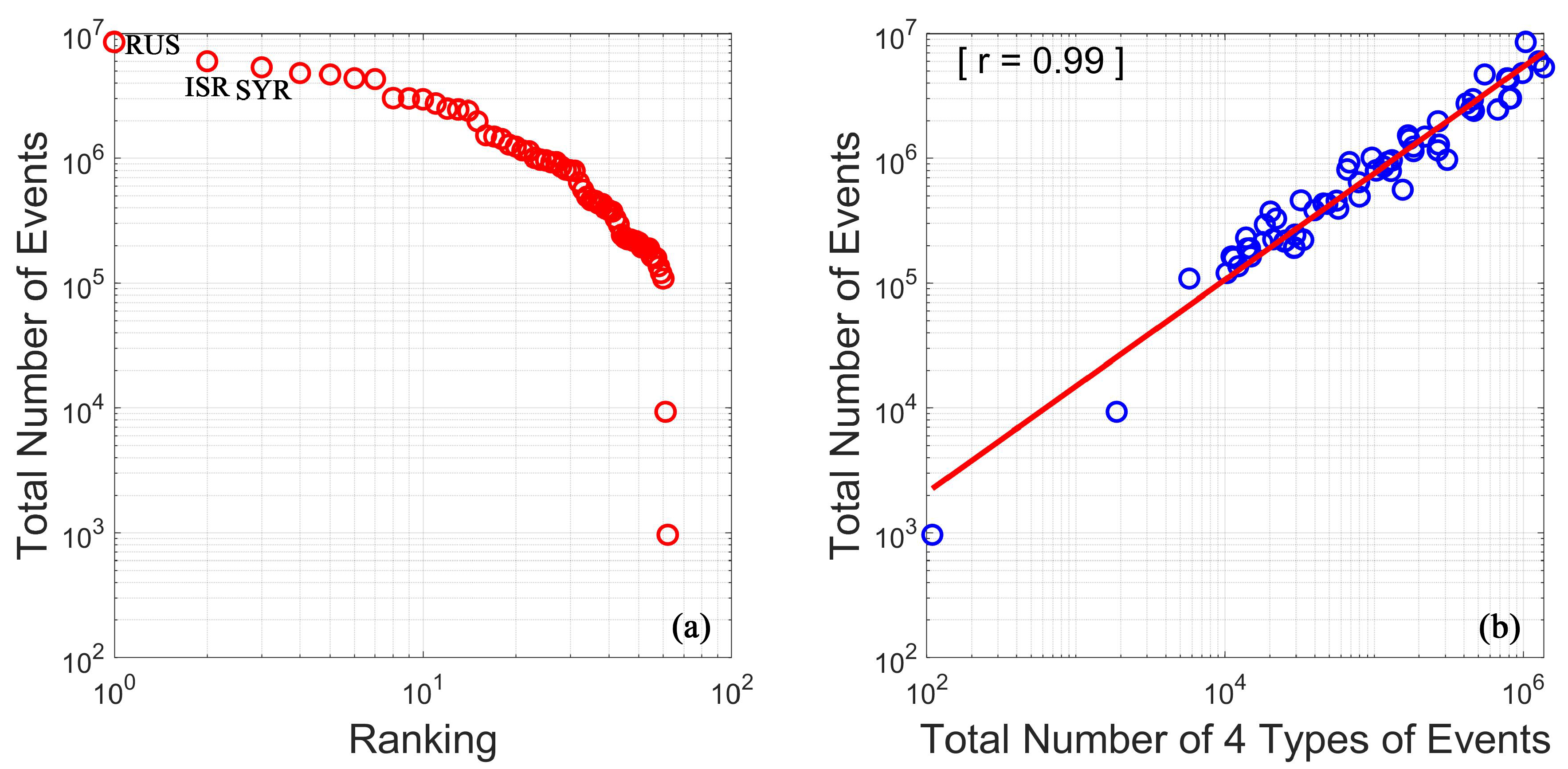

4.2. Using the Number of Events for Assessing Political Risk Is in Appropriate

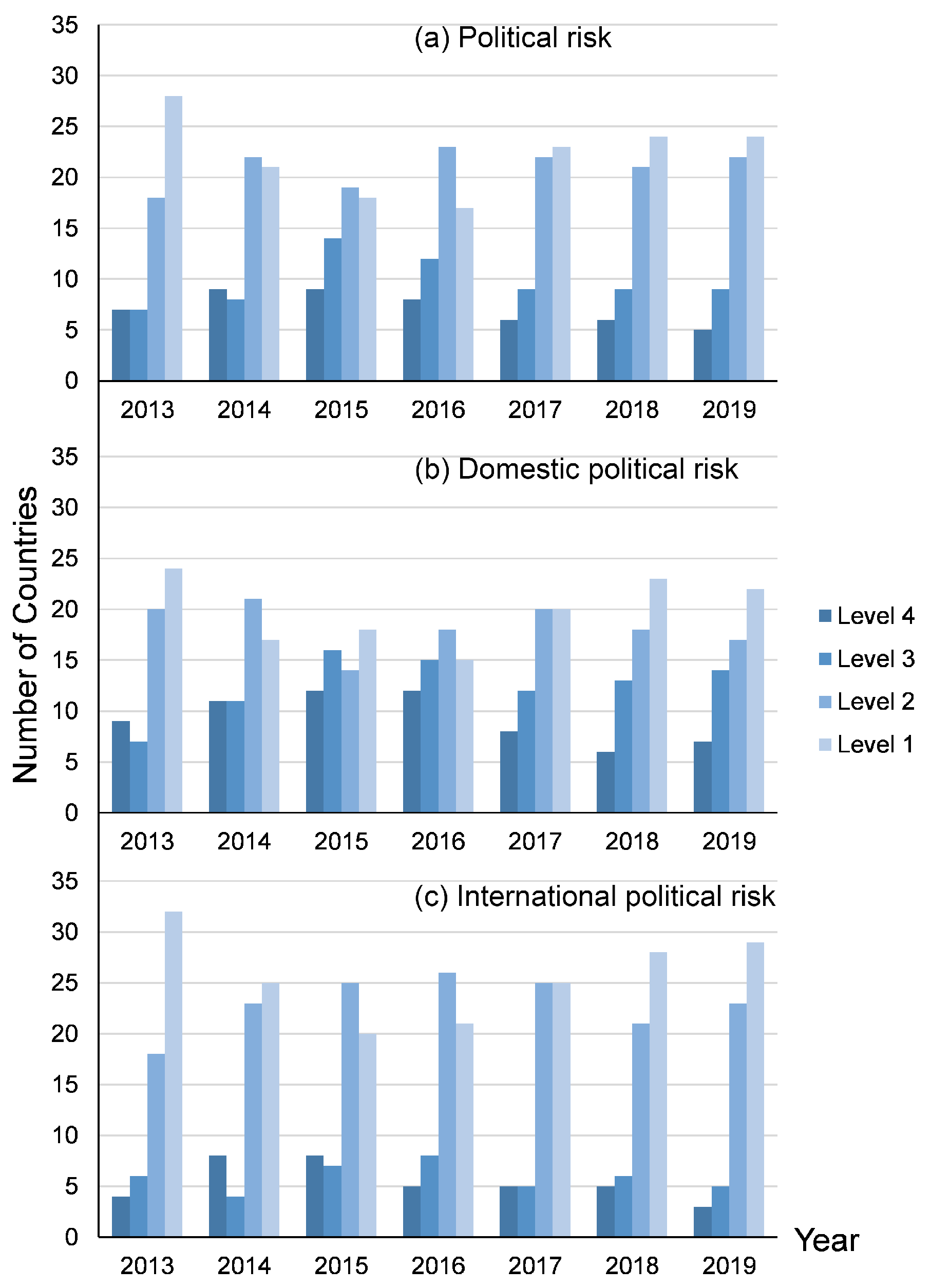

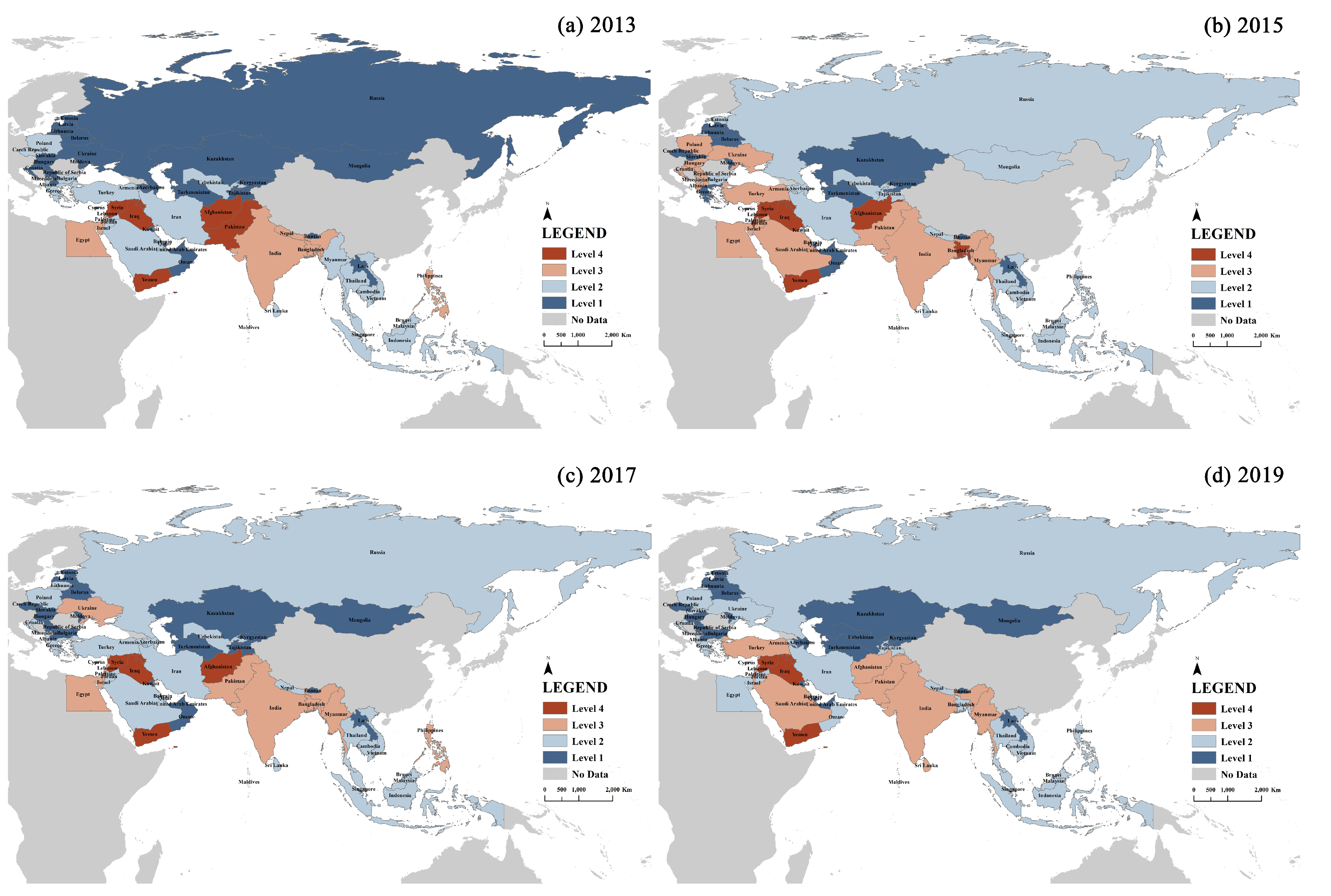

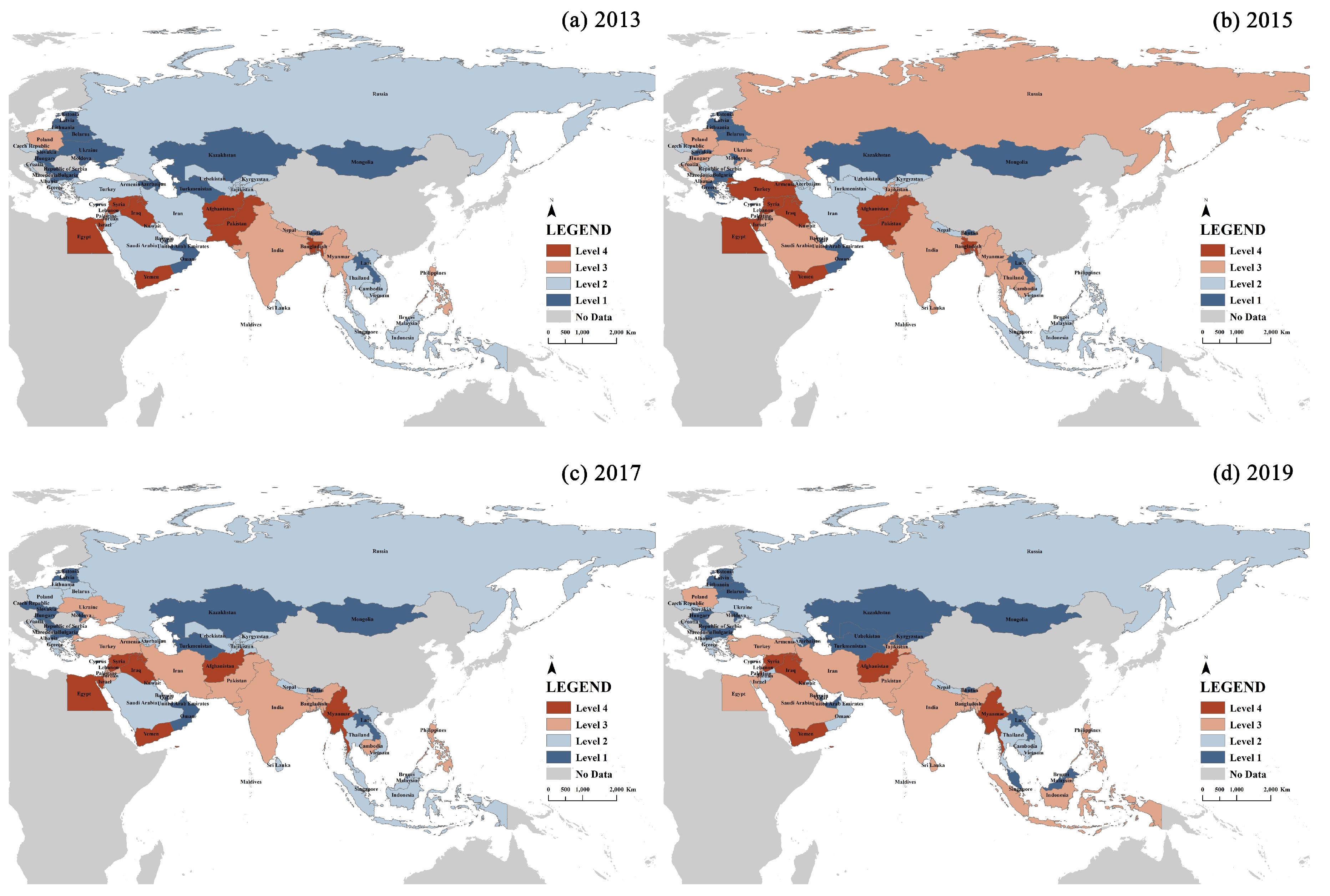

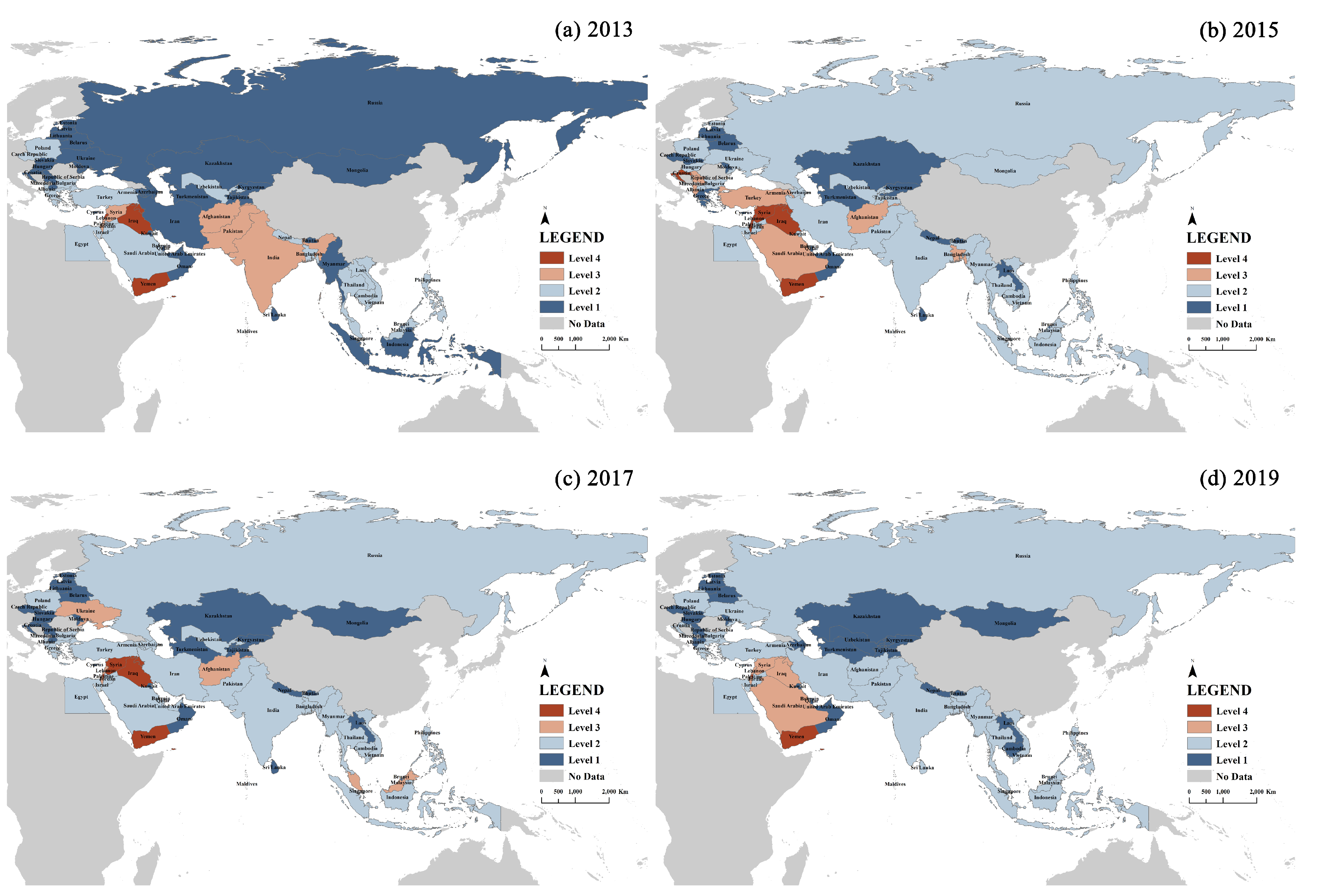

4.3. Spatiotemporal Evolution of Political Risk along the Belt and Road

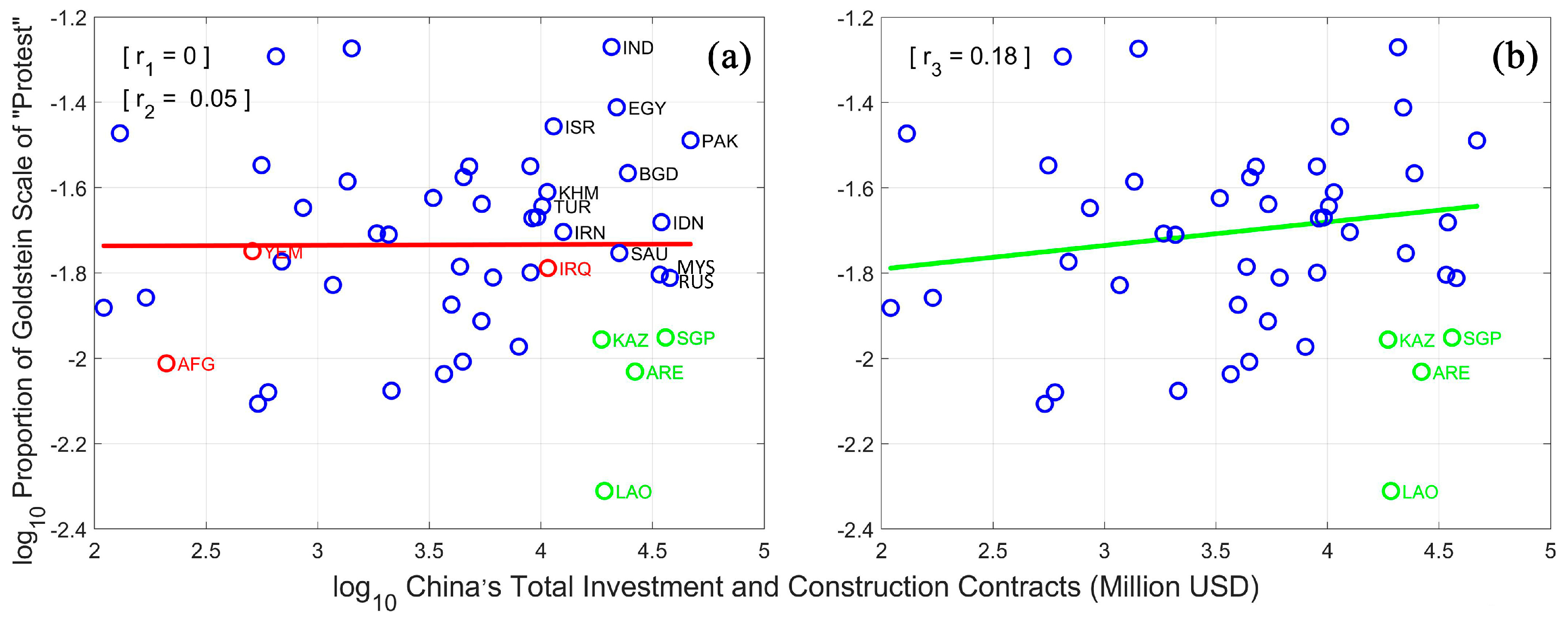

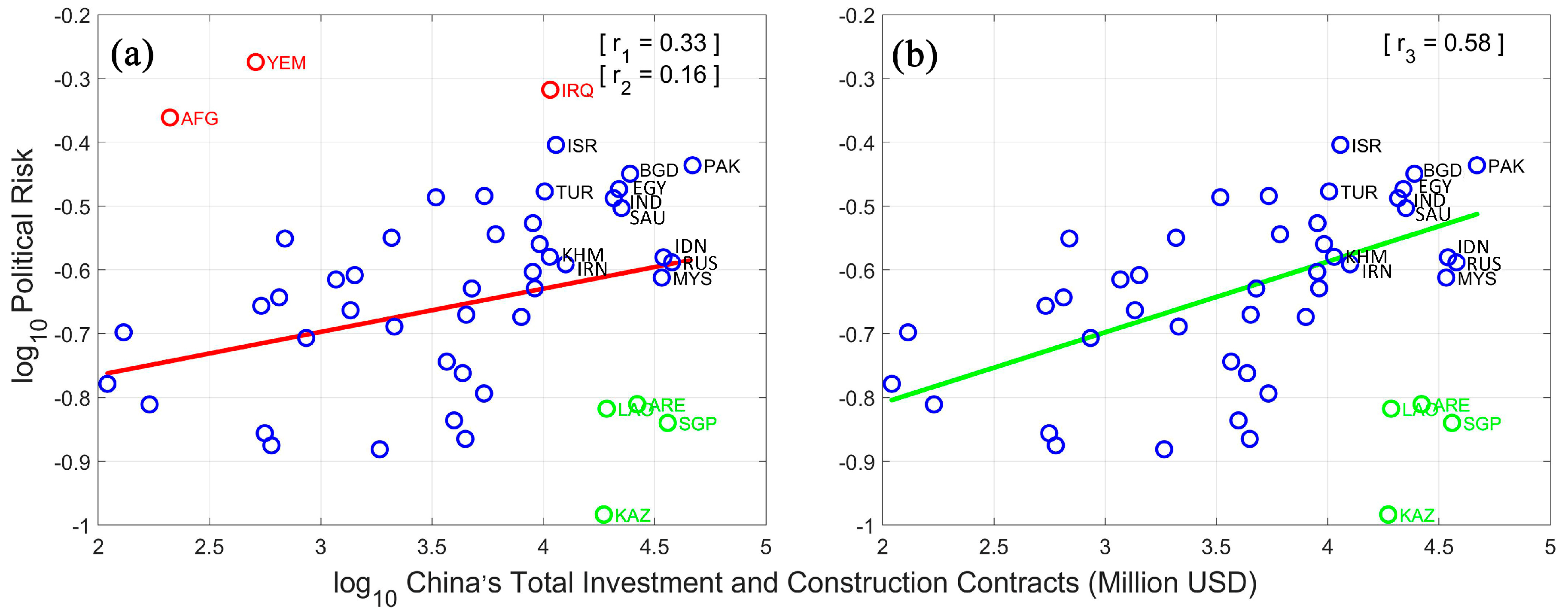

4.4. The Correlation between Political Risk and China’S Foreign Investments and Construction Contracts

5. Conclusions

6. Discussions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Jakobsen, J. Old problems remain, new ones crop up: Political risk in the 21st century. Bus. Horiz. 2010, 53, 481–490. [Google Scholar] [CrossRef]

- Bosley, L.T.C.C. The “New” Normal: Instability Risk Assessment in an Uncertainty—Based Strategic Environment. Int. Stud. Rev. 2017, 19, 206–277. [Google Scholar] [CrossRef]

- Morris, D. Political risk on the Belt and Road. In A Geopolitical Assessment of the Belt and Road Initiative, Proceedings of the 3rd Oriental Business and Innovation Center (OBIC) Conference titled “The V4 in East Asia and East Asia in the V4: Present Economic and Political Relations between the Visegrad Four Countries and East Asia”, Budapest, Hungary, 2–3 May 2019; Moldicz, C., Ed.; Budapest Business School, University of Applied Sciences, Oriental Business and Innovation Center Book Series: Budapest, Hungary, 2019. [Google Scholar]

- Eduardsen, J.; Marinova, S. Internationalisation and risk: Literature review, integrative framework and research agenda. Int. Bus. Rev. 2020, 29, 101688. [Google Scholar] [CrossRef]

- Hussain, J.; Zhou, K.; Guo, S.L.; Khan, A. Investment risk and natural resource potential in “Belt & Road Initiative” countries: A multi-criteria decision-making approach. Sci. Total Environ. 2020, 723, 137981. [Google Scholar] [PubMed]

- Karlis, T.; Polemis, D. The Belt and Road Initiative: A geopolitical risk. In Proceedings of the 27th Annual Conference of the International Association of Maritime Economists (IAME), Athens, Greece, 25–28 June 2019. [Google Scholar]

- Belt and Road Portal, Countries Which have Signed the Belt and Road Initiative Cooperation Documents with China. 2020. Available online: https://www.yidaiyilu.gov.cn/xwzx/roll/77298.htm (accessed on 16 October 2020).

- Ministry of Commerce of the People’s Republic of China; National Bureau of Statistics; State Administration of Foreign Exchange. Statistical Bulletin of China’s Outward Foreign Direct Investment (2019); CHINA COMMERCE AND TRADE PRESS: Beijing, China, 2020.

- Huang, Y.P. Understanding China’s Belt & Road Initiative: Motivation, framework and assessment. China Econ. Rev. 2016, 40, 314–321. [Google Scholar]

- Zeng, L.L. Conceptual Analysis of China’s Belt and Road Initiative: A Road towards a Regional Community of Common Destiny. Chin. J. Int. Law 2017, 15, 517–541. [Google Scholar]

- Liu, W.D.; Dunford, M.; Gao, B.Y. A discursive construction of the Belt and Road Initiative: From neo-liberal to inclusive globalization. J. Geogr. Sci. 2018, 28, 1199–1214. [Google Scholar] [CrossRef] [Green Version]

- Visvizi, A.; Lytras, M.D.; Jin, P.Q. Belt and Road Initiative (BRI): New Forms of International and Cross-Industry Collaboration for Sustainable Growth and Development. Sustainability 2020, 12, 193. [Google Scholar] [CrossRef] [Green Version]

- Shao, Z.Z.; Ma, Z.J.; Sheu, J.B.; Gao, H.O. Evaluation of large-scale transnational high-speed railway construction priority in the belt and road region. Transp. Res. Part E Logist. Transp. Rev. 2018, 117, 40–57. [Google Scholar] [CrossRef]

- Wang, J.J.; Yau, S. Case studies on transport infrastructure projects in belt and road initiative: An actor network theory perspective. Transp. Geogr. 2018, 71, 213–223. [Google Scholar] [CrossRef]

- Du, J.L.; Zhang, Y.F. Dose One Belt One Road initiative promote Chinses overseas direct investment? China Econ. Rev. 2018, 47, 189–205. [Google Scholar] [CrossRef]

- Liu, H.Y.; Tang, T.K.; Chen, X.L.; Poznanska, J. The Determinants of Chinese Outward FDI in Countries along “One Belt One Road”. Emerg. Mark. Financ. Trade 2017, 53, 1374–1387. [Google Scholar] [CrossRef]

- Yu, S.; Qian, X.W.; Liu, T.X. Belt and road initiative and Chinese firm’s outward foreign direct investment. Emerg. Mark. Rev. 2019, 41, 100629. [Google Scholar] [CrossRef]

- Vangeli, A. China’s Engagement with Sixteen Countries of Central, East and Southeast Europe under the Belt and Road Initiative. China World Econ. 2017, 25, 101–124. [Google Scholar] [CrossRef]

- Zeng, J.H. Does Europe Matter? The Role of Europe in Chinese Narratives of ‘One Belt One Road’ and ‘New Type of Great Power Relations’. JCMS-J. Common Mark. Stud. 2017, 55, 1162–1176. [Google Scholar] [CrossRef]

- Flint, C.; Zhu, C.P. The geopolitics of connectivity, cooperation, and hegemonic competition: The Belt and Road Initiative. Geoforum 2019, 99, 95–101. [Google Scholar] [CrossRef]

- Liu, H.; Lim, G. The Political Economy of a Rising China in Southeast Asia: Malaysia’s Response to the Belt and Road Initiative. J. Contemp. China 2019, 28, 216–231. [Google Scholar] [CrossRef] [Green Version]

- Hu, W.; Ge, Y.J.; Dang, Q.; Huang, Y.; Hu, Y.; Ye, S.; Wang, S.F. Analysis of the Development Level of Geo-Economic Relations between China and Countries along the Belt and Road. Sustainability 2020, 12, 816. [Google Scholar] [CrossRef] [Green Version]

- Zhao, S.D.; Wang, X.P.; Hu, X.F.; Li, D.X. Evaluation Research on Planning Implementation of Chinese Overseas Economic and Trade Cooperation Zones along the Belt and Road: Evidence from Longjiang Industrial Park, Vietnam. Sustainability 2020, 12, 8488. [Google Scholar] [CrossRef]

- Pan, C.Y.; Wei, W.X.; Muralidharan, E.; Liao, J.; Andreosso-O’Callaghan, B. Does China’s Outward Direct Investment Improve the Institutional Quality of the Belt and Road Countries? Sustainability 2020, 12, 415. [Google Scholar] [CrossRef] [Green Version]

- Yu, C.J.; Zhang, R.; An, L.; Yu, Z.X. Has China’s Belt and Road Initiative Intensified Bilateral Trade Links between China and the Involved Countries? Sustainability 2020, 12, 6747. [Google Scholar] [CrossRef]

- Kliman, D.; Doshi, R.; Lee, K.; Cooper, Z. Grading China’s Belt and Road; Center for a New American Security (CNAS): Washington, DC, USA, 2019. [Google Scholar]

- Blanchard, J.-M.F.; Flint, C. The Geopolitics of China’s Maritime Silk Road Initiative. Geopolitics 2017, 22, 223–245. [Google Scholar] [CrossRef]

- CNR News (China National Radio News), The Current Project in Iran is for Electrification Transformation, the Agreement of China-Iran High-Speed Railway Has Not been Unfrozen. 2016. Available online: http://finance.cnr.cn/gundong/20160214/t20160214_521374901.shtml (accessed on 17 October 2020).

- Institute for Economics & Peace (IEP). COVID-19 and Peace; Institute for Economics & Peace (IEP): Sydney, Australia, 2020; Available online: http://visionofhumanity.org/reports. (accessed on 4 December 2020).

- ABC News. Protests Against Coronavirus Lockdown Measures Spread in the UK and Across Europe. Available online: https://www.abc.net.au/news/2020-05-17/protests-against-coronavirus-lockdown-in-uk-and-europe-covid-19/12256802 (accessed on 4 December 2020).

- International Monetary Fund (IMF). Available online: https://www.imf.org/external/datamapper/profile/WEOWORLD (accessed on 4 December 2020).

- Jiang, H. The geopolitical risk assessment and management along the Belt and Road. Intertrade 2015, 8, 21–24. [Google Scholar]

- Zhao, M.Y.; Dong, S.C.; Wang, J.; Cheng, H.; Qin, F.M.; Li, Y.; Li, Z.H.; Li, F. Assessment of countries’ security situation along the Belt and Road and Countermeasures. Bull. Chin. Acad. Sci. 2016, 6, 689–696. [Google Scholar]

- Ji, G.B.; Liang, H.G. Annual Report on Investment Security of China’s the “Belt and Road” Construction (2020), 1st ed.; Social Academic Press (CHINA): Beijing, China, 2020; pp. 1–57. [Google Scholar]

- Fitzpatrick, M. The definition and assessment of political risk in international business: A review of the literature. Acad. Manag. Rev. 1983, 8, 249–254. [Google Scholar] [CrossRef]

- Khattab, A.A.; Anchor, J.; Davies, E. Managerial perceptions of political risk in international projects. J. Proj. Manag. 2007, 25, 734–743. [Google Scholar] [CrossRef] [Green Version]

- The Political Risk Services (PRS) Group. The International Country Risk Guide (ICRG) Methodology. Available online: https://www.prsgroup.com/explore-our-products/international-country-risk-guide/ (accessed on 29 October 2020).

- The Fund For Peace (FFP). Fragile States Index and CAST Framework Methodology. Available online: https://fragilestatesindex.org/2017/05/13/fragile-states-index-and-cast-framework-methodology/ (accessed on 5 November 2020).

- Busse, M.; Hefeker, C. Political Risk, institutions and foreign direct investment. Eur. J. Polit. Econ. 2007, 23, 397–415. [Google Scholar] [CrossRef] [Green Version]

- Clark, E. Valuing political risk. J. Int. Money Finan. 1997, 16, 477–490. [Google Scholar] [CrossRef]

- Adebiyi, J.; Sanni, G.A.; Oyetunji, A.K. Assessment of political risk factors influencing the corporate performance of multinationals construction companies in northeastern Nigeria. Glob. J. Business Econ. Manag. Curr. Issues 2019, 9, 63–75. [Google Scholar] [CrossRef] [Green Version]

- Mellers, B.A.; Tetlock, P.E.; Backer, J.D.; Friedman, J.A.; Zeckhauser, R. Chapter 12: Improving the Accuracy of Geopolitical Risk Assessments. In The Future of Risk Management; Kunreuther, H., Meyer, R.J., Michel-Kerjan, E.O., Eds.; University of Pennsylvania Press: Philadelphia, PA, USA, 2019; pp. 209–226. [Google Scholar]

- Zhang, C.C.; Xiao, C.W.; Liu, H.L. Spatial Big Data Analysis of Political Risks along the Belt and Road. Sustainability 2019, 11, 2216. [Google Scholar] [CrossRef] [Green Version]

- Buckley, P.J.; Chen, L.; Clegg, L.J.; Voss, H. Risk propensity in the foreign direct investment location decision of emerging multinationals. J. Int. Bus. Stud. 2018, 49, 153–171. [Google Scholar] [CrossRef]

- Holburn, G.L.F.; Zelner, B.A. Political capabilities, policy risk, and international investment strategy: Evidence from the global electric power generation industry. Strateg. Manag. J. 2010, 31, 1290–1315. [Google Scholar] [CrossRef]

- Bekeart, G.; Harvey, C.R.; Lundblad, C.T.; Siegel, S. Political risk and international valuation. J. Corp. Financ. 2016, 37, 1–23. [Google Scholar] [CrossRef]

- Kluge, J.N. Foreign direct investment, political risk and the limited access order. New Polit. Econ. 2017, 22, 109–127. [Google Scholar] [CrossRef]

- Giambona, E.; Graham, J.R.; Harvey, C.R. The management of political risk. J. Int. Bus. Stud. 2017, 48, 523–533. [Google Scholar] [CrossRef]

- Howell, L.D.; Chaddick, B. Models of Political risk for foreign-investment and trade: An assessment of 3 approaches. Columbia J. World Bus. 1994, 29, 70–91. [Google Scholar] [CrossRef]

- Leitner, J. Political risk and international business: Where they interfere, consequences and options. In State Capture, Political Risks and International Business: Case from Black Sea Region Countries; Leitner, J., Meissner, H., Eds.; Routledge: London, UK, 2017; pp. 26–40. [Google Scholar]

- De Mortanges, C.P.; Allers, V. Political risk assessment: Theory and the experience of Dutch firms. Int. Bus. Rev. 1996, 5, 303–318. [Google Scholar] [CrossRef]

- Garcia-Canal, E.; Guillen, M.F. Risk and the strategy of foreign location choice in regulated industries. Strateg. Manag. J. 2008, 29, 1097–1115. [Google Scholar] [CrossRef] [Green Version]

- Quer, D.; Claver, E.; Rienda, L. Political risk, cultural distance, and outward foreign direct investment: Empirical evidence from large Chinese firms. Asia Pac. J. Manag. 2012, 29, 1089–1104. [Google Scholar] [CrossRef]

- Deng, X.P.; Peng, L.S. Understanding the critical variables affecting the level of political risks in international construction projects. KSCE J. Civ. Eng. 2013, 17, 895–907. [Google Scholar]

- Chang, T.Y.; Deng, X.P.; Hwang, B.G.; Zhao, X.J. Political Risk Paths in International Construction Projects: Case Study from Chinese Construction Enterprises. Adv. Civ. Eng. 2018, 2018, 6939828. [Google Scholar] [CrossRef]

- Brink, C.H. Measuring Political Risk: Risks to Foreign Investment, 2nd ed.; Routledge: London, UK, 2016; pp. 17–45. [Google Scholar]

- Tracy, E.F.; Shvarts, E.; Simonov, E.; Babenko, M. China’s new Eurasian ambitions: The environmental risks of the Silk Road Economic Belt. Eurasian Geogr. Econ. 2017, 58, 56–88. [Google Scholar] [CrossRef] [Green Version]

- Duan, F.; Ji, Q.; Liu, B.Y.; Fan, Y. Energy investment risk assessment for nations along China’s Belt and Road Initiative. J. Clean Prod. 2018, 170, 535–547. [Google Scholar] [CrossRef]

- Liu, Y.Y.; Hao, Y. The dynamic links between CO2 emissions, energy consumption and economic development in the countries along the “the Belt and Road”. Sci. Total Environ. 2018, 645, 674–683. [Google Scholar] [CrossRef]

- Han, L.; Han, B.T.; Shi, X.P.; Su, B.; Lv, X.; Lei, X. Energy efficiency convergence across countries in the context of China’s Belt and Road Initiative. Appl. Energy 2018, 213, 112–122. [Google Scholar] [CrossRef] [Green Version]

- Saud, S.; Chen, S.S.; Danish; Haseeb, A. Impact of financial development and economic growth on environment quality: An empirical analysis from Belt and Road Initiative (BRI) countries. Environ. Sci. Pollut. Res. 2019, 26, 2253–2269. [Google Scholar] [CrossRef]

- Sheng, J. Analyzing the Risks of China’s ‘One Belt, One Road’ Initiative. In Proceedings of the 8th International NASD Conference on Economic and Legal Challenges, L’viv, Ukraine, 14 January 2018. [Google Scholar]

- Huang, Y.Y. Environmental risks and opportunities for countries along the Belt and Road: Location choice of China’s investment. J. Clean Prod. 2018, 211, 14–26. [Google Scholar] [CrossRef]

- Rockett, J.P. Definitions are not what they seem. Risk Manag. 1999, 1, 37–47. [Google Scholar] [CrossRef]

- Kobrin, S.J. Political risk: Review and reconsideration. J. Int. Bus. Stud. 1979, 10, 67–80. [Google Scholar] [CrossRef]

- Robock, S.H. Political risk: Identification and assessment. Columbia J. World Bus. 1971, 6, 6–20. [Google Scholar]

- Butler, K.C.; Joaquin, D.C. A note on political risk and the required return on foreign direct investment. J. Int. Bus. Stud. 1998, 29, 599–607. [Google Scholar] [CrossRef]

- Jensen, N.M. Nation-Sates and the Multinational Corporation: A Political Economy of Foreign Direct Investment; Princeton University Press: Princeton, NJ, USA, 2006; pp. 53–71. [Google Scholar]

- Fagersten, B. Political risk and the commercial sector: Aligning theory and practice. Risk Manag. 2015, 17, 23–39. [Google Scholar] [CrossRef] [Green Version]

- Beiber, J.; Brandt, P.T.; Halterman, A.; Schrodt, P.A.; Simpson, E.M. Generating Political Event Data in Near Real Time: Opportunities and Challenges. In Computational Social Science: Discovery and Prediction; Alvarez, R.M., Ed.; Cambridge University Press: New York, NY, USA, 2016; pp. 98–120. [Google Scholar]

- GDELT. The GDELT Event Database Data Format Codebook v2.0. Available online: http://data.gdeltproject.org/documentation/GDELT-Event_Codebook-V2.0.pdf. (accessed on 24 November 2020).

- Goldstein, J.S. A Conflict-Cooperation Scale for WEIS Events Data. J. Confl. Resolut. 1992, 36, 369–385. [Google Scholar] [CrossRef]

- American Enterprise Institute (AEI). China Global Investment Tracker (CGIT). Available online: https://www.aei.org/china-global-investment-tracker/ (accessed on 27 December 2020).

- Raleigh, C.; Linke, A.; Hegre, H.; Karlsen, J. Introducing ACLED: An Armed Conflict Location and Event Dataset. J. Peace Res. 2010, 47, 651–660. [Google Scholar] [CrossRef]

- Kubik, J. Institutionalization of Protest during Democratic Consolidation in Central Europe. In The Social Movement Society: Contentious Politics for a New Century; Meyer, D.S., Tarrow, S., Eds.; Rowman & Littlefield Publishers, Inc.: Lanham, MD, USA, 1998; pp. 131–152. [Google Scholar]

- Hammond, J.; Weidmann, N.B. Using machine-coded event data for the micro-level study of political violence. Res. Polit. 2014, 1, 1–8. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Regions | Countries (Country Codes) |

|---|---|

| Northeast Asia | Mongolia (MNG), Russia (RUS) |

| Southeast Asia | Singapore (SGP), Indonesia (IDN), Malaysia (MYS), Thailand (THA), Vietnam (VNM), Philippines (PHL), Cambodia (KHM), Myanmar (MMR), Laos (LAO), Brunei (BRN) |

| South Asia | India (IND), Pakistan (PAK), Sri Lanka, (LKA), Bangladesh (BGD), Nepal (NPL), Maldives (MDV), Bhutan (BTN) |

| West Asia and North Africa | United Arab Emirates (ARE), Kuwait (KWT), Turkey (TUR), Qatar (QAT), Oman (OMN), Lebanon (LBN), Saudi Arabia (SAU), Bahrain (BHR), Israel (ISR), Yemen (YEM), Egypt (EGY), Iran (IRN), Jordan (JOR), Syria (SYR), Iraq (IRQ), Afghanistan (AFG), Palestine (PLE), Azerbaijan (AZE), Georgia (GEO), Armenia (ARM), Bahrain (BHR) |

| Central and Eastern Europe | Poland (POL), Albania (ALB), Estonia (EST), Lithuania (LTU), Slovenia (SVN), Bulgaria (BGR), Czech (CZE), Hungary (HUN), Macedonia (MKD), Serbia (SRB), Romania (ROU), Slovakia (SVK), Croatia (HRV), Latvia (LVA),Ukraine (UKR), Belarus (BLR), Moldova (MDA), Greece (GRC), Cyprus (CYP) |

| Central Asia | Kazakhstan (KAZ), Kyrgyzstan (KGZ), Turkmenistan (TKM), Tajikistan (TJK), Uzbekistan (UZB) |

| Exhibit Force Posture | Reduce Relations | Coerce | Assault | Fight | Use Unconventional Mass Violence |

|---|---|---|---|---|---|

| Demonstrate military or police power | Reduce relations | Coerce | Use unconventional violence | Use conventional military force | Use unconventional mass violence |

| Increase police alert status | Reduce or break diplomatic relations | Seize or damage property | Abduct/hijack /take hostage | Impose blockade /restrict movement | Engage in mass expulsion |

| Increase military alert status | Reduce or stop material aid | Impose administrative sanctions | Physically assault | Occupy territory | Engage in mass killings |

| Mobilize or increase police power | Impose embargo/ boycott/sanctions | Arrest/detain/charge with legal action | Conduct suicide/ car/other non-military bombing | Fight with small arms and light weapons | Engage in ethnic cleansing |

| Mobilize or increase armed forces | Halt negotiations | Expel or deport individuals | Use as human shield | Fight with artillery and tanks | Use weapons of mass destruction |

| Mobilize or increase cyber-forces | Halt mediation | Use tactics of violent repression | Attempt to assassinate | Employ aerial weapons | |

| Expel or withdraw | Attack cybernetically | Assassinate | Violate ceasefire |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sun, X.; Gao, J.; Liu, B.; Wang, Z. Big Data-Based Assessment of Political Risk along the Belt and Road. Sustainability 2021, 13, 3935. https://doi.org/10.3390/su13073935

Sun X, Gao J, Liu B, Wang Z. Big Data-Based Assessment of Political Risk along the Belt and Road. Sustainability. 2021; 13(7):3935. https://doi.org/10.3390/su13073935

Chicago/Turabian StyleSun, Xiaohui, Jianbo Gao, Bin Liu, and Zhenzhen Wang. 2021. "Big Data-Based Assessment of Political Risk along the Belt and Road" Sustainability 13, no. 7: 3935. https://doi.org/10.3390/su13073935

APA StyleSun, X., Gao, J., Liu, B., & Wang, Z. (2021). Big Data-Based Assessment of Political Risk along the Belt and Road. Sustainability, 13(7), 3935. https://doi.org/10.3390/su13073935