Employees’ Perceptions on the Relationship of Intellectual Capital and Business Performance of ICT Companies

Abstract

:1. Introduction

2. Literature Overview

- (a)

- Human Capital

- (b)

- Structural Capital

- (c)

- Relational Capital

3. Materials and Methods

4. Results

5. Discussion

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Stewart, T.A. Intellectual Capital: The New Wealth of Organizations; Doubleday/Currency: New York, NY, USA, 1997. [Google Scholar]

- Škuflić, L.; Vlahinić-Dizdarević, N. Koncept Nove ekonomije i značaj informacijsko–komunikacijske tehnologije u Republici Hrvatskoj. Ekon. Pregl. 2003, 54, 460–479. Available online: https://hrcak.srce.hr/25464 (accessed on 15 August 2021).

- Vlada Republike Srbije. Strategija Razvoja Industrije Informacionih Tehnologija za Period od 2017. do 2020. Godine. Available online: https://www.srbija.gov.rs/dokument/45678/strategije-programi-planovi-.php (accessed on 15 August 2021).

- Kleibrink, A.; Radovanović, N.; Kroll, H.; Horvat, D.; Kutlača, D.; Živković, L. The Potential of ICT in Serbia: An Emerging Industry in the European Context; Publications Office of the European Union: Luxembourg, 2018. [Google Scholar] [CrossRef]

- Narodna Banka Srbije. Platni Bilans. 2020. Available online: https://www.nbs.rs/internet/cirilica/80/platni_bilans.html (accessed on 15 August 2021).

- Matijević, M.; Šolaja, M. ICT in Serbia—At a Glance, 2020; Vojvođanski IKT klaster: Novi Sad, Serbia, 2020; Available online: https://www.ict-cs.org/rs/multimedija/publikacije/ (accessed on 17 August 2021).

- Matijević, M. Perspektive IT Industrije. 2019. Available online: https://www.sito.rs/perspektive-it-industrije/ (accessed on 17 August 2021).

- Lekić, S.; Vapa-Tankosić, J.; Mandić, S.; Rajaković-Mijailović, J.; Lekić, N.; Mijailović, J. Analysis of the Quality of the Employee–Bank Relationship in Urban and Rural Areas. Sustainability 2020, 12, 5448. [Google Scholar] [CrossRef]

- Lekić, N.; Vukosavljević, D.; Vapa-Tankosić, J.; Lekić, S.; Mandić, S. Impact of motivational factors on organizational commitment of bank employees. Ekon. Teor. I Praksa 2021, 14, 1–22. [Google Scholar] [CrossRef]

- Bontis, N. Intellectual capital: An exploratory study that develops measures and models. Manag. Decis. 1998, 36, 63–76. [Google Scholar] [CrossRef] [Green Version]

- De Wall, A.A. The Characteristics of a High-Performance Organization; Center for Organizational Performance: Hilversum, The Netherlands, 2010; Available online: https://www.hpocenter.nl/wp-content/uploads/2013/07/Research-paper-The-characteristics-of-a-HPO-HPO-Center-January-20102.pdf (accessed on 17 August 2020).

- Kliestik, T.; Belas, J.; Valaskova, K.; Nica, E.; Durana, P. Earnings management in V4 countries: The evidence of earnings smoothing and inflating. Econ. Res.-Ekon. Istraživanja 2021, 34, 1452–1470. [Google Scholar] [CrossRef]

- Podhorska, I.; Valaskova, K.; Stehel, V.; Kliestik, T. Possibility of Company Goodwill Valuation: Verification in Slovak and Czech Republic. Manag. Marketing. Chall. Knowl. Soc. 2019, 14, 338–356. [Google Scholar] [CrossRef] [Green Version]

- Kliestik, T.; Kovacova, M.; Podhorska, I.; Kliestikova, J. Searching for Key Sources of Goodwill Creation as New Global Managerial Challenge. Pol. J. Manag. Stud. 2018, 17, 144–154. [Google Scholar] [CrossRef]

- Mouritsen, J.; Bukh, P.N.; Flagstad, K.; Thorbjørnsen, S.; Johansen, M.R.; Kotnis, S.; Larsen, H.T.; Nielsen, C.; Kjærgaard, I.; Krag, L.; et al. Intellectual Capital Statements—The New Guideline; Danish Ministry of Science, Technology and Innovation: Copenhagen, Denmark, 2003; Available online: https://pure.au.dk/ws/files/32340329/guideline_uk.pdf (accessed on 17 August 2021).

- Brennan, N.; Connell, B. Intellectual capital: Current issues and policy implications. J. Intellect. Cap. 2000, 1, 206–240. [Google Scholar] [CrossRef]

- Lentjušenkova, O.; Inga, L. The Transformation of the Organization’s Intellectual Capital: From Resource to Capital. J. Intellect. Cap. 2016, 17, 610–631. [Google Scholar] [CrossRef]

- Roos, G.; Roos, J. Measuring Your Company’s Intellectual Performance. Long Range Plan. 1997, 30, 413–426. Available online: http://capitalintelectual.egc.ufsc.br/wp-content/uploads/2016/05/1997-%E2%80%93-ROOS-y-ROOS-Measuring-your-company%E2%80%99s-Intellectual-performance.pdf (accessed on 17 August 2021). [CrossRef]

- Sveiby, K.E. The Intangible Assets Monitor. J. Hum. Resour. Costing Account. 1997, 2, 73–97. [Google Scholar] [CrossRef]

- Bontis, N. Assessing Knowledge Assets: A Review of the Models Used to Measure Intellectual Capital. Int. J. Manag. Rev. 2002, 3, 41–60. [Google Scholar] [CrossRef]

- Miller, M.; DuPont, B.D.; Fera, V.; Jeffrey, R.; Mahon, B.; Payer, B.M.; Starr, A. Measuring and reporting intellectual capital from a diverse Canadian industry perspective: Experiences, issues and prospects. In Proceedings of the OECD Symposium, Amsterdam, The Netherlands, 9–11 June 1999; Available online: https://www.oecd.org/industry/ind/1947855.pdf (accessed on 19 August 2021).

- Bontis, N.; Chua, C.K.W.; Richardson, S. Intellectual capital and business performance in Malaysian industries. J. Intellect. Cap. 2000, 1, 85–100. [Google Scholar] [CrossRef] [Green Version]

- Do Rosário Cabrita, M.; Bontis, N. Intellectual Capital and Business performance in the Portugese Banking Industry. Int. J. Technol. Manag. 2008, 43, 212–237. [Google Scholar] [CrossRef] [Green Version]

- Joia, L.A.; Malheiros, R. Strategic alliances and the intellectual capital of firms. J. Intellect. Cap. 2009, 10, 539–558. [Google Scholar] [CrossRef]

- Sharabati, A.A.A.; Jawad, S.N.; Bontis, N. Intellectual capital and business performance in the pharmaceutical sector of Jordan. Manag. Decis. 2010, 48, 105–131. [Google Scholar] [CrossRef]

- Cheng-Ping, S.; Wen-Chih, C.; Morrison, M. The Impact of Intellectual Capital on Business Performance in Taiwanese Design Industry. J. Knowl. Manag. Pract. 2010, 11. Available online: http://www.tlainc.com/jkmpv11n110.htm (accessed on 29 August 2021).

- Dženopoljac, V.; Janoševic, S.; Bontis, N. Intellectual capital and financial performance in the Serbian ICT industry. J. Intellect. Cap. 2016, 17, 373–396. [Google Scholar] [CrossRef]

- Chahal, H.; Bakshi, P. Measurement of Intellectual Capital in the Indian Banking Sector. J. Decis. Mak. 2016, 41, 61–73. [Google Scholar] [CrossRef] [Green Version]

- Ramadan, B.; Dahiyat, S.; Bontis, N.; Al-dalahmeh, M. Intellectual Capital, Knowledge Management and Social Capital within the ICT Sector in Jordan. J. Intellect. Cap. 2017, 18, 437–462. [Google Scholar] [CrossRef]

- Andreeva, T.; Garanina, T. Intellectual Capital and Its Impact on the Financial Performance of Russian Manufacturing Companies. Foresight STI Gov. 2017, 11, 31–40. [Google Scholar] [CrossRef]

- Komnenić, B.; Pokrajčić, D. Intellectual capital and corporate performance of MNCs in Serbia. J. Intellect. Cap. 2012, 13, 106–119. [Google Scholar] [CrossRef]

- Pew Tan, H.; Plowman, D.; Hancock, P. Intellectual Capital and Financial Returns of Companies. J. Intellect. Cap. 2007, 8, 76–95. [Google Scholar] [CrossRef]

- Tovstiga, G.; Tulugurova, E. Intellectual capital practices and performance in Russian enterprises. J. Intellect. Cap. 2007, 8, 695–707. [Google Scholar] [CrossRef]

- Petty, R.; Guthrie, J. Intellectual capital literature review: Measurement, reporting and management. J. Intellect. Cap. 2000, 1, 155–176. [Google Scholar] [CrossRef]

- Stewart, T.A. The Wealth of Knowledge: Intellectual Capital and the Twenty-First Century Organization; Nicholas Brealey: London, UK, 1997. [Google Scholar]

- Steenkamp, N.; Kashyap, V. Importance and contribution of intangible assets; SME managers’ perceptions. J. Intellect. Cap. 2010, 11, 368–390. [Google Scholar] [CrossRef]

- Edvinsson, L. Developing intellectual capital at Skandia. Long Range Plan. 1997, 30, 366–373. [Google Scholar] [CrossRef]

- Edvinsson, L.; Sullivan, P. Developing a Model for Managing Intellectual Capital. Eur. Manag. J. 1996, 14, 356–364. [Google Scholar] [CrossRef]

- Grantham, C.; Nichols, L.; Schonberner, M. A Framework for Management of Intellectual Capital in the Health Care Industry. J. Health Care Financ. 1997, 23, 1–19. [Google Scholar]

- Saint-Onge, H. Tacit Knowledge: The Key to the Strategic Alignment of Intellectual Capital. Strategy Leadersh. 1996, 24, 10–16. [Google Scholar] [CrossRef]

- Bontis, N. There’s a price on your head: Managing intellectual capital strategically. Ivey Bus. Q. 1996, 60, 40–47. [Google Scholar]

- Janoševic, S.; Dženopoljac, V. Impact of intellectual capital on financial performance of Serbian companies. Actual Probl. Econ. 2012, 133, 554–564. Available online: https://www.researchgate.net/publication/287702499_Impact_of_intellectual_capital_on_financial_performance_of_Serbian_companies (accessed on 19 August 2021).

- Marti, J.M.V. ICBS—Intellectual Capital Benchmarking System. J. Intellect. Cap. 2001, 2, 148–165. [Google Scholar] [CrossRef] [Green Version]

- Burns, P. Entrepreneurship and Small Business: Start-Up, Growth and Maturity, 3rd ed.; Palgrave Macmillan: New York, NY, USA, 2011. [Google Scholar]

- Seleim, A.; Ashour, A.; Bontis, N. Human Capital and Organizational Performance: A Study of Egyptian Software Companies. Manag. Decis. 2007, 45, 789–901. [Google Scholar] [CrossRef] [Green Version]

- Bontis, N.; Janošević, S.; Dženopoljac, V. Intellectual capital in Serbia’s hotel industry. Int. J. Contemp. Hosp. Manag. 2015, 27, 1365–1384. [Google Scholar] [CrossRef]

- Nunnally, J.C. Psychometric Theory, 2nd ed.; McGraw-Hill: New York, NY, USA, 1978. [Google Scholar]

- Churchill, G.A. A paradigm for developing better measures of marketing constructs. J. Mark. Res. 1979, 16, 64–73. [Google Scholar] [CrossRef]

- Hair, J.F.; Risher, J.J.; Sarstedt, M.; Ringle, C.M. When to use and how to report the results of PLS-SEM. Eur. Bus. Rev. 2019, 31, 2–24. [Google Scholar] [CrossRef]

- Subotić, S. Pregled metoda za utvrđivanje broja faktora i komponenti (u EFA i PCA). Primenj. Psihol. 2013, 6, 203–229. [Google Scholar] [CrossRef] [Green Version]

- Worthington, R.L.; Whittaker, T.A. Scale development research: A content analysis and recommendations for best practices. Couns. Psychol. 2006, 34, 806–838. [Google Scholar] [CrossRef]

- Kahn, J.H. Factor analysis in counseling psychology research, training, and practice: Principles, advances, and applications. Couns. Psychol. 2006, 34, 684–718. [Google Scholar] [CrossRef]

- Steger, M.F. An illustration of issues in factor extraction and identification of dimensionality in psychological assessment data. J. Personal. Assess. 2006, 86, 263–272. [Google Scholar] [CrossRef] [PubMed]

- Velicer, W.F.; Jackson, D.N. Component Analysis versus Common Factor Analysis: Some Issues in Selecting an Appropriate procedure. Multivar. Behav. Res. 1990, 25, 1–28. [Google Scholar] [CrossRef] [PubMed]

- Hair, J.F.; Hult, G.T.M.; Ringle, C.M.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling; Sage: Thousand Oaks, CA, USA, 2014. [Google Scholar]

- Sarstedt, M.; Ringle, C.M.; Hair, J.F. Partial least squares structural equation modeling. In Handbook of Market Research; Homburg, C., Klarmann, M., Vomberg, A., Eds.; Springer: Heidelberg, Germany, 2017; pp. 1–40. [Google Scholar] [CrossRef]

- Hair, J.; Hollingsworth, C.L.; Randolph, A.B.; Chong, A.Y.L. An updated and expanded assessment of PLS-SEM in information systems research. Ind. Manag. Data Syst. 2017, 117, 442–458. [Google Scholar] [CrossRef]

- Komšić, J. Mjerenje Reputacije Turističke Destinacije na Društvenim Medijima i Zadovoljstva Turista. Doktorski rad, Sveučilište u Rijeci, Fakultet za Menadžment u Turizmu i Ugostiteljstvu: Opatija, Croatia, 2018. Available online: https://urn.nsk.hr/urn:nbn:hr:191:941056 (accessed on 20 August 2021).

- Barclay, D.; Higgins, C.; Thompson, R. The partial least squares (PLS) approach to causal modelling: Personal computer adaptation and use as an illustration. Technol. Stud. 1995, 2, 285–309. [Google Scholar]

- Hair, J.F.; Sarstedt, M.; Hopkins, L.; Kuppelwieser, V.G. Partial least squares structural equation modeling (PLS-SEM): An emerging tool in business research. Eur. Bus. Rev. 2014, 26, 106–121. [Google Scholar] [CrossRef]

- Nunnally, J.C.; Bernstein, I.H. Psychometic Theory, 3rd ed.; McGraw-Hill: New York, NY, USA, 1994. [Google Scholar]

- Onyekachi, A.M.; Olanrewaju, S.O. A Comparison of Principal Component Analysis, Maximum Likelihood and the Principal Axis in Factor Analysis. Am. J. Math. Stat. 2020, 10, 44–54. [Google Scholar] [CrossRef]

- Fosnot, C.T. Constructivism, Theory, Perspectives, and Practice; Teachers College Press: New York, NY, USA, 1996. [Google Scholar]

- Von Glasersfeld, E. An Exposition of Constructivism: Why Some Like it Radical. In Facets of Systems Science; Klir, G.J., Ed.; Plenum: New York, NY, USA, 1991; pp. 229–238. Available online: http://www.vonglasersfeld.com/127 (accessed on 20 August 2021).

- Chin, W.W. The partial least squares approach for structural equation modeling. In Modern Methods for Business Research; Marcoulides, G.A., Ed.; Lawrence Erlbaum Associates: Mahwah, NJ, USA, 1998; pp. 295–336. [Google Scholar]

- Bontis, N. Managing Organizational Knowledge by Diagnosing Intellectual Capital: Framing and Advancing the State of the Field. Int. J. Technol. Manag. 1999, 18, 433–462. [Google Scholar] [CrossRef]

- Tenenhaus, M.; Esposito Vinzi, V.; Chatelin, Y.M.; Lauro, C. PLS path modeling. Comput. Stat. Data Anal. 2005, 48, 159–205. [Google Scholar] [CrossRef]

- Ringle, C.M.; Wende, S.; Will, A. SmartPLS 2.0 M3; University of Hamburg: Hamburg, Germany, 2005; Available online: http://www.smartpls.de (accessed on 20 August 2021).

- Ringle, C.M.; Wende, S.; Becker, J.M. SmartPLS 3; SmartPLS GmbH: Bönningstedt, Germany, 2015; Available online: http://www.smartpls.com (accessed on 20 August 2021).

- Götz, O.; Liehr-Gobbers, K.; Krafft, M. Evaluation of structural equation models using the partial least squares (PLS) Approach. In Handbook of Partial Least Squares: Concepts, Methods and Applications; Esposito Vinzi, V., Chin, W.W., Henseler, J., Wang, H., Eds.; Springer Handbooks of Computational Statistics Series; Springer: Berlin/Heidelberg, Germany, 2010; pp. 691–711. [Google Scholar] [CrossRef]

- Henseler, J.; Fassott, G. Testing moderating effects in PLS path models: An illustration of available procedures. In Handbook of Partial Least Squares: Concepts, Methods and Applications; Esposito Vinzi, V., Chin, W.W., Henseler, J., Wang, H., Eds.; Springer Handbooks of Computational Statistics Series; Springer: Berlin/Heidelberg, Germany, 2010; pp. 713–735. [Google Scholar] [CrossRef]

- Henseler, J.; Hubona, G.S.; Ray, P.A. Using PLS path modeling in new technology research: Updated guidelines. Ind. Manag. Data Syst. 2016, 116, 1–19. [Google Scholar] [CrossRef]

- Černe, K.; Etinger, D. IT as a part of intellectual capital and its impact on the performance of business entities. Croat. Oper. Res. Rev. 2016, 7, 389–408. [Google Scholar] [CrossRef] [Green Version]

- Zlatković, M. Intellectual capital and organizational effectiveness: PLS-SEM approach. Industrija 2018, 46, 145–169. [Google Scholar] [CrossRef]

- Aguirre-Urreta, M.I.; Rönkkö, M. Statistical Inference with PLSc Using Bootstrap Confidence Intervals. MIS Q. 2018, 42, 1001–1020. [Google Scholar] [CrossRef]

- Sarstedt, M.; Ringle, C.M.; Smith, D.; Reams, R.; Hair, J.F. Partial Leas Squares Structural Equation Modeling (PLS-SEM): A Useful Tool for family business researcher. J. Fam. Bus. Strategy 2014, 5, 105–115. [Google Scholar] [CrossRef]

- Yildiz, O.; Kitapci, H. Exploring Factors Affecting Consumers’ Adoption of Shopping via Mobile Applications in Turkey. Int. J. Mark. Stud. 2018, 10, 60–75. [Google Scholar] [CrossRef] [Green Version]

- Wong, K.K.K. Partial least squares structural equation modeling (PLS-SEM) techniques using SmartPLS. Mark. Bull. 2013, 24, 1–32. Available online: http://marketing-bulletin.massey.ac.nz/v24/mb_v24_t1_wong.pdf (accessed on 20 August 2021).

- Kianto, A.; Sáenz, J.; Aramburu, N. Knowledge-based human resource management practices, intellectual capital and innovation. J. Bus. Res. 2017, 81, 11–20. [Google Scholar] [CrossRef]

- Hair, J.F.; Ringle, C.M.; Sarstedt, M. Partial least squares structural equation modeling: Rigorous applications, better results and higher acceptance. Long Range Plan. 2013, 46, 1–12. [Google Scholar] [CrossRef]

- Chin, W.W. PLS-Graph User’s Guide Version 3.0. C.T.; Bauer College of Business, University of Houston: Houston, TX, USA, 2001. [Google Scholar]

- Chin, W.W. How to Write Up and Report PLS Analyses. In Handbook of Partial Least Squares: Concepts, Methods and Applications; Esposito Vinzi, V., Chin, W.W., Henseler, J., Wang, H., Eds.; Springer: Berlin/Heidelberg, Germany, 2010; pp. 655–699. [Google Scholar] [CrossRef]

- Cohen, J. Statistical Power Analysis for the Behavioral Sciences, 2nd ed.; Lawrence Erlbaum Associates: Mahwah, NJ, USA, 1988. [Google Scholar]

- Berglund, R.; Grönvall, T.; Johnson, M. Intellectual Capital’s Leverage on Market Value. Master’s Thesis, Lund School of Economics and Management Lund University, Lund, Sweden, 2002. Available online: https://lup.lub.lu.se/luur/download?func=downloadFile&recordOId=1341958&fileOId=2433109 (accessed on 20 August 2021).

- Sofian, S.; Tayles, M.E.; Pike, R.H. Intellectual Capital: An Evolutionary Change in Management Accounting Practice; Working Paper Series 04/29; Bradford University School of Management: Bradfor, UK, 2004; Available online: http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.571.8491&rep=rep1&type=pdf (accessed on 23 August 2021).

- Moslehi, A.; Mohagharl, A.; Badie1, K.; Lucas, C. Introducing a toolbox for IC measurement in the Iran insurance industry. Electron. J. Knowl. Manag. 2006, 4, 169–180. Available online: http://www.ejkm.com (accessed on 23 August 2021).

- Bin Ismail, M. The Influence of Intellectual Capital on the Performance of Telekom Malaysia (Telco). Unpublished Doctoral Dissertation, Business & Advanced Technology Centre, University of Technology Malaysia: Skunda, Malaysia, 2005. Available online: https://studylib.net/doc/14553197/the-influence-of-intellectual-capital-on-the-performance-(accessed on 23 August 2021).

- Lekić, N.; Vapa-Tankosić, J.; Rajaković-Mijailović, J.; Lekić, S. Analysis of structural capital as a component of intellectual capital. Oditor 2020, 6, 33–54. [Google Scholar] [CrossRef]

- Bollen, L.; Vargauwen, P.; Schnieders, S. Linking intellectual capital and intellectual property to company performance. Manag. Decis. 2005, 43, 1161–1185. [Google Scholar] [CrossRef] [Green Version]

- Wang, W.Y.; Chang, C. Intellectual Capital and Performance in Causal Models: Evidence from the Information Technology Industry in Taiwan. J. Intellect. Cap. 2005, 6, 222–236. [Google Scholar] [CrossRef] [Green Version]

- Hassan, S. Impact of HRM Practices on Employee’s Performance. Int. J. Acad. Res. Account. 2016, 6, 15–22. [Google Scholar] [CrossRef]

- Rukumba, S.; Iravo, M.A.; Kaigiri, A. Influence of training and development on performance of telecommunication industry in Kenya. J. Hum. Resour. Leadersh. 2019, 4, 22–31. Available online: https://www.iprjb.org/journals/index.php/JHRL/article/view/855 (accessed on 20 August 2021). [CrossRef]

- Eronimus, A.; Rajeswari, T. Impact of Training Practises on Employee Performance in Software Industry—A Study on HOV Service Limited in Chennai. Train. Dev. J. 2017, 8, 89–94. [Google Scholar] [CrossRef]

- Dayasindhu, N. Embeddedness, knowledge transfer, industry clusters and global competitiveness: A case study of the India software industry. Technovation 2002, 22, 555–560. [Google Scholar] [CrossRef]

- Lekić, N.J.; Vukosavljević, D.D. The importance of human resources in the development of ICT enterprises. Kult. Polisa 2021, XVIII, 293–305. [Google Scholar] [CrossRef]

- Bontis, N.; Fitz-enz, J. Intellectual Capital ROI: A Causal Map of Human Capital Antecedents and Consequents. J. Intellect. Cap. 2002, 3, 223–247. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

| Human Capital | Mean (Std. Dev.) | Variance | Skewness (Std. Error of Skewness = 0.099) | Kurtosis (Std. Error of Kurtosis = 0.197) |

|---|---|---|---|---|

| Competences of employees in the ICT company are in accordance with the requirements and responsibilities of the workplace (HC-1) | 3.60 (1.590) | 2.529 | −0.672 | −1.208 |

| The ICT company has the best results when its employees cooperate with each other in performing team tasks (HC-2) | 3.35 (1.166) | 1.360 | −0.202 | −0.992 |

| Every year, the ICT company’s employees have continuous training programs (HC-3) | 3.55 (1.286) | 1.654 | −0.469 | −1.047 |

| Employees of the ICT company are able to constantly learn from each other (HC-4) | 3.29 (1.193) | 1.423 | −0.219 | −1.084 |

| The education of employees in the ICT company is in line with the average education of employees in this sector (HC-5) | 3.45 (1.236) | 1.527 | −0.440 | −0.934 |

| The ICT company encourages the upgrade and development of knowledge and skills of employees (HC-6) | 3.42 (1.215) | 1.476 | −0.270 | −1.078 |

| The market position of the ICT company has been continuously improving in the last few years (HC-7) | 3.56 (1.253) | 1.571 | −0.463 | −0.958 |

| Employee learning and education have a positive impact on ICT company productivity (HC-8) | 3.53 (1.261) | 1.591 | −0.383 | −1.119 |

| Learning and education of employees positively affect the profitability of the ICT company (HC-9) | 3.68 (1.234) | 1.523 | −0.609 | −0.823 |

| Learning and education of employees positively affect the market position of the ICT company (HC-10) | 3.65 (1.253) | 1.569 | −0.536 | −0.958 |

| The ICT company’s employees are experts in their field (HC-11) | 3.66 (1.541) | 2.375 | −0.726 | −1.074 |

| Employees in the ICT company, when performing work tasks, give their maximum (HC-12) | 3.30 (1.157) | 1.338 | −0.092 | −1.037 |

| The employees of the ICT company give their maximum and that is the comparative advantage of this company (HC-13) | 3.60 (1.300) | 1.690 | −0.557 | −0.940 |

| Employees of the ICT company have been working in it for years (outflow of employees is very low) (HC-14) | 3.29 (1.182) | 1.398 | −0.151 | −0.998 |

| The ICT company is proud of its efficiency (HC-15) | 3.58 (1.242) | 1.542 | −0.563 | −0.772 |

| The employees are extremely professional (HC-16) | 3.36 (1.239) | 1.535 | −0.230 | −1.086 |

| The ICT company has the lowest transaction costs of anyone in the industry (HC-17) | 3.48 (1.251) | 1.565 | −0.353 | −1.040 |

| Experience and expertise of employees positively affect the productivity of the ICT company (HC-18) | 3.44 (1.233) | 1.519 | −0.412 | −0.928 |

| Experience and expertise of employees positively affect the profitability of the ICT company (HC-19) | 3.50 (1.269) | 1.611 | −0.425 | −1.025 |

| Experience and expertise of employees positively affect the market position of the ICT company (HC-20) | 3.70 (1.179) | 1.389 | −0.561 | −0.782 |

| Employees in the ICT company are creative (compared to other companies in the industry) (HC-21) | 3.66 (1.557) | 2.425 | −0.716 | −1.112 |

| Employees of the ICT company are ready to express their opinion in group discussions (HC-22) | 3.31 (1.192) | 1.421 | −0.234 | −0.912 |

| Employees in the ICT company are developing new ideas (HC-23) | 3.56 (1.332) | 1.774 | −0.507 | −1.053 |

| The ICT company launches a larger number of new products compared to the competition (HC-24) | 3.28 (1.208) | 1.458 | −0.206 | −0.985 |

| When performing work tasks, employees in the ICT company are continuously encouraged to apply new knowledge and ideas, as well as to share their knowledge with colleagues (HC-25) | 3.40 (1.284) | 1.650 | −0.424 | −0.997 |

| Employees in the ICT company are satisfied with the innovation policies and programs of their ICT company (HC-26) | 3.38 (1.165) | 1.358 | −0.174 | −1.037 |

| The employees of the ICT company are highly motivated and want to share new great ideas within this company (HC-27) | 3.51 (1.229) | 1.509 | −0.473 | −0.863 |

| Innovation and creativity of employees affect the productivity of the ICT company (HC-28) | 3.51 (1.170) | 1.368 | −0.364 | −0.932 |

| Innovation and creativity of employees affect the profitability of the ICT company (HC-29) | 3.65 (1.241) | 1.540 | −0.641 | −0.700 |

| Innovation and creativity of employees positively affect the market position of the ICT company (HC-30) | 3.74 (1.167) | 1.362 | −0.624 | −0.661 |

| Human capital (HC) | 3.50 (0.655) | 1.60 | −0.064 | −0.227 |

| Structural Capital | Mean (Std. Dev.) | Variance | Skewness (Std. Error of Skewness = 0.099) | Kurtosis (Std. Error of Kurtosis = 0.197) |

|---|---|---|---|---|

| The ICT company has training programs in order to train internal resources in the form of potential successors for holders of senior and major positions (SC-1) | 3.58 (1.594) | 2.539 | −0.593 | −1.302 |

| The culture and atmosphere of the ICT company is stimulating and pleasant (SC-2) | 3.35 (1.198) | 1.436 | −0.248 | −0.925 |

| Employee recruitment programs are aimed at hiring the best available candidates (SC-3) | 3.50 (1.316) | 1.732 | −0.485 | −1.013 |

| The ICT company has a well-developed performance reward system (SC-4) | 3.33 (1.179) | 1.389 | −0.229 | −0.930 |

| The ICT company continuously supports its employees in improving their skills and education whenever necessary (SC-5) | 3.45 (1.237) | 1.530 | −0.413 | −0.950 |

| Employees have influence over ICT company decisions (SC-6) | 3.36 (1.222) | 1.493 | −0.319 | −0.928 |

| This ICT company is not a “bureaucratic nightmare” (SC-7) | 3.49 (1.258) | 1.581 | −0.362 | −1.101 |

| ICT company systems and programs affect its productivity (SC-8) | 3.47 (1.207) | 1.456 | −0.401 | −0.880 |

| ICT company systems and programs affect its profitability (SC-9) | 3.64 (1.216) | 1.478 | −0.575 | −0.764 |

| ICT company systems and programs affect the market position (SC-10) | 3.63 (1.213) | 1.470 | −0.461 | −0.936 |

| The ICT company is considered a leader in the field of research (SC-11) | 3.63 (1.591) | 2.530 | −0.620 | −1.289 |

| The ICT company is continuously developing work processes (SC-12) | 3.25 (1.254) | 1.572 | −0.196 | −1.073 |

| The ICT company is continuously developing and reorganizing based on the results of research and development (SC-13) | 3.48 (1.305) | 1.703 | −0.372 | −1.171 |

| The ICT company monitors and adopts the latest scientific and technical achievements around the world (SC-14) | 3.31 (1.188) | 1.412 | −0.235 | −0.931 |

| ICT company systems and procedures support innovation (SC-15) | 3.46 (1.242) | 1.544 | −0.421 | −0.980 |

| The ICT company determines an appropriate and adequate budget for research and development activities (SC-16) | 3.34 (1.228) | 1.508 | −0.294 | −0.991 |

| The ICT company’s top management is supported and relies heavily on the research and development department (SC-17) | 3.43 (1.256) | 1.577 | −0.324 | −1.087 |

| ICT company research and development affects the productivity (SC-18) | 3.39 (1.228) | 1.508 | −0.290 | −1.025 |

| ICT company research and development affects the profitability (SC-19) | 3.47 (1.277) | 1.630 | −0.390 | −1.047 |

| ICT company research and development affects the market position (SC-20) | 3.55 (1.253) | 1.570 | −0.415 | −1.049 |

| The ICT company has clear strategies and procedures for intellectual property management (SC-21) | 3.56 (1.614) | 2.604 | −0.589 | −1.335 |

| The ICT company monitors its IPR portfolio (SC-22) | 3.20 (1.205) | 1.453 | −0.228 | −0.933 |

| The ICT company implements the IPR licensing strategy (SC-23) | 3.45 (1.319) | 1.740 | −0.398 | −1.099 |

| The ICT company actively encourages and rewards creation in order to maximize IPR revenues (SC-24) | 3.19 (1.194) | 1.426 | −0.096 | −1.009 |

| IPR is a key intellectual asset for top management. which is considered to create value for the ICT company (SC-25) | 3.39 (1.246) | 1.553 | −0.317 | −1.050 |

| The ICT company makes maximum use of IPR (SC-26) | 3.29 (1.214) | 1.474 | −0.218 | −1.028 |

| The ICT company has a high number of IPRs per year compared to competitors (SC-27) | 3.37 (1.226) | 1.502 | −0.241 | −1.052 |

| IPR affects the productivity of the ICT company (SC-28) | 3.31 (1.225) | 1.501 | −0.214 | −1.021 |

| IPR affects the profitability of the ICT company (SC-29) | 3.40 (1.248) | 1.558 | −0.299 | −1.053 |

| IPR affects the market position of the ICT company (SC-30) | 3.42 (1.263) | 1.595 | −0.307 | −1.066 |

| Structural capital (SC) | 3.42 (0.679) | 1.64 | −0.097 | −0.111 |

| Relational Capital | Mean (Std. Dev.) | Variance | Skewness (Std. Error of Skewness = 0.099) | Kurtosis (Std. Error of Kurtosis = 0.197) |

|---|---|---|---|---|

| The ICT company is currently working on joint projects with many other companies (RC-1) | 3.58 (1.609) | 2.589 | −0.604 | −1.319 |

| The ICT company has different distribution channels (RC-2) | 3.24 1.261) | 1.590 | −0.175 | −1.107 |

| High level of business activities of the ICT company is performed through established strategic alliances (RC-13) | 3.52 (1.279) | 1.637 | −0.437 | −1.069 |

| The ICT company has many different strategic alliances (for research and development, production, marketing, distribution, etc.) (RC-4) | 3.26 (1.192) | 1.420 | −0.194 | −0.975 |

| When making decisions within the ICT company, people outside the company are consulted (RC-5) | 3.33 (1.282) | 1.644 | −0.281 | −1.142 |

| The ICT company is able to learn and create added value through its partners (RC-6) | 3.41 (1.216) | 1.479 | −0.358 | −0.949 |

| The ICT company is proud to be oriented towards strategic partnership (RC-7) | 3.35 (1.248) | 1.557 | −0.302 | −1.045 |

| Strategic alliances of companies affect the productivity of companies (RC-8) | 3.52 (1.188) | 1.411 | −0.402 | −0.892 |

| Strategic alliances of companies affect the profitability of companies (RC-9) | 3.49 (1.218) | 1.483 | −0.343 | −1.074 |

| Strategic alliances of companies affect the market position of companies (RC-10) | 3.60 (1.190) | 1.417 | −0.479 | −0.826 |

| The survey on the satisfaction of the ICT company’s clients shows that they are loyal and satisfied (RC-11) | 3.62 (1.591) | 2.532 | −0.648 | −1.235 |

| When it comes to new business, the ICT company’s customers in the last few years are increasingly choosing the company’s products over competitors (RC-12) | 3.22 (1.191) | 1.417 | −0.114 | −0.996 |

| The ICT company is constantly striving to meet the wishes and needs of its customers with the desire that the customers are always satisfied (RC-13) | 3.54 (1.282) | 1.642 | −0.427 | −1.069 |

| The ICT company invests a lot of time in selecting its suppliers (RC-14) | 3.36 (1.176) | 1.383 | −0.281 | −0.923 |

| The ICT company maintains a long-term relationship with suppliers (RC-15) | 3.38 (1.281) | 1.640 | −0.288 | −1.121 |

| The ICT company has greatly reduced the time required to solve customer problems (RC-16) | 3.35 (1.200) | 1.440 | −0.236 | −1.038 |

| The ICT company is certain that its customers will continue to do business with it (RC-17) | 3.47 (1.244) | 1.548 | −0.382 | −0.998 |

| The ICT company’s relationship with the buyer and supplier affects the company’s productivity (RC-18) | 3.54 (1.208) | 1.459 | −0.396 | −0.982 |

| The ICT company’s relationship with the buyer and supplier affects the company’s profitability (RC-19) | 3.59 (1.232) | 1.518 | −0.481 | −0.951 |

| The ICT company’s relationship with the buyer and supplier affects the market position of the company (RC-20) | 3.65 (1.225) | 1.501 | −0.566 | −0.774 |

| It is important for an ICT company to share customer knowledge with its partners (RC-21) | 3.66 (1.568) | 2.460 | −0.694 | −1.157 |

| The ICT company receives much feedback from customers (RC-22) | 3.30 (1.205) | 1.451 | −0.212 | −0.988 |

| Knowledge of customers is widespread throughout the ICT company (RC-23) | 3.50 (1.285) | 1.650 | −0.440 | −1.061 |

| Customer data are constantly updated (RC-24) | 3.35 (1.171) | 1.372 | −0.274 | −0.951 |

| The ICT company has relatively complete data on customers (RC-25) | 3.51 (1.305) | 1.703 | −0.431 | −1.073 |

| The ICT company is in constant contact with customers to identify their wishes (RC-26) | 3.28 (1.242) | 1.542 | −0.177 | −1.088 |

| The ICT company has a useful and up-to-date information system in use (RC-27) | 3.56 (1.234) | 1.522 | −0.510 | −0.881 |

| Knowledge of customers affects the productivity of the ICT company (RC-28) | 3.47 (1.194) | 1.427 | −0.435 | −0.869 |

| Knowledge of customers affects the profitability of the ICT company (RC-29) | 3.55 (1.217) | 1.481 | −0.441 | −0.944 |

| Knowledge of customers affects the market position of the ICT company (RC-30) | 3.68 (1.175) | 1.380 | −0.500 | −0.840 |

| Relational capital (RC) | 3.46 (0.659) | 1.61 | −0.035 | 0.211 |

| Business Performance | Mean (Std. Dev.) | Variance | Skewness (Std. Error of Skewness = 0.099) | Kurtosis (Std. Error of Kurtosis = 0.197) |

|---|---|---|---|---|

| Leadership in the ICT sector (BP-1) | 3.69 (1.562) | 2.440 | −0.720 | −1.103 |

| Business prospects (BP-2) | 3.13 (1.162) | 1.349 | 0.089 | −0.916 |

| Willingness to react quickly to the actions of competitors (BP-3) | 3.69 (1.257) | 1.581 | −0.602 | −0.841 |

| Success rate in launching new products (BP-4) | 3.20 (1.158) | 1.340 | −0.083 | −0.892 |

| Overall business performance and success (BP-5) | 3.59 (1.264) | 1.597 | −0.513 | −0.896 |

| Employee productivity (BP-6) | 3.31 (1.228) | 1.509 | −0.239 | −0.957 |

| Process productivity (BP-7) | 3.53 (1.244) | 1.548 | −0.477 | −0.869 |

| Sales growth (BP-8) | 3.40 (1.203) | 1.447 | −0.269 | −0.937 |

| Profit growth (BP-9) | 3.44 (1.201) | 1.443 | −0.319 | −0.929 |

| Market position of the ICT company (BP-10) | 3.49 (1.218) | 1.483 | −0.290 | −1.007 |

| Share of export profits in the ICT company turnover (BP-11) | 3.45 (1.249) | 1.560 | −0.331 | −0.937 |

| Business performance (BP) | 3.45 (0.791) | 1.57 | −0.244 | −0.248 |

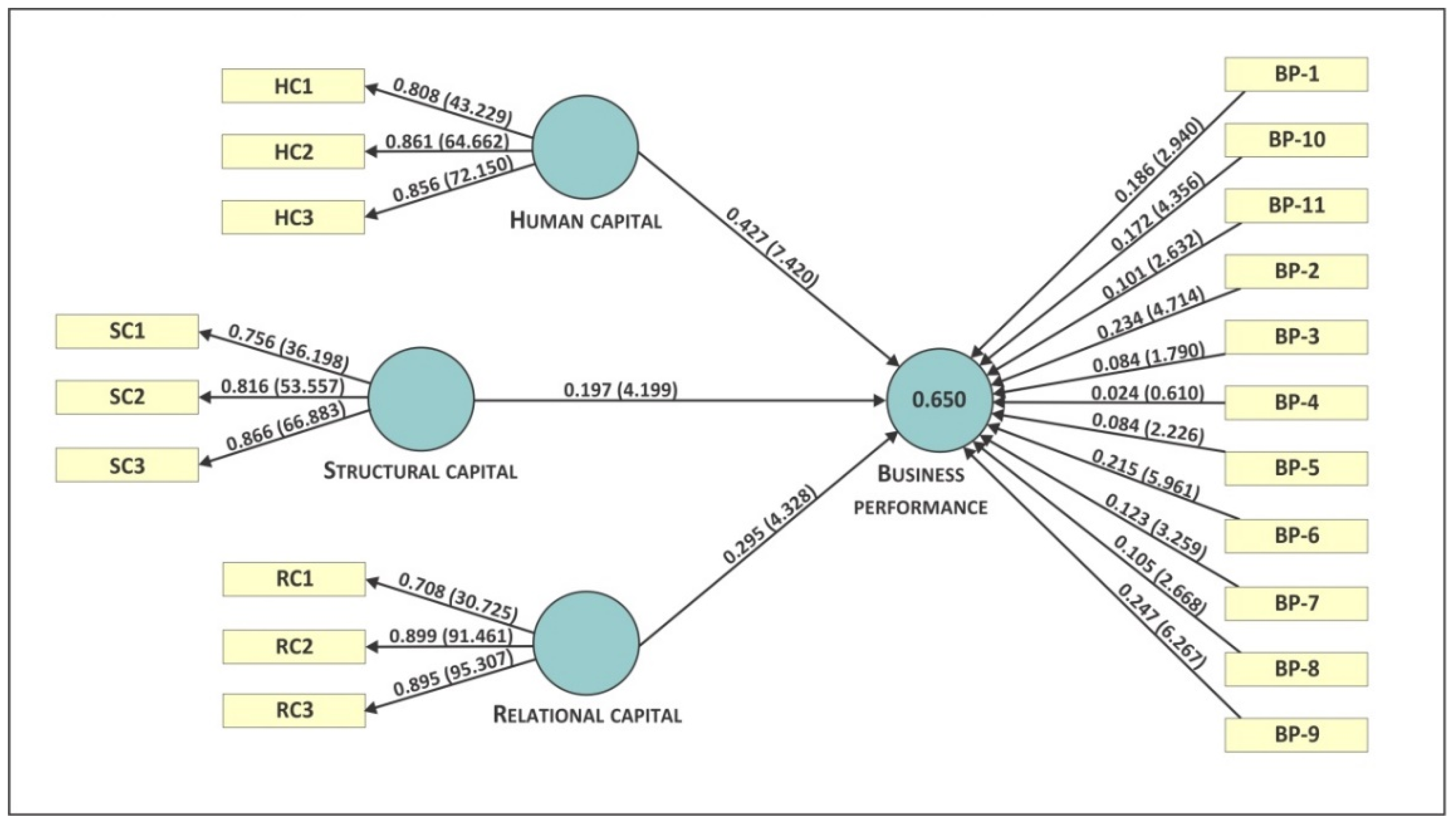

| Variable | Factor Loadings (Path Coefficients) | |

|---|---|---|

| Human Capital | Competences, training and development of employees (HC-1) | 0.808 |

| Learning and development, productivity and teamwork (HC-2) | 0.861 | |

| Innovation and creativity (HC-3) | 0.856 | |

| Structural Capital | Organizational structure, processes and procedures (SC-1) | 0.756 |

| Patents, licenses and copyrights (SC-2) | 0.816 | |

| Leadership and organizational learning (SC-3) | 0.866 | |

| Relational Capital | Cooperation and customer knowledge (RC-1) | 0.708 |

| Strategic alliances, customer and supplier loyalty (RC-2) | 0.899 | |

| Relations with customers and suppliers (RC-3) | 0.895 |

| Relationship | Total Effects | Hypothesis Confirmation |

|---|---|---|

| Human capital → Business performance | 0.427 *** | + |

| Structural capital → Business performance | 0.197 *** | + |

| Relational capital → Business performance | 0.295 *** | + |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lekić, N.; Carić, M.; Soleša, D.; Vapa Tankosić, J.; Rajaković-Mijailović, J.; Bogetić, S.; Vučičević, M. Employees’ Perceptions on the Relationship of Intellectual Capital and Business Performance of ICT Companies. Sustainability 2022, 14, 275. https://doi.org/10.3390/su14010275

Lekić N, Carić M, Soleša D, Vapa Tankosić J, Rajaković-Mijailović J, Bogetić S, Vučičević M. Employees’ Perceptions on the Relationship of Intellectual Capital and Business Performance of ICT Companies. Sustainability. 2022; 14(1):275. https://doi.org/10.3390/su14010275

Chicago/Turabian StyleLekić, Nemanja, Marko Carić, Dragan Soleša, Jelena Vapa Tankosić, Jasmina Rajaković-Mijailović, Srđan Bogetić, and Marko Vučičević. 2022. "Employees’ Perceptions on the Relationship of Intellectual Capital and Business Performance of ICT Companies" Sustainability 14, no. 1: 275. https://doi.org/10.3390/su14010275

APA StyleLekić, N., Carić, M., Soleša, D., Vapa Tankosić, J., Rajaković-Mijailović, J., Bogetić, S., & Vučičević, M. (2022). Employees’ Perceptions on the Relationship of Intellectual Capital and Business Performance of ICT Companies. Sustainability, 14(1), 275. https://doi.org/10.3390/su14010275