The Effects of Environmental Regulation on Investment Efficiency—An Empirical Analysis of Manufacturing Firms in the Beijing–Tianjin–Hebei Region, China

Abstract

:1. Introduction

- What is the effect of environmental regulation on the investment efficiency of listed manufacturing companies in the Beijing–Tianjin–Hebei region?

- What is the impact mechanism of environmental regulation on the investment efficiency of listed manufacturing companies in the Beijing–Tianjin–Hebei region?

2. Case Overview

3. Literature Review

3.1. Relationship between Environmental Regulation and Enterprise Investment

3.2. Research on the Threshold Effect of Environmental Regulation

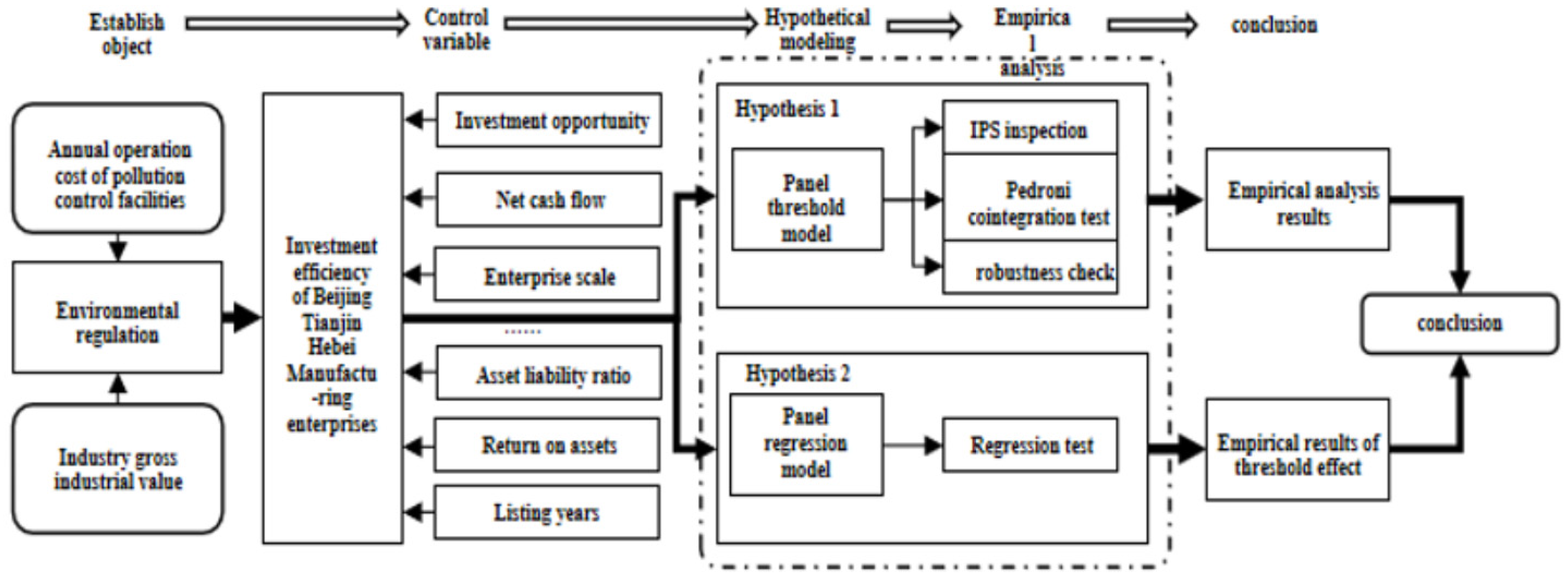

4. Methodology

4.1. Research Design

4.2. Sample Selection and Data Processing

4.3. Measurement of Environmental Regulation

4.4. Measurement of Investment Efficiency

4.5. Control Variables

4.6. Research Model Design

4.7. Establishment of Panel Threshold Model

5. Model Testing

5.1. Data Stationery Test

5.2. Cointegration Test

5.3. Panel Regression Results

5.4. Model Robustness Test

6. Analysis of Threshold Effect

7. Discussion

8. Conclusions

8.1. Summary

8.2. Key Findings

- (1)

- The whole impact of environmental regulation on investment efficiency is negative. Environmental regulation can affect the sensitivity of investment expenditure to investment opportunities by affecting investment opportunities and investment expenditure, that is, investment efficiency. But because there are simultaneous positive and negative effects: environmental regulation may reduce investment efficiency by causing over-investment or underinvestment and may also promote the innovation and transformation of enterprises in order to improve investment efficiency, so the negative impact is not significant.

- (2)

- The intensity of environmental regulation has a “threshold effect”; that is, there is a threshold value of environmental regulation, which tends to improve the impact on enterprise investment efficiency, but this role is not significant. When the intensity of environmental regulation is higher than the threshold value of 2.2358, environmental regulation has a significant inhibitory effect on the investment efficiency of enterprises.

8.3. Policy Implications

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Wang, C. Study of the Relationship of Inflation and Investment Efficiency in China; Dongbei University of Finance and Economics: Dalian, China, 2011. [Google Scholar]

- Pashigian, B.P. The effect of environmental regulation on optimal plant size and factor shares. J. Law Econ. 1984, 27, 1–28. [Google Scholar] [CrossRef]

- Wan, M.Y. Analysis on the influencing factors and mechanism of enterprise investment efficiency in China. Co-Oper. Econ. Sci. 2018, 64–67. Available online: https://www.baidu.com/link?url=usa661TiQEALvRNK5vUatr2ANemalumnqsRxmWYnq6tJO9FZKtd2MV1cOLI_AK9oyjB8V-6yv5TbdP-GGkyXWyI5dI-FGrz1EXQ9HpPoc2EZI6yluzaRP2mi4l94iygc&wd=&eqid=9cec124a0005a07900000002628b21f1 (accessed on 9 February 2022).

- Liu, H.; Liu, Z. Recycling utilization patterns of coal mining waste in China. Resour. Conserv. Recycl. 2010, 54, 1331–1340. [Google Scholar]

- Zhou, X.H. Enterprise Green Investment Decisions Oriented to Circular-economy: Status Quo, Problems and Solutions. Commer. Sci. Res. 2021, 42, 29–34. [Google Scholar]

- Chen, L.; Huang, J.; Cao, F.; Zhou, Z.B. Executive shareholding, economic policy uncertainty and corporate green investment. Theory Pract. Financ. Econ. 2021, 3, 58–64. [Google Scholar]

- Tan, Y.W. Environmental regulation and technological innovation: A literature review on “Porter Hypothesis”. Mod. Bus. 2021, 32, 138–140. [Google Scholar]

- Sheng, P.F.; Wei, H.H. Environmental regulation and global value chain enhancement in China’s industrial sector: An empirical re-examination on Poter Hypothesis. Mod. Financ. Econ.-J. Tianjin Univ. Financ. Econ. 2020, 40, 85–98. [Google Scholar]

- Zhou, G.C.; Liu, W.D.; Zhang, L.M.; She, K.W. Can Environmental Regulation Flexibility Explain the Porter Hypothesis?—An Empirical Study Based on the Data of China’s Listed Enterprises. Sustainability 2019, 11, 2214. [Google Scholar] [CrossRef] [Green Version]

- Li, G.P. Coordinated development of Beijing, Tianjin and Hebei: Current situation, problems and direction. Front 2020, 1, 59–62. [Google Scholar]

- An, L. Collaborative Development and Effective Governance: System Optimization of Pollution Control in Beijing, Tianjin and Hebei. J. Hebei Univ. Environ. Eng. 2019, 29, 54–56. [Google Scholar]

- Tian, C.X.; Li, H.Y. Comparative Analysis of Environmental Regulations in Beijing, Tianjin and Hebei and Their Effects. Sustain. Dev. 2021, 11, 17–25. [Google Scholar] [CrossRef]

- Zheng, X.J.; Wang, D.H. Ecological environment management strategy in the Beijing-Tianjin-Hebei region. Co-Oper. Econ. Sci. 2016, 15, 36–37. [Google Scholar]

- Liu, Y.; Li, S.Y. Effectiveness and Coordination of Local Environmental Policies in Beijing-Tianjin-Hebei Region. Rev. Econ. Trends 2020, 1, 170–186. [Google Scholar]

- Yu, H.L. Analysis on Synergy of Environmental Governmental Governance Policies in the Beijing-Tianjin-Hebei Region; Yanshan University: Qinhuangdao, China, 2021; Volume 6. [Google Scholar]

- Sharma, S. Managerial Interpretations and Organizational Context as Predictors of Corporate Choice of Environmental Strategy. Acad. Manag. J. 2000, 43, 681–697. [Google Scholar]

- Paulsson, F.; Malmborg, F.V. Carbon dioxide emission trading, or not? An institutional analysis of company behavior in Sweden. Corp. Soc. Responsib. Environ. Manag. 2004, 11, 211–221. [Google Scholar]

- Piot-Lepetit, I.; Le Moing, M. Productivity and Environmental Regulation: The Effect of the Nitrates Directive in the French Pig Sector. Environ. Resour. Econ. 2007, 38, 433–446. [Google Scholar] [CrossRef]

- Chintrakarn, P. Environmental regulation and U.S. states’ technical inefficiency. Econ. Lett. 2008, 100, 363–365. [Google Scholar] [CrossRef]

- Stoever, J.; Weche, J.P. Environmental regulation and sustainable competitiveness: Evaluating the role of firm-level green investments in the context of the Porter Hypothesis. Environ. Resour. Econ. 2018, 70, 429–455. [Google Scholar] [CrossRef] [Green Version]

- Andrea, L.; Arno, P.; Hannes, W.L. Environmental regulation and investment: Evidence from European industry data. Ecol. Econ. 2011, 70, 759–770. [Google Scholar]

- Ramanathan, R.; Ramanathan, U.; Bentley, Y. The debate on flexibility of environmental regulations, innovation capabilities and financial performance—A novel use of DEA. Omega 2017, 75, 131–138. [Google Scholar] [CrossRef] [Green Version]

- Song, H.X. Research on the Effects of Environmental Regulation on Firms Investment Efficiency—An Empirical Analysis of Chinese Listed Manufacturing Firms; Dongbei University of Finance & Economics: Dalian, China, 2016. [Google Scholar]

- Garcia-Quevedo, J.; Jove-Llopis, E. Environmental policies and energy efficiency investments. An industry-level analysis. Energy Policy 2021, 156, 112461. [Google Scholar] [CrossRef]

- Wu, F.; Fu, X.P.; Zhang, T.; Wu, D.; Sindakis, S. Examining whether government environmental regulation promotes green innovation efficiency-evidence from China’s Yangtze River Economic Belt. Sustainability 2022, 14, 1827. [Google Scholar] [CrossRef]

- Zhang, J. The Impact of Environmental Regulation on Corporate Environmental Investment; Nanjing University of Aeronautics and Astronautics: Nanjing, China, 2016. [Google Scholar]

- Yao, D.; Jiang, L.; Zhou, Y.D. The Impact of Environmental Regulations on Private Investment Efficiency. In Proceedings of the 5th International Conference on Industrial Economics System and Industrial Security Engineering, Toronto, ON, Canada, 3–6 August 2018. [Google Scholar]

- Feng, Z.J.; Zeng, B.; Ming, Q. Environmental Regulation, Two-Way Foreign Direct Investment, and Green Innovation Efficiency in China’s Manufacturing Industry. Int. J. Environ. Res. Public Health 2018, 15, 2292. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Jaffe, A.B.; Palmer, K. Environmental regulation and innovation: A panel data study. Rev. Econ. Stat. 1997, 79, 610–619. [Google Scholar] [CrossRef]

- Brunnermeier, S.B.; Cohen, M.A. Determinants of environmental innovation in US manufacturing industries. J. Environ. Econ. Manag. 2003, 45, 278–293. [Google Scholar] [CrossRef]

- Hamamoto, M. Environmental regulation and the productivity of Japanese manufacturing industries. Resour. Energy Econ. 2006, 28, 299–312. [Google Scholar] [CrossRef]

- Pan, X.F.; Ai, B.W.; Li, C.Y.; Pan, X.Y.; Yan, Y.B. Dynamic relationship among environmental regulation, technological innovation and energy efficiency based on large scale provincial panel data in China. Technol. Forecast. Soc. Chang. 2019, 144, 428–435. [Google Scholar] [CrossRef]

- Yang, Y.L.; Song, W.F. Environmental regulation’s long-term and short-term heterogeneity effect on industrial Green Total Factor Productivity. West Forum Econ. Manag. 2020, 31, 81–88. [Google Scholar]

- Zhou, H.N. Internal control and environmental policy for environmental protection investment in enterprises. Commun. Financ. Account. 2019, 6, 88–91. [Google Scholar]

- Wang, X.H.; Wang, M.Y. Research on the impact of environmental regulation and government subsidies on the investment efficiency of listed manufacturing companies. Inn. Mong. Sci. Technol. Econ. 2020, 14, 37–40. [Google Scholar]

- Li, T. Environmental regulation policy and enterprise investment efficiency. Commun. Financ. Account. 2021, 20, 26–29, 74. [Google Scholar]

- Shen, N.; Liu, F.C. Can intensive environmental regulation promote technological innovation? Porter Hypothesis Reexamined. China Soft Sci. 2012, 4, 49–59. [Google Scholar]

- Su, H. Research on the Influence of Environmental Regulation on the Scale and Efficiency of Enterprise Environmental Protection Investment. Master’s Thesis, Jiangsu University, Zhenjiang, China, 2018. [Google Scholar]

- Conrad, K.; Wastl, D. The impact of environmental regulation on productivity in German industries. Empir. Econ. 1995, 20, 615–633. [Google Scholar] [CrossRef]

- Lanoie, P.; Patry, M.; Lajeunesse, R. Environmental regulation and productivity: Testing the Porter Hypothesis. J. Product. Anal. 2008, 30, 121–128. [Google Scholar] [CrossRef]

- Pang, M.C.; Ning, F.X. Local government investment and resource mismatch in the perspective of economic transformation: The threshold effect of environmental regulation and the moderating effect of state-owned enterprise dependence. West Forum 2021, 31, 1–17. [Google Scholar]

- Song, W.X.; Han, W.H. Environmental regulation, OFDI and industrial structure upgrading—Also on the threshold effect of heterogeneous environmental regulation. Mod. Econ. Sci. 2021, 43, 109–122. [Google Scholar]

{kind=link}

| Variables | t-Bar | W[t-Bar] | p-Value | Stationarity |

|---|---|---|---|---|

| −3.296 | −18.257 | 0.000 | Y | |

| −2.324 | −8.445 | 0.000 | Y | |

| −1.896 | −4.122 | 0.000 | Y | |

| −1.739 | −2.535 | 0.006 | Y | |

| −1.993 | −5.103 | 0.000 | Y | |

| −2.191 | −7.1 | 0.000 | Y | |

| −2.781 | −13.058 | 0.000 | Y | |

| −1.535 | −0.479 | 0.006 | Y |

| Statistic | p-Value | |

|---|---|---|

| Modified Phillips–Perron test | 26.8105 | 0.0000 |

| Phillips–Perron test | −9.6828 | 0.0000 |

| Augmented Dickey–Fuller test | 22.7401 | 0.0000 |

| Coef. | Std. Err. | t | p-Value | |

|---|---|---|---|---|

| 0.0033783 *** | 0.0011367 | 2.97 | 0.003 | |

| 0.0063069 | 0.0055841 | 1.13 | 0.259 | |

| −0.0038093 *** | 0.0013031 | −2.92 | 0.004 | |

| −0.0371227 * | 0.0212962 | −1.74 | 0.082 | |

| −0.0124431 | 0.0127347 | −0.98 | 0.329 | |

| −0.0001564 | 0.003236 | −0.05 | 0.961 | |

| −0.0026413 | 0.123079 | −0.21 | 0.830 | |

| 0.0412172 * | 0.0240414 | 1.71 | 0.087 | |

| 0.0938498 | 0.0882991 | 1.06 | 0.288 | |

| R-sq | 0.2242 | |||

| F-test | 14.51 *** | |||

| Coef. | Std. Err. | t | p-Value | |

|---|---|---|---|---|

| 0.0030931 *** | 0.0015462 | 2.37 | 0.004 | |

| 0.0045164 | 0.0046324 | 1.34 | 0.221 | |

| −0.0029864 *** | 0.0019643 | −2.78 | 0.002 | |

| −0.0562468 * | 0.0362462 | −1.64 | 0.081 | |

| −0.0236537 | 0.0174253 | −0.87 | 0.313 | |

| −0.0001534 | 0.002783 | −0.05 | 0.932 | |

| −0.0029532 | 0.174263 | −0.26 | 0.821 | |

| 0.0535143 * | 0.0362542 | 1.85 | 0.086 | |

| 0.0685438 | 0.0964253 | 1.21 | 0.254 | |

| R-sq | 0.2554 | |||

| F-test | 12.35 *** | |||

| Threshold Number | F-Value | p Value | Threshold Value | 10% | 5% | 1% |

|---|---|---|---|---|---|---|

| Single | 17.47 ** | 0.0333 | 2.2358 | 13.18 64 | 16.1936 | 21.1981 |

| Double | 5.00 | 0.5800 | 2.2358 | 13.70 38 | 18.165 51 | 24.4599 |

| 0.4336 | ||||||

| Triply | 5.88 | 0.4100 | 2.2358 | 12.2595 | 14.81/43 | 19.68/78 |

| 0.4703 | ||||||

| 0.4336 |

| Coef. | t-Value | p-Value | |

|---|---|---|---|

| 0.0018156 * | 1.36 | 0.092 | |

| −0.0050565 *** | −4.24 | 0.000 | |

| −0.039362 * | −1.87 | 0.061 | |

| −0.0137783 | −1.09 | 0.276 | |

| −0.0015878 | −0.51 | 0.613 | |

| −0.007169 | −0.59 | 0.555 | |

| 0.0486278 ** | 2.07 | 0.039 | |

| −0.006699 *** | −9.17 | 0.000 | |

| 0.161001 ** | 2.46 | 0.014 | |

| R-sq | 0.2240 | ||

| F-Value | 27.43 *** | ||

| Threshold and Interval | Industry |

|---|---|

| Agricultural and sideline products processing industry, food manufacturing industry, wine, beverage and refined tea manufacturing industry, textile industry, textile clothing, clothing industry, leather, fur and feather products and footwear, printing and recording media reproduction, rubber and plastic products, metal products, general equipment manufacturing, special equipment manufacturing, transportation equipment manufacturing, electrical machinery and equipment manufacturing, computer, communications and other electronic equipment manufacturing, instrumentation manufacturing | |

| Petroleum processing, coking and nuclear fuel processing, chemical raw materials and chemical products manufacturing, pharmaceutical manufacturing, non-metallic mineral products industry, ferrous metal smelting and calendering industry, non-ferrous metal smelting and calendering industry |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Qi, P.; Shang, Y.; Han, F. The Effects of Environmental Regulation on Investment Efficiency—An Empirical Analysis of Manufacturing Firms in the Beijing–Tianjin–Hebei Region, China. Sustainability 2022, 14, 6371. https://doi.org/10.3390/su14106371

Qi P, Shang Y, Han F. The Effects of Environmental Regulation on Investment Efficiency—An Empirical Analysis of Manufacturing Firms in the Beijing–Tianjin–Hebei Region, China. Sustainability. 2022; 14(10):6371. https://doi.org/10.3390/su14106371

Chicago/Turabian StyleQi, Peng, Yu Shang, and Fang Han. 2022. "The Effects of Environmental Regulation on Investment Efficiency—An Empirical Analysis of Manufacturing Firms in the Beijing–Tianjin–Hebei Region, China" Sustainability 14, no. 10: 6371. https://doi.org/10.3390/su14106371

APA StyleQi, P., Shang, Y., & Han, F. (2022). The Effects of Environmental Regulation on Investment Efficiency—An Empirical Analysis of Manufacturing Firms in the Beijing–Tianjin–Hebei Region, China. Sustainability, 14(10), 6371. https://doi.org/10.3390/su14106371