Management, Cooperatives and Sustainability: A New Methodological Proposal for a Holistic Analysis

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction: Theoretical Approaches

- The new globalisation. A new geostrategic correlation is developing that has a direct bearing on geopolitics and geoeconomics. This translation is of vital importance for understanding the new frame of reference through which globalisation is evolving and which basically focuses on the configuration of new poles of activity generation on a planetary scale and on the role that traditional actors and developing regions are taking on. By way of summary, we identify six key movements that explain the new globalisation [1,2,3,4,5]:

- Europe, which is seeking to grow eastwards, is doing so with certain difficulties, stemming from the convergence between the new member states and the more established ones. In relational terms, the south (Spain in particular) can act as a strategic link between the North African coast and the European Union.

- An Asian space in full expansion, with two clear dominators: China and India.

- A third area is Latin America, with a diffused economic leadership between Mexico and Brazil.

- Fourthly, sub-Saharan Africa, separated from North Africa. An area rich in resources but devoid of political, social, and tribal cohesion, with perennial wars. It has become, within its extreme social poverty, a fundamental target for new capitalist expansions.

- The upheaval caused by Russia’s attitude to the war initiated by Putin in Ukraine. Especially regarding its status as a nuclear power with imperialist pretensions towards the easternmost part of Europe and territories rich in natural and geostrategic resources.

- Finally, the sixth major economic area is the United States, a nuclear power in crisis, questioned in the new dynamism of globalisation but still with latent capabilities in the different fields of scientific and applied knowledge.

- 2.

- Climate change is a transcendental phenomenon that we consider in our analysis. The literature and international organisations agree that climate change is the most far-reaching challenge facing humanity. In this context, we believe that cooperatives and other forms of social economy enterprises have a significant role to play in tackling this challenge. Their idiosyncrasies and understanding of production and management make them key players in building a sustainable development model. There is sufficient evidence to support the view that the climate issue is going to become the most influential and determining economic axis, and the one that will end up conditioning the strategies of companies that want to adapt to these externalities in order to try to correct them [8]. Hence the relevance of establishing new methodologies and metrics (already explored in regional and macroeconomic studies) to complement business analysis [9]. The aspects that we have described lead us to seek the concretion of the business analysis. In this sense, we think that cooperatives constitute an organisational model that has positive factors in different fields: the social aspect; complicity of leaders and workers; agreed objectives in many cases; concern for adapting to very competitive markets, but under ethical precepts that, in general, are social; concern about environmental externalities; transparent accountability. For these reasons, it has been considered appropriate to focus the analysis on this business typology, in contrast to other organisation models. Cooperatives and Social Economy companies focus their business model on people, social responsibility and trying to incorporate in all phases of their activity values such as participation, transparency, democracy, solidarity, social cohesion, and the promotion of responsible consumption. Therefore, a characteristic element of the social economy is its ability to promote social transformation from the business model itself.

2. Theoretical Background Section

2.1. Cooperatives in the Face of New Challenges

2.2. The Enterprise Faced with New Challenges: The Environmental Emphasis

2.3. Insufficient Metrics: A New Economic Paradigm to Develop

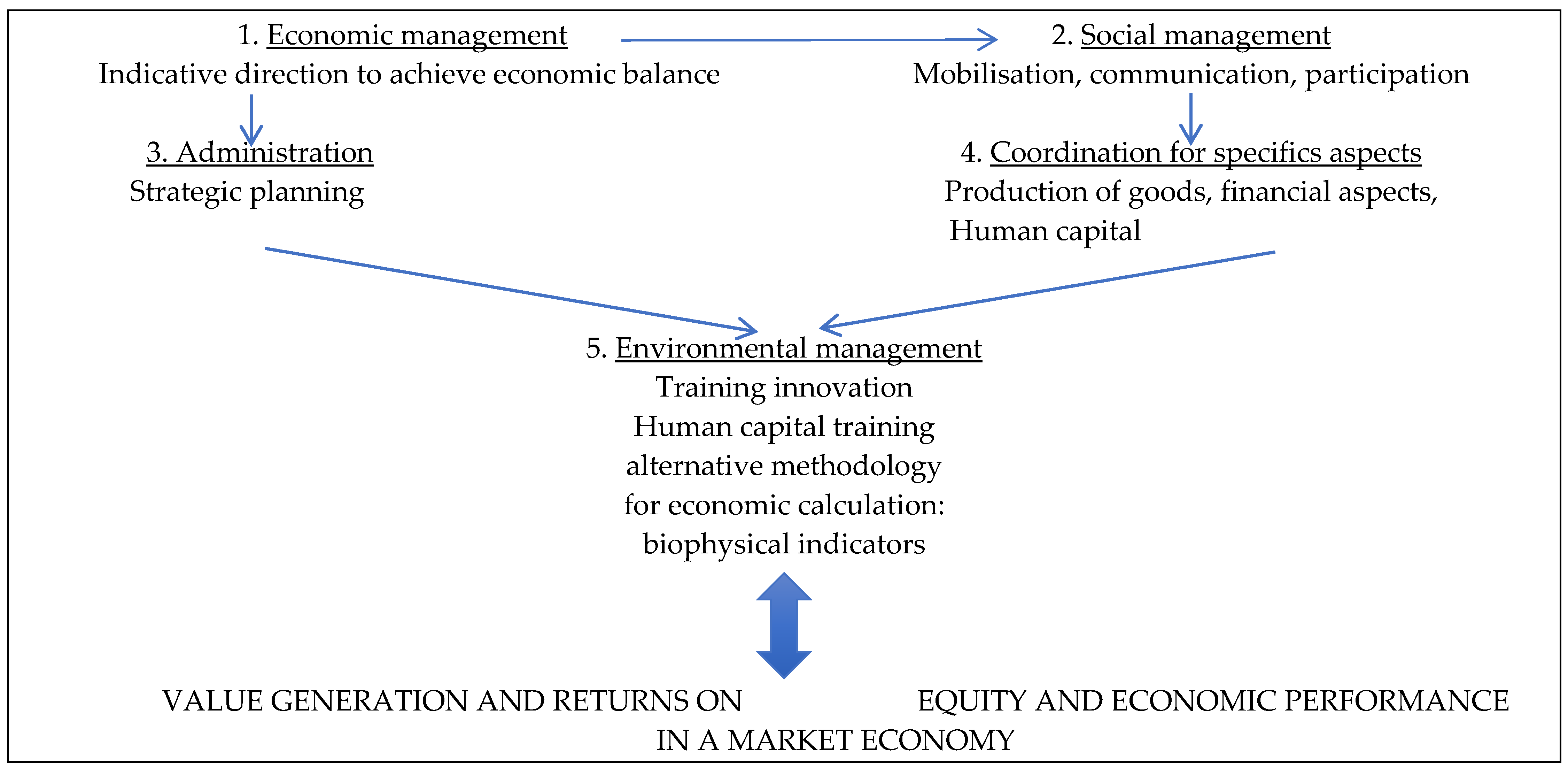

2.4. Some Theoretical Proposals

- They do not present insurmountable methodological difficulties for data collection and subsequent calculation, so that they can be perfectly assumed as a scorecard by policy makers. The quality and profusion of statistical services will mark the research route to be followed.

- They mix magnitudes of a chrematistic nature (GDP, GDP per capita, for example) with others of a more specific biophysical nature (MSW production, energy, and water consumption), illustrative of the externalities of growth.

- They do not neglect the social side of the growth process by incorporating data on inequality (Gini index) and consumption capabilities (through wage indicators).

- They help to identify the ecological externalities of economic growth.

- They provide a different reading of the growth process since they specify and systematise dispersed variables that do not usually appear in the regular diagnoses of public administrations.

- Prescott-Allen’s Ecosystem Wellbeing Index [61], which measures ecosystem diversity, ecosystem quality, and quality of life, covering 180 countries for the time period (1997–1999), using 51 variables.

- Environmental Performance Index, Yale University, which has two dimensions, environmental health and ecosystem vitality, 24 variables, covering 180 countries and the years 2014–2016.

- Environment and Gender Index, International Union for Conservation of Nature (IUCN), of the United Nations [62], which measures gender equality and women’s empowerment in the environmental field.

- Environmental Vulnerability Index, which measures the vulnerability of the natural environment to future natural and anthropogenic shocks. It covers 234 countries for the period 2000–2003 and is based on 50 indicators.

- Sustainable Society Index, which measures the level of sustainability of a country and monitors it, aggregating three dimensions: human well-being, environmental well-being, and economic well-being; it is based on 21 variables, covers 154 countries and the time period is 2006–2018.

3. Results and Discussion

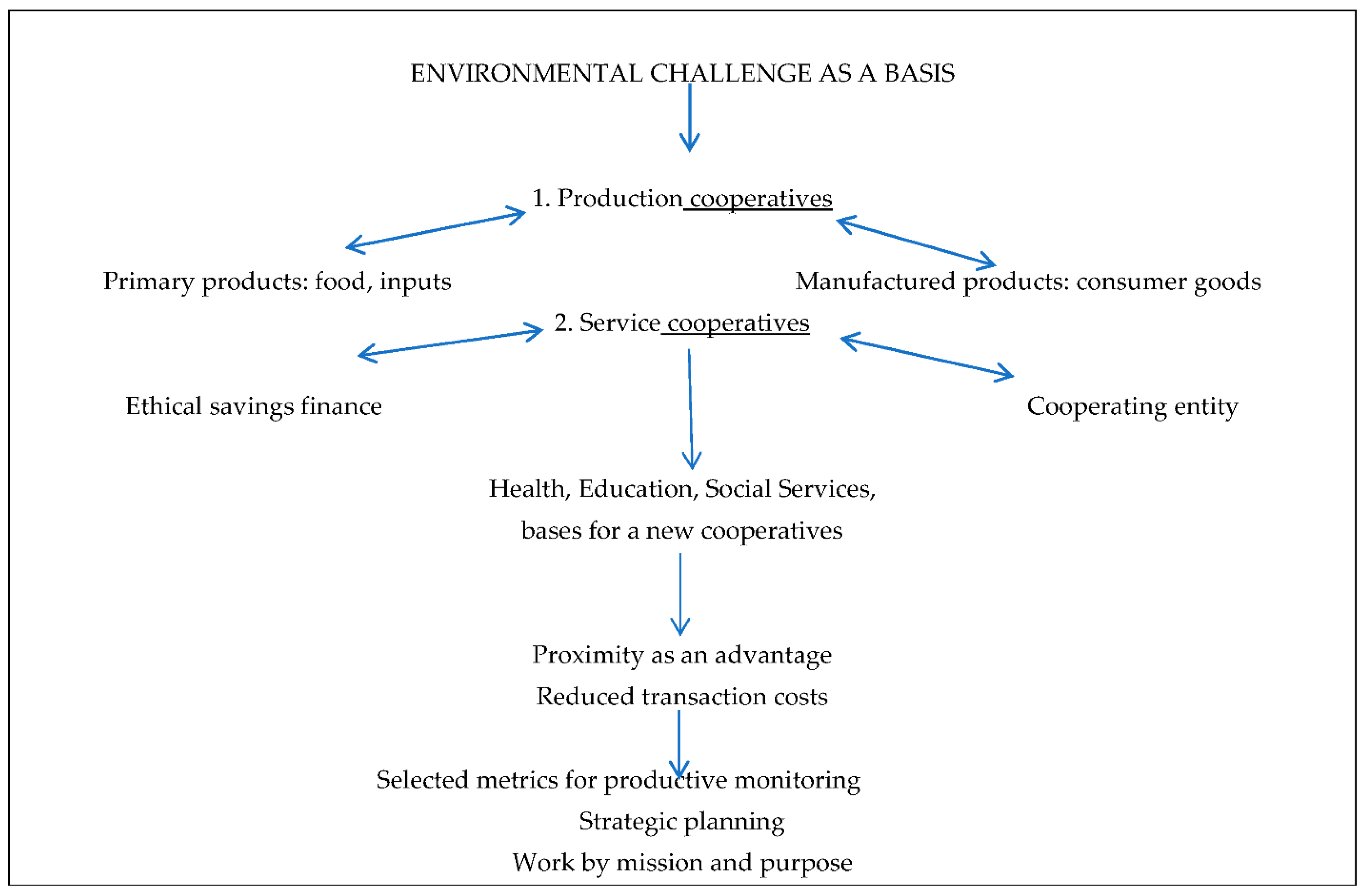

Indicators for Cooperatives

- Company profitability

- Company valuation

- Compensation related to the labour market

- The variables that respond most efficiently to the dynamics comparable with for-profit entities, in which the magnitudes are extracted from the information contained in the financial statements; for example: net profit, level of assets, equity, factors that relate to the contributions made by their members and, on these bases, offer products and services that generate a cooperative surplus.

- From a renewed and alternative point of view, it is necessary to specify those indicators that link up with more holistic horizons, not strictly limited to the most chrematistic theses. The descriptions provided in previous sections help to guide these choices, hence the crucial importance of this framework. The importance is that choosing the right indicators should also facilitate the ability to compare with other co-operatives and/or different enterprises. In other words, in addition to the results with a more conventional profile, others of a quite different nature must also be included. Among the former, the following should be highlighted, oriented towards compliance with the established production plan:

- Productivity

- Total economic results

- Sales

- Liquidity

- The cost of sales

- The costs of the production process

- Quality parameters, if applicable

As for the latter, and depending on what has been explained in previous parts of the text, the following can be considered:- The physical results of production (necessary indicator for the preceding block)

- Greenhouse gas emissions of the cooperative

- The energy intensity of production

- The economic circularity strategy, measured in terms of proximity parameters

- Waste production

- The measure of recycling

- The connection of the co-operative with other complementary, positive situational incomes

- The percentage of women with the same wage level as men

- The deviation, if any, in relation to the SMI.

- In agriculture and fisheries, by reviewing energy use and emissions

- To consumers, by seeking to reduce carbon footprints in shops, nested activities, and those of suppliers. We are actively working to disseminate education to members and consumers

- In housing, with the use of sustainable building materials and green building design.

- In the financial sector, with co-operative banks and credit unions, incentivising investments in energy efficient technologies

- In the energy sector, with the aim of providing clean and sustainable energy such as wind, solar and biofuels

4. Conclusions

- (a)

- The lack of statistical regularity to obtain the necessary indicators, which have been pointed out in the investigation. This affects both the macroeconomic and microeconomic spheres. There is no tradition of descriptive statistics that addresses environmental problems. At this point, the researcher must literally dive into different databases to obtain those that meet the essential requirements. The most important of them is homogeneity, that is, the ability to make contrasts with other countries in the macro sphere and companies in the micro sphere.

- (b)

- The applicability of mathematical models to the panel of data obtained: econometric methods of causality, development of regressions with comparisons between indicators, etc.

- (c)

- In the microeconomic context, access to business data. There are many reluctances on the part of managers of companies to provide figures and magnitudes of their daily operations. This is an important entry barrier that the researcher must overcome with other resources (consultations, for example, of information of a commercial nature deposited in commercial registries, where companies must communicate specific results).

- (a)

- The justification of cooperatives as economic analysis laboratories, in which indicators that have already been verified in regional economies are adopted and must be adapted to the microeconomic sphere.

- (b)

- The fixing of those indicators that affect determining aspects in the operation of the companies. Not only the income statement, but also the waste they generate, the specific parameters of the circular economy they develop, the energy intensity they consume, and the emissions they cause are crucial elements that, increasingly, are going to be incorporated, with great force, into the analysis of the economy.

- (c)

- The linking of the two previous points with a broader context: the new globalisation and climate change, with specific challenges that have been detailed and commented on in the previous pages.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Baldwin, R. EAEA16 Keynote Address: The Future of Globalization. Asian Econ. J. 2019, 33, 3–12. [Google Scholar] [CrossRef] [Green Version]

- Barthe-Dejean, G. Shifting paradigms: Regionalisation and the post-COVID-19 risk matrix. J. Risk Manag. Financ. Inst. 2021, 14, 355–366. [Google Scholar]

- Bekkers, E.; Schroeter, S. An Economic Analysis of the US-China Trade Conflict; WTO Staff Working. Paper No. ERSD-2020-04; WTO: Geneva, Switzerland, 2020. [Google Scholar]

- Yang, C.; Yuen-Tung, D. Market Expansion of Domestic Gaming Firms in Shenzhen, China: Dilemma of Globalisation and Regionalisation. J. Econ. Hum. Geogr. 2021, 112, 256–273. [Google Scholar] [CrossRef]

- Kataryniuk, I.; Javier Perez, J.; Viani, F. (De-)Globalisation of Trade and Regionalisation: A Survey of the Facts and Arguments; Banco de España Occasional Paper No. 2124; Banco de España: Madrid, Spain, 2021. [Google Scholar]

- Grosse, R.; Trevino, L. New institutional economics and FDI location in Central and Eastern Europe. MIR: Manag. Int. Rev. 2005, 45, 123–145. [Google Scholar]

- Wright, M.; Filatotchev, I.; Hoskisson, R.E.; Peng, M.W. Strategy research in emerging economies: Challenging the conventional wisdom. J. Manag. Stud. 2005, 42, 1–33. [Google Scholar] [CrossRef]

- Hoffman, A.; Woody, J. Climate Change: What’s Your Business Strategy? Harvard Business Press: Boston, MA, USA, 2008. [Google Scholar]

- Manera, C.; Serrano, E.; Pérez-Montiel, J.; Buil-Fabregà, M. Construction of Biophysical Indicators for the Catalan Economy: Building a New Conceptual Framework. Sustainability 2021, 13, 7462. [Google Scholar] [CrossRef]

- Rowley, C.; Benson, J. Globalization and Labour in the Asia Pacific Region; FrankCass Publishers: London, UK, 2000. [Google Scholar]

- Lardy, N. Integrating China in the World Economy; Brookings Institution Press: Washington, DC, USA, 2002. [Google Scholar]

- Studwell, J. The China Dream. The Elusive Quest for the Greatest Untapped Market on Earth; Profile Book: London, UK, 2002. [Google Scholar]

- Maddison, A. L’Économie Chinoise. Une Perspective Historique; OECD: Paris, France, 1998. [Google Scholar]

- Wang, H.; Fidrmuc, J.; Luo, O. A spatial analysis of inward FDI and urban–rural wage inequality in China. Econ. Syst. 2021, 45, 100902. [Google Scholar] [CrossRef]

- Hou, L.; Li, K.; Li, Q.; Ouyang, M. Revisiting the location of FDI in China: A panel data approach with heterogeneous shocks. J. Econom. 2021, 221, 483–509. [Google Scholar] [CrossRef]

- Tongxin, A.; Xu, C.; Liao, X. The impact of FDI on environmental pollution in China: Evidence from spatial panel data. Environ. Sci. Pollut. Res. 2021, 28, 44085–44097. [Google Scholar]

- Lemoine, F. L’Économie Chinoise; La Découverte: Paris, France, 2003. [Google Scholar]

- Apergis, N.; Giray, G.; Keung, C.; Lau, M. Globalization and environmental problems in developing countries. Environ. Sci. Pollut. Res. 2021, 28, 33719–33721. [Google Scholar] [CrossRef]

- Kyove, J.; Streltsova, K.; Odibo, U.; Cirella, G. Globalization Impact on Multinational Enterprises. World 2021, 2, 216–230. [Google Scholar] [CrossRef]

- Ma, T.; Wang, Y. Globalization and environment: Effects of international trade on emission intensity reduction of pollutants causing global and local concerns. J. Environ. Manag. 2021, 297, 113249. [Google Scholar] [CrossRef]

- Aluko, O.A.; Opoku, E.E.O.; Ibrahim, M. Investigating the environmental effect of globalization: Insights from selected industrialized countries. J. Environ. Manag. 2021, 281, 111892. [Google Scholar] [CrossRef]

- Salazar, S. Las cooperativas como organizaciones inteligentes para disminuir la desigualdad social. Rev. Centroam. Adm. Pública 2021, 80, 86–98. [Google Scholar] [CrossRef]

- Onyekachi, O. Capitalization and Co-operative Competitiveness: The Linkage. Hub Int. J. Entrep. Coop. Stud. 2020, 3, 34–44. [Google Scholar]

- Bretos, I.; Díaz-Foncea, M.; Marcuello, C. Cooperativas e internacionalización: Un análisis de las 300 mayores cooperativas del mundo. Rev. Econ. Pública Soc. Y Coop. 2018, 92, 5–37. [Google Scholar] [CrossRef]

- Bretos, I.; Marcuello, C. Revisiting globalization challenges and opportunities in the development of cooperatives. Ann. Public Coop. Econ. 2017, 88, 47–73. [Google Scholar] [CrossRef] [Green Version]

- Parrilla-González, J.; Ortega-Alons, D. Social Innovation in Olive Oil Cooperatives: A Case Study in Southern Spain. Sustainability 2021, 13, 7. [Google Scholar]

- Walzberg, J.; Lonca, G.; Hanes, R.J.; Eberle, A.L.; Carpenter, A.; Heath, G.A. Do we need a new sustainability assessment method for the circular economy? A critical literature review. Front. Sustain. 2021, 1, 12. [Google Scholar] [CrossRef]

- Rincón, F.; López, A. Economía Social: Principios y valores para el desarrollo sostenible. CIRIEC-España Rev. Econ. Pública Soc. Y Coop. 2021, 102, 33–59. [Google Scholar]

- Alcívar, M.; Rodríguez-Borges, C. La gestión ambiental una propuesta de planificación en cooperativas de ahorro y crédito. Polo Del Conoc. Rev. Científico-Prof. 2021, 6, 569–590. [Google Scholar]

- Bustio, A.; Labrador, O.; Mitjans, M. Estrategia ambiental desde la perspectiva de la gestión de empresas cooperativas. Coop. Y Desarro. 2021, 9, 986–1016. [Google Scholar]

- Cavalcante Quezado, T.C.; Cavalcante, W.Q.F.; Fortes, N.; Ramos, R.F. Corporate Social Responsibility and Marketing: A bibliometric and visualization analysis of the literature between the years 1994 and 2020. Sustainability 2022, 14, 1694. [Google Scholar] [CrossRef]

- Dipak, B.; Das, G.; Varshneya, G. Corporate social responsibility: A boon or bane for innovative firms? J. Strateg. Mark. 2019, 27, 50–66. [Google Scholar]

- Pope, S.; Wæraas, A. CSR-washing is rare: A conceptual framework, literature review, and critique. J. Bus. Ethics 2016, 137, 173–193. [Google Scholar] [CrossRef]

- Dikau, S.; Volz, U. Central bank mandates, sustainability objectives and the promotion of green finance. Ecol. Econ. 2021, 184, 107022. [Google Scholar] [CrossRef]

- González, C.; Núñez, S. Markets, Financial Institutions and Central Banks in the Face of Climate Change: Challenges and Opportunities; Banco de España Occasional Paper No. 2126; Banco de España: Madrid, Spain, 2021. [Google Scholar]

- Jones, E. El BCE y el cambio climático. Cuad. Inf. Econòmica 2020, 274, 41–47. [Google Scholar]

- Robert Costanza, R.; Daly, H. Natural capital and sustainable development. Conserv. Biol. 1992, 6, 37–46. [Google Scholar] [CrossRef]

- Tisdell, C. Capital natural resource substitution. Ecol. Econ. 1997, 22, 289–291. [Google Scholar] [CrossRef]

- Gómez-Baggethun, E.; Groot, R. Capital natural y funciones de los ecosistemas: Explorando las bases ecológicas de la economía. Ecosistemas 2007, 16, 4–14. [Google Scholar]

- Rodríguez, D.; Gómez, T. Sostenibilidad: Apuntes sobre sostenibilidad fuerte y débil, capital manufacturado y natural. Inclusión Y Desarro. 2021, 8, 131–143. [Google Scholar] [CrossRef]

- Tschirhart, T. Integrated ecological-economic models. Annu. Rev. Resour. Econ. 2009, 1, 381–407. [Google Scholar] [CrossRef]

- Stern, D. Limits to substitution and irreversibility in production and consumption: A neoclassical interpretation of ecological economics. Ecol. Econ. 1997, 21, 197–215. [Google Scholar] [CrossRef]

- Gowdy, J.; Erickson, J. The approach of ecological economics. Camb. J. Econ. 2005, 29, 207–222. [Google Scholar] [CrossRef] [Green Version]

- Pirgmaier, E. The value of value theory for ecological economics. Ecol. Econ. 2021, 179, 106790. [Google Scholar] [CrossRef] [PubMed]

- Burkett, P. Marxism and Ecological Economics: Toward a Red and Green Political Economy; Brill: Leiden, The Netherlands, 2006. [Google Scholar]

- Leszinski, R.; Marn, M. Setting value, not price. Ind. Laund. 1997, 48, 51–58. [Google Scholar]

- Nieto, J.; Carpintero, Ó.; Lobejón, L.F.; Miguel, L.J. An ecological macroeconomics model: The energy transition in the EU. Energy Policy 2020, 145, 111726. [Google Scholar] [CrossRef]

- Nieto, J.; Carpintero, Ó.; Miguel, L.J.; de Blas, I. Macroeconomic modelling under energy constraints: Global low carbon transition scenarios. Energy Policy 2020, 137, 111090. [Google Scholar] [CrossRef] [Green Version]

- Manera, C.; Pérez-Montiel, J.; Ferran Navinés, F. Non-Chrematistic Indicators and Growth in the Balearic Islands. Symphonya 2021, 1, 85–99. [Google Scholar] [CrossRef]

- Giampietro, M.; Mayumi, K.; Sorman, A. The Metabolic Pattern of Societies: Where Economists Fall Short; Routledge: Abingdon, UK, 2011. [Google Scholar]

- Eurostat. Economy-Wide Material Flow Accounts. Compilation Guide. 2013. Available online: http://ec.europa.eu/eurostat/documents/1798247/6191533/2013-EW-MFA-Guide-10Sep2013.pdf/ (accessed on 21 April 2022).

- Eurostat. Material Flow Accounts Statistics—Material Footprints. 2017. Available online: http://ec.europa.eu/eurostat/statistics-explained/index.php/Material_flow_accounts_statistics_-_material_footprints (accessed on 21 April 2022).

- Fischer-Kowalski, M.; Krausmann, F.; Giljum, S.; Lutter, S.; Mayer, A.; Bringezu, S.; Moriguchi, Y.; Schütz, H.; Schandl, H.; Weisz, H. Methodology and indicators of economy-wide material flow accounting: State of the art and reliability across sources. J. Ind. Ecol. 2011, 15, 855–876. [Google Scholar] [CrossRef]

- De Molina, M.; Toledo, V. The Social Metabolism: A Socio-Ecological Theory of Historical Change; Springer: Berlin/Heidelberg, Germany, 2014; Volume 3. [Google Scholar]

- UN. Transforming Our World: The 2030 Agenda for Sustainable Development; Resolution 70/1 adopted by the General Assembly on 25 September 2015; UN: New York, NY, USA, 2015. [Google Scholar]

- Carpintero, O. El Metabolismo Económico Regional Espanyol, FUHEM Ecosocial, Madrid. 2015. Available online: http://www.fuhem.es/ecosocial/noticias.aspx?v=9753&n=0 (accessed on 21 April 2022).

- Moranta, J.; Torres, C.; Murray, I.; Hidalgo, M.; Hinz, H.; Gouraguine, A. Transcending capitalism growth strategies for biodiversity conservation. Conserv. Biol. 2021, 36, e13821. [Google Scholar] [CrossRef] [PubMed]

- Català, B. Criteris de Sostenibilitat en Fruiters en Producció Ecològica. Bachelor’s Thesis, Universitat Politècnica de Catalunya, Barcelona, Spain, 2017. [Google Scholar]

- Sansó, A. Proposta d’Indicador Compost de Sostenibilitat; Projecte d’investigació; Universitat de les Illes Balears: Palma, Spain, 2021. [Google Scholar]

- OECD. Handbook on Constructing Composite Indicators; OECD: Paris, France, 2018. [Google Scholar]

- Prescott-Allen, R. The Wellbeing of Nations; Island Press: Washington, DC, USA, 2001. [Google Scholar]

- IUCN. The Environment and Gender Index (EGI) 2013 Pilot; International Union for Conservation of Nature (IUCN): Washington, DC, USA, 2013; Available online: http://genderandenvironment.org/wp-content/uploads/2014/12/The-Environment-and-Gender-Index-2013-Pilot.pdf (accessed on 21 April 2022).

- Briceño, Y.; Mariluz, I. Propuesta de Un Modelo de Indicadores de Gestión para Las Asociaciones Cooperativas de Servicios Que Laboran en La Planta de Distribución de PDVSA Yagua. Master’s Thesis, 2011. Available online: http://mriuc.bc.uc.edu.ve/bitstream/handle/123456789/5638/iynojosa.pdf?sequence=1 (accessed on 21 April 2022).

- Pardo, R.; Gonzales, T. Influencia de control eficiente en la gestión de la cooperativa ACAH. RevIA 2021, 9, 3–21. [Google Scholar]

- Rincón, R. Los indicadores de gestión organizacional: Una guía para su definición. Rev. Univ. EAFIT 1998, 34, 43–59. [Google Scholar]

- Rosanas, J. Indicadores de Gestión, Incentivos, Motivación y Ética en El Control de Gestion; Occasional Paper OP No. 06/11; Universidad de Navarra: Pamplona, Spain, 2006. [Google Scholar]

- Correa-García, J.; Gómez, S.; Londoño, F. Indicadores financieros y su eficiencia en la explicación de la generación de valor en el sector cooperative. Rev. Fac. Cienc. Económicas 2018, 26, 129–144. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Manera, C.; Serrano, E. Management, Cooperatives and Sustainability: A New Methodological Proposal for a Holistic Analysis. Sustainability 2022, 14, 7489. https://doi.org/10.3390/su14127489

Manera C, Serrano E. Management, Cooperatives and Sustainability: A New Methodological Proposal for a Holistic Analysis. Sustainability. 2022; 14(12):7489. https://doi.org/10.3390/su14127489

Chicago/Turabian StyleManera, Carles, and Eloi Serrano. 2022. "Management, Cooperatives and Sustainability: A New Methodological Proposal for a Holistic Analysis" Sustainability 14, no. 12: 7489. https://doi.org/10.3390/su14127489

APA StyleManera, C., & Serrano, E. (2022). Management, Cooperatives and Sustainability: A New Methodological Proposal for a Holistic Analysis. Sustainability, 14(12), 7489. https://doi.org/10.3390/su14127489