An Integrated Online/Offline Social Network-Based Model for Crowdfunding Support in Developing Countries: The Case of Nigeria

, ,

, ,  ,

,  and

and

Abstract

:1. Introduction

2. Related Work

2.1. Crowdfunding in the Context of the Developed Nations

2.2. Crowdfunding in the Developing Nations: Problems, Potentials and Prospects

2.3. The Importance of Crowdfunding Adoption to Nigeria and the Wider Developing World

2.4. The Gap in Knowledge—Can Social Media Be Used as a Crowdfunding Platform in Developing Countries?

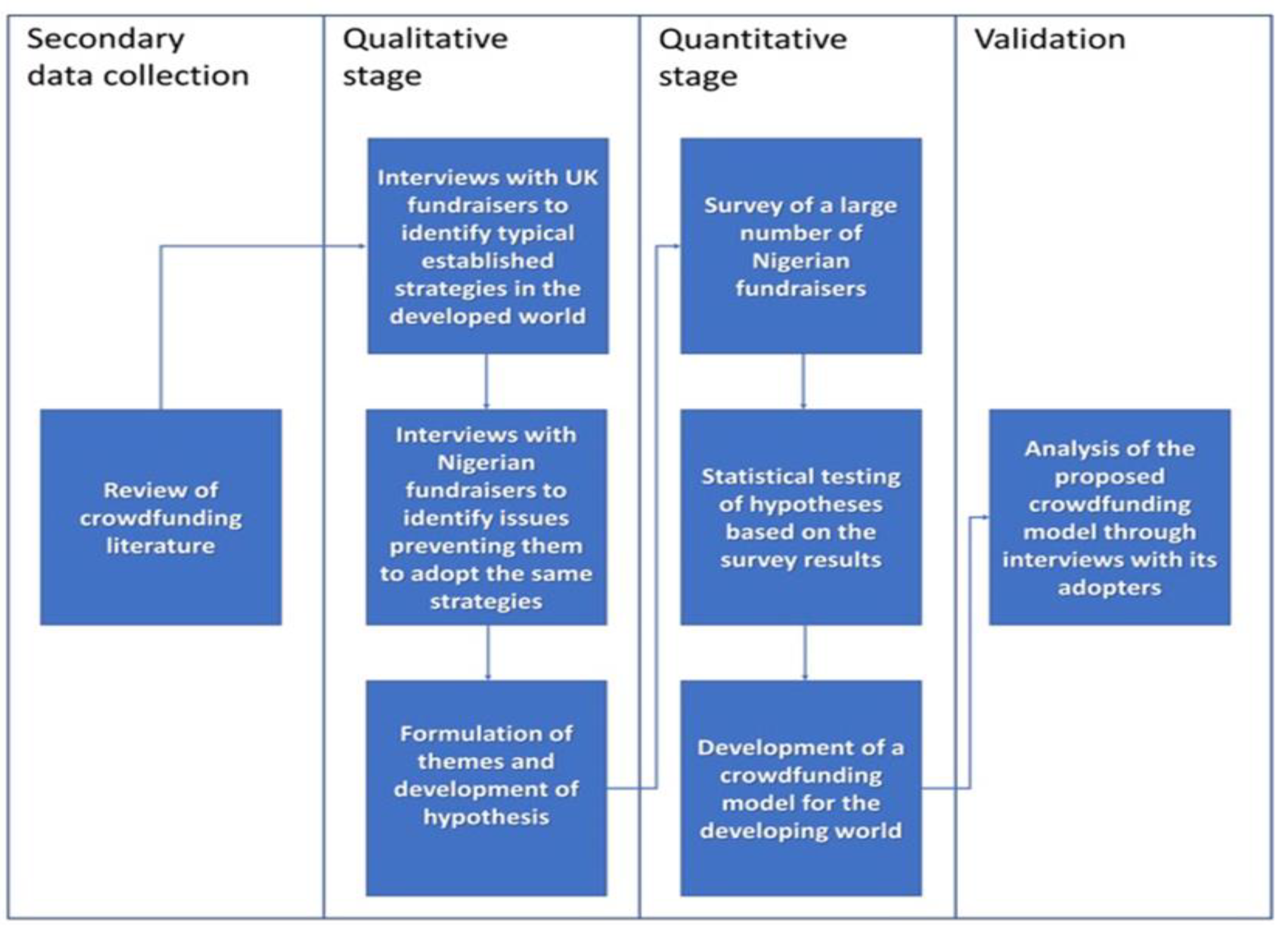

3. Methodology

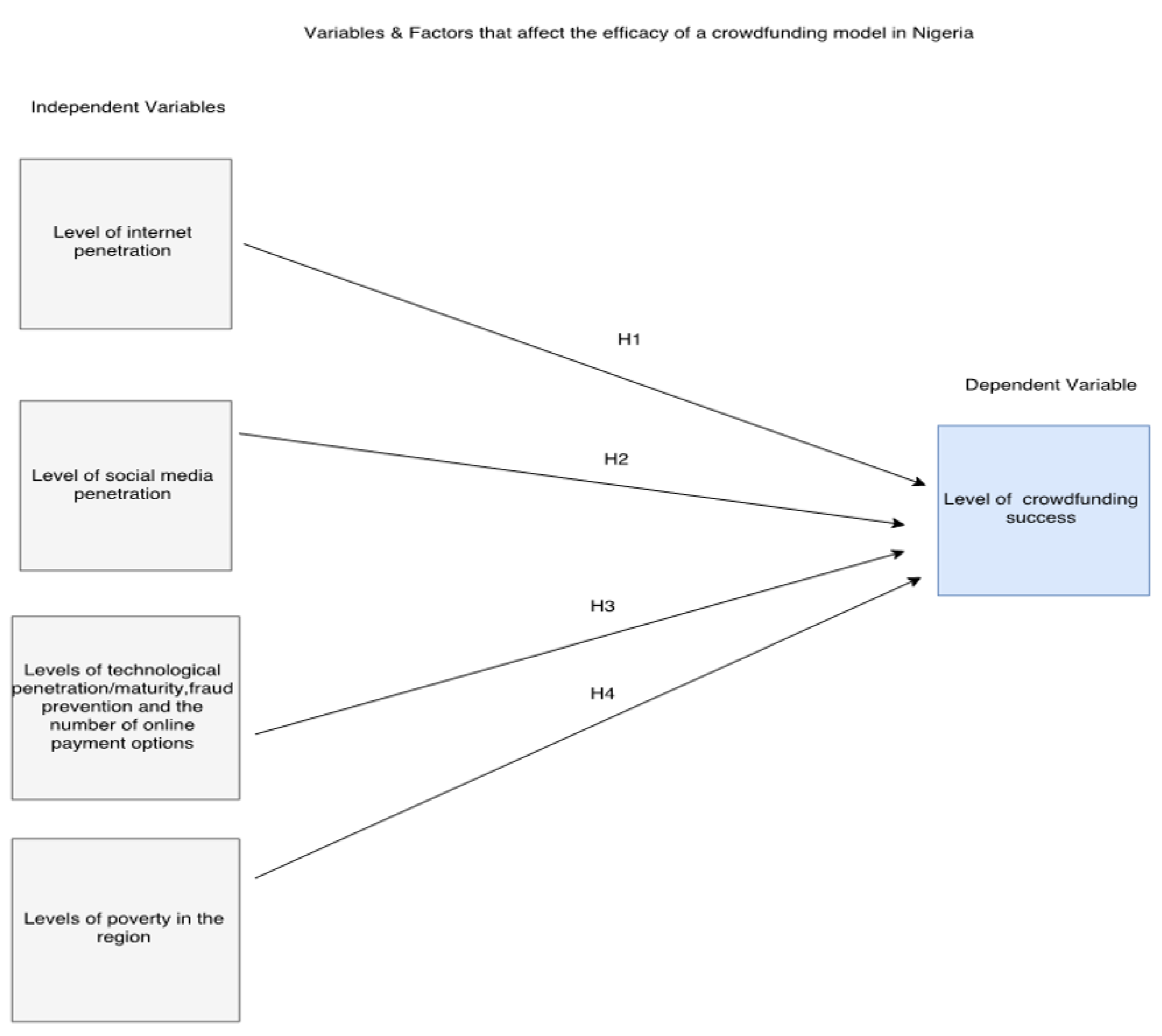

4. Results and Discussion

4.1. Qualitative Analysis

4.2. Quantitative Analysis

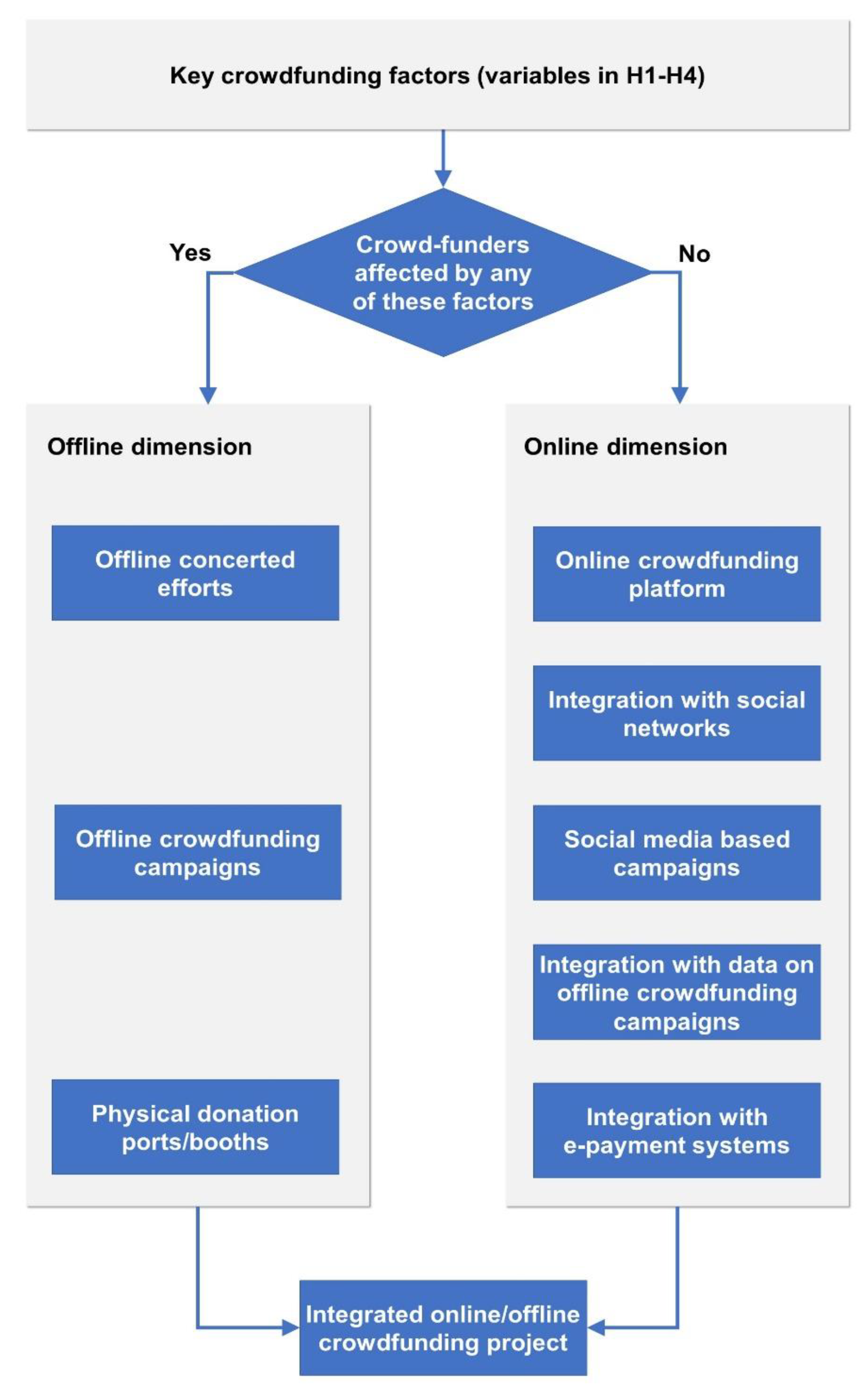

5. Proposed Crowdfunding Model for Developing Countries

Proposed Model

- (1)

- In a situation in which a donor joins the fundraising campaign online, but does not have access to online payment facilities, such donors can be redirected to the closest offline donation port/booth nearest to them or be provided with the details of the specified bank account of the fundraisers or the account provided by the crowdfunding platform hosting the campaign, where cash or wire transfer deposits can be channelled to.

- (2)

- Donors who are fortunate enough to have access to online banking and/or Internet-based payment options can easily complete the donation process by making direct debit payments and/or Internet transfers towards the project right on the crowdfunding platform hosting the campaign. This is the dimension of social media-based crowdfunding practiced in the developed crowdfunding marketplace.

6. Validation Considerations

7. Conclusions

7.1. Key Contributions

7.2. Implications for Theory

7.3. Implications for Practice

7.4. Limitations

7.5. Directions for Future Research

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Yusoff, M.; Zainol, F.; Ismail, M.; Redzuan, R.; Abdul Rahim Merican, R.; Razik, M.; Afthanorhan, A. The Role of Government Financial Support Programmes, Risk-Taking Propensity, and Self-Confidence on Propensity in Business Ventures. Sustainability 2021, 13, 380. [Google Scholar] [CrossRef]

- Yang, Y.; Chen, X.; Gu, J.; Fujita, H. Alleviating Financing Constraints of SMEs through Supply Chain. Sustainability 2019, 11, 673. [Google Scholar] [CrossRef] [Green Version]

- Oshora, B.; Desalegn, G.; Gorgenyi-Hegyes, E.; Fekete-Farkas, M.; Zeman, Z. Determinants of Financial Inclusion in Small and Medium Enterprises: Evidence from Ethiopia. J. Risk Financ. Manag. 2021, 14, 1–19. [Google Scholar] [CrossRef]

- Asare, E.; Nketia, J.; Beldona, S.; Wysong, S. The Role of Culture on SME Access to Credit: Implications for Developing Nations. J. Account. Financ. 2021, 21, 41–62. [Google Scholar]

- Akoh, A. Barriers to the Growth of Micro Tailoring Businesses in Nigeria: Assessing Socio-Economic and Socio-Cultural Environments. Soc. Bus. Rev. 2020, 15, 397–414. [Google Scholar] [CrossRef]

- Taiwo, J.; Falohun, T.; Agwu, M. SMEs Financing and Its Effects on Nigerian Economic Growth. Eur. J. Bus. Econ. Account. 2016, 4, 18. [Google Scholar]

- Central Bank of Nigeria. SME Finance. Available online: https://www.cbn.gov.ng/devfin/smefinance.asp (accessed on 29 December 2021).

- FSS SME Sector Report. 2007. Available online: http://npc.gov.ng (accessed on 29 December 2021).

- Amadi, O. CBN Disburses N3bn Under Nigeria Youth Investment Fund (NYIF) CBN Update. Available online: https://www.cbn.gov.ng/Out/2021/CCD/CBN%20Update%202021%20(August)%20.pdf (accessed on 29 December 2021).

- Motylska-Kuzma, A. Crowdfunding and Sustainable Development. Sustainability 2018, 10, 4650. [Google Scholar] [CrossRef] [Green Version]

- Schwienbacher, A.; Larralde, B. Crowdfunding of Small Entrepreneurial Ventures. In The Oxford Handbook of Entreprenuerial Finance; Oxford University Press: Oxford, UK, 2012. [Google Scholar]

- Daowd, A.; Kamal, M.M.; Eldabi, T.; Hasan, R.; Missi, F.; Dey, B. The Impact of Social Media on the Performance of Microfinance Institutions in Developing Countries: A Quantitative Approach. Inf. Technol. People 2020, 34, 25–49. [Google Scholar] [CrossRef]

- Diniz, E.; Jayo, M.; Pozzebon, M.; Lavoie, F.; Foguel, F. ICT Helping to Scale up Microfinance: The Case of a Successful Bank-MFI Partnership in Brazil. J. Glob. Inf. Manag. 2014, 22, 34–50. [Google Scholar] [CrossRef]

- Xu, Y.; Luo, C.; Chen, D.; Zheng, H. What Influences the Market Outcome of Online P2P Lending Marketplace?: A Cross-Country Analysis. J. Glob. Inf. Manag. 2015, 23, 23–40. [Google Scholar] [CrossRef]

- Sathye, M.; Prasad, B.; Sharma, D.; Sharma, P.; Sathye, S. Mobile Value-Added Services in Fiji: Institutional Drivers, Industry Challenges, and Adoption by Women Micro Entrepreneurs. J. Glob. Inf. Manag. 2017, 25, 1–14. [Google Scholar] [CrossRef] [Green Version]

- Poor Nigerians to Hit 95.1m in 2022, Says World Bank. Available online: https://punchng.com/poor-nigerians-to-hit-95-1m-in-2022-says-wbank/ (accessed on 23 May 2022).

- Digital 2020: Nigeria. Available online: https://datareportal.com/reports/digital-2022-nigeria (accessed on 20 May 2022).

- Okeleke, K.; Suardi, S. The Mobile Economy Sub-Saharan Africa 2021; GSMA Intelligence: London, UK, 2021. [Google Scholar]

- Martínez-Climent, C.; Costa-Climent, R.; Oghazi, P. Sustainable Financing through Crowdfunding. Sustainability 2019, 11, 934. [Google Scholar] [CrossRef] [Green Version]

- Konhäusner, P.; Thielmann, M.; Câmpian, V.; Dabija, D.-C. Crowdfunding for Independent Print Media: E-Commerce, Marketing, and Business Development. Sustainability 2021, 13, 11100. [Google Scholar] [CrossRef]

- Yasar, B. The New Investment Landscape: Equity Crowdfunding. Cent. Bank Rev. 2021, 21, 1–16. [Google Scholar] [CrossRef]

- Scott-Briggs, B. Crowdfunding Grows Up as VC Activity Declines. Available online: https://www.techbullion.com/crowdfunding-grows-vc-activity-declines/ (accessed on 29 December 2021).

- Ziegler, T.; Shneor, R.; Zhang, B.Z. The Global Status of the Crowdfunding Industry. In Advances in Crowdfunding: Research and Practice; Shneor, R., Zhao, L., Flaten, B.-T., Eds.; Springer International Publishing: Cham, Switzerland, 2020; pp. 43–61. ISBN 978-3-030-46309-0. [Google Scholar]

- Gallastegui, L.; Forradellas, R.; Alonso, S.; Jorge-Vázquez, J. Advanced E-Commerce Support Framework to Be Applied in Digital Electronic Commerce and Digital Services with an Impact on the European Commission’s Digital Economy and Society Index. In Digitization of Organizations: Competitive Advantage or Forced Adaptation; Universidad de La Rioja y Academia Europea de Dirección y Economía de la Empresa (AEDEM): Rioja, Spain, 2021; pp. 472–495. [Google Scholar]

- Cosh, A.; Cumming, D.; Hughes, A. Outside Entrepreneurial Capital. Econ. J. 2009, 119, 1494–1533. [Google Scholar] [CrossRef]

- Kuppuswamy, V.; Bayus, B.L. Crowdfunding Creative Ideas: The Dynamics of Project Backers. In The Economics of Crowdfunding; Cumming, D., Hornuf, L., Eds.; Palgrave Macmillan: London, UK, 2018; Volume 24, pp. 151–182. [Google Scholar]

- Kahtan, M. Crowdfunding: The Disruptor’s, Disruptor. Ivey Bus. J. 2013. Available online: https://iveybusinessjournal.com/publication/crowdfunding-the-disruptors-disruptor/ (accessed on 23 May 2022).

- Ariyo, D. Small Firms Are the Backbone of the Nigerian Economy. Afr. Econ. Anal. 1999. Available online: http://www.afbis.com/analysis/small.htm (accessed on 19 January 2022).

- Egene, G. SEC Rules out Crowdfunding for Now. Available online: http://www.thisdaylive.com/index.php/2016/08/15/sec-rules-out-crowdfunding-in-nigeria-for-now/ (accessed on 29 December 2021).

- Bernardino, S.; Santos, J. Crowdfunding: An Exploratory Study on Knowledge, Benefits and Barriers Perceived by Young Potential Entrepreneurs. J. Risk Financ. Manag. 2020, 13, 81. [Google Scholar] [CrossRef]

- Ogwu, K.; Pimenidis, E.; Kozlovski, E. Funding Bright Ideas in The Dark Continent. Int. J. Strateg. Manag. Decis. Support Syst. Strateg. Manag. 2018, 23, 33–41. [Google Scholar] [CrossRef] [Green Version]

- Zhang, Z.Y. Financing Problems and Solutions of SMEs. Manag. Sci. Eng. 2014, 8, 50–56. [Google Scholar]

- Agrawal, A.K.; Catalini, C.; Goldfarb, A. The Geography of Crowdfunding. Available online: https://www.nber.org/papers/w16820 (accessed on 12 December 2021).

- Kim, K.; Viswanathan, S. The Experts in the Crowd: The Role of Reputable Investors in a Crowdfunding Market. MIS Q. 2019, 43, 347–372. [Google Scholar]

- Kim, K.; Hann, I. Crowdfunding and the Democratization of Access to Capital—An Illusion? Evidence from Housing Prices. Inf. Syst. Res. 2019, 30, 276–290. [Google Scholar] [CrossRef]

- Mollick, E. The Dynamics of Crowdfunding: An Exploratory Study. J. Bus. Ventur. 2014, 29, 1–16. [Google Scholar] [CrossRef] [Green Version]

- Zheng, H.; Dahui, L.; Jing, W.; Yun, X. The Role of Multidimensional Social Capital in Crowdfunding: A Comparative Study in China and US. J. Inf. Manag. 2014, 51, 488–496. [Google Scholar] [CrossRef]

- RSI Roberts Space Industries. Available online: https://robertsspaceindustries.com/funding-goals (accessed on 29 December 2021).

- Rooney, K. A Blockchain Start-up Just Raised $4 Billion without a Live Product. Available online: https://www.cnbc.com/2018/05/31/a-blockchain-start-up-just-raised-4-billion-without-a-live-product.html (accessed on 29 December 2021).

- Sachgau, O. German Solar Car Startup Sono to Stay in Business After Crowdfunding Success. Available online: https://europe.autonews.com/automakers/german-solar-car-startup-sono-will-stay-business-after-crowdfunding-success (accessed on 29 December 2021).

- IGG Flow Hive: Honey on Tap Directly From Your Beehive? Available online: https://www.indiegogo.com/projects/flow-hive-honey-on-tap-directly-from-your-beehive#/ (accessed on 29 December 2021).

- Kickstarter Snapmaker: The All-Metal 3D Printer. Available online: https://www.kickstarter.com/projects/snapmaker/snapmaker-the-all-metal-3d-printer (accessed on 29 December 2021).

- Light, A.; Briggs, J. Crowdfunding Platforms and the Design of Paying Publics. In Proceedings of the 2017 CHI Conference on Human Factors in Computing Systems, Denve, CO, USA, 6–11 May 2017; pp. 797–809. [Google Scholar]

- Haque, A.; Aston, J.; Kozlovski, E. The Impact of Stressors on Organizational Commitment of Managerial and Non-Managerial Personnel in Contrasting Economies: Evidences from Canada and Pakistan. Int. J. Bus. 2018, 23, 166–182. [Google Scholar]

- Deng, L.; Ye, Q.; Xu, D.; Sun, W.; Jiang, G. A Literature Review and Integrated Framework for the Determinants of Crowdfunding Success. Financ. Innov. 2022, 8, 41. [Google Scholar] [CrossRef]

- Haque, A.U.; Basuki, B.; Aston, J.; Widyanti, R. Do Different Stressors Affect Working Efficiency of Public University Personnel Differently? Pol. J. Manag. Stud. 2021, 23, 172–187. [Google Scholar] [CrossRef]

- Saunders, M.; Lewis, P.; Thornhill, A. Research Methods for Business Students, 8th ed.; Pearson Education Limited: London, UK, 2019. [Google Scholar]

- Thompson, S. Sampling, 3rd ed.; Wiley: Hoboken, NJ, USA, 2012. [Google Scholar]

- Roscoe, J.T. Fundamental Research Statistics for the Behavioural Sciences, 2nd ed; Holt Rinehart and Winston: New York, NY, USA, 1975. [Google Scholar]

- Moore, D. Basic Practice of Statistics, 6th ed.; W. H. Freeman & Company: New-York, NY, USA, 2013. [Google Scholar]

- Rana, R.; Singhal, R. Chi-Square Test and Its Application in Hypothesis Testing. J. Pract. Cardiovasc. Sci. 2015, 1, 69–71. [Google Scholar]

- Haque, A.U.; Aston, J.; Kozlovski, E.; Caha, Z. Role of External CSR and Social Support Programme for Sustaining Human Capital in Contrasting Economies. Pol. J. Manag. Stud. 2020, 22, 147–168. [Google Scholar] [CrossRef]

- Haque, A.U. Handbook of Research on the Complexities and Strategies of Occupational Stress; IGI Global: Hershey, PA, USA, 2022. [Google Scholar] [CrossRef]

- Haque, A.U.; Yamoah, F.A. The Role of Ethical Leadership in Managing Occupational Stress to Promote Innovative Work Behaviour: A Cross-Cultural Management Perspective. Sustainability 2021, 13, 9608. [Google Scholar] [CrossRef]

- Agresti, A. An Introduction to Categorical Data Analysis, 3rd ed.; Wiley: Hoboken, NJ, USA, 2018. [Google Scholar]

- Bhattacharya, P.; Burman, P. Theory and Methods of Statistics, 1st ed.; Academic Press: Cambridge, MA, USA, 2016; ISBN 0-12-804123-4. [Google Scholar]

- Nigeria: Facebook Users 2022, by Age Group. Available online: https://www.statista.com/statistics/1028428/facebook-user-share-in-nigeria-by-age/ (accessed on 27 May 2022).

- Saxton, G.; Wang, L. The Social Network Effect: The Determinants of Giving Through Social Media. Nonprofit Volunt. Sect. Q. 2014, 43, 850–868. [Google Scholar] [CrossRef]

- Davidson, R.; Poor, N. The Barriers Facing Artists’ Use of Crowdfunding Platforms: Personality, Emotional Labor, and Going to the Well One Too Many Times. New Media Soc. 2015, 17, 289–307. [Google Scholar] [CrossRef]

- Kraemer, D. What Do the Poorest Countries Want from Climate Summit? Available online: https://www.bbc.com/news/science-environment-59054696 (accessed on 29 December 2021).

- von Selasinsky, C.; Lutz, C. The Effects of Pro-Social and Pro-Environmental Orientation on Crowdfunding Performance. Sustainability 2021, 13, 6064. [Google Scholar] [CrossRef]

- Kim, M.J.; Hall, C.M.; Han, H. Behavioral Influences on Crowdfunding SDG Initiatives: The Importance of Personality and Sub-Jective Well-Being. Sustainability 2021, 13, 3796. [Google Scholar] [CrossRef]

- Moysidou, K.; Hausberg, J. In Crowdfunding We Trust: A Trust-Building Model in Lending Crowdfunding. J. Small Bus. Manag. 2019, 58, 511–543. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Project/Funding | Platform | Reference |

|---|---|---|

| Star Citizen (video game) Campaign Goal: USD 2 M Raised: USD 423,000,000+ | Kickstarter | [38] |

| EOS (blockchain operating system) Campaign Goal: open Raised: USD 4,100,000,000 | Ethereum | [39] |

| Solar Electric Vehicle (electric car) Campaign Goal: EUR 50 M Raised: EUR 53,342,998 | Independent project | [40] |

| Flow Hive (beehive) Campaign Goal: USD 70 K Raised: USD 13,289,097 | Indiegogo | [41] |

| Snapmaker (3D Printer) Campaign Goal: USD 50 K Raised: USD 2,277,182 | Kickstarter | [42] |

| No. | Identified Theme Relevant to the Facilitation of Crowdfunding | Perceptions of the UK Participants | Perceptions of the Nigerian Participants |

|---|---|---|---|

| 1 | Internet penetration | The level of Internet penetration is high. Internet access is available at low costs. | The level of Internet penetration is low. High costs of data plan packages and Internet access. |

| 2 | Social media penetration | High penetration of social media. | Low penetration of social media. |

| 3 | Technological level of maturity, fraud prevention and options of online payment | Technological maturity and ample options of online payment. The extent of concerns related to fraud and its risks is low. | Poor choice of online payment options resulting from immaturity of technological infrastructures. The levels of risks and fraud concerns are very high. |

| 4 | Level of poverty in the region | Economic prosperity | Poverty found in broad population strata |

| Variable | Response Categories | Chi Square Critical | Df | p * | ||||

|---|---|---|---|---|---|---|---|---|

| High | Medium | Low | Total | Chi Square | ||||

| Level of Internet penetration and its impact on crowdfunding in the region. | 140 | 40 | 20 | 200 | 339.200 | 43.773 | 30 | 0.00 |

| Variable | Response Categories | Chi Square Critical | Df | p * | ||||

|---|---|---|---|---|---|---|---|---|

| High | Medium | Low | Total | Chi Square | ||||

| Level of social media penetration and its impact on crowdfunding in the region. | 12 | 20 | 168 | 200 | 337.705 | 43.773 | 30 | 0.001 |

| Cross Tabulation | |||||||

|---|---|---|---|---|---|---|---|

| Count | |||||||

| Availability of Payment Options | Total | Chi Square Computed | p * | Remarks | |||

| Available | Not Available | ||||||

| levels of technological penetration, fraud prevention and the number of online payment options | High | 70 | 26 | 96 | 22.105 | 0.001 | Relationship exist |

| Low | 22 | 82 | 104 | ||||

| Total | 73 | 127 | 200 | ||||

| Variable | N | Mean | Std.Dev | Df | Correlation Index * | p | Remarks |

|---|---|---|---|---|---|---|---|

| Poverty | 200 | 12.5414 | 0.6874 | 198 | −0.892 | 0.005 | |

| Significant influence exist | |||||||

| Fund raising efforts | 200 | 13.246 | 1.0032 |

| Element of the Proposed Crowdfunding Model | Evidence from the Validators | |

|---|---|---|

| Off-line dimension | Off-line concerted efforts | “By including the offline dimension of the model in my CF campaign, I was able to raise 60% of my funding goal from my local community” |

| Off-line crowdfunding campaigns | “The offline campaign consolidated the online campaign brilliantly. The fundraising was inclusive and dynamic” | |

| Physical donation ports/booth | “The offline crowd who have no access to the Internet proved to be very useful as they donated via the donation ports/booths. Without the use of donation ports/booth, we would have lost 40% of donations received via this channel” | |

| Online dimension | Online crowdfunding platform | “The online crowdfunding platform still played a key role as a good percentage of donors donated directly through the crowdfunding platform that hosted our crowdfunding campaign.” |

| Social media integration with physical donations | “Integrating our social media network with our offline strategy ensured that some donors who discovered the project online and could not donate due to a lack of online payment options were directed towards the nearest payment booth where donations were made physically and vis-à-vis” | |

| Online payment options | “Both users who discovered the campaign offline and online and had the means of donating via Internet-based payment options, found the online payment options convenient. However, the most effective strategy was a combination of the online and payment crowdfunding models” |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ogwu, K.; Hickey, P.; Okeke, O.J.-P.; Haque, A.u.; Pimenidis, E.; Kozlovski, E. An Integrated Online/Offline Social Network-Based Model for Crowdfunding Support in Developing Countries: The Case of Nigeria. Sustainability 2022, 14, 9333. https://doi.org/10.3390/su14159333

Ogwu K, Hickey P, Okeke OJ-P, Haque Au, Pimenidis E, Kozlovski E. An Integrated Online/Offline Social Network-Based Model for Crowdfunding Support in Developing Countries: The Case of Nigeria. Sustainability. 2022; 14(15):9333. https://doi.org/10.3390/su14159333

Chicago/Turabian StyleOgwu, Kanayo, Patrick Hickey, Okeoma John-Paul Okeke, Adnan ul Haque, Elias Pimenidis, and Eugene Kozlovski. 2022. "An Integrated Online/Offline Social Network-Based Model for Crowdfunding Support in Developing Countries: The Case of Nigeria" Sustainability 14, no. 15: 9333. https://doi.org/10.3390/su14159333

APA StyleOgwu, K., Hickey, P., Okeke, O. J. -P., Haque, A. u., Pimenidis, E., & Kozlovski, E. (2022). An Integrated Online/Offline Social Network-Based Model for Crowdfunding Support in Developing Countries: The Case of Nigeria. Sustainability, 14(15), 9333. https://doi.org/10.3390/su14159333