1. Introduction

Innovation is an important force in promoting the development of a country as well as in the development of all human society. Corporate innovation is an important area of social innovation and also forms the foundation for enterprises to obtain their core competitiveness and sustainable growth [

1,

2]. Innovation requires a large amount of R&D investment [

3], and decisions in R&D investment are mainly controlled by management. Thus, management plays an important role in corporate innovation. An increasing amount of research focuses on the influence of management on corporate innovation. For example, empirical studies have found that the professional background and political connections of the CEO [

4], self-confidence [

5,

6], gender [

7], founder’s identity [

8], military experience [

9], academic work experience [

10], pilot qualifications [

11], and organizational identification [

12] have a significant impact on corporate innovation. However, these studies have focused on CEOs, rarely on CFOs.

CFOs play an important role in business management, a role that differs from that of CEOs. Since the 1960s, CFOs have emerged and have come to fulfill an indispensable role in enterprises [

13]. CFOs not only need to participate in the formulation of enterprise development strategies and important business decisions, but are also responsible for corporate finance, accounting, and internal control [

14]. Empirical research has shown that CFOs can significantly influence a firm’s accounting policies and tools [

15,

16,

17], quality of internal control [

18,

19], accounting information quality [

20,

21], financing costs [

22,

23], tax policy [

24], social responsibility [

25], and other areas. Additionally, there is a clear division of labor between CFOs and CEOs, and there are clear differences in their roles in enterprises. It is generally believed that the CEO is the most important daily business decision-maker in a company, while the CFO oversees the company’s financial decisions.

Given the differences in the roles of CEOs and CFOs, we believe it is essential to distinguish between the CEO and the CFO. The differences in the roles of the CEO and the CFO result in the possibility that the same variables of the CEO and the CFO may have different outcomes for the enterprise. These different outcomes can be specified in three ways: (1) the intensities of the impact of the CEO and the CFO are different. For example, Geiger and North (2006) [

26] find that discretionary accruals decrease significantly following the appointment of a new CFO, but these changes are not caused by the appointment of a new CEO. Because one of the main responsibilities of a CFO is financial reporting, a CFO’s equity incentive plays a greater role than does a CEO’s equity incentive in earnings management [

27] and the risk of stock price crash [

23]. (2) The aspects of the impact of the CEO and the CFO are different. Chava and Purnanandam (2010) [

28] show that the CEO (CFO) equity incentive affects the company’s capital structure and cash-holding decisions (debt-maturity structure and accrual management). Baker et al. (2019) [

29] find that accrual earnings management (real earnings management) is greater when the CEO (CFO) is powerful relative to the CFO (CEO). (3) The directions of the impact of the CEO and the CFO are opposite. Xu et al. (2022) [

30] find that CEO organizational identification can positively affect corporate philanthropy, whereas the opposite holds for CFO organizational identification. Therefore, the advantages of the process of distinguishing between the CEO and the CFO are obvious, i.e., it leads to more precise conclusions, drives research forward, and is more informative for practice. However, it also has disadvantages in that it requires a finer granularity of data and the research costs are higher. In summary, if conditions permit, the process of distinguishing between the CEO and the CFO is essential.

In this study, we attempt to explore the question: what role do CFOs play in corporate innovation? In general, a CFO’s functions include strategic support and supervisory control [

26], and these two functions are named as the supporter role and the supervisor role, respectively. These two roles can in most cases be compatible, but in terms of innovative activities, they conflict. Innovation is characterized by high investment, high return, and high risk [

31]. Therefore, on one hand, when performing the supporter role, CFOs are undoubtedly responsible for the large amount of R&D investment required for innovation. On the other hand, CFOs uphold the principle of conservatism when performing the supervisor role and may be resistant to riskier R&D investments.

The conflict between the two roles of CFOs in innovation activities can be understood as an internal conflict in the CFO’s role—that is, the intrarole conflict of CFOs. The concept of intrarole conflict comes from role theory, the theory that explains how individuals cope with role conflict. Role theory holds that a role is a set of special behavioral expectations for individuals with specific social identities, and role expectations are beliefs and attitudes about what role actors should and should not do [

32]. An intrarole conflict, a type of role conflict, refers to the conflict caused by different and incompatible expectations from different groups of the same role [

33]. A role conflict can be coped with by establishing the priority level of different roles and playing the top priority role first [

34].

To explore the way that CFOs cope with intrarole conflicts in corporate innovation, we must first see CFOs “enter their role,” that is, ensure that CFOs have a high enough role performance. However, like other executives, CFOs also face agency problems [

35]; this means that they may not be able to devote themselves to the role of the CFO. In alleviating the CFO agency problem, previous studies have largely focused on conventional corporate governance mechanisms—such as compensation incentives [

14,

21], equity incentives [

28,

36], replacing incompetent CFOs [

16,

37], putting CFOs on the board of directors [

18], and strengthening the supervision of CFOs by the board of directors [

38]. However, these methods are “external forces” and only regulate CFOs’ behaviors, and so it is difficult to observe their inner state. Further, it is, of course, difficult to directly gage CFO role performance.

In recent years, scholars have begun to pay attention to internal psychological factors—such as organizational identification—in their research on how to alleviate the corporate agency problem. Organizational identification is a special form of social identification, which is a state in which individuals define themselves according to a specific organizational membership or a perception of belonging to a specific organization [

34,

39]. In short, members with stronger organizational identification are more willing to align their interests with the organization, and so there are fewer agency conflicts. Previous studies have found that CEO organizational identification can reduce agency costs [

40] and reduce the level of earnings management [

41]. Thus, compared to conventional governance mechanisms, organizational identification is a more appropriate measure of role performance.

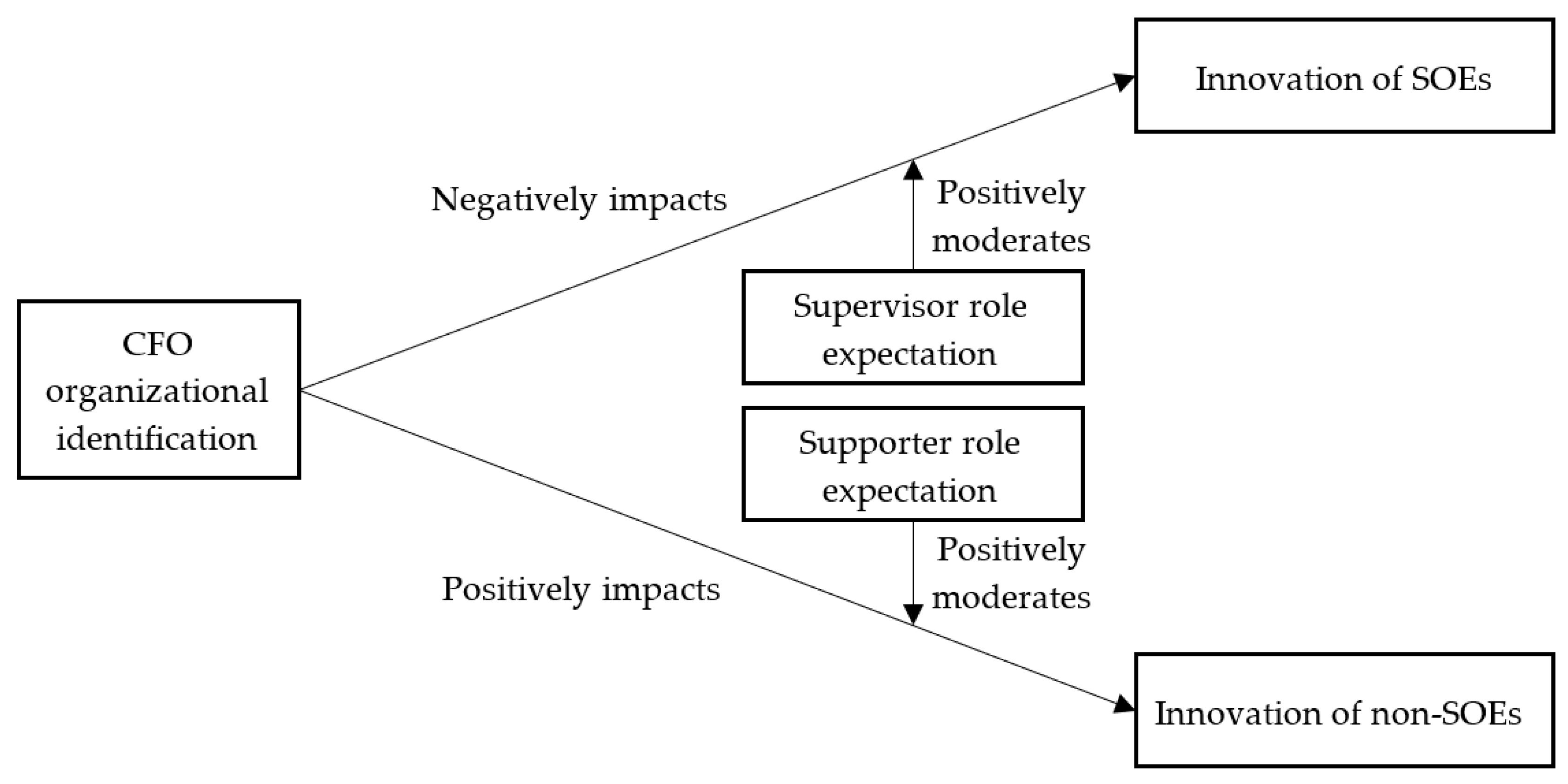

Based on role theory, we measure CFO role performance by organizational identification, and we measure role expectation by corporate owner type, misconduct experience, and CFO financial industry experience, in order to explore the role of CFOs in corporate innovation. The largest challenge of this study lay in the measurement of CFO organizational identification. We obtained data about CFO organizational identification from a survey on listed companies conducted by the China Securities Regulatory Commission (CSRC) in 2014. Other data are from the China Stock Market and Accounting Research (CSMAR) database. Our results suggest that: (1) CFO organizational identification is negatively associated with innovation output in SOEs and positively associated with innovation output in non-SOEs; (2) corporate misconduct experience strengthens the supervisor role expectation of the CFO and positively moderates the relationship between CFO organizational identification and innovation in SOEs; (3) CFO financial industry experience strengthens the supporter role expectation of the CFO and positively moderates the relationship between CFO organizational identification and innovation in non-SOEs. The results show that CFOs play the supervisor role in innovation in SOEs and the supporter role in innovation in non-SOEs.

Our study produces three main theoretical contributions. First, our study explores the role of CFOs in corporate innovation. Most existing studies focus on the role of CEOs in corporate innovation, and the research on the role of CFOs is limited to financial and accounting decision-making. Our study examines the role of CFOs in corporate innovation, enriching the literature on the influencing factors of corporate innovation and conducting research on how the CFO influences enterprise decision-making. Second, our study expands research on organizational identification. Existing research on organizational identification mostly focuses on ordinary employees [

42,

43]. The sparse literature related to top management organizational identification is mostly about CEO organizational identification. Our study explores the consequences of CFO organizational identification, contributing to literature about organizational identification. Third, our study enriches the application scenarios of role theory. Role theory, derived from social psychology, has been used to explore work-family conflict [

44] and leadership style [

45] in management research. We use role theory to explain how CFOs respond to role conflict in corporate innovation, exploring new application scenarios of this theory.

6. Conclusions and Discussion

Based on the perspective of role theory, we measure CFO role performance by organizational identification and we measure role expectation by corporate owner type, misconduct experience, and CFO financial industry experience—to explore the role of CFOs in corporate innovation. We obtained data of CFO organizational identification from a survey of listed companies conducted by the China Securities Regulatory Commission (CSRC) in 2014. Other data are from the China Stock Market and Accounting Research (CSMAR) database.

6.1. Findings

Our results suggest that: (1) CFO organizational identification is negatively associated with innovation output in SOEs and positively associated with innovation output in non-SOEs; (2) corporate misconduct experience strengthens the supervisor role expectation of the CFO and positively moderates the relationship between CFO organizational identification and innovation in SOEs; (3) CFO financial industry experience strengthens the supporter role expectation of the CFO and positively moderates the relationship between CFO organizational identification and innovation in non-SOEs. Our results show that CFOs take on the supervisor role in innovation in SOEs and the supporter role in innovation in non-SOEs.

6.2. Contributions and Implications

Our study addresses the gaps in current literature in a timely manner. First, our study enriches the research on the executive-level influence factors on corporate innovation. Corporate innovation has received much scholarly attention in recent years. The CEO’s pivotal role in corporate decision-making has led to a large number of studies focusing on the impact of CEO characteristics on corporate innovation [

4,

5,

6,

7,

8,

9,

10,

11,

12], but few studies have focused on CFOs. However, the differences between the roles of CEOs and CFOs result in the proposal that the research conclusions related to CEOs cannot be directly applied to CFOs. For example, Du et al. (2022) [

12] find that CEO organizational identification helps promote corporate innovation. In contrast, our study finds that CFO organizational identification promotes innovation in non-SOEs and inhibits innovation in SOEs. Thus, our study enriches, in a timely manner the research on the impact of executives’ personal characteristics, especially organizational identification, on corporate innovation. Second, our study enriches the research on the corporate consequences of CFOs. After the global financial crisis in 2008, firms are paying more and more attention to risk management. Accordingly, the position of CFOs in enterprises is growing day by day, which has received a great deal of research attention. Empirical research has shown that CFOs can significantly influence a firm’s accounting policies and tools [

15,

16,

17], quality of internal control [

18,

19], accounting information quality [

20,

21], financing costs [

22,

23], tax policy [

24], social responsibility [

25], and so on. With the increasing importance of corporate innovation, it is urgent to explore the role of CFOs in corporate innovation. Our study is therefore timely in addressing the gaps in the research on the corporate consequences of CFOs.

Our study also has the following practical implications. First, our findings indicate that CFOs should focus their efforts according to their role expectations in different types of enterprises. CFOs with strong organizational identification are more committed to innovation in non-SOEs (where CFOs play the supporter role), while the opposite holds true for CFOs in SOEs (where CFOs play the supervisor role). CFOs with strong organizational identification in non-SOEs, especially with financial industry experience, can participate in more corporate innovation-related projects to better support corporate innovation. However, CFOs with strong organizational identification in SOEs can be less involved in corporate innovation-related projects and more invested in compliance-related work, especially in companies with misconduct experiences.

Secondly, our findings are useful for CEOs to nominate a CFO and assign the CFO’s work. A CEO needs to be paired with the right CFO and assign the right projects to the CFO in order to better leverage synergies. Innovation activities are high-risk, and an aspiring CEO should ideally be paired with a like-minded CFO to best promote corporate innovation. However, prior research has been controversial about the risk preferences of CFOs [

23,

30]. Our study somewhat reconciles this controversy by finding that CFOs support innovation in non-SOEs and inhibit innovation in SOEs. Thus, CEOs committed to innovation in non-SOEs can nominate a CFO with strong organizational identification, especially with financial industry experience, to assist them in driving corporate innovation. CFOs with strong organizational identification in SOEs are not good partners for CEOs committed to innovation. The CEOs in SOEs can place the CFO with strong organizational identification in more compliance-related tasks and fewer innovation-related tasks to reduce the CFO’s inhibitions in regards to innovation.

Finally, our findings are also informative for the Chinese government in promoting SOE reform. The current focus of SOE reform remains on ownership structure reform [

78]. Our study argues that CFOs in SOEs inhibit innovation for multiple reasons, including SOE goal diversification and a high degree of executive job stability. Therefore, for SOEs with innovation potential, government authorities can reduce the policy burden on these SOEs, or can implement pilot market-based hiring of executives in these SOEs, thus stimulating innovation in these SOEs.

6.3. Limitations and Prospects

This study has limitations that provide promising directions for future research. First, to examine what role the conscientious CFO performs in corporate innovation, we use organizational identification to measure CFO role performance. Such a measure, while richly supported by theory, is not meant to be a perfect measure. For example, CFOs with strong organizational identification but weak capability do not necessarily perform well, and conversely, CFOs with weak organizational identification but strong capability do not necessarily perform poorly. Although we have added CFO personal characteristics as controls in our robustness tests, the effects of measurement bias and omitted variables cannot be completely ruled out. Therefore, future research should look for variables that directly measure CFO role performance. Second, we use a sample of Chinese listed companies to test our hypotheses. China is the world’s most populous country and the world’s second largest economy, so our findings have a wide range of applications. However, China is still an emerging market country with unique institutions and culture, so our findings are not necessarily applicable to other countries. Future research could be conducted across cultures to test the applicability of our findings.

{kind=link}