Digital Transformation of the Greek Banking Sector in the COVID Era

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

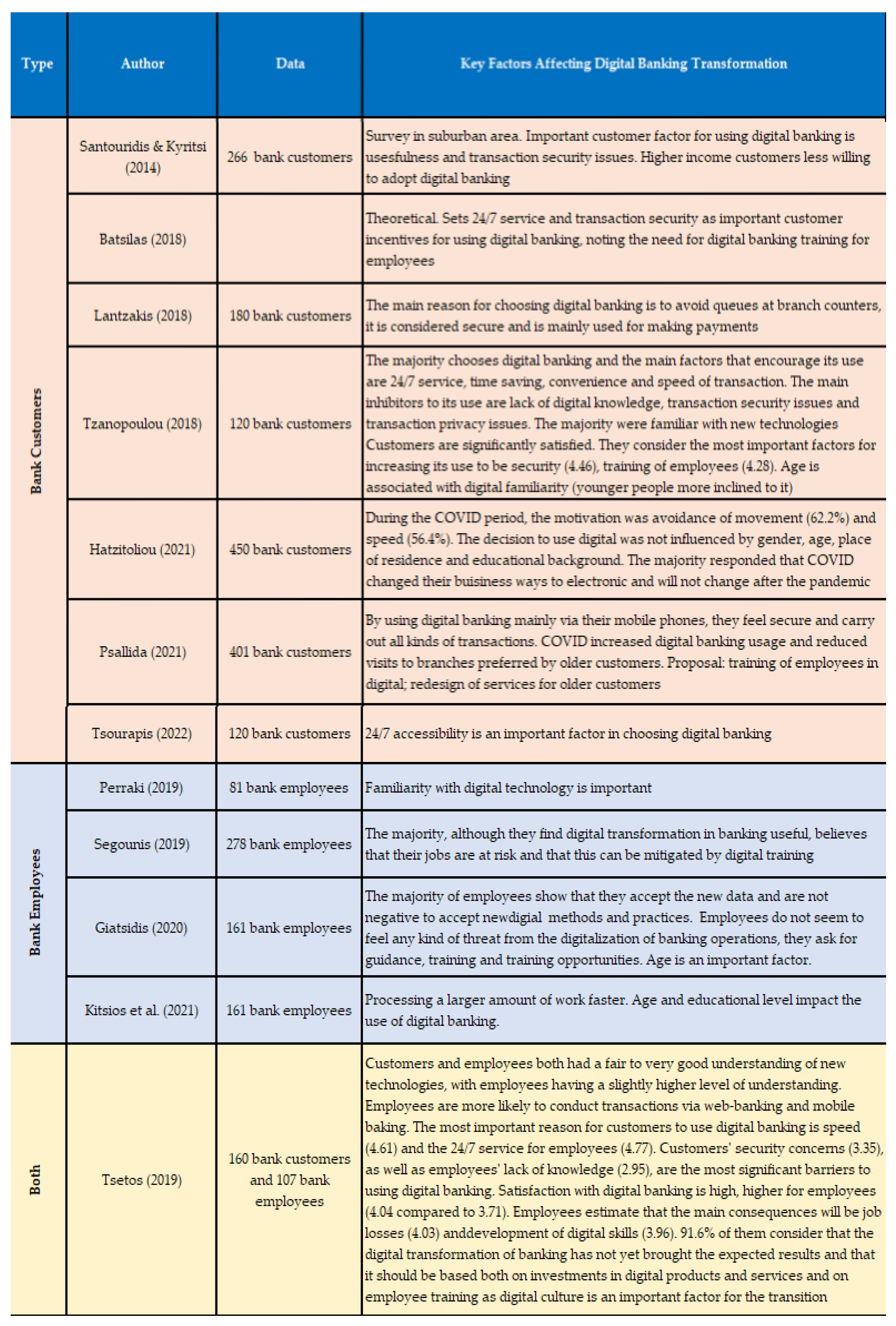

2. Literature Review

- Transforming the customer experience. Digital tools, such as social media, which utilize the digital skills and knowledge of the company aid it in promptly comprehending customer preferences whilst allowing it to export data for future use.

- Transformation of business processes. The use of automated processes allows business executives to focus on strategic processes, increasing their efficiency in this way and contributing to further business development. Meanwhile, the implementation of digital collaboration and visualization tools allows for working away from the office (teleworking) whilst facilitating collaboration and mutual communication. The COVID-19 pandemic has urged digital transformation to proceed at a much quicker pace in both private and public sectors, to expand telework working hours, and to look for new ways of organizing production both locally and internationally.

- Transformation of business models. Digital transformation is revealed through modifications in the experiences and mentality of the consumer, leading to the digitization of the availability of products and services, as well as the formation of new economic models related to the advanced operations of a company.

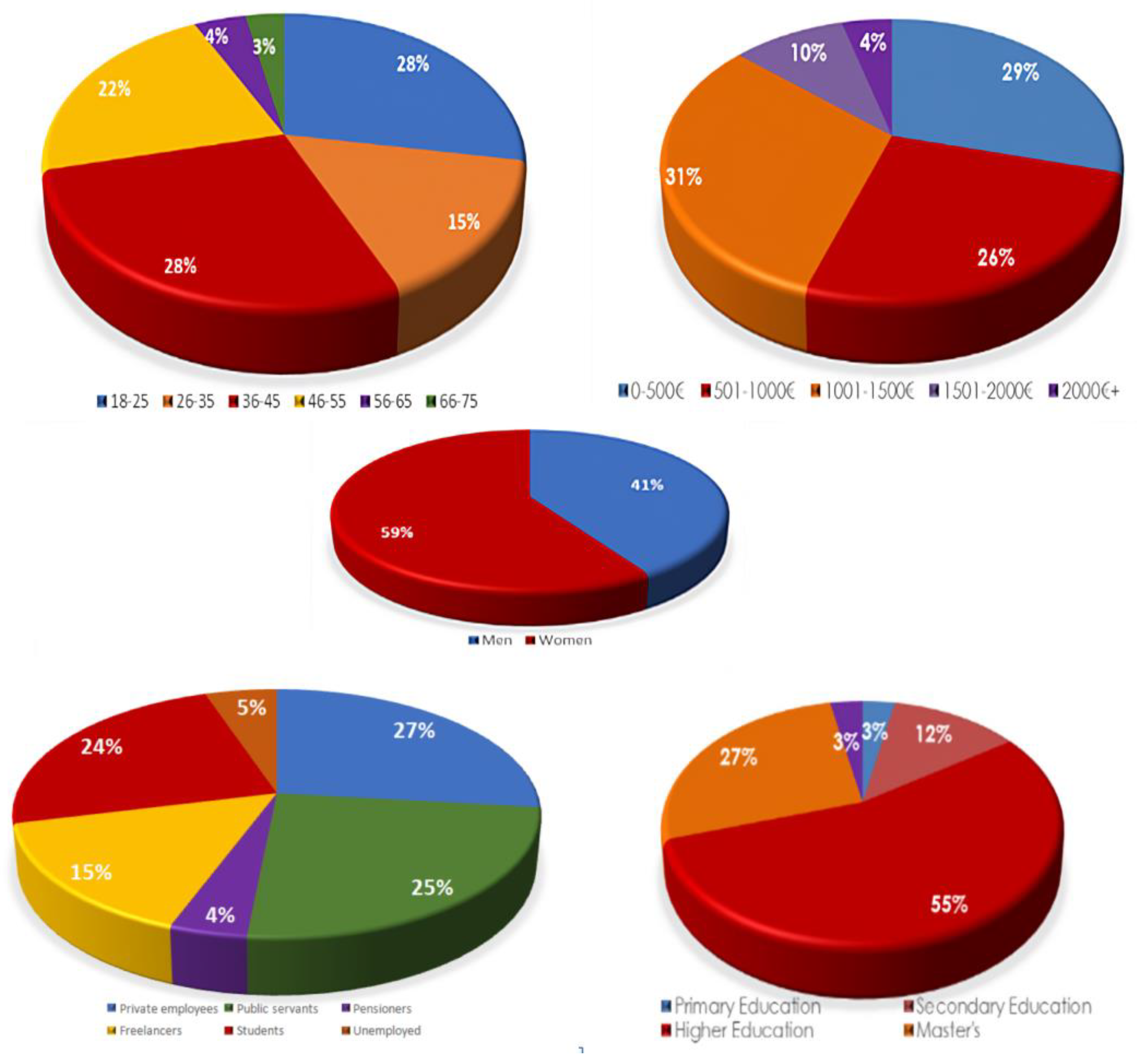

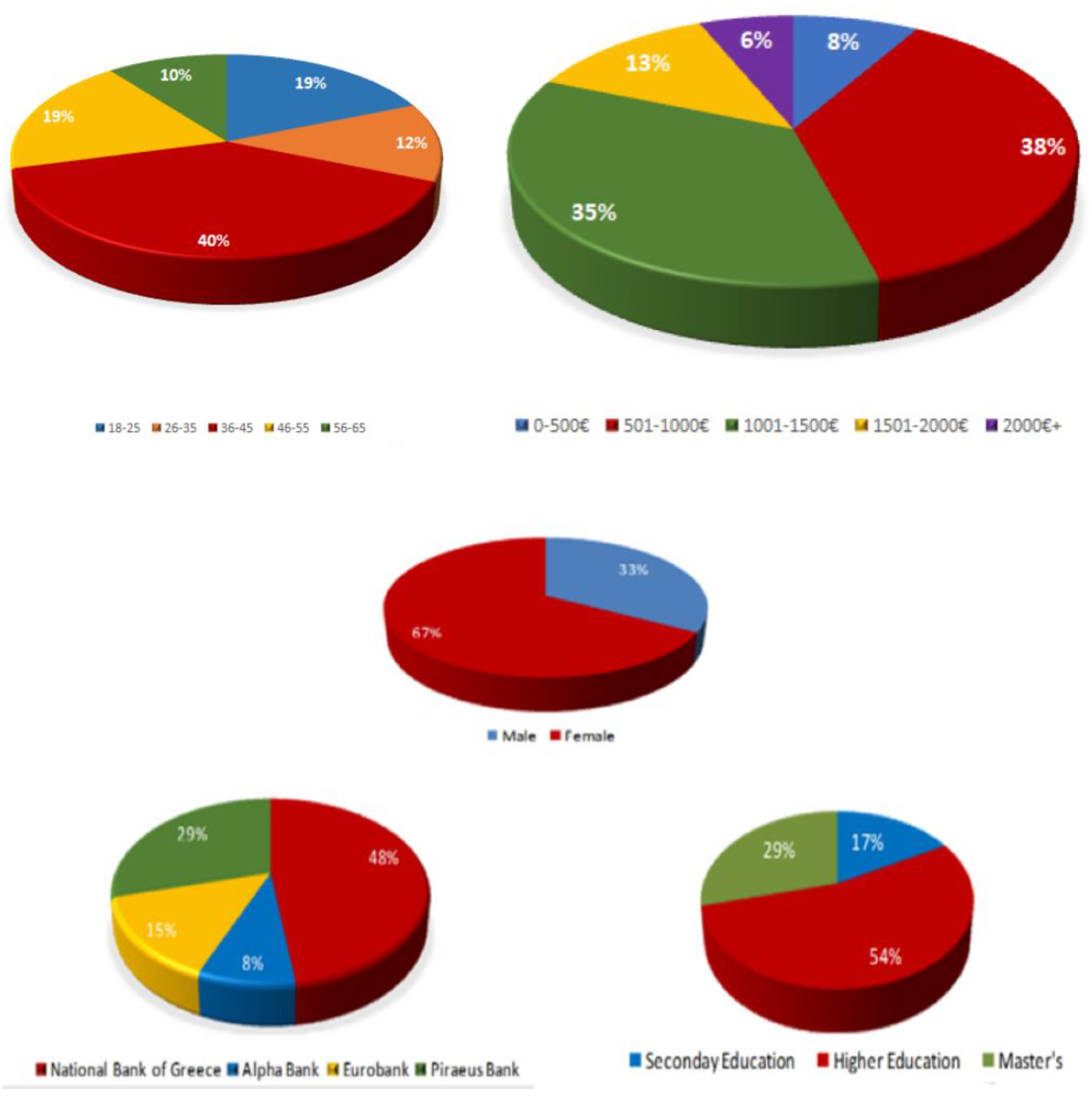

3. Data Description and Methodology

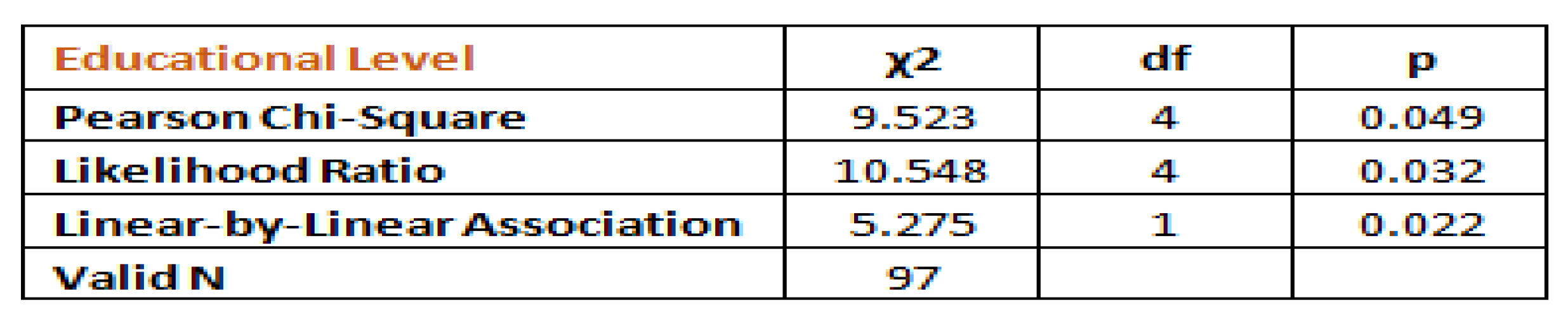

4. Empirical Findings and Discussion

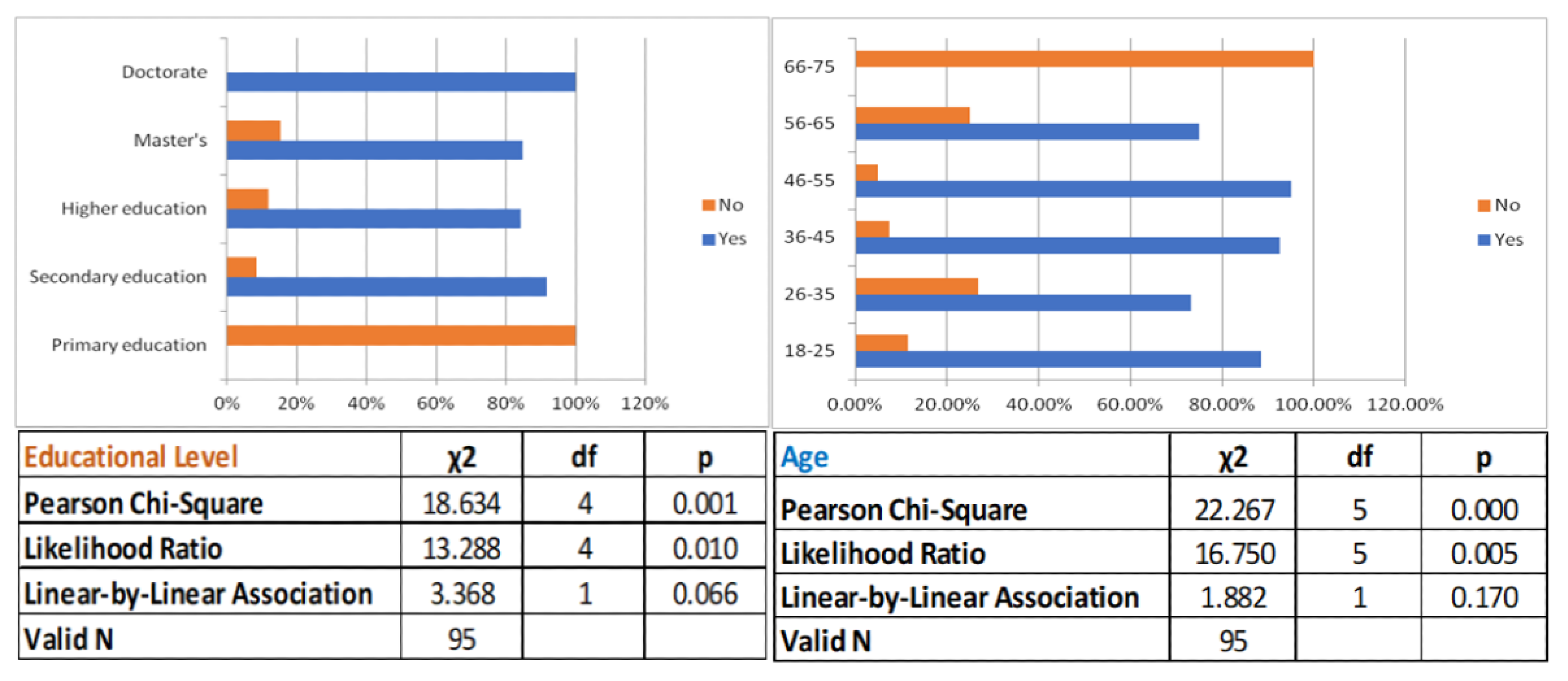

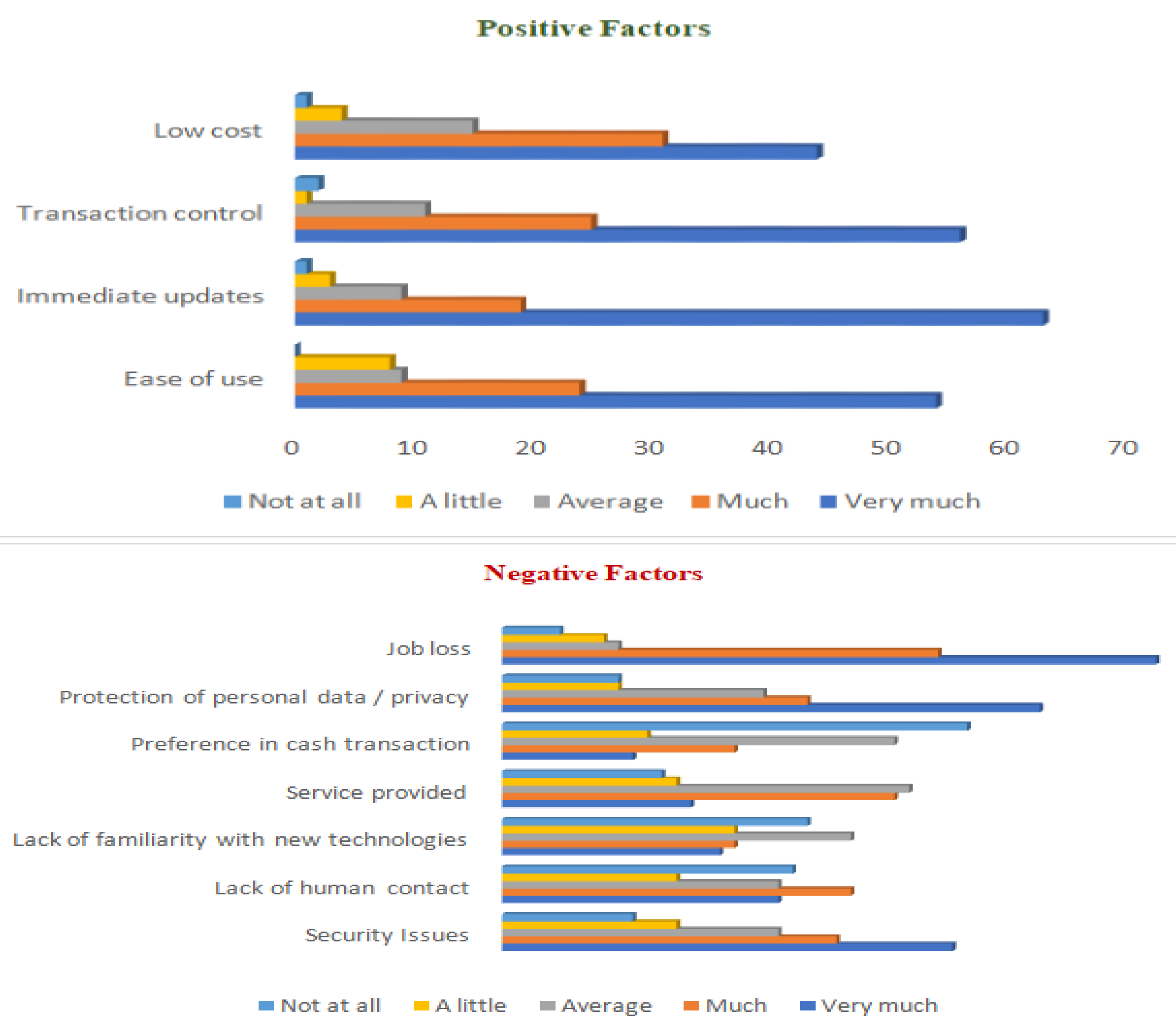

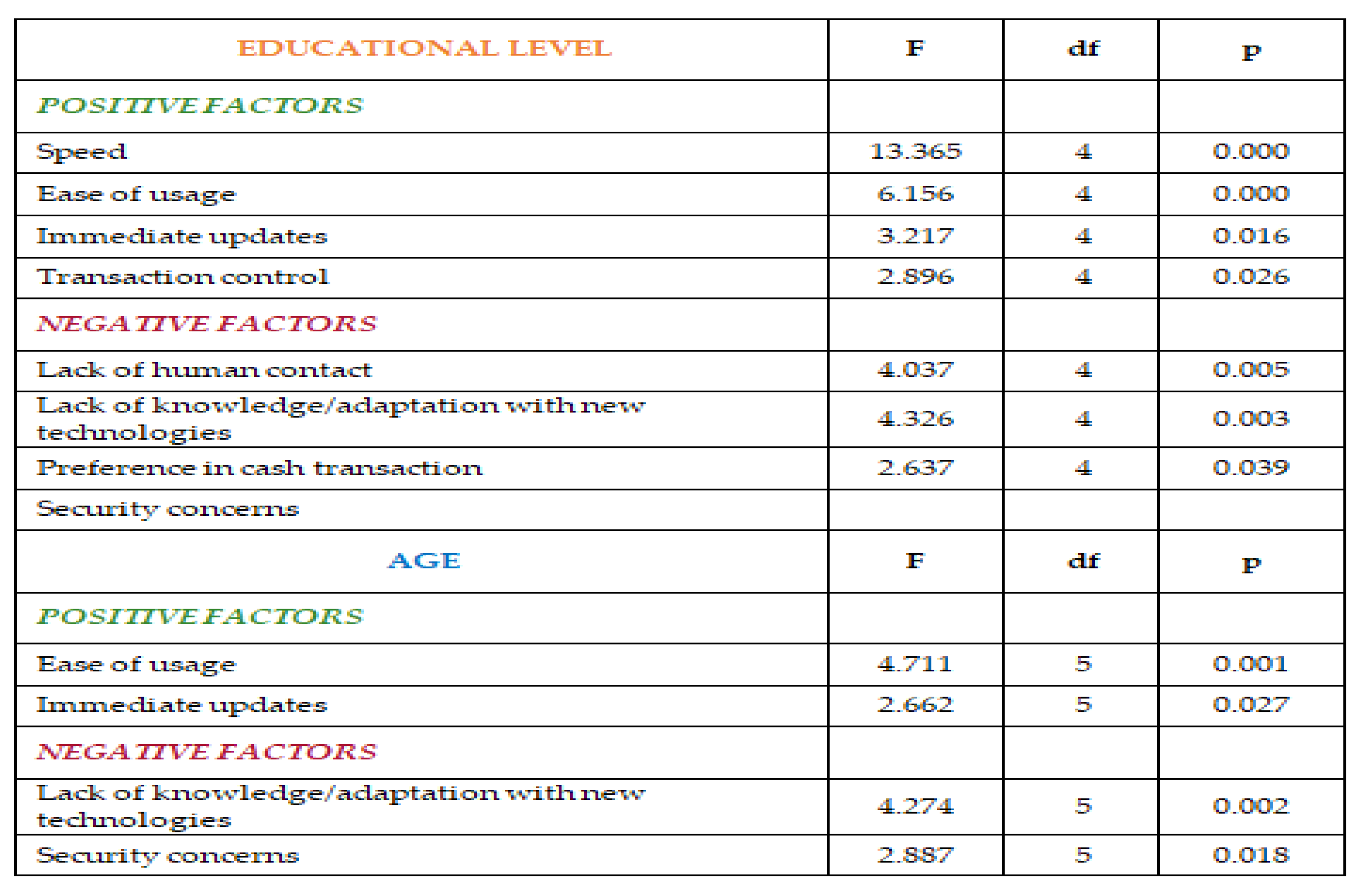

4.1. Bank Customers Analysis

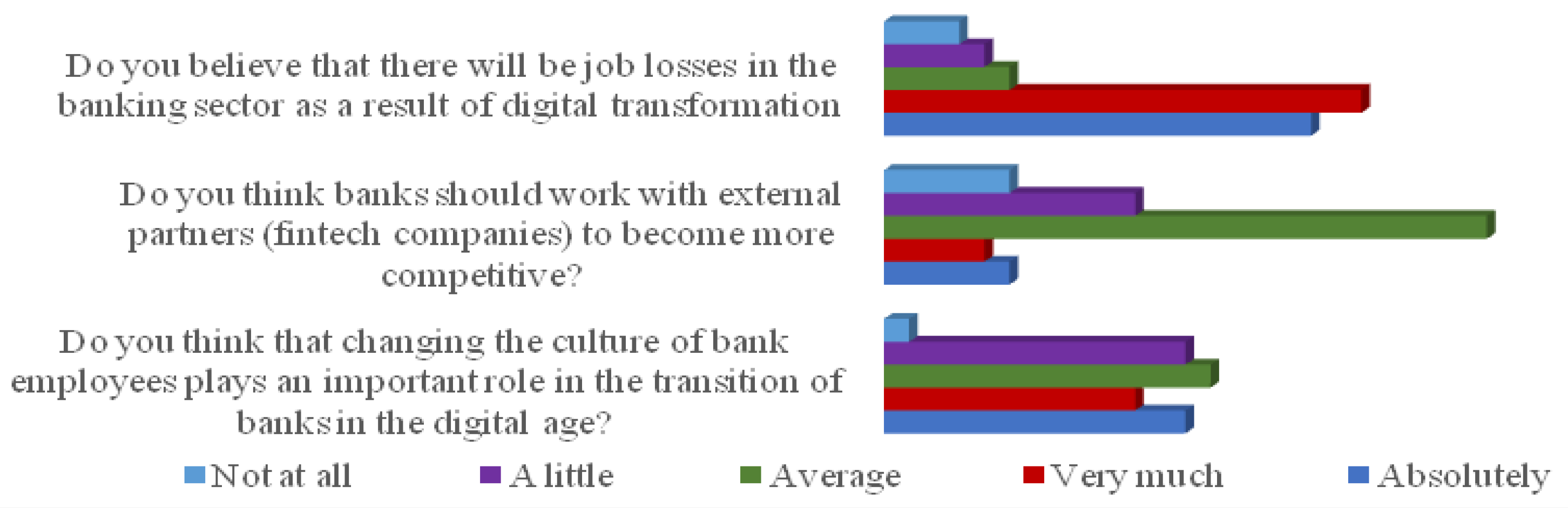

4.2. Bank Employees Analysis

5. Concluding Remarks

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Jensen, J. Urban Change Detection Mapping Using Landsat Digital Data. Am. Cartogr. 1981, 8, 127–147. [Google Scholar] [CrossRef]

- Stolterman, E.; Fors, A.; Wastel, D.; Truex, D. Information Technology and the Good Life. In Information Systems Research: Information Systems Research: Relevant Theory and Informed Practice; Springer: Boston, MA, USA, 2004; pp. 687–692. [Google Scholar] [CrossRef]

- Martin, A. Digital Literacy and the “Digital Society”. In Digital Literacies Concepts Policies Practices; Peter Lang Publishing Inc.: New York, NY, USA, 2008; Volume 30, pp. 151–176. Available online: https://www.academia.edu/293040/Digital_Literacies_Concepts_Policies_and_Practices (accessed on 20 June 2021).

- Liu, D.; Chen, S.; Chou, T. Resource Fit in Digital Transformation. Manag. Decis. 2011, 49, 1728–1742. [Google Scholar] [CrossRef]

- Westerman, G.; Calméjane, C.; Bonnet, D.; Ferraris, P.; McAfee, A. Digital Transformation: A Roadmap for Billion-Dollar Organization. MIT Center Digit. Bus. Capgemini Consult. 2011, 21, 8–10. [Google Scholar]

- Solis, B.; Li, C.; Szymanski, J. The 2014 State of Digital Transformation. Altimeter Group 2014, 1, 1–33. [Google Scholar]

- Fitzgerald, M.; Kruschwitz, N.; Bonnet, D.; Welch, M. Embracing Digital Technology: A New Strategic Imperative; MIT Sloan Management Review; Massachusetts Institute of Technology: Cambridge, MA, USA, 2014; Volume 55, p. 1. [Google Scholar]

- Bondar, S.; Hsu, J.; Pfouga, A.; Stjepandić, J. Agile Digital Transformation of System-of-Systems Architecture Models using Zachman Framework. J. Ind. Inf. Integr. 2017, 7, 33–43. [Google Scholar] [CrossRef]

- Hinings, B.; Gegenhuber, T.; Greenwood, R. Digital Innovation and Transformation: An institutional perspective. Inf. Organ. 2018, 28, 52–61. [Google Scholar] [CrossRef]

- Kraus, S.; Jones, P.; Kailer, N.; Weinmann, A.; Chaparro-Banegas, N.; Roig-Tierno, N. Digital Transformation: An Overview of the Current State of the Art of Research. SAGE Open 2021, 11, 21582440211047576. [Google Scholar] [CrossRef]

- Legris, P.; Ingham, J.; Collerette, P. Why do People Use Information Technology? A Critical Review of the Technology Acceptance Model. Inf. Manag. 2003, 40, 191–204. [Google Scholar] [CrossRef]

- Venkatesh, V.; Bala, H. Technology Acceptance Model 3 and a Research Agenda on Interventions. Decis. Sci. 2008, 39, 273–315. [Google Scholar] [CrossRef]

- Reis, J.; Amorim, M.; Melão, N.; Matos, P. Digital Transformation: A Literature Review and Guidelines for Future Research. In Advances in Intelligent Systems and Computing; Springer: Cham, Switzerland, 2018; pp. 411–421. [Google Scholar] [CrossRef]

- Vial, G. Understanding Digital Transformation: A Review and a Research Agenda. J. Strateg. Inf. Syst. 2019, 28, 118–144. [Google Scholar] [CrossRef]

- Katsamakas, E. Digital Transformation, and Sustainable Business Models. Sustainability 2022, 14, 6414. [Google Scholar] [CrossRef]

- Singh, A.; Klarner, P.; Hess, T. How Do Chief Digital Officers Pursue Digital Transformation Activities? The Role of Organization Design Parameters. Long Range Plan. 2020, 53, 101890. [Google Scholar] [CrossRef]

- Sloboda, L.; Dunas, N.; Limanski, A. Contemporary Challenges and Risks of Retail Banking Development in Ukraine. Banks Bank Syst. 2018, 13, 88–97. [Google Scholar] [CrossRef]

- National Bank of Greece (NBG). A Digital Reboot for the Greek Economy, Sectoral Report, April 2020; National Bank of Greece: Athens, Greece, 2020. [Google Scholar]

- Kitsios, F.; Giatsidis, I.; Kamariotou, M. Digital Transformation and Strategy in the Banking Sector: Evaluating the Acceptance Rate of E-Services. J. Open Innov. Technol. Mark. Complex. 2021, 7, 204. [Google Scholar] [CrossRef]

- Stavrou, N. Digital Transformation and Business: Challenges and Opportunities; University of Piraeus: Piraeus, Greece, 2018. [Google Scholar]

- Microsoft. Your Roadmap for a Digital-First Business: Transformation at Microsoft; Microsoft: Redmond, WA, USA, 2018. [Google Scholar]

- Cuesta, C.; Ruesta, M.; Tuesta, D.; Urbiola, P. The Digital Tansformation of the Banking Industry. BBVA Res. 2015, 1–10. Available online: https://www.bbvaresearch.com/wp-content/uploads/2015/08/EN_Observatorio_Banca_Digital_vf3.pdf (accessed on 10 June 2021).

- Laforet, S.; Li, X. Consumers’ Attitudes Towards Online and Mobile Banking in China. Int. J. Bank Mark. 2005, 23, 362–380. [Google Scholar] [CrossRef]

- Amin, M. Internet Banking Service Quality and its Implication on E-Customer Satisfaction and E-Customer Loyalty. Int. J. Bank Mark. 2016, 34, 280–306. [Google Scholar] [CrossRef]

- Suhaimi, A.; Bin Abu Hassan, M. Determinants of Branchless Digital Banking Acceptance Among Generation Y in Malaysia. In Proceedings of the 2018 IEEE Conference on e-Learning, e-Management and e-Services (IC3e), Langkawi, Malaysia, 21–22 November 2018. [Google Scholar] [CrossRef]

- Sudarsono, H.; Nugrohowati, R.N.I.; Tumewang, Y.K. The Effect of COVID-19 Pandemic on the Adoption of Internet Banking in Indonesia: Islamic Bank and Conventional Bank. J. Asian Financ. Econ. Bus. 2020, 7, 789–800. [Google Scholar] [CrossRef]

- Shahabi, V.; Azar, A.; Razi, F.F.; Shams, M.F.F. Simulation of the Effect of COVID-19 Outbreak on the Development of Branchless Banking in Iran: Case Study of Resalat Qard–al-Hasan Bank. Rev. Behav. Financ. 2021, 13, 85–108. [Google Scholar] [CrossRef]

- Diener, F.; Špaček, M. Digital Transformation in Banking: A Managerial Perspective on Barriers to Change. Sustainability 2021, 13, 2032. [Google Scholar] [CrossRef]

- Santouridis, I.; Kyritsi, M. Investigating the Determinants of Internet Banking Adoption in Greece. Procedia Econ. Financ. 2014, 9, 501–510. [Google Scholar] [CrossRef]

- Lantzakis, K. Digital Banking; HOU: Patras, Greece, 2018. [Google Scholar]

- Tzanopoulou, E. Digital Banking: The Digital Transformation of Greek Banks; HOU: Patras, Greece, 2018. [Google Scholar]

- Tsetos, D. Digital Banking the Digital Transformation of Greek Banks; HOU: Patras, Greece, 2019. [Google Scholar]

- Psallida, M. Digital Banking; HOU: Patras, Greece, 2021. [Google Scholar]

- Batsilas, A. Digital Age: Opportunities and Threats in the Banking Area. Case Study: National Bank of Greece; University of Piraeus: Piraeus, Greece, 2018. [Google Scholar]

- Tsourapis, V. Information Systems in the Banking Sector; University of Patras: Patras, Greece, 2022. [Google Scholar]

- Hatzitoliou, C. The Impact of the COVID Pandemia in the Digital Transformation of the Banking Sector; University of West Attica: Egaleo, Greece, 2021. [Google Scholar]

- Perraki, S. Digital Transformation in the Banking Sector; University of Piraeus: Piraeus, Greece, 2020; Available online: https://dione.lib.unipi.gr/xmlui/bitstream/handle/unipi/12907/Perraki_MOES_1841.pdf (accessed on 20 May 2021).

- Segounis, I. Digital Transformation of Banks and Job Losses. NBG Case-Stud; HOU: Patras, Greece, 2021. [Google Scholar]

- Giatsidis, I. The Degree of Acceptance of the Digital Transformation of the Banking Services by the Staff of the Greek Banks; University of Macedonia: Thessaloniki, Greece, 2020. [Google Scholar]

- Never, M. Sampling in Research; IGI Global: Hershey, PA, USA, 2016. [Google Scholar] [CrossRef]

- Kitsios, F.; Kamariotou, M. Artificial Intelligence and Business Strategy Towards Digital Transformation: A Research Agenda. Sustainability 2021, 13, 2025. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Boufounou, P.; Mavroudi, M.; Toudas, K.; Georgakopoulos, G. Digital Transformation of the Greek Banking Sector in the COVID Era. Sustainability 2022, 14, 11855. https://doi.org/10.3390/su141911855

Boufounou P, Mavroudi M, Toudas K, Georgakopoulos G. Digital Transformation of the Greek Banking Sector in the COVID Era. Sustainability. 2022; 14(19):11855. https://doi.org/10.3390/su141911855

Chicago/Turabian StyleBoufounou, Paraskevi, Magdalini Mavroudi, Kanellos Toudas, and Georgios Georgakopoulos. 2022. "Digital Transformation of the Greek Banking Sector in the COVID Era" Sustainability 14, no. 19: 11855. https://doi.org/10.3390/su141911855

APA StyleBoufounou, P., Mavroudi, M., Toudas, K., & Georgakopoulos, G. (2022). Digital Transformation of the Greek Banking Sector in the COVID Era. Sustainability, 14(19), 11855. https://doi.org/10.3390/su141911855