European Green Transition Implications on Africa’s Livestock Sector Development and Resilience to Climate Change

Abstract

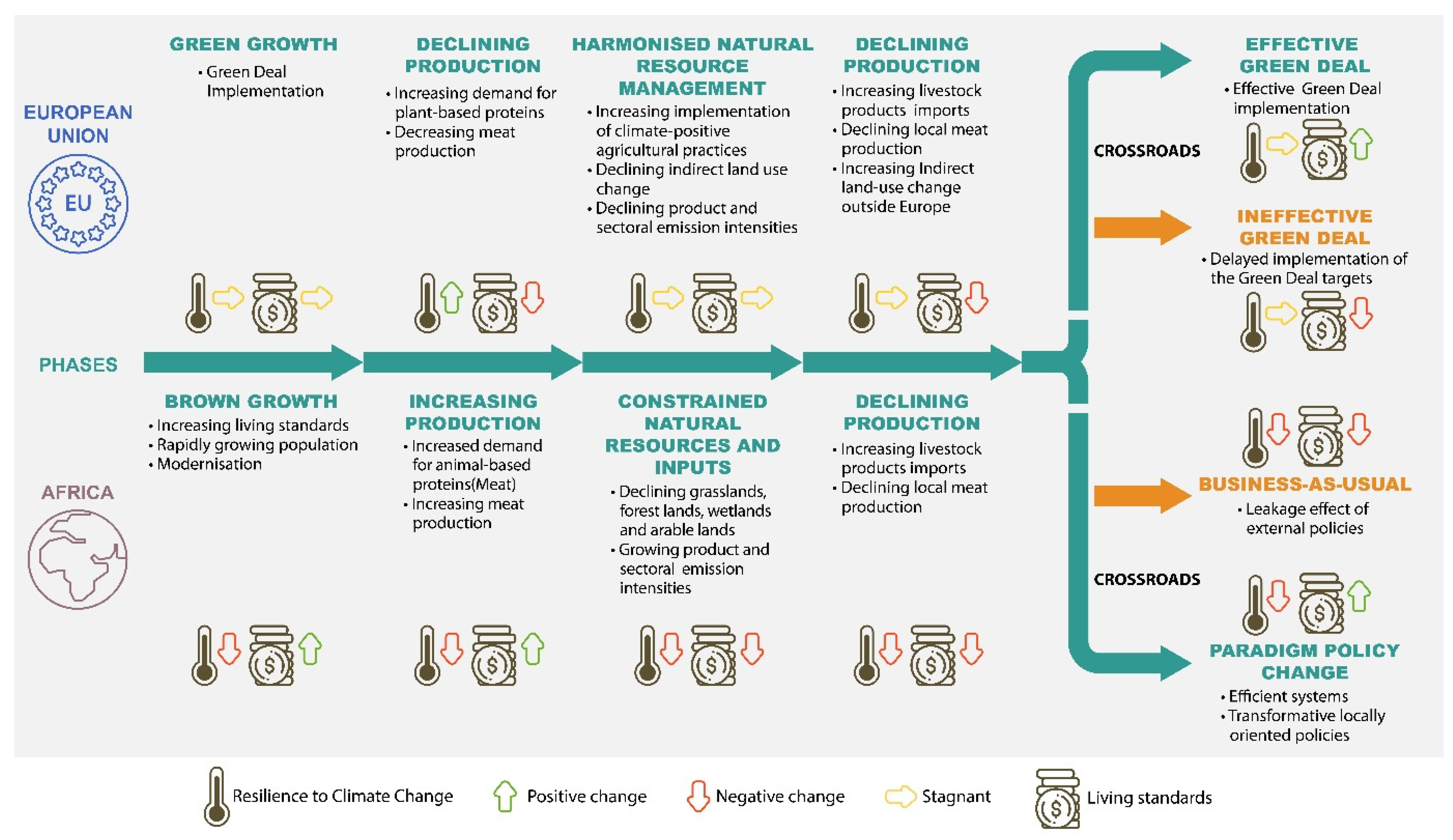

:1. Introduction

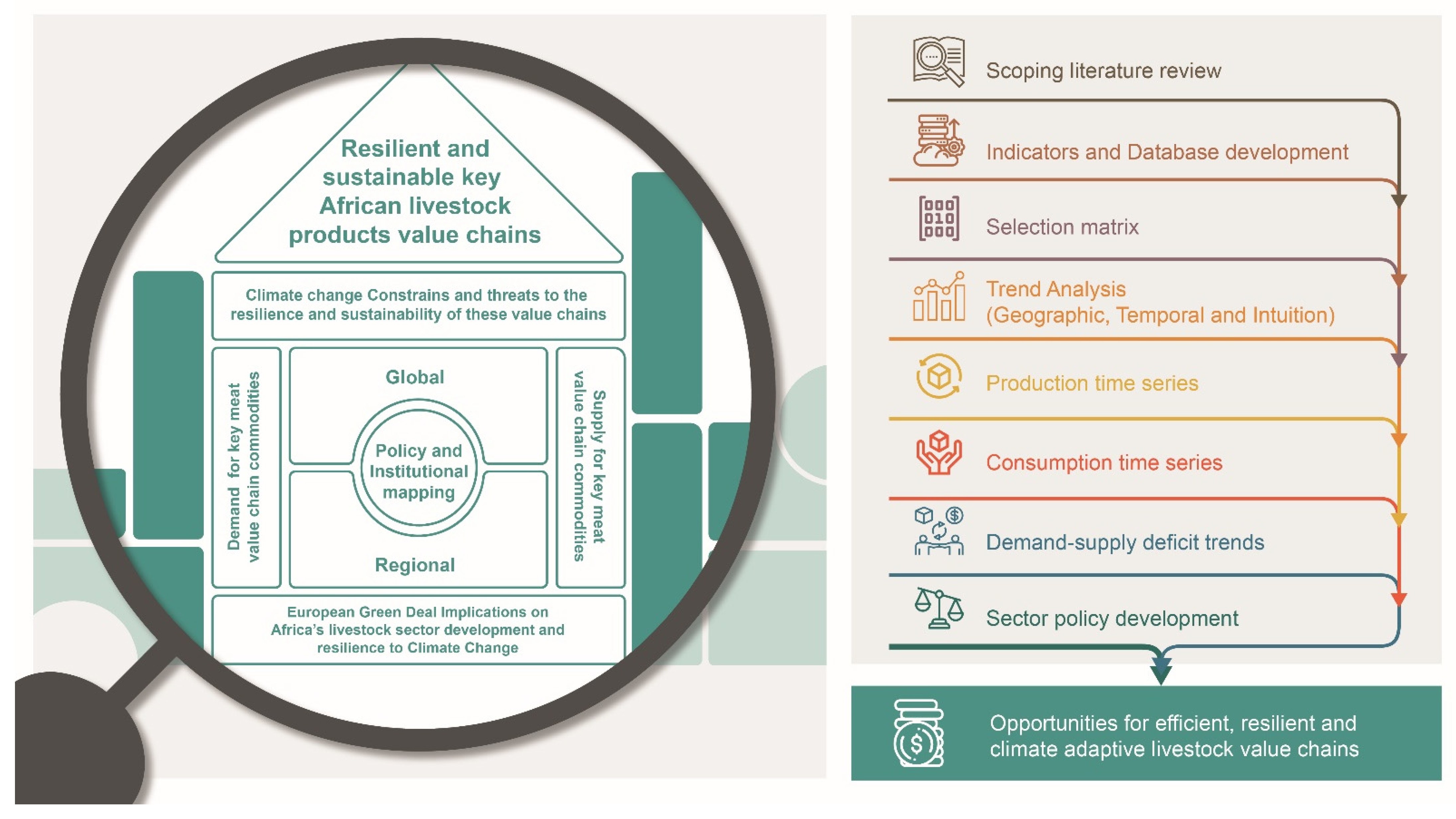

2. Materials and Methods

3. Results

3.1. Indicators and Database Development

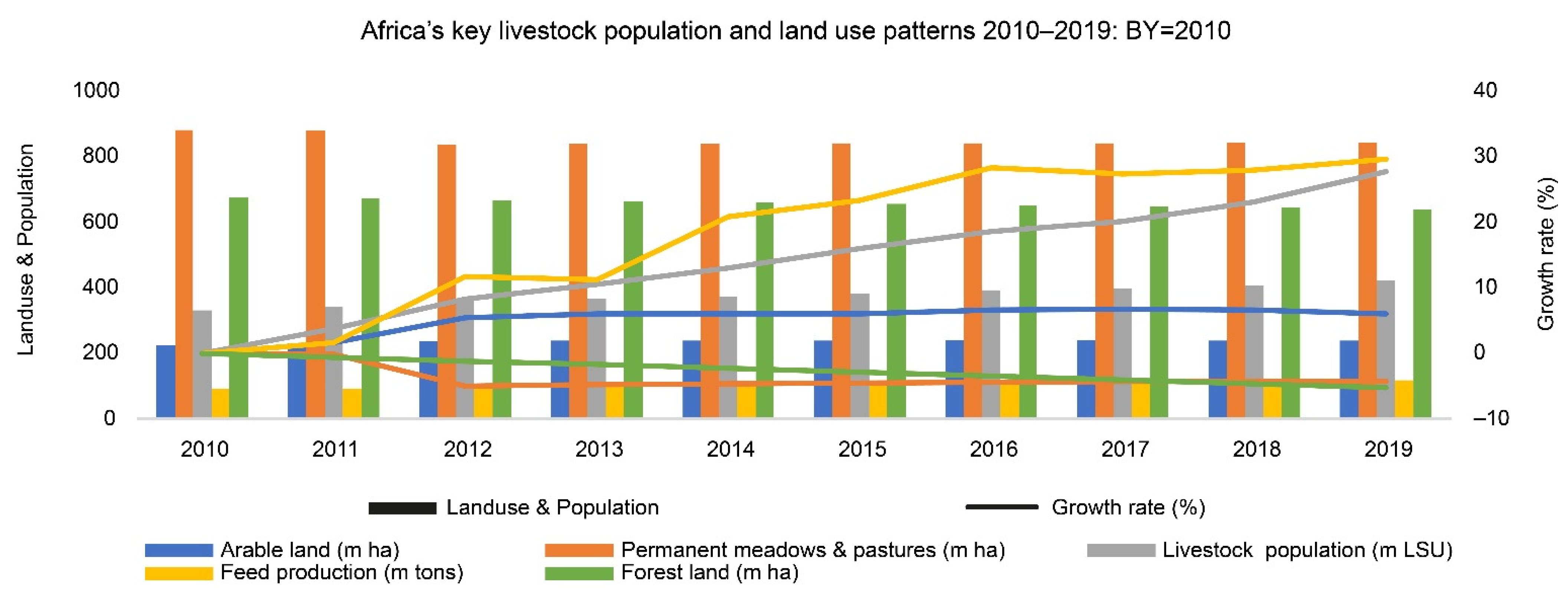

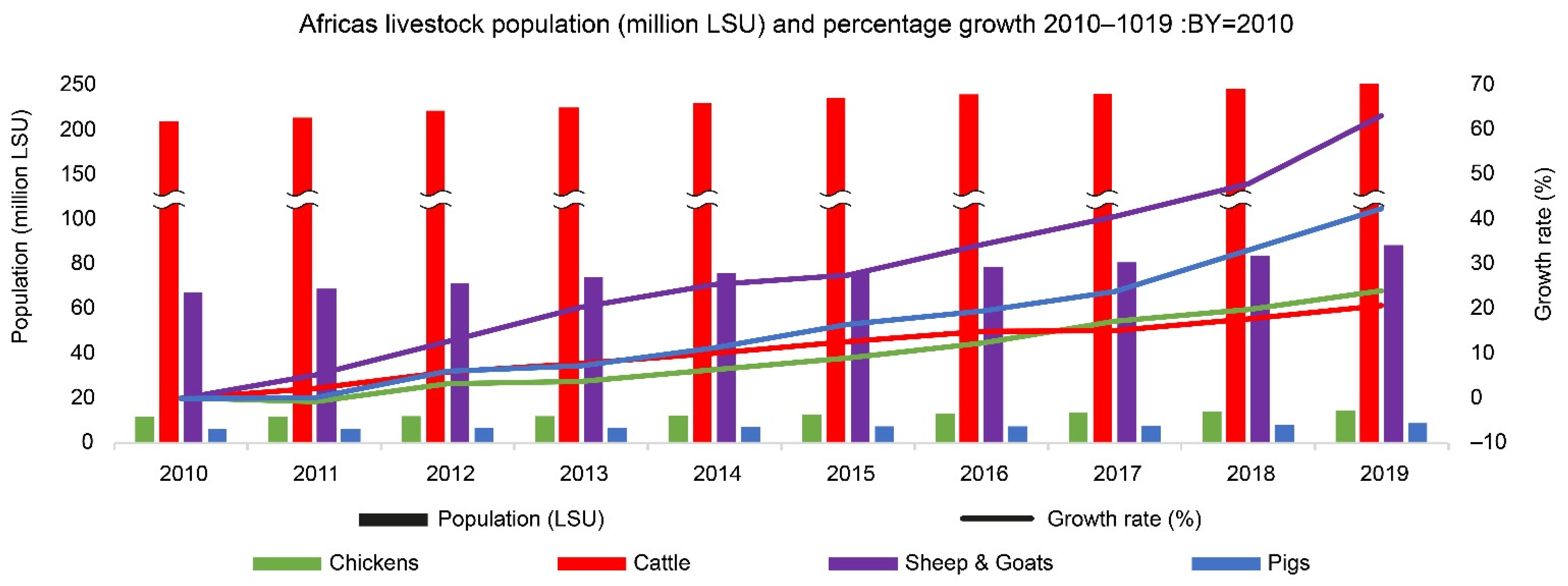

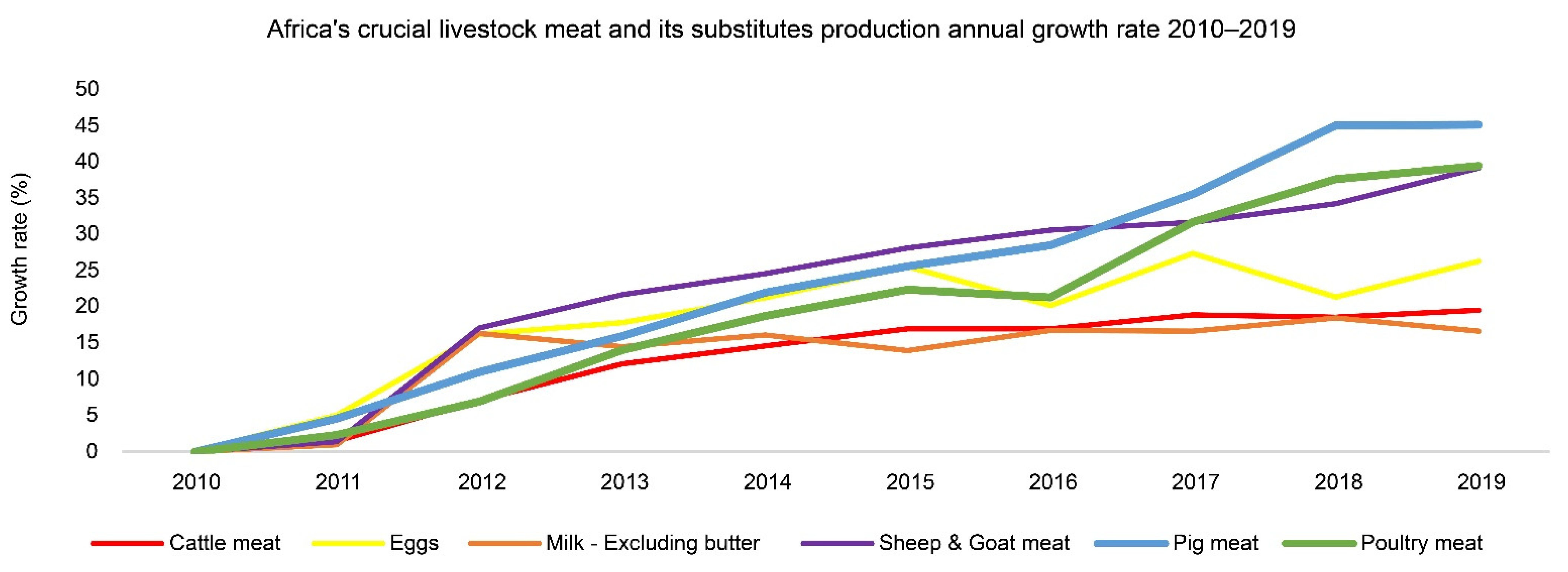

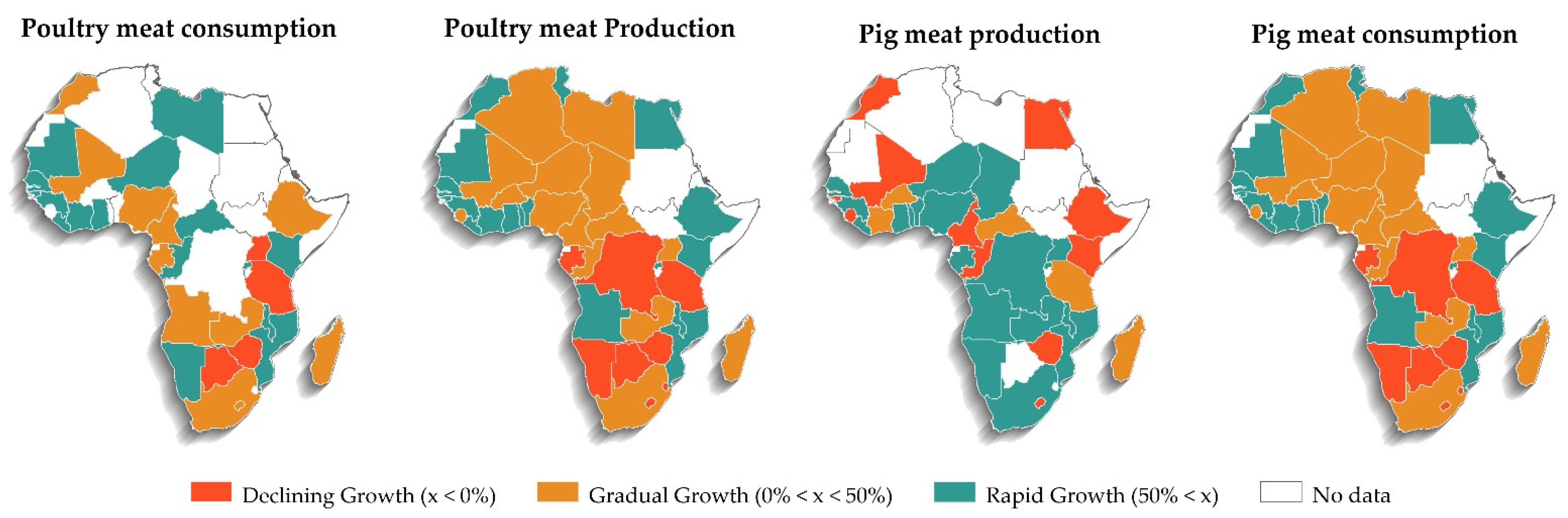

3.2. Africa’s Livestock Production Capacity Trends and How They Are Influencing the Sector

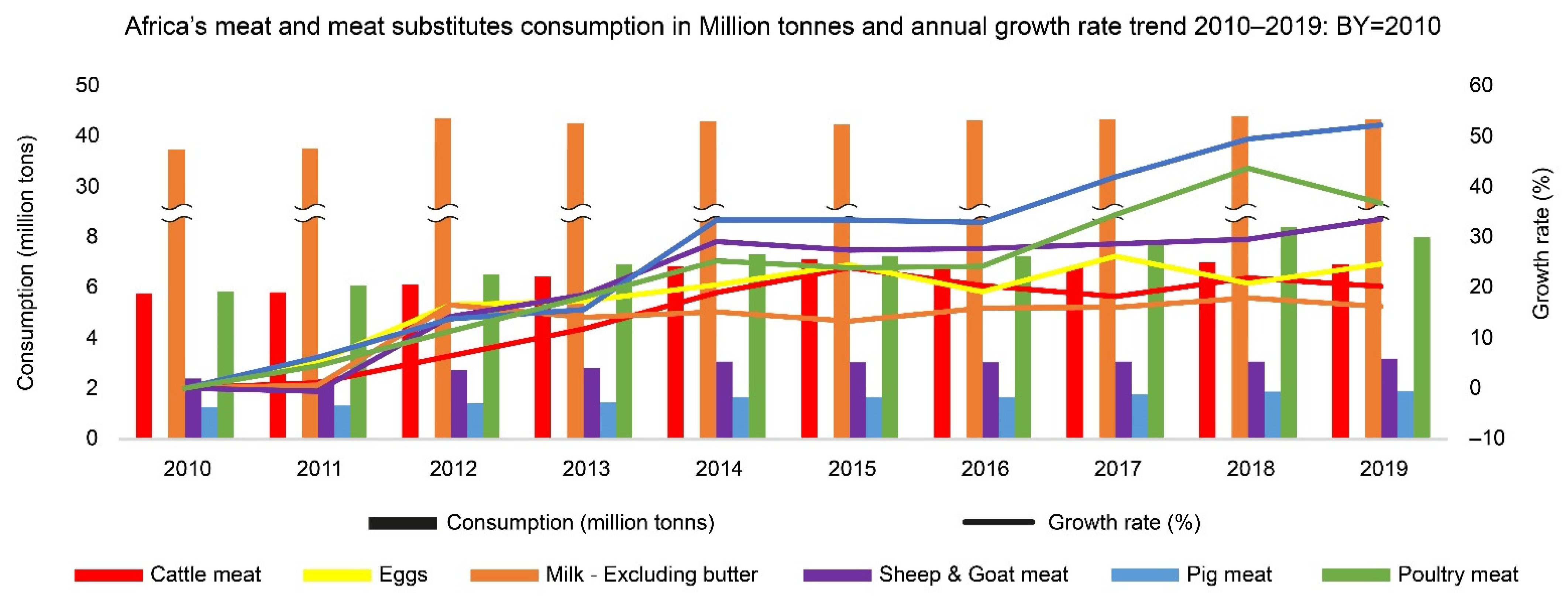

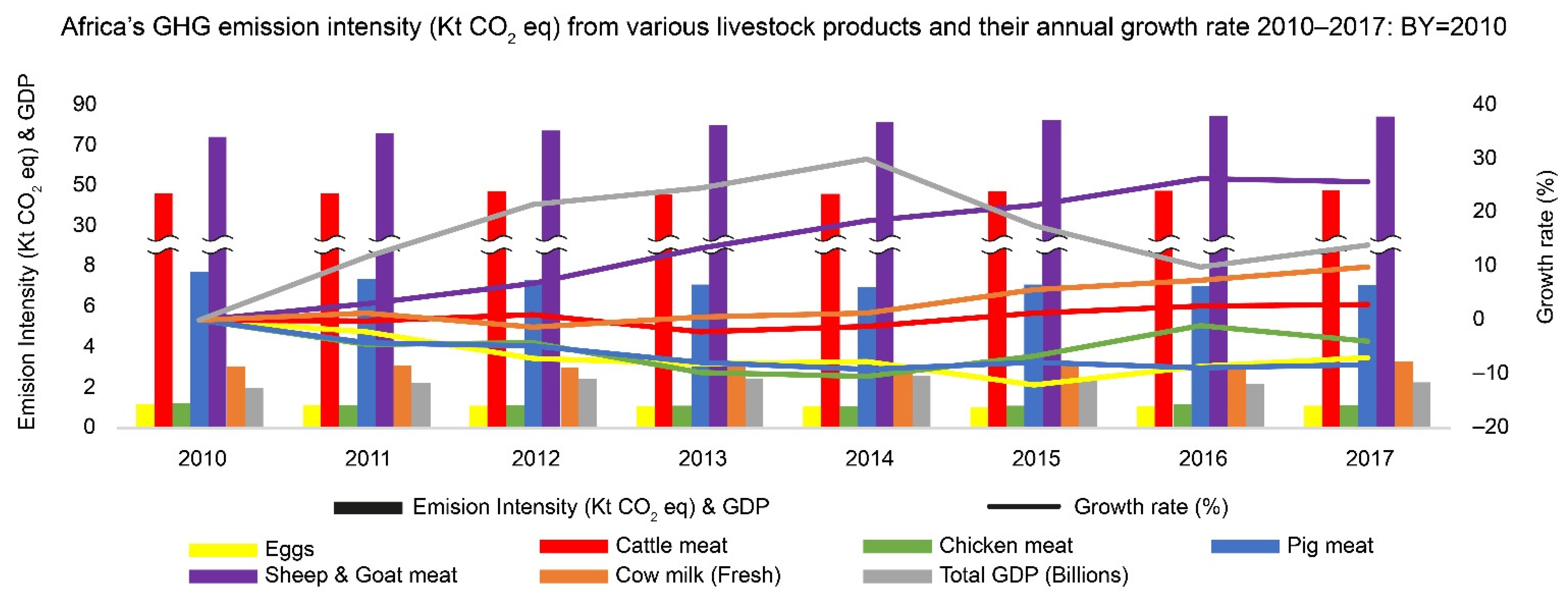

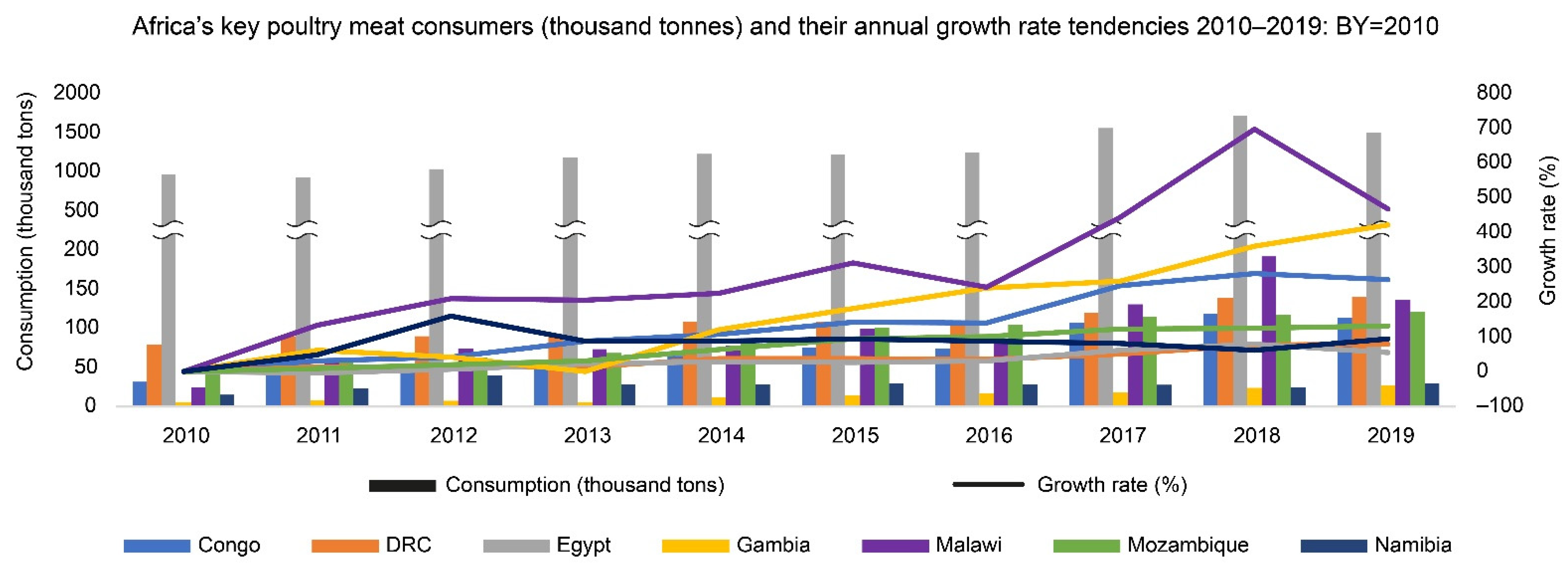

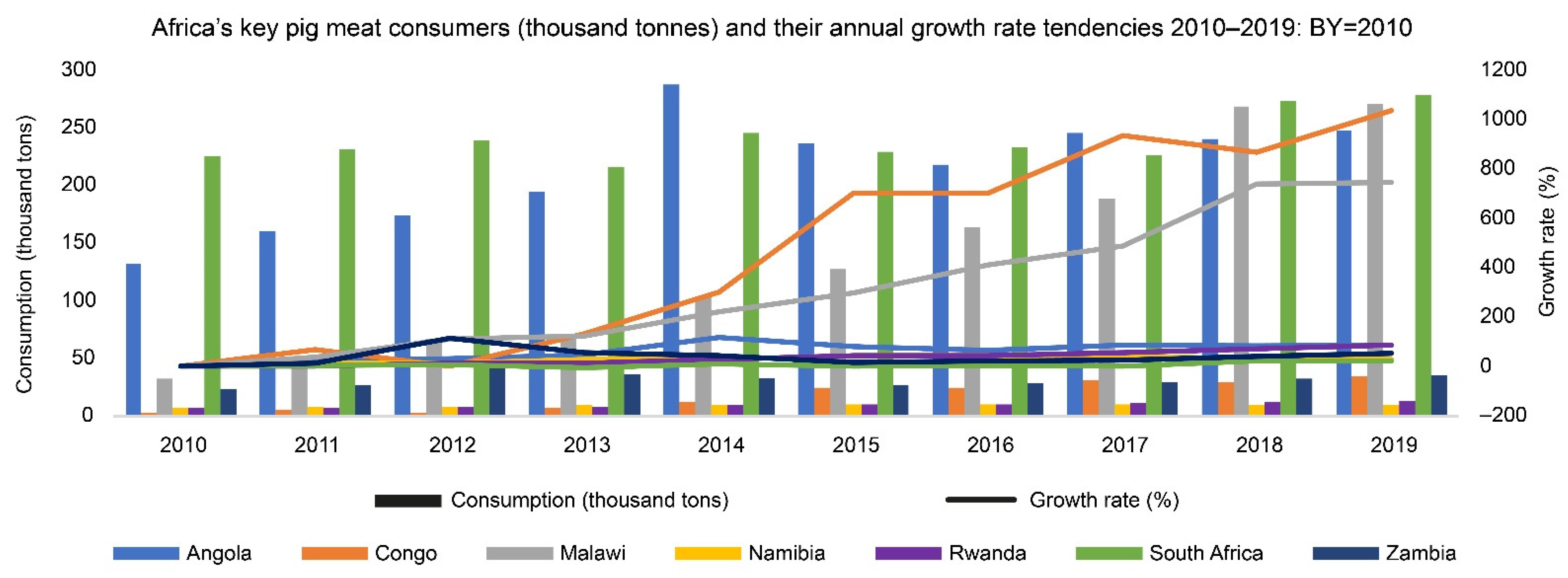

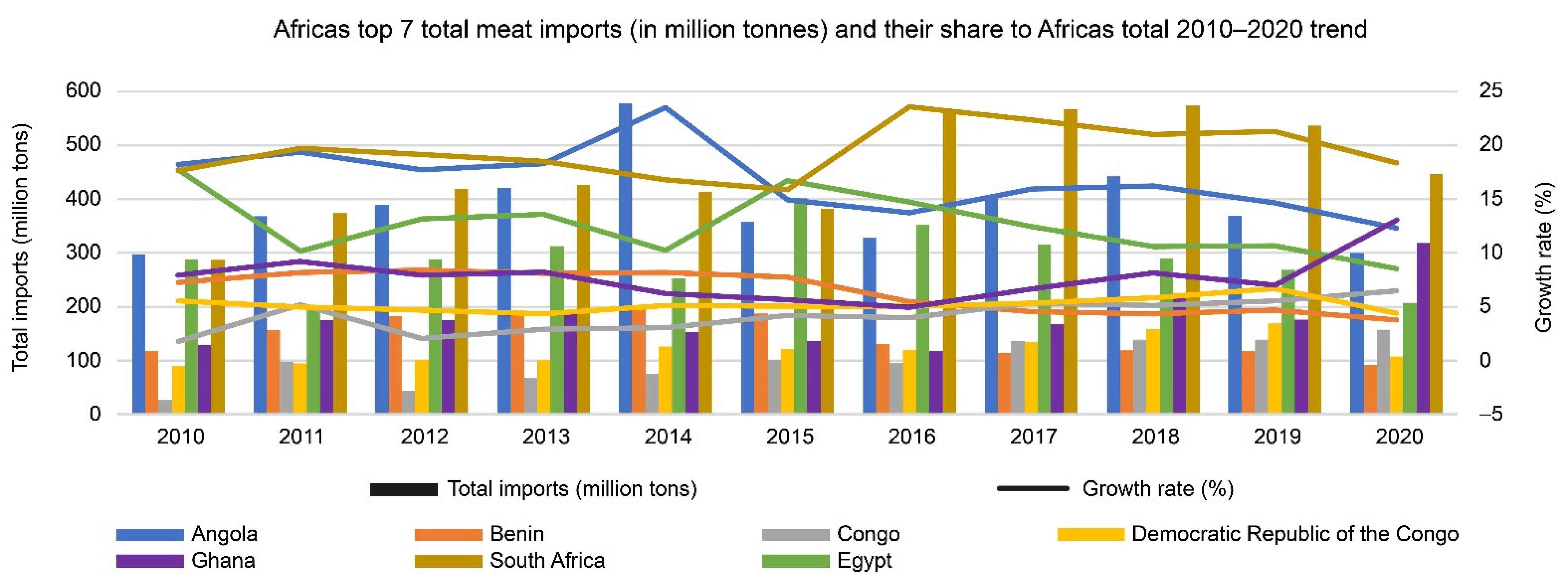

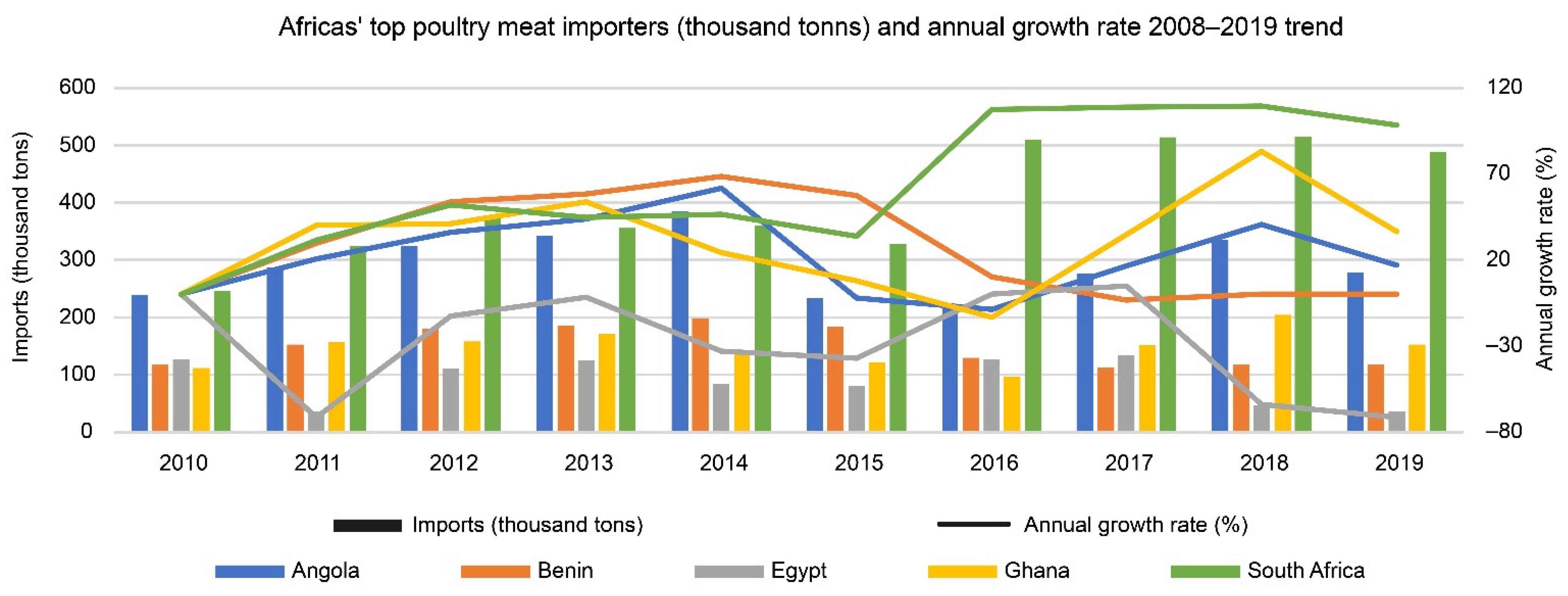

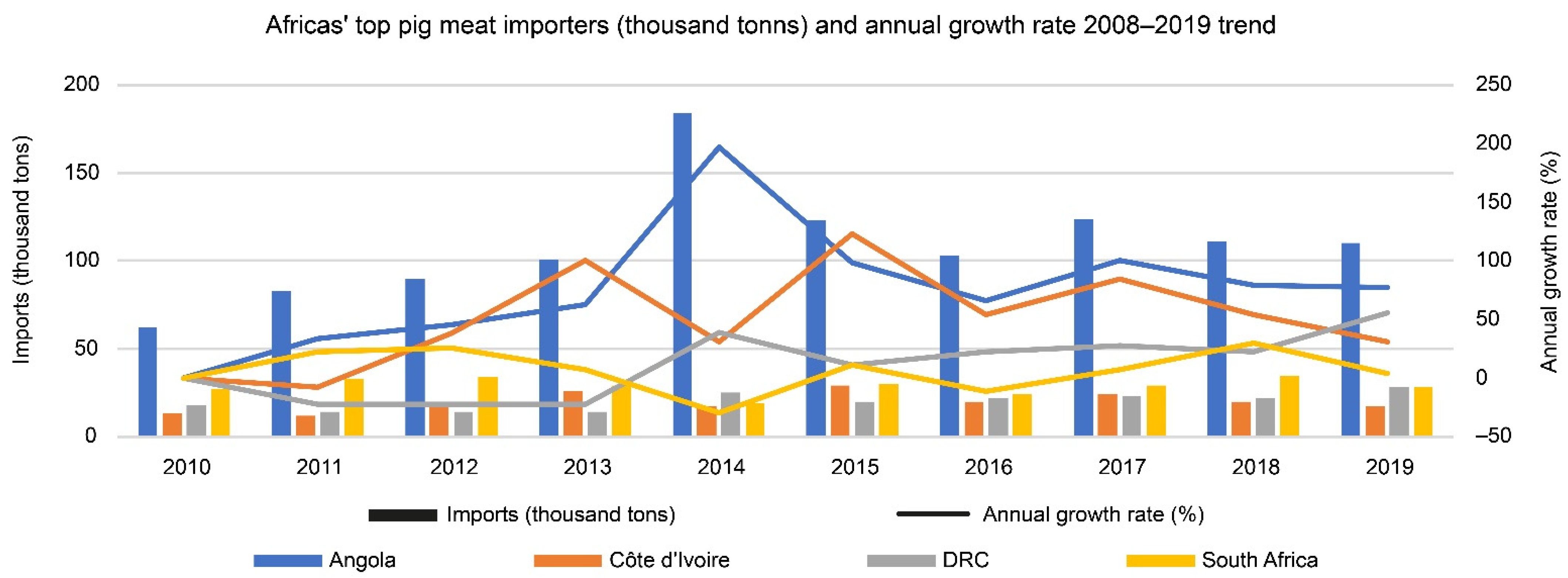

3.3. African Livestock Products Consumption Tendencies and How They Influence the Sector

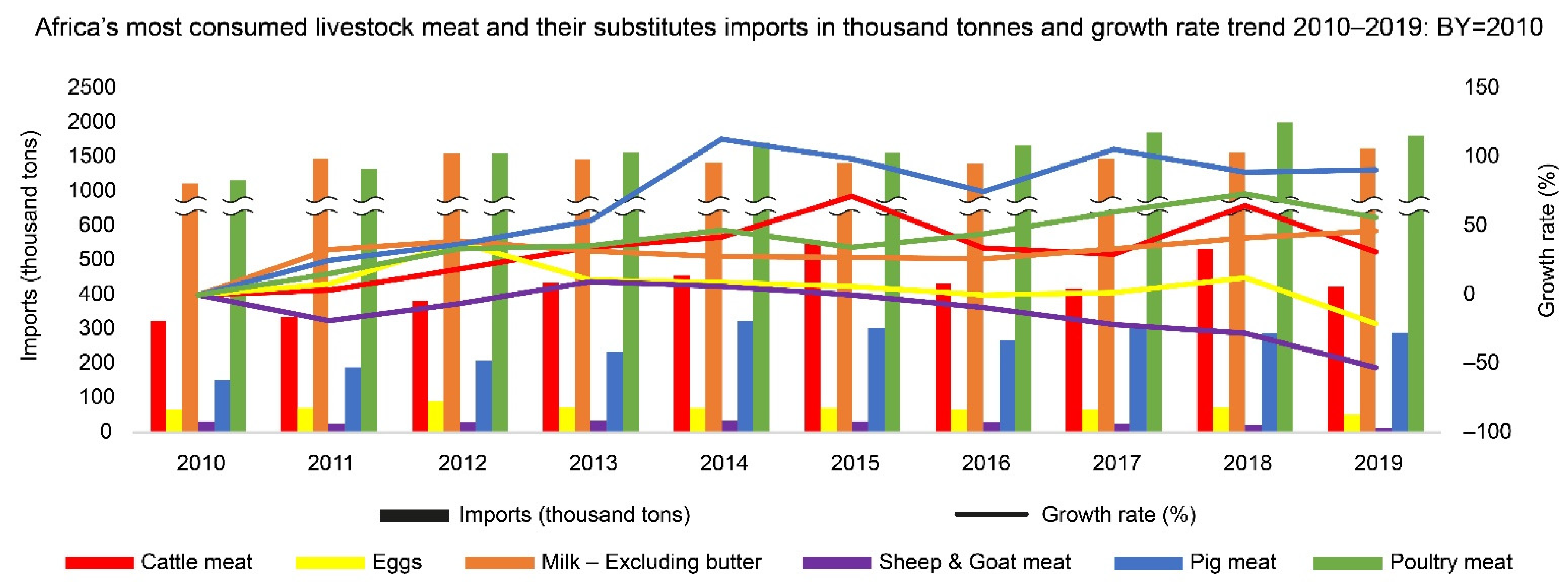

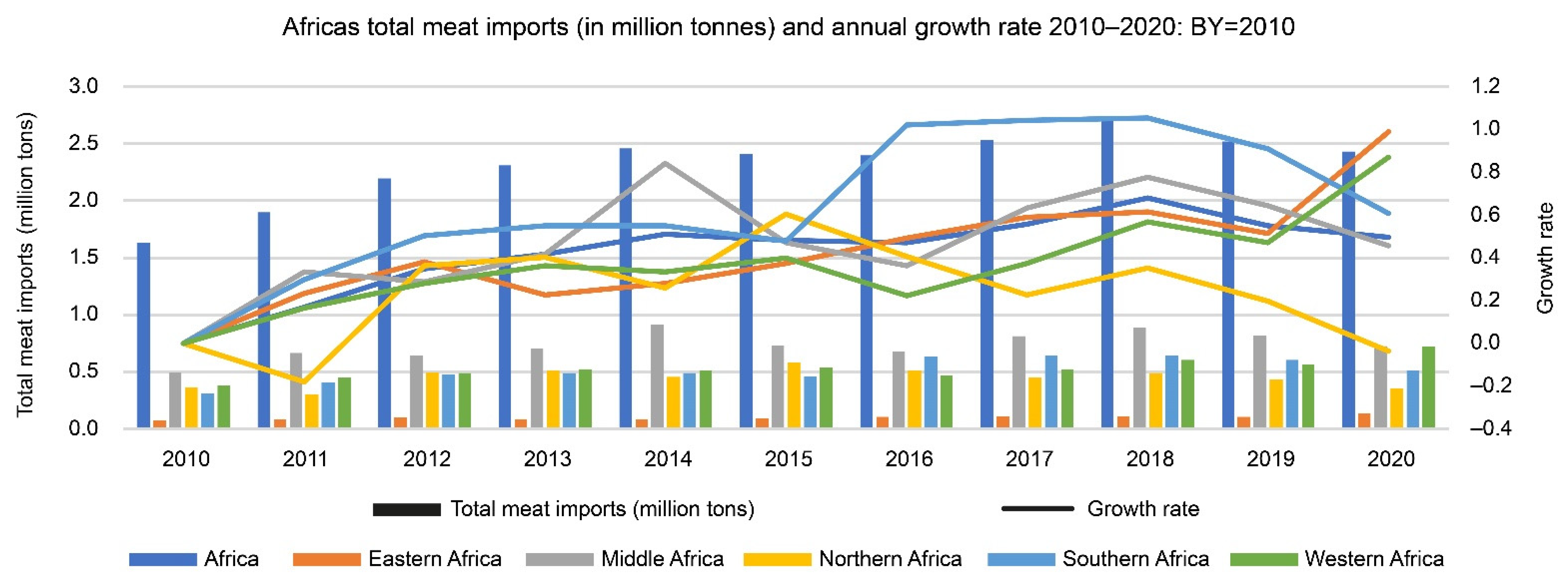

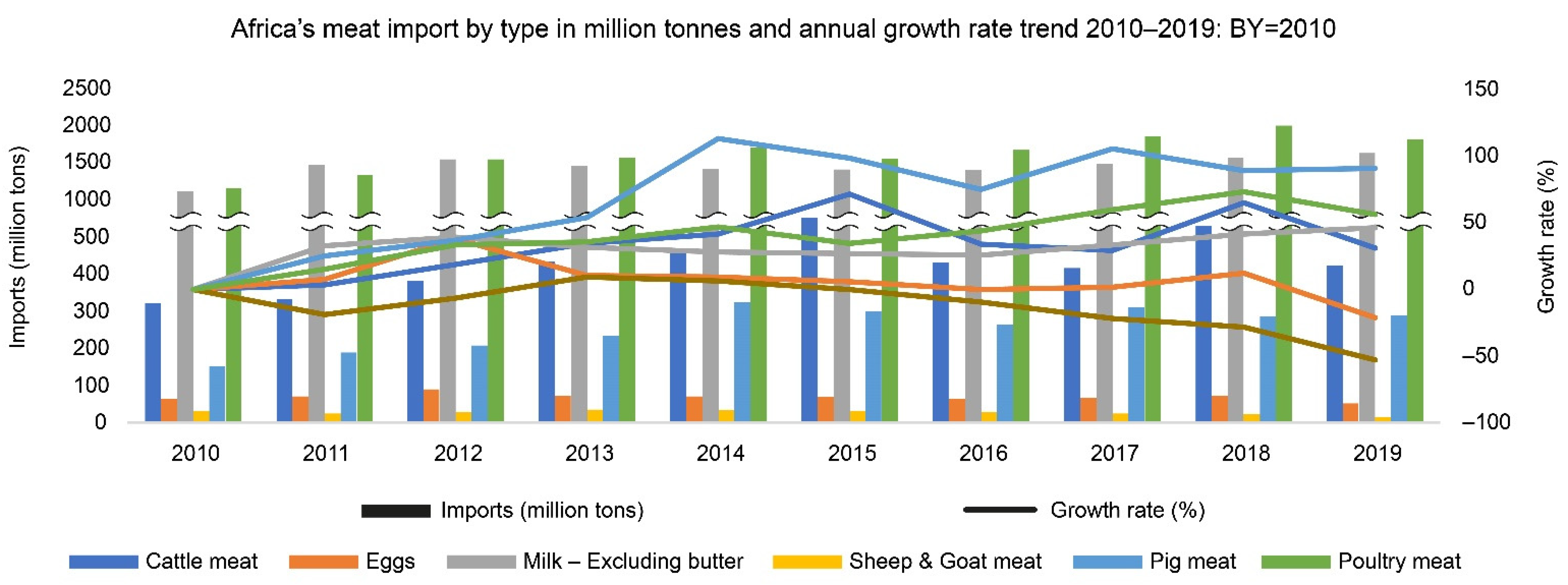

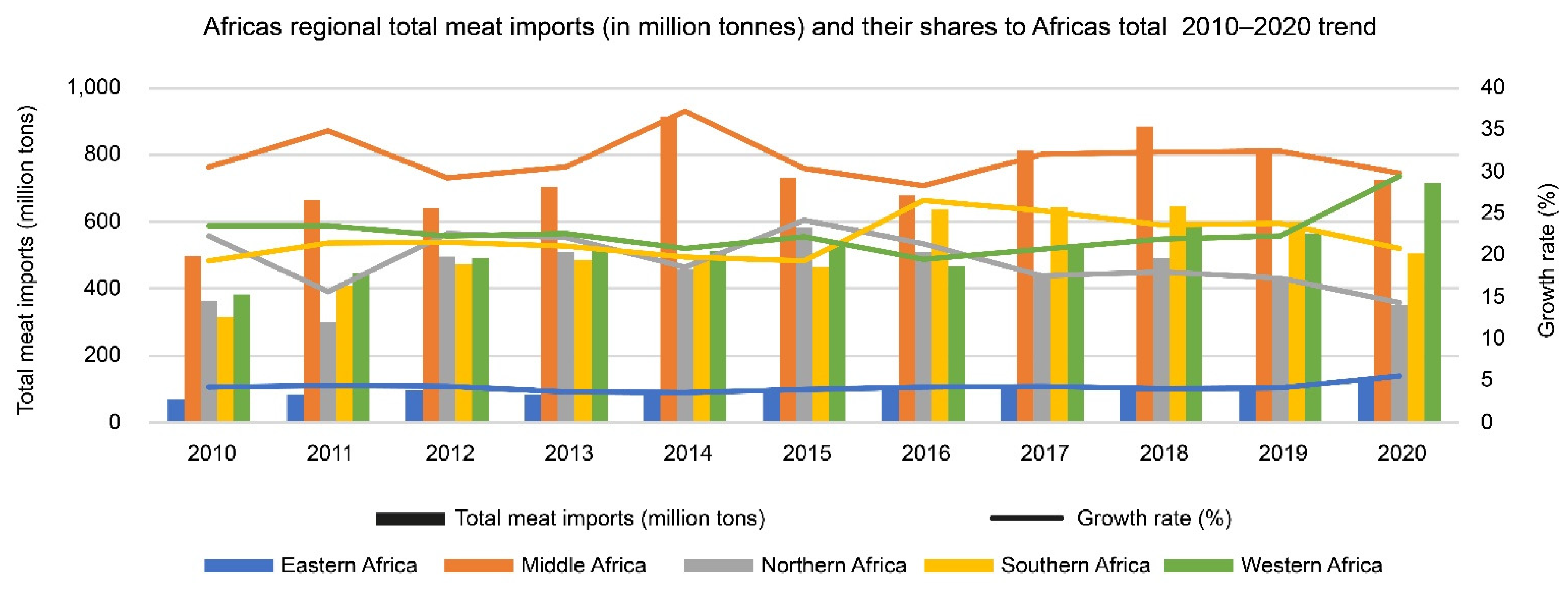

3.4. Trends and Tendencies in Addressing the Demand-Supply Deficit and Its Associated Impacts

3.5. Policy Developments on Africa’s Growing Demand for Meat Products and Their Implications on Climate

3.5.1. Policy Approaches and Strategies Defining the Revitalisation of the African Meat Industry

3.5.2. Implications of Addressing Policy Gaps and Future Actions to Implement

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Philip, K.T. Livestock Production: Recent Trends, Future Prospects. Philos. Trans. R. Soc. B 2010, 365, 2853–2867. [Google Scholar] [CrossRef] [Green Version]

- Ndue, K.; Pál, G. Life Cycle Assessment Perspective for Sectoral Adaptation to Climate Change: Environmental Impact Assessment of Pig Production. Land 2022, 11, 827. [Google Scholar] [CrossRef]

- Havlík, P.; Valin, H.; Herrero, M.; Obersteiner, M.; Schmid, E.; Rufino, M.C.; Mosnier, A.; Thornton, P.K.; Böttcher, H.; Conant, R.T.; et al. Climate change mitigation through livestock system transitions. Proc. Natl. Acad. Sci. USA 2014, 111, 3709–3714. [Google Scholar] [CrossRef] [Green Version]

- Weiss, F.; Leip, A. Greenhouse gas emissions from the EU livestock sector: A life cycle assessment carried out with the CAPRI model. Agric. Ecosyst. Environ. 2012, 149, 124–134. [Google Scholar] [CrossRef]

- Kiebert, G.M.; Curran, D.; Aaronson, N.K.; Bolla, M.; Menten, J.; Rutten, E.H.; Nordman, E.; Silvestre, M.E.; Pierart, M.; Karim, A.B. Quality of life after radiation therapy of cerebral low-grade gliomas of the adult: Results of a randomised phase III trial on dose response (EORTC trial 22844). Eur. J. Cancer 1998, 34, 1902–1909. [Google Scholar] [CrossRef]

- Rojas-Downing, M.M.; Nejadhashemi, A.P.; Harrigan, T.; Woznicki, S.A. Climate change and livestock: Impacts, adaptation, and mitigation. Clim. Risk Manag. 2017, 16, 145–163. [Google Scholar] [CrossRef]

- Leinonen, I. Achieving environmentally sustainable livestock production. Sustainability 2019, 11, 246. [Google Scholar] [CrossRef] [Green Version]

- Lezoche, M.; Hernandez, J.E.; Díaz, M.D.; Panetto, H.; Kacprzyk, J. Agri-food 4.0: A survey of the supply chains and technologies for the future agriculture. Comput. Ind. 2020, 117, 103187. [Google Scholar] [CrossRef]

- Simpkin, P.; Cramer, L.; Ericksen, P.J.; Thornton, P.K. Current situation and plausible future scenarios for livestock management systems under climate change in Africa. In CCAFS Working Paper No. 307; CCAFS: Wagenningen, The Netherland, 2020. [Google Scholar]

- Schmitz, C.; Van Meijl, H.; Kyle, P.; Nelson, G.C.; Fujimori, S.; Gurgel, A.; Havlik, P.; Heyhoe, E.; d’Croz, D.M.; Popp, A.; et al. Land-use change trajectories up to 2050: Insights from a global agro-economic model comparison. Agric. Econ. 2014, 45, 69–84. [Google Scholar] [CrossRef]

- Bishop, M.L.; Payne, A. Steering towards reglobalization: Can a reformed G20 rise to the occasion? Globalizations 2021, 18, 120–140. [Google Scholar] [CrossRef]

- Enahoro, D.; Mason-D’Croz, D.; Mul, M.; Rich, K.M.; Robinson, T.P.; Thornton, P.; Staal, S.S. Supporting sustainable expansion of livestock production in South Asia and Sub-Saharan Africa: Scenario analysis of investment options. Glob. Food Secur. 2019, 20, 114–121. [Google Scholar] [CrossRef]

- Herrero, M.; Havlik, P.; McIntire, J.; Palazzo, A.; Valin, H. African Livestock Futures: Realising the Potential of Livestock for Food Security, Poverty Reduction and the Environment in Sub-Saharan Africa; Office of the Special Representative of the UN Secretary General for Food Security and Nutrition and the United Nations System Influenza Coordination (UNSIC): Geneva, Switzerland, 2014; p. 118. [Google Scholar]

- Amole, T.; Augustine, A.; Balehegn, M.; Adesogoan, A.T. Livestock feed resources in the West African Sahel. Agron. J. 2022, 114, 26–45. [Google Scholar] [CrossRef] [PubMed]

- Filho, W.L.; Sousa, L.O.; Pretorius, R. Future Prospects of Sustainable Development in Africa. In Sustainable Development in Africa; Springer: Cham, Switzerland, 2021; pp. 733–741. [Google Scholar]

- Baumüller, H.; von Braun, J.; Admassie, A.; Badiane, O.; Baraké, E.; Börner, J.; Bozic, I.; Chichaibelu, B.B.; Daum, T.; Gatiso, T.; et al. From Potentials to Reality: Transforming Africa’s Food Production; University of Bonn: Bonn, Germany, 2020. [Google Scholar]

- Otte, J.; Pica-Ciamarra, U.; Morzaria, S. A comparative overview of the livestock-environment interactions in Asia and Sub-Saharan Africa. Front. Vet. Sci. 2019, 6, 37. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Sakho-Jimbira, S.; Hathie, I. The future of agriculture in Sub-Saharan Africa. Policy Brief 2020, 2, 18. [Google Scholar]

- Rampa, F.; Knaepen, H. Sustainable Food Systems through Diversification and Indigenous Vegetables. An Analysis of the Southern Nakuru County; ECDPM: Maastricht, The Netherlands, 2019. [Google Scholar]

- Magnusson, U. Sustainable Global Livestock Development for Food Security and Nutrition Including Roles for SWEDEN; Ministry of Enterprise and Innovation, Swedish FAO Committee: Stockholm, Sweden, 2016.

- Food and Agriculture Organization (FAO). Africa Sustainable Livestock 2050; FAO: Stockholm, Sweden, 2017. [Google Scholar]

- Nakimbugwe, D.; Ssepuuya, G.; Male, D.; Lutwama, V.; Mukisa, I.M.; Fiaboe, K.K. Status of the regulatory environment for utilisation of insects as food and feed in Sub-Saharan Africa-a review. Crit. Rev. Food Sci. Nutr. 2021, 61, 1269–1278. [Google Scholar] [CrossRef]

- Beckman, J.; Ivanic, M.; Jelliffe, J.L.; Baquedano, F.G.; Scott, S.G. Economic and Food Security Impacts of Agricultural Input Reduction Under the European Union Green Deal’s Farm to Fork and Biodiversity Strategies; USDA: Washington, DC, USA, 2020. [Google Scholar]

- Greiner, S.; Hoch, S.; Victoria, G.A.; Singh, A. Cop26 Digest: The Significance of Article 6 and CDM Transition Outcomes for Africa; Climate Focus: Amsterdam, The Netherlands, 2022. [Google Scholar]

- Hackenesch, C.; Högl, M.; Knaepen, H.; Iacobuta, G.; Asafu-Adjaye, J. Green Transitions in Africa–Europe Relations: What Role for the European Green Deal; ETTG: Brussel, Belgium, 2021. [Google Scholar]

- Union, A. Agenda 2063 Report of the Commission on the African Union Agenda 2063 the Africa We Want in 2063; African Union: Addis Ababa, Ethiopia, 2020; p. 59. [Google Scholar]

- Chambiwa, E.; Majoni, J.; Mapuranga, L.L. The African Union and its Role in Ensuring African Economic and Environmental Sovereignty. Sovereignty Becoming Pulvereignty: Unpacking the Dark Side of Slave 4.0 Within Industry 4.0 in Twenty-First Century Africa. In Sovereignty Becoming Pulvereignty: Unpacking the Dark Side of Slave 4.0 Within Industry 4.0 in Twenty-First Century Africa; Langaa Research & Publishing Common Initiative Group: Bamenda, Cameroon, 2022; p. 299. [Google Scholar]

- Rennkamp, B. Negotiating Climate Change between Unequal Parties: COP25 from an African Perspective. Available online: https://www.africaportal.org/features/negotiating-climate-change-between-unequal-parties-cop25-african-perspective/ (accessed on 19 October 2022).

- Cilliers, J. The future of work in Africa. In The Future of Africa; Palgrave Macmillan: Cham, Switzerland, 2021; pp. 195–219. [Google Scholar]

- Sonnino, R.; Callenius, C.; Lähteenmäki, L.; Breda, J.; Cahill, J.; Caron, P.; Damianova, Z.; Gurinovic, M.; Lang, T.; Lapperière, A.; et al. Research and Innovation Supporting the Farm to Fork Strategy of the European Commission. Available online: https://research.vu.nl/en/publications/research-and-innovation-supporting-the-farm-to-fork-strategy-of-t (accessed on 5 September 2022).

- Dekeyser, K.; Rampa, F. Implications for Ireland’s Development Programming and Policy Influencing; ECDPM: Masstricht, The Netherlands, 2021. [Google Scholar]

- European Comission. Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions: A Farm to Fork Strategy for a Fair, Healthy and Environmentally-Friendly Food System COM/2020/381 Final. Available online: https://eur-lex.europa.eu/legal-content/EN/ALL/?uri=CELEX:52020DC0381 (accessed on 5 September 2022).

- Plan, C.E. For a Cleaner and More Competitive Europe; European Commission (EC): Brussels, Belgium, 2020. [Google Scholar]

- European Commission. Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions Critical Raw Materials Resilience: Charting a Path towards Greater Security and Sustainability; European Commission: Brussels, Belgium, 2020. [Google Scholar]

- Hammond, D.R.; Brady, T.F. Critical minerals for green energy transition: A United States perspective. Int. J. Min. Reclam. Environ. 2022, 1–8. [Google Scholar] [CrossRef]

- Outlook, S.A. World Energy Outlook Special Report; International Energy Agency: Paris, France, 2015; p. 135. [Google Scholar]

- Schebesta, H.; Candel, J.J. Game-changing potential of the EU’s Farm to Fork Strategy. Nat. Food 2020, 1, 586–588. [Google Scholar] [CrossRef]

- Cantore, N. The Potential Impact of a Greener CAP on Developing Countries; Overseas Development Institute: London, UK, 2012. [Google Scholar]

- Paarlberg, R. The trans-Atlantic conflict over “green” farming. Food Policy 2022, 108, 102229. [Google Scholar] [CrossRef]

- Beckman, J.; Ivanic, M.; Jelliffe, J. Market impacts of Farm to Fork: Reducing agricultural input usage. Appl. Econ. Perspect. Policy 2021. [Google Scholar] [CrossRef]

- Hurle, J.B.; Bogonos, M.; Himics, M.; Hristov, J.; Dominguez, I.P.; Sahoo, A.; Salputra, G.; Weiss, F.; Baldoni, E.; Elleby, C. Modelling Environmental and Climate Ambition in the Agricultural Sector with the CAPRI Model; Joint Research Centre: Brussel, Belgium, 2021. [Google Scholar]

- Dekeyser, K.; Woolfrey, S. A greener Europe at the expense of Africa? In Why the EU Must Address the External Implications of the Farm to Fork Strategy; ECDPM: Masstricht, The Netherlands, 2020. [Google Scholar]

- Hedrick, B.P.; Heberling, J.M.; Meineke, E.K.; Turner, K.G.; Grassa, C.J.; Park, D.S.; Kennedy, J.; Clarke, J.A.; Cook, J.A.; Blackburn, D.C.; et al. Digitisation and the future of natural history collections. BioScience 2020, 70, 243–251. [Google Scholar] [CrossRef]

- Bataille, C.; Waisman, H.; Briand, Y.; Svensson, J.; Vogt-Schilb, A.; Jaramillo, M.; Delgado, R.; Arguello, R.; Clarke, L.; Wild, T.; et al. Net-zero deep decarbonisation pathways in Latin America: Challenges and opportunities. Energy Strat. Rev. 2020, 30, 100510. [Google Scholar] [CrossRef]

- Zimmer, Y. EU Farm to Fork Strategy: How Reasonable is the Turmoil Predicted by USDA. Available online: https://www.globalaginvesting.com/contributed-content-eu-farm-fork-strategy-reasonable-turmoil-predicted-usda/ (accessed on 5 September 2022).

- Springmann, M.; Clark, M.; Mason-D’Croz, D.; Wiebe, K.; Bodirsky, B.L.; Lassaletta, L.; de Vries, W.; Vermeulen, S.J.; Herrero, M.; Carlson, K.M.; et al. Options for keeping the food system within environmental limits. Nature 2018, 562, 519–525. [Google Scholar] [CrossRef] [PubMed]

- Willett, W.; Rockström, J.; Loken, B.; Springmann, M.; Lang, T.; Vermeulen, S.; Garnett, T.; Tilman, D.; DeClerck, F.; Wood, A.; et al. Food in the Anthropocene: The EAT–Lancet Commission on healthy diets from sustainable food systems. Lancet 2019, 393, 447–492. [Google Scholar] [CrossRef]

- Sanchez-Sabate, R.; Sabaté, J. Consumer attitudes towards environmental concerns of meat consumption: A systematic review. Int. J. Environ. Res. Public Health 2019, 16, 1220. [Google Scholar] [CrossRef] [Green Version]

- Eker, S.; Reese, G.; Obersteiner, M. Modelling the drivers of a widespread shift to sustainable diets. Nat. Sustain. 2019, 2, 725–735. [Google Scholar] [CrossRef] [Green Version]

- Headey, D.; Fan, S. Anatomy of a crisis: The causes and consequences of surging food prices. Agric. Econ. 2008, 39, 375–391. [Google Scholar] [CrossRef] [Green Version]

- Trade Policy and Food Security: Improving Access to Food in Developing Countries in the Wake of High World Prices; Gillson, I.; Fouad, A. (Eds.) World Bank Publications: Washington, DC, USA, 2014. [Google Scholar]

- d’Amour, C.B.; Wenz, L.; Kalkuhl, M.; Steckel, J.C.; Creutzig, F. Teleconnected food supply shocks. Environ. Res. Lett. 2016, 11, 035007. [Google Scholar] [CrossRef]

- Smith, V.H.; Glauber, J.W. Trade, policy, and food security. Agric. Econ. 2020, 51, 159–171. [Google Scholar] [CrossRef] [Green Version]

- van Ittersum, M.K.; van Bussel, L.G.; Wolf, J.; Grassini, P.; van Wart, J.; Guilpart, N.; Claessens, L.; de Groot, H.; Wiebe, K.; Mason-D’Croz, D.; et al. Can sub-Saharan Africa feed itself? Proc. Natl. Acad. Sci. USA 2016, 113, 14964–14969. [Google Scholar] [CrossRef] [Green Version]

- Hertel, T.W. Food security under climate change. Nat. Clim. Chang. 2016, 6, 10–13. [Google Scholar] [CrossRef]

- Fellmann, T.; Witzke, P.; Weiss, F.; van Doorslaer, B.; Drabik, D.; Huck, I.; Salputra, G.; Jansson, T.; Leip, A. Major challenges of integrating agriculture into climate change mitigation policy frameworks. Mitig. Adapt. Strat. Glob. Chang. 2018, 23, 451–468. [Google Scholar] [CrossRef] [PubMed]

- OECD; FAO. OECD-FAO Agricultural Outlook 2021–2030; OECD: Paris, France; FAO: Rome, Italy,, 2021. [Google Scholar]

- Jayne, T.S.; Chapoto, A.; Sitko, N.; Nkonde, C.; Muyanga, M.; Chamberlin, J. Is the scramble for land in Africa foreclosing a smallholder agricultural expansion strategy? J. Int. Aff. 2014, 67, 35–53. [Google Scholar]

- Crippa, M.; Solazzo, E.; Guizzardi, D.; Monforti-Ferrario, F.; Tubiello, F.N.; Leip, A.J. Food systems are responsible for a third of global anthropogenic GHG emissions. Nat. Food 2021, 2, 198–209. [Google Scholar] [CrossRef]

- Laborde, D.; Parent, M.; Smaller, C. Ending Hunger, Increasing Incomes, and Protecting the Climate: What Would It Cost Donors; IFPRI: Wahington, DC, USA, 2020. [Google Scholar]

- Vieira, A.C.; da Silva, E.M.; Odakura, V.V. Development of a Web Application for Individual Carbon Footprint Calculation. In Proceedings of the 2021 XLVII Latin American Computing Conference (CLEI), Cartago, Costa Rica, 25–29 October 2021; IEEE: Manhattan, NY, USA, 2021; pp. 1–8. [Google Scholar]

- Matthews, A. Greening CAP Payments: A Missed Opportunity; Institute for International and European Affairs: Dublin, Ireland, 2013. [Google Scholar]

- European Commission. Europe’s Moment: Repair and Prepare for the Next Generation; European Commission: Brussel, Belgium, 2020. [Google Scholar]

- Fonta, W.M.; Ayuk, E.T.; van Huysen, T. Africa and the Green Climate Fund: Current challenges and future opportunities. Clim. Policy 2018, 18, 1210–1225. [Google Scholar] [CrossRef]

- Recio, M.E. Dancing like a toddler? The Green Climate Fund and REDD+ international rule-making. Rev. Eur. Comp. Int. Environ. Law 2019, 28, 122–135. [Google Scholar] [CrossRef]

- Guyomard, H.; Bureau, J.C.; Chatellier, V.; Détang-Dessendre, C.; Dupraz, P.; Jacquet, F.; Reboud, X.; Réquillart, V.; Soler, L.G.; Tysebaert, M. The Green Deal and the CAP: Policy Implications to Adapt Farming Practices and to Preserve the EU’s Natural Resources. Ph.D. Dissertation, Centre de Recherche Bretagne, Rennes, France, 2020. [Google Scholar]

- Panel, M.M. Meat, Milk and More: Policy Innovations to Shepherd Inclusive and Sustainable Livestock Systems in Africa; International Food Policy Research Institute: Washington, DC, USA, 2020. [Google Scholar]

- Shapiro, B.I.; Gebru, G.; Desta, S.; Negassa, A.; Negussie, K.; Aboset, G.; Mechal, H. Ethiopia Livestock Master Plan: Roadmaps for Growth and Transformation; International Livestock Research Instutute: Addis Ababa, Ethiopia, 2015. [Google Scholar]

- Queenan, K.; Sobratee, N.; Davids, R.; Mabhaudhi, T.; Chimonyo, M.; Slotow, R.; Shankar, B.; Häsler, B. A systems analysis and conceptual system dynamics model of the livestock-derived food system in South Africa: A tool for policy guidance. J. Agric. Food Syst. Commun. Dev. 2020, 9, 021. [Google Scholar] [CrossRef]

- Shakhbazova, O.P.; Slozhenkina, M.I.; Kholodov, O.A.; Kholodova, M.A.; Mosolova, N.I.; Glushenko, A.V.; Mosolova, D.A. Scheduling and forecasting trends in agricultural sector of economy in modern conditions: Methodological approaches. IOP Conf. Ser. Earth Environ. Sci. 2021, 677, 032026. [Google Scholar] [CrossRef]

- Latino, L.R.; Pica-Ciamarra, U.; Wisser, D. Africa: The livestock revolution urbanises. Glob. Food Secur. 2020, 26, 100399. [Google Scholar] [CrossRef]

- Chapman, E.J.; Byron, C.J. The flexible application of carrying capacity in ecology. Glob. Ecol. Conserv. 2018, 13, e00365. [Google Scholar] [CrossRef]

- Delgado, C.L.; Rosegrant, M.W.; Meijer, S. Livestock to 2020: The Revolution Continues. Available online: https://ideas.repec.org/p/ags/iatr01/14560.html (accessed on 8 June 2022).

- Arima, E.Y.; Richards, P.; Walker, R.; Caldas, M.M. Statistical confirmation of indirect land use change in the Brazilian Amazon. Environ. Res. Lett. 2011, 6, 024010. [Google Scholar] [CrossRef]

- Lambin, E.F.; Meyfroidt, P. Global land use change, economic globalisation, and the looming land scarcity. Proc. Natl. Acad. Sci. USA 2011, 108, 3465–3472. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Moss, J.; Morley, P.; Baker, D.; Al Moadhen, H.; Downie, R. Improving Methods for Estimating Livestock Production and Productivity; University of New England: Biddeford, UK, 2016. [Google Scholar]

- Chicca, F.; Vale, B.; Vale, R. Calculating the ecological footprints of the stories. In Everyday Lifestyles and Sustainability: The Environmental Impact of Doing the Same Things Differently; Routledge: Oxfordshire, UK, 2018. [Google Scholar]

- Mottet, A.; Henderson, B.; Opio, C.; Falcucci, A.; Tempio, G.; Silvestri, S.; Chesterman, S.; Gerber, P.J. Climate change mitigation and productivity gains in livestock supply chains: Insights from regional case studies. Reg. Environ. Chang. 2017, 17, 129–141. [Google Scholar] [CrossRef]

- Kulak, M.; Nemecek, T.; Frossard, E.; Gaillard, G. Eco-efficiency improvement by using integrative design and life cycle assessment. The case study of alternative bread supply chains in France. J. Clean. Prod. 2016, 112, 2452–2461. [Google Scholar] [CrossRef]

- Girvetz, E.; Ramirez-Villegas, J.; Claessens, L.; Lamanna, C.; Navarro-Racines, C.; Nowak, A.; Thornton, P.; Rosenstock, T.S. Future climate projections in Africa: Where are we headed? In The Climate-Smart Agriculture Papers; Springer: Cham, Switzerland, 2019; pp. 15–27. [Google Scholar]

- Nijdam, D.; Rood, T.; Westhoek, H. The price of protein: Review of land use and carbon footprints from life cycle assessments of animal food products and their substitutes. Food Policy 2012, 37, 760–770. [Google Scholar] [CrossRef]

- Pica-Ciamarra, U.; Baker, D.; Morgan, N.; Ly, C.; Nouala, S. Business and Livelihoods in African Livestock: Investments to Overcome Information Gaps; World Bank: Washington, DC, USA, 2014. [Google Scholar]

- Harrison, M.T.; Cullen, B.R.; Armstrong, D. Management options for dairy farms under climate change: Effects of intensification, adaptation and simplification on pastures, milk production and profitability. Agric. Syst. 2017, 155, 19–32. [Google Scholar] [CrossRef]

- Zhang, Y.; Li, K.; Wu, Y.; Liu, Y.; Wu, R.; Zhong, Y.; Xiao, S.; Mao, H.; Li, G.; Wang, Y.; et al. Distribution and correlation between antibiotic resistance genes and host-associated markers before and after swine fever in the longjiang watershed. Environ. Pollut. 2022, 313, 120101. [Google Scholar] [CrossRef]

- USDA. Ukraine: Poultry and Products Annual. FAS USDA. 2020. Available online: https://apps.fas.usda.gov/newgainapi/api/Report/DownloadReportByFileName (accessed on 20 July 2022).

- Tittonell, P. Livelihood strategies, resilience and transformability in African agroecosystems. Agric. Syst. 2014, 126, 3–14. [Google Scholar] [CrossRef]

- Jenkins, G.P.; Miklyaev, M.; Ujeneza, N.; Afra, S.; Matanhire, B.; Basikiti, P.; Nsenkyire, A. Comparative Economic Advantage of Crop Production in Rwanda. Available online: https://econpapers.repec.org/paper/qeddpaper/3006.htm (accessed on 8 June 2022).

- Poulton, C.; Berhanu, K.; Chinsinga, B.; Cooksey, B.; Golooba-Mutebi, F.; Loada, A. The Comprehensive Africa Agriculture Development Programme (CAADP): Political Incentives, Value Added and Ways Forward; Future Agricultures Consortium: Brighton, UK, 2014. [Google Scholar]

- Lang, T.; Barling, D. Food security and food sustainability: Reformulating the debate. Geogr. J. 2012, 178, 313–326. [Google Scholar] [CrossRef]

- Wanjiku, J.; Ogada, M.; Guthiga, P.M.; Karugia, J.T.; Massawe, S.C.; Wambua, J. Exploiting opportunities in intra-regional trade in food staples in COMESA region. In Proceedings of the International Association of Agricultural Economics (IAAE) Triennial Conference, Foz do Iguacu, Brazil, 18–24 August 2022. [Google Scholar]

- Behnke, R.H. The Contribution of Livestock to the Economies of IGAD Member States: Study Findings, Application of the Methodology in Ethiopia and Recommendations for Further Work; IGAD: Djidbouti, 2010; pp. 2–10. [Google Scholar]

- Geboye, M. The Regulatory Framework for Trade in IGAD Livestock Products; IGAD: Djidbouti, 2008; pp. 7–8. [Google Scholar]

- Van Rooyen, J.; Sigwele, H. Towards regional food security in southern Africa: A (new) policy framework for the agricultural sector. Food Policy 1998, 23, 491–504. [Google Scholar] [CrossRef]

- Batjes, N.H.; Milne, E.; Williams, S. Map-based estimates of present carbon stocks of grazing lands in Sub-Sahara Africa. In Grazing Lands, Livestock and Climate Resilient Mitigation in Sub-Saharan Africa: The State of the Science; United States Agency for International Development (USAID): Washington, DC, USA, 2015; pp. 31–33. [Google Scholar]

- Nabarro, D.; Wannous, C. The potential contribution of livestock to food and nutrition security: The application of the One Health approach in livestock policy and practice. Rev. Sci. Tech. 2014, 33, 475–485. [Google Scholar] [CrossRef]

- Molomo, M.; Mumba, T. Drivers for animal welfare policies in Africa. Rev. Sci. Tech. 2014, 33, 47–53. [Google Scholar] [CrossRef] [PubMed]

- Upton, M.; Otte, J. The impact of trade agreements on livestock producers. BSAP Occas. Publ. 2004, 33, 67–84. [Google Scholar] [CrossRef]

- de Haan, C.; Cervigni, R.; Mottet, A.; Conchedda, G.; Gerber, P.; Msangi, S.; Lesnoff, M.; Ham, F.; Fillol, E.; Nigussie, K. Vulnerability and Resilience in Livestock Systems in the Drylands of Sub-Saharan Africa; World Bank: Washington, DC, USA, 2016. [Google Scholar]

- Kamuanga, M.J.; Somda, J.; Sanon, Y.; Kagoné, H. Livestock and Regional Market in the Sahel and West Africa: Potentials and Challenges; OECD: Paris, France, 2008. [Google Scholar]

- World Bank. Opportunities for Climate Finance in the Livestock Sector: Removing Obstacles and Realising Potential; World Bank: Washington, DC, USA, 2021. [Google Scholar]

- van Veelen, B. Cash cows? Assembling low-carbon agriculture through green finance. Geoforum 2021, 118, 130–139. [Google Scholar] [CrossRef]

- Batini, N. Transforming agri-food sectors to mitigate climate change: The role of green finance. Vierteljahrsh. Wirtsch. 2019, 88, 7–42. [Google Scholar] [CrossRef]

- Chowdhury, T.; Datta, R.; Mohajan, H. Green finance is essential for economic development and sustainability. IJRCM 2013, 3, 104–109. [Google Scholar]

- Mukasa, A.N.; Woldemichael, A.D.; Salami, A.O.; Simpasa, A.M. Africa’s agricultural transformation: Identifying priority areas and overcoming challenges. Af. Econ. Brief 2017, 8, 1–6. [Google Scholar]

- Balázs, B.; Kelemen, E.; Centofanti, T.; Vasconcelos, M.W.; Iannetta, P.P. Integrated policy analysis to identify transformation paths to more sustainable legume-based food and feed value-chains in Europe. Agroecol. Sustain. Food Syst. 2021, 45, 931–953. [Google Scholar] [CrossRef]

- Owusu-Sekyere, E.; Scheepers, M.E.; Jordaan, H. Water footprint of milk produced and processed in South Africa: Implications for policymakers and stakeholders along the dairy value chain. Water 2016, 8, 322. [Google Scholar] [CrossRef] [Green Version]

- de Laurentiis, V.; Hunt, D.V.; Rogers, C.D. Overcoming food security challenges within an energy/water/food nexus (EWFN) approach. Sustainability 2016, 8, 95. [Google Scholar] [CrossRef] [Green Version]

- Franz, M.; Schlitz, N.; Schumacher, K.P. Globalisation and the water-energy-food nexus–Using the global production networks approach to analyse society-environment relations. Environ. Sci. Policy 2018, 90, 201–212. [Google Scholar] [CrossRef]

- Rosenzweig, C.; Tubiello, F.N.; Sandalow, D.; Benoit, P.; Hayek, M.N. Finding and fixing food system emissions: The double helix of science and policy. Environ. Res. Lett. 2021, 16, 061002. [Google Scholar] [CrossRef]

- Schroeder, T.C.; Tonsor, G.T. International cattle ID and traceability: Competitive implications for the US. Food Policy 2012, 37, 31–40. [Google Scholar] [CrossRef]

- Monteiro, D.M.S.; Caswell, J.A. The Economics of Implementing Traceability in Beef Supply Chains: Trends in Major Producing and Trading Countries; University of Massachusetts Amherst: Amherst, MA, USA, 2004. [Google Scholar]

- Bilali, H.E.; Allahyari, M.S. Transition towards sustainability in agriculture and food systems: Role of information and communication technologies. Inf. Process. Agric. 2018, 5, 456–464. [Google Scholar] [CrossRef]

- Bahn, R.A.; Yehya, A.A.; Zurayk, R. Digitalization for sustainable agri-food systems: Potential, status, and risks for the MENA region. Sustainability 2021, 13, 3223. [Google Scholar] [CrossRef]

- Becker, G.S. Resources, Science, and Industry Division. In Animal Identification and Meat Traceability; Congressional Research Service, Library of Congress: Wasgington, DC, USA, 2004. [Google Scholar]

- Conrad, Z.; Niles, M.T.; Neher, D.A.; Roy, E.D.; Tichenor, N.E.; Jahns, L. Relationship between food waste, diet quality, and environmental sustainability. PLoS ONE 2018, 13, e0195405. [Google Scholar] [CrossRef] [Green Version]

- Farmery, A.K.; Brewer, T.D.; Farrell, P.; Kottage, H.; Reeve, E.; Thow, A.M.; Andrew, N.L. Conceptualising value chain research to integrate multiple food system elements. Glob. Food Secur. 2021, 28, 100500. [Google Scholar] [CrossRef]

- Guarino, M.; Norton, T.; Berckmans, D.; Vranken, E.; Berckmans, D. A blueprint for developing and applying precision livestock farming tools: A key output of the EU-PLF project. Anim. Front. 2017, 7, 12–17. [Google Scholar] [CrossRef] [Green Version]

- Ugo, P.C.; Baker, D.; Morgan, N.; Ly, C.; Nouala, S. Investing in African Livestock: Business Opportunities in 2030–2050; World Bank: Washington, DC, USA, 2013. [Google Scholar]

- Delgado, C. Sources of growth in smallholder agriculture in sub-Saharan Africa: The role of vertical integration of smallholders with processors and marketers of high value-added items. Agrekon 1999, 38, 165–189. [Google Scholar] [CrossRef]

- Stoll-Kleemann, S.; O’Riordan, T. The sustainability challenges of our meat and dairy diets. Environ. Sci. Policy Sustain. Dev. 2015, 57, 34–48. [Google Scholar] [CrossRef]

- Taylor, D.H. Strategic considerations in the development of lean agri-food supply chains: A case study of the UK pork sector. Supply Chain. Manag. Int. J. 2006, 11, 271–280. [Google Scholar] [CrossRef]

- Boström, M. Regulatory credibility and authority through inclusiveness: Standardisation organisations in cases of eco-labelling. Organisation 2006, 13, 345–367. [Google Scholar] [CrossRef]

- Barrett, C.B.; Reardon, T.; Webb, P. Nonfarm income diversification and household livelihood strategies in rural Africa: Concepts, dynamics, and policy implications. Food Policy 2001, 26, 315–331. [Google Scholar] [CrossRef]

- Meissner, H.H.; Scholtz, M.M.; Palmer, A.R. Sustainability of the South African livestock sector towards 2050 Part 1: Worth and impact of the sector. S. Afr. J. Anim. Sci. 2013, 43, 282–297. [Google Scholar] [CrossRef]

- Sumuni, C. Poultry Meat Supply Chain in East Africa: Literature Review and a Proposed Framework for Future Research. Eur. J. Bus. Manag. 2020, 12, 103–110. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Indicator | Selected African Countries 2010–2019 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Gross National Income (GNI) per capita growth | Guinea-Bissau | South Africa | Ethiopia | Cote d Ivoire | Cape Verde | Benin | Guinea | Mauritius | Uganda | Gambia |

| Human Development Index (HDI) | Algeria | Tunisia | Botswana | Libya | South Africa | Egypt | Gabon | Morocco | Namibia | Swaziland |

| Population growth | Niger | Uganda | Equatorial Guinea | Angola | DRC | Burundi | Mali | Chad | Tanzania | Gambia |

| Gross Domestic Product (GDP) per capita growth | Rwanda | Djibouti | Ethiopia | Cabo Verde | Seychelles | Ghana | Benin | Cote d Ivoire | Egypt | Sierra Leone |

| Share of Urban population (%) | Gabon | Libya | Sao Tome and Principe | Djibouti | Algeria | Botswana | Tunisia | Angola | Congo | South Africa |

| Poultry meat producers(tons) | South Africa | Egypt | Morocco | Algeria | Nigeria | Malawi | Libya | Tanzania | Mozambique | Madagascar |

| Pig meat Producers (tons) | Nigeria | Malawi | South Africa | Uganda | Mozambique | Angola | Madagascar | Burkina Faso | Cameroon | Zambia |

| Pig meat shares to total meat | Guinea-Bissau | Cape Verde | Malawi | Mozambique | Seychelles | Sao Tome and Principe | Angola | Liberia | Uganda | Burundi |

| Poultry meat shares to total meat | Mauritius | Libya | Tunisia | Morocco | Egypt | South Africa | Seychelles | Togo | Sao Tome and Principe | Sierra Leone |

| Per capita, poultry consumption shares to the total | Mauritius | Benin | Sao Tome andPrincipe | Tunisia | Morocco | South Africa | Liberia | Togo | Cape Verde | Congo |

| Per capita pig meat consumption shares to the total | Guinea-Bissau | Malawi | Mozambique | Angola | Cape Verde | Uganda | Sao Tome and Principe | Liberia | Lesotho | Madagascar |

| Net Meat importers | South Africa | Egypt | Ghana | DRC | Congo | Benin | Gabon | Libya | Guinea | Namibia |

| Net pig meat importers | South Africa | DRC | Congo | Gabon | Cote d Ivoire | Sierra Leone | Ghana | Mauritius | Nigeria | Cape Verde |

| Net chicken meat importers | South Africa | Ghana | DRC | Congo | Libya | Benin | Gabon | Egypt | Guinea | Mauritania |

| Variable | Cluster | Error | Sig. | |

|---|---|---|---|---|

| Mean Square | Mean Square | F | ||

| Poultry Production | 10.566 | 0.404 | 26.179 | 0.000 |

| Poultry Consumption | 8.555 | 0.506 | 16.917 | 0.000 |

| Pig meat Production | 12.452 | 0.161 | 77.234 | 0.000 |

| Pig meat Consumption | 14.462 | 0.093 | 155.239 | 0.000 |

| Population | 0.530 | 0.743 | 0.714 | 0.550 |

| Gross Domestic Product (GDP) | 5.569 | 0.540 | 10.313 | 0.000 |

| Human Development Index (HDI) | 2.876 | 0.444 | 6.471 | 0.001 |

| Emission Intensity | 1.788 | 0.527 | 3.391 | 0.028 |

| Policy Tool | Main Goal |

|---|---|

| Agenda 2063 (Africa We Want) | Launched in 2014 as Africa’s long-term development plan after reviewing the (MDGs) performance. The importance of the livestock sector features in the plan’s first goal reflecting recognition of the sector’s importance in economic and livelihood transformation [21]. Three goals of the aspirations desire to enhance the industry to improve livelihoods while providing well-balanced, rich animal-sourced food and advocating for policies that enhance value addition to at least double the productivity of the sector. |

| Malabo Declaration | To actualise Agenda 2063, African countries agreed to promote growth in the sector by accelerating access to affordable inputs for poverty eradication by 2025. It aims to protect smallholder pastoralists from the impacts of climate change while improving their livelihoods, ensuring at least 30 per cent are resilient by 2025. However, an AU analysis of the progress made by member states in the declaration to fast-track their commitments reported that no single member state was on track toward meeting the goal [22]. This development track puts the sector’s sustainability to the test when approached from a global perspective faced with recent uncertainties in the market. |

| The Livestock Development Strategy for Africa (LiDeSA) | Established by the AU in 2015 to promote equitable growth and socio-economic development. Equitable growth was desired as the driving force through which the livestock sector could contribute toward the expected six per cent annual growth [20]. As an advocacy tool and framework, it is operational until 2035, with the primary goal of increasing public–private partnerships to strengthen the resilience of the production systems and access to markets. To actualise LiDeSA’s aspirations, several programs on the theme of livestock for livelihood and sustainable development have been initiated at the country level by the AU-Inter African Bureau for Animal Resources (IBAR) [86]. |

| AU Policy Framework for Pastoralists in Africa (PEFA) | Established as the first continental political tool to actualise political will and commitment to rural development in Africa for enhanced livelihood. To achieve its goals, PEFA has been championing livestock’s significant role at national, regional and continental levels [86]. |

| Comprehensive African Agriculture Development Programme (CAADP) | Pre-2010, the livestock sector was under general agriculture until the Comprehensive African Agriculture Development Programme (CAADP), which operationalised three areas for intervention, specifically in the sector emphasising accessibility to water, pasture management, mainstreaming mobility and provision of animal health services [86]. |

| Regional Instruments | At the regional level, the Common Market for Eastern and Southern Africa (COMESA) adoption and validation of a regional livestock policy framework was a milestone in promoting intra-trade on livestock products and strengthening production [85]. Although a regional policy exists, the bottleneck at the country level is that the livestock sector is treated under the general Ministry of Agriculture [20]. A different regional approach for the East African Community (EAC) exists, driven by promoting enhanced domestic production and a sustainable mechanism for enhancing resilience to climate change [86]. Moving towards the western side of the continent, the Economic Community of Western African States (ECOWAS), the second region with the highest demand for livestock products, operates under the Strategic Action Plan for developing and transforming the livestock sector (2011–2020). The plan aims to achieve food security and increase livelihood benefits. However, the AU 2019 sectoral review reported that most member states in the region have no strategy or policy dedicated to livestock or veterinary services [17,21]. The IGAD region, due to its large share of livestock in the economy, has seen most member states adopt the IGAD Centre for Pastoral Areas and Livestock Development, launched in 2013 as a platform for addressing regional livestock issues [87,88]. Similarly, the South African Development Cooperation (SADC) launched its Regional Agricultural policy in 2013 and was adopted by the member states. The policy advocates for a mechanism to increase regional competitiveness in the livestock sector to meet international standards [89,90,91]. |

| Global instruments | Beyond the continent’s scope, the SDGs highly influence the sector. Over 50 per cent of the 17 SDG goals are directly linked to the sector [14,64,65,92]. The strong relationship between the industry and the SDGs has seen a strong presence of many international Development organisations execute their mandate in Africa concerning livestock policy. The FAO, the World Health Organization (WHO), and the World Organization for Animal Health (OIE) are some of the major organisations which are on the frontline in ensuring the elimination of animal diseases, the improvement of animal welfare and the prevention of zoonotic diseases which could adversely affect the sector in the region [93]. This has resulted in many programmes established in many member states by the organisations, especially FAO, to increase resilience and livelihood improvement for pastoralists and livestock farmers. The presence of many policies, programmes and stakeholders is a clear indication of the vital role the sector plays in the region and the necessity for a joint approach to promote the sustainability of the sector [14,20,90,94,95,96,97]. One future policy tool and instrument that will be instrumental in addressing these regional gaps in the sector will be achieved through establishing a joint innovative financial mechanism [98]. Funding for the designed ambitious strategies can be seen as an obstacle to achieving the aspirations. However, a standard financial tool and policy will result in practical programming and an implementable design [62,63,64,65,99,100,101]. |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ndue, K.; Pál, G. European Green Transition Implications on Africa’s Livestock Sector Development and Resilience to Climate Change. Sustainability 2022, 14, 14401. https://doi.org/10.3390/su142114401

Ndue K, Pál G. European Green Transition Implications on Africa’s Livestock Sector Development and Resilience to Climate Change. Sustainability. 2022; 14(21):14401. https://doi.org/10.3390/su142114401

Chicago/Turabian StyleNdue, Kennedy, and Goda Pál. 2022. "European Green Transition Implications on Africa’s Livestock Sector Development and Resilience to Climate Change" Sustainability 14, no. 21: 14401. https://doi.org/10.3390/su142114401

APA StyleNdue, K., & Pál, G. (2022). European Green Transition Implications on Africa’s Livestock Sector Development and Resilience to Climate Change. Sustainability, 14(21), 14401. https://doi.org/10.3390/su142114401